Management Accounting Report: KEF Ltd Performance Analysis and Systems

VerifiedAdded on 2021/02/20

|18

|4527

|51

Report

AI Summary

This report provides a comprehensive analysis of management accounting systems and reporting, focusing on KEF Ltd. It begins with an introduction to management accounting, its systems (cost accounting, inventory management, job costing, and price optimization), and their benefits. The report then explores various management accounting reporting methods, including budget reports, accounts receivable aging reports, job cost reports, inventory reports, and performance reports. The integration of management accounting systems and reporting within organizational processes is also discussed. The report further delves into the calculation of net profit/loss under marginal and absorption costing methods for KEF Ltd, providing detailed calculations and interpretations. Finally, it defines the advantages and disadvantages of various planning tools, such as budgetary control, and analyzes their application in financial planning. The report concludes by comparing management accounting systems used to overcome financial issues and evaluating their role in organizational success.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

LO 1.................................................................................................................................................3

P 1. Systems of MA.....................................................................................................................3

M 1. Benefits of MA system........................................................................................................4

P 2 Methods used for Management Accounting Reporting ........................................................5

D1 Evaluation of management accounting systems and reporting is integrated within

organisational processes...............................................................................................................6

LO 2.................................................................................................................................................7

P 3 Calculation of net profit/(loss) under Marginal costing and absorption costing of KEF Ltd7

M 2 Application of management accounting techniques produce appropriate financial

reporting documents.....................................................................................................................9

D 2 Application of financial reports and interpretation of data for complex business activities9

LO 3 ..............................................................................................................................................10

P4. Defining advantages and disadvantages of vatious planning tools. ...................................10

M3 & D 3. Analysing uses and application of the different planning tools..............................12

LO 4...............................................................................................................................................13

P 5. Comparing management accounting system used for overcoming financial issues...........13

M4. Evaluating use of management accounting system in organisation success......................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

LO 1.................................................................................................................................................3

P 1. Systems of MA.....................................................................................................................3

M 1. Benefits of MA system........................................................................................................4

P 2 Methods used for Management Accounting Reporting ........................................................5

D1 Evaluation of management accounting systems and reporting is integrated within

organisational processes...............................................................................................................6

LO 2.................................................................................................................................................7

P 3 Calculation of net profit/(loss) under Marginal costing and absorption costing of KEF Ltd7

M 2 Application of management accounting techniques produce appropriate financial

reporting documents.....................................................................................................................9

D 2 Application of financial reports and interpretation of data for complex business activities9

LO 3 ..............................................................................................................................................10

P4. Defining advantages and disadvantages of vatious planning tools. ...................................10

M3 & D 3. Analysing uses and application of the different planning tools..............................12

LO 4...............................................................................................................................................13

P 5. Comparing management accounting system used for overcoming financial issues...........13

M4. Evaluating use of management accounting system in organisation success......................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting (MA) is an effective process which helps internal management

of the organization to achieve desired results and outcomes on time by attaining organizational

goals and objectives. MA helps in effective decision making and controlling cost for higher

operational standards. This study will highlight, various systems of MA and also determine

different methods of MA reports. Furthermore, this study identifies various MA techniques and

interpret the data using effective methods. This report further identifies various planning tools for

budget. This study also compare the MA tool to solve financial problems.

KEF Ltd. Company is a manufacturing company which was established in the year 1961

by Raymond Cooke and is headquartered in Maidstone, England. This company mainly deals in

ipod speakers, headphones, studio monitors, loudspeakers and drivers subwoofer.

LO 1

P 1. Systems of MA.

Management accounting (MA)

It is an effective tool which helps management of the organization in determining the

performance of the company and taking strategic decision which leads to higher operational

standards and efficacy (Management Accounting: Meaning, Functions and Characteristics,

2019). It also helps management in planning, forecasting the future and analysing the trends

(Hiebl, 2018).

Management Accounting System

System of MA helps in strategic decision making and also identify the areas to critically

solve various financial problems for smooth functioning of KEF Ltd. company. MA system

includes capital budgeting analysis, future forecasting and variance analysis to determine the

cause of the problem and take necessary measures to resolve the issue for long term sustainable

growth (Otley, 2016).

Cost accounting system: This tool helps in crucial analysis of the cost attached to the

each manufacturing unit of the production process in KEF Ltd. Company. This report helps in

analysing the profitability and controlling the cost (Fleischman and Parker, 2017). This system

helps management in giving detailed information about the output levels, level of accuracy of

each production and selling process, machines, labour, raw material, etc. This tool also helps in

Management accounting (MA) is an effective process which helps internal management

of the organization to achieve desired results and outcomes on time by attaining organizational

goals and objectives. MA helps in effective decision making and controlling cost for higher

operational standards. This study will highlight, various systems of MA and also determine

different methods of MA reports. Furthermore, this study identifies various MA techniques and

interpret the data using effective methods. This report further identifies various planning tools for

budget. This study also compare the MA tool to solve financial problems.

KEF Ltd. Company is a manufacturing company which was established in the year 1961

by Raymond Cooke and is headquartered in Maidstone, England. This company mainly deals in

ipod speakers, headphones, studio monitors, loudspeakers and drivers subwoofer.

LO 1

P 1. Systems of MA.

Management accounting (MA)

It is an effective tool which helps management of the organization in determining the

performance of the company and taking strategic decision which leads to higher operational

standards and efficacy (Management Accounting: Meaning, Functions and Characteristics,

2019). It also helps management in planning, forecasting the future and analysing the trends

(Hiebl, 2018).

Management Accounting System

System of MA helps in strategic decision making and also identify the areas to critically

solve various financial problems for smooth functioning of KEF Ltd. company. MA system

includes capital budgeting analysis, future forecasting and variance analysis to determine the

cause of the problem and take necessary measures to resolve the issue for long term sustainable

growth (Otley, 2016).

Cost accounting system: This tool helps in crucial analysis of the cost attached to the

each manufacturing unit of the production process in KEF Ltd. Company. This report helps in

analysing the profitability and controlling the cost (Fleischman and Parker, 2017). This system

helps management in giving detailed information about the output levels, level of accuracy of

each production and selling process, machines, labour, raw material, etc. This tool also helps in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

removing unnecessary cost and taking necessary measure for higher sustainable growth.

Inventory management system: This MA system keeps proper track and record of the

inventory levels, orders, sales and delivery for higher operational efficiency. This helps in

automating the records and tracking inventory which makes it easier for management to take

strategic decision (Maskell, Baggaley and Grasso, 2017). It is also useful in reducing manual

labour and focus on more skilled work for higher operational efficiency. There are various

inventory management methods such as LIFO, FIFO, JIT method, ABC methods, stock review

and weighted average method.

Job costing system: This system is useful in accumulating and distributing cost to each

individual unit of production which leads to higher operational standards and attainment of goals.

This helps management in determining the cost of the job and also analyse the most profitable

units in order to prioritize the job for higher growth of the KEF Ltd. Company (Maas,

Schaltegger and Crutzen, 2016). This system helps management in keeping proper track of the

expenses of each job for strategic decision making. This can be done by accurately categorizing

the cost of manufacturing into direct material, labour and overhead cost.

Price optimization system: This system is an effective process which helps in critically

analysing and predicting the behaviour of the consumers with the change in the price of the

particular product of the KEF Ltd. Company. This system helps in evaluating the accurate price

in order to attain greater profitability (Taleizadeh, Noori-daryan and Cárdenas-Barrón, 2015).

This tool effectively evaluates the price of the varied products and services to meet the

organizational goals and objectives and generate higher revenues and profit. This system also

critically examines the change in the demand and supply with the variation in price of the goods

and services offered by KEF Ltd. Company.

M 1. Benefits of MA system.

Cost accounting system: This tool is beneficial because it helps management of the

organization in evaluating the accurate cost of the production units in order to generate higher

profits (Fleischman and Parker, 2017). This system helps in determining the most profitable units

of the company and have proper control over the materials for smooth functioning of the

business.

Inventory management system: This tool is useful as it helps in increasing efficiency by

using ERP management tool and also helps ins saving cost by minimizing expenses and

Inventory management system: This MA system keeps proper track and record of the

inventory levels, orders, sales and delivery for higher operational efficiency. This helps in

automating the records and tracking inventory which makes it easier for management to take

strategic decision (Maskell, Baggaley and Grasso, 2017). It is also useful in reducing manual

labour and focus on more skilled work for higher operational efficiency. There are various

inventory management methods such as LIFO, FIFO, JIT method, ABC methods, stock review

and weighted average method.

Job costing system: This system is useful in accumulating and distributing cost to each

individual unit of production which leads to higher operational standards and attainment of goals.

This helps management in determining the cost of the job and also analyse the most profitable

units in order to prioritize the job for higher growth of the KEF Ltd. Company (Maas,

Schaltegger and Crutzen, 2016). This system helps management in keeping proper track of the

expenses of each job for strategic decision making. This can be done by accurately categorizing

the cost of manufacturing into direct material, labour and overhead cost.

Price optimization system: This system is an effective process which helps in critically

analysing and predicting the behaviour of the consumers with the change in the price of the

particular product of the KEF Ltd. Company. This system helps in evaluating the accurate price

in order to attain greater profitability (Taleizadeh, Noori-daryan and Cárdenas-Barrón, 2015).

This tool effectively evaluates the price of the varied products and services to meet the

organizational goals and objectives and generate higher revenues and profit. This system also

critically examines the change in the demand and supply with the variation in price of the goods

and services offered by KEF Ltd. Company.

M 1. Benefits of MA system.

Cost accounting system: This tool is beneficial because it helps management of the

organization in evaluating the accurate cost of the production units in order to generate higher

profits (Fleischman and Parker, 2017). This system helps in determining the most profitable units

of the company and have proper control over the materials for smooth functioning of the

business.

Inventory management system: This tool is useful as it helps in increasing efficiency by

using ERP management tool and also helps ins saving cost by minimizing expenses and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

achieving economies of scale (Maskell, Baggaley and Grasso, 2017).

Job costing system: This tool is beneficial when there are different varied products

manufactured by the company and each product has a particular cost attached with the products

(Laudon and Laudon, 2016). This system is useful as it helps in determining the cost of each job,

controlling expenses which leads to higher performance and productivity.

Price optimization system: This is an effective system of MA which helps in determining

the production process and evaluating accurate price for higher revenue generation and

profitability (Taleizadeh, Noori-daryan and Cárdenas-Barrón, 2015). This system is referred to as

effectively finding the balance between value and profit by optimizing the price of various goods

and services rendered by KEF Ltd. Company.

P 2 Methods used for Management Accounting Reporting

Management Accounting Reporting are the reports used in the evaluation of Financial

Statements. These reports are prepared for the purpose of taking decision in KEF Ltd. This

reports are used by internal stakeholders in order to certain decisions and for external

stakeholders in order to know the financial position of KEF Ltd. There are various reports such

as-

Budget Reports-

These reports are prepared in order to set the budgets by the company about the future

targets. Budget reports are compared with the actual reports of KEF Ltd. The budgets are set

targets by the company which are to be achieved by the company and then take decisions related

to the deviations occurred in the company (Kihn, 2015). Budget reports are generally prepared in

order to analyse the performance of the company on the basis of the deviations occurred in

budgets and actual performance of the company.

Accounts Receivable Aging Reports-

These reports are prepared in order to know that in how much time KEF ltd. Convert

their debtors into the cash. This report is very essential for any company because it shows that in

how much time cash inflows will be there in the company (Schaltegger 2017). This report can be

used by the manager in order to prepare the policy in the company related to cash collection from

debtors.

Job costing system: This tool is beneficial when there are different varied products

manufactured by the company and each product has a particular cost attached with the products

(Laudon and Laudon, 2016). This system is useful as it helps in determining the cost of each job,

controlling expenses which leads to higher performance and productivity.

Price optimization system: This is an effective system of MA which helps in determining

the production process and evaluating accurate price for higher revenue generation and

profitability (Taleizadeh, Noori-daryan and Cárdenas-Barrón, 2015). This system is referred to as

effectively finding the balance between value and profit by optimizing the price of various goods

and services rendered by KEF Ltd. Company.

P 2 Methods used for Management Accounting Reporting

Management Accounting Reporting are the reports used in the evaluation of Financial

Statements. These reports are prepared for the purpose of taking decision in KEF Ltd. This

reports are used by internal stakeholders in order to certain decisions and for external

stakeholders in order to know the financial position of KEF Ltd. There are various reports such

as-

Budget Reports-

These reports are prepared in order to set the budgets by the company about the future

targets. Budget reports are compared with the actual reports of KEF Ltd. The budgets are set

targets by the company which are to be achieved by the company and then take decisions related

to the deviations occurred in the company (Kihn, 2015). Budget reports are generally prepared in

order to analyse the performance of the company on the basis of the deviations occurred in

budgets and actual performance of the company.

Accounts Receivable Aging Reports-

These reports are prepared in order to know that in how much time KEF ltd. Convert

their debtors into the cash. This report is very essential for any company because it shows that in

how much time cash inflows will be there in the company (Schaltegger 2017). This report can be

used by the manager in order to prepare the policy in the company related to cash collection from

debtors.

Job Cost Reports-

This report is prepared by the cost accountant of KEF Ltd in order to know the total cost

of the company. It is generally prepared in order to control the extra cost allocated in the

department which is not giving any profits to the company. This also helps in knowing that

because of which extra expenses company is having low margin profits (Kocakulah and et.al

2016). This report also helps in allocation of costs in different department in the company as per

their needs in this department.

Inventory Reports-

These reports are prepared in order to know that how much time KEF Ltd takes in order

convert its inventory into sales. This report shows the production and sales of the company. This

report helps the inventory manager to know the production budget for the company and also

what will be the actual sales of the company. It is mainly prepared in on the basis of previous

year's production and sales of the company (Bjursell, 2015).

Performance Reports-

Performance reports helps in knowing the performance of the company by comparing the

actual performance of the company to budgeted performance of the company (Kihn, 2015). This

helps the company in finding the deviations and taking the corrective actions in order to solve the

problem. This also helps in taking the decision for KEF Ltd.

D1 Evaluation of management accounting systems and reporting is integrated within

organisational processes

Management Accounting systems and reporting both are integrated to each other.

In case any one of them are not presented in the company than the preparation of financial

statements are not possible. For example, Job cost reports are necessary to be prepared because

regarding the costs decisions are taken on the basis of job cost reports only. These reports are

needed preparation of financial statements of KEF Ltd. These reports are the base of

management accounting systems and both of them are interrelated and interconnected to each

other.

This report is prepared by the cost accountant of KEF Ltd in order to know the total cost

of the company. It is generally prepared in order to control the extra cost allocated in the

department which is not giving any profits to the company. This also helps in knowing that

because of which extra expenses company is having low margin profits (Kocakulah and et.al

2016). This report also helps in allocation of costs in different department in the company as per

their needs in this department.

Inventory Reports-

These reports are prepared in order to know that how much time KEF Ltd takes in order

convert its inventory into sales. This report shows the production and sales of the company. This

report helps the inventory manager to know the production budget for the company and also

what will be the actual sales of the company. It is mainly prepared in on the basis of previous

year's production and sales of the company (Bjursell, 2015).

Performance Reports-

Performance reports helps in knowing the performance of the company by comparing the

actual performance of the company to budgeted performance of the company (Kihn, 2015). This

helps the company in finding the deviations and taking the corrective actions in order to solve the

problem. This also helps in taking the decision for KEF Ltd.

D1 Evaluation of management accounting systems and reporting is integrated within

organisational processes

Management Accounting systems and reporting both are integrated to each other.

In case any one of them are not presented in the company than the preparation of financial

statements are not possible. For example, Job cost reports are necessary to be prepared because

regarding the costs decisions are taken on the basis of job cost reports only. These reports are

needed preparation of financial statements of KEF Ltd. These reports are the base of

management accounting systems and both of them are interrelated and interconnected to each

other.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LO 2

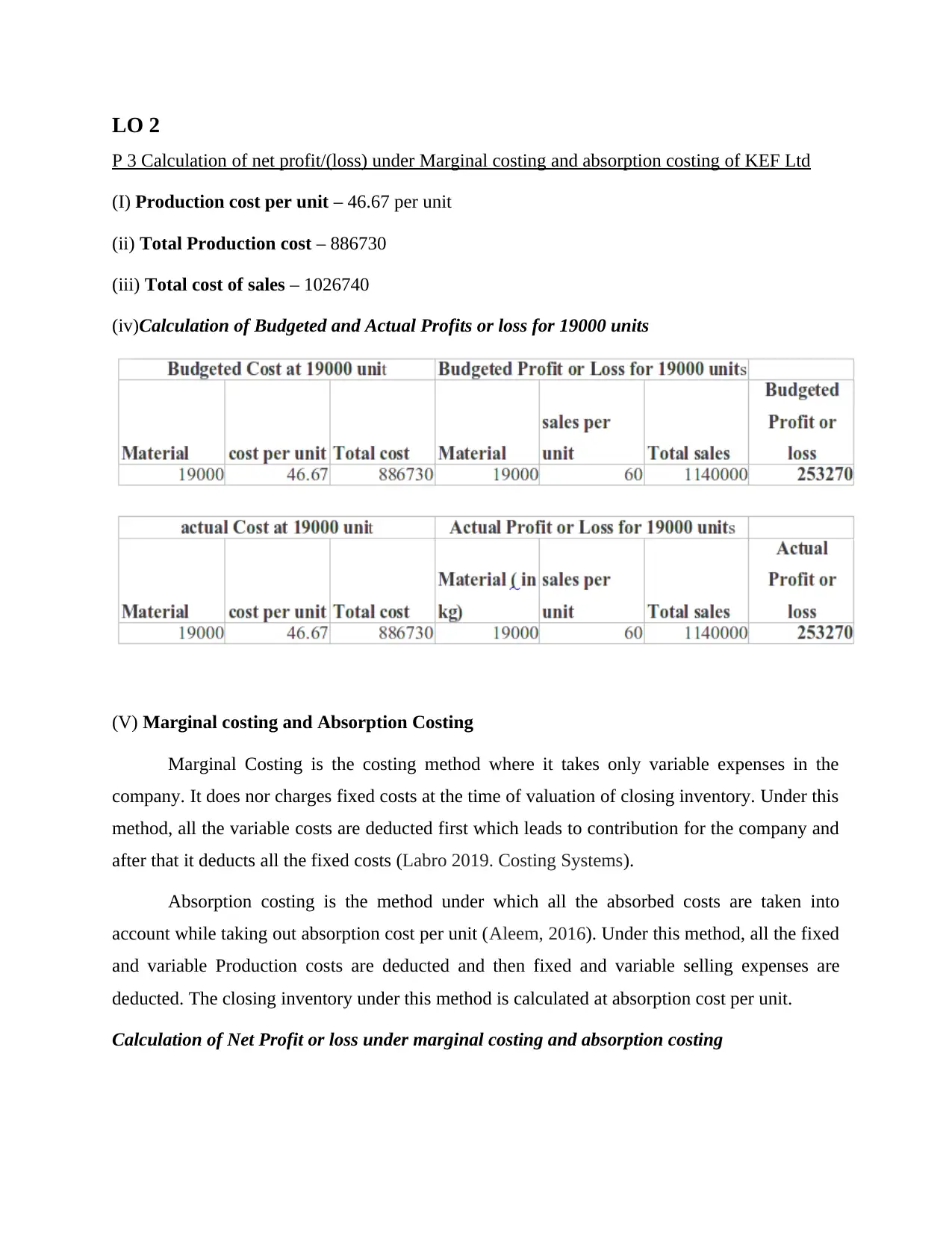

P 3 Calculation of net profit/(loss) under Marginal costing and absorption costing of KEF Ltd

(I) Production cost per unit – 46.67 per unit

(ii) Total Production cost – 886730

(iii) Total cost of sales – 1026740

(iv)Calculation of Budgeted and Actual Profits or loss for 19000 units

(V) Marginal costing and Absorption Costing

Marginal Costing is the costing method where it takes only variable expenses in the

company. It does nor charges fixed costs at the time of valuation of closing inventory. Under this

method, all the variable costs are deducted first which leads to contribution for the company and

after that it deducts all the fixed costs (Labro 2019. Costing Systems).

Absorption costing is the method under which all the absorbed costs are taken into

account while taking out absorption cost per unit (Aleem, 2016). Under this method, all the fixed

and variable Production costs are deducted and then fixed and variable selling expenses are

deducted. The closing inventory under this method is calculated at absorption cost per unit.

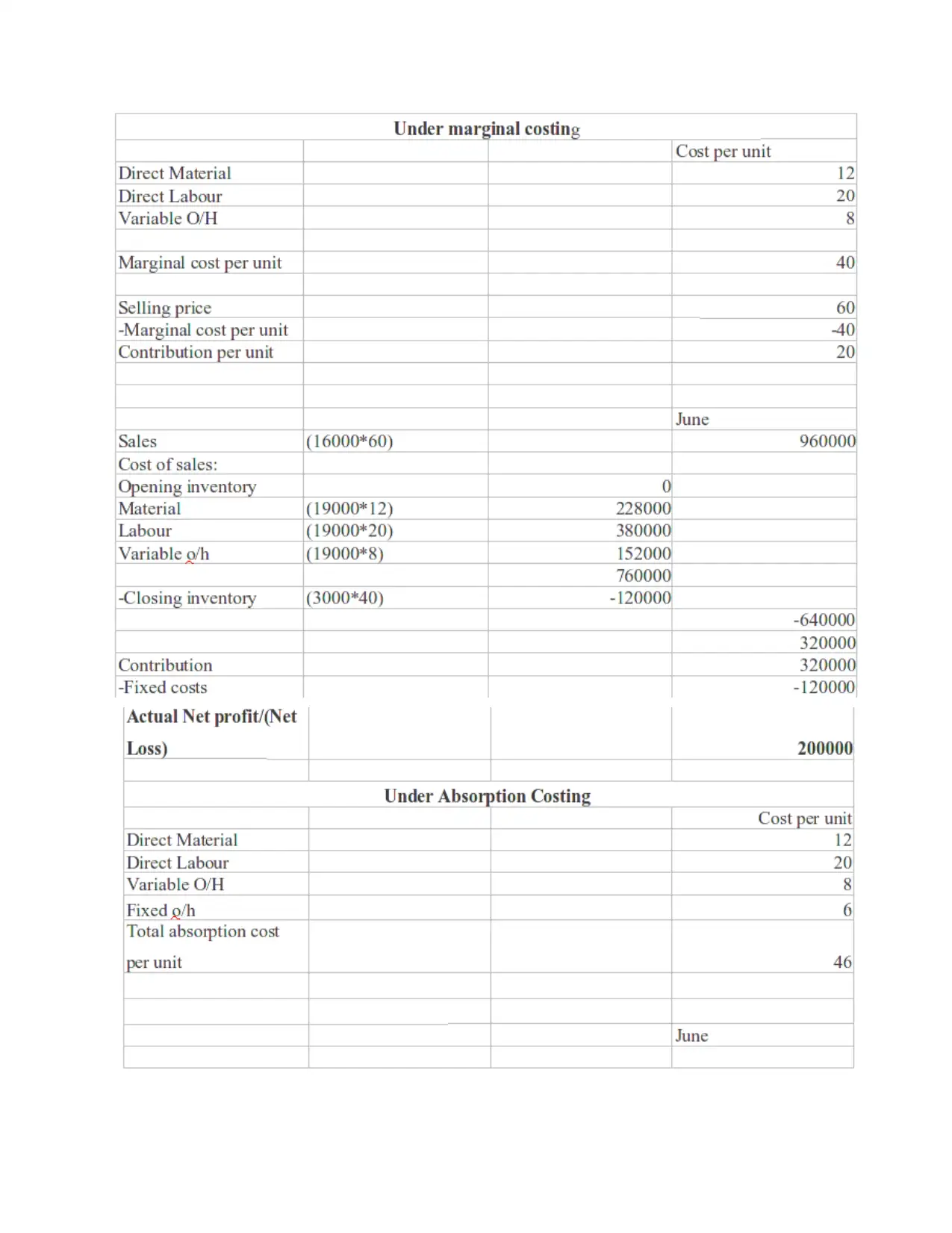

Calculation of Net Profit or loss under marginal costing and absorption costing

P 3 Calculation of net profit/(loss) under Marginal costing and absorption costing of KEF Ltd

(I) Production cost per unit – 46.67 per unit

(ii) Total Production cost – 886730

(iii) Total cost of sales – 1026740

(iv)Calculation of Budgeted and Actual Profits or loss for 19000 units

(V) Marginal costing and Absorption Costing

Marginal Costing is the costing method where it takes only variable expenses in the

company. It does nor charges fixed costs at the time of valuation of closing inventory. Under this

method, all the variable costs are deducted first which leads to contribution for the company and

after that it deducts all the fixed costs (Labro 2019. Costing Systems).

Absorption costing is the method under which all the absorbed costs are taken into

account while taking out absorption cost per unit (Aleem, 2016). Under this method, all the fixed

and variable Production costs are deducted and then fixed and variable selling expenses are

deducted. The closing inventory under this method is calculated at absorption cost per unit.

Calculation of Net Profit or loss under marginal costing and absorption costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

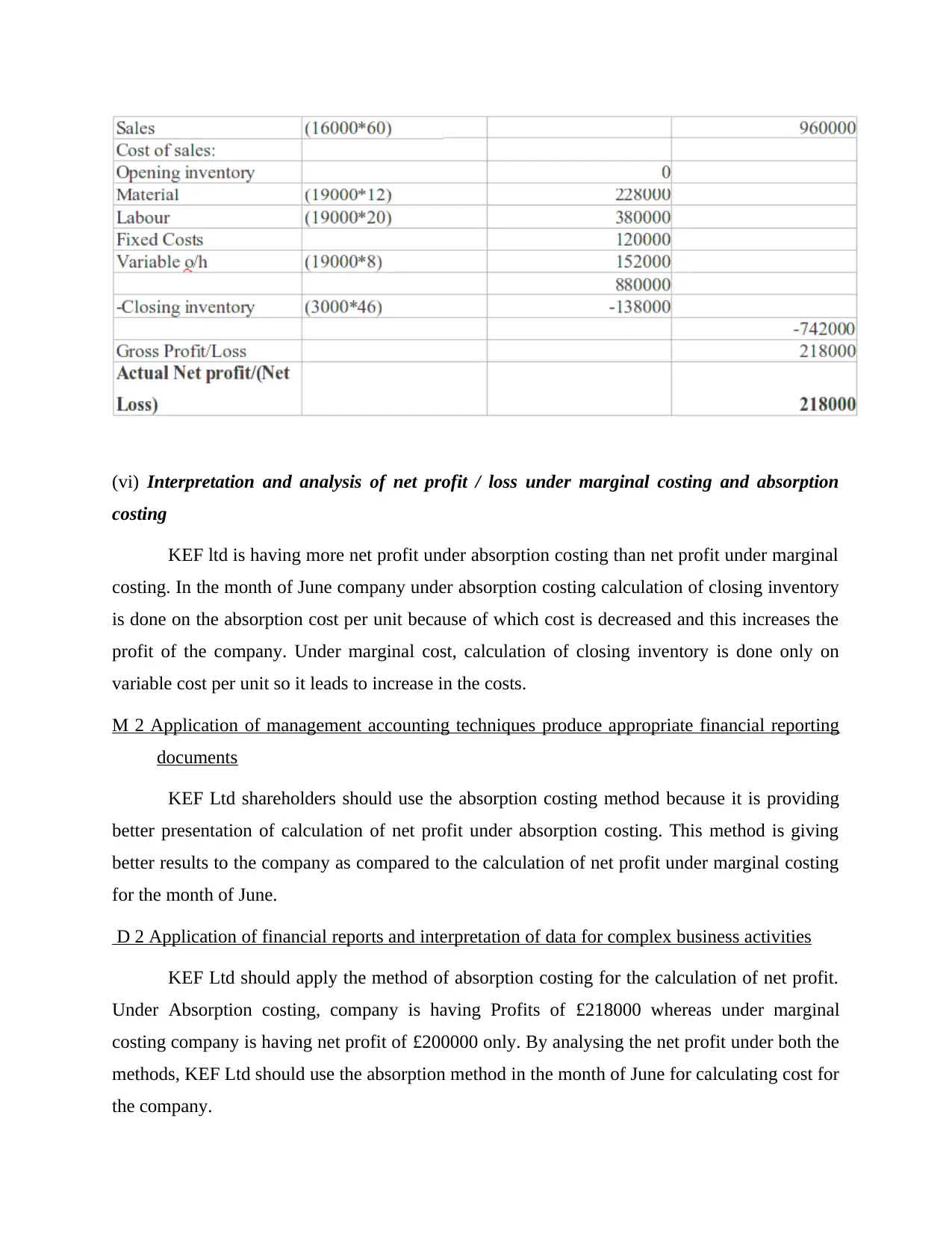

(vi) Interpretation and analysis of net profit / loss under marginal costing and absorption

costing

KEF ltd is having more net profit under absorption costing than net profit under marginal

costing. In the month of June company under absorption costing calculation of closing inventory

is done on the absorption cost per unit because of which cost is decreased and this increases the

profit of the company. Under marginal cost, calculation of closing inventory is done only on

variable cost per unit so it leads to increase in the costs.

M 2 Application of management accounting techniques produce appropriate financial reporting

documents

KEF Ltd shareholders should use the absorption costing method because it is providing

better presentation of calculation of net profit under absorption costing. This method is giving

better results to the company as compared to the calculation of net profit under marginal costing

for the month of June.

D 2 Application of financial reports and interpretation of data for complex business activities

KEF Ltd should apply the method of absorption costing for the calculation of net profit.

Under Absorption costing, company is having Profits of £218000 whereas under marginal

costing company is having net profit of £200000 only. By analysing the net profit under both the

methods, KEF Ltd should use the absorption method in the month of June for calculating cost for

the company.

costing

KEF ltd is having more net profit under absorption costing than net profit under marginal

costing. In the month of June company under absorption costing calculation of closing inventory

is done on the absorption cost per unit because of which cost is decreased and this increases the

profit of the company. Under marginal cost, calculation of closing inventory is done only on

variable cost per unit so it leads to increase in the costs.

M 2 Application of management accounting techniques produce appropriate financial reporting

documents

KEF Ltd shareholders should use the absorption costing method because it is providing

better presentation of calculation of net profit under absorption costing. This method is giving

better results to the company as compared to the calculation of net profit under marginal costing

for the month of June.

D 2 Application of financial reports and interpretation of data for complex business activities

KEF Ltd should apply the method of absorption costing for the calculation of net profit.

Under Absorption costing, company is having Profits of £218000 whereas under marginal

costing company is having net profit of £200000 only. By analysing the net profit under both the

methods, KEF Ltd should use the absorption method in the month of June for calculating cost for

the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LO 3

P4. Defining advantages and disadvantages of vatious planning tools.

Budgetary control is defined as a process which is related with the formulation of sound

and effective financial plans and objectives with budgeted target amount for an accounting

period. It helps every business organisation in proper use of available limited financial resources

of the business. By preparing budget it helps in making comparison of actual result with

forecasted one and makes changes if required. Following are the types of budgetary planning

tools which are available for KEF Ltd:

Flexible Budget - Is a budget which is having flexibility in its nature in context of

volume and sales activity changes. It has ability to makes adjustment on its own with change in

level of business activity or sales volume. This budget helps KEF Ltd in measuring the actual

revenue with estimated one maintained for future use at the time of framing budget after

completion of an accounting period. In this budget form, actual expenses are compared with

actual revenues for determining all the unnecessary cost expense and thus control it. It's changing

feature helps in providing several benefits to business at the time variations in the business.

Advantages Disadvantages

It helps in determining relevant and

necessary changes as required in

respect of business activity change for

increasing result accuracy and take

corrective action against variance if any

(Boyabatlı, Leng and Toktay, 2015).

It provides a metric for measuring

performance of company & its

employees both at regular interval time.

Each expense and revenue amount is

adjusted on continuous basis for

It is considered as one of the

difficult process as it takes into

accounts all the changes in it.

A time-consuming process as it

requires lot of time in formulation

of final budget as it considers all

the changes.

P4. Defining advantages and disadvantages of vatious planning tools.

Budgetary control is defined as a process which is related with the formulation of sound

and effective financial plans and objectives with budgeted target amount for an accounting

period. It helps every business organisation in proper use of available limited financial resources

of the business. By preparing budget it helps in making comparison of actual result with

forecasted one and makes changes if required. Following are the types of budgetary planning

tools which are available for KEF Ltd:

Flexible Budget - Is a budget which is having flexibility in its nature in context of

volume and sales activity changes. It has ability to makes adjustment on its own with change in

level of business activity or sales volume. This budget helps KEF Ltd in measuring the actual

revenue with estimated one maintained for future use at the time of framing budget after

completion of an accounting period. In this budget form, actual expenses are compared with

actual revenues for determining all the unnecessary cost expense and thus control it. It's changing

feature helps in providing several benefits to business at the time variations in the business.

Advantages Disadvantages

It helps in determining relevant and

necessary changes as required in

respect of business activity change for

increasing result accuracy and take

corrective action against variance if any

(Boyabatlı, Leng and Toktay, 2015).

It provides a metric for measuring

performance of company & its

employees both at regular interval time.

Each expense and revenue amount is

adjusted on continuous basis for

It is considered as one of the

difficult process as it takes into

accounts all the changes in it.

A time-consuming process as it

requires lot of time in formulation

of final budget as it considers all

the changes.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

overcoming prevailing conditions.

Fixed Budget – Is a financial plan which doesn't modifies or changes during the time

period of budget irrespective of changes which is taking place in the business activity on actual

basis. It remains unaffected with change in other resources of business such as sales, units

produced etc.

Advantages Disadvantages

One of the simple method of budgeting

as it doesn’t affected by any changes in

respect of the sales level etc.

Flexible budgets are known as static

and master budget as it helps

companies in analyzing data and

prediction for future.

Is considered as unrealistic budget

as it remains unchanged as a result

any change in the expenses and

revenue cannot be determined.

Forecasting is not possible due to

lack of presence of actual changes

with the changing business

environment.

Cash Budget — It assists in predicting requirements of cash & finance in business for

conducting future operations. It helps in process of forecasting related to cash inflow & outflow

from business operations performed in future time period.

Advantages Disadvantages

It helps in evaluating all cash

expenditure and incomes for specific

period.

It acts as basis for making comparison

of actual with estimation made and

ensures cash is spend as per budget

design.

It heavily relies on estimation made

as a result allocation of previous

year as of cash inflows and

outflows are used for proper cash

allocation process to all items in the

coming year budget.

It affects decision-making process

of business by considering cash

present in business.

Fixed Budget – Is a financial plan which doesn't modifies or changes during the time

period of budget irrespective of changes which is taking place in the business activity on actual

basis. It remains unaffected with change in other resources of business such as sales, units

produced etc.

Advantages Disadvantages

One of the simple method of budgeting

as it doesn’t affected by any changes in

respect of the sales level etc.

Flexible budgets are known as static

and master budget as it helps

companies in analyzing data and

prediction for future.

Is considered as unrealistic budget

as it remains unchanged as a result

any change in the expenses and

revenue cannot be determined.

Forecasting is not possible due to

lack of presence of actual changes

with the changing business

environment.

Cash Budget — It assists in predicting requirements of cash & finance in business for

conducting future operations. It helps in process of forecasting related to cash inflow & outflow

from business operations performed in future time period.

Advantages Disadvantages

It helps in evaluating all cash

expenditure and incomes for specific

period.

It acts as basis for making comparison

of actual with estimation made and

ensures cash is spend as per budget

design.

It heavily relies on estimation made

as a result allocation of previous

year as of cash inflows and

outflows are used for proper cash

allocation process to all items in the

coming year budget.

It affects decision-making process

of business by considering cash

present in business.

M3 & D 3. Analysing uses and application of the different planning tools.

Planning tools Uses Application

Flexible Budget It can be used for making

future estimates associated

with business operation of

KEF Ltd.

It assists in controlling

unnecessary cost expenses

of business areas (Kaplan

and Atkinson, 2015).

Is suitable for those

business organizations

where business activity

varies at regular time

period.

Also, it assists in making

future estimates and

forecasting demand

related to the new product

and service of KEF Ltd.

Fixed Budget This tool helps KEF Ltd. in

measuring performance

level and makes strategies,

plans and budget

accordingly.

Provides better efficiency

by allocating fixed figure

for carrying on business

operations.

Suitable where business

operations and activities

are of consistent nature.

Cash Budget It helps in making effective

utilization of available cash

resources by developing

cash plan.

It determines current

liquidity & solvency

position of company.

Can be prepared for

mitigating issues related

to excess of

nonproductive cash

balances of the firm.

KEF Ltd. By making

proper use of available

cash amount for making

Planning tools Uses Application

Flexible Budget It can be used for making

future estimates associated

with business operation of

KEF Ltd.

It assists in controlling

unnecessary cost expenses

of business areas (Kaplan

and Atkinson, 2015).

Is suitable for those

business organizations

where business activity

varies at regular time

period.

Also, it assists in making

future estimates and

forecasting demand

related to the new product

and service of KEF Ltd.

Fixed Budget This tool helps KEF Ltd. in

measuring performance

level and makes strategies,

plans and budget

accordingly.

Provides better efficiency

by allocating fixed figure

for carrying on business

operations.

Suitable where business

operations and activities

are of consistent nature.

Cash Budget It helps in making effective

utilization of available cash

resources by developing

cash plan.

It determines current

liquidity & solvency

position of company.

Can be prepared for

mitigating issues related

to excess of

nonproductive cash

balances of the firm.

KEF Ltd. By making

proper use of available

cash amount for making

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.