Management Accounting Report

VerifiedAdded on 2020/02/05

|14

|3016

|611

Report

AI Summary

This report on management accounting focuses on McDonald's, detailing the importance of management accounting, cost classification by function and behavior, variance analysis, and various operational budgets. It emphasizes the role of management accounting in enhancing business efficiency and decision-making, providing insights into cost management and financial planning.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

Importance of management accounting.......................................................................................4

Difference between management accounting and financial accounting......................................5

TASK 2............................................................................................................................................5

Evaluating classification of cost by function, behaviour, type and relevance.............................5

TASK 3............................................................................................................................................7

Explaining variance analysis and discussing common variances................................................7

TASK 4............................................................................................................................................9

Identifying different operational budgets.....................................................................................9

Advantages of preparing different operational budgets.............................................................12

CONCLUSION AND RECOMMEDATION ...............................................................................13

REFERENCES..............................................................................................................................14

2

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

Importance of management accounting.......................................................................................4

Difference between management accounting and financial accounting......................................5

TASK 2............................................................................................................................................5

Evaluating classification of cost by function, behaviour, type and relevance.............................5

TASK 3............................................................................................................................................7

Explaining variance analysis and discussing common variances................................................7

TASK 4............................................................................................................................................9

Identifying different operational budgets.....................................................................................9

Advantages of preparing different operational budgets.............................................................12

CONCLUSION AND RECOMMEDATION ...............................................................................13

REFERENCES..............................................................................................................................14

2

Index of Tables

Table 1: Difference between management and financial accounting..............................................5

Table 2: Sales budget.....................................................................................................................9

Table 3: Production budget........................................................................................................10

Table 4: Direct material usage budget.......................................................................................10

Table 5: Direct labor budget..........................................................................................................10

Table 6: Direct material purchase budget......................................................................................11

Table 7: Fixed and variable o/h budget.........................................................................................11

Table 8: Deprecation per quarter...................................................................................................12

3

Table 1: Difference between management and financial accounting..............................................5

Table 2: Sales budget.....................................................................................................................9

Table 3: Production budget........................................................................................................10

Table 4: Direct material usage budget.......................................................................................10

Table 5: Direct labor budget..........................................................................................................10

Table 6: Direct material purchase budget......................................................................................11

Table 7: Fixed and variable o/h budget.........................................................................................11

Table 8: Deprecation per quarter...................................................................................................12

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is the imperative field of managing business. It assists the

corporation to manage financial statements and determine long run growth in the marketplace.

The present report is based on Mcdonalds which is a fast food outlet restaurant firm of the UK

Furthermore, the report covers the importance of management accounting so the organisation can

stay competitive in the marketplace. In addition to this, classification of costs has been evaluated

in accordance to the functions, types and behaviour of this cited firm. Moreover, different

budgets and advantages of different operational financial plans have been explained.

TASK 1

Importance of management accounting

Furthermore, importance of management accounting has been explained as follows- Cost analysis-The concept of management accounting enables Mcdonalds to assess the

cost of products and services. Accordingly, they set margin of profit, by fixing selling

prices effectively. However, management takes into account the preferences of buyers

and profile for particular segment for which product has been developed (Caliskan,

2014). Measurement of performance-Management accounting consists of different aspects like

budgetary control, assessment of cost and variance management. These all parameters

make it possible to assess performance of Mcdonalds for particular time span. Increasing efficiency of business-Under management accounting, target is set for each

department of Mcdonalds. Those targets serve as a basis of increasing efficiency of

organisational production and profits. This is because; targets provide information

regarding achievement of cash flow targets with respect to improvements required

(Oliveira and et. al., 2010).

Providing effective management control- With the help of management accounting,

Mcdonalds plans, controls and coordinate among its different departments. Furthermore,

variations are analyzed by considering the actual and expected performance. This leads

the corporation to adopt effective techniques to control variation (Sandalgrh and Bukh,

2014).

4

Management accounting is the imperative field of managing business. It assists the

corporation to manage financial statements and determine long run growth in the marketplace.

The present report is based on Mcdonalds which is a fast food outlet restaurant firm of the UK

Furthermore, the report covers the importance of management accounting so the organisation can

stay competitive in the marketplace. In addition to this, classification of costs has been evaluated

in accordance to the functions, types and behaviour of this cited firm. Moreover, different

budgets and advantages of different operational financial plans have been explained.

TASK 1

Importance of management accounting

Furthermore, importance of management accounting has been explained as follows- Cost analysis-The concept of management accounting enables Mcdonalds to assess the

cost of products and services. Accordingly, they set margin of profit, by fixing selling

prices effectively. However, management takes into account the preferences of buyers

and profile for particular segment for which product has been developed (Caliskan,

2014). Measurement of performance-Management accounting consists of different aspects like

budgetary control, assessment of cost and variance management. These all parameters

make it possible to assess performance of Mcdonalds for particular time span. Increasing efficiency of business-Under management accounting, target is set for each

department of Mcdonalds. Those targets serve as a basis of increasing efficiency of

organisational production and profits. This is because; targets provide information

regarding achievement of cash flow targets with respect to improvements required

(Oliveira and et. al., 2010).

Providing effective management control- With the help of management accounting,

Mcdonalds plans, controls and coordinate among its different departments. Furthermore,

variations are analyzed by considering the actual and expected performance. This leads

the corporation to adopt effective techniques to control variation (Sandalgrh and Bukh,

2014).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

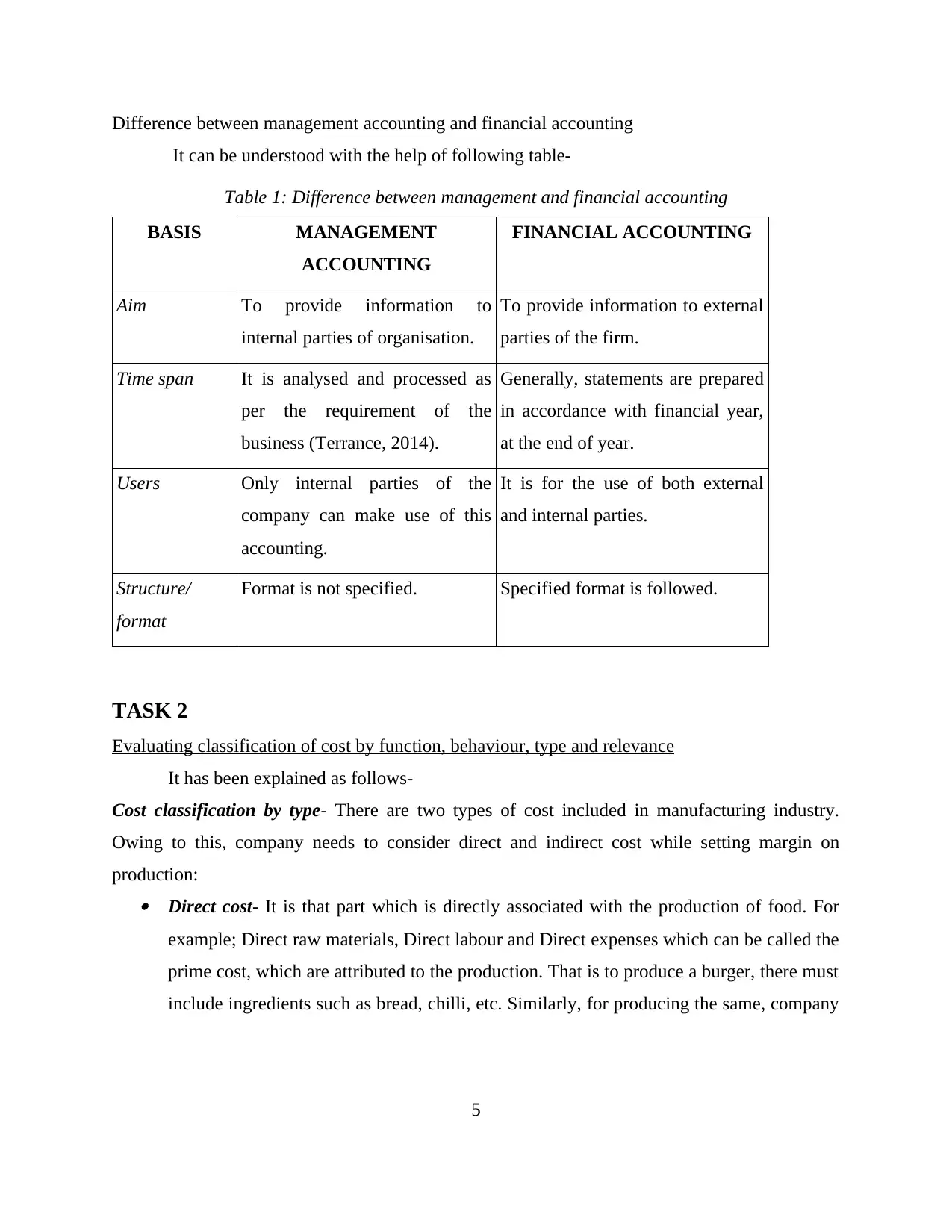

Difference between management accounting and financial accounting

It can be understood with the help of following table-

Table 1: Difference between management and financial accounting

BASIS MANAGEMENT

ACCOUNTING

FINANCIAL ACCOUNTING

Aim To provide information to

internal parties of organisation.

To provide information to external

parties of the firm.

Time span It is analysed and processed as

per the requirement of the

business (Terrance, 2014).

Generally, statements are prepared

in accordance with financial year,

at the end of year.

Users Only internal parties of the

company can make use of this

accounting.

It is for the use of both external

and internal parties.

Structure/

format

Format is not specified. Specified format is followed.

TASK 2

Evaluating classification of cost by function, behaviour, type and relevance

It has been explained as follows-

Cost classification by type- There are two types of cost included in manufacturing industry.

Owing to this, company needs to consider direct and indirect cost while setting margin on

production: Direct cost- It is that part which is directly associated with the production of food. For

example; Direct raw materials, Direct labour and Direct expenses which can be called the

prime cost, which are attributed to the production. That is to produce a burger, there must

include ingredients such as bread, chilli, etc. Similarly, for producing the same, company

5

It can be understood with the help of following table-

Table 1: Difference between management and financial accounting

BASIS MANAGEMENT

ACCOUNTING

FINANCIAL ACCOUNTING

Aim To provide information to

internal parties of organisation.

To provide information to external

parties of the firm.

Time span It is analysed and processed as

per the requirement of the

business (Terrance, 2014).

Generally, statements are prepared

in accordance with financial year,

at the end of year.

Users Only internal parties of the

company can make use of this

accounting.

It is for the use of both external

and internal parties.

Structure/

format

Format is not specified. Specified format is followed.

TASK 2

Evaluating classification of cost by function, behaviour, type and relevance

It has been explained as follows-

Cost classification by type- There are two types of cost included in manufacturing industry.

Owing to this, company needs to consider direct and indirect cost while setting margin on

production: Direct cost- It is that part which is directly associated with the production of food. For

example; Direct raw materials, Direct labour and Direct expenses which can be called the

prime cost, which are attributed to the production. That is to produce a burger, there must

include ingredients such as bread, chilli, etc. Similarly, for producing the same, company

5

require machines, chef etc. These all are direct cost of product for the Mcdonalds

Company (Cost and Cost Classifications, 2013). Indirect cost- This are those costs that cannot be traced to a specific unit area or cannot

be easily pinned to an individual product which is known as Overhead. Example of

indirect cost for producing food and services are indirect manufacturing cost;

administration, rent, rates and taxes. Furthermore, selling and distribution cost, Indirect

finance costs is also included in indirect cost of Mcdonalds (Tilanus, 2011).

Cost classification by function-Cost is classified on the basis of function because corporation

needs to perform several operations. There are different kinds of functions performed by

company like production or manufacturing (these are costs associated with the factory),

administration (costs associated with the general office departments), marketing/selling and

distribution (costs associated with sales, marketing, warehousing and transport departments).

Therefore, cost of all these functions are considered before making a decision related to selling

price of products and services: Production cost-This is the cost where company put efforts to produce products and

services. Under this, management of Mcdonalds needs to ensure inclusion of direct

labour, material and expenses. It is also known as prime cost thereby products and

services are delivered to end users (Macintosh and Quattrone, 2010). Non-Production cost-All inputs other than direct cost are considered as non-production

cost. It includes administration, financing, selling and distribution cost. Similarly, cost of

research and development is also included in non-production cost. In this way, accounts

department of Mcdonalds analyzes overall cost of products and services.

Cost classification by behaviour-According to the behaviour, cost is classified into two parts

such as fixed and variable. It is very important to consider different fixed and variables cost so-

as-to take right decision. It has been explained as follows- Fixed cost-This cost does not vary in accordance with volume of production. Here,

Mcdonalds needs to pay fixed amount of production on rent, rates and electricity bill. For

example; part of electricity cost is fixed and some of the same remain variables. Thus,

company should pay fixed cost whether it is earning/ producing or not. It will be up to the

Management Accountant to split the electricity semi variable cost by fixed and variable

6

Company (Cost and Cost Classifications, 2013). Indirect cost- This are those costs that cannot be traced to a specific unit area or cannot

be easily pinned to an individual product which is known as Overhead. Example of

indirect cost for producing food and services are indirect manufacturing cost;

administration, rent, rates and taxes. Furthermore, selling and distribution cost, Indirect

finance costs is also included in indirect cost of Mcdonalds (Tilanus, 2011).

Cost classification by function-Cost is classified on the basis of function because corporation

needs to perform several operations. There are different kinds of functions performed by

company like production or manufacturing (these are costs associated with the factory),

administration (costs associated with the general office departments), marketing/selling and

distribution (costs associated with sales, marketing, warehousing and transport departments).

Therefore, cost of all these functions are considered before making a decision related to selling

price of products and services: Production cost-This is the cost where company put efforts to produce products and

services. Under this, management of Mcdonalds needs to ensure inclusion of direct

labour, material and expenses. It is also known as prime cost thereby products and

services are delivered to end users (Macintosh and Quattrone, 2010). Non-Production cost-All inputs other than direct cost are considered as non-production

cost. It includes administration, financing, selling and distribution cost. Similarly, cost of

research and development is also included in non-production cost. In this way, accounts

department of Mcdonalds analyzes overall cost of products and services.

Cost classification by behaviour-According to the behaviour, cost is classified into two parts

such as fixed and variable. It is very important to consider different fixed and variables cost so-

as-to take right decision. It has been explained as follows- Fixed cost-This cost does not vary in accordance with volume of production. Here,

Mcdonalds needs to pay fixed amount of production on rent, rates and electricity bill. For

example; part of electricity cost is fixed and some of the same remain variables. Thus,

company should pay fixed cost whether it is earning/ producing or not. It will be up to the

Management Accountant to split the electricity semi variable cost by fixed and variable

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

for management accounting reporting purposes. Another element of fixed cost is step

cost, here the Management Accountant needs to identify for how long the fixed cost will

remain constant for example if they increase capacity to fulfil a customer order they

invest in a new building incurring further fixed costs for example Rent. It will be upto the

Management Accountant to analyse the additional fixed cost increase and determine if

investing in the new building to fulfil a few customer orders will eat into the overall

profits and determine whether to increase their capacity or make the decision not to invest

in the new building. A variable cost-Under this, cost varies in accordance with the volume of production. It is

based on units to be produced. The most common example of variables cost in

Mcdonalds are; recipe chefs, raw material like buns, meat patties, spices and cheese

(Schoute and Wiersma E2011).

Cost classification by relevance- Cost, in this category is classified into two parts such as

relevant and irrelevant. Accordingly, forecasting can also be done for future profit and loss of

business: Relevant cost- It consists of total cost of product and focus is laid on only relevant cost

which contribute towards the decision making process. The most common examples of

such kind are cost of future, cash, variable and opportunity cost. In addition to this,

avoidable cost is also included in relevant costs. For example, Mcdonalds is planning to

open its new outlet and wants to invest retained profit for the same option (Debarshi,

2011). At this juncture, there will be opportunity cost for current business of corporation.

Irrelevant cost- It consists of different aspects of costs such as sunk, unavoidable, fixed

and committed. For example; irreversibly incurred cost does not affect the decision

making process of corporation. Such kinds of costs are generally avoided at the time of

making decision. It facilitates organisation to take right decision with regard to growth

and success.

TASK 3

Explaining variance analysis and discussing common variances

Variance analysis is the process of assessing and evaluating budget in order to examine if

difference between planned and actual cost exists. It is qualitative investigation under which

7

cost, here the Management Accountant needs to identify for how long the fixed cost will

remain constant for example if they increase capacity to fulfil a customer order they

invest in a new building incurring further fixed costs for example Rent. It will be upto the

Management Accountant to analyse the additional fixed cost increase and determine if

investing in the new building to fulfil a few customer orders will eat into the overall

profits and determine whether to increase their capacity or make the decision not to invest

in the new building. A variable cost-Under this, cost varies in accordance with the volume of production. It is

based on units to be produced. The most common example of variables cost in

Mcdonalds are; recipe chefs, raw material like buns, meat patties, spices and cheese

(Schoute and Wiersma E2011).

Cost classification by relevance- Cost, in this category is classified into two parts such as

relevant and irrelevant. Accordingly, forecasting can also be done for future profit and loss of

business: Relevant cost- It consists of total cost of product and focus is laid on only relevant cost

which contribute towards the decision making process. The most common examples of

such kind are cost of future, cash, variable and opportunity cost. In addition to this,

avoidable cost is also included in relevant costs. For example, Mcdonalds is planning to

open its new outlet and wants to invest retained profit for the same option (Debarshi,

2011). At this juncture, there will be opportunity cost for current business of corporation.

Irrelevant cost- It consists of different aspects of costs such as sunk, unavoidable, fixed

and committed. For example; irreversibly incurred cost does not affect the decision

making process of corporation. Such kinds of costs are generally avoided at the time of

making decision. It facilitates organisation to take right decision with regard to growth

and success.

TASK 3

Explaining variance analysis and discussing common variances

Variance analysis is the process of assessing and evaluating budget in order to examine if

difference between planned and actual cost exists. It is qualitative investigation under which

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

management ensure that business activities are in proper control. The analysis of variance can

only be done after review of differences between expected and actual outcome.

Commonly derived variances Labour rate variance-It is the magnitude of difference between actual price for direct

labor used in the production process and budgeted one. The variance of the same can be

found through actual price paid for labor minus expected cost multiply by units used.

Purchase price variance-Price variance is occurred because of difference in the planned

cost of material and actual cost of the same. The variance is used to spot instances in

which a business may be overpaying for raw materials and components. The formula is:

(Actual price - Standard price) x Actual quantity used = Material price variance

(What is variance analysis?, 2016). Selling price variance-Under this management of Mcdonalds can assess the difference

between expected selling price and actual one. It leads to assess the variation and

accordingly bring modification in the current working condition or processes. Fixed Overhead spending variance-The variance of fixed overhead is easy to asses

under which management just find the difference between actual and expected overhead.

Material Yield variance-In order to find overhead spending variance, quantity if expected

material is subtracted from actual level and it is multiply by remainder by the standard

price/unit (Mistry and et. al., 2014).

Problems and limitations

The major problem for variation in actual and expected flow of production or cost are

related to experience of accounting staff. Also, impact of external factors like sudden changes in

weather and political parties. This tend to increase cost from the expected one and reduce overall

rate of return of corporation. Apart from this, less skilled workforce and production management

is also the potential barrier behind high difference in actual and planned results (Caliskan,

2014). Similarly, internal issues like inappropriate work culture, staff attitude and lack of

motivation are also issues behind poor performance of company. At this juncture, Mcdonalds can

provide training among employees to increase their expertise. In this manner, company can

resolve its issues and manage its performance in an effectual manner.

8

only be done after review of differences between expected and actual outcome.

Commonly derived variances Labour rate variance-It is the magnitude of difference between actual price for direct

labor used in the production process and budgeted one. The variance of the same can be

found through actual price paid for labor minus expected cost multiply by units used.

Purchase price variance-Price variance is occurred because of difference in the planned

cost of material and actual cost of the same. The variance is used to spot instances in

which a business may be overpaying for raw materials and components. The formula is:

(Actual price - Standard price) x Actual quantity used = Material price variance

(What is variance analysis?, 2016). Selling price variance-Under this management of Mcdonalds can assess the difference

between expected selling price and actual one. It leads to assess the variation and

accordingly bring modification in the current working condition or processes. Fixed Overhead spending variance-The variance of fixed overhead is easy to asses

under which management just find the difference between actual and expected overhead.

Material Yield variance-In order to find overhead spending variance, quantity if expected

material is subtracted from actual level and it is multiply by remainder by the standard

price/unit (Mistry and et. al., 2014).

Problems and limitations

The major problem for variation in actual and expected flow of production or cost are

related to experience of accounting staff. Also, impact of external factors like sudden changes in

weather and political parties. This tend to increase cost from the expected one and reduce overall

rate of return of corporation. Apart from this, less skilled workforce and production management

is also the potential barrier behind high difference in actual and planned results (Caliskan,

2014). Similarly, internal issues like inappropriate work culture, staff attitude and lack of

motivation are also issues behind poor performance of company. At this juncture, Mcdonalds can

provide training among employees to increase their expertise. In this manner, company can

resolve its issues and manage its performance in an effectual manner.

8

TASK 4

Identifying different operational budgets

There are different operation budget used in Mcdonalds which are presented as follows-

1. Sales budget

This is what the management expects to sell and the revenues collected from these sales.

(ACCA, 2015)

Table 2: Sales budget Illustration of theory in practice

2. Closing stock of finished goods budget- A business’s remaining stock at the end of an

accounting period. Ending Inventory = Opening Stock + Purchases during the year – Cost of

Goods sold.

3. Production budget

The production budget is the calculation of the number of units of products that must be

manufactured from a combination of the sales forecast and the planned amount of finished goods

inventory (Bhimani, Horngren, Datar, & Rajan, 2015), as illustrated in the table below.

Table 3: Production budget

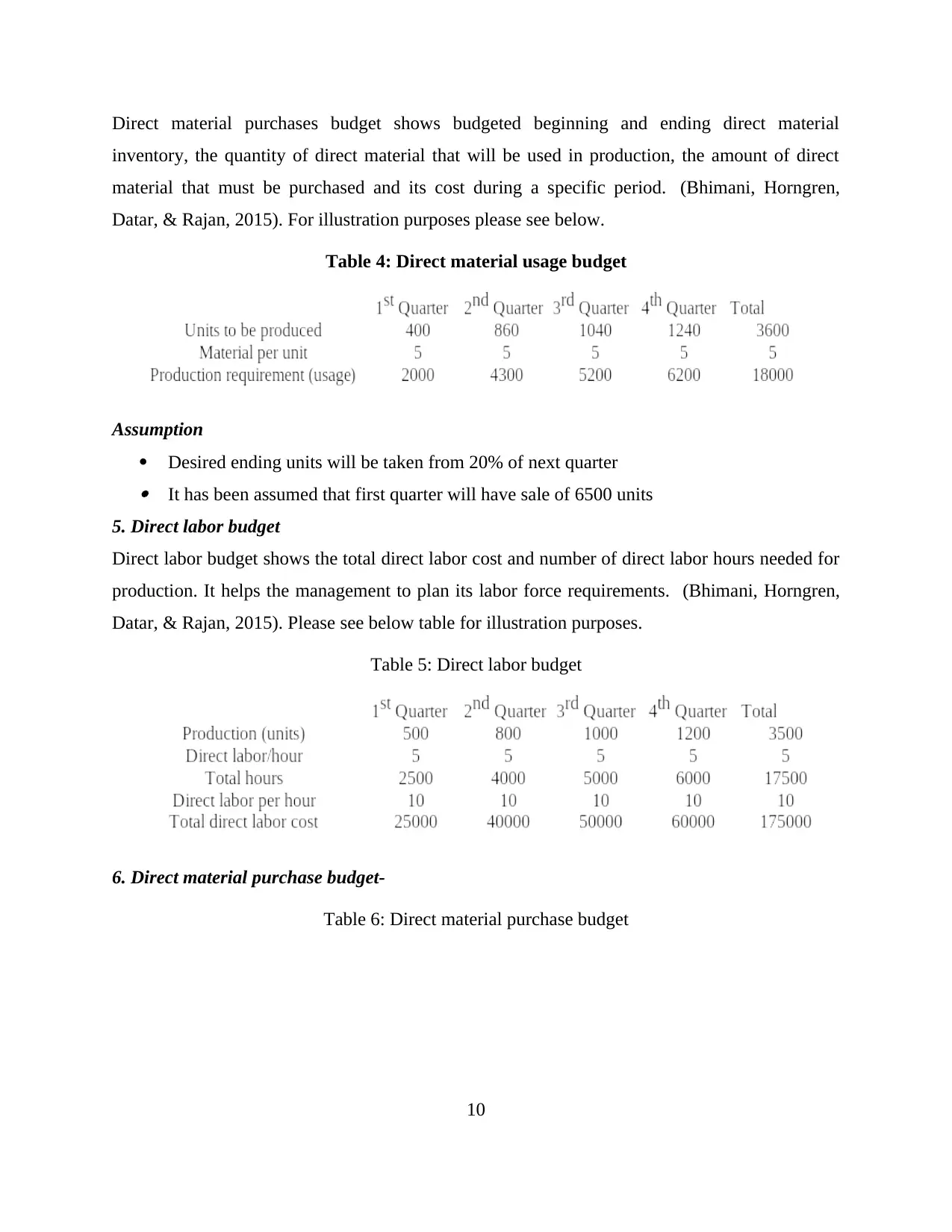

4. Direct material usage budget

9

Identifying different operational budgets

There are different operation budget used in Mcdonalds which are presented as follows-

1. Sales budget

This is what the management expects to sell and the revenues collected from these sales.

(ACCA, 2015)

Table 2: Sales budget Illustration of theory in practice

2. Closing stock of finished goods budget- A business’s remaining stock at the end of an

accounting period. Ending Inventory = Opening Stock + Purchases during the year – Cost of

Goods sold.

3. Production budget

The production budget is the calculation of the number of units of products that must be

manufactured from a combination of the sales forecast and the planned amount of finished goods

inventory (Bhimani, Horngren, Datar, & Rajan, 2015), as illustrated in the table below.

Table 3: Production budget

4. Direct material usage budget

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Direct material purchases budget shows budgeted beginning and ending direct material

inventory, the quantity of direct material that will be used in production, the amount of direct

material that must be purchased and its cost during a specific period. (Bhimani, Horngren,

Datar, & Rajan, 2015). For illustration purposes please see below.

Table 4: Direct material usage budget

Assumption

Desired ending units will be taken from 20% of next quarter It has been assumed that first quarter will have sale of 6500 units

5. Direct labor budget

Direct labor budget shows the total direct labor cost and number of direct labor hours needed for

production. It helps the management to plan its labor force requirements. (Bhimani, Horngren,

Datar, & Rajan, 2015). Please see below table for illustration purposes.

Table 5: Direct labor budget

6. Direct material purchase budget-

Table 6: Direct material purchase budget

10

inventory, the quantity of direct material that will be used in production, the amount of direct

material that must be purchased and its cost during a specific period. (Bhimani, Horngren,

Datar, & Rajan, 2015). For illustration purposes please see below.

Table 4: Direct material usage budget

Assumption

Desired ending units will be taken from 20% of next quarter It has been assumed that first quarter will have sale of 6500 units

5. Direct labor budget

Direct labor budget shows the total direct labor cost and number of direct labor hours needed for

production. It helps the management to plan its labor force requirements. (Bhimani, Horngren,

Datar, & Rajan, 2015). Please see below table for illustration purposes.

Table 5: Direct labor budget

6. Direct material purchase budget-

Table 6: Direct material purchase budget

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

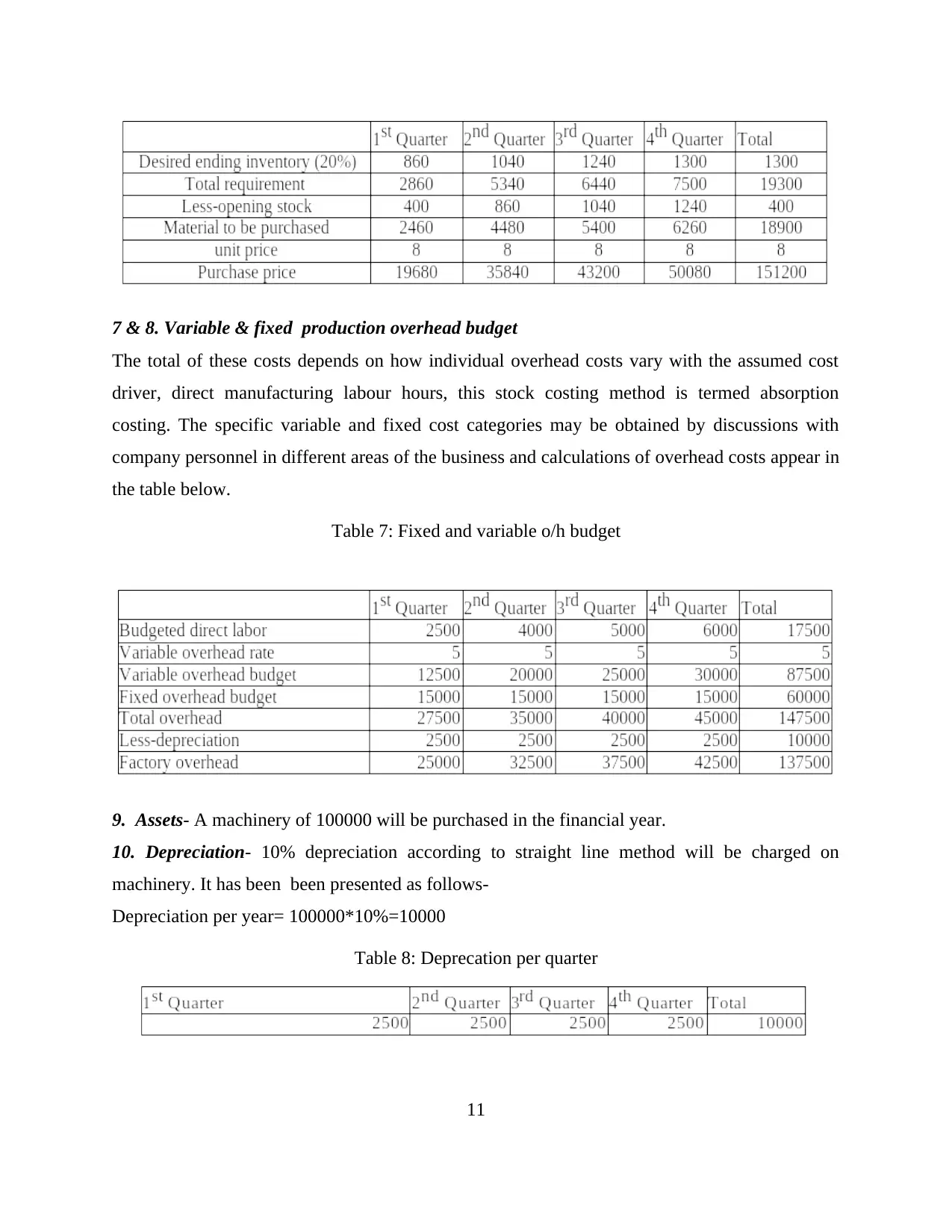

7 & 8. Variable & fixed production overhead budget

The total of these costs depends on how individual overhead costs vary with the assumed cost

driver, direct manufacturing labour hours, this stock costing method is termed absorption

costing. The specific variable and fixed cost categories may be obtained by discussions with

company personnel in different areas of the business and calculations of overhead costs appear in

the table below.

Table 7: Fixed and variable o/h budget

9. Assets- A machinery of 100000 will be purchased in the financial year.

10. Depreciation- 10% depreciation according to straight line method will be charged on

machinery. It has been been presented as follows-

Depreciation per year= 100000*10%=10000

Table 8: Deprecation per quarter

11

The total of these costs depends on how individual overhead costs vary with the assumed cost

driver, direct manufacturing labour hours, this stock costing method is termed absorption

costing. The specific variable and fixed cost categories may be obtained by discussions with

company personnel in different areas of the business and calculations of overhead costs appear in

the table below.

Table 7: Fixed and variable o/h budget

9. Assets- A machinery of 100000 will be purchased in the financial year.

10. Depreciation- 10% depreciation according to straight line method will be charged on

machinery. It has been been presented as follows-

Depreciation per year= 100000*10%=10000

Table 8: Deprecation per quarter

11

Advantages of preparing different operational budgets

Operational budget is prepared to cater need of business and keep record related to daily

business activities. For example sales budget provide the information that how much unit is to be

produced over a specified time span. Accordingly corporation come to know about the closing

stock (Sandalgrh and Bukh, 2014). This provides right estimation related to production of current

year. Furthermore, operational budget facilitates to achieve long as well as short term objectives.

In addition to this, operational budget proves to be effective in forecasting profit and loss of

current as well as coming time span. Likewise, operational budget help company in controlling

cost and increasing overall rate of return.

CONCLUSION AND RECOMMENDATION

The aforementioned report concludes that management accounting serves as the

imperative aspect of company and it facilitates to carry out all business activities in right manner.

Cash, production and sales budget prove to be effective in controlling cash and increase overall

rate of return. Owing to this, Mcdonalds need to formulate effective policies of management

accounting. It leads to set appropriate margin on production and create competitive edge in the

marketplace. Furthermore, company should provide in time training for its finance personnel in

accordance with variation found in budgets. This help in reducing gap between actual and

expected results.

12

Operational budget is prepared to cater need of business and keep record related to daily

business activities. For example sales budget provide the information that how much unit is to be

produced over a specified time span. Accordingly corporation come to know about the closing

stock (Sandalgrh and Bukh, 2014). This provides right estimation related to production of current

year. Furthermore, operational budget facilitates to achieve long as well as short term objectives.

In addition to this, operational budget proves to be effective in forecasting profit and loss of

current as well as coming time span. Likewise, operational budget help company in controlling

cost and increasing overall rate of return.

CONCLUSION AND RECOMMENDATION

The aforementioned report concludes that management accounting serves as the

imperative aspect of company and it facilitates to carry out all business activities in right manner.

Cash, production and sales budget prove to be effective in controlling cash and increase overall

rate of return. Owing to this, Mcdonalds need to formulate effective policies of management

accounting. It leads to set appropriate margin on production and create competitive edge in the

marketplace. Furthermore, company should provide in time training for its finance personnel in

accordance with variation found in budgets. This help in reducing gap between actual and

expected results.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.