Management Accounting Report: Oshodi Plc Financial Analysis

VerifiedAdded on 2021/02/20

|15

|4887

|213

Report

AI Summary

This report delves into the management accounting practices of Oshodi Plc, a UK-based production company specializing in JOJO fruit juice. The introduction outlines the importance of management accounting in decision-making and performance monitoring, highlighting various systems like cost accounting, inventory management, and price optimization. Task 1 examines these systems in detail, along with different methods for preparing accounting reports, such as performance reports, accounts receivable aging reports, and budget reports. Task 2 focuses on cost calculation techniques, comparing marginal and absorption costing methods, and providing income statements using marginal costing. Task 3 analyzes planning tools used for budgetary control, including their advantages, disadvantages, and applicability in constructing and predicting budgets. Finally, Task 4 compares how organizations adapt accounting systems to resolve financial issues, evaluating the use of planning tools to address problems and drive business success. The report concludes with a comprehensive overview of management accounting's role in organizational effectiveness and financial management.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting..................................................................................................1

P2. Methods for preparing accounting reports.......................................................................3

M1. Benefits of systems with their applicability....................................................................4

D1. Evaluation of accounting systems as well as accounting reporting that are integrated with

organisational processes.........................................................................................................5

TASK 2............................................................................................................................................5

P3. Cost calculation with distinct costing techniques............................................................5

M2 Applications of management accounting techniques.......................................................7

D2 Data Interpretation............................................................................................................7

TASK 3............................................................................................................................................7

P4 Pros and shortcomings of planning tools that are utilised for budgetary control..............7

M3 Planning tools usages as well as applicability for constructing and predicting budgets. 9

TASK 4............................................................................................................................................9

P5. Comparison between organisation in the ways they adapt accounting systems for

resolving financial issues. ......................................................................................................9

M4. analysis of ways problems are responded through accounting to attain success..........11

D3. Ways planning tools are used to resolve problems such that business success is leaded.11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting..................................................................................................1

P2. Methods for preparing accounting reports.......................................................................3

M1. Benefits of systems with their applicability....................................................................4

D1. Evaluation of accounting systems as well as accounting reporting that are integrated with

organisational processes.........................................................................................................5

TASK 2............................................................................................................................................5

P3. Cost calculation with distinct costing techniques............................................................5

M2 Applications of management accounting techniques.......................................................7

D2 Data Interpretation............................................................................................................7

TASK 3............................................................................................................................................7

P4 Pros and shortcomings of planning tools that are utilised for budgetary control..............7

M3 Planning tools usages as well as applicability for constructing and predicting budgets. 9

TASK 4............................................................................................................................................9

P5. Comparison between organisation in the ways they adapt accounting systems for

resolving financial issues. ......................................................................................................9

M4. analysis of ways problems are responded through accounting to attain success..........11

D3. Ways planning tools are used to resolve problems such that business success is leaded.11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is a procedure of gathering, analysing, supervising activities of

company and functions are utilised through managers for the decision-making process (Beattie,

2014). It is applied by every organisation in order to smoothly run their functional and

operational activities. Through the reports get all detailed information that will help for decision

making and further invest for generate profit. Current time, the atmosphere of the company

impact on the culture and they tries to monitor performance of business that price-based data. It

is supplied by traditional financial accounting data from historical general ledger systems. Good

management accounting consists of different systems that will use by business to understand

operational activities effectively and consist of several techniques like marginal costing &

absorption costing.

To understand the concept of management accounting selected organisation Oshodi plc,

which is UK based production company and specialise into JOJO fruit juice brackets. Different

topics are going to cover in the report such as different management accounting systems and

reports, calculation of cost by using marginal and absorption costing method. Along with,

advantages and disadvantages of planning tools and how it is utilised for budgetary control.

Additionally, the management accounting system responds to financial problems and application

management tools.

TASK 1

P1. Management accounting.

Management accounting is a procedure of creating reports and accounts which presents

reliable and well-timed financial and statistical information needed by director to take decisions.

As per the management reports analysing the performance of company then take prepare

effective strategy to enhance performance. Oshodi Plc apply it on routine basis to measure actual

performance of company.

Management accounting systems: It defines as organise study of accounting

information that is used by an organization to measure and evaluate the performance to manage

business activities. It is applied by the manager to deal with information that comes out from the

company such as creditors and stakeholders. To smoothly run business activities Oshodi plc

applied different types of management accounting systems.

1

Management accounting is a procedure of gathering, analysing, supervising activities of

company and functions are utilised through managers for the decision-making process (Beattie,

2014). It is applied by every organisation in order to smoothly run their functional and

operational activities. Through the reports get all detailed information that will help for decision

making and further invest for generate profit. Current time, the atmosphere of the company

impact on the culture and they tries to monitor performance of business that price-based data. It

is supplied by traditional financial accounting data from historical general ledger systems. Good

management accounting consists of different systems that will use by business to understand

operational activities effectively and consist of several techniques like marginal costing &

absorption costing.

To understand the concept of management accounting selected organisation Oshodi plc,

which is UK based production company and specialise into JOJO fruit juice brackets. Different

topics are going to cover in the report such as different management accounting systems and

reports, calculation of cost by using marginal and absorption costing method. Along with,

advantages and disadvantages of planning tools and how it is utilised for budgetary control.

Additionally, the management accounting system responds to financial problems and application

management tools.

TASK 1

P1. Management accounting.

Management accounting is a procedure of creating reports and accounts which presents

reliable and well-timed financial and statistical information needed by director to take decisions.

As per the management reports analysing the performance of company then take prepare

effective strategy to enhance performance. Oshodi Plc apply it on routine basis to measure actual

performance of company.

Management accounting systems: It defines as organise study of accounting

information that is used by an organization to measure and evaluate the performance to manage

business activities. It is applied by the manager to deal with information that comes out from the

company such as creditors and stakeholders. To smoothly run business activities Oshodi plc

applied different types of management accounting systems.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost Accounting system – This type of system applied by the manager of Oshodi Plc in

order to determine how an organization is doing and allows managers make decision on the basis

of cost of the company. The approach of cost accounting system applied every type off business

whether it is manufacturing or trading goods or whether it is delivering services. To understand

of this system, it is essential to analysis the differences between fixed costs and variable costs

(BenDavid-Hadar, 2015). It is mainly designed for manufacturers to record the flow of stocks

continually direct the several phases of manufacturing.

Inventory management system - An inventory management system is a instrument for

tracking products around the value chain of an enterprise. It simplifies the entire range from the

positioning of orders with seller to the shipment to client, tracking the overall product path. This

system mainly designed for production companies due to track production activities and know

about material utilisation. Oshodi Plc applied this system to arrange inventories, commodity and

work in process goods in suitable way. The purpose of this system to track record of material and

timing from starting to finished goods. To calculate inventory apply three methods such as LIFO,

FIFO and AVCO. LIFO (Last in first out) – The particular method states that which was purchased

recently that is used firstly for production activities. FIFO (First in first out) – This method defined that company sale product first which

was purchased firstly or consumed during production.

AVCO (Average cost) – According to this method company sell out their products and

services on average cost.

The selected company applied FIFO method due to maintain inventory effective manner

and reduce wastages.

Price optimization system - As its name suggests, it is primarily used to set optimal rates

for all trade good that produced by the organization. It is also known as mathematical analysis

that are applied by organizations to analysis the reviews of different types of customers for

different products and services. Prices are very delicate variables that promote customers to buy

these products and services. It has an important organizational necessity to fix prices for goods

and services that assist to attract clients. The manager of Oshodi plc set the price of JOJO fruit

juice by using this system which assess customers and help to meet with objectives like profit

maximization.

2

order to determine how an organization is doing and allows managers make decision on the basis

of cost of the company. The approach of cost accounting system applied every type off business

whether it is manufacturing or trading goods or whether it is delivering services. To understand

of this system, it is essential to analysis the differences between fixed costs and variable costs

(BenDavid-Hadar, 2015). It is mainly designed for manufacturers to record the flow of stocks

continually direct the several phases of manufacturing.

Inventory management system - An inventory management system is a instrument for

tracking products around the value chain of an enterprise. It simplifies the entire range from the

positioning of orders with seller to the shipment to client, tracking the overall product path. This

system mainly designed for production companies due to track production activities and know

about material utilisation. Oshodi Plc applied this system to arrange inventories, commodity and

work in process goods in suitable way. The purpose of this system to track record of material and

timing from starting to finished goods. To calculate inventory apply three methods such as LIFO,

FIFO and AVCO. LIFO (Last in first out) – The particular method states that which was purchased

recently that is used firstly for production activities. FIFO (First in first out) – This method defined that company sale product first which

was purchased firstly or consumed during production.

AVCO (Average cost) – According to this method company sell out their products and

services on average cost.

The selected company applied FIFO method due to maintain inventory effective manner

and reduce wastages.

Price optimization system - As its name suggests, it is primarily used to set optimal rates

for all trade good that produced by the organization. It is also known as mathematical analysis

that are applied by organizations to analysis the reviews of different types of customers for

different products and services. Prices are very delicate variables that promote customers to buy

these products and services. It has an important organizational necessity to fix prices for goods

and services that assist to attract clients. The manager of Oshodi plc set the price of JOJO fruit

juice by using this system which assess customers and help to meet with objectives like profit

maximization.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job order costing system - This is another system of management accounting that

designed for tracking costs and income as per job to boost productivity per job. In certain words,

this is a technique that managers use to track production work costs rather than system costs. It

has vital necessities such as no organisation can keep a record of the expenses of each work

without this system, a manager keeping information which is more valuable for organisation.

The manager of Oshodi plc determine the cost of specific jobs which helps in tracking expenses

within company and take appropriate decision to present business operation efficiently.

P2. Methods for preparing accounting reports

Managerial Accounting Reports: These accounting statements are the consequence

reports which include deviation between estimations and actual results in relation to various

operations and activities and are created by managerial accountants to assist the establishment in

planning befitting strategies and guidelines and controlling for improvement of the workers and

the processes as well (Bredmar and Et. Al., 2014). Following are the description of some

managerial accounting reports:

Performance Report: These reports are like the report card that provide the information

about the efficiency and performance of an individual or an activity. This performance report is

provided to the person so that the employee can evaluate the work performance deliver by the

employee. The management of Oshodi Plc prepares this report for all of its employees and

evaluate the performance of the workers. It also ensure the execution of any remedial activity if

required.

Accounts Receivable Aging Report: When an establishment deals in terms of credit

transaction, it is essential for the company to keep an adequate record of all the information

about debtors, trade receivables or clients. An accounts receivable aging report includes all the

information about due receipts, interest on dues, upcoming receivables' dates, contact details of

the debtors, doubtable amount of debt, etc. The management of Oshodi PLC prepares and

updates this report so that liquidity of the firm and debtor turnover ratio can be improved, due

receipts can be recovered on time and credit policies can be modify regularly.

Budget Report: Budget report can be described as a detailed statement that includes the

information about the variances and reasons behind the variances between estimated budget and

actual outcomes. The managerial accountant prepared an estimated budget with the help of

previous budgets and reports that is compared with the actual reports at the last of the financial

3

designed for tracking costs and income as per job to boost productivity per job. In certain words,

this is a technique that managers use to track production work costs rather than system costs. It

has vital necessities such as no organisation can keep a record of the expenses of each work

without this system, a manager keeping information which is more valuable for organisation.

The manager of Oshodi plc determine the cost of specific jobs which helps in tracking expenses

within company and take appropriate decision to present business operation efficiently.

P2. Methods for preparing accounting reports

Managerial Accounting Reports: These accounting statements are the consequence

reports which include deviation between estimations and actual results in relation to various

operations and activities and are created by managerial accountants to assist the establishment in

planning befitting strategies and guidelines and controlling for improvement of the workers and

the processes as well (Bredmar and Et. Al., 2014). Following are the description of some

managerial accounting reports:

Performance Report: These reports are like the report card that provide the information

about the efficiency and performance of an individual or an activity. This performance report is

provided to the person so that the employee can evaluate the work performance deliver by the

employee. The management of Oshodi Plc prepares this report for all of its employees and

evaluate the performance of the workers. It also ensure the execution of any remedial activity if

required.

Accounts Receivable Aging Report: When an establishment deals in terms of credit

transaction, it is essential for the company to keep an adequate record of all the information

about debtors, trade receivables or clients. An accounts receivable aging report includes all the

information about due receipts, interest on dues, upcoming receivables' dates, contact details of

the debtors, doubtable amount of debt, etc. The management of Oshodi PLC prepares and

updates this report so that liquidity of the firm and debtor turnover ratio can be improved, due

receipts can be recovered on time and credit policies can be modify regularly.

Budget Report: Budget report can be described as a detailed statement that includes the

information about the variances and reasons behind the variances between estimated budget and

actual outcomes. The managerial accountant prepared an estimated budget with the help of

previous budgets and reports that is compared with the actual reports at the last of the financial

3

year to find out the variances between them. Managers of Oshodi Plc follow this practice so that

rewards can be determined for the favourable results and remedies can be adopted for the

adverse outcomes. It also helps in understanding market changes and trends.

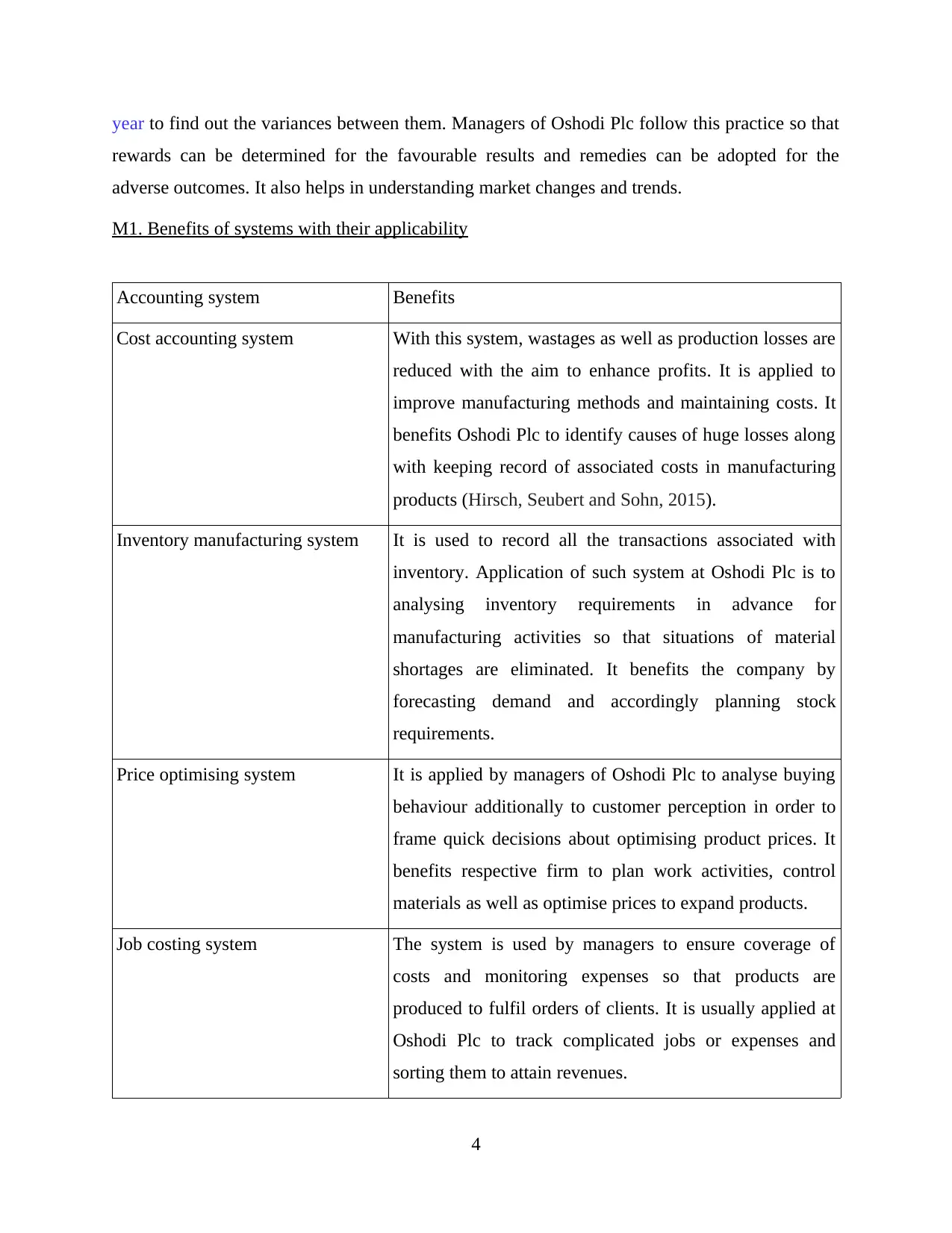

M1. Benefits of systems with their applicability

Accounting system Benefits

Cost accounting system With this system, wastages as well as production losses are

reduced with the aim to enhance profits. It is applied to

improve manufacturing methods and maintaining costs. It

benefits Oshodi Plc to identify causes of huge losses along

with keeping record of associated costs in manufacturing

products (Hirsch, Seubert and Sohn, 2015).

Inventory manufacturing system It is used to record all the transactions associated with

inventory. Application of such system at Oshodi Plc is to

analysing inventory requirements in advance for

manufacturing activities so that situations of material

shortages are eliminated. It benefits the company by

forecasting demand and accordingly planning stock

requirements.

Price optimising system It is applied by managers of Oshodi Plc to analyse buying

behaviour additionally to customer perception in order to

frame quick decisions about optimising product prices. It

benefits respective firm to plan work activities, control

materials as well as optimise prices to expand products.

Job costing system The system is used by managers to ensure coverage of

costs and monitoring expenses so that products are

produced to fulfil orders of clients. It is usually applied at

Oshodi Plc to track complicated jobs or expenses and

sorting them to attain revenues.

4

rewards can be determined for the favourable results and remedies can be adopted for the

adverse outcomes. It also helps in understanding market changes and trends.

M1. Benefits of systems with their applicability

Accounting system Benefits

Cost accounting system With this system, wastages as well as production losses are

reduced with the aim to enhance profits. It is applied to

improve manufacturing methods and maintaining costs. It

benefits Oshodi Plc to identify causes of huge losses along

with keeping record of associated costs in manufacturing

products (Hirsch, Seubert and Sohn, 2015).

Inventory manufacturing system It is used to record all the transactions associated with

inventory. Application of such system at Oshodi Plc is to

analysing inventory requirements in advance for

manufacturing activities so that situations of material

shortages are eliminated. It benefits the company by

forecasting demand and accordingly planning stock

requirements.

Price optimising system It is applied by managers of Oshodi Plc to analyse buying

behaviour additionally to customer perception in order to

frame quick decisions about optimising product prices. It

benefits respective firm to plan work activities, control

materials as well as optimise prices to expand products.

Job costing system The system is used by managers to ensure coverage of

costs and monitoring expenses so that products are

produced to fulfil orders of clients. It is usually applied at

Oshodi Plc to track complicated jobs or expenses and

sorting them to attain revenues.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

D1. Evaluation of accounting systems as well as accounting reporting that are integrated with

organisational processes

Managerial accounting is a crucial concern of the establishment that provides managerial

accounting systems and reports which both helps in assessing and controlling the effectiveness

and performance of the company (Jamil and Et. Al., 2015). Managerial accounting system

provides structure, policies and information for the reporting activities, on the other hand,

accounting reports provide the information regarding variances and reasons behind those

variances. For the example, it management accounting system does not provide adequate policies

and techniques for maintaining the system, it will be difficult to report appropriate results and

without sufficient variance reports and performance evaluation, it will not be possible to manage

the systems accurately. Therefore, it is crucial for the administration of the selected firm to

develop co-ordination between the managerial accounting reports and systems.

TASK 2

P3. Cost calculation with distinct costing techniques

Cost – An expenditure needed to manufacturing or sell a product or get an asset ready

for normal use is cost. In another words it is the amount paid to produce a product, buy stock,

sell commodity or get equipment ready to use in a business procedure. There are different types

of costs that is calculated during to manufacturing products such as fixed cost, variable cost.

These costs are recorded as expenses.

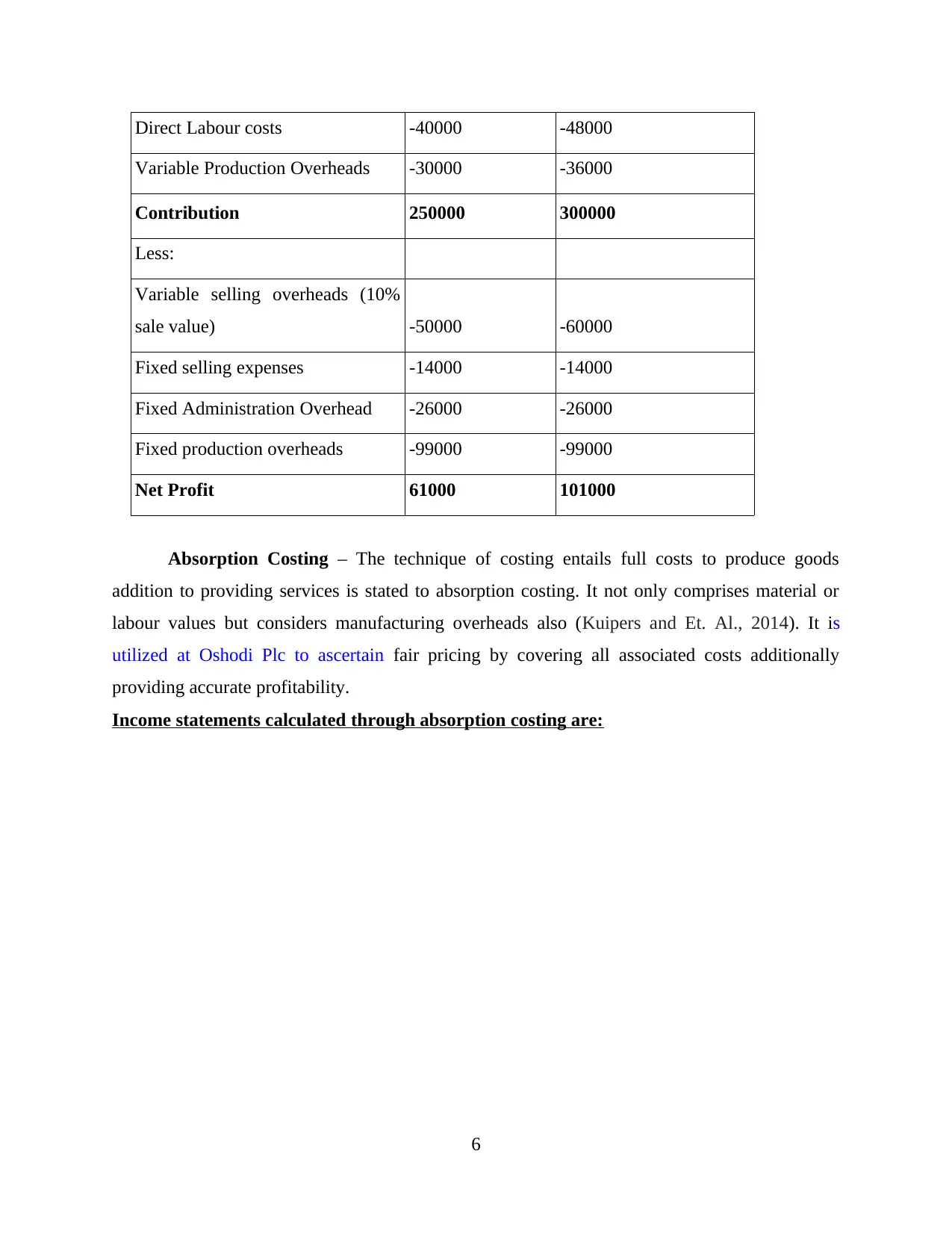

Marginal Costing – Cost involved in production of one additional product unit is said to

marginal costing. It involves changes in opportunity cost at the time additional single additional

unit is attached in manufacturing. The technique is adopted at Oshodi Plc to make decisions by

analysing cost data.

Income statement prepared by using marginal costing technique:

Particulars November (£) December (£)

Sales 500000 600000

Less: Cost of sales

Direct Material Costs -180000 -216000

5

organisational processes

Managerial accounting is a crucial concern of the establishment that provides managerial

accounting systems and reports which both helps in assessing and controlling the effectiveness

and performance of the company (Jamil and Et. Al., 2015). Managerial accounting system

provides structure, policies and information for the reporting activities, on the other hand,

accounting reports provide the information regarding variances and reasons behind those

variances. For the example, it management accounting system does not provide adequate policies

and techniques for maintaining the system, it will be difficult to report appropriate results and

without sufficient variance reports and performance evaluation, it will not be possible to manage

the systems accurately. Therefore, it is crucial for the administration of the selected firm to

develop co-ordination between the managerial accounting reports and systems.

TASK 2

P3. Cost calculation with distinct costing techniques

Cost – An expenditure needed to manufacturing or sell a product or get an asset ready

for normal use is cost. In another words it is the amount paid to produce a product, buy stock,

sell commodity or get equipment ready to use in a business procedure. There are different types

of costs that is calculated during to manufacturing products such as fixed cost, variable cost.

These costs are recorded as expenses.

Marginal Costing – Cost involved in production of one additional product unit is said to

marginal costing. It involves changes in opportunity cost at the time additional single additional

unit is attached in manufacturing. The technique is adopted at Oshodi Plc to make decisions by

analysing cost data.

Income statement prepared by using marginal costing technique:

Particulars November (£) December (£)

Sales 500000 600000

Less: Cost of sales

Direct Material Costs -180000 -216000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Direct Labour costs -40000 -48000

Variable Production Overheads -30000 -36000

Contribution 250000 300000

Less:

Variable selling overheads (10%

sale value) -50000 -60000

Fixed selling expenses -14000 -14000

Fixed Administration Overhead -26000 -26000

Fixed production overheads -99000 -99000

Net Profit 61000 101000

Absorption Costing – The technique of costing entails full costs to produce goods

addition to providing services is stated to absorption costing. It not only comprises material or

labour values but considers manufacturing overheads also (Kuipers and Et. Al., 2014). It is

utilized at Oshodi Plc to ascertain fair pricing by covering all associated costs additionally

providing accurate profitability.

Income statements calculated through absorption costing are:

6

Variable Production Overheads -30000 -36000

Contribution 250000 300000

Less:

Variable selling overheads (10%

sale value) -50000 -60000

Fixed selling expenses -14000 -14000

Fixed Administration Overhead -26000 -26000

Fixed production overheads -99000 -99000

Net Profit 61000 101000

Absorption Costing – The technique of costing entails full costs to produce goods

addition to providing services is stated to absorption costing. It not only comprises material or

labour values but considers manufacturing overheads also (Kuipers and Et. Al., 2014). It is

utilized at Oshodi Plc to ascertain fair pricing by covering all associated costs additionally

providing accurate profitability.

Income statements calculated through absorption costing are:

6

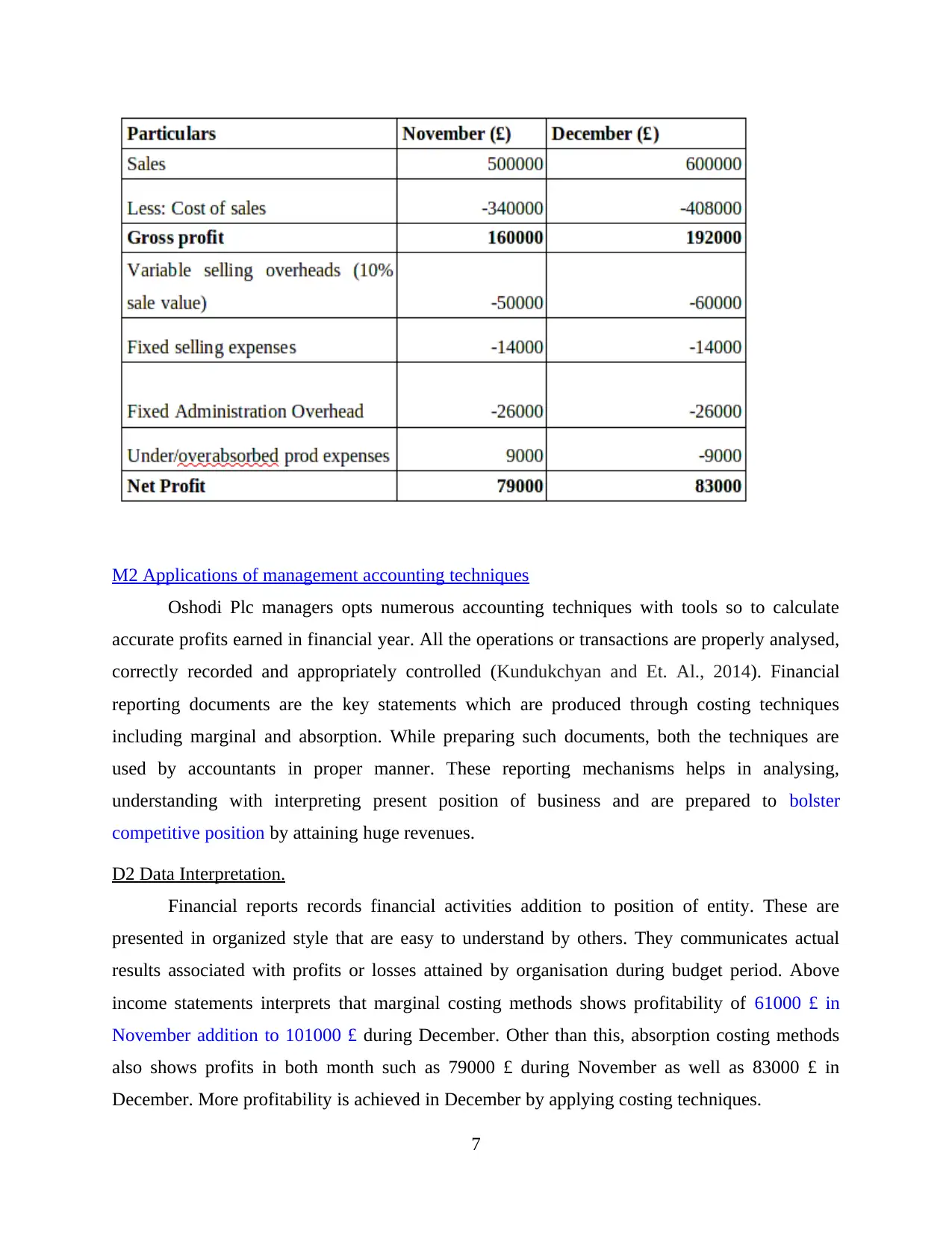

M2 Applications of management accounting techniques

Oshodi Plc managers opts numerous accounting techniques with tools so to calculate

accurate profits earned in financial year. All the operations or transactions are properly analysed,

correctly recorded and appropriately controlled (Kundukchyan and Et. Al., 2014). Financial

reporting documents are the key statements which are produced through costing techniques

including marginal and absorption. While preparing such documents, both the techniques are

used by accountants in proper manner. These reporting mechanisms helps in analysing,

understanding with interpreting present position of business and are prepared to bolster

competitive position by attaining huge revenues.

D2 Data Interpretation.

Financial reports records financial activities addition to position of entity. These are

presented in organized style that are easy to understand by others. They communicates actual

results associated with profits or losses attained by organisation during budget period. Above

income statements interprets that marginal costing methods shows profitability of 61000 £ in

November addition to 101000 £ during December. Other than this, absorption costing methods

also shows profits in both month such as 79000 £ during November as well as 83000 £ in

December. More profitability is achieved in December by applying costing techniques.

7

Oshodi Plc managers opts numerous accounting techniques with tools so to calculate

accurate profits earned in financial year. All the operations or transactions are properly analysed,

correctly recorded and appropriately controlled (Kundukchyan and Et. Al., 2014). Financial

reporting documents are the key statements which are produced through costing techniques

including marginal and absorption. While preparing such documents, both the techniques are

used by accountants in proper manner. These reporting mechanisms helps in analysing,

understanding with interpreting present position of business and are prepared to bolster

competitive position by attaining huge revenues.

D2 Data Interpretation.

Financial reports records financial activities addition to position of entity. These are

presented in organized style that are easy to understand by others. They communicates actual

results associated with profits or losses attained by organisation during budget period. Above

income statements interprets that marginal costing methods shows profitability of 61000 £ in

November addition to 101000 £ during December. Other than this, absorption costing methods

also shows profits in both month such as 79000 £ during November as well as 83000 £ in

December. More profitability is achieved in December by applying costing techniques.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

P4 Pros and shortcomings of planning tools that are utilised for budgetary control

Budget – Comprehensive and written plan which is primarily stated in numerical terms

for resources together with operations of business for particular specified future duration is said

as budget. It acts as blue map that provides directions for spendings and earnings. It is designed

to execute various functions including planning activities, communication, authorising actions,

implementing plans and monitoring. With budget statements, Oshodi Plc finance department

identifies availability of capital in current time, estimating expenditures and anticipating income

revenues.

Budgetary Control – Procedures or tools to set performance with financial objectives by

using budgets and comparing actual results in order to make further adjustments is expressed to

budgetary control. It starts with preparing budgets, recording actual outcomes, comparing true

figures with budgeted estimates, finding discrepancies, taking remedial measures. Respective

planning tools facilitating budgetary control at Oshodi Plc are:

Cash Budget – Written estimate about organisations future cash position is termed to

cash budget. It is used at Oshodi Plc to predict sources from where cash can be received,

different purposes where cash will be disbursed and final results of cash position. During stable

cash flows, it prepared for annual period but in uncertain outlooks, projections is done for

quarterly basis.

Advantages: It helps in establishing sound basis to control position of cash in current

period by setting limits for cash disbursements (Matano, 2016). Finance team of Oshodi Plc with

such budget determines surplus additionally fund shortages and accordingly undertakes suitable

actions.

Disadvantages: Using such budget, managers fails to predict time segments associated

with cash flows. Chosen organisation can not rely on on cash forecasts as future is uncertain and

anticipates forecast may be incorrect.

Master budget - Aggregate of other individual budgets is master budget. It helps in

providing directions or judging performances of responsibility centres residing within Oshodi Plc

as to have decent control on allocation of funds. It is preferred by management to coordinate

activities of overall business in order to reach stated objectives.

8

P4 Pros and shortcomings of planning tools that are utilised for budgetary control

Budget – Comprehensive and written plan which is primarily stated in numerical terms

for resources together with operations of business for particular specified future duration is said

as budget. It acts as blue map that provides directions for spendings and earnings. It is designed

to execute various functions including planning activities, communication, authorising actions,

implementing plans and monitoring. With budget statements, Oshodi Plc finance department

identifies availability of capital in current time, estimating expenditures and anticipating income

revenues.

Budgetary Control – Procedures or tools to set performance with financial objectives by

using budgets and comparing actual results in order to make further adjustments is expressed to

budgetary control. It starts with preparing budgets, recording actual outcomes, comparing true

figures with budgeted estimates, finding discrepancies, taking remedial measures. Respective

planning tools facilitating budgetary control at Oshodi Plc are:

Cash Budget – Written estimate about organisations future cash position is termed to

cash budget. It is used at Oshodi Plc to predict sources from where cash can be received,

different purposes where cash will be disbursed and final results of cash position. During stable

cash flows, it prepared for annual period but in uncertain outlooks, projections is done for

quarterly basis.

Advantages: It helps in establishing sound basis to control position of cash in current

period by setting limits for cash disbursements (Matano, 2016). Finance team of Oshodi Plc with

such budget determines surplus additionally fund shortages and accordingly undertakes suitable

actions.

Disadvantages: Using such budget, managers fails to predict time segments associated

with cash flows. Chosen organisation can not rely on on cash forecasts as future is uncertain and

anticipates forecast may be incorrect.

Master budget - Aggregate of other individual budgets is master budget. It helps in

providing directions or judging performances of responsibility centres residing within Oshodi Plc

as to have decent control on allocation of funds. It is preferred by management to coordinate

activities of overall business in order to reach stated objectives.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages: Entire year estimations are done with master budget that helps managers to

identify problems in early time and fix them with effective planning to attain long term goals

with appropriately channelizing resources.

Disadvantages: Preparing master budget requires financial analysts who can track

variances within all other budgets. It can adds overhead expenses resulting in decreasing profits.

Operating budget: Summary schedules including projected revenues additionally

associated expenses are recorded in operating budget. In context to Oshodi Plc, it recorded daily

transactions including revenues or expenses generated through sales. It shows transactions such

as staff salary, raw material purchase, administrative expenses, processing cost and loan interest.

Advantages: At Oshodi Plc, it benefits in improving efficiency by controlling expenses as

well as encouraging revenues through sales.

Disadvantages: Managing operating budget requires additional costs while running

different divisions that may not match with set allocations which can hamper estimates and

becomes impossible to control variances.

M3 Planning tools usages as well as applicability for constructing and predicting budgets

Planning tools are mainly used by management of Oshodi Plc to interpret plans towards

successful achievements. These are the instrument that guides actionable steps concerned with

implementing schedules or new innovations (Neogy, 2014). Such tools comprises logics that

breaks programmes or schemes into smaller conveyances which helps in accomplishing typical

objects conveniently. Planning tools like operating budget, cash budget along with master budget

are preferred or used while projecting future additionally planning ahead. Master budget at

selected entity is used to determine performances as well as coordinating activities with other

budgets and controlling variances.

TASK 4

P5. Comparison between organisation in the ways they adapt accounting systems for resolving

financial issues.

Financial Problems: Financial difficulties are the fund or money concerned obstacles

which give the tension to the management in operating and managing its regular day-to-day

operations and transactions. These difficulties can be created by the internal factors and external

9

identify problems in early time and fix them with effective planning to attain long term goals

with appropriately channelizing resources.

Disadvantages: Preparing master budget requires financial analysts who can track

variances within all other budgets. It can adds overhead expenses resulting in decreasing profits.

Operating budget: Summary schedules including projected revenues additionally

associated expenses are recorded in operating budget. In context to Oshodi Plc, it recorded daily

transactions including revenues or expenses generated through sales. It shows transactions such

as staff salary, raw material purchase, administrative expenses, processing cost and loan interest.

Advantages: At Oshodi Plc, it benefits in improving efficiency by controlling expenses as

well as encouraging revenues through sales.

Disadvantages: Managing operating budget requires additional costs while running

different divisions that may not match with set allocations which can hamper estimates and

becomes impossible to control variances.

M3 Planning tools usages as well as applicability for constructing and predicting budgets

Planning tools are mainly used by management of Oshodi Plc to interpret plans towards

successful achievements. These are the instrument that guides actionable steps concerned with

implementing schedules or new innovations (Neogy, 2014). Such tools comprises logics that

breaks programmes or schemes into smaller conveyances which helps in accomplishing typical

objects conveniently. Planning tools like operating budget, cash budget along with master budget

are preferred or used while projecting future additionally planning ahead. Master budget at

selected entity is used to determine performances as well as coordinating activities with other

budgets and controlling variances.

TASK 4

P5. Comparison between organisation in the ways they adapt accounting systems for resolving

financial issues.

Financial Problems: Financial difficulties are the fund or money concerned obstacles

which give the tension to the management in operating and managing its regular day-to-day

operations and transactions. These difficulties can be created by the internal factors and external

9

factors as well. Some of the major financial problems that are being faced by the respective firm,

are mentioned below:

Business Cycles: Business cycles which are also known as economic or trade cycles can

be described as the rises and falls in production results or outcomes in an economy and these ups

and downs affect the overall gross domestic products or adjusted GDP which is the major reason

for inflation or recession in the economy of the nation. This is one of the biggest challenge for

the Oshodi Plc to plan the strategies for the inescapable cyclic downswings so that the

establishment can proceed business activities through bad economical situation (Quaye, 2014).

Unforeseen Expenses: Unforeseen expenses are those which have not been taken into

consideration at the time of preparation of the budget for the expenses but they have arise

meanwhile the financial period due to some unexpected events such as machinery breakdown,

technology changes, regulatory alterations or decisions, natural disasters, etc. These unexpected

events or expenditures create huge problems for the establishments such as Oshodi Plc when the

company is already facing the financial problems due to the trade cycles.

Late payments from the customers: The companies which rely on the credit term

business, have to render services and products to the consumers for the approved period.

Sometimes these customers or debtors fail to make the payment on the given time that affect the

budget and transactions of the organization itself. These situations can arise within the firm due

to weak management of the credit policies. Regular practise of late payments from the debtors

can create high failure in the survival of the business of the selected firm.

Management accounting provides various methods, techniques and measurements that

can help the professionals in identifying these financial problems even before they take place

within the organization or get bigger (Schwartz, Connolly and Valgardson, 2018). Some of these

techniques, which can assist the managers of Oshodi PLC in determining these financial issues

are mentioned below:

Key Performance Indicators (KPI): KPI is a method that assists the administration in

examining the performance and efficiency of whole business in respect to level of success in

attaining objectives and goals. Key performance indicators aids the management to measure

deemed significant components which are extremely required and functional in relation to

accomplish business targets. The management of Oshodi Plc firm apply KPI method to assist the

10

are mentioned below:

Business Cycles: Business cycles which are also known as economic or trade cycles can

be described as the rises and falls in production results or outcomes in an economy and these ups

and downs affect the overall gross domestic products or adjusted GDP which is the major reason

for inflation or recession in the economy of the nation. This is one of the biggest challenge for

the Oshodi Plc to plan the strategies for the inescapable cyclic downswings so that the

establishment can proceed business activities through bad economical situation (Quaye, 2014).

Unforeseen Expenses: Unforeseen expenses are those which have not been taken into

consideration at the time of preparation of the budget for the expenses but they have arise

meanwhile the financial period due to some unexpected events such as machinery breakdown,

technology changes, regulatory alterations or decisions, natural disasters, etc. These unexpected

events or expenditures create huge problems for the establishments such as Oshodi Plc when the

company is already facing the financial problems due to the trade cycles.

Late payments from the customers: The companies which rely on the credit term

business, have to render services and products to the consumers for the approved period.

Sometimes these customers or debtors fail to make the payment on the given time that affect the

budget and transactions of the organization itself. These situations can arise within the firm due

to weak management of the credit policies. Regular practise of late payments from the debtors

can create high failure in the survival of the business of the selected firm.

Management accounting provides various methods, techniques and measurements that

can help the professionals in identifying these financial problems even before they take place

within the organization or get bigger (Schwartz, Connolly and Valgardson, 2018). Some of these

techniques, which can assist the managers of Oshodi PLC in determining these financial issues

are mentioned below:

Key Performance Indicators (KPI): KPI is a method that assists the administration in

examining the performance and efficiency of whole business in respect to level of success in

attaining objectives and goals. Key performance indicators aids the management to measure

deemed significant components which are extremely required and functional in relation to

accomplish business targets. The management of Oshodi Plc firm apply KPI method to assist the

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.