Management Accounting Report: Oshodi Plc's Financial Performance

VerifiedAdded on 2021/02/22

|15

|4424

|59

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices at Oshodi Plc, a UK-based fruit juice manufacturer. It begins with an introduction to management accounting and its essential requirements, focusing on the different accounting systems like cost accounting, inventory management, and price optimization. The report then explores the benefits of these systems and their integration within organizational processes, emphasizing the importance of various management accounting reports such as performance reports, inventory management reports, and accounts receivable reports. Furthermore, the report delves into the application of cost analysis techniques to prepare income statements using both marginal and absorption costing methods, including detailed calculations and comparisons. The analysis includes income statements for November and December, showcasing the impact of different costing methods on profitability. The report concludes by summarizing the key findings and their implications for effective decision-making within Oshodi Plc.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Management accounting is an idea that involves an assessment of inner management

company operations that facilitates smart decision-making. It will be regarded as cost accounting

also, which assists in analyse the organization's expenses of further supporting the development

of financials depicting the workings of the organizations ' inner departments. This will include

the use of accounting regulations to determine the economic and statistical data that further

supports the efficient control of company activities resulting in the achievement of organizational

goals within a specified time-frame (Al-Mawali, Zainuddin and Nasir Kader Ali, 2012). This will

enable the organizations ' inner stakeholders to match their concerns completely with the

organization's processes to achieve effectiveness in their very own job. Oshodi Plc is

manufacturer in UK that specializes in production of fruit juice named “JOJO” across whole age

groups. The primary goal behind preparing of this study is providing data about the relationship

and working of inner departments for sound decision-making to the organization's internal

shareholders.

This study includes the vital content about management accounting and requirements of

distinct kinds of accounting management systems, accounting management's reports and

applying of proper cost analysis techniques in the forming of income or revenue statement

through marginal and absorption approaches. The study also analyse planning tools'

disadvantages and advantages in structure of budgetary control and utilisation of management

accounting systems to address and short out economic issues.

TASK 1

P1 Management accounting and essential requirements of management accounting systems:

Introduction: Management accounting is a branch of accounting which deals with the

presentation of key financial statements and information to the management. The management

uses financial information to draw inferences about the performance of the organisation, and

design strategies for the future endeavours (Management Accounting. 2018). Oshodi PLC is a

beverage manufacturing firm engaged in making fruit juice under the brand 'Jojo fruit juice' . At

Oshodi PLC Management Accounting systems is made up of various accounts and sub systems

where all such systems work together in mechanising critical information about the business

which the management uses to design policy framework.

1

Management accounting is an idea that involves an assessment of inner management

company operations that facilitates smart decision-making. It will be regarded as cost accounting

also, which assists in analyse the organization's expenses of further supporting the development

of financials depicting the workings of the organizations ' inner departments. This will include

the use of accounting regulations to determine the economic and statistical data that further

supports the efficient control of company activities resulting in the achievement of organizational

goals within a specified time-frame (Al-Mawali, Zainuddin and Nasir Kader Ali, 2012). This will

enable the organizations ' inner stakeholders to match their concerns completely with the

organization's processes to achieve effectiveness in their very own job. Oshodi Plc is

manufacturer in UK that specializes in production of fruit juice named “JOJO” across whole age

groups. The primary goal behind preparing of this study is providing data about the relationship

and working of inner departments for sound decision-making to the organization's internal

shareholders.

This study includes the vital content about management accounting and requirements of

distinct kinds of accounting management systems, accounting management's reports and

applying of proper cost analysis techniques in the forming of income or revenue statement

through marginal and absorption approaches. The study also analyse planning tools'

disadvantages and advantages in structure of budgetary control and utilisation of management

accounting systems to address and short out economic issues.

TASK 1

P1 Management accounting and essential requirements of management accounting systems:

Introduction: Management accounting is a branch of accounting which deals with the

presentation of key financial statements and information to the management. The management

uses financial information to draw inferences about the performance of the organisation, and

design strategies for the future endeavours (Management Accounting. 2018). Oshodi PLC is a

beverage manufacturing firm engaged in making fruit juice under the brand 'Jojo fruit juice' . At

Oshodi PLC Management Accounting systems is made up of various accounts and sub systems

where all such systems work together in mechanising critical information about the business

which the management uses to design policy framework.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting : It is a fundamental science which deals with preparation of

annual financial statements using standards, providing just and fair financial data to the

management to study the behaviour of organisation and the designing policies and strategies for

the upcoming business periods. It is in complete contrast with financial accounting, since both

have different purposes. Management accounting is concerned with internal executives only ,

while financial accounting is the information provided to the external stakeholders.

Management Accounting systems : Management accounting is a fundamental approach

to deal with the financial information of an organisation which is supported by several functional

sub-sets. These sub-sets include various systems such as inventory management system, cost

accounting system, price optimisation system etc (Abdelmoneim Mohamed and Jones, 2014).

These all systems have individual characteristics and functions of generating relevant

information belonging to their core principles. These sub systems has helped Oshodi Plc for

years in devising cost cutting mechanisms, achieving higher net profit margins and ensuring

profitability index at high. These systems are discussed in detail as follows :

Cost accounting system : This system is used to determine the various costs incurred on

the production of Jojo fruit juice as per the volume. There are different kinds of costs associated

with the production function such as fixed costs, variable costs, direct and indirect costs and

overhead expenses. Costing system helps in allocation of costs to each input working in the

preparation of final product as an internal factor of production. By allocating costs , it would be

easier for the management to identify the final price for the product.

Inventory management system : This system deals with the management of stock, raw

materials, and the flow of goods from the initial stage of preparation to the final stage of

delivery. It helps the Oshodi Plc inventory manager in procuring the required raw materials

needed for the preparation of juices based on the ordering capacity. It also helps in maintaining

accurate supply chain and distribution channels to all the retailers and distributors by keeping

live record of the present flow of goods. Reordering of raw materials is done by Economic order

quantity method at Oshodi plc.

Price optimisation system : This system helps the Oshodi plc's management in

designing pricing strategies for the range of products. It also helps in analysing price of each

activity which supports the management with the insights on the areas where extra cost could be

saved from dilution. It is based on the mix of cost model and sales model. The combination of

2

annual financial statements using standards, providing just and fair financial data to the

management to study the behaviour of organisation and the designing policies and strategies for

the upcoming business periods. It is in complete contrast with financial accounting, since both

have different purposes. Management accounting is concerned with internal executives only ,

while financial accounting is the information provided to the external stakeholders.

Management Accounting systems : Management accounting is a fundamental approach

to deal with the financial information of an organisation which is supported by several functional

sub-sets. These sub-sets include various systems such as inventory management system, cost

accounting system, price optimisation system etc (Abdelmoneim Mohamed and Jones, 2014).

These all systems have individual characteristics and functions of generating relevant

information belonging to their core principles. These sub systems has helped Oshodi Plc for

years in devising cost cutting mechanisms, achieving higher net profit margins and ensuring

profitability index at high. These systems are discussed in detail as follows :

Cost accounting system : This system is used to determine the various costs incurred on

the production of Jojo fruit juice as per the volume. There are different kinds of costs associated

with the production function such as fixed costs, variable costs, direct and indirect costs and

overhead expenses. Costing system helps in allocation of costs to each input working in the

preparation of final product as an internal factor of production. By allocating costs , it would be

easier for the management to identify the final price for the product.

Inventory management system : This system deals with the management of stock, raw

materials, and the flow of goods from the initial stage of preparation to the final stage of

delivery. It helps the Oshodi Plc inventory manager in procuring the required raw materials

needed for the preparation of juices based on the ordering capacity. It also helps in maintaining

accurate supply chain and distribution channels to all the retailers and distributors by keeping

live record of the present flow of goods. Reordering of raw materials is done by Economic order

quantity method at Oshodi plc.

Price optimisation system : This system helps the Oshodi plc's management in

designing pricing strategies for the range of products. It also helps in analysing price of each

activity which supports the management with the insights on the areas where extra cost could be

saved from dilution. It is based on the mix of cost model and sales model. The combination of

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

two determinants manifests key model of pricing the products. It is a set of mathematical models

which determine the variation in demand for various price levels which in addition to cost helps

in deciding final price for the juice.

Job costing system : This system provides critical data about the costs associated with

various services within the organisation. This system determines the cost allocation to each

factor input which in turn gives valuable information to the client about the costs specified

(Bagautdinova, Kundakchyan and Malakhov, 2013). Further more, it also helps in evaluation of

profit making capacity of each job in respect to the cost which has been incurred on it.

Conclusion : Management accounting system is an integral part of an organisation in the

modern day corporate scenario where every single digit of financial information is critical in

decision making. Management accounting systems aids the executives in providing key sectoral

data to form part of ultimate financial information for the business.

M1 benefits of management Accounting systems

Cost accounting system

This scheme will help assess the effectiveness of distinct procedures and afterwards help

introduce further changes.

This will aid in fixation and reduction of price.

Job costing system

It will assist Oshodi to assess all types of task expenses during the fruit juice “JOJO”

preparation phase.

It helps to reduce effort which may arise due to duplication.

Price optimisation system

By adopting the highest effective rates, it helps Oshodi maximize its operating profit.

This will assist in determining consumer behaviour based on product's distinct prices

(Demski, 2013).

Inventory management system

It minimise time and cost involved in managing stocks.

This assist in developing framework for accurate and systematic sequences of inventory's

order.

3

which determine the variation in demand for various price levels which in addition to cost helps

in deciding final price for the juice.

Job costing system : This system provides critical data about the costs associated with

various services within the organisation. This system determines the cost allocation to each

factor input which in turn gives valuable information to the client about the costs specified

(Bagautdinova, Kundakchyan and Malakhov, 2013). Further more, it also helps in evaluation of

profit making capacity of each job in respect to the cost which has been incurred on it.

Conclusion : Management accounting system is an integral part of an organisation in the

modern day corporate scenario where every single digit of financial information is critical in

decision making. Management accounting systems aids the executives in providing key sectoral

data to form part of ultimate financial information for the business.

M1 benefits of management Accounting systems

Cost accounting system

This scheme will help assess the effectiveness of distinct procedures and afterwards help

introduce further changes.

This will aid in fixation and reduction of price.

Job costing system

It will assist Oshodi to assess all types of task expenses during the fruit juice “JOJO”

preparation phase.

It helps to reduce effort which may arise due to duplication.

Price optimisation system

By adopting the highest effective rates, it helps Oshodi maximize its operating profit.

This will assist in determining consumer behaviour based on product's distinct prices

(Demski, 2013).

Inventory management system

It minimise time and cost involved in managing stocks.

This assist in developing framework for accurate and systematic sequences of inventory's

order.

3

D1 Integration of management accounting system and report within organisational process

Type of reporting & Systems Integration with organisational process

Performance report: It is formed according

to the informations gathered from one or

more systems. It contains data about actual

or existing performance of personnels across

different departments within Oshodi Plc.

Integration of such report in different process can

be determined from fact that it would be helpful

in acquiring differentiation in producing fruit

juice because all variations can be abstracted

using such report.

Inventory management report: Respective

report is being prepared through integration

of content and information gathered from

inventory system (DRURY, 2013).

Integration of such report in entity's process can

be easily understood as it assist Oshodi to

organise essential items to prepare fruit juice and

approximation of needed scale of orders for

purchase.

P2 Different methods of management accounting reports:

Introduction : This part will introduce various types of management accounting reports

as suggested in the literature and their uses in an organisation to help it increase efficiency and

achieve targets. And their role in helping management with decision making.

Management accounting reports : Management accounting reports provide insights

which are very informational and important for a business. These reports helps in decision

making, promulgating strategies and measuring performance of the business areas. Major

business decisions are based on these reports authenticity. The major reports prepared at Oshodi

plc are as follows:

Inventory management report : This report contains information about the inventory

level at all times in the organisation. The report includes data about the raw materials ordered per

volume, the capacity of stock to produce material, goods delivered on the depots and the goods

which are in transit (Eierle and Schultze, 2013). This report helps the management in identifying

the production capacity of the plant and conducting the demand supply analysis.

Performance report: This report contains the performance evaluation of the various

functional departments and the employees working in the organisation. This report helps the

Human resource department at Oshodi plc to identify the key performing departments and

employees, their share in the profit generation and the capacity of them to build the organisation

4

Type of reporting & Systems Integration with organisational process

Performance report: It is formed according

to the informations gathered from one or

more systems. It contains data about actual

or existing performance of personnels across

different departments within Oshodi Plc.

Integration of such report in different process can

be determined from fact that it would be helpful

in acquiring differentiation in producing fruit

juice because all variations can be abstracted

using such report.

Inventory management report: Respective

report is being prepared through integration

of content and information gathered from

inventory system (DRURY, 2013).

Integration of such report in entity's process can

be easily understood as it assist Oshodi to

organise essential items to prepare fruit juice and

approximation of needed scale of orders for

purchase.

P2 Different methods of management accounting reports:

Introduction : This part will introduce various types of management accounting reports

as suggested in the literature and their uses in an organisation to help it increase efficiency and

achieve targets. And their role in helping management with decision making.

Management accounting reports : Management accounting reports provide insights

which are very informational and important for a business. These reports helps in decision

making, promulgating strategies and measuring performance of the business areas. Major

business decisions are based on these reports authenticity. The major reports prepared at Oshodi

plc are as follows:

Inventory management report : This report contains information about the inventory

level at all times in the organisation. The report includes data about the raw materials ordered per

volume, the capacity of stock to produce material, goods delivered on the depots and the goods

which are in transit (Eierle and Schultze, 2013). This report helps the management in identifying

the production capacity of the plant and conducting the demand supply analysis.

Performance report: This report contains the performance evaluation of the various

functional departments and the employees working in the organisation. This report helps the

Human resource department at Oshodi plc to identify the key performing departments and

employees, their share in the profit generation and the capacity of them to build the organisation

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

more bigger. This helps the managers to design the motivation, training and development

programmes for the underperforming employees.

Account receivable report : This report provides information about the bills to be

received from the debtors, cash memos, invoices, bills paid and received, and other cash related

information. This report helps the Oshodi plc in identifying the liquidity position of the firm.

This also helps in managing the cash flow fluently and ensuring that no funds gets siphoned due

to poor management. This report is instrumental in designing effective reserve policy.

Conclusion : It is been concluded from the segment that management accounting

reports has a key role to play in the success of the business as they report critical information

about the key areas of the business.

TASK 2

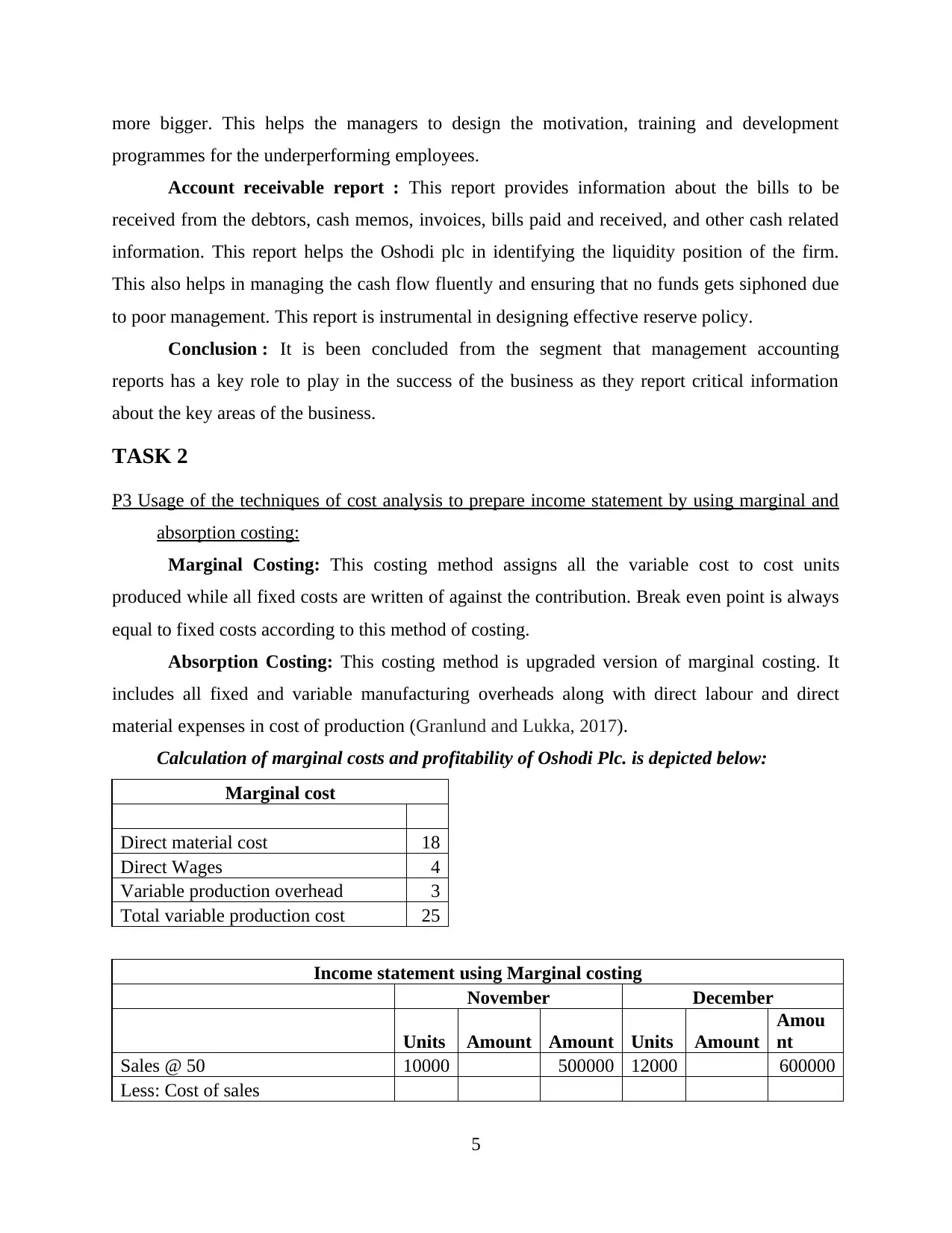

P3 Usage of the techniques of cost analysis to prepare income statement by using marginal and

absorption costing:

Marginal Costing: This costing method assigns all the variable cost to cost units

produced while all fixed costs are written of against the contribution. Break even point is always

equal to fixed costs according to this method of costing.

Absorption Costing: This costing method is upgraded version of marginal costing. It

includes all fixed and variable manufacturing overheads along with direct labour and direct

material expenses in cost of production (Granlund and Lukka, 2017).

Calculation of marginal costs and profitability of Oshodi Plc. is depicted below:

Marginal cost

Direct material cost 18

Direct Wages 4

Variable production overhead 3

Total variable production cost 25

Income statement using Marginal costing

November December

Units Amount Amount Units Amount

Amou

nt

Sales @ 50 10000 500000 12000 600000

Less: Cost of sales

5

programmes for the underperforming employees.

Account receivable report : This report provides information about the bills to be

received from the debtors, cash memos, invoices, bills paid and received, and other cash related

information. This report helps the Oshodi plc in identifying the liquidity position of the firm.

This also helps in managing the cash flow fluently and ensuring that no funds gets siphoned due

to poor management. This report is instrumental in designing effective reserve policy.

Conclusion : It is been concluded from the segment that management accounting

reports has a key role to play in the success of the business as they report critical information

about the key areas of the business.

TASK 2

P3 Usage of the techniques of cost analysis to prepare income statement by using marginal and

absorption costing:

Marginal Costing: This costing method assigns all the variable cost to cost units

produced while all fixed costs are written of against the contribution. Break even point is always

equal to fixed costs according to this method of costing.

Absorption Costing: This costing method is upgraded version of marginal costing. It

includes all fixed and variable manufacturing overheads along with direct labour and direct

material expenses in cost of production (Granlund and Lukka, 2017).

Calculation of marginal costs and profitability of Oshodi Plc. is depicted below:

Marginal cost

Direct material cost 18

Direct Wages 4

Variable production overhead 3

Total variable production cost 25

Income statement using Marginal costing

November December

Units Amount Amount Units Amount

Amou

nt

Sales @ 50 10000 500000 12000 600000

Less: Cost of sales

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Opening stock @ 25 2000 50000

Variable cost of production @ 25 12000 300000 10000 250000

Less: Closing stock @ 25 2000 50000

250000 300000

Variable selling overhead 50000 60000

Total variable cost of sales 300000 360000

Contribution 200000 240000

Fixed overheads:

Production 99000 99000

Selling 14000 14000

Administration 26000 139000 26000 139000

Net profit 61000 101000

Calculation of net profit using absorption costing along with ascertainment of over

(under) absorption cost:

Income statement using Absorption costing

November December

Units Amount Amount Units Amount

Amou

nt

Sales @ 50 10000 500000 12000 600000

Less: Cost of sales

Opening stock @ 29 2000 58000

Variable cost of production @ 29 12000 348000 10000 290000

Less: Closing stock @ 29 2000 58000

290000 348000

Gross profit 210000 252000

Adjustment for over / under ab-

sorption of overheads 9000 9000

219000 243000

Fixed overheads:

Variable selling overhead 50000 60000

Fixed selling overhead 14000 14000

Fixed Administration overhead 26000 90000 26000 100000

Net profit 129000 143000

Working Notes:

Fixed production overhead absorption rate 99000/11000 9

Full production cost for one unit to be used in stock valuation

is: 29

Variable cost 25

6

Variable cost of production @ 25 12000 300000 10000 250000

Less: Closing stock @ 25 2000 50000

250000 300000

Variable selling overhead 50000 60000

Total variable cost of sales 300000 360000

Contribution 200000 240000

Fixed overheads:

Production 99000 99000

Selling 14000 14000

Administration 26000 139000 26000 139000

Net profit 61000 101000

Calculation of net profit using absorption costing along with ascertainment of over

(under) absorption cost:

Income statement using Absorption costing

November December

Units Amount Amount Units Amount

Amou

nt

Sales @ 50 10000 500000 12000 600000

Less: Cost of sales

Opening stock @ 29 2000 58000

Variable cost of production @ 29 12000 348000 10000 290000

Less: Closing stock @ 29 2000 58000

290000 348000

Gross profit 210000 252000

Adjustment for over / under ab-

sorption of overheads 9000 9000

219000 243000

Fixed overheads:

Variable selling overhead 50000 60000

Fixed selling overhead 14000 14000

Fixed Administration overhead 26000 90000 26000 100000

Net profit 129000 143000

Working Notes:

Fixed production overhead absorption rate 99000/11000 9

Full production cost for one unit to be used in stock valuation

is: 29

Variable cost 25

6

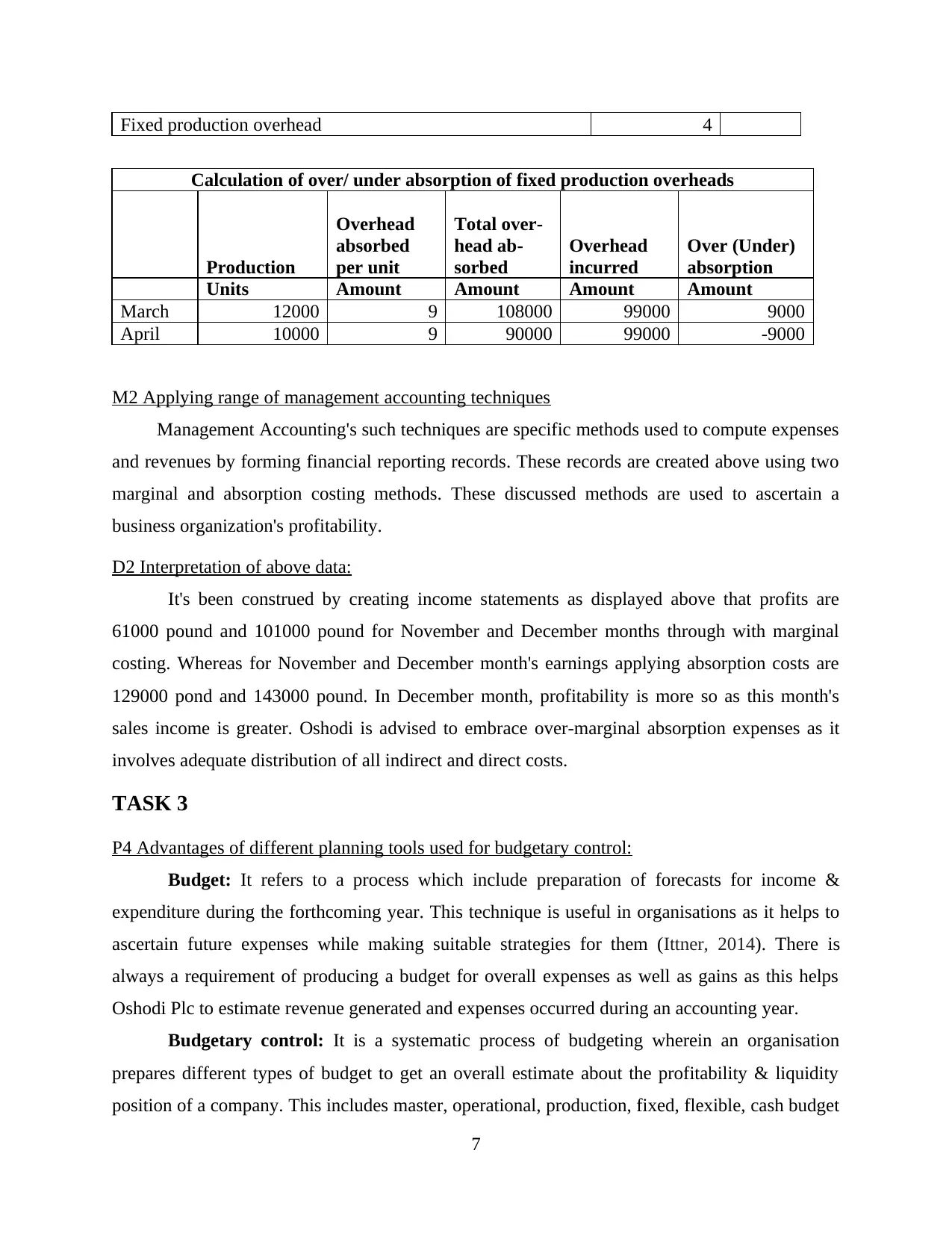

Fixed production overhead 4

Calculation of over/ under absorption of fixed production overheads

Production

Overhead

absorbed

per unit

Total over-

head ab-

sorbed

Overhead

incurred

Over (Under)

absorption

Units Amount Amount Amount Amount

March 12000 9 108000 99000 9000

April 10000 9 90000 99000 -9000

M2 Applying range of management accounting techniques

Management Accounting's such techniques are specific methods used to compute expenses

and revenues by forming financial reporting records. These records are created above using two

marginal and absorption costing methods. These discussed methods are used to ascertain a

business organization's profitability.

D2 Interpretation of above data:

It's been construed by creating income statements as displayed above that profits are

61000 pound and 101000 pound for November and December months through with marginal

costing. Whereas for November and December month's earnings applying absorption costs are

129000 pond and 143000 pound. In December month, profitability is more so as this month's

sales income is greater. Oshodi is advised to embrace over-marginal absorption expenses as it

involves adequate distribution of all indirect and direct costs.

TASK 3

P4 Advantages of different planning tools used for budgetary control:

Budget: It refers to a process which include preparation of forecasts for income &

expenditure during the forthcoming year. This technique is useful in organisations as it helps to

ascertain future expenses while making suitable strategies for them (Ittner, 2014). There is

always a requirement of producing a budget for overall expenses as well as gains as this helps

Oshodi Plc to estimate revenue generated and expenses occurred during an accounting year.

Budgetary control: It is a systematic process of budgeting wherein an organisation

prepares different types of budget to get an overall estimate about the profitability & liquidity

position of a company. This includes master, operational, production, fixed, flexible, cash budget

7

Calculation of over/ under absorption of fixed production overheads

Production

Overhead

absorbed

per unit

Total over-

head ab-

sorbed

Overhead

incurred

Over (Under)

absorption

Units Amount Amount Amount Amount

March 12000 9 108000 99000 9000

April 10000 9 90000 99000 -9000

M2 Applying range of management accounting techniques

Management Accounting's such techniques are specific methods used to compute expenses

and revenues by forming financial reporting records. These records are created above using two

marginal and absorption costing methods. These discussed methods are used to ascertain a

business organization's profitability.

D2 Interpretation of above data:

It's been construed by creating income statements as displayed above that profits are

61000 pound and 101000 pound for November and December months through with marginal

costing. Whereas for November and December month's earnings applying absorption costs are

129000 pond and 143000 pound. In December month, profitability is more so as this month's

sales income is greater. Oshodi is advised to embrace over-marginal absorption expenses as it

involves adequate distribution of all indirect and direct costs.

TASK 3

P4 Advantages of different planning tools used for budgetary control:

Budget: It refers to a process which include preparation of forecasts for income &

expenditure during the forthcoming year. This technique is useful in organisations as it helps to

ascertain future expenses while making suitable strategies for them (Ittner, 2014). There is

always a requirement of producing a budget for overall expenses as well as gains as this helps

Oshodi Plc to estimate revenue generated and expenses occurred during an accounting year.

Budgetary control: It is a systematic process of budgeting wherein an organisation

prepares different types of budget to get an overall estimate about the profitability & liquidity

position of a company. This includes master, operational, production, fixed, flexible, cash budget

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

etc. It also ensures that a comparison has been done between actual as well as budgeted data so

that chances of error are less. Oshodi Plc follows a budgetary control procedure that comprise of

producing various kinds of forecast to analyse any variations in the process of budgeting.

Some of the budgetary control procedures are mentioned below:

Master budget: It is a planning tool which shows a summarised format of all individual

budgets prepared by an organisation. This can include cash, sales, production, manufacturing

budget etc. Every forecast that is produced is related with a different purpose and helps Oshodi

Plc in that way (Lääts and Haldma, 2012). For example, a cash forecast provides information

about the availability of cash whereas a manufacturing budget will include all the activities

related to products & services etc.

Advantages:

A master budget involves master planning about the resources which will be allocated among

different functional units.

This budget facilitates organisations like Oshodi Plc by summarising all individual budgets under

a single forecasted statement.

Disadvantages:

It includes a collective sum of all the budgets prepared so if managers at Oshodi Plc need

to find out the estimation of a separate budget then in that case it become a complex

process to brainstorm the figures presented.

This is difficult to update in case of any changes in estimation of amounts since it

complies all smaller budgets into a single forecast (Morden, 2016).

Zero-based budget: This refers to a planning tool in which forecasts are prepared from

scratch without considering previous year's income or expenses. It is a budget which is produced

from a zero-base and is required by managers of Oshodi Plc to plan & discuss how much funds

should be allotted to each department within an organisation.

Advantages:

It enhances co-ordination as well as communication among staff while preparing the

zero-based budget.

This also helps Oshodi Plc as with the help of this budgetary tool they can keep an eye on

every income generated and expense spent by the employees.

Disadvantages:

8

that chances of error are less. Oshodi Plc follows a budgetary control procedure that comprise of

producing various kinds of forecast to analyse any variations in the process of budgeting.

Some of the budgetary control procedures are mentioned below:

Master budget: It is a planning tool which shows a summarised format of all individual

budgets prepared by an organisation. This can include cash, sales, production, manufacturing

budget etc. Every forecast that is produced is related with a different purpose and helps Oshodi

Plc in that way (Lääts and Haldma, 2012). For example, a cash forecast provides information

about the availability of cash whereas a manufacturing budget will include all the activities

related to products & services etc.

Advantages:

A master budget involves master planning about the resources which will be allocated among

different functional units.

This budget facilitates organisations like Oshodi Plc by summarising all individual budgets under

a single forecasted statement.

Disadvantages:

It includes a collective sum of all the budgets prepared so if managers at Oshodi Plc need

to find out the estimation of a separate budget then in that case it become a complex

process to brainstorm the figures presented.

This is difficult to update in case of any changes in estimation of amounts since it

complies all smaller budgets into a single forecast (Morden, 2016).

Zero-based budget: This refers to a planning tool in which forecasts are prepared from

scratch without considering previous year's income or expenses. It is a budget which is produced

from a zero-base and is required by managers of Oshodi Plc to plan & discuss how much funds

should be allotted to each department within an organisation.

Advantages:

It enhances co-ordination as well as communication among staff while preparing the

zero-based budget.

This also helps Oshodi Plc as with the help of this budgetary tool they can keep an eye on

every income generated and expense spent by the employees.

Disadvantages:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is a very time-consuming process as every penny spent on manufacturing JOJO fruit

juice should be recorded.

For long-term practice, zero-based budgeting is not appropriate as the price that would be

charged for fruit juice cannot be estimated now.

Operational budget: It is a type of budget which records all the day-to-day monetary

transactions occurring in an organisation. With the help of operational budget, Oshodi Plc can

project all the estimated income and expenses based on forecasted sales revenue during an

accounting year (Mussnig, 2013). The company can also use this budget to set p[rices for its

JOJO fruit juice offered to the public.

Advantages:

With the help of operational budget, Oshodi Plc keeps a track on current expenses

incurred in the manufacturing of JOJO fruit juice packages.

This also helps the management by ensuring that all the daily expenses are effectively

managed within an organisation.

Disadvantages:

It creates a difficulty in allocation of funds to various activities in an organisation. Oshodi

Plc is having difficulties in determining the price that should be availed on large bottles

of JOJO fruit juice.

Operating budget does not account for capital expenses due to which it can result in

manipulation of figures.

M3. Analyze the use of different planning tools and their application for preparing and

forecasting budgets;

In Oshodi Plc, planning tools contribute in providing framework to build a reliable base

for estimation of vital amount in budgets. Company's managerial personnels prepares sub

budgets and budgets to adjust company's processes to address any issues and determine futuristic

figures. The cash budget is being used to measuring the amount of funds an organization has

throughout all the distinct quarters. This will assist keep the money limit that offers an chance to

carry out their money transactions, reducing interest expenses. This would also assist to achieve

sustainable achievement as a means of achieving adequate profit margin.

9

juice should be recorded.

For long-term practice, zero-based budgeting is not appropriate as the price that would be

charged for fruit juice cannot be estimated now.

Operational budget: It is a type of budget which records all the day-to-day monetary

transactions occurring in an organisation. With the help of operational budget, Oshodi Plc can

project all the estimated income and expenses based on forecasted sales revenue during an

accounting year (Mussnig, 2013). The company can also use this budget to set p[rices for its

JOJO fruit juice offered to the public.

Advantages:

With the help of operational budget, Oshodi Plc keeps a track on current expenses

incurred in the manufacturing of JOJO fruit juice packages.

This also helps the management by ensuring that all the daily expenses are effectively

managed within an organisation.

Disadvantages:

It creates a difficulty in allocation of funds to various activities in an organisation. Oshodi

Plc is having difficulties in determining the price that should be availed on large bottles

of JOJO fruit juice.

Operating budget does not account for capital expenses due to which it can result in

manipulation of figures.

M3. Analyze the use of different planning tools and their application for preparing and

forecasting budgets;

In Oshodi Plc, planning tools contribute in providing framework to build a reliable base

for estimation of vital amount in budgets. Company's managerial personnels prepares sub

budgets and budgets to adjust company's processes to address any issues and determine futuristic

figures. The cash budget is being used to measuring the amount of funds an organization has

throughout all the distinct quarters. This will assist keep the money limit that offers an chance to

carry out their money transactions, reducing interest expenses. This would also assist to achieve

sustainable achievement as a means of achieving adequate profit margin.

9

TASK 4

P5 Adoption of management accounting systems to respond financial problems:

Introduction : Management accounting systems have a wide contribution in an

organisation by analysing problems and providing solutions of the possible problems. This apart

covers the financial problems which an organisation may face and the possible solutions to these

problems. Oshodi plc is working in a competitive market and it is evident from the examples

surrounded that any organisation can fall prey to the havoc of financial dilution if not managed

properly. The possible financial problems which can be faced by Oshodi plc are :

Poor cash management : Siphoning and mismanagement of funds is the biggest reason a

n organisation dooms. The profits earned by the business often fall prey to the ill deeds of some

managers or the loopholes in the system (Myers, 2013).

Inappropriate decision making : Right decisions makes an organisation and wrong

decisions destroys it. Decision making power should be based on some key factors and the power

to make robust decisions should be centralised.

To take on these key problems, Oshodi plc has invested in some managerial tactics which

comes quite handy in fighting these issues. Each has its own budgetary control contribution and

enables the organization to react to economic or financial problems and improve internal

strength. There is utilization of various management tools and significant systems such as

Benchmarking and KPI. Their functioning helps to construct norms and adjust accordingly,

resulting in the future to resolve financial problems that become the organization's reason for

failure. The tools used by it are as follows :

Benchmarking : It is a technique to evaluate organisational performance by comparing it

with the industrial parameters known as 'benchmarks' set by the top management practices.

Comparing performance with the industries best practices motivates the employees and

management to reach at par with the best practices and ensure continuous development

(Namakonzi and Inanga, 2014). This technique has helped Oshodi Plc in achieving optimum

utilisation of its resources.

Key performance indicators : KPI are key determinants which help in evaluating

performance on each stage of time. These key factors are used as internal benchmarks by the

firm. It is the continuous effort of the employees to achieve these key targets during the

production activities. The key indicators ensure that the organisation is working at its full

10

P5 Adoption of management accounting systems to respond financial problems:

Introduction : Management accounting systems have a wide contribution in an

organisation by analysing problems and providing solutions of the possible problems. This apart

covers the financial problems which an organisation may face and the possible solutions to these

problems. Oshodi plc is working in a competitive market and it is evident from the examples

surrounded that any organisation can fall prey to the havoc of financial dilution if not managed

properly. The possible financial problems which can be faced by Oshodi plc are :

Poor cash management : Siphoning and mismanagement of funds is the biggest reason a

n organisation dooms. The profits earned by the business often fall prey to the ill deeds of some

managers or the loopholes in the system (Myers, 2013).

Inappropriate decision making : Right decisions makes an organisation and wrong

decisions destroys it. Decision making power should be based on some key factors and the power

to make robust decisions should be centralised.

To take on these key problems, Oshodi plc has invested in some managerial tactics which

comes quite handy in fighting these issues. Each has its own budgetary control contribution and

enables the organization to react to economic or financial problems and improve internal

strength. There is utilization of various management tools and significant systems such as

Benchmarking and KPI. Their functioning helps to construct norms and adjust accordingly,

resulting in the future to resolve financial problems that become the organization's reason for

failure. The tools used by it are as follows :

Benchmarking : It is a technique to evaluate organisational performance by comparing it

with the industrial parameters known as 'benchmarks' set by the top management practices.

Comparing performance with the industries best practices motivates the employees and

management to reach at par with the best practices and ensure continuous development

(Namakonzi and Inanga, 2014). This technique has helped Oshodi Plc in achieving optimum

utilisation of its resources.

Key performance indicators : KPI are key determinants which help in evaluating

performance on each stage of time. These key factors are used as internal benchmarks by the

firm. It is the continuous effort of the employees to achieve these key targets during the

production activities. The key indicators ensure that the organisation is working at its full

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.