Management Accounting: T&K Accounting Services Case Study Report

VerifiedAdded on 2022/11/27

|10

|1431

|387

Report

AI Summary

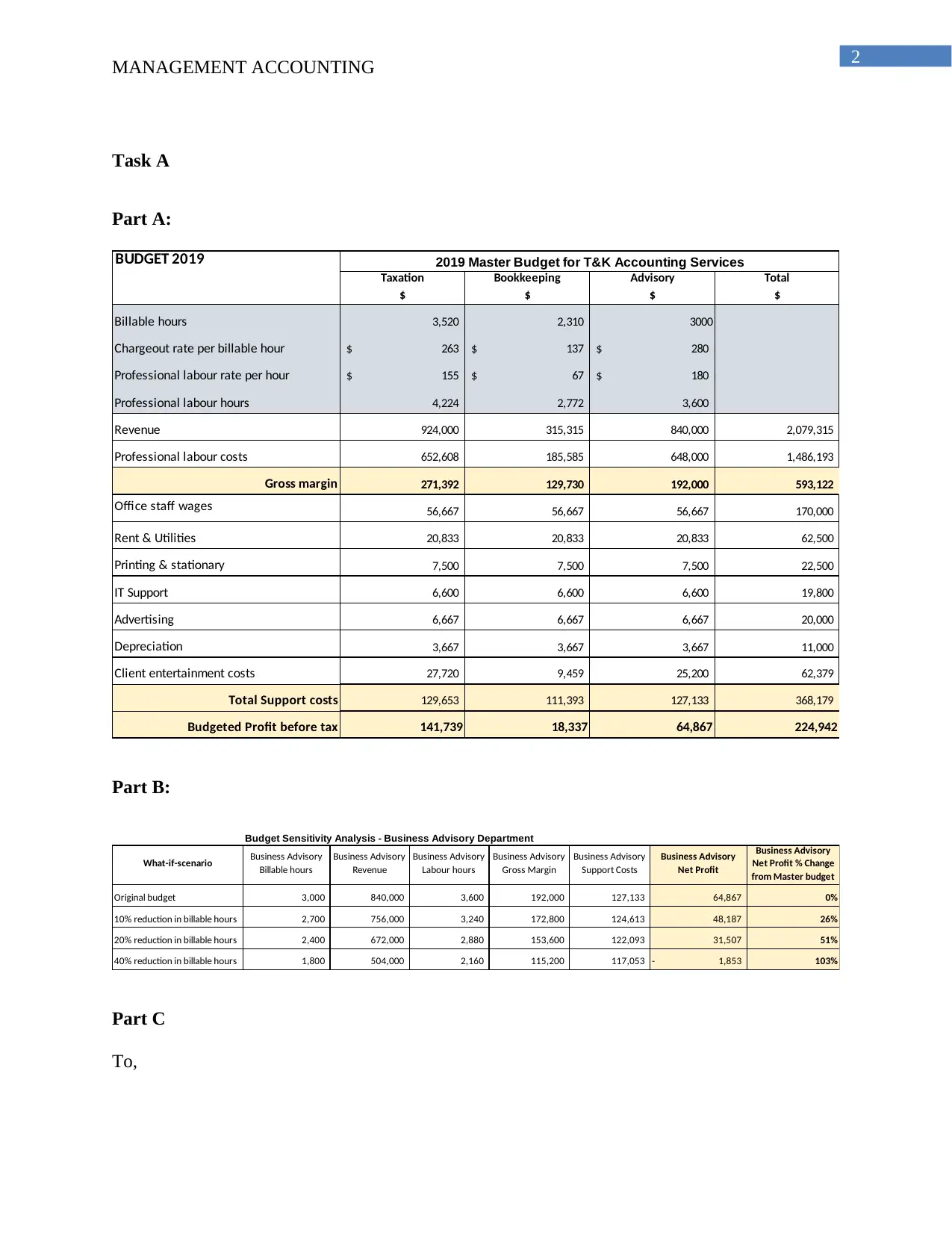

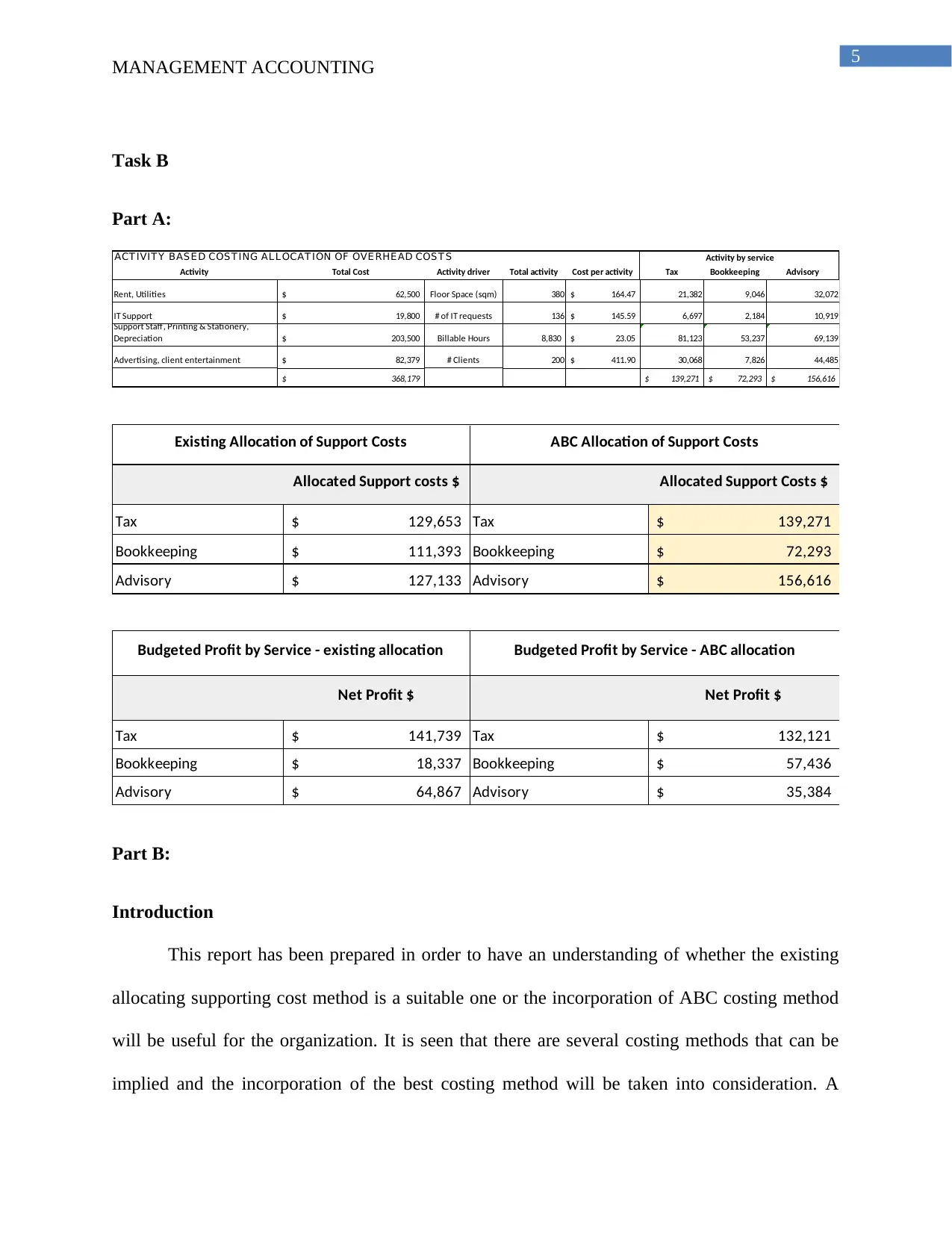

This report presents a comprehensive analysis of T&K Accounting Services, focusing on management accounting principles. Task A evaluates the potential addition of an advisory department, comparing projected costs and profits to determine its financial viability. The analysis uses provided financial data, including billable hours, chargeout rates, and support costs, to assess the impact on net profit before tax. Task B examines the suitability of the current cost allocation method versus the Activity-Based Costing (ABC) method. It compares the costs and net profits of the tax, bookkeeping, and advisory departments under both methods. The report concludes that the ABC method is more effective for aligning costs and profits, leading to improved decision-making and overall business development. The report includes an introduction, discussion, conclusion, and a reference list to support the analysis.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.