Management Accounting Report for R.L. Maynard Ltd.

VerifiedAdded on 2020/01/16

|21

|5435

|7391

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices at R.L. Maynard Ltd., a construction and property development company. It covers various management accounting systems such as traditional cost accounting, throughput accounting, lean accounting, and transfer pricing. The report also discusses different methods for management accounting reporting, including cost reports, budgets, and performance reports. Furthermore, it includes the preparation of income statements using marginal and absorption costing methods, highlighting the differences between the two. The report also evaluates different planning tools like capital budgeting, budgeting, and ratio analysis, discussing their advantages and disadvantages. Finally, it compares how the organization can manage its results and performances using different management accounting systems, concluding with an overview of the company's management accounting practices and their impact on decision-making.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management Accounting and essential requirements of different types of management

accounting systems......................................................................................................................1

M1 Benefits of management accounting systems.......................................................................3

P2 Different methods used for management accounting reporting.............................................4

D1 Integration of management accounting systems and reporting with organisational

processes.....................................................................................................................................4

TASK 2............................................................................................................................................4

P3 Preparation of income statements..........................................................................................4

M 2..............................................................................................................................................7

D 2...............................................................................................................................................7

TASK 3............................................................................................................................................7

P3 Advantages and disadvantages of different types of planning tools......................................7

P5 Compare how organisation can manage their results and performances with accounting

management system..................................................................................................................13

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management Accounting and essential requirements of different types of management

accounting systems......................................................................................................................1

M1 Benefits of management accounting systems.......................................................................3

P2 Different methods used for management accounting reporting.............................................4

D1 Integration of management accounting systems and reporting with organisational

processes.....................................................................................................................................4

TASK 2............................................................................................................................................4

P3 Preparation of income statements..........................................................................................4

M 2..............................................................................................................................................7

D 2...............................................................................................................................................7

TASK 3............................................................................................................................................7

P3 Advantages and disadvantages of different types of planning tools......................................7

P5 Compare how organisation can manage their results and performances with accounting

management system..................................................................................................................13

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

The process of analysing, interpretation and presentation of information related to

accounting is known as management accounting. This information is gathered using costing and

accounting information and it helps the management in making decision for short term period or

day-to-day operations. The management accounts and reports are very useful for the managers in

decision-making, formulation of various policies and regulation of commercial activities of

business (Cullen and Whelan, 2011). This report provides several relevant information including

amount of cash available, position of accounts receivable and payable, number of orders in hand,

outstanding debt, inventory, revenue generated from sales, raw materials and variance charts,

statistics, trend charts and like. The process of management accounting involves measurement of

performance, assessment of risk, preparation and presentation of financial statements to the

management. The present assignment provides a detailed understanding of management

accounting and different methods used for its reporting in R. L. Maynard Ltd. The company is

basically engaged in the business of construction and development of property. Further, the

report focuses on preparation of income statements on the basis of marginal and absorption

costing method and the reason of difference between the two methods. Lastly, the study focuses

on the use of management accounting system by R. L. Maynard for responding to financial

problems.

TASK 1

P1 Management Accounting and essential requirements of different types of management

accounting systems

The process of analysing, interpretation and presentation of information related to

accounting is known as management accounting. This information is gathered using costing and

accounting information and it helps the management in making decision for short term period or

day-to-day operations. The process of management accounting involves measurement of

performance, assessment of risk, preparation and presentation of financial statements to the

management (ter Bogt and van Helden, 2012). It encapsulates the three major aspects of a

business – management, accounts and finance. The management report projects all kinds of

information in relation to business strategies, financial status of the organisation which assists the

management of R. L. Maynard Ltd. to ascertain performance of business and make corrective

decisions wherever needed.

1

The process of analysing, interpretation and presentation of information related to

accounting is known as management accounting. This information is gathered using costing and

accounting information and it helps the management in making decision for short term period or

day-to-day operations. The management accounts and reports are very useful for the managers in

decision-making, formulation of various policies and regulation of commercial activities of

business (Cullen and Whelan, 2011). This report provides several relevant information including

amount of cash available, position of accounts receivable and payable, number of orders in hand,

outstanding debt, inventory, revenue generated from sales, raw materials and variance charts,

statistics, trend charts and like. The process of management accounting involves measurement of

performance, assessment of risk, preparation and presentation of financial statements to the

management. The present assignment provides a detailed understanding of management

accounting and different methods used for its reporting in R. L. Maynard Ltd. The company is

basically engaged in the business of construction and development of property. Further, the

report focuses on preparation of income statements on the basis of marginal and absorption

costing method and the reason of difference between the two methods. Lastly, the study focuses

on the use of management accounting system by R. L. Maynard for responding to financial

problems.

TASK 1

P1 Management Accounting and essential requirements of different types of management

accounting systems

The process of analysing, interpretation and presentation of information related to

accounting is known as management accounting. This information is gathered using costing and

accounting information and it helps the management in making decision for short term period or

day-to-day operations. The process of management accounting involves measurement of

performance, assessment of risk, preparation and presentation of financial statements to the

management (ter Bogt and van Helden, 2012). It encapsulates the three major aspects of a

business – management, accounts and finance. The management report projects all kinds of

information in relation to business strategies, financial status of the organisation which assists the

management of R. L. Maynard Ltd. to ascertain performance of business and make corrective

decisions wherever needed.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

There are different types of management accounting systems that can be used by an

organisation for collection and presentation of financial and statistical information. The cited

organisation uses different systems of management accounting that helps it to carry out the

activities of construction and development effectively (Burritt and Schaltegger, 2010). It takes

into consideration several factors such as cost of production related to the goods produced and

services provided by R. L. Maynard Ltd. The management accounting systems used by the cited

organisation are described below :

Traditional cost accounting system : This method is also known as conventional

method of accounting. All direct and indirect costs are considered in traditional

accounting system and it highlights the cause and effect relationship. The costs incurred

in the production are allocated to the product produced and indirect costs are assigned to

the unit of production which are incurred in the production process. The basis of this

accounting system is volume of units of production, overheads related to production and

direct labour overheads (Cadez and Guilding, 2012). As per traditional costing, average

overhead rate is the basis of allocation of costs of a product. All the indirect expenditures

are pooled together and assigned equally on the basis of an appropriate cost driver which

may be direct labour hours, machine hours and direct material hours.

Throughput accounting : Throughput can be defined as the quantity of product or raw

material which is passed through a process or system. Throughput accounting in

management accounting system is mainly determined as a costing activity. The main

reason behind this is that the focus is on determination of constraints which arises during

manufacturing of units. These constraints may be in relation to labour turnover, raw

materials, wastage in capacity of plant etc. Basically, this method focuses on elimination

of all such constraints and insists more throughputs in order to ensure that the quantity

and quality of production is enhanced. In throughput costing, only direct materials are

allocated to the costs of inventory while all other manufacturing costs including variable

factory overheads and direct labour are treated as period costs (Englund and Gerdin,

2011). Selling and distribution overheads are also charged as period costs under this

method. This method ensures that costings are minimised for each units produced. It

enables in effective and efficient production while working in line with job and process

costing.

2

organisation for collection and presentation of financial and statistical information. The cited

organisation uses different systems of management accounting that helps it to carry out the

activities of construction and development effectively (Burritt and Schaltegger, 2010). It takes

into consideration several factors such as cost of production related to the goods produced and

services provided by R. L. Maynard Ltd. The management accounting systems used by the cited

organisation are described below :

Traditional cost accounting system : This method is also known as conventional

method of accounting. All direct and indirect costs are considered in traditional

accounting system and it highlights the cause and effect relationship. The costs incurred

in the production are allocated to the product produced and indirect costs are assigned to

the unit of production which are incurred in the production process. The basis of this

accounting system is volume of units of production, overheads related to production and

direct labour overheads (Cadez and Guilding, 2012). As per traditional costing, average

overhead rate is the basis of allocation of costs of a product. All the indirect expenditures

are pooled together and assigned equally on the basis of an appropriate cost driver which

may be direct labour hours, machine hours and direct material hours.

Throughput accounting : Throughput can be defined as the quantity of product or raw

material which is passed through a process or system. Throughput accounting in

management accounting system is mainly determined as a costing activity. The main

reason behind this is that the focus is on determination of constraints which arises during

manufacturing of units. These constraints may be in relation to labour turnover, raw

materials, wastage in capacity of plant etc. Basically, this method focuses on elimination

of all such constraints and insists more throughputs in order to ensure that the quantity

and quality of production is enhanced. In throughput costing, only direct materials are

allocated to the costs of inventory while all other manufacturing costs including variable

factory overheads and direct labour are treated as period costs (Englund and Gerdin,

2011). Selling and distribution overheads are also charged as period costs under this

method. This method ensures that costings are minimised for each units produced. It

enables in effective and efficient production while working in line with job and process

costing.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Lean accounting : It is a new concept in the field of management accounting which

differs from other accounting systems. Under conventional method of costing, the focus

is mainly on the allocation of costs that are incurred in the process of production but lean

accounting focuses on reducing of costs by maintaining control over the wastages which

are caused in the production process. Various tactical methods are combined under this

technique which emphasizes on elimination of non value added activities (wastes) and

enables R. L. Maynard Ltd. to offer quality products on time. It involves value streaming

assessment, measurement of profits and decision-making by the assigned officers

(Morales and Lambert, 2013). Any excess costs are cut down with the help of

information provided by above mentioned categories. The main benefits of lean

accounting are – increase in revenue generated through sales due to reduction of

wastages, enhancing the capacity of plants as reducing the capacity utilised in the

generation of waste materials, cost step down helps in saving money etc.

Transfer pricing : Transfer pricing is generated when the goods are transferred from one

department to other or from one process to other or from holding company to its

subsidiary. Whenever the goods are transferred or shifted from one place to another, it

leads to generation of some extra costs due to such transfer.

M1 Benefits of management accounting systems

Traditional cost accounting system : R.L. Maynard Ltd. uses this method as it

takes into account cause and effect relationship and it enables managers to make

appropriate decisions as all direct and indirect costs are considered.

Throughput accounting : This method ensures that the constraints of the cited

firm are minimised for each units produced (Cullen and Whelan, 2011). It enables

in effective and efficient production while working in line with job and process

costing.

Lean accounting : The main benefits of lean accounting for R.L. Maynard Ltd.

are – increase in revenue generated through sales due to reduction of wastages,

enhancing the capacity of plants as reducing the capacity utilised in the generation

of waste materials, cost step down helps in saving money etc.

3

differs from other accounting systems. Under conventional method of costing, the focus

is mainly on the allocation of costs that are incurred in the process of production but lean

accounting focuses on reducing of costs by maintaining control over the wastages which

are caused in the production process. Various tactical methods are combined under this

technique which emphasizes on elimination of non value added activities (wastes) and

enables R. L. Maynard Ltd. to offer quality products on time. It involves value streaming

assessment, measurement of profits and decision-making by the assigned officers

(Morales and Lambert, 2013). Any excess costs are cut down with the help of

information provided by above mentioned categories. The main benefits of lean

accounting are – increase in revenue generated through sales due to reduction of

wastages, enhancing the capacity of plants as reducing the capacity utilised in the

generation of waste materials, cost step down helps in saving money etc.

Transfer pricing : Transfer pricing is generated when the goods are transferred from one

department to other or from one process to other or from holding company to its

subsidiary. Whenever the goods are transferred or shifted from one place to another, it

leads to generation of some extra costs due to such transfer.

M1 Benefits of management accounting systems

Traditional cost accounting system : R.L. Maynard Ltd. uses this method as it

takes into account cause and effect relationship and it enables managers to make

appropriate decisions as all direct and indirect costs are considered.

Throughput accounting : This method ensures that the constraints of the cited

firm are minimised for each units produced (Cullen and Whelan, 2011). It enables

in effective and efficient production while working in line with job and process

costing.

Lean accounting : The main benefits of lean accounting for R.L. Maynard Ltd.

are – increase in revenue generated through sales due to reduction of wastages,

enhancing the capacity of plants as reducing the capacity utilised in the generation

of waste materials, cost step down helps in saving money etc.

3

Transfer pricing : Transfer pricing includes price of shifting and opportunity price

which includes the amount that is borne by R. L. Maynard Ltd. in outsourcing of

goods and services outside the organisation.

P2 Different methods used for management accounting reporting

Management accounting is the process of preparation of management reports and

accounts that assists the managers in providing accurate and timely information regarding

financial status and strategies of business which help them in decision-making. R. L. Maynard

Ltd. several methods for management accounting reporting which are explained here under :

Cost reports : The procedure of providing information related to the costs to the

managers that enables the management in controlling the future costs is known as cost

accounting (Burritt and Schaltegger, 2010). The cost is computed on the basis of costs of

raw materials, labour, overheads and any other additional costs. To arrive at cost per unit,

the total costs incurred in the production is divided by the number of units produced. Cost

reports summarizes all the above information and assist managers in ascertaining the unit

cost of manufactured products and provide internal report system.

Budget : Budgets are prepared as an internal part that enables the managers to compare

the actual results of an organisation with the estimated ones and measure the performance

level over a specified period.

Performance reports : The performance report summarizes the differences projected in

the budgets and help managers in preparation of new budgets.

D1 Integration of management accounting systems and reporting with organisational processes

Management accounting systems and management accounting reporting are closely inter

linked and dependent on each other (Malmi, 2010). The preparation of management reports is

not possible without the systems and the system would lose its utility if the timely and accurate

reports are not provided to the managers for decision-making. Thus, it is imperative to integrate

the management accounting system and reporting with the operations of R.L. Maynard Ltd. to

ensure that the organisational goals are achieved.

TASK 2

P3 Preparation of income statements

Table: 1 Income statement for marginal costing

4

which includes the amount that is borne by R. L. Maynard Ltd. in outsourcing of

goods and services outside the organisation.

P2 Different methods used for management accounting reporting

Management accounting is the process of preparation of management reports and

accounts that assists the managers in providing accurate and timely information regarding

financial status and strategies of business which help them in decision-making. R. L. Maynard

Ltd. several methods for management accounting reporting which are explained here under :

Cost reports : The procedure of providing information related to the costs to the

managers that enables the management in controlling the future costs is known as cost

accounting (Burritt and Schaltegger, 2010). The cost is computed on the basis of costs of

raw materials, labour, overheads and any other additional costs. To arrive at cost per unit,

the total costs incurred in the production is divided by the number of units produced. Cost

reports summarizes all the above information and assist managers in ascertaining the unit

cost of manufactured products and provide internal report system.

Budget : Budgets are prepared as an internal part that enables the managers to compare

the actual results of an organisation with the estimated ones and measure the performance

level over a specified period.

Performance reports : The performance report summarizes the differences projected in

the budgets and help managers in preparation of new budgets.

D1 Integration of management accounting systems and reporting with organisational processes

Management accounting systems and management accounting reporting are closely inter

linked and dependent on each other (Malmi, 2010). The preparation of management reports is

not possible without the systems and the system would lose its utility if the timely and accurate

reports are not provided to the managers for decision-making. Thus, it is imperative to integrate

the management accounting system and reporting with the operations of R.L. Maynard Ltd. to

ensure that the organisational goals are achieved.

TASK 2

P3 Preparation of income statements

Table: 1 Income statement for marginal costing

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

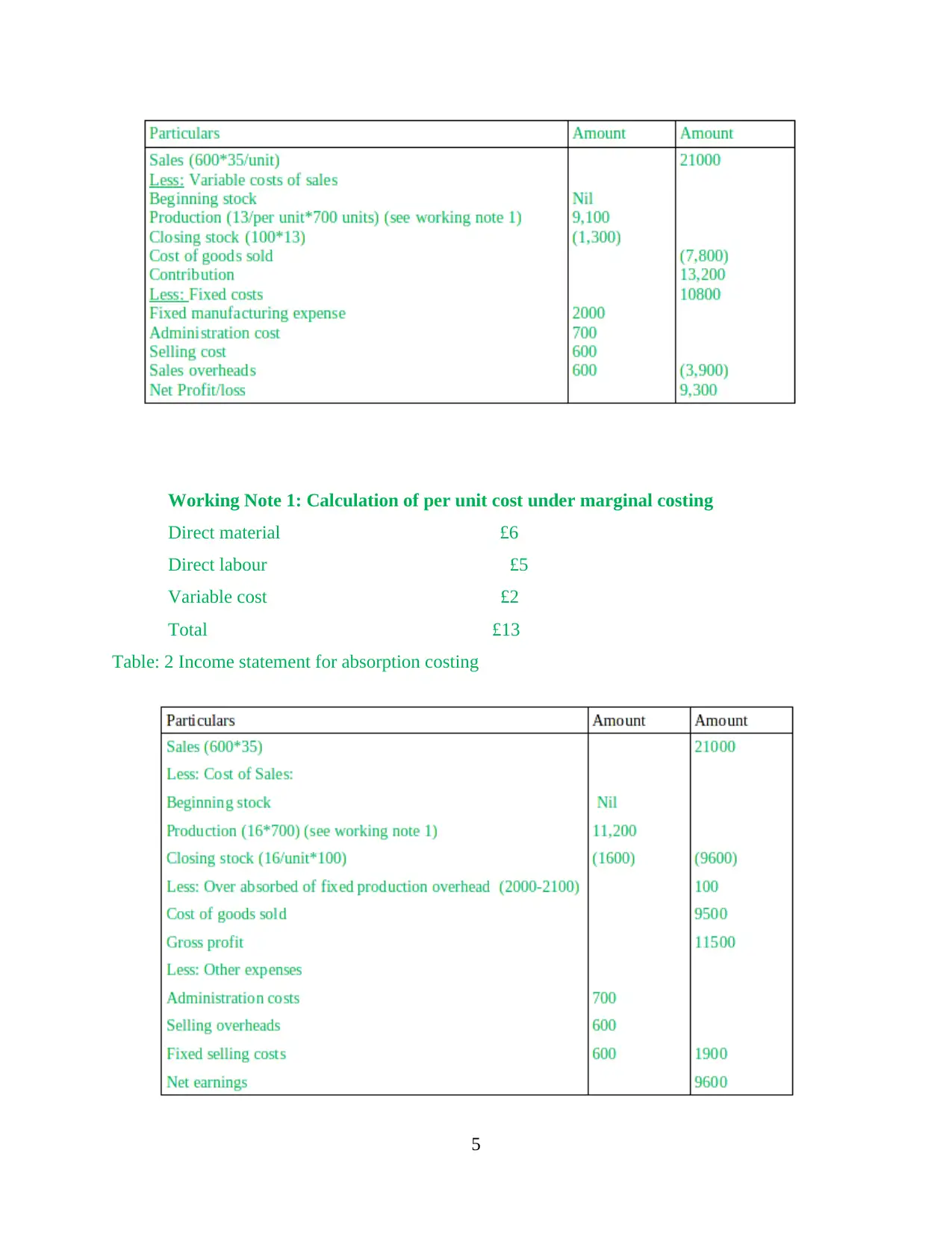

Working Note 1: Calculation of per unit cost under marginal costing

Direct material £6

Direct labour £5

Variable cost £2

Total £13

Table: 2 Income statement for absorption costing

5

Direct material £6

Direct labour £5

Variable cost £2

Total £13

Table: 2 Income statement for absorption costing

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Working Note 1: Calculation of per unit cost under absorption costing

Direct material £6

Direct labor £5

Variable cost £2

Fixed cost £3

Total production cost/unit £16

It can be interpreted from the above income statements that the company is generating

better profits at the end of the month (Cadez and Guilding, 2012). The net profit as per

absorption costing method is £9600 which is less than the profit computed as per marginal

costing which comes to £9300. The reason of difference between these two amounts is

absorption costing method takes into account both fixed cost and variable cost unlike marginal

costing method which considers variable costs only.

R.L. Maynard Ltd. uses absorption costing method because it provides clear and

appropriate financial performance of the organisation as it takes into all types of costs.

Difference between marginal and absorption costing method

Absorption costing Marginal costing

For computation of net profits, all costs i.e.

fixed and variable are considered.

This method considers direct costs and variable

cost only.

Both fixed and variable costs are considered as

period costs.

Variable cost is a product cost and fixed cost is

a period cost (Richardson, 2012).

The stock at the year end is carried forward to

the next year as it is valued as total production

cost at the year end.

Stock is not carried forward in the next year as

it considered as total variable expense of

production cost.

M 2

In order to perform effective functions and operations, there are various elements which

need to be taken at workplace. In this aspect, R. L. Maynard Ltd. can use financial statements'

analysis and cost accounting. It will assist to make profitability and effective results at workplace

(Villalobos, Dulce and Almero-Encio, 2016). The business has aim to enhance their profits so

6

Direct material £6

Direct labor £5

Variable cost £2

Fixed cost £3

Total production cost/unit £16

It can be interpreted from the above income statements that the company is generating

better profits at the end of the month (Cadez and Guilding, 2012). The net profit as per

absorption costing method is £9600 which is less than the profit computed as per marginal

costing which comes to £9300. The reason of difference between these two amounts is

absorption costing method takes into account both fixed cost and variable cost unlike marginal

costing method which considers variable costs only.

R.L. Maynard Ltd. uses absorption costing method because it provides clear and

appropriate financial performance of the organisation as it takes into all types of costs.

Difference between marginal and absorption costing method

Absorption costing Marginal costing

For computation of net profits, all costs i.e.

fixed and variable are considered.

This method considers direct costs and variable

cost only.

Both fixed and variable costs are considered as

period costs.

Variable cost is a product cost and fixed cost is

a period cost (Richardson, 2012).

The stock at the year end is carried forward to

the next year as it is valued as total production

cost at the year end.

Stock is not carried forward in the next year as

it considered as total variable expense of

production cost.

M 2

In order to perform effective functions and operations, there are various elements which

need to be taken at workplace. In this aspect, R. L. Maynard Ltd. can use financial statements'

analysis and cost accounting. It will assist to make profitability and effective results at workplace

(Villalobos, Dulce and Almero-Encio, 2016). The business has aim to enhance their profits so

6

that financial planning is very good element. Further, cost accounting is the important element

which provide effective cost structure which assist to manage business results and performances.

D 2

In respect to perform effective results and performances, R. L. Maynard Ltd. has

responsibility to make proper statements. In this way, they have to analysis different range of

accounts balances which can be included within the report (A. Hammad, Jusoh and Ghozali,

2013). Thus, it can be specify type of account in grouping of report. It is major duty of the

chosen business to get right balance between results and performances which assist to create

profits and revenue at workplace.

TASK 3

P3 Advantages and disadvantages of different types of planning tools

In order to perform functions and operations, there are different types of tools and

techniques are available within the market. It enables to R. L. Maynard Ltd. to control disposals

at their workplace. In respect to this, following are such techniques at workplace which can be

used to generate high revenue and profits:

Capital budgeting techniques

This is planning tool that can be used to make effective performance and investment

decisions. It will assist to create high return at R. L. Maynard Ltd. This is because, manager of

the chosen organisation can maintains high position at workplace through choosing the best

option among various alternatives (Pondeville, Swaen and De Rongé, 2013). There are various

projects in which they have to select the effective one which assist to gain high profits and

revenue. In this way, different elements are considers at workplace such as Payback, NPV, Post

payback, IRR and many more.

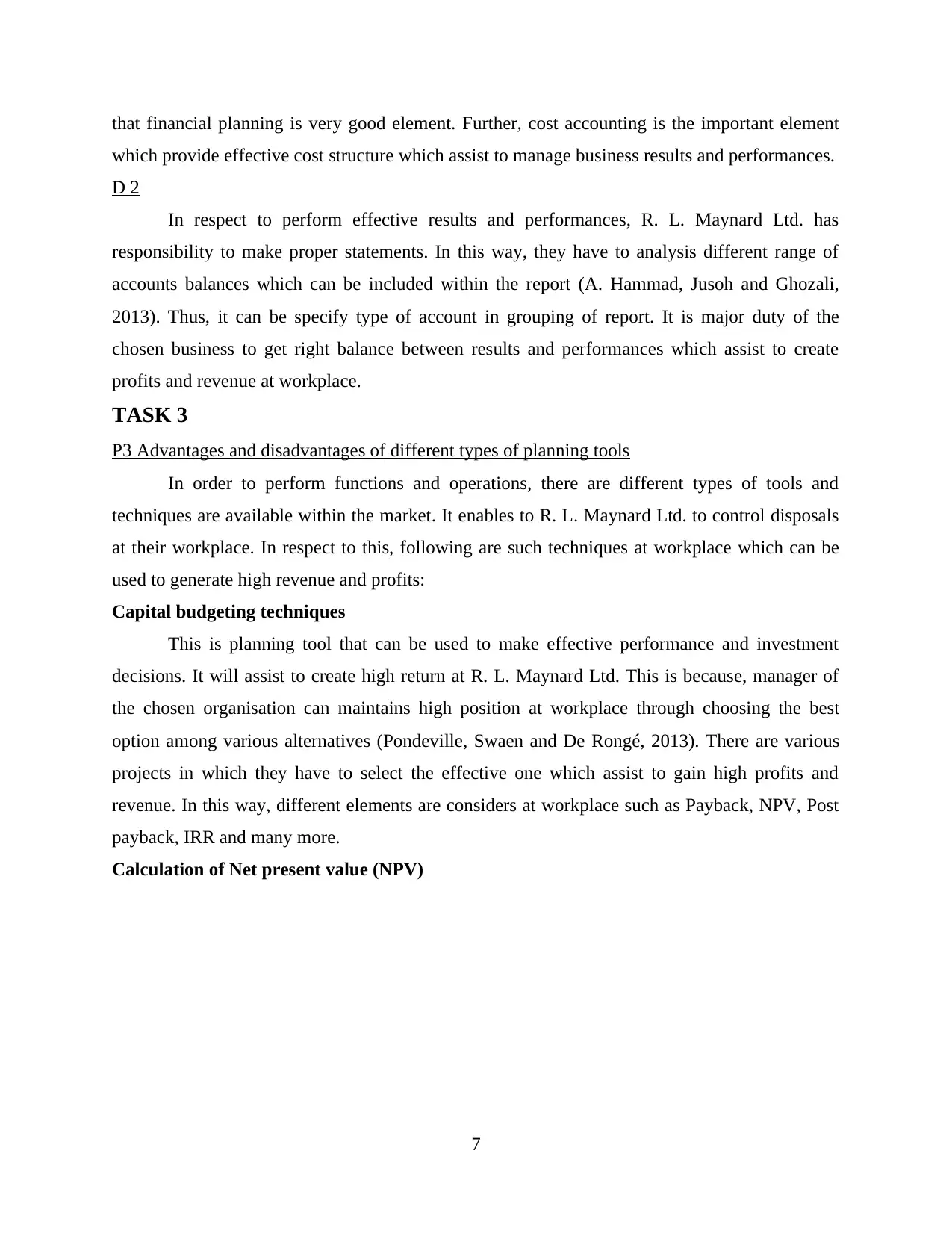

Calculation of Net present value (NPV)

7

which provide effective cost structure which assist to manage business results and performances.

D 2

In respect to perform effective results and performances, R. L. Maynard Ltd. has

responsibility to make proper statements. In this way, they have to analysis different range of

accounts balances which can be included within the report (A. Hammad, Jusoh and Ghozali,

2013). Thus, it can be specify type of account in grouping of report. It is major duty of the

chosen business to get right balance between results and performances which assist to create

profits and revenue at workplace.

TASK 3

P3 Advantages and disadvantages of different types of planning tools

In order to perform functions and operations, there are different types of tools and

techniques are available within the market. It enables to R. L. Maynard Ltd. to control disposals

at their workplace. In respect to this, following are such techniques at workplace which can be

used to generate high revenue and profits:

Capital budgeting techniques

This is planning tool that can be used to make effective performance and investment

decisions. It will assist to create high return at R. L. Maynard Ltd. This is because, manager of

the chosen organisation can maintains high position at workplace through choosing the best

option among various alternatives (Pondeville, Swaen and De Rongé, 2013). There are various

projects in which they have to select the effective one which assist to gain high profits and

revenue. In this way, different elements are considers at workplace such as Payback, NPV, Post

payback, IRR and many more.

Calculation of Net present value (NPV)

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Calculation of internal rate of return

As per the following statements, it can be articulated that investment in A project is more

beneficial instead of B. This is because, net present value and internal rate of return in A project

8

As per the following statements, it can be articulated that investment in A project is more

beneficial instead of B. This is because, net present value and internal rate of return in A project

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of R. L. Maynard Ltd. is high than B. There are various advantages and disadvantages of using

these techniques at workplace of chosen enterprises. They are as follows:

Advantages

Capital budgeting is helpful to R. L. Maynard Ltd. to invest money in those project which

gives more benefits. It gives high return with potential investment at chosen firm.

It is very effective tool which demonstrate to make decisions for select a particular

project (Villalobos, Dulce and Almero-Encio, 2016).

In addition to this, it also determines profitability within the different projects and

outcomes at workplace. It possesses short and simple calculations so that technique easily understand within the

business environment (A. Hammad, Jusoh and Ghozali, 2013).

Disadvantages

Other tools of capital budgeting such as payback period and many other take more time

to calculate. Thus, it is time consuming process.

For calculating, this tools, R. L. Maynard Ltd. requires skilled people at their workplace.

Wrong calculation of capital budgeting can affect to long term profitability of the chosen

firm. As results, it remains with high risk element at workplace (Villalobos, Dulce and

Almero-Encio, 2016).

Budget

It is also very important element which demonstrates to manage business financial

elements and accounts. Thus, the cited firm is able to manage ascertain financial and accounting

performances which assist to gain future response. It assists to make forecast for future to

generate high income and profits at workplace. In addition to this, R. L. Maynard Ltd. can make

sheet of performances of the business through they can operate effective functions and

operations (Pondeville, Swaen and De Rongé, 2013). It also includes different types of budget

such as cash state-owned, production statement and various other per forma. There are different

budget statement are take place as follows:

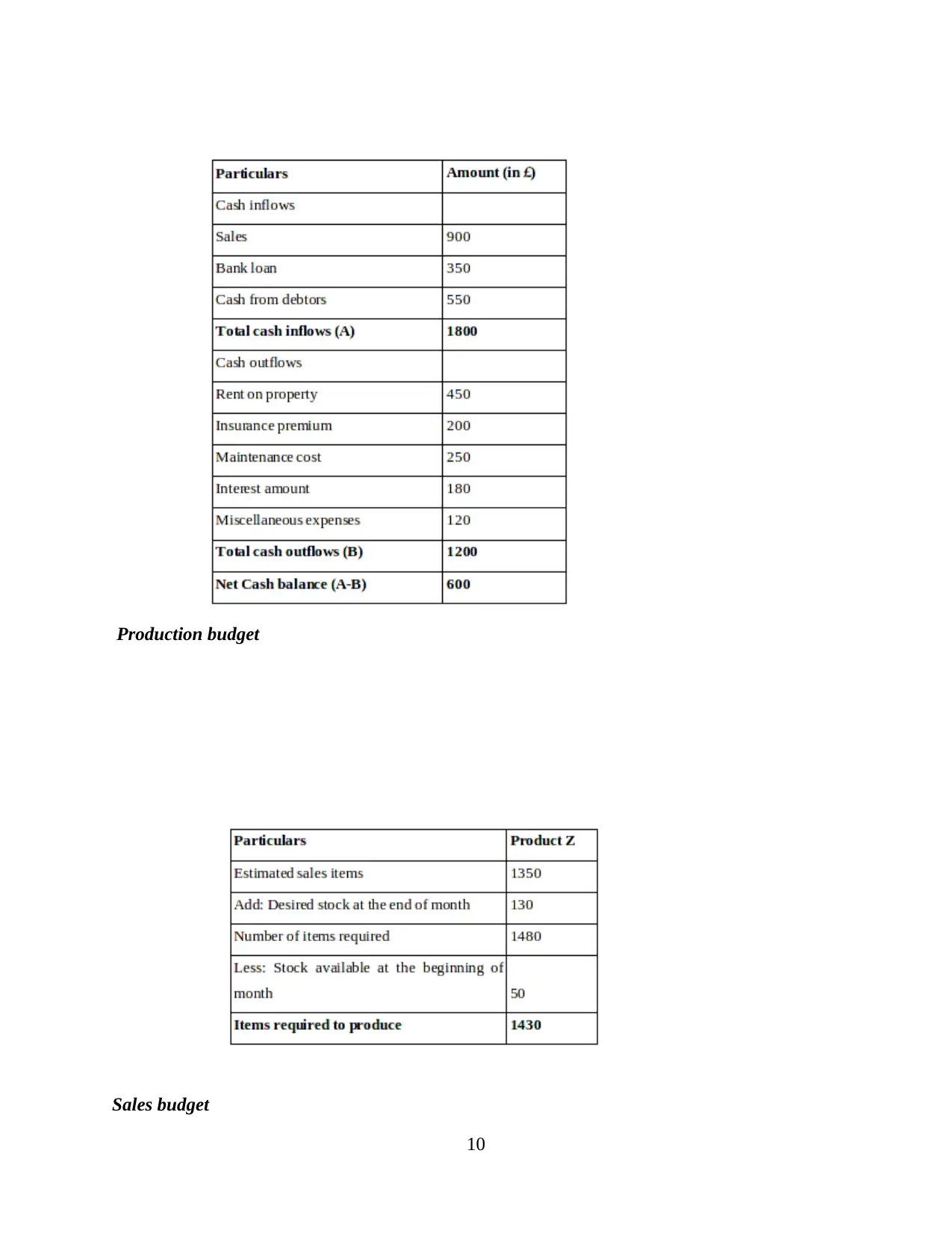

Cash budget

9

these techniques at workplace of chosen enterprises. They are as follows:

Advantages

Capital budgeting is helpful to R. L. Maynard Ltd. to invest money in those project which

gives more benefits. It gives high return with potential investment at chosen firm.

It is very effective tool which demonstrate to make decisions for select a particular

project (Villalobos, Dulce and Almero-Encio, 2016).

In addition to this, it also determines profitability within the different projects and

outcomes at workplace. It possesses short and simple calculations so that technique easily understand within the

business environment (A. Hammad, Jusoh and Ghozali, 2013).

Disadvantages

Other tools of capital budgeting such as payback period and many other take more time

to calculate. Thus, it is time consuming process.

For calculating, this tools, R. L. Maynard Ltd. requires skilled people at their workplace.

Wrong calculation of capital budgeting can affect to long term profitability of the chosen

firm. As results, it remains with high risk element at workplace (Villalobos, Dulce and

Almero-Encio, 2016).

Budget

It is also very important element which demonstrates to manage business financial

elements and accounts. Thus, the cited firm is able to manage ascertain financial and accounting

performances which assist to gain future response. It assists to make forecast for future to

generate high income and profits at workplace. In addition to this, R. L. Maynard Ltd. can make

sheet of performances of the business through they can operate effective functions and

operations (Pondeville, Swaen and De Rongé, 2013). It also includes different types of budget

such as cash state-owned, production statement and various other per forma. There are different

budget statement are take place as follows:

Cash budget

9

Production budget

Sales budget

10

Sales budget

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.