Comprehensive Management Accounting Report: SDK Jewellers Case Study

VerifiedAdded on 2020/10/22

|15

|5040

|85

Report

AI Summary

This report delves into the realm of management accounting, exploring its various facets through the lens of SDK Jewellers, a manufacturing company based in the UK. It commences with an introduction to management accounting, its significance in organizational decision-making, and its role in addressing future uncertainties. The report then dissects the management accounting system, differentiating between cost accounting, price optimization, inventory management, and job costing systems, and their respective benefits. A key section focuses on management accounting reporting, encompassing budget, account receivables, performance, and inventory reports. Furthermore, the report explores cost calculation techniques, planning tools, and budgetary control, alongside their advantages and disadvantages. The report also addresses the responses of the management accounting system to financial problems and their impact on organizational success. The report provides valuable insights into the practical application of management accounting principles within a real-world context, making it a useful resource for students and professionals alike. The report concludes with a discussion on the integration of management accounting and its reporting in driving organizational success.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting system and its types.......................................................................1

P2 Management accounting reporting and its types...................................................................3

M1 Benefits of management accounting system........................................................................4

D1 Integration of management accounting system and its reporting in organisational success. 5

TASK 2............................................................................................................................................5

P3 Calculation of cost using an appropriate techniques..............................................................5

M2 Various management accounting techniques.......................................................................7

D2 Data interpretation.................................................................................................................7

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different planning tools used for budgetary control........8

M3 Uses and applications of planning tools for preparing and forecasting budgets..................9

TASK 4............................................................................................................................................9

P5: Responses of management accounting system to deal with financial problems..................9

M4: Management accounting lead to sustainable success in responding to financial problems

...................................................................................................................................................11

D3: Planning tools respond appropriately to resolve financial problems.................................11

CONCLUSION..............................................................................................................................11

REFERENCES ...............................................................................................................................1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting system and its types.......................................................................1

P2 Management accounting reporting and its types...................................................................3

M1 Benefits of management accounting system........................................................................4

D1 Integration of management accounting system and its reporting in organisational success. 5

TASK 2............................................................................................................................................5

P3 Calculation of cost using an appropriate techniques..............................................................5

M2 Various management accounting techniques.......................................................................7

D2 Data interpretation.................................................................................................................7

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different planning tools used for budgetary control........8

M3 Uses and applications of planning tools for preparing and forecasting budgets..................9

TASK 4............................................................................................................................................9

P5: Responses of management accounting system to deal with financial problems..................9

M4: Management accounting lead to sustainable success in responding to financial problems

...................................................................................................................................................11

D3: Planning tools respond appropriately to resolve financial problems.................................11

CONCLUSION..............................................................................................................................11

REFERENCES ...............................................................................................................................1

INTRODUCTION

Management accounting is tool which is used by managers to determine organisational

goals and objectives. It helps to make financial and non financial decisions which is required to

deal with uncertainties that may occur in future. It is a process of recording business information

which is provided to the internal stakeholders of the company to gain their trust. In management

accounting various reports are generated to analyse the performance of the company. Its main

objective is to get the insider and actual information of the business so that weak areas are

identified and managers can plan for improvements in those areas (Abdelmoneim Mohamed and

Jones, 2014). SDK Jewellers is a manufacturing company and its headquarter is in UK.

This project report covers various topics such as management accounting system and its

reports, planning tools used in budgetary control, various costing techniques etc. Various

techniques to deal financial problem that an organisation have to face are also covered under this

report.

TASK 1

P1 Management accounting system and its types

Management accounting is the process examining financial data that facilitates the

strategic decision making process of managers. It helps to formulate policies that helps to lead

the organisation toward success. It direct the managers to perform various functions such as

planning, organising, controlling etc. Managers of SDK Jewellers use management accounting

system to determine customers needs and provide them such products that may fulfil their

demand. Stakeholders can get various information such as cash in the company, its total sales, its

account receivables and payables. The management of SDK Jewellers follow management

accounting system to maintain proper status of the company in the market. There are four types

of management accounting system, that are explained below:

Cost accounting system: It is used by various companies to determine the actual cost

which is involved in manufacturing process. It is very useful for manufacturing

companies because it can provide the detailed information of cost of different

departments. It helps the managers to control the cost of production (AlMaryani and

Sadik, 2012). Management of SDK Jewellers use this system to analyse the cost of each

segment of Jewellery. The managers analyse the production activities with the help of

1

Management accounting is tool which is used by managers to determine organisational

goals and objectives. It helps to make financial and non financial decisions which is required to

deal with uncertainties that may occur in future. It is a process of recording business information

which is provided to the internal stakeholders of the company to gain their trust. In management

accounting various reports are generated to analyse the performance of the company. Its main

objective is to get the insider and actual information of the business so that weak areas are

identified and managers can plan for improvements in those areas (Abdelmoneim Mohamed and

Jones, 2014). SDK Jewellers is a manufacturing company and its headquarter is in UK.

This project report covers various topics such as management accounting system and its

reports, planning tools used in budgetary control, various costing techniques etc. Various

techniques to deal financial problem that an organisation have to face are also covered under this

report.

TASK 1

P1 Management accounting system and its types

Management accounting is the process examining financial data that facilitates the

strategic decision making process of managers. It helps to formulate policies that helps to lead

the organisation toward success. It direct the managers to perform various functions such as

planning, organising, controlling etc. Managers of SDK Jewellers use management accounting

system to determine customers needs and provide them such products that may fulfil their

demand. Stakeholders can get various information such as cash in the company, its total sales, its

account receivables and payables. The management of SDK Jewellers follow management

accounting system to maintain proper status of the company in the market. There are four types

of management accounting system, that are explained below:

Cost accounting system: It is used by various companies to determine the actual cost

which is involved in manufacturing process. It is very useful for manufacturing

companies because it can provide the detailed information of cost of different

departments. It helps the managers to control the cost of production (AlMaryani and

Sadik, 2012). Management of SDK Jewellers use this system to analyse the cost of each

segment of Jewellery. The managers analyse the production activities with the help of

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

this method. It is very beneficial for the management department, as it can provide

transparent information of cost which is used to minimise cost.

Price optimisation system: It is mainly concerned with the pricing strategy of the

company. Managers use this system when they are looking for accurate price for their

products that can maximise profits as well as attract customers to fulfil their demand.

SDK Jewellers use this system while they want to analyse customers reaction toward

price changing strategy (Arjaliès and Mundy, 2013). The major objective of the managers

of SDK Jewellers, is to determine the best price for their products that will help to meet

their organisational goals and mission. It is very advantageous for the company because it

provides the ideas to set appropriate prices for the products.

Inventory management system: It is used to track the products in supply chain of the

company. It is mainly concerned with the information of inventory which is may be in

warehouse or transportation (Bennett, Schaltegger and Zvezdov, 2013). Management of

SDK Jewellers use inventory management system to determine the quantity of the

inventory within the company. It is very important for the organisations like SDK

Jewellers, because it helps the managers and owners to keep a track record of inventory

whether it is, inside or outside of the company. It is very beneficial for the managers

because it provide the information of inventory. There are three types of inventory

management system, LIFO, FIFO, AVCO. LIFO stands for Last in first out, it is a

method which is used to evaluate the most recently received units first. FIFO stands for

first in first out, it is a method which is used to evaluate the earlier received units first.

AVCO stands for Average cost method, in this method units are recorded on weighted

average basis to calculate the cost of the units.

Job costing system: It is concerned with the examination of cost which is involved in

the job that is performed by the company or its employees. It is mainly used when the

jobs are totally different from each other. Managers of SDK Jewellers use this system to

analyse cost of each task of the company. Job costing system helps the management of

SDK Jewellers to determine the manufacturing cost which in incurred in various jobs of

the organisation. Managers make decision to control the cost of the company if the cost is

comparatively higher then competitors (Bovens, Goodin and Schillemans, 2014). This

2

transparent information of cost which is used to minimise cost.

Price optimisation system: It is mainly concerned with the pricing strategy of the

company. Managers use this system when they are looking for accurate price for their

products that can maximise profits as well as attract customers to fulfil their demand.

SDK Jewellers use this system while they want to analyse customers reaction toward

price changing strategy (Arjaliès and Mundy, 2013). The major objective of the managers

of SDK Jewellers, is to determine the best price for their products that will help to meet

their organisational goals and mission. It is very advantageous for the company because it

provides the ideas to set appropriate prices for the products.

Inventory management system: It is used to track the products in supply chain of the

company. It is mainly concerned with the information of inventory which is may be in

warehouse or transportation (Bennett, Schaltegger and Zvezdov, 2013). Management of

SDK Jewellers use inventory management system to determine the quantity of the

inventory within the company. It is very important for the organisations like SDK

Jewellers, because it helps the managers and owners to keep a track record of inventory

whether it is, inside or outside of the company. It is very beneficial for the managers

because it provide the information of inventory. There are three types of inventory

management system, LIFO, FIFO, AVCO. LIFO stands for Last in first out, it is a

method which is used to evaluate the most recently received units first. FIFO stands for

first in first out, it is a method which is used to evaluate the earlier received units first.

AVCO stands for Average cost method, in this method units are recorded on weighted

average basis to calculate the cost of the units.

Job costing system: It is concerned with the examination of cost which is involved in

the job that is performed by the company or its employees. It is mainly used when the

jobs are totally different from each other. Managers of SDK Jewellers use this system to

analyse cost of each task of the company. Job costing system helps the management of

SDK Jewellers to determine the manufacturing cost which in incurred in various jobs of

the organisation. Managers make decision to control the cost of the company if the cost is

comparatively higher then competitors (Bovens, Goodin and Schillemans, 2014). This

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

reports is very important for the manufacturing companies because it helps to get the

exact information of cost involved in various jobs..

P2 Management accounting reporting and its types

Management accounting reporting system is a method of generating various management

reports that helps to analyse actual position and performance of the company. It provides various

information to the managers that helps them while decision making (Cardoni, 2012). It contain

information of budgets, owed amount by clients, performance of each employee and business,

inventory status, manufacturing process etc. These reports are prepared by the management

department of SDK Jewellers to make decisions, formulate strategies and policies, set

organisational as well as individuals goals that are based on above mentioned informations. It

facilitates the decision making process with the helps of various reports. Type of management

accounting reports are described below:

Budget reports: These reports are mainly concerned with the comparison of forecasted

budgets and actual performance of the company. It helps the managers to identify budget

for each department and control them accordingly. Financial data is recorded in budget

reports, which is analysed by managers of the company to identify fields where the cost

can be controlled (Carlsson-Wall, Kraus, and Lind, 2015). The management of SDK

Jewellers design budget reports to identify that how the organisation is performing in

market with available resources. The managers try to find out the reason behind the

variation in actual and budgeted figures. These reports are very important for the business

because it helps the management to form strategies according to the requirement of the

company..

Account receivables reports: These reports are mainly generated to analyse the owed

amount of clients. It is a tool that helps the managers to determine the actual receivables

of the company and to whom it relates (Fourie, M. L., Opperman, Scott and Kumar,

2015). Account receivables reports are formed by the managers of SDK Jewellers to get

the information of those customers who fails to pay their amount on due date of payment.

It helps to get detailed information of actual owed amount of various clients, hence it is

very important for every organisation. These reports are very important for the company

as well as its managers to determine the total receivables of the company.

3

exact information of cost involved in various jobs..

P2 Management accounting reporting and its types

Management accounting reporting system is a method of generating various management

reports that helps to analyse actual position and performance of the company. It provides various

information to the managers that helps them while decision making (Cardoni, 2012). It contain

information of budgets, owed amount by clients, performance of each employee and business,

inventory status, manufacturing process etc. These reports are prepared by the management

department of SDK Jewellers to make decisions, formulate strategies and policies, set

organisational as well as individuals goals that are based on above mentioned informations. It

facilitates the decision making process with the helps of various reports. Type of management

accounting reports are described below:

Budget reports: These reports are mainly concerned with the comparison of forecasted

budgets and actual performance of the company. It helps the managers to identify budget

for each department and control them accordingly. Financial data is recorded in budget

reports, which is analysed by managers of the company to identify fields where the cost

can be controlled (Carlsson-Wall, Kraus, and Lind, 2015). The management of SDK

Jewellers design budget reports to identify that how the organisation is performing in

market with available resources. The managers try to find out the reason behind the

variation in actual and budgeted figures. These reports are very important for the business

because it helps the management to form strategies according to the requirement of the

company..

Account receivables reports: These reports are mainly generated to analyse the owed

amount of clients. It is a tool that helps the managers to determine the actual receivables

of the company and to whom it relates (Fourie, M. L., Opperman, Scott and Kumar,

2015). Account receivables reports are formed by the managers of SDK Jewellers to get

the information of those customers who fails to pay their amount on due date of payment.

It helps to get detailed information of actual owed amount of various clients, hence it is

very important for every organisation. These reports are very important for the company

as well as its managers to determine the total receivables of the company.

3

Performance reports: It is generated to analyse the performance of company and

various individuals within the organisation. The main objective of these reports is to

determine the performance which helps to run business in effective way. It is very

important for every organisation to keep the idea to its business operations to ignore

future consequences (Hall, 2016). In SDK Jewellers performance reports are created to

analyse execution capability of business and its market image. It is a detailed document

that provides internal and confidential information of business operation and their

performances to the managers and stakeholders of the company. These reports are very

important for the business because it helps the managers to get the knowledge of

performance of each individual who is working in the organisation.

Inventory and manufacturing reports: Inventory reports consists information of

inventory of an organisation and manufacturing reports are concerned with the process

of product manufacturing. It provides detailed information related to the stock which is

kept by the company to produce products (Leitner, 2013). These reports are generated by

the management of SDK Jewellers to keep the actual information related to the material

which is used to make jewellery. It also help the managers to reduce the waste in

manufacturing process by keeping information of actual inventory. It is very important

for the companies like SDK Jewellers because they have little inventory whose value is

very high.

M1 Benefits of management accounting system

Management accounting system Benefits

Cost accounting system It is implemented to analyse and modify the

effectiveness of the company.

It is very important for the company as it helps the

managers in strategic decision making.

Price optimisation system It is used to record customers reaction toward price

changing strategy of the company.

This system is essential for organisations because it

helps to set appropriate prices for the products that

can help to generate profits for the company and

4

various individuals within the organisation. The main objective of these reports is to

determine the performance which helps to run business in effective way. It is very

important for every organisation to keep the idea to its business operations to ignore

future consequences (Hall, 2016). In SDK Jewellers performance reports are created to

analyse execution capability of business and its market image. It is a detailed document

that provides internal and confidential information of business operation and their

performances to the managers and stakeholders of the company. These reports are very

important for the business because it helps the managers to get the knowledge of

performance of each individual who is working in the organisation.

Inventory and manufacturing reports: Inventory reports consists information of

inventory of an organisation and manufacturing reports are concerned with the process

of product manufacturing. It provides detailed information related to the stock which is

kept by the company to produce products (Leitner, 2013). These reports are generated by

the management of SDK Jewellers to keep the actual information related to the material

which is used to make jewellery. It also help the managers to reduce the waste in

manufacturing process by keeping information of actual inventory. It is very important

for the companies like SDK Jewellers because they have little inventory whose value is

very high.

M1 Benefits of management accounting system

Management accounting system Benefits

Cost accounting system It is implemented to analyse and modify the

effectiveness of the company.

It is very important for the company as it helps the

managers in strategic decision making.

Price optimisation system It is used to record customers reaction toward price

changing strategy of the company.

This system is essential for organisations because it

helps to set appropriate prices for the products that

can help to generate profits for the company and

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

attract more customers.

Inventory management system It helps to gather actual information of inventory.

Helps to the managers by providing them idea, when

to order inventory for the business.

Job costing system Helps to improve productivity of the company.

It provides information of actual cost which is

involved in various jobs.

D1 Integration of management accounting system and its reporting in organisational success

Management accounting system and its reporting help the managers and stakeholder to

analyse performance and market image of the company. It contributes in organisational success

by preparing various reports that shows the actual and running condition of the company. It is

very important for the company to properly form management reports to achieve organisational

goals and to lead the organisation toward success. Managers of an organisation are concerned

with the improvements in various fields of the organisation to make the strategies successful that

are implemented by them. Account receivable reports helps the managers to determine the actual

receivables of the company from different clients which helps the managers to tighten the credit

policies. Performance reports help to analyse individual as well as organisational performance

which helps to improve efficiency of operations.

TASK 2

P3 Calculation of cost using an appropriate techniques

Cost: It is a monetary value of a product, it includes various expenses like material,

overheads, labour etc. It is an amount which is used to manufacture a particular unit. If a

company is willing to acquire more market share than it is suggested to the managers to set lower

cost for the product so that it will help to attract more and more customers for the company and

increase the market share (Schaltegger and Burritt, 2017).

SDK Jewellers is a company who deals in jewellery and a producer of different jewellery

items, it is mainly based in UK. If managers of the company want to maximise profits then they

should set lower costs as compare to their competitors. It will help the company to increase

profits and set a positive image in the mind of customers.

5

Inventory management system It helps to gather actual information of inventory.

Helps to the managers by providing them idea, when

to order inventory for the business.

Job costing system Helps to improve productivity of the company.

It provides information of actual cost which is

involved in various jobs.

D1 Integration of management accounting system and its reporting in organisational success

Management accounting system and its reporting help the managers and stakeholder to

analyse performance and market image of the company. It contributes in organisational success

by preparing various reports that shows the actual and running condition of the company. It is

very important for the company to properly form management reports to achieve organisational

goals and to lead the organisation toward success. Managers of an organisation are concerned

with the improvements in various fields of the organisation to make the strategies successful that

are implemented by them. Account receivable reports helps the managers to determine the actual

receivables of the company from different clients which helps the managers to tighten the credit

policies. Performance reports help to analyse individual as well as organisational performance

which helps to improve efficiency of operations.

TASK 2

P3 Calculation of cost using an appropriate techniques

Cost: It is a monetary value of a product, it includes various expenses like material,

overheads, labour etc. It is an amount which is used to manufacture a particular unit. If a

company is willing to acquire more market share than it is suggested to the managers to set lower

cost for the product so that it will help to attract more and more customers for the company and

increase the market share (Schaltegger and Burritt, 2017).

SDK Jewellers is a company who deals in jewellery and a producer of different jewellery

items, it is mainly based in UK. If managers of the company want to maximise profits then they

should set lower costs as compare to their competitors. It will help the company to increase

profits and set a positive image in the mind of customers.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Marginal costing: It is a costing technique which is used to analyse the increment or

decrement in cost because of extra production unit. The cost for additional unit of production is

known as marginal cost. These costs are variable costs that are related to labour and raw

material. In this technique the managers try to determine the actual cost of additional production

units (Shields, 2015).

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200 + 1200 + 1500 ) 5900

Net profit 17500

Absorption costing: It a costing method which is used by various companies to assure

that the cost involved in the production of various units are going to be absorbed from the sales

of same units. This methods is used by managers of SDK Jewellers to determine actual

manufacturing cost.

Calculation of net profit by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

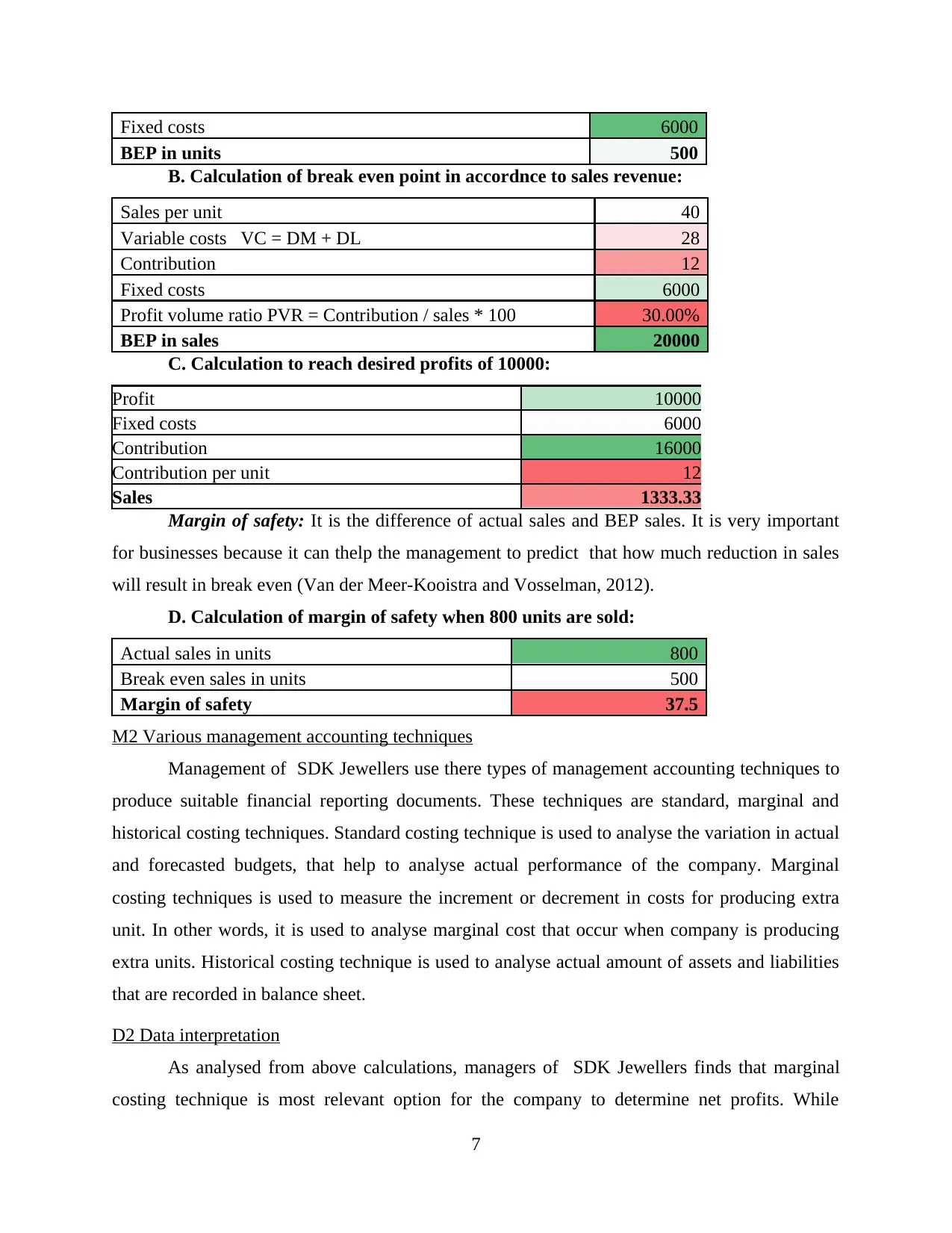

Break even analysis: It is a method which is used to analyse break even point where

company earns a profit which is equal to the cost incurred in the production of the units. In this

situation company is earing no profits and bearing no loss. It is calculated with the help of fixed

cost, variable cost and total sales of the company.

A Total number of products sold:

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

6

decrement in cost because of extra production unit. The cost for additional unit of production is

known as marginal cost. These costs are variable costs that are related to labour and raw

material. In this technique the managers try to determine the actual cost of additional production

units (Shields, 2015).

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200 + 1200 + 1500 ) 5900

Net profit 17500

Absorption costing: It a costing method which is used by various companies to assure

that the cost involved in the production of various units are going to be absorbed from the sales

of same units. This methods is used by managers of SDK Jewellers to determine actual

manufacturing cost.

Calculation of net profit by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break even analysis: It is a method which is used to analyse break even point where

company earns a profit which is equal to the cost incurred in the production of the units. In this

situation company is earing no profits and bearing no loss. It is calculated with the help of fixed

cost, variable cost and total sales of the company.

A Total number of products sold:

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

6

Fixed costs 6000

BEP in units 500

B. Calculation of break even point in accordnce to sales revenue:

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

C. Calculation to reach desired profits of 10000:

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: It is the difference of actual sales and BEP sales. It is very important

for businesses because it can thelp the management to predict that how much reduction in sales

will result in break even (Van der Meer-Kooistra and Vosselman, 2012).

D. Calculation of margin of safety when 800 units are sold:

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2 Various management accounting techniques

Management of SDK Jewellers use there types of management accounting techniques to

produce suitable financial reporting documents. These techniques are standard, marginal and

historical costing techniques. Standard costing technique is used to analyse the variation in actual

and forecasted budgets, that help to analyse actual performance of the company. Marginal

costing techniques is used to measure the increment or decrement in costs for producing extra

unit. In other words, it is used to analyse marginal cost that occur when company is producing

extra units. Historical costing technique is used to analyse actual amount of assets and liabilities

that are recorded in balance sheet.

D2 Data interpretation

As analysed from above calculations, managers of SDK Jewellers finds that marginal

costing technique is most relevant option for the company to determine net profits. While

7

BEP in units 500

B. Calculation of break even point in accordnce to sales revenue:

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

C. Calculation to reach desired profits of 10000:

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: It is the difference of actual sales and BEP sales. It is very important

for businesses because it can thelp the management to predict that how much reduction in sales

will result in break even (Van der Meer-Kooistra and Vosselman, 2012).

D. Calculation of margin of safety when 800 units are sold:

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2 Various management accounting techniques

Management of SDK Jewellers use there types of management accounting techniques to

produce suitable financial reporting documents. These techniques are standard, marginal and

historical costing techniques. Standard costing technique is used to analyse the variation in actual

and forecasted budgets, that help to analyse actual performance of the company. Marginal

costing techniques is used to measure the increment or decrement in costs for producing extra

unit. In other words, it is used to analyse marginal cost that occur when company is producing

extra units. Historical costing technique is used to analyse actual amount of assets and liabilities

that are recorded in balance sheet.

D2 Data interpretation

As analysed from above calculations, managers of SDK Jewellers finds that marginal

costing technique is most relevant option for the company to determine net profits. While

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

calculating net profits from marginal and absorption costing technique, it shows a difference of

£1825 in profits. Net profits from marginal costing technique are £17500 and from absorption

costing technique the profits are £15675. The break even sales of the company is £20000 when

the sales is 500 units. As SDK Jewellers is willing to earn a profit of £10000, to reach the profit

it has to sale 1333.33 units. If company is selling 800 units then the margin of safety will be 37.5

TASK 3

P4 Advantages and disadvantages of different planning tools used for budgetary control

Budgetary Control: It refers to how appropriately the managers utilize, monitor and

control the costs to run the business operations smoothly. Budgetary control help the managers to

compare actual figures and budgeted figures of the organsiation. There are various steps to

follow while preparing budgets of the company (an Helden and Uddin, 2016). Budgetary control

process involve setting objectives, measuring budget outcomes, preparing budget manuals and

forming budget commeetee. Managers of SDK Jewellers are liable to control the budgets of the

organisation because it helps to make plan and reserve funds for future risks or events that may

occur. Management of SDK Jewellers use three planning tools in budgetary control:

Forecasting tools: As its names describes that these tools are concerned with forecasting

process of the company. It helps the managers to forecast future expenses such as

promotional expenses and, reserve fund for those expenses so that it help to ignore major

crisis that might occur in future. It helps the management to predict future events that are

based on past events and current trends.

Advantages Disadvantages

It helps to forecast future expenses. It is totally based on past data, hence its is not

fully reliable.

It helps the managers to reserves funds for

future expanses.

It is not possible to forecast future accurately.

Contingency tools: These tools are mainly concerned with negative events that may

occur in future. It is used by managers of SDK Jewellers to determine any unfavourable

event that have posibility to happen. It helps the managers to pre plan for the events that

can affect the operational activities and execution process of the company.

8

£1825 in profits. Net profits from marginal costing technique are £17500 and from absorption

costing technique the profits are £15675. The break even sales of the company is £20000 when

the sales is 500 units. As SDK Jewellers is willing to earn a profit of £10000, to reach the profit

it has to sale 1333.33 units. If company is selling 800 units then the margin of safety will be 37.5

TASK 3

P4 Advantages and disadvantages of different planning tools used for budgetary control

Budgetary Control: It refers to how appropriately the managers utilize, monitor and

control the costs to run the business operations smoothly. Budgetary control help the managers to

compare actual figures and budgeted figures of the organsiation. There are various steps to

follow while preparing budgets of the company (an Helden and Uddin, 2016). Budgetary control

process involve setting objectives, measuring budget outcomes, preparing budget manuals and

forming budget commeetee. Managers of SDK Jewellers are liable to control the budgets of the

organisation because it helps to make plan and reserve funds for future risks or events that may

occur. Management of SDK Jewellers use three planning tools in budgetary control:

Forecasting tools: As its names describes that these tools are concerned with forecasting

process of the company. It helps the managers to forecast future expenses such as

promotional expenses and, reserve fund for those expenses so that it help to ignore major

crisis that might occur in future. It helps the management to predict future events that are

based on past events and current trends.

Advantages Disadvantages

It helps to forecast future expenses. It is totally based on past data, hence its is not

fully reliable.

It helps the managers to reserves funds for

future expanses.

It is not possible to forecast future accurately.

Contingency tools: These tools are mainly concerned with negative events that may

occur in future. It is used by managers of SDK Jewellers to determine any unfavourable

event that have posibility to happen. It helps the managers to pre plan for the events that

can affect the operational activities and execution process of the company.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages Disadvantages

Provides the idea of possible future events that

may affect the operations.

It is only useful at the time of contingency and

provide guidance to deal with the same.

It helps the managers to be ready to face

possible negative events in future.

The process of implementing these tools is

very complicated.

Scenario tools: This tool is concerned with the identification and evaluation of possible

future events and than make a professional framework to explore those events. The

managers of SDK Jewellers make assumptions on the basis of past and current data for

upcoming events that impact on business environment. It is used in SDK Jewellers to

identify specific set of consequences that might happen in future.

Advantages Disadvantages

It help the mangers to identify critical issue

that may affect the operations of the company.

It is not useful for the small size companies

like SDK Jewellers.

It facilitates long term planning and decision

making process.

It is very difficult to implement this tool

because the market trends change rapidly.

M3 Uses and applications of planning tools for preparing and forecasting budgets

The managers of SDK Jewellers use three planning tools, that are forecasting,

contingency and scenario tools. These tools help the managers to forecast future events and

consequences. Planning tools are used to determine favourable and unfavourable events of

future. It also help the managers to be ready to face any kind of uncertainty in future. These tools

help while preparing and forecasting budgets because, they provides valuable informations to the

managers that help them to make decision according to the situations.

TASK 4

P5: Responses of management accounting system to deal with financial problems

Financial problems are related to lack of funds in company's activities or operations.

Many organisation are facing several financial issues like high debt level, insufficiency of funds,

improper money management, insolvency etc. in its operations. SDK jewellers is a small scale

company and wish to expand in future. So, for expansion company needs more finance. It is also

9

Provides the idea of possible future events that

may affect the operations.

It is only useful at the time of contingency and

provide guidance to deal with the same.

It helps the managers to be ready to face

possible negative events in future.

The process of implementing these tools is

very complicated.

Scenario tools: This tool is concerned with the identification and evaluation of possible

future events and than make a professional framework to explore those events. The

managers of SDK Jewellers make assumptions on the basis of past and current data for

upcoming events that impact on business environment. It is used in SDK Jewellers to

identify specific set of consequences that might happen in future.

Advantages Disadvantages

It help the mangers to identify critical issue

that may affect the operations of the company.

It is not useful for the small size companies

like SDK Jewellers.

It facilitates long term planning and decision

making process.

It is very difficult to implement this tool

because the market trends change rapidly.

M3 Uses and applications of planning tools for preparing and forecasting budgets

The managers of SDK Jewellers use three planning tools, that are forecasting,

contingency and scenario tools. These tools help the managers to forecast future events and

consequences. Planning tools are used to determine favourable and unfavourable events of

future. It also help the managers to be ready to face any kind of uncertainty in future. These tools

help while preparing and forecasting budgets because, they provides valuable informations to the

managers that help them to make decision according to the situations.

TASK 4

P5: Responses of management accounting system to deal with financial problems

Financial problems are related to lack of funds in company's activities or operations.

Many organisation are facing several financial issues like high debt level, insufficiency of funds,

improper money management, insolvency etc. in its operations. SDK jewellers is a small scale

company and wish to expand in future. So, for expansion company needs more finance. It is also

9

suffering from financial issue like inadequacy of funds, large number of creditor and too much of

unnecessary expenses. These problems are discussed below in detail:

Large number of creditors: Continuous credit sales lead to more credit customers. SDK

jewellers offer credit option to buyers but not able to recover the due amount.

Inadequacy of funds: As company wants to expand but not have sufficient funds for

expansion. Therefore, they need finance in order to increase their capital.

Unnecessary expenses: Marketing manager of SDK jewellers spent unnecessary on

promotional activities. It amount of expenses are more then revenue that negatively

impact on company's income.

Company follow key performance indicator, benchmarking and financial governance techniques

to deal with it's financial problems. These tools are explained below:

KPI(Key performance indicator): Company's performance is examine and measure

under this tool within a specific time period which assist in decision-making. SDK jewellers

evaluate its production and financial performance which negatively influence its operations.

Company is facing financial problem related to unnecessary spending over expenditure. SDK

jewellers use types of key performance indicators for resolving this issue (Wouters, and

Kirchberger, 2015).

Leading KPI- In this tool organisation estimates future events and evaluate

changes at marketplace. SDK jewellers use leading indicator for identifying and

measuring unnecessary expense on promotion which are unrelated to present

period. Company control this expenditure and estimates related expense

accurately which assist in enhancing income.

Lagging KPI- In this tool company increase its jewellery sales in way to generate

revenues. SDK jewellers use lagging indicator for measuring its output in order to

achieve success.

Benchmarking: This approach help in comparing company's performance with other

organisation in similar industry. Many companies are using this technique in order to increase

productivity and performance. SDK jewellers follow benchmarking to compare its performance

with competitors and resolve issue related to customers. Company set credit standards as its

successful competitor is using and recover due amount from creditor (What is Benchmarking,

2018).

10

unnecessary expenses. These problems are discussed below in detail:

Large number of creditors: Continuous credit sales lead to more credit customers. SDK

jewellers offer credit option to buyers but not able to recover the due amount.

Inadequacy of funds: As company wants to expand but not have sufficient funds for

expansion. Therefore, they need finance in order to increase their capital.

Unnecessary expenses: Marketing manager of SDK jewellers spent unnecessary on

promotional activities. It amount of expenses are more then revenue that negatively

impact on company's income.

Company follow key performance indicator, benchmarking and financial governance techniques

to deal with it's financial problems. These tools are explained below:

KPI(Key performance indicator): Company's performance is examine and measure

under this tool within a specific time period which assist in decision-making. SDK jewellers

evaluate its production and financial performance which negatively influence its operations.

Company is facing financial problem related to unnecessary spending over expenditure. SDK

jewellers use types of key performance indicators for resolving this issue (Wouters, and

Kirchberger, 2015).

Leading KPI- In this tool organisation estimates future events and evaluate

changes at marketplace. SDK jewellers use leading indicator for identifying and

measuring unnecessary expense on promotion which are unrelated to present

period. Company control this expenditure and estimates related expense

accurately which assist in enhancing income.

Lagging KPI- In this tool company increase its jewellery sales in way to generate

revenues. SDK jewellers use lagging indicator for measuring its output in order to

achieve success.

Benchmarking: This approach help in comparing company's performance with other

organisation in similar industry. Many companies are using this technique in order to increase

productivity and performance. SDK jewellers follow benchmarking to compare its performance

with competitors and resolve issue related to customers. Company set credit standards as its

successful competitor is using and recover due amount from creditor (What is Benchmarking,

2018).

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.