Management Accounting Report: Analysis for Smart Looks Ltd

VerifiedAdded on 2020/02/14

|18

|3165

|106

Report

AI Summary

This management accounting report examines Smart Looks Ltd, a UK-based clothing retailer, and applies various management accounting tools. The report begins with cost classifications (fixed, variable, semi-variable, direct, indirect, product, period, controllable, sunk, and opportunity costs) and then calculates total and unit costs, analyzing the relationship between production volume and cost. Inventory valuation methods (FIFO, LIFO, and average cost) are calculated. The report also provides a cost of goods sold report, suggests critical factors and performance indicators, and explores cost reduction and value enhancement strategies. Task 2 focuses on budgeting, including sales, production, raw materials, labor, overhead, and cash budgets. Finally, the report considers marginal costing techniques to determine selling prices and compares budgeted and actual profits. Overall, the report provides a comprehensive analysis of Smart Looks Ltd's financial performance and offers recommendations for improvement.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................5

TASK 1............................................................................................................................................5

Q1...........................................................................................................................................5

a) Classify the costs into Fixed, Variable and Semi-variable cost.........................................5

b) Explain other ways of classifying cost...............................................................................5

Q2...........................................................................................................................................7

a) Calculate total and unit costs.............................................................................................7

b) Analyze the cost data.........................................................................................................7

Q3. Calculation of inventory..................................................................................................8

1.FIFO Method ......................................................................................................................8

2.LIFO Method.......................................................................................................................8

3.Average Cost Method..........................................................................................................9

Q4. Prepare report of cost of goods sold................................................................................9

Q5.........................................................................................................................................10

a) Suggest 2 critical factors and performance indicators .....................................................10

B (1) How costs can be reduced...........................................................................................10

B (2) How value and quality can be enhanced.....................................................................11

TASK 2..........................................................................................................................................11

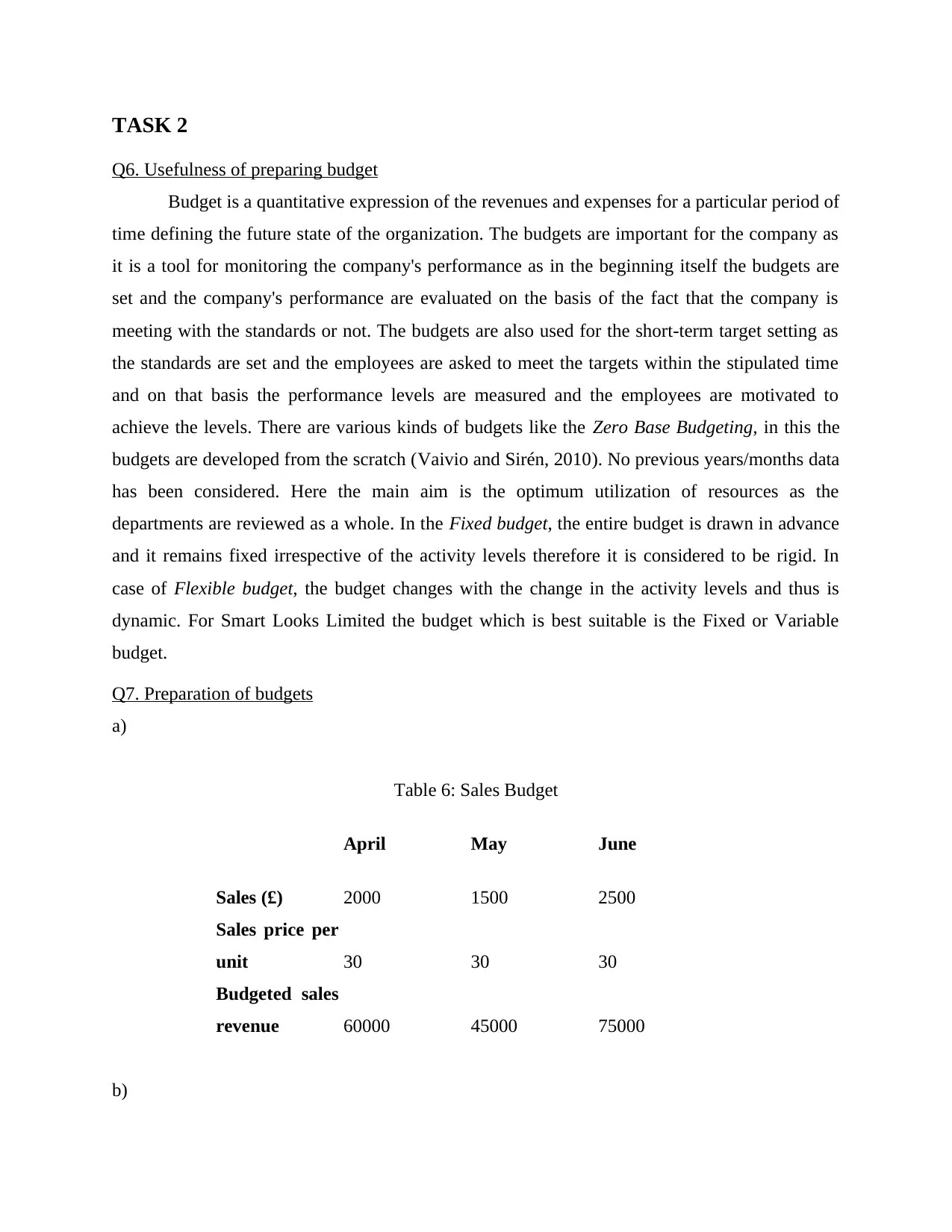

Q6. Usefulness of preparing budget.....................................................................................11

Q7. Preparation of budgets...................................................................................................12

Q8. Preparation of cash budget............................................................................................13

TASK 3..........................................................................................................................................14

Q9) 4.2 Comparison of budgeted and actual profit for Smart Looks Ltd............................14

Computation of selling price by considering the marginal costing technique.....................14

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................5

TASK 1............................................................................................................................................5

Q1...........................................................................................................................................5

a) Classify the costs into Fixed, Variable and Semi-variable cost.........................................5

b) Explain other ways of classifying cost...............................................................................5

Q2...........................................................................................................................................7

a) Calculate total and unit costs.............................................................................................7

b) Analyze the cost data.........................................................................................................7

Q3. Calculation of inventory..................................................................................................8

1.FIFO Method ......................................................................................................................8

2.LIFO Method.......................................................................................................................8

3.Average Cost Method..........................................................................................................9

Q4. Prepare report of cost of goods sold................................................................................9

Q5.........................................................................................................................................10

a) Suggest 2 critical factors and performance indicators .....................................................10

B (1) How costs can be reduced...........................................................................................10

B (2) How value and quality can be enhanced.....................................................................11

TASK 2..........................................................................................................................................11

Q6. Usefulness of preparing budget.....................................................................................11

Q7. Preparation of budgets...................................................................................................12

Q8. Preparation of cash budget............................................................................................13

TASK 3..........................................................................................................................................14

Q9) 4.2 Comparison of budgeted and actual profit for Smart Looks Ltd............................14

Computation of selling price by considering the marginal costing technique.....................14

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

Index of Tables

Table 1: Calculation of total costs and unit costs...........................................................................7

Table 2: Analysis of cost data..........................................................................................................7

Table 3: FIFO Method.....................................................................................................................8

Table 4: LIFO Method.....................................................................................................................8

Table 5: Average Cost Method........................................................................................................9

Table 6: Sales Budget....................................................................................................................12

Table 7: Production budget............................................................................................................12

Table 8: Raw Material purchases budget.......................................................................................12

Table 9: Labor budget....................................................................................................................13

Table 10: overhead budget.............................................................................................................13

Table 11: Cash Budget...................................................................................................................14

Table 1: Calculation of total costs and unit costs...........................................................................7

Table 2: Analysis of cost data..........................................................................................................7

Table 3: FIFO Method.....................................................................................................................8

Table 4: LIFO Method.....................................................................................................................8

Table 5: Average Cost Method........................................................................................................9

Table 6: Sales Budget....................................................................................................................12

Table 7: Production budget............................................................................................................12

Table 8: Raw Material purchases budget.......................................................................................12

Table 9: Labor budget....................................................................................................................13

Table 10: overhead budget.............................................................................................................13

Table 11: Cash Budget...................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Illustration Index

Illustration 1: Cost Classificationsource:http://www.yourarticlelibrary.com..................................6

Illustration 1: Cost Classificationsource:http://www.yourarticlelibrary.com..................................6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

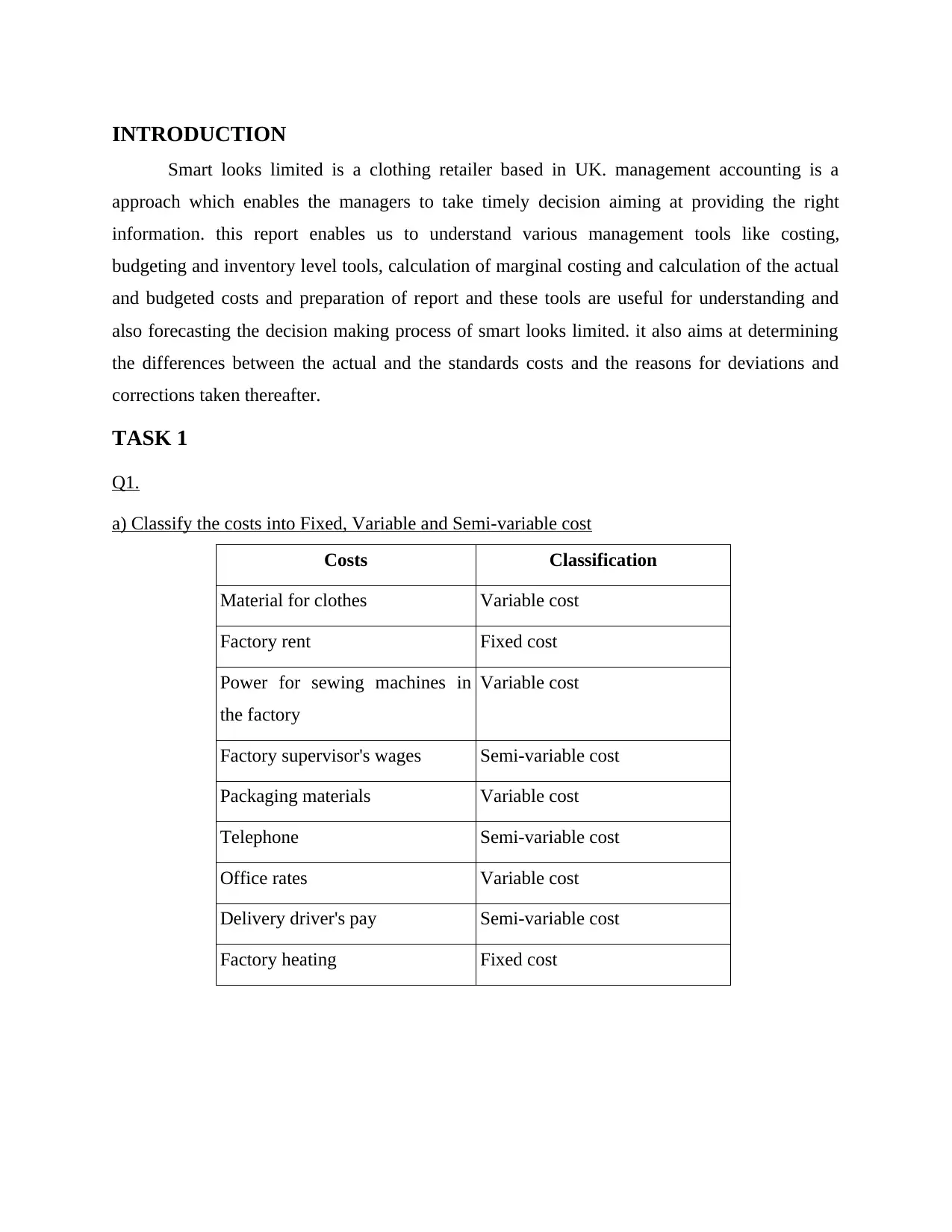

INTRODUCTION

Smart looks limited is a clothing retailer based in UK. management accounting is a

approach which enables the managers to take timely decision aiming at providing the right

information. this report enables us to understand various management tools like costing,

budgeting and inventory level tools, calculation of marginal costing and calculation of the actual

and budgeted costs and preparation of report and these tools are useful for understanding and

also forecasting the decision making process of smart looks limited. it also aims at determining

the differences between the actual and the standards costs and the reasons for deviations and

corrections taken thereafter.

TASK 1

Q1.

a) Classify the costs into Fixed, Variable and Semi-variable cost

Costs Classification

Material for clothes Variable cost

Factory rent Fixed cost

Power for sewing machines in

the factory

Variable cost

Factory supervisor's wages Semi-variable cost

Packaging materials Variable cost

Telephone Semi-variable cost

Office rates Variable cost

Delivery driver's pay Semi-variable cost

Factory heating Fixed cost

Smart looks limited is a clothing retailer based in UK. management accounting is a

approach which enables the managers to take timely decision aiming at providing the right

information. this report enables us to understand various management tools like costing,

budgeting and inventory level tools, calculation of marginal costing and calculation of the actual

and budgeted costs and preparation of report and these tools are useful for understanding and

also forecasting the decision making process of smart looks limited. it also aims at determining

the differences between the actual and the standards costs and the reasons for deviations and

corrections taken thereafter.

TASK 1

Q1.

a) Classify the costs into Fixed, Variable and Semi-variable cost

Costs Classification

Material for clothes Variable cost

Factory rent Fixed cost

Power for sewing machines in

the factory

Variable cost

Factory supervisor's wages Semi-variable cost

Packaging materials Variable cost

Telephone Semi-variable cost

Office rates Variable cost

Delivery driver's pay Semi-variable cost

Factory heating Fixed cost

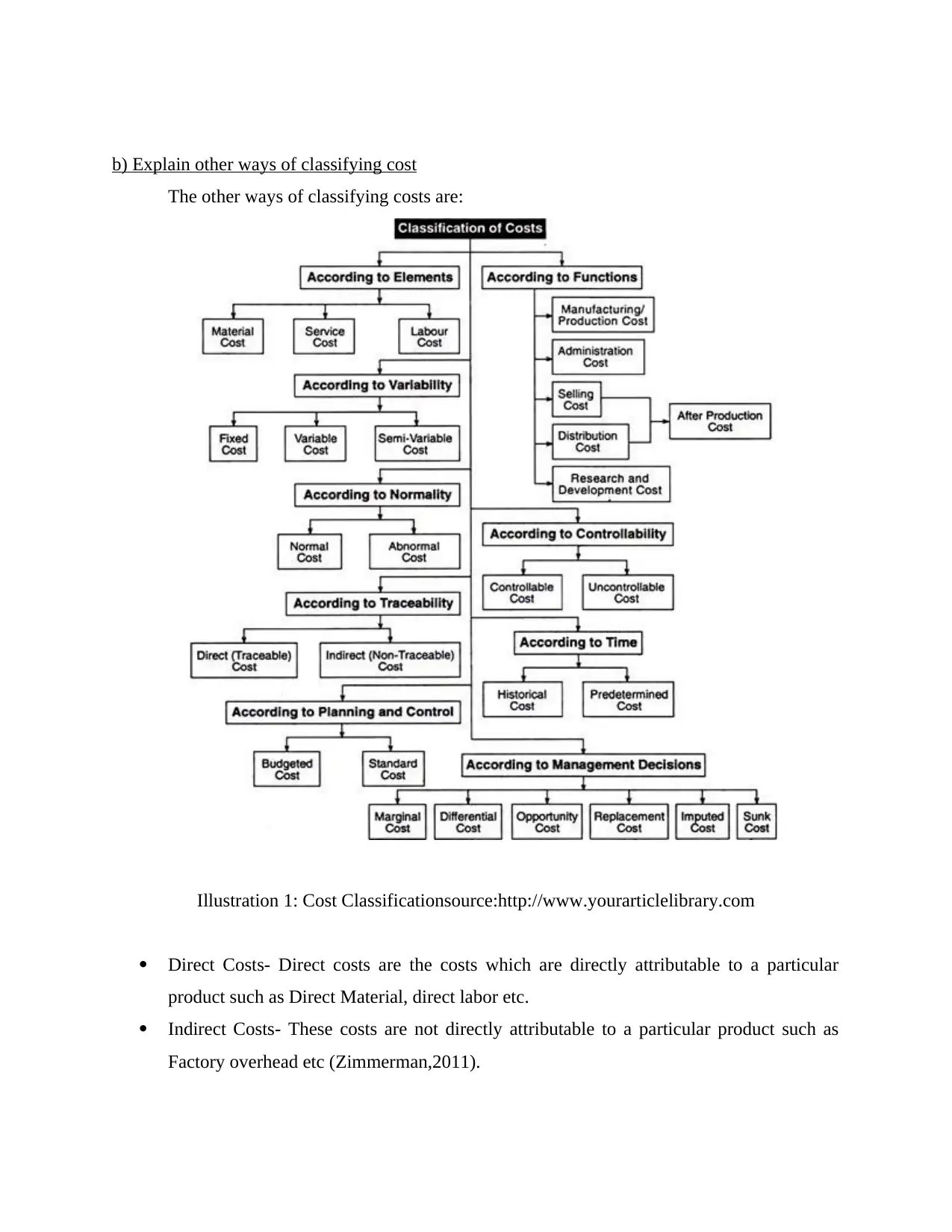

b) Explain other ways of classifying cost

The other ways of classifying costs are:

Illustration 1: Cost Classificationsource:http://www.yourarticlelibrary.com

Direct Costs- Direct costs are the costs which are directly attributable to a particular

product such as Direct Material, direct labor etc.

Indirect Costs- These costs are not directly attributable to a particular product such as

Factory overhead etc (Zimmerman,2011).

The other ways of classifying costs are:

Illustration 1: Cost Classificationsource:http://www.yourarticlelibrary.com

Direct Costs- Direct costs are the costs which are directly attributable to a particular

product such as Direct Material, direct labor etc.

Indirect Costs- These costs are not directly attributable to a particular product such as

Factory overhead etc (Zimmerman,2011).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Product Costs- These costs can be identifies to a individual product. It is the cost which is

incurred when we create a product. Examples are direct material, Factory overhead etc.

Period Costs- These costs cannot be identifies on the individual product and these cost

continues for a period of time like depreciation, advertising expenses etc.

Controllable costs- Controllable costs are the costs can be controlled by the management

like direct expenses, labor etc.

Sunk Costs- As the name suggests, these are the costs which cannot be recovered as they

have already been incurred and thus they are not even considered for decision making.

Example can the cost incurred on training (Pitkänen and Lukka, 2011).

Opportunity Costs- When once alternative is chosen over the another and the cost so

foregone is opportunity costs. These are costs which are considered for decision making.

Q2.

a) Calculate total and unit costs

Table 1: Calculation of total costs and unit costs

15000 units 20000 units 25000 units

Material £5 £75000 £100000 £125000

Labor £6 £90000 £120000 £150000

Total fixed costs £50000 £50000 £50000

Unit Costs ( Total cost /

number of units)

£14.33 £13.5 £13

Material £5 £75000 £100000 £125000

Labor £6 £90000 £120000 £150000

Total fixed costs £50000 £50000 £50000

Total Costs £215000 £270000 £325000

incurred when we create a product. Examples are direct material, Factory overhead etc.

Period Costs- These costs cannot be identifies on the individual product and these cost

continues for a period of time like depreciation, advertising expenses etc.

Controllable costs- Controllable costs are the costs can be controlled by the management

like direct expenses, labor etc.

Sunk Costs- As the name suggests, these are the costs which cannot be recovered as they

have already been incurred and thus they are not even considered for decision making.

Example can the cost incurred on training (Pitkänen and Lukka, 2011).

Opportunity Costs- When once alternative is chosen over the another and the cost so

foregone is opportunity costs. These are costs which are considered for decision making.

Q2.

a) Calculate total and unit costs

Table 1: Calculation of total costs and unit costs

15000 units 20000 units 25000 units

Material £5 £75000 £100000 £125000

Labor £6 £90000 £120000 £150000

Total fixed costs £50000 £50000 £50000

Unit Costs ( Total cost /

number of units)

£14.33 £13.5 £13

Material £5 £75000 £100000 £125000

Labor £6 £90000 £120000 £150000

Total fixed costs £50000 £50000 £50000

Total Costs £215000 £270000 £325000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b) Analyze the cost data

Table 2: Analysis of cost data

Unit costs Total Costs

The unit cost is calculated by dividing

the total cost with the number of units

produced. Unit costs for 15000 units

came out to be £14.33 and that for

2000 units came out to be £13.5 and

for 25000 units the unit cost was £13

which indicates that the per unit costs

increases as the number of units

increases as the per unit cost is the

total expenditure incurred by the

company and includes all the costs

like variable, fixed, labor, overhead

and material costs. Unit cost changes

with the change in the number of

units. Here the fixed cost is not

attributable to the number of units

produced.

It is the cost which includes all the costs

to produce a product. This costs are not

attributable to particular units. The total

costs includes the total fixed costs and

total variable costs. Here the variable

costs the material and the labor costs and

these changes with the change in the

number of units but the fixed cost

remains the same irrespective of the

number of units produced. For producing

15000 units the total cost came out to be

£215000 and for 20000 units the total

cost was £270000 and that for 25000

units the cost was £325000. the total cost

also increases with the increase in the

number of units as it includes some

portion of variable cost which changes

with the change in output.

Q3. Calculation of inventory.

1.FIFO Method

Table 3: FIFO Method

Date Particulars Purchases Sales Balance

Unit Unit cost Total Units Unit cost Total Units Unit cost Total

1 500 £20 £10000

18 800 £24 £19200

25 700 £26 £18200

Table 2: Analysis of cost data

Unit costs Total Costs

The unit cost is calculated by dividing

the total cost with the number of units

produced. Unit costs for 15000 units

came out to be £14.33 and that for

2000 units came out to be £13.5 and

for 25000 units the unit cost was £13

which indicates that the per unit costs

increases as the number of units

increases as the per unit cost is the

total expenditure incurred by the

company and includes all the costs

like variable, fixed, labor, overhead

and material costs. Unit cost changes

with the change in the number of

units. Here the fixed cost is not

attributable to the number of units

produced.

It is the cost which includes all the costs

to produce a product. This costs are not

attributable to particular units. The total

costs includes the total fixed costs and

total variable costs. Here the variable

costs the material and the labor costs and

these changes with the change in the

number of units but the fixed cost

remains the same irrespective of the

number of units produced. For producing

15000 units the total cost came out to be

£215000 and for 20000 units the total

cost was £270000 and that for 25000

units the cost was £325000. the total cost

also increases with the increase in the

number of units as it includes some

portion of variable cost which changes

with the change in output.

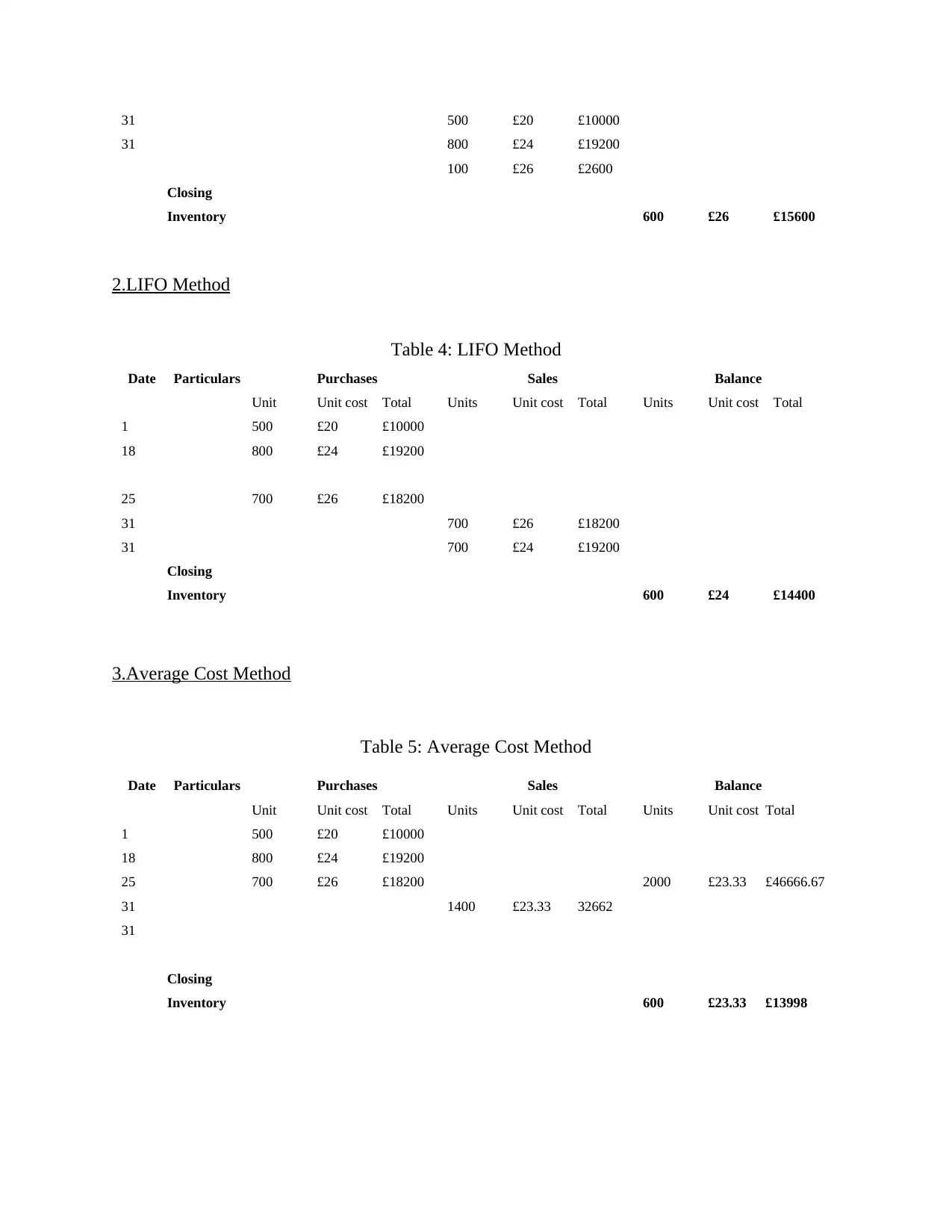

Q3. Calculation of inventory.

1.FIFO Method

Table 3: FIFO Method

Date Particulars Purchases Sales Balance

Unit Unit cost Total Units Unit cost Total Units Unit cost Total

1 500 £20 £10000

18 800 £24 £19200

25 700 £26 £18200

31 500 £20 £10000

31 800 £24 £19200

100 £26 £2600

Closing

Inventory 600 £26 £15600

2.LIFO Method

Table 4: LIFO Method

Date Particulars Purchases Sales Balance

Unit Unit cost Total Units Unit cost Total Units Unit cost Total

1 500 £20 £10000

18 800 £24 £19200

25 700 £26 £18200

31 700 £26 £18200

31 700 £24 £19200

Closing

Inventory 600 £24 £14400

3.Average Cost Method

Table 5: Average Cost Method

Date Particulars Purchases Sales Balance

Unit Unit cost Total Units Unit cost Total Units Unit cost Total

1 500 £20 £10000

18 800 £24 £19200

25 700 £26 £18200 2000 £23.33 £46666.67

31 1400 £23.33 32662

31

Closing

Inventory 600 £23.33 £13998

31 800 £24 £19200

100 £26 £2600

Closing

Inventory 600 £26 £15600

2.LIFO Method

Table 4: LIFO Method

Date Particulars Purchases Sales Balance

Unit Unit cost Total Units Unit cost Total Units Unit cost Total

1 500 £20 £10000

18 800 £24 £19200

25 700 £26 £18200

31 700 £26 £18200

31 700 £24 £19200

Closing

Inventory 600 £24 £14400

3.Average Cost Method

Table 5: Average Cost Method

Date Particulars Purchases Sales Balance

Unit Unit cost Total Units Unit cost Total Units Unit cost Total

1 500 £20 £10000

18 800 £24 £19200

25 700 £26 £18200 2000 £23.33 £46666.67

31 1400 £23.33 32662

31

Closing

Inventory 600 £23.33 £13998

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Q4. Prepare report of cost of goods sold

To

Director,

Smart Looks Ltd.

Cost Of Goods Sold is the summation of all the costs which are incurred in the creation

of that product. As Smart Looks Ltd (Smart Look Ltd, 2016). is using periodic inventory

system, the cost of goods sold includes the beginning inventory, purchases and deducting the

ending inventory. When First in, first out method is used to calculate the ending inventory one

assumes that the oldest units of inventory are sold first. Hence the calculation of 600 units of

closing inventory were valued at £26 so it came out to be the total of £15600. whereas when last

in, first out method is used than the newest inventory are sold first than any other inventory so

the calculation goes like the 600 units were sold at £24 with the total of £14400. Lastly, in the

average cost method, it is based on the average cost per unit and on that basis the cost of goods

sold is calculated. The average cost is calculated by calculating the mean of the data then the

average cost so calculated is multiplied with the number of units 600 and the cost comes out to

be £23.33 (20+24+26=70/3=23.33 ) and the total comes out to be £13998. here as the periodic

methods is used, the inventory count happens at the end of each period. Hence the highest cost

of goods sold came the first in, first out (FIFO) method with the total of £15600.

Q5.

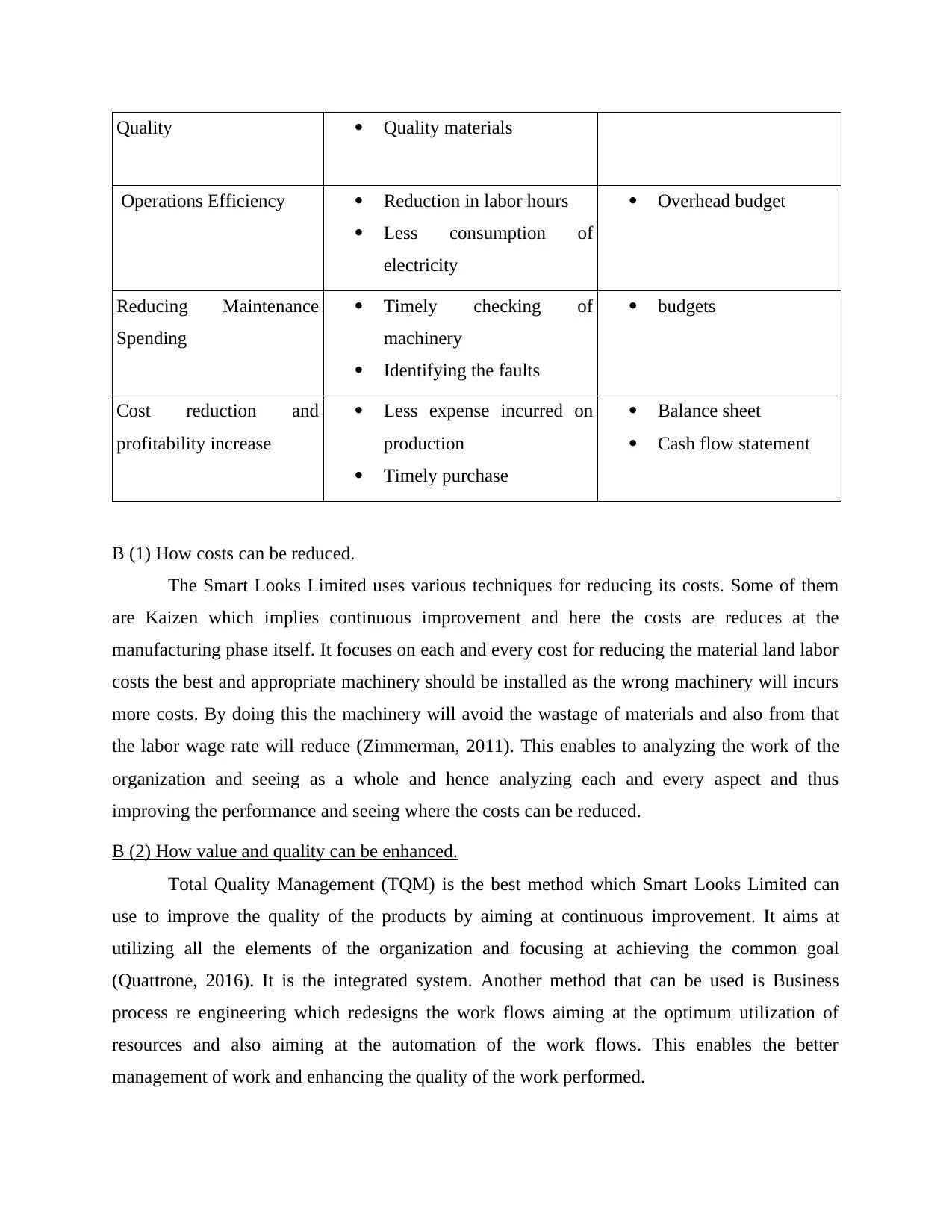

a) Suggest 2 critical factors and performance indicators

The two critical factors for determining customer experience are coordination among the

managers and timeliness and the performance indicators are overall satisfaction, conversion rate.

Critical Factors Performance indicators

Customer Experience Coordination among the

managers

timeliness

Overall satisfaction

Conversion rate

Supplier and Product Materials Repeated purchase

To

Director,

Smart Looks Ltd.

Cost Of Goods Sold is the summation of all the costs which are incurred in the creation

of that product. As Smart Looks Ltd (Smart Look Ltd, 2016). is using periodic inventory

system, the cost of goods sold includes the beginning inventory, purchases and deducting the

ending inventory. When First in, first out method is used to calculate the ending inventory one

assumes that the oldest units of inventory are sold first. Hence the calculation of 600 units of

closing inventory were valued at £26 so it came out to be the total of £15600. whereas when last

in, first out method is used than the newest inventory are sold first than any other inventory so

the calculation goes like the 600 units were sold at £24 with the total of £14400. Lastly, in the

average cost method, it is based on the average cost per unit and on that basis the cost of goods

sold is calculated. The average cost is calculated by calculating the mean of the data then the

average cost so calculated is multiplied with the number of units 600 and the cost comes out to

be £23.33 (20+24+26=70/3=23.33 ) and the total comes out to be £13998. here as the periodic

methods is used, the inventory count happens at the end of each period. Hence the highest cost

of goods sold came the first in, first out (FIFO) method with the total of £15600.

Q5.

a) Suggest 2 critical factors and performance indicators

The two critical factors for determining customer experience are coordination among the

managers and timeliness and the performance indicators are overall satisfaction, conversion rate.

Critical Factors Performance indicators

Customer Experience Coordination among the

managers

timeliness

Overall satisfaction

Conversion rate

Supplier and Product Materials Repeated purchase

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Quality Quality materials

Operations Efficiency Reduction in labor hours

Less consumption of

electricity

Overhead budget

Reducing Maintenance

Spending

Timely checking of

machinery

Identifying the faults

budgets

Cost reduction and

profitability increase

Less expense incurred on

production

Timely purchase

Balance sheet

Cash flow statement

B (1) How costs can be reduced.

The Smart Looks Limited uses various techniques for reducing its costs. Some of them

are Kaizen which implies continuous improvement and here the costs are reduces at the

manufacturing phase itself. It focuses on each and every cost for reducing the material land labor

costs the best and appropriate machinery should be installed as the wrong machinery will incurs

more costs. By doing this the machinery will avoid the wastage of materials and also from that

the labor wage rate will reduce (Zimmerman, 2011). This enables to analyzing the work of the

organization and seeing as a whole and hence analyzing each and every aspect and thus

improving the performance and seeing where the costs can be reduced.

B (2) How value and quality can be enhanced.

Total Quality Management (TQM) is the best method which Smart Looks Limited can

use to improve the quality of the products by aiming at continuous improvement. It aims at

utilizing all the elements of the organization and focusing at achieving the common goal

(Quattrone, 2016). It is the integrated system. Another method that can be used is Business

process re engineering which redesigns the work flows aiming at the optimum utilization of

resources and also aiming at the automation of the work flows. This enables the better

management of work and enhancing the quality of the work performed.

Operations Efficiency Reduction in labor hours

Less consumption of

electricity

Overhead budget

Reducing Maintenance

Spending

Timely checking of

machinery

Identifying the faults

budgets

Cost reduction and

profitability increase

Less expense incurred on

production

Timely purchase

Balance sheet

Cash flow statement

B (1) How costs can be reduced.

The Smart Looks Limited uses various techniques for reducing its costs. Some of them

are Kaizen which implies continuous improvement and here the costs are reduces at the

manufacturing phase itself. It focuses on each and every cost for reducing the material land labor

costs the best and appropriate machinery should be installed as the wrong machinery will incurs

more costs. By doing this the machinery will avoid the wastage of materials and also from that

the labor wage rate will reduce (Zimmerman, 2011). This enables to analyzing the work of the

organization and seeing as a whole and hence analyzing each and every aspect and thus

improving the performance and seeing where the costs can be reduced.

B (2) How value and quality can be enhanced.

Total Quality Management (TQM) is the best method which Smart Looks Limited can

use to improve the quality of the products by aiming at continuous improvement. It aims at

utilizing all the elements of the organization and focusing at achieving the common goal

(Quattrone, 2016). It is the integrated system. Another method that can be used is Business

process re engineering which redesigns the work flows aiming at the optimum utilization of

resources and also aiming at the automation of the work flows. This enables the better

management of work and enhancing the quality of the work performed.

TASK 2

Q6. Usefulness of preparing budget

Budget is a quantitative expression of the revenues and expenses for a particular period of

time defining the future state of the organization. The budgets are important for the company as

it is a tool for monitoring the company's performance as in the beginning itself the budgets are

set and the company's performance are evaluated on the basis of the fact that the company is

meeting with the standards or not. The budgets are also used for the short-term target setting as

the standards are set and the employees are asked to meet the targets within the stipulated time

and on that basis the performance levels are measured and the employees are motivated to

achieve the levels. There are various kinds of budgets like the Zero Base Budgeting, in this the

budgets are developed from the scratch (Vaivio and Sirén, 2010). No previous years/months data

has been considered. Here the main aim is the optimum utilization of resources as the

departments are reviewed as a whole. In the Fixed budget, the entire budget is drawn in advance

and it remains fixed irrespective of the activity levels therefore it is considered to be rigid. In

case of Flexible budget, the budget changes with the change in the activity levels and thus is

dynamic. For Smart Looks Limited the budget which is best suitable is the Fixed or Variable

budget.

Q7. Preparation of budgets

a)

Table 6: Sales Budget

April May June

Sales (£) 2000 1500 2500

Sales price per

unit 30 30 30

Budgeted sales

revenue 60000 45000 75000

b)

Q6. Usefulness of preparing budget

Budget is a quantitative expression of the revenues and expenses for a particular period of

time defining the future state of the organization. The budgets are important for the company as

it is a tool for monitoring the company's performance as in the beginning itself the budgets are

set and the company's performance are evaluated on the basis of the fact that the company is

meeting with the standards or not. The budgets are also used for the short-term target setting as

the standards are set and the employees are asked to meet the targets within the stipulated time

and on that basis the performance levels are measured and the employees are motivated to

achieve the levels. There are various kinds of budgets like the Zero Base Budgeting, in this the

budgets are developed from the scratch (Vaivio and Sirén, 2010). No previous years/months data

has been considered. Here the main aim is the optimum utilization of resources as the

departments are reviewed as a whole. In the Fixed budget, the entire budget is drawn in advance

and it remains fixed irrespective of the activity levels therefore it is considered to be rigid. In

case of Flexible budget, the budget changes with the change in the activity levels and thus is

dynamic. For Smart Looks Limited the budget which is best suitable is the Fixed or Variable

budget.

Q7. Preparation of budgets

a)

Table 6: Sales Budget

April May June

Sales (£) 2000 1500 2500

Sales price per

unit 30 30 30

Budgeted sales

revenue 60000 45000 75000

b)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.