Analysis of Management Accounting for Capital Joinery Ltd (Unit 5)

VerifiedAdded on 2023/01/03

|16

|4157

|33

Report

AI Summary

This report examines management accounting practices within the context of Capital Joinery Ltd, a financial consulting firm. It covers various management accounting systems, including cost accounting, job costing, and inventory management, and their relevance to the firm. The report details different methods of management accounting reporting, such as account receivable aging reports, performance reports, and job cost reports. It also analyzes the uses, advantages, and disadvantages of planning tools like operating budgets, cash budgets, and zero-based budgeting. The report includes a comparison of organizational adaptations to management accounting systems in response to financial problems and a discussion of marginal and absorption costing. Overall, the report provides a comprehensive overview of management accounting principles and their practical application in a real-world business scenario.

UNIT-5 MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

SCENARIO 1...................................................................................................................................3

P:1 Management accounting and different types of management accounting systems and its

requirement.................................................................................................................................3

P:2 Different methods of management accounting reporting.....................................................5

P:4 Uses, advantages and disadvantages of various planning tools used in management

accounting...................................................................................................................................7

LO:4 Comparison of organisation in adapting management accounting system to respond to

financial problems.......................................................................................................................9

SCENARIO 2.................................................................................................................................11

P:3 Marginal and absorption costing........................................................................................11

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

SCENARIO 1...................................................................................................................................3

P:1 Management accounting and different types of management accounting systems and its

requirement.................................................................................................................................3

P:2 Different methods of management accounting reporting.....................................................5

P:4 Uses, advantages and disadvantages of various planning tools used in management

accounting...................................................................................................................................7

LO:4 Comparison of organisation in adapting management accounting system to respond to

financial problems.......................................................................................................................9

SCENARIO 2.................................................................................................................................11

P:3 Marginal and absorption costing........................................................................................11

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION

The management accounting is defined as that branch of accounting which assist the

company in dealing with the analysis of the financial information to take effective decision for

management of company (Amara and Benelifa, 2017). It helps in identifying the weaker or loss

making areas of business beforehand. Management accounting is done for internal use by the

managers and is not required to be shared with external parties. The main purpose of

management accounting is the internal management of the company by using various financial

information.

This report is based on the management accounting system and its application in the

context of Capital Joinery Ltd, a medium sized financial consulting firm headquartered in

London, UK.

This report includes different types of management accounting system and its need and

application, methods of management accounting reporting, advantages and disadvantages of

various planning tools in budgetary control and how Capital Joinery Ltd has adapted

management accounting systems in order to respond to various financial problems.

SCENARIO 1

P:1 Management accounting and different types of management accounting systems and its

requirement

Management accounting as the term itself has management is used for managerial

purposes which involves collecting financial and non-financial information, analysing the

information, applying various tools and techniques of management accounting, interpreting the

results and communicating the same for decision making, problem solving and policy

formulation. Management accounting helps in the internal management of the organization and

its outcomes remains in the business itself and is not meant for sharing with anyone outside the

organization. Also, the reports of management accounting need not be audited by the auditors.

There are some of the most important benefits and objectives of management accounting

for the fulfilment of which the management resort to management accounting. It helps in

decision making, solving financial problems, strategy formulation, effective planning,

controlling and organizing business activities and adopting the efficient business practices

(Azudin and Mansor, 2018.).

The management accounting is defined as that branch of accounting which assist the

company in dealing with the analysis of the financial information to take effective decision for

management of company (Amara and Benelifa, 2017). It helps in identifying the weaker or loss

making areas of business beforehand. Management accounting is done for internal use by the

managers and is not required to be shared with external parties. The main purpose of

management accounting is the internal management of the company by using various financial

information.

This report is based on the management accounting system and its application in the

context of Capital Joinery Ltd, a medium sized financial consulting firm headquartered in

London, UK.

This report includes different types of management accounting system and its need and

application, methods of management accounting reporting, advantages and disadvantages of

various planning tools in budgetary control and how Capital Joinery Ltd has adapted

management accounting systems in order to respond to various financial problems.

SCENARIO 1

P:1 Management accounting and different types of management accounting systems and its

requirement

Management accounting as the term itself has management is used for managerial

purposes which involves collecting financial and non-financial information, analysing the

information, applying various tools and techniques of management accounting, interpreting the

results and communicating the same for decision making, problem solving and policy

formulation. Management accounting helps in the internal management of the organization and

its outcomes remains in the business itself and is not meant for sharing with anyone outside the

organization. Also, the reports of management accounting need not be audited by the auditors.

There are some of the most important benefits and objectives of management accounting

for the fulfilment of which the management resort to management accounting. It helps in

decision making, solving financial problems, strategy formulation, effective planning,

controlling and organizing business activities and adopting the efficient business practices

(Azudin and Mansor, 2018.).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting uses various systems in order to evaluate and analyse the

operations and activities of organization for the purpose of management is termed as

management accounting system. Such systems vary with the type of industry the management is

working and accordingly the type of system to be applied has been decided. Like here in this

report we are taking the financial consultancy firm Capital Joinery Ltd, which has its own way of

doing management accounting which would be best suited to them in working efficiently and it

must be adopting one of the management accounting system for its internal evaluation. There are

certain types of management accounting systems like cost accounting system, job costing

system, inventory management system and price optimization (Cescon, Costantini and Grassetti,

2019).

Cost accounting system is the technique used by management for cost controlling, estimating

cost of various business activities, profitability measurement, inventory pricing, etc. The cost

evaluation helps in profitable business operations and helps in maintaining efficiency in

operations. Cost accounting system is of two types job order costing and process costing where

the former is based on manufacturing costs of each job in the production of products and the

latter is based on manufacturing costs of each process involves in the product manufacturing.

Here Capital Joinery Ltd also has different job and processes required in financial consultancy

and incurs cost accordingly. So to minimize the cost and maximize profits they must have proper

cost accounting system in place (Fuzi and et.al., 2019).

Advantages Disadvantages

Cost reduction

Elimination of unnecessary waste and losses

Advising on making or buying decision

Based on past performance

Cost is ascertained on basis of full utilisation

Job costing system is the type of management accounting system which helps in

knowing the cost associated with each and every job performed as per the customer’s

specifications. The system is useful in estimating the cost in order to define the price of each job

offered, so that the reasonable amount of profit can be earned.

Advantages Disadvantages

Cost is ascertained at any stage of completion

of job

There is not any standardisation of job

This is expensive

operations and activities of organization for the purpose of management is termed as

management accounting system. Such systems vary with the type of industry the management is

working and accordingly the type of system to be applied has been decided. Like here in this

report we are taking the financial consultancy firm Capital Joinery Ltd, which has its own way of

doing management accounting which would be best suited to them in working efficiently and it

must be adopting one of the management accounting system for its internal evaluation. There are

certain types of management accounting systems like cost accounting system, job costing

system, inventory management system and price optimization (Cescon, Costantini and Grassetti,

2019).

Cost accounting system is the technique used by management for cost controlling, estimating

cost of various business activities, profitability measurement, inventory pricing, etc. The cost

evaluation helps in profitable business operations and helps in maintaining efficiency in

operations. Cost accounting system is of two types job order costing and process costing where

the former is based on manufacturing costs of each job in the production of products and the

latter is based on manufacturing costs of each process involves in the product manufacturing.

Here Capital Joinery Ltd also has different job and processes required in financial consultancy

and incurs cost accordingly. So to minimize the cost and maximize profits they must have proper

cost accounting system in place (Fuzi and et.al., 2019).

Advantages Disadvantages

Cost reduction

Elimination of unnecessary waste and losses

Advising on making or buying decision

Based on past performance

Cost is ascertained on basis of full utilisation

Job costing system is the type of management accounting system which helps in

knowing the cost associated with each and every job performed as per the customer’s

specifications. The system is useful in estimating the cost in order to define the price of each job

offered, so that the reasonable amount of profit can be earned.

Advantages Disadvantages

Cost is ascertained at any stage of completion

of job

There is not any standardisation of job

This is expensive

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Profit is earned from every job

Inventory management system refers to that system where the goods are being tracked

right from its procurement till the final supply in order to avoid both overstocking and under

stocking because both of these condition results in decrease in profits. This system can be more

beneficial if the techniques of inventory management have been applied properly.

Advantages Disadvantages

Cost saving

Time saving

It is very complex

Expensive

Price optimization is a system which involves the behaviour of demand function at

different prices, and then, this information is incorporated with the cost and inventory data in

order to define the price of the product that will generate good profits. Capital Joinery Ltd can

define its consultancy fees according to the cost they paid for hiring professionals for financial

advisory and their position in the market in terms of demand (Gibassier and Alcouffe,2018).

Advantages Disadvantages

It is time saving

There is having market transparency

It is very complex process

There is low security

P:2 Different methods of management accounting reporting

Management accounting reporting is all about preparing reports by the management for

future planning, regulating various organizational activities, timely decision making and

measuring the company's performance against the set standards. These reports are prepared on

regular basis in accordance with the requirements. Managers then critically analyse these reports

in order to introduce the required changes. Capital Joinery Ltd as a financial consultancy firm

follows management accounting reporting for analysing the reliability of its professional advice.

The different methods of management accounting reporting used by the organization are as

follows:

Account receivable aging reports involves information regarding how much credit has

been extended and how much collection has been done. This helps in avoiding bad debts because

a manager must have strived for minimizing bad debts as it will directly affect their profitability.

Inventory management system refers to that system where the goods are being tracked

right from its procurement till the final supply in order to avoid both overstocking and under

stocking because both of these condition results in decrease in profits. This system can be more

beneficial if the techniques of inventory management have been applied properly.

Advantages Disadvantages

Cost saving

Time saving

It is very complex

Expensive

Price optimization is a system which involves the behaviour of demand function at

different prices, and then, this information is incorporated with the cost and inventory data in

order to define the price of the product that will generate good profits. Capital Joinery Ltd can

define its consultancy fees according to the cost they paid for hiring professionals for financial

advisory and their position in the market in terms of demand (Gibassier and Alcouffe,2018).

Advantages Disadvantages

It is time saving

There is having market transparency

It is very complex process

There is low security

P:2 Different methods of management accounting reporting

Management accounting reporting is all about preparing reports by the management for

future planning, regulating various organizational activities, timely decision making and

measuring the company's performance against the set standards. These reports are prepared on

regular basis in accordance with the requirements. Managers then critically analyse these reports

in order to introduce the required changes. Capital Joinery Ltd as a financial consultancy firm

follows management accounting reporting for analysing the reliability of its professional advice.

The different methods of management accounting reporting used by the organization are as

follows:

Account receivable aging reports involves information regarding how much credit has

been extended and how much collection has been done. This helps in avoiding bad debts because

a manager must have strived for minimizing bad debts as it will directly affect their profitability.

If the company is facing more and more defaulters, then it must redefine its credit policies as

because a reasonable amount of cash flow is necessary for business operation (Hutaibat and

Alhatabat, 2020.).

Performance reports are generated to give the deep insight over the performance of the

organization. Such reports are also prepared on departmental and individual basis where the

former gives insight into the individual contribution in the organization while the latter is based

on different departments in the organization. Performance reports helps in comparing the actual

performance with the set standards which is beneficial in devising various strategies for

achieving organizational goals. Capital Joinery Ltd prepares this report for evaluating the

performance of its professionals by analysing the investment growth and financial stability.

Job cost reports are based on evaluating costs of various job offered by the company

where each and every job are compared in terms of its costs and revenue so that the company can

focus on that particular job which generate more revenue rather than wasting time and resources

on those jobs which are less attractive and loss making. Capital Joinery Ltd can prepare this

report for analysing its professionals and expert’s capability and excellence in various financial

advisory so that they can focus more on that financial service where they can maximize their

returns (Langfield-Smith, Thorne and Hilton, 2018.).

M1

Management accounting system has many benefits for capital joinery if applied properly and it

must be helpful in decision making and internal management. If cost accounting system has been

followed by capital joinery, then they can have better control over their costs and would be

helpful in increased profit margins.

In case of job costing system where the cost of each job are ascertained and evaluated on regular

basis can help capital joinery to focus more on that job where they can generate more profits due

to lower cost.

Through inventory management system capital joinery can avoid losses due to overstocking and

under stocking because both the situation has an extra cost in terms of actual and notional costs

respectively.

D1

because a reasonable amount of cash flow is necessary for business operation (Hutaibat and

Alhatabat, 2020.).

Performance reports are generated to give the deep insight over the performance of the

organization. Such reports are also prepared on departmental and individual basis where the

former gives insight into the individual contribution in the organization while the latter is based

on different departments in the organization. Performance reports helps in comparing the actual

performance with the set standards which is beneficial in devising various strategies for

achieving organizational goals. Capital Joinery Ltd prepares this report for evaluating the

performance of its professionals by analysing the investment growth and financial stability.

Job cost reports are based on evaluating costs of various job offered by the company

where each and every job are compared in terms of its costs and revenue so that the company can

focus on that particular job which generate more revenue rather than wasting time and resources

on those jobs which are less attractive and loss making. Capital Joinery Ltd can prepare this

report for analysing its professionals and expert’s capability and excellence in various financial

advisory so that they can focus more on that financial service where they can maximize their

returns (Langfield-Smith, Thorne and Hilton, 2018.).

M1

Management accounting system has many benefits for capital joinery if applied properly and it

must be helpful in decision making and internal management. If cost accounting system has been

followed by capital joinery, then they can have better control over their costs and would be

helpful in increased profit margins.

In case of job costing system where the cost of each job are ascertained and evaluated on regular

basis can help capital joinery to focus more on that job where they can generate more profits due

to lower cost.

Through inventory management system capital joinery can avoid losses due to overstocking and

under stocking because both the situation has an extra cost in terms of actual and notional costs

respectively.

D1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Both management accounting system and management accounting reporting has its important

role to play in every organization. By following the management accounting system,

management accounting reporting can be performed.

As per the view of management consultant Jim Henry, who says that if management accounting

systems and reporting are integrated properly in its processes then it will aid in decision making

and managing the internal affairs of the business efficiently. Also, the profit earning capacity can

be enhanced and the goals of the organization can be achieved successfully.

As against this, the management expertise John Gems says that not all organization can reap the

same benefits as other because it has been argued that only big organization who has a good

financial base can afford to have proper management accounting systems and reporting in place.

Also, it is regarded as a wastage of time on every small thing (Nagirikandalage and et.al., 2020).

P:4 Uses, advantages and disadvantages of various planning tools used in management

accounting

Budgetary control is the method of controlling various affairs of the organization, where a

budget is developed in advance and then the actual outcomes are compared with the budgeted

figures at the end of the period, and if any deviations are found then some corrective measures

are introduced to remove the deviations. Variances help in improving efficiency and better

decision making.

Budgetary control helps organisation in planning, controlling, coordinating and

improving performance.

Some planning tools used for budgetary control are as follows:

Operating budget controls day to day operations of the business and helps in improving

performance without delay. This budget involves control over operating expenses and makes it

easy to earn monthly targeted revenue. This budget provides smooth running of day to day

operations of the organization.

Application of operating budget in capital joinery is that they can set their target revenue and

operating expenses in the budget and at the end they can compare the actual revenue earned and

expenses incurred. This will help in avoiding past deviations by taking corrective actions on time

(Phan, Baird and Su, 2017).

Advantages of operating budget is that it helps in achieving smooth operations in day to day

business activities and capital joinery can achieve its desired revenue by controlling its costs.

role to play in every organization. By following the management accounting system,

management accounting reporting can be performed.

As per the view of management consultant Jim Henry, who says that if management accounting

systems and reporting are integrated properly in its processes then it will aid in decision making

and managing the internal affairs of the business efficiently. Also, the profit earning capacity can

be enhanced and the goals of the organization can be achieved successfully.

As against this, the management expertise John Gems says that not all organization can reap the

same benefits as other because it has been argued that only big organization who has a good

financial base can afford to have proper management accounting systems and reporting in place.

Also, it is regarded as a wastage of time on every small thing (Nagirikandalage and et.al., 2020).

P:4 Uses, advantages and disadvantages of various planning tools used in management

accounting

Budgetary control is the method of controlling various affairs of the organization, where a

budget is developed in advance and then the actual outcomes are compared with the budgeted

figures at the end of the period, and if any deviations are found then some corrective measures

are introduced to remove the deviations. Variances help in improving efficiency and better

decision making.

Budgetary control helps organisation in planning, controlling, coordinating and

improving performance.

Some planning tools used for budgetary control are as follows:

Operating budget controls day to day operations of the business and helps in improving

performance without delay. This budget involves control over operating expenses and makes it

easy to earn monthly targeted revenue. This budget provides smooth running of day to day

operations of the organization.

Application of operating budget in capital joinery is that they can set their target revenue and

operating expenses in the budget and at the end they can compare the actual revenue earned and

expenses incurred. This will help in avoiding past deviations by taking corrective actions on time

(Phan, Baird and Su, 2017).

Advantages of operating budget is that it helps in achieving smooth operations in day to day

business activities and capital joinery can achieve its desired revenue by controlling its costs.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Disadvantages of operating budget are that it’s a time consuming and expensive affair for such

a medium sized organization like capital joinery.

Cash budget controls the various inflows and outflows in day to day business activities. It

makes sure that the business has requires level of cash in hand to meet its day to day obligations

and also ensures that the cash has not been kept idle by investing the idle cash in short term

investment and earn profit on it.

Application of cash budget in capital joinery is that it can prepare cash budget to avoid

surplus or idle cash by making profitable investment and ensure its financial stability in meeting

its present short term obligations.

Advantages of cash budget is that it helps capital joinery in managing its inflows and

outflows of cash on weekly and monthly basis through this budget and ensures its short term

financial stability. It also helps in avoiding surplus and shortage of cash. Cash budget is one of

the indicators of financial position of the organization.

Disadvantages of cash budget are, if there is any mistake in ascertaining cash

requirement or preparing cash budget then the financial stability of the company will be affected

very much. If effective cash budget is not prepared, then there are chances of theft as well.

Sometimes limitations on spending can give negative results from losing profitable opportunity

(Quattrone, 2016.).

Zero-Based budgeting is the method of preparing budget for expenses that are going to be

incurred in the future on actual basis and not on some past trends or expenses that are already

incurred. As the name suggest that it is a zero- based which means the budget is prepared from

zero level as against the traditional way of budgeting where the previous budgets are just revised

by making alterations. For this budget re- evaluation of all business activities has been done and

each and every expense is justified before taking it into the budget.

Application of zero-based budgeting in capital joinery is that it can follow zero-based

budgeting for avoiding past mistakes in preparing budget because all the expenses that are

actually going to be incurred are considered here. This budgeting technique would be more

beneficial particularly for capital joinery because they are approaching for management

accounting consultancy for the first time, so they may not be having effective past budgets.

Advantages of zero-based budgeting is that it helps in efficient resource allocation as it

is not depended on past numbers and instead rely on actual figures which makes it more accurate

a medium sized organization like capital joinery.

Cash budget controls the various inflows and outflows in day to day business activities. It

makes sure that the business has requires level of cash in hand to meet its day to day obligations

and also ensures that the cash has not been kept idle by investing the idle cash in short term

investment and earn profit on it.

Application of cash budget in capital joinery is that it can prepare cash budget to avoid

surplus or idle cash by making profitable investment and ensure its financial stability in meeting

its present short term obligations.

Advantages of cash budget is that it helps capital joinery in managing its inflows and

outflows of cash on weekly and monthly basis through this budget and ensures its short term

financial stability. It also helps in avoiding surplus and shortage of cash. Cash budget is one of

the indicators of financial position of the organization.

Disadvantages of cash budget are, if there is any mistake in ascertaining cash

requirement or preparing cash budget then the financial stability of the company will be affected

very much. If effective cash budget is not prepared, then there are chances of theft as well.

Sometimes limitations on spending can give negative results from losing profitable opportunity

(Quattrone, 2016.).

Zero-Based budgeting is the method of preparing budget for expenses that are going to be

incurred in the future on actual basis and not on some past trends or expenses that are already

incurred. As the name suggest that it is a zero- based which means the budget is prepared from

zero level as against the traditional way of budgeting where the previous budgets are just revised

by making alterations. For this budget re- evaluation of all business activities has been done and

each and every expense is justified before taking it into the budget.

Application of zero-based budgeting in capital joinery is that it can follow zero-based

budgeting for avoiding past mistakes in preparing budget because all the expenses that are

actually going to be incurred are considered here. This budgeting technique would be more

beneficial particularly for capital joinery because they are approaching for management

accounting consultancy for the first time, so they may not be having effective past budgets.

Advantages of zero-based budgeting is that it helps in efficient resource allocation as it

is not depended on past numbers and instead rely on actual figures which makes it more accurate

than other budgeting techniques. This budgeting helps in achieving cost efficiency by removing

non-productive activities and focusing more on productive and profitable areas.

Disadvantages of zero-based budgeting is that it is quite time consuming affair as

against traditional budgeting because here a lot of time is required for preparing budget from

zero level every time. Also, justifying each and every activity before taking into budget require

high, experienced and expertise manpower which is a very costly affair for a middle sized

organization like capital joinery.

Sales budget- this is an estimation which is made for the purpose of forecasting of the estimated

sales. This budget will assist the company Capital Joinery ltd in managing the work and

operations as per the estimates sales of the company.

Advantages

The major advantage of using this budget is that this assists the company in managing the

operations as per the estimated sales in the sales budget.

Disadvantages

On the other side the major drawback of this method is that for the business it is not static that

the future condition or the condition of the business environment is not stable.

In addition to this another major drawback of this method is that it is not at all easy for Capital

Joinery Ltd to forecast the future.

LO:4 Comparison of organisation in adapting management accounting system to respond to

financial problems.

Financial problems are referred as those circumstances where an organization has

financial instability. Such problem can arise any time in the life of the business may be due to

ineffective planning and cash flow issues. When a company is not even capable of providing for

its working capital, occurrence of unexpected expenses, capital inadequacy is some of the

financial problems faced by the organization anytime.

Some of the management accounting systems that are being used to respond such

financial problems are as follows:

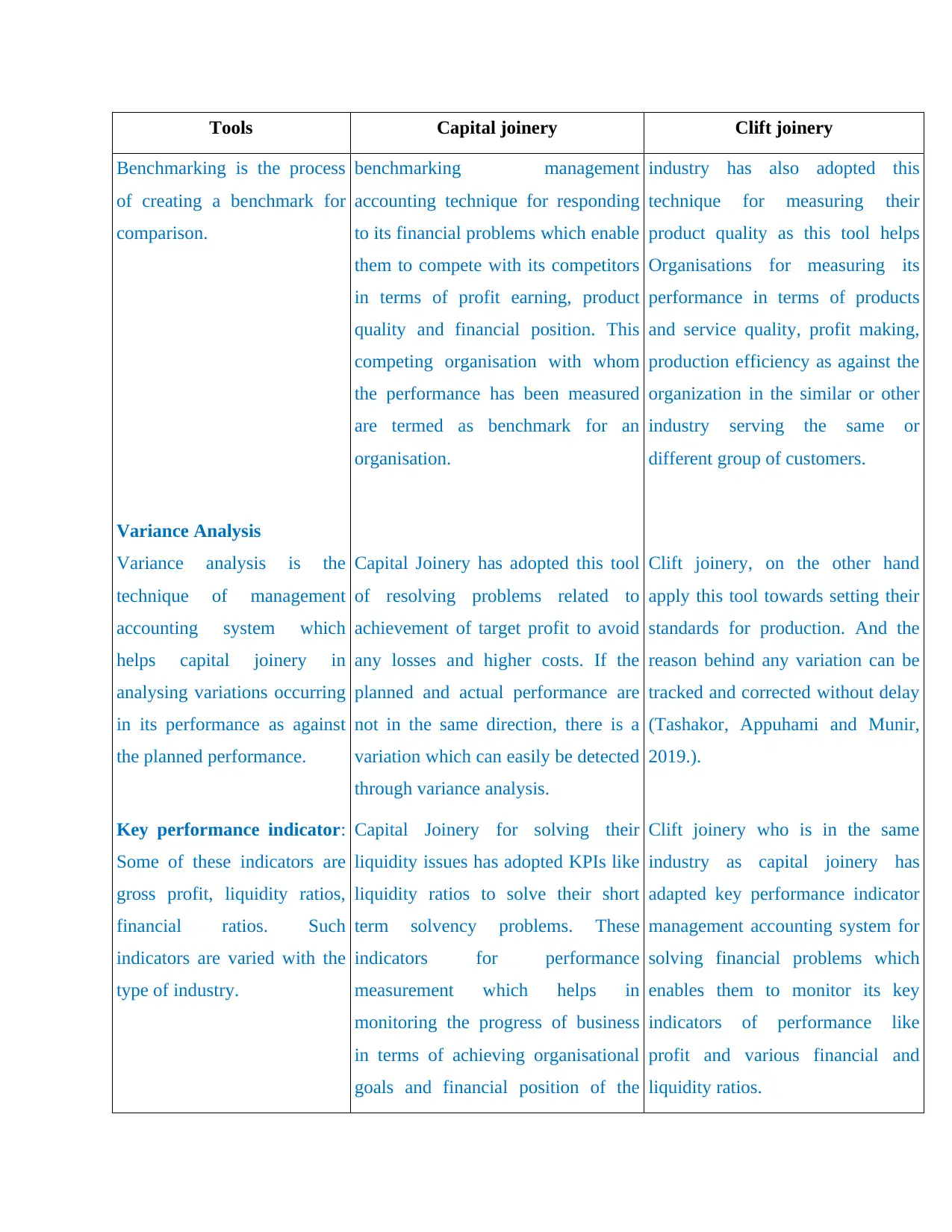

Comparison of two organizations

Tools Capital joinery Clift joinery

Benchmarking Capital joinery has adapted the Clift joinery operating in the same

non-productive activities and focusing more on productive and profitable areas.

Disadvantages of zero-based budgeting is that it is quite time consuming affair as

against traditional budgeting because here a lot of time is required for preparing budget from

zero level every time. Also, justifying each and every activity before taking into budget require

high, experienced and expertise manpower which is a very costly affair for a middle sized

organization like capital joinery.

Sales budget- this is an estimation which is made for the purpose of forecasting of the estimated

sales. This budget will assist the company Capital Joinery ltd in managing the work and

operations as per the estimates sales of the company.

Advantages

The major advantage of using this budget is that this assists the company in managing the

operations as per the estimated sales in the sales budget.

Disadvantages

On the other side the major drawback of this method is that for the business it is not static that

the future condition or the condition of the business environment is not stable.

In addition to this another major drawback of this method is that it is not at all easy for Capital

Joinery Ltd to forecast the future.

LO:4 Comparison of organisation in adapting management accounting system to respond to

financial problems.

Financial problems are referred as those circumstances where an organization has

financial instability. Such problem can arise any time in the life of the business may be due to

ineffective planning and cash flow issues. When a company is not even capable of providing for

its working capital, occurrence of unexpected expenses, capital inadequacy is some of the

financial problems faced by the organization anytime.

Some of the management accounting systems that are being used to respond such

financial problems are as follows:

Comparison of two organizations

Tools Capital joinery Clift joinery

Benchmarking Capital joinery has adapted the Clift joinery operating in the same

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tools Capital joinery Clift joinery

Benchmarking is the process

of creating a benchmark for

comparison.

benchmarking management

accounting technique for responding

to its financial problems which enable

them to compete with its competitors

in terms of profit earning, product

quality and financial position. This

competing organisation with whom

the performance has been measured

are termed as benchmark for an

organisation.

industry has also adopted this

technique for measuring their

product quality as this tool helps

Organisations for measuring its

performance in terms of products

and service quality, profit making,

production efficiency as against the

organization in the similar or other

industry serving the same or

different group of customers.

Variance Analysis

Variance analysis is the

technique of management

accounting system which

helps capital joinery in

analysing variations occurring

in its performance as against

the planned performance.

Capital Joinery has adopted this tool

of resolving problems related to

achievement of target profit to avoid

any losses and higher costs. If the

planned and actual performance are

not in the same direction, there is a

variation which can easily be detected

through variance analysis.

Clift joinery, on the other hand

apply this tool towards setting their

standards for production. And the

reason behind any variation can be

tracked and corrected without delay

(Tashakor, Appuhami and Munir,

2019.).

Key performance indicator:

Some of these indicators are

gross profit, liquidity ratios,

financial ratios. Such

indicators are varied with the

type of industry.

Capital Joinery for solving their

liquidity issues has adopted KPIs like

liquidity ratios to solve their short

term solvency problems. These

indicators for performance

measurement which helps in

monitoring the progress of business

in terms of achieving organisational

goals and financial position of the

Clift joinery who is in the same

industry as capital joinery has

adapted key performance indicator

management accounting system for

solving financial problems which

enables them to monitor its key

indicators of performance like

profit and various financial and

liquidity ratios.

Benchmarking is the process

of creating a benchmark for

comparison.

benchmarking management

accounting technique for responding

to its financial problems which enable

them to compete with its competitors

in terms of profit earning, product

quality and financial position. This

competing organisation with whom

the performance has been measured

are termed as benchmark for an

organisation.

industry has also adopted this

technique for measuring their

product quality as this tool helps

Organisations for measuring its

performance in terms of products

and service quality, profit making,

production efficiency as against the

organization in the similar or other

industry serving the same or

different group of customers.

Variance Analysis

Variance analysis is the

technique of management

accounting system which

helps capital joinery in

analysing variations occurring

in its performance as against

the planned performance.

Capital Joinery has adopted this tool

of resolving problems related to

achievement of target profit to avoid

any losses and higher costs. If the

planned and actual performance are

not in the same direction, there is a

variation which can easily be detected

through variance analysis.

Clift joinery, on the other hand

apply this tool towards setting their

standards for production. And the

reason behind any variation can be

tracked and corrected without delay

(Tashakor, Appuhami and Munir,

2019.).

Key performance indicator:

Some of these indicators are

gross profit, liquidity ratios,

financial ratios. Such

indicators are varied with the

type of industry.

Capital Joinery for solving their

liquidity issues has adopted KPIs like

liquidity ratios to solve their short

term solvency problems. These

indicators for performance

measurement which helps in

monitoring the progress of business

in terms of achieving organisational

goals and financial position of the

Clift joinery who is in the same

industry as capital joinery has

adapted key performance indicator

management accounting system for

solving financial problems which

enables them to monitor its key

indicators of performance like

profit and various financial and

liquidity ratios.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tools Capital joinery Clift joinery

company.

M4

By adopting all this management accounting system in responding to financial problems, like for

example capital joinery has adapted the benchmarking system which will help it in setting the

benchmark as its competitor. When the competitor is set as standards it would become easier to

compete in the market and leads to sustainable success through confidence and set expectations.

D3

Different planning tools like cash flow budget, operating budget are helpful in responding to

various financial problems because a budgeting is a technique which gives in advance an idea

about how many resources and fund are required and how much expense are expected to be

incurred to achieve the target. This advance knowledge helps in making timely arrangement for

the same efficiently.

SCENARIO 2

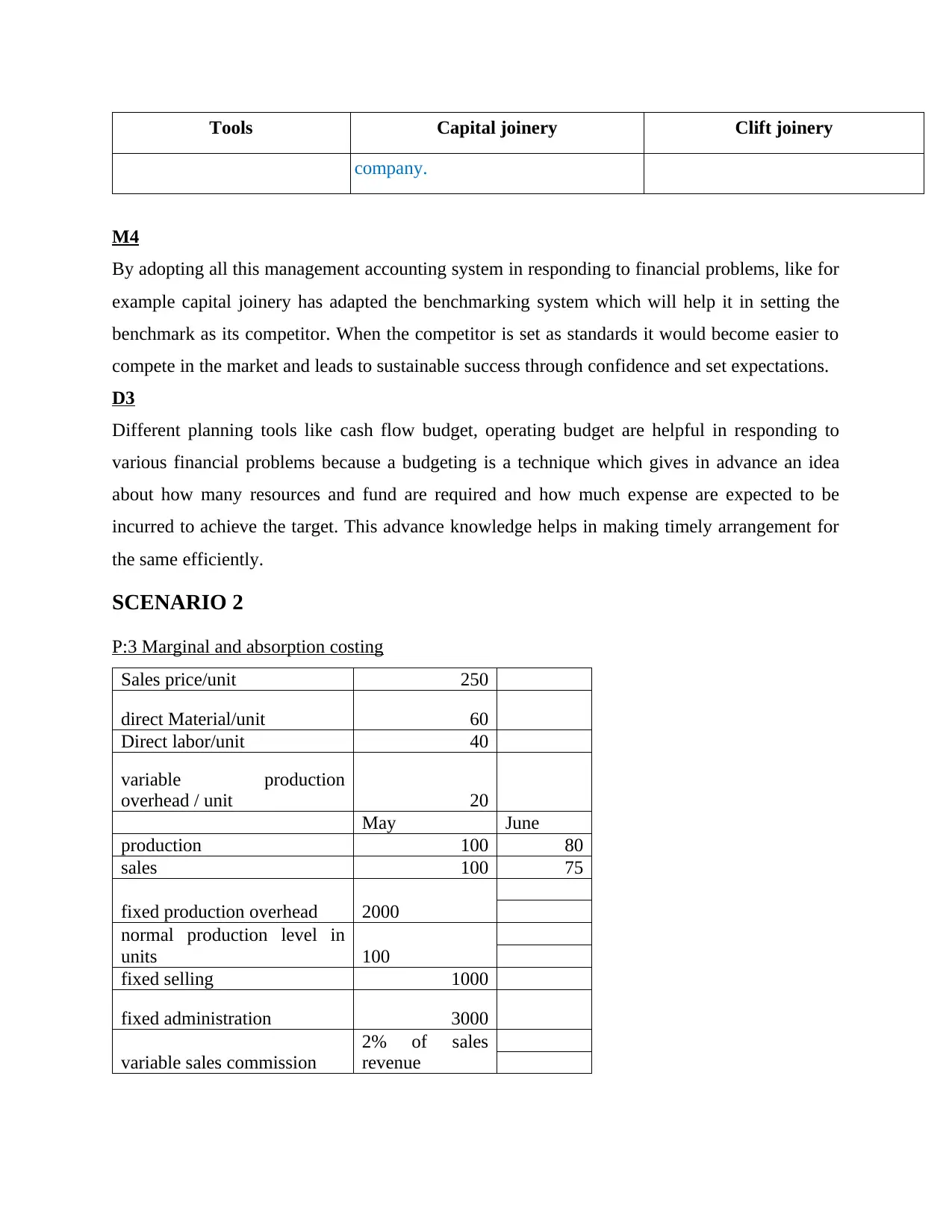

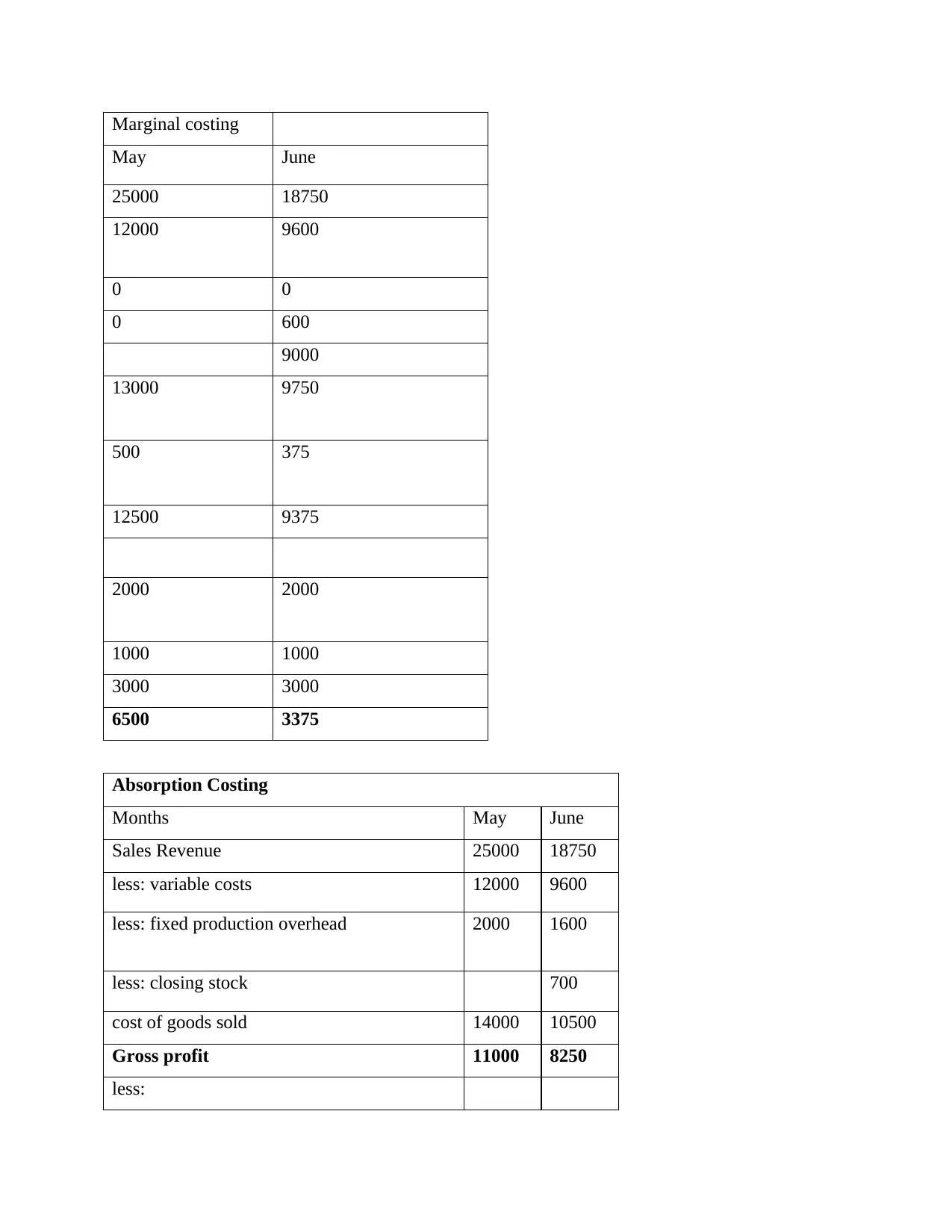

P:3 Marginal and absorption costing

Sales price/unit 250

direct Material/unit 60

Direct labor/unit 40

variable production

overhead / unit 20

May June

production 100 80

sales 100 75

fixed production overhead 2000

normal production level in

units 100

fixed selling 1000

fixed administration 3000

variable sales commission

2% of sales

revenue

company.

M4

By adopting all this management accounting system in responding to financial problems, like for

example capital joinery has adapted the benchmarking system which will help it in setting the

benchmark as its competitor. When the competitor is set as standards it would become easier to

compete in the market and leads to sustainable success through confidence and set expectations.

D3

Different planning tools like cash flow budget, operating budget are helpful in responding to

various financial problems because a budgeting is a technique which gives in advance an idea

about how many resources and fund are required and how much expense are expected to be

incurred to achieve the target. This advance knowledge helps in making timely arrangement for

the same efficiently.

SCENARIO 2

P:3 Marginal and absorption costing

Sales price/unit 250

direct Material/unit 60

Direct labor/unit 40

variable production

overhead / unit 20

May June

production 100 80

sales 100 75

fixed production overhead 2000

normal production level in

units 100

fixed selling 1000

fixed administration 3000

variable sales commission

2% of sales

revenue

Marginal costing

May June

25000 18750

12000 9600

0 0

0 600

9000

13000 9750

500 375

12500 9375

2000 2000

1000 1000

3000 3000

6500 3375

Absorption Costing

Months May June

Sales Revenue 25000 18750

less: variable costs 12000 9600

less: fixed production overhead 2000 1600

less: closing stock 700

cost of goods sold 14000 10500

Gross profit 11000 8250

less:

May June

25000 18750

12000 9600

0 0

0 600

9000

13000 9750

500 375

12500 9375

2000 2000

1000 1000

3000 3000

6500 3375

Absorption Costing

Months May June

Sales Revenue 25000 18750

less: variable costs 12000 9600

less: fixed production overhead 2000 1600

less: closing stock 700

cost of goods sold 14000 10500

Gross profit 11000 8250

less:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.