Management Accounting Report: Financial Planning and Analysis, Report

VerifiedAdded on 2020/10/22

|17

|4256

|380

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its application within Rolls-Royce Holdings. It begins with an introduction to management accounting, explaining its role in business development and decision-making, and then delves into different management accounting systems, including cost accounting, price optimization, and inventory management. The report also explores the integration of these systems within organizational processes and highlights the benefits of each. Part B of the report examines various planning tools, particularly those used for budgetary control, such as flexible budgets. It compares marginal costing and absorption costing methods, providing income statements for both and interpreting the financial outcomes. Furthermore, the report discusses the use of Activity-Based Costing (ABC) and its application in Rolls-Royce. Overall, the report offers insights into how management accounting can be utilized to improve business operations and achieve sustainable success, supported by financial analysis and planning tools.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION..........................................................................................................................1

DEMONSTRATE UNDERSTANDING OF MANAGEMENT ACCOUNTING SYSTEMS

..........................................................................................................................................................1

Explain the management accounting and also explain needs of management accounting

systems ..................................................................................................................................1

Management accounting system and the reporting integration within organisational processes

................................................................................................................................................3

PART B..................................................................................................................................3

EXPLAIN USE OF PLANNING TOOLING USED IN THE MANAGEMENT

ACCOUNTING..............................................................................................................................7

Use of various planning tools and their application...............................................................9

COMPARISON OF ORGANISATION USING MANAGEMENT ACCOUNTING TO

RESPOND TO FINANCIAL ISSUES..........................................................................................11

Comparison of how organisations are adapting management accounting systems to..........12

Respond to financial problems............................................................................................12

An analysis of how in responding to financial problems, management accounting can lead12

organisation to sustainable success.....................................................................................12

An evaluation of how planning tools for accounting help to solve problems and support. .13

Organisations with sustainable success...............................................................................13

CONCLUSION............................................................................................................................13

BIBLIOGRAPHY........................................................................................................................14

REFERENCES.............................................................................................................................15

INTRODUCTION..........................................................................................................................1

DEMONSTRATE UNDERSTANDING OF MANAGEMENT ACCOUNTING SYSTEMS

..........................................................................................................................................................1

Explain the management accounting and also explain needs of management accounting

systems ..................................................................................................................................1

Management accounting system and the reporting integration within organisational processes

................................................................................................................................................3

PART B..................................................................................................................................3

EXPLAIN USE OF PLANNING TOOLING USED IN THE MANAGEMENT

ACCOUNTING..............................................................................................................................7

Use of various planning tools and their application...............................................................9

COMPARISON OF ORGANISATION USING MANAGEMENT ACCOUNTING TO

RESPOND TO FINANCIAL ISSUES..........................................................................................11

Comparison of how organisations are adapting management accounting systems to..........12

Respond to financial problems............................................................................................12

An analysis of how in responding to financial problems, management accounting can lead12

organisation to sustainable success.....................................................................................12

An evaluation of how planning tools for accounting help to solve problems and support. .13

Organisations with sustainable success...............................................................................13

CONCLUSION............................................................................................................................13

BIBLIOGRAPHY........................................................................................................................14

REFERENCES.............................................................................................................................15

INTRODUCTION

Management accounting refers to analysis of the financial data and the advice to

company for the use in business development. This process of analysing the operations as well as

business cost for the purpose of prepare the internal financial reports and records helps top

management in process of decision making to attain set business objectives. It is an act of

making the sense of costing and financial data and then translating it into useful information for

top management within company (Bouten and Hoozée, 2013). This present report is based on

Rolls-Royce Holdings that is an engineering firm, focus on world- class propulsion, and power

system. In this mention report will discussed about the management accounting and essential

requirements of different types of systems. Benefits and disadvantages of different types of

planning tools, which are mainly used for the budgetary control, will discussed here.

DEMONSTRATE UNDERSTANDING OF MANAGEMENT

ACCOUNTING SYSTEMS

Explain the management accounting and also explain needs of management accounting systems

Management accounting is mainly used through the managers for purpose of taking the

effective decision for performing business operation and control the different functions for

business productivity. It consists creation of the Management accounting reports to give accurate

information to formulate short term as well as long-term plans for achieving company objectives

(Cadez and Guilding, 2012). For assure that work is to be performed according to planned

activities, there are different kinds of accounting system mention below:

Cost accounting system: It is a kind of Management Accounting system that is mainly

used by managers for the purpose of recording activities tracking materials and examining the

production cost at various production phrases from the raw material to finish. This system aids in

approximation associated cost for measuring profit level valuation of inventory and controlling

cost. Rolls-Royce applies this system for examining the different cost at every product stage and

focus on the products, which will be benefited, more to firm (DRURY, 2013).

Price optimisation system: Price optimisation system is used to set prices of products

used by companies so that company and customers both can be in profitable stage. Through

using this method, company can meet with its objectives like enhancing operational costs.

1

Management accounting refers to analysis of the financial data and the advice to

company for the use in business development. This process of analysing the operations as well as

business cost for the purpose of prepare the internal financial reports and records helps top

management in process of decision making to attain set business objectives. It is an act of

making the sense of costing and financial data and then translating it into useful information for

top management within company (Bouten and Hoozée, 2013). This present report is based on

Rolls-Royce Holdings that is an engineering firm, focus on world- class propulsion, and power

system. In this mention report will discussed about the management accounting and essential

requirements of different types of systems. Benefits and disadvantages of different types of

planning tools, which are mainly used for the budgetary control, will discussed here.

DEMONSTRATE UNDERSTANDING OF MANAGEMENT

ACCOUNTING SYSTEMS

Explain the management accounting and also explain needs of management accounting systems

Management accounting is mainly used through the managers for purpose of taking the

effective decision for performing business operation and control the different functions for

business productivity. It consists creation of the Management accounting reports to give accurate

information to formulate short term as well as long-term plans for achieving company objectives

(Cadez and Guilding, 2012). For assure that work is to be performed according to planned

activities, there are different kinds of accounting system mention below:

Cost accounting system: It is a kind of Management Accounting system that is mainly

used by managers for the purpose of recording activities tracking materials and examining the

production cost at various production phrases from the raw material to finish. This system aids in

approximation associated cost for measuring profit level valuation of inventory and controlling

cost. Rolls-Royce applies this system for examining the different cost at every product stage and

focus on the products, which will be benefited, more to firm (DRURY, 2013).

Price optimisation system: Price optimisation system is used to set prices of products

used by companies so that company and customers both can be in profitable stage. Through

using this method, company can meet with its objectives like enhancing operational costs.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management system: It is mainly used for production manager in order to

track the status of the current and needed stock for performing the business operations. It helps in

reducing the situation such as under stock and over stock of inventory at workplace. In context to

Rolls Royce, Inventory management system is mainly used for purpose of looking stock at the

warehousing as well as Shipping in order to track the outgoing and incoming products through

using supply chain management.

Management accounting reporting: The management accounting reports produces reports for

internal stakeholders of an organization as opposed to external stakeholders. It helps in providing

the accurate statistically and financial account records in proper time to management for purpose

of making short- term decisions (Fullerton, Kennedy and Widener, 2014). Different management

reports are given below:

Budget reports: This is formal statement and estimation of the revenue and expenditure.

This report is mainly prepare for future purpose to attain the business goal. On the other hand, it

can be prepared for the long-term and short-term purpose. It is effective for the performance

measurement and planning purpose and helpful in take necessary decision regarding growth of

firm. As Rolls-Royce, develop budget in order to anticipate the expenses as well as income for

the future and helpful in take the business decisions for the purpose of Business expansion

(Herzig and et. al., 2012).

Account receivable ageing report: This kind of report is developed by company under

which management records the details of those customers which buy product on credit basis.

This kind of report is mainly developed through those organisations, which perform trading in

credit that traits are clearly mentioned with name and other details related to credit transactions.

Rolls-Royce develop this kind of report through gathering information for identifying the

invoices, which are due for the payment purpose (Hiebl, 2014). This is mainly used for

management in order to examining potential of bad debts and this is revised for doubtful

accounts.

Evaluation of benefits of various management accounting systems

The benefits of different Management Accounting system mention below:

Advantages of cost accounting system- The main benefit of cost accounting system is

to measure expenses and the cost. It allows an organisation to measure efficiency of business.

Another benefit of this system is that it can help in identify unprofitable activities of business.

2

track the status of the current and needed stock for performing the business operations. It helps in

reducing the situation such as under stock and over stock of inventory at workplace. In context to

Rolls Royce, Inventory management system is mainly used for purpose of looking stock at the

warehousing as well as Shipping in order to track the outgoing and incoming products through

using supply chain management.

Management accounting reporting: The management accounting reports produces reports for

internal stakeholders of an organization as opposed to external stakeholders. It helps in providing

the accurate statistically and financial account records in proper time to management for purpose

of making short- term decisions (Fullerton, Kennedy and Widener, 2014). Different management

reports are given below:

Budget reports: This is formal statement and estimation of the revenue and expenditure.

This report is mainly prepare for future purpose to attain the business goal. On the other hand, it

can be prepared for the long-term and short-term purpose. It is effective for the performance

measurement and planning purpose and helpful in take necessary decision regarding growth of

firm. As Rolls-Royce, develop budget in order to anticipate the expenses as well as income for

the future and helpful in take the business decisions for the purpose of Business expansion

(Herzig and et. al., 2012).

Account receivable ageing report: This kind of report is developed by company under

which management records the details of those customers which buy product on credit basis.

This kind of report is mainly developed through those organisations, which perform trading in

credit that traits are clearly mentioned with name and other details related to credit transactions.

Rolls-Royce develop this kind of report through gathering information for identifying the

invoices, which are due for the payment purpose (Hiebl, 2014). This is mainly used for

management in order to examining potential of bad debts and this is revised for doubtful

accounts.

Evaluation of benefits of various management accounting systems

The benefits of different Management Accounting system mention below:

Advantages of cost accounting system- The main benefit of cost accounting system is

to measure expenses and the cost. It allows an organisation to measure efficiency of business.

Another benefit of this system is that it can help in identify unprofitable activities of business.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages of price optimisation system- It gives benefit of identifying the reliable

cost of business product and services in open markets. In identifying the price level, which can

provide advantage to consumer as well, as firms (Kaplan and Atkinson, 2015). This kind of

system is helpful for the business manager of Rolls-Royce in assigning the accurate cost of

ensuring product through considering customers’ perception towards cost.

Advantages of inventory management system- It is helpful in eliminating the excess

wastage and the overstocking of products. This kind of system gives status of the present along

with necessary inventory for eliminating today’s in completion of the project. It enables firm to

maintain centralized record of each assets.

Management accounting system and the reporting integration within organisational processes

Management accounting reports and systems both are interrelated within organisational

processes. It consists various systems like cost price optimisation system, accounting system,

job-costing system etc. All these systems play an essential role for developing the management

accounting reports through giving financial and non-financial information. If these systems fail

in give necessary information then it will be complex for management to develop management

accounting reports. Financial managers of Rolls-Royce uses the management accounting systems

for preparing management accounting reports through using different techniques. Under this,

Accounting systems minimize complexities for better composition of reports (Hilton and Platt,

2013).

PART B

ANNEX (A)

Marginal costing method- It refers to cost that change in total cost when quality

manufactured in incremented through even one unit. It is known as one of the principle costing

methods that are mainly used through mangers in process of decision-making.

Absorption costing method- This method entails full cost of the manufacturing and

offering service (Lukka and Vinnari, 2014).

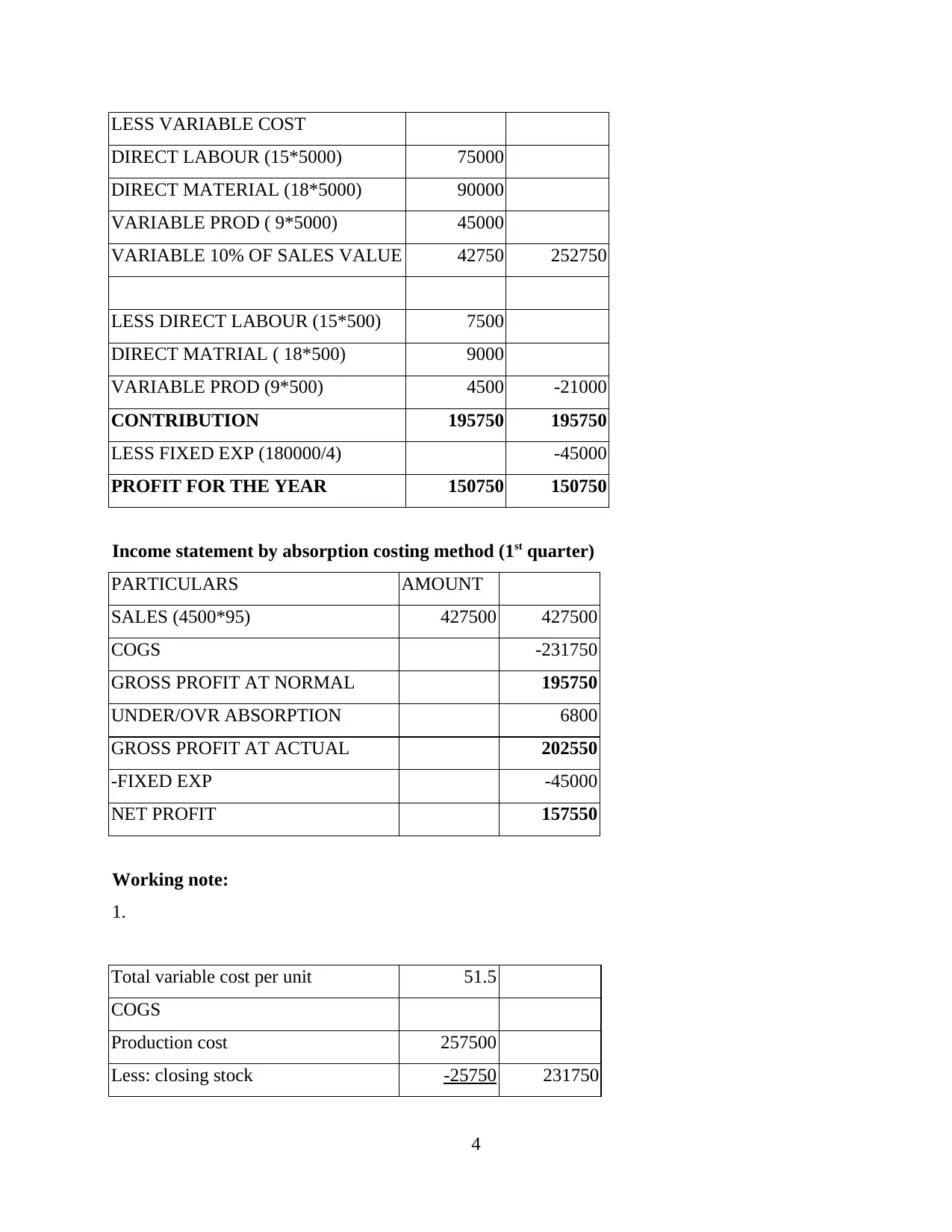

Income statement by marginal costing method:

PARTICULARS AMOUNT

SALES 427500 427500

3

cost of business product and services in open markets. In identifying the price level, which can

provide advantage to consumer as well, as firms (Kaplan and Atkinson, 2015). This kind of

system is helpful for the business manager of Rolls-Royce in assigning the accurate cost of

ensuring product through considering customers’ perception towards cost.

Advantages of inventory management system- It is helpful in eliminating the excess

wastage and the overstocking of products. This kind of system gives status of the present along

with necessary inventory for eliminating today’s in completion of the project. It enables firm to

maintain centralized record of each assets.

Management accounting system and the reporting integration within organisational processes

Management accounting reports and systems both are interrelated within organisational

processes. It consists various systems like cost price optimisation system, accounting system,

job-costing system etc. All these systems play an essential role for developing the management

accounting reports through giving financial and non-financial information. If these systems fail

in give necessary information then it will be complex for management to develop management

accounting reports. Financial managers of Rolls-Royce uses the management accounting systems

for preparing management accounting reports through using different techniques. Under this,

Accounting systems minimize complexities for better composition of reports (Hilton and Platt,

2013).

PART B

ANNEX (A)

Marginal costing method- It refers to cost that change in total cost when quality

manufactured in incremented through even one unit. It is known as one of the principle costing

methods that are mainly used through mangers in process of decision-making.

Absorption costing method- This method entails full cost of the manufacturing and

offering service (Lukka and Vinnari, 2014).

Income statement by marginal costing method:

PARTICULARS AMOUNT

SALES 427500 427500

3

LESS VARIABLE COST

DIRECT LABOUR (15*5000) 75000

DIRECT MATERIAL (18*5000) 90000

VARIABLE PROD ( 9*5000) 45000

VARIABLE 10% OF SALES VALUE 42750 252750

LESS DIRECT LABOUR (15*500) 7500

DIRECT MATRIAL ( 18*500) 9000

VARIABLE PROD (9*500) 4500 -21000

CONTRIBUTION 195750 195750

LESS FIXED EXP (180000/4) -45000

PROFIT FOR THE YEAR 150750 150750

Income statement by absorption costing method (1st quarter)

PARTICULARS AMOUNT

SALES (4500*95) 427500 427500

COGS -231750

GROSS PROFIT AT NORMAL 195750

UNDER/OVR ABSORPTION 6800

GROSS PROFIT AT ACTUAL 202550

-FIXED EXP -45000

NET PROFIT 157550

Working note:

1.

Total variable cost per unit 51.5

COGS

Production cost 257500

Less: closing stock -25750 231750

4

DIRECT LABOUR (15*5000) 75000

DIRECT MATERIAL (18*5000) 90000

VARIABLE PROD ( 9*5000) 45000

VARIABLE 10% OF SALES VALUE 42750 252750

LESS DIRECT LABOUR (15*500) 7500

DIRECT MATRIAL ( 18*500) 9000

VARIABLE PROD (9*500) 4500 -21000

CONTRIBUTION 195750 195750

LESS FIXED EXP (180000/4) -45000

PROFIT FOR THE YEAR 150750 150750

Income statement by absorption costing method (1st quarter)

PARTICULARS AMOUNT

SALES (4500*95) 427500 427500

COGS -231750

GROSS PROFIT AT NORMAL 195750

UNDER/OVR ABSORPTION 6800

GROSS PROFIT AT ACTUAL 202550

-FIXED EXP -45000

NET PROFIT 157550

Working note:

1.

Total variable cost per unit 51.5

COGS

Production cost 257500

Less: closing stock -25750 231750

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

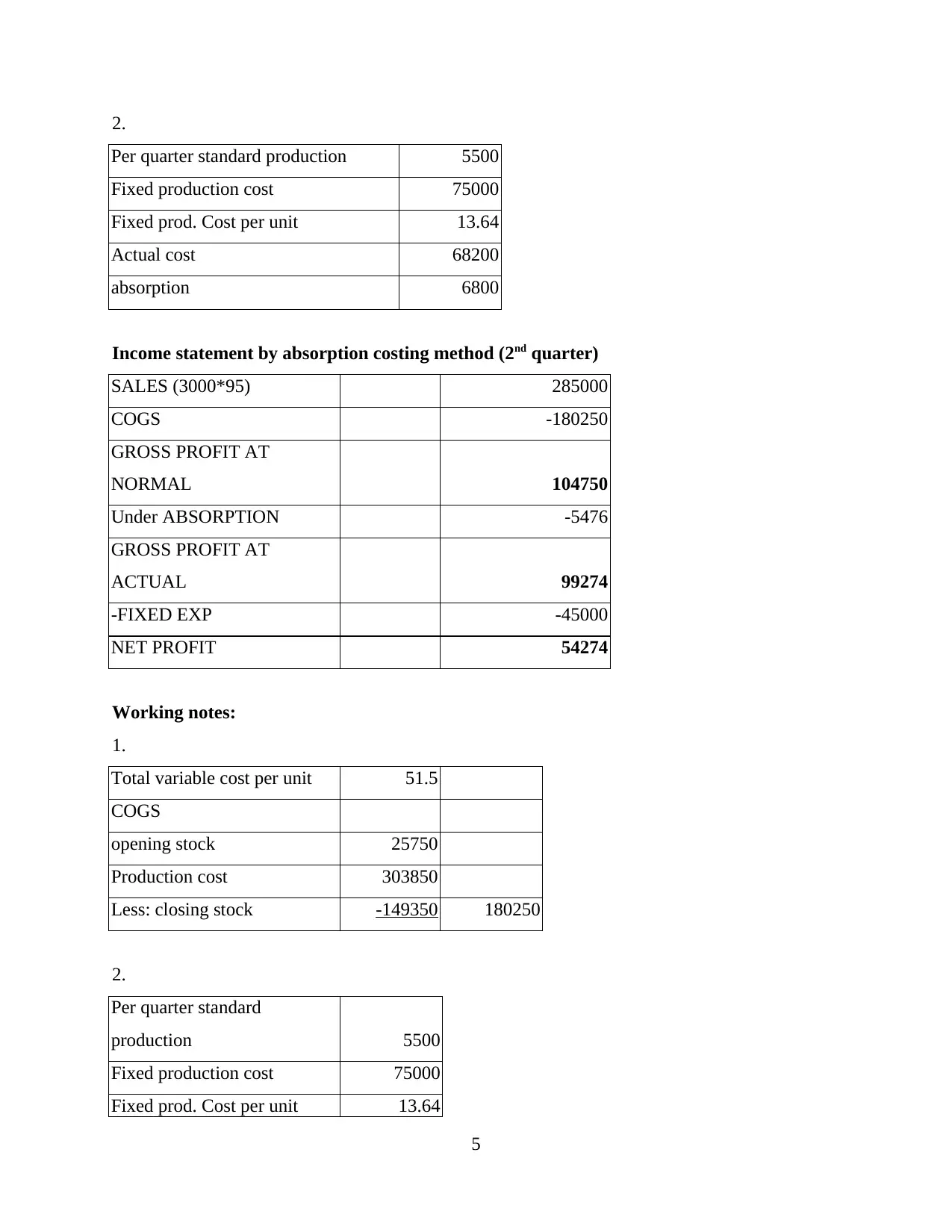

2.

Per quarter standard production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 68200

absorption 6800

Income statement by absorption costing method (2nd quarter)

SALES (3000*95) 285000

COGS -180250

GROSS PROFIT AT

NORMAL 104750

Under ABSORPTION -5476

GROSS PROFIT AT

ACTUAL 99274

-FIXED EXP -45000

NET PROFIT 54274

Working notes:

1.

Total variable cost per unit 51.5

COGS

opening stock 25750

Production cost 303850

Less: closing stock -149350 180250

2.

Per quarter standard

production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

5

Per quarter standard production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 68200

absorption 6800

Income statement by absorption costing method (2nd quarter)

SALES (3000*95) 285000

COGS -180250

GROSS PROFIT AT

NORMAL 104750

Under ABSORPTION -5476

GROSS PROFIT AT

ACTUAL 99274

-FIXED EXP -45000

NET PROFIT 54274

Working notes:

1.

Total variable cost per unit 51.5

COGS

opening stock 25750

Production cost 303850

Less: closing stock -149350 180250

2.

Per quarter standard

production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

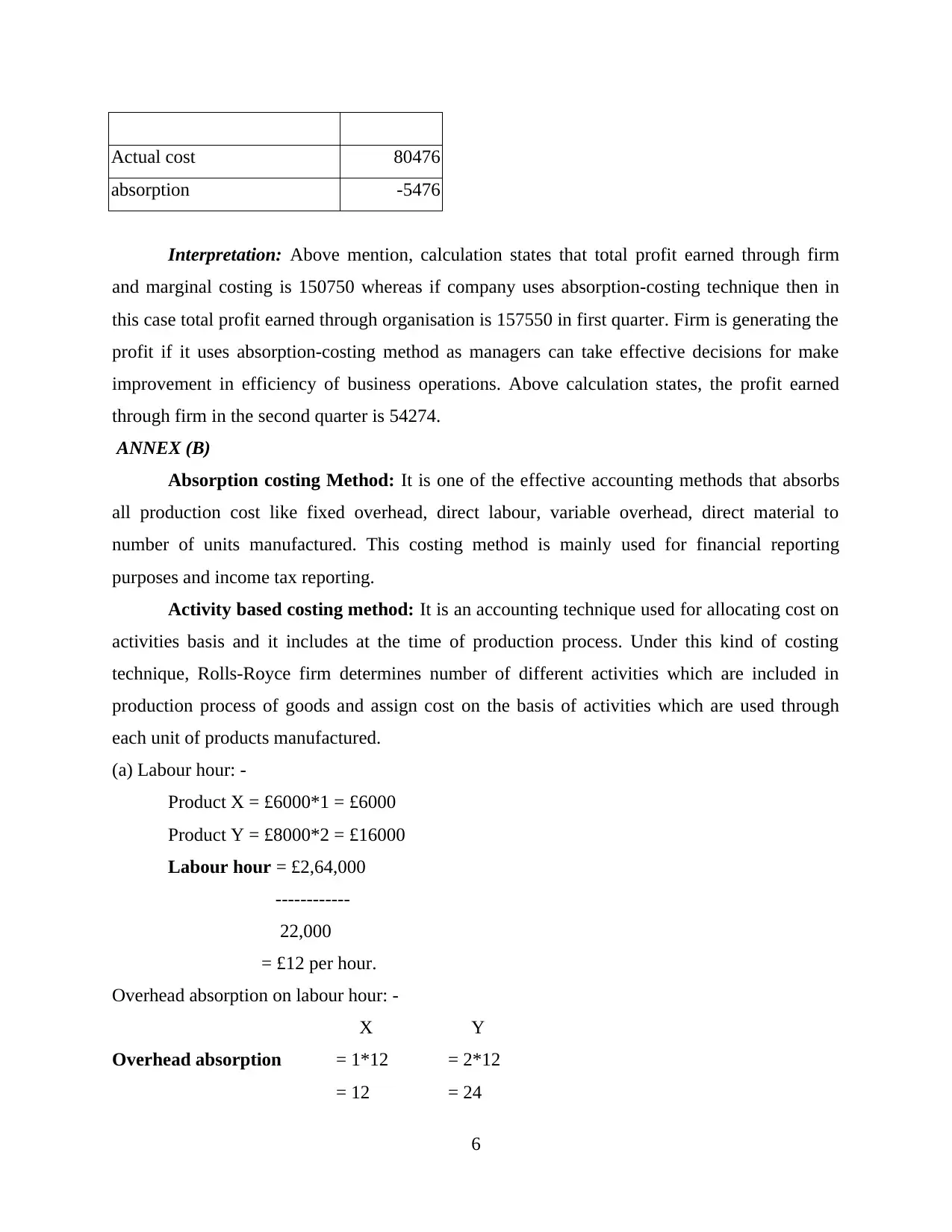

Actual cost 80476

absorption -5476

Interpretation: Above mention, calculation states that total profit earned through firm

and marginal costing is 150750 whereas if company uses absorption-costing technique then in

this case total profit earned through organisation is 157550 in first quarter. Firm is generating the

profit if it uses absorption-costing method as managers can take effective decisions for make

improvement in efficiency of business operations. Above calculation states, the profit earned

through firm in the second quarter is 54274.

ANNEX (B)

Absorption costing Method: It is one of the effective accounting methods that absorbs

all production cost like fixed overhead, direct labour, variable overhead, direct material to

number of units manufactured. This costing method is mainly used for financial reporting

purposes and income tax reporting.

Activity based costing method: It is an accounting technique used for allocating cost on

activities basis and it includes at the time of production process. Under this kind of costing

technique, Rolls-Royce firm determines number of different activities which are included in

production process of goods and assign cost on the basis of activities which are used through

each unit of products manufactured.

(a) Labour hour: -

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

6

absorption -5476

Interpretation: Above mention, calculation states that total profit earned through firm

and marginal costing is 150750 whereas if company uses absorption-costing technique then in

this case total profit earned through organisation is 157550 in first quarter. Firm is generating the

profit if it uses absorption-costing method as managers can take effective decisions for make

improvement in efficiency of business operations. Above calculation states, the profit earned

through firm in the second quarter is 54274.

ANNEX (B)

Absorption costing Method: It is one of the effective accounting methods that absorbs

all production cost like fixed overhead, direct labour, variable overhead, direct material to

number of units manufactured. This costing method is mainly used for financial reporting

purposes and income tax reporting.

Activity based costing method: It is an accounting technique used for allocating cost on

activities basis and it includes at the time of production process. Under this kind of costing

technique, Rolls-Royce firm determines number of different activities which are included in

production process of goods and assign cost on the basis of activities which are used through

each unit of products manufactured.

(a) Labour hour: -

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

6

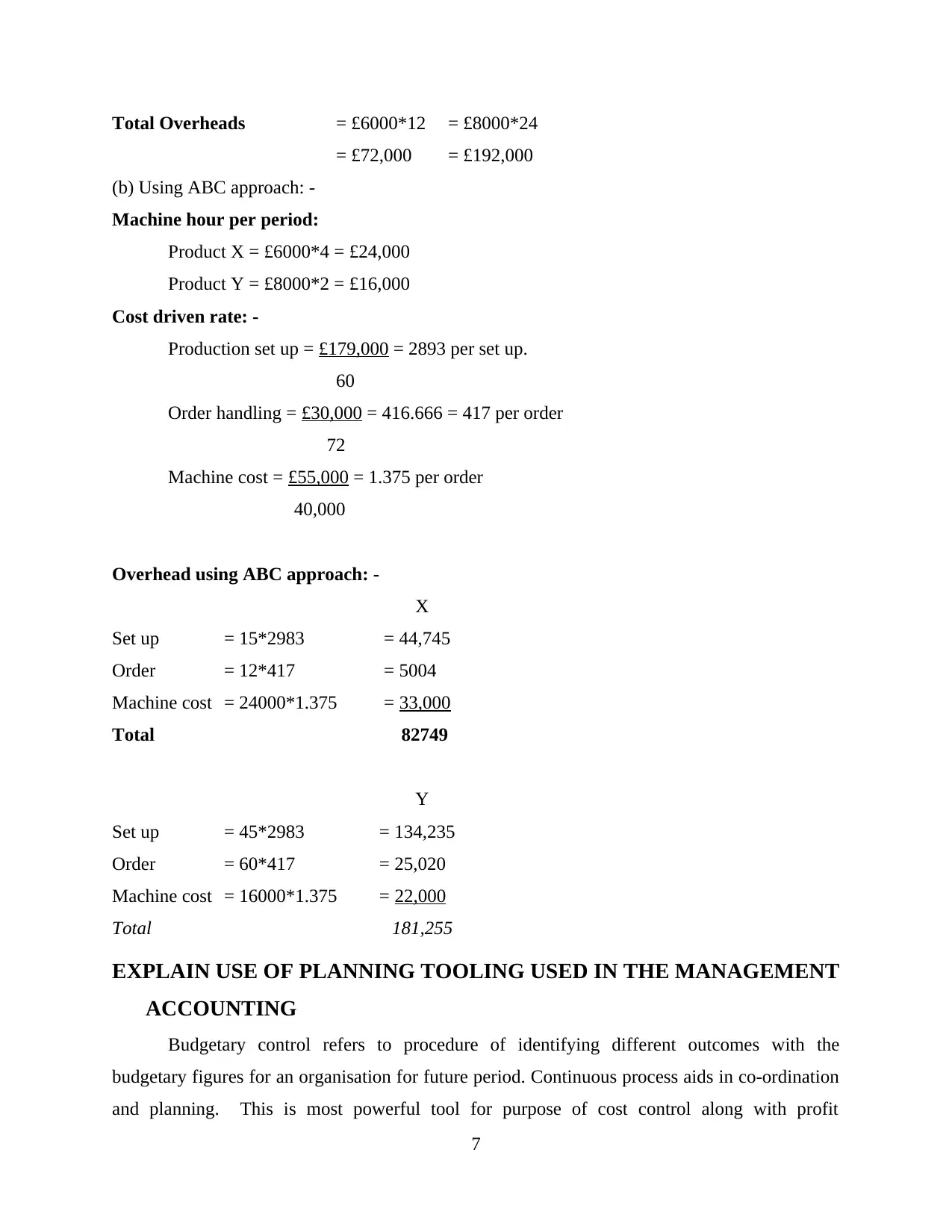

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

EXPLAIN USE OF PLANNING TOOLING USED IN THE MANAGEMENT

ACCOUNTING

Budgetary control refers to procedure of identifying different outcomes with the

budgetary figures for an organisation for future period. Continuous process aids in co-ordination

and planning. This is most powerful tool for purpose of cost control along with profit

7

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

EXPLAIN USE OF PLANNING TOOLING USED IN THE MANAGEMENT

ACCOUNTING

Budgetary control refers to procedure of identifying different outcomes with the

budgetary figures for an organisation for future period. Continuous process aids in co-ordination

and planning. This is most powerful tool for purpose of cost control along with profit

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

maximisation. It is a procedure of preparing of budgets for different activities and then

comparing budgeted figures for arriving at deviations. Continuous process aids in coordination

and planning. It plays a necessary role to aid senior management in order to operating as well as

monitoring the operations of business in better way for attaining objectives. The manager of

Rolls-Royce use various types of planning tools for purpose of framing financial and non-

financial objectives. The benefits and disadvantages of various kinds of planning tools, which are

mainly used for the budgetary control, are given below:

Flexible budgets: This type of tool helps managers to examining any deviations between

expected output and actual output for doing some modifications in the budget statements at time

they occurs (Maas, Schaltegger and Crutzen, 2016). Financial managers are responsible for

Rolls-Royce Company to use flexible budgets for adjusts modifications in statements concerned

to alterations in tasks which can help in provide desired outcomes.

Advantages

Flexible budget makes this possible to establish the budget cost for any activity level

within relevant range. It aids in measuring effects of different activities volumes on cash position and profits.

Disadvantages

Flexible budget tends to maintain the fixed cost at same output level. (Morales and

Lambert, 2013).

As activities while developing the flexible budgets there is fluctuation with changes in

outcomes. It is complex for the financial managers of Rolls-Royce to handle every

variable.

Incremental budget: This budget is mainly used for developing budget of current year

through developing any kind of changes in budget of the previous year. Last year budget is

generally used for getting better ideas which are concerned with the current performance (Otley

and Emmanuel, 2013). Rolls-Royce managers applies these budget for the purpose of arrive at

new budget through make changing the past budget.

Advantages

This budget provides advantages to company to reduce any excess expenses in current

year budget.

8

comparing budgeted figures for arriving at deviations. Continuous process aids in coordination

and planning. It plays a necessary role to aid senior management in order to operating as well as

monitoring the operations of business in better way for attaining objectives. The manager of

Rolls-Royce use various types of planning tools for purpose of framing financial and non-

financial objectives. The benefits and disadvantages of various kinds of planning tools, which are

mainly used for the budgetary control, are given below:

Flexible budgets: This type of tool helps managers to examining any deviations between

expected output and actual output for doing some modifications in the budget statements at time

they occurs (Maas, Schaltegger and Crutzen, 2016). Financial managers are responsible for

Rolls-Royce Company to use flexible budgets for adjusts modifications in statements concerned

to alterations in tasks which can help in provide desired outcomes.

Advantages

Flexible budget makes this possible to establish the budget cost for any activity level

within relevant range. It aids in measuring effects of different activities volumes on cash position and profits.

Disadvantages

Flexible budget tends to maintain the fixed cost at same output level. (Morales and

Lambert, 2013).

As activities while developing the flexible budgets there is fluctuation with changes in

outcomes. It is complex for the financial managers of Rolls-Royce to handle every

variable.

Incremental budget: This budget is mainly used for developing budget of current year

through developing any kind of changes in budget of the previous year. Last year budget is

generally used for getting better ideas which are concerned with the current performance (Otley

and Emmanuel, 2013). Rolls-Royce managers applies these budget for the purpose of arrive at

new budget through make changing the past budget.

Advantages

This budget provides advantages to company to reduce any excess expenses in current

year budget.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It does not need specific qualifications to prepare this budget. Person can develop

incremental budget through understanding previous budgets.

Disadvantages

The estimations are mainly used in previous year budget, which may not be certain in

current year budget.

It consists more spending in order to obtain the favourable variables for existing

budgeting of transactions of organisation (Parker, 2012).

Contingency planning tool: It is mainly used for the purpose of managing unexpected

conditions at the time of performing any activities for attains the business outcomes. Such tool

aids for Rolls-Royce in developing as well as executing plans, actions and strategies in order to

deal with risky and unfavourable conditions, which are arising at workplace.

Advantages

Through this tool, managers of Rolls-Royce can address issues quickly for reducing any

risks to attain the desired outcomes. Contingency planning tool provide the benefits through searching unfavourable

conditions and take corrective actions for minimise any kind of hurdles.

Disadvantages

The actions taken are not helpful to get over from situations because of adequacy of

knowledge for better understand arisen situations.

It is more time taking and reactive procedure that can develop negative impact on

business.

Use of various planning tools and their application

In decision-making process, planning tools plays a most necessary role. It aids

management of Rolls-Royce to take important decision for make improvement in business

operations in significant way for earn high profit. With the help of this, company can retain at

market place for long period and make improvement in its financial position (Renz, 2016). There

are many different planning tools for an instance Incremental budget, Flexible budgets and

Contingency planning tool, which aids management to examine its past performance and search

problems. The issues can be related to the financial and market position of company. The

manager of Rolls-Royce firm uses its past budget for preparing the new strategies for maximise

9

incremental budget through understanding previous budgets.

Disadvantages

The estimations are mainly used in previous year budget, which may not be certain in

current year budget.

It consists more spending in order to obtain the favourable variables for existing

budgeting of transactions of organisation (Parker, 2012).

Contingency planning tool: It is mainly used for the purpose of managing unexpected

conditions at the time of performing any activities for attains the business outcomes. Such tool

aids for Rolls-Royce in developing as well as executing plans, actions and strategies in order to

deal with risky and unfavourable conditions, which are arising at workplace.

Advantages

Through this tool, managers of Rolls-Royce can address issues quickly for reducing any

risks to attain the desired outcomes. Contingency planning tool provide the benefits through searching unfavourable

conditions and take corrective actions for minimise any kind of hurdles.

Disadvantages

The actions taken are not helpful to get over from situations because of adequacy of

knowledge for better understand arisen situations.

It is more time taking and reactive procedure that can develop negative impact on

business.

Use of various planning tools and their application

In decision-making process, planning tools plays a most necessary role. It aids

management of Rolls-Royce to take important decision for make improvement in business

operations in significant way for earn high profit. With the help of this, company can retain at

market place for long period and make improvement in its financial position (Renz, 2016). There

are many different planning tools for an instance Incremental budget, Flexible budgets and

Contingency planning tool, which aids management to examine its past performance and search

problems. The issues can be related to the financial and market position of company. The

manager of Rolls-Royce firm uses its past budget for preparing the new strategies for maximise

9

profitability of company and make some improvement in its market position. Planning tools are

helpful for to develop better road map for attain the organisational objectives.

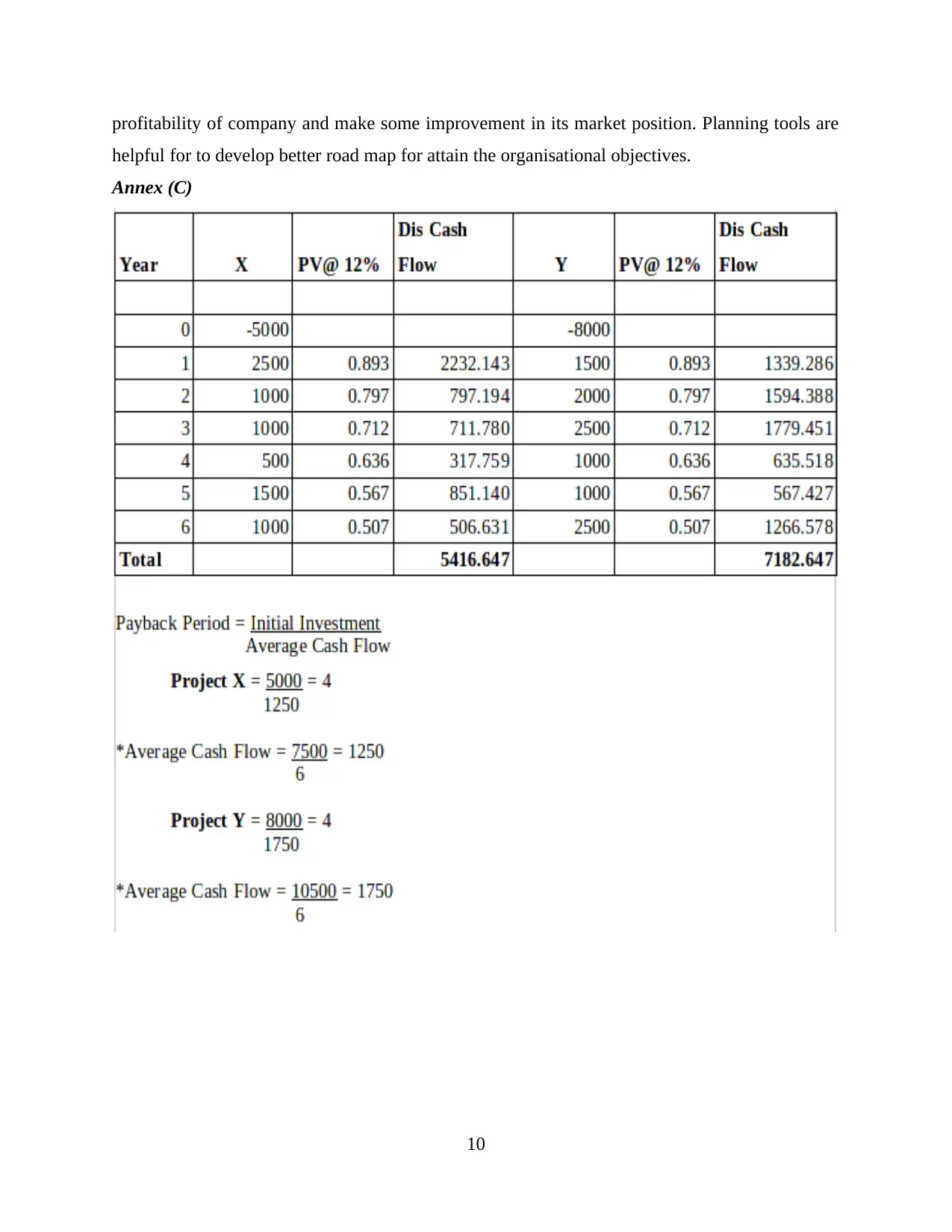

Annex (C)

10

helpful for to develop better road map for attain the organisational objectives.

Annex (C)

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.