Management Accounting Report: Costing Techniques, Planning Tools

VerifiedAdded on 2023/01/19

|20

|5307

|57

Report

AI Summary

This report delves into the realm of management accounting, focusing on its application within Rolls Royce, a prominent car manufacturing company. The report comprehensively examines various management accounting systems, including inventory management, price optimization, job order costing, and cost accounting, and their significance in assessing business costs and operational activities. It further explores diverse reporting methods like performance, budget, account receivable, and inventory management reports. The report showcases the practical application of costing techniques, specifically marginal and absorption costing, through detailed income statements, and provides a comparative analysis of their impact on profitability. Additionally, it evaluates different planning tools employed in budgetary control, highlighting their advantages and disadvantages. The report also compares how different organizations implement management accounting systems to address financial challenges, thereby offering a holistic understanding of management accounting's role in strategic decision-making and financial performance evaluation. The analysis covers the integration of accounting systems and reports within an organizational context. The report concludes with recommendations for Rolls Royce on the use of costing techniques.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

Explaining different systems of management accounting and their requirements......................1

Various methods of reporting which are used in management accounting.................................2

LO 2.................................................................................................................................................5

Using costing techniques to prepare income statement...............................................................5

LO 3.................................................................................................................................................9

Different planning tools used in budgetary control with their advantages and disadvantages....9

LO 4...............................................................................................................................................11

Comparison of different organisations on the basis of the ways in which they implement

management accounting system to resolve financial problems.................................................11

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

APPENDIX (P3)............................................................................................................................17

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

Explaining different systems of management accounting and their requirements......................1

Various methods of reporting which are used in management accounting.................................2

LO 2.................................................................................................................................................5

Using costing techniques to prepare income statement...............................................................5

LO 3.................................................................................................................................................9

Different planning tools used in budgetary control with their advantages and disadvantages....9

LO 4...............................................................................................................................................11

Comparison of different organisations on the basis of the ways in which they implement

management accounting system to resolve financial problems.................................................11

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

APPENDIX (P3)............................................................................................................................17

INTRODUCTION

Management accounting is a procedure which is focused by managers of companies in

order to evaluate actual performance the business. Main purpose of it is to guide internal

stakeholders such as employees, managers etc. to analyse that business's position is good or not.

If an entity is ignoring it then it can affect the formulating of accurate reports on insider activities

(Abdel-Maksoud, Cheffi and Ghoudi, 2016). The enterprise which is selected for this report is

Rolls Royce. It is one of the major car manufacturing companies which are established in United

Kingdom and selling its products in national as well as international market. This assignment

covers various topics which includes detailed analysis of management accounting, its systems

and reporting, application of costing techniques, advantages and disadvantages of planning tools

used in budgetary control. Apart from this, comparison of two companies on the basis of using

management accounting to respond financial issues is also covered in this project.

LO1

Explaining different systems of management accounting and their requirements

Management accounting: It can be explained as the technique which is utilised by

managers of the organisations for the purpose of assessing business costs and operational

activities so that financial reports could be prepared for future (Arunruangsirilert and

Chonglerttham, 2017). Managers in Rolls Royce also pay attention towards it so that higher level

of accuracy could be provided to internal stakeholders with the help of management reports.

Management accounting systems: It is the combination of internal systems of the

organisation so that all the processes and procedures of management could be measured and

evaluated (Ghasemi, R. and et.al., 2016). Top level executives of Rolls Royce guide managers to

follow some of them that may help to collect appropriate data. These are analysed underneath:

Inventory management system: The method which is mainly concerned with

monitoring and recording of information related to stock used for carrying out operations is

known as inventory management system. For organisations such as Rolls Royce it is very

important to use it because it helps to keep detailed information about goods which are utilised

for business processes. It is required for the company as with the help of it managers will be able

to check that inventory is needed for operational activities or not. Three different kinds of it are

discussed below:

1

Management accounting is a procedure which is focused by managers of companies in

order to evaluate actual performance the business. Main purpose of it is to guide internal

stakeholders such as employees, managers etc. to analyse that business's position is good or not.

If an entity is ignoring it then it can affect the formulating of accurate reports on insider activities

(Abdel-Maksoud, Cheffi and Ghoudi, 2016). The enterprise which is selected for this report is

Rolls Royce. It is one of the major car manufacturing companies which are established in United

Kingdom and selling its products in national as well as international market. This assignment

covers various topics which includes detailed analysis of management accounting, its systems

and reporting, application of costing techniques, advantages and disadvantages of planning tools

used in budgetary control. Apart from this, comparison of two companies on the basis of using

management accounting to respond financial issues is also covered in this project.

LO1

Explaining different systems of management accounting and their requirements

Management accounting: It can be explained as the technique which is utilised by

managers of the organisations for the purpose of assessing business costs and operational

activities so that financial reports could be prepared for future (Arunruangsirilert and

Chonglerttham, 2017). Managers in Rolls Royce also pay attention towards it so that higher level

of accuracy could be provided to internal stakeholders with the help of management reports.

Management accounting systems: It is the combination of internal systems of the

organisation so that all the processes and procedures of management could be measured and

evaluated (Ghasemi, R. and et.al., 2016). Top level executives of Rolls Royce guide managers to

follow some of them that may help to collect appropriate data. These are analysed underneath:

Inventory management system: The method which is mainly concerned with

monitoring and recording of information related to stock used for carrying out operations is

known as inventory management system. For organisations such as Rolls Royce it is very

important to use it because it helps to keep detailed information about goods which are utilised

for business processes. It is required for the company as with the help of it managers will be able

to check that inventory is needed for operational activities or not. Three different kinds of it are

discussed below:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AVCO (Average Cost Method): In this system all the inventory is used for business

activities on the basis of average cost.

LIFO (Last in First Out): This method guides managers to utilised recently acquired

goods for carrying out operations.

FIFO (First in First Out): This system demonstrate that if it is used by management

then they should use earlier bought material for manufacturing cars.

Managers in Rolls Royce are using first in first out method as it helps to utilise inventory

properly.

Price optimisation system: For all the organisations it is very important to set

appropriate price for all their products so that large number of customers could be attracted

toward the business. For this purpose, companies such as Rolls Royce apply this system which

helps to analyse responses of clients on different prices which could be set by them for their

goods. It also guides to set the right and most preferable rates for the cars engineered by them. It

is very important for the enterprises to use it because without it, it will be very difficult to figure

out that what price will be right for the products.

Job order costing: All the organisations perform different activities for carrying out

operations and to keep detailed track of all of them this system could be used. Management in

Rolls Royce are utilising it to accumulate and assign engineering costs to different units that are

manufactured by it. It is essential for the company to use it as it is required to segregate the

expenses on the basis of different jobs which are performed according to conditions of

patronages (Banham and He, 2014).

Cost accounting system: It can be defined as a framework which is focused for the

purpose of estimating costs of various items manufactured by the company. Rolls Royce's

managers are using it estimate the right cost which have taken place while engineering the cars

so that most profitable operations could be determined. It is very important for the management

to use it as with the help of it forecasting of future expenses could be performed.

Various methods of reporting which are used in management accounting

Management accounting reporting It is the process of generating management reports

so that all the activities of the organisations could be planned and regulated systematically. It is

also used in decision making and performance measuring (Weetman, 2019).

2

activities on the basis of average cost.

LIFO (Last in First Out): This method guides managers to utilised recently acquired

goods for carrying out operations.

FIFO (First in First Out): This system demonstrate that if it is used by management

then they should use earlier bought material for manufacturing cars.

Managers in Rolls Royce are using first in first out method as it helps to utilise inventory

properly.

Price optimisation system: For all the organisations it is very important to set

appropriate price for all their products so that large number of customers could be attracted

toward the business. For this purpose, companies such as Rolls Royce apply this system which

helps to analyse responses of clients on different prices which could be set by them for their

goods. It also guides to set the right and most preferable rates for the cars engineered by them. It

is very important for the enterprises to use it because without it, it will be very difficult to figure

out that what price will be right for the products.

Job order costing: All the organisations perform different activities for carrying out

operations and to keep detailed track of all of them this system could be used. Management in

Rolls Royce are utilising it to accumulate and assign engineering costs to different units that are

manufactured by it. It is essential for the company to use it as it is required to segregate the

expenses on the basis of different jobs which are performed according to conditions of

patronages (Banham and He, 2014).

Cost accounting system: It can be defined as a framework which is focused for the

purpose of estimating costs of various items manufactured by the company. Rolls Royce's

managers are using it estimate the right cost which have taken place while engineering the cars

so that most profitable operations could be determined. It is very important for the management

to use it as with the help of it forecasting of future expenses could be performed.

Various methods of reporting which are used in management accounting

Management accounting reporting It is the process of generating management reports

so that all the activities of the organisations could be planned and regulated systematically. It is

also used in decision making and performance measuring (Weetman, 2019).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

For all the business entities it is very important to formulate management reports so that

actual and accurate information about operational activities could be collected. The process

which if focused for the purpose of formulating them, is known as management accounting

reporting. If these are not formed by companies then it may affect the mindset of stakeholders

such as employees because they will not have any idea of that organisation in which they are

working. Different methods of performing this process are discussed underneath:

Performance report: Large as well as small organisations formulate different reports to

keep detailed information of performance of operations and staff members. It is also one of them

that helps management of companies such as Rolls Royce to analyse that business is showing

favourable results or not. With the help of it they can also get aware of efforts of employees to

attain organisational objectives. It is very beneficial for the enterprise because with the help of it,

it will be easy for management to offer rewards, bonuses and compensation to workforce

according to their performance (Guffey and Harp, 2016).

Budget report: Most of the organisations compare their actual and budgeted figures in

order to analyse that projected goals are achieved or not. This report is one of the major

documents which could be used for same purpose. Managers in Rolls Royce are using it to

maintain financial spendings according to requirements of different manufacturing activities.

This report may provide various benefits such as reduction in overspending of funds so it should

be created by management.

Account receivable report: For large and small companies which are offering credit to

the clients or retailers it is very important to keep detailed information of all the debtors. For the

purpose of recording this data account receivable report could be generated. It is one of the

primary tool which is used by managers of Rolls Royce so that they can calculate the due amount

of clients. This report is very beneficial for the company because it helps in the analysis of the

owed amount of clients and tighten credit policies so that the outstandings could be recovered on

time (Harrison and Lock, 2017).

Inventory management report: The companies which are operating business under

manufacturing sector it is very important to keep detailed information of stocks which are used

to carry out operations. It is formed by managers of Rolls Royce in order to get real time insight

into the movement of goods which are used to engineer cars. This report is advantageous for the

company because with the help of it management will be able to check the stock left on hand.

3

actual and accurate information about operational activities could be collected. The process

which if focused for the purpose of formulating them, is known as management accounting

reporting. If these are not formed by companies then it may affect the mindset of stakeholders

such as employees because they will not have any idea of that organisation in which they are

working. Different methods of performing this process are discussed underneath:

Performance report: Large as well as small organisations formulate different reports to

keep detailed information of performance of operations and staff members. It is also one of them

that helps management of companies such as Rolls Royce to analyse that business is showing

favourable results or not. With the help of it they can also get aware of efforts of employees to

attain organisational objectives. It is very beneficial for the enterprise because with the help of it,

it will be easy for management to offer rewards, bonuses and compensation to workforce

according to their performance (Guffey and Harp, 2016).

Budget report: Most of the organisations compare their actual and budgeted figures in

order to analyse that projected goals are achieved or not. This report is one of the major

documents which could be used for same purpose. Managers in Rolls Royce are using it to

maintain financial spendings according to requirements of different manufacturing activities.

This report may provide various benefits such as reduction in overspending of funds so it should

be created by management.

Account receivable report: For large and small companies which are offering credit to

the clients or retailers it is very important to keep detailed information of all the debtors. For the

purpose of recording this data account receivable report could be generated. It is one of the

primary tool which is used by managers of Rolls Royce so that they can calculate the due amount

of clients. This report is very beneficial for the company because it helps in the analysis of the

owed amount of clients and tighten credit policies so that the outstandings could be recovered on

time (Harrison and Lock, 2017).

Inventory management report: The companies which are operating business under

manufacturing sector it is very important to keep detailed information of stocks which are used

to carry out operations. It is formed by managers of Rolls Royce in order to get real time insight

into the movement of goods which are used to engineer cars. This report is advantageous for the

company because with the help of it management will be able to check the stock left on hand.

3

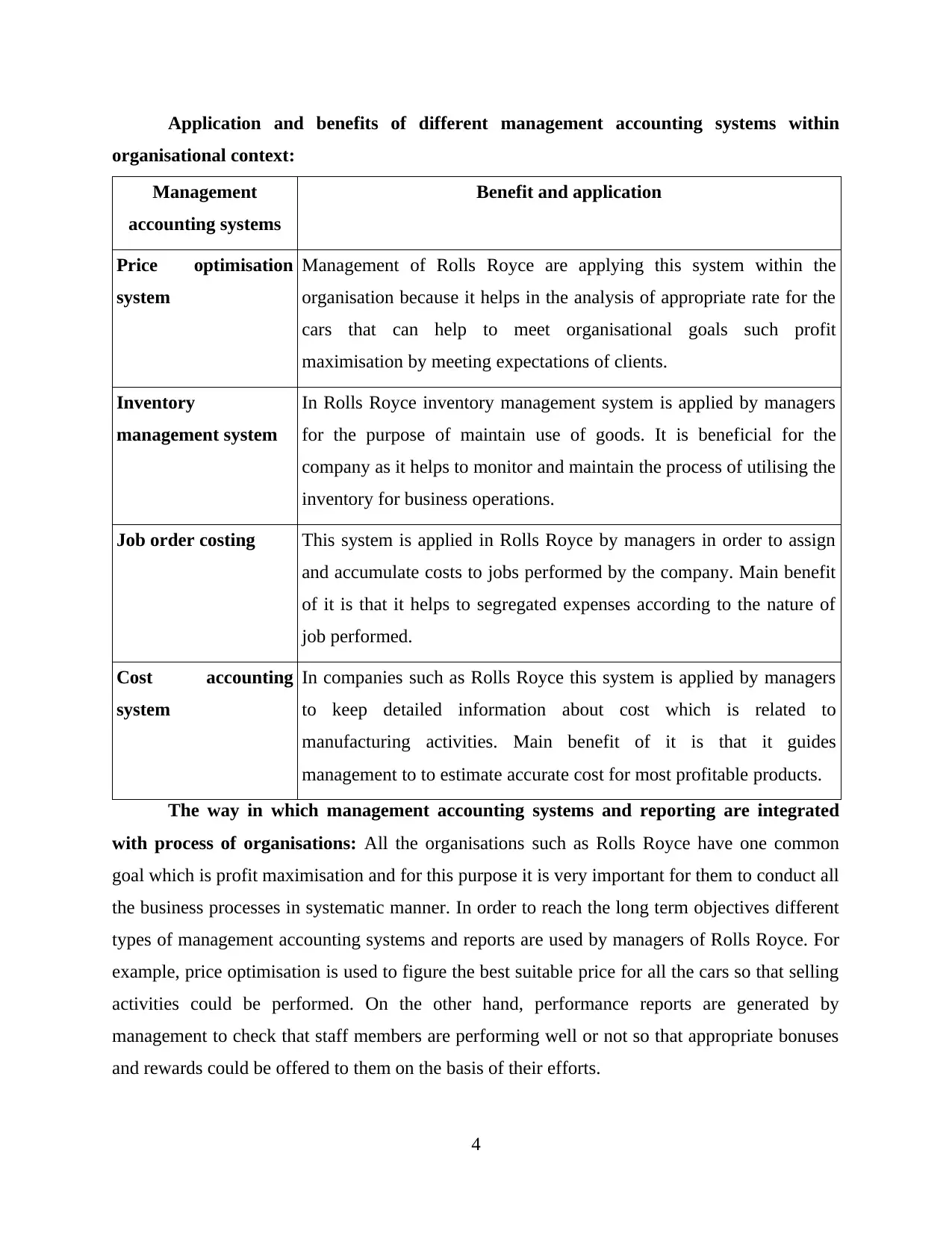

Application and benefits of different management accounting systems within

organisational context:

Management

accounting systems

Benefit and application

Price optimisation

system

Management of Rolls Royce are applying this system within the

organisation because it helps in the analysis of appropriate rate for the

cars that can help to meet organisational goals such profit

maximisation by meeting expectations of clients.

Inventory

management system

In Rolls Royce inventory management system is applied by managers

for the purpose of maintain use of goods. It is beneficial for the

company as it helps to monitor and maintain the process of utilising the

inventory for business operations.

Job order costing This system is applied in Rolls Royce by managers in order to assign

and accumulate costs to jobs performed by the company. Main benefit

of it is that it helps to segregated expenses according to the nature of

job performed.

Cost accounting

system

In companies such as Rolls Royce this system is applied by managers

to keep detailed information about cost which is related to

manufacturing activities. Main benefit of it is that it guides

management to to estimate accurate cost for most profitable products.

The way in which management accounting systems and reporting are integrated

with process of organisations: All the organisations such as Rolls Royce have one common

goal which is profit maximisation and for this purpose it is very important for them to conduct all

the business processes in systematic manner. In order to reach the long term objectives different

types of management accounting systems and reports are used by managers of Rolls Royce. For

example, price optimisation is used to figure the best suitable price for all the cars so that selling

activities could be performed. On the other hand, performance reports are generated by

management to check that staff members are performing well or not so that appropriate bonuses

and rewards could be offered to them on the basis of their efforts.

4

organisational context:

Management

accounting systems

Benefit and application

Price optimisation

system

Management of Rolls Royce are applying this system within the

organisation because it helps in the analysis of appropriate rate for the

cars that can help to meet organisational goals such profit

maximisation by meeting expectations of clients.

Inventory

management system

In Rolls Royce inventory management system is applied by managers

for the purpose of maintain use of goods. It is beneficial for the

company as it helps to monitor and maintain the process of utilising the

inventory for business operations.

Job order costing This system is applied in Rolls Royce by managers in order to assign

and accumulate costs to jobs performed by the company. Main benefit

of it is that it helps to segregated expenses according to the nature of

job performed.

Cost accounting

system

In companies such as Rolls Royce this system is applied by managers

to keep detailed information about cost which is related to

manufacturing activities. Main benefit of it is that it guides

management to to estimate accurate cost for most profitable products.

The way in which management accounting systems and reporting are integrated

with process of organisations: All the organisations such as Rolls Royce have one common

goal which is profit maximisation and for this purpose it is very important for them to conduct all

the business processes in systematic manner. In order to reach the long term objectives different

types of management accounting systems and reports are used by managers of Rolls Royce. For

example, price optimisation is used to figure the best suitable price for all the cars so that selling

activities could be performed. On the other hand, performance reports are generated by

management to check that staff members are performing well or not so that appropriate bonuses

and rewards could be offered to them on the basis of their efforts.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LO 2

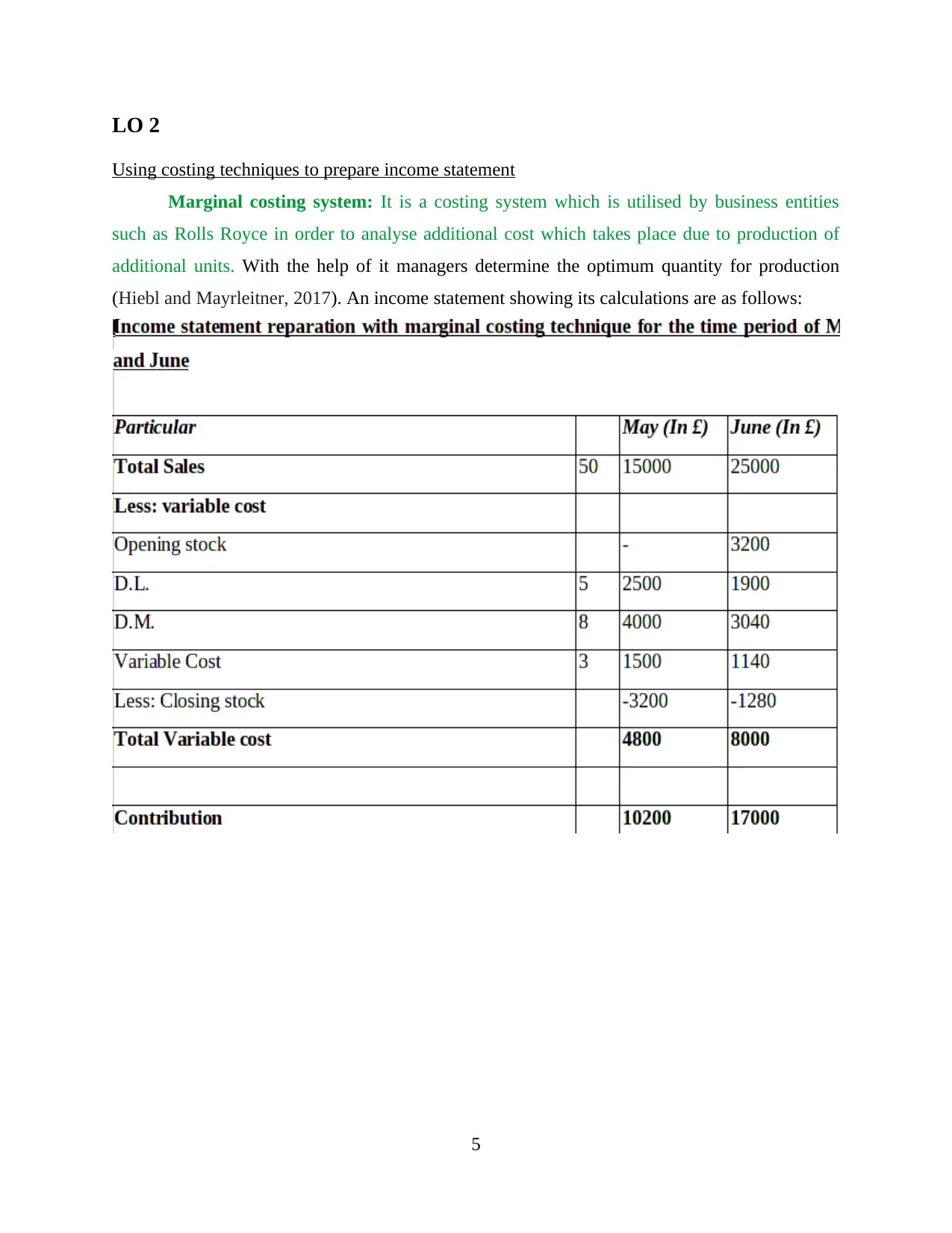

Using costing techniques to prepare income statement

Marginal costing system: It is a costing system which is utilised by business entities

such as Rolls Royce in order to analyse additional cost which takes place due to production of

additional units. With the help of it managers determine the optimum quantity for production

(Hiebl and Mayrleitner, 2017). An income statement showing its calculations are as follows:

5

Using costing techniques to prepare income statement

Marginal costing system: It is a costing system which is utilised by business entities

such as Rolls Royce in order to analyse additional cost which takes place due to production of

additional units. With the help of it managers determine the optimum quantity for production

(Hiebl and Mayrleitner, 2017). An income statement showing its calculations are as follows:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

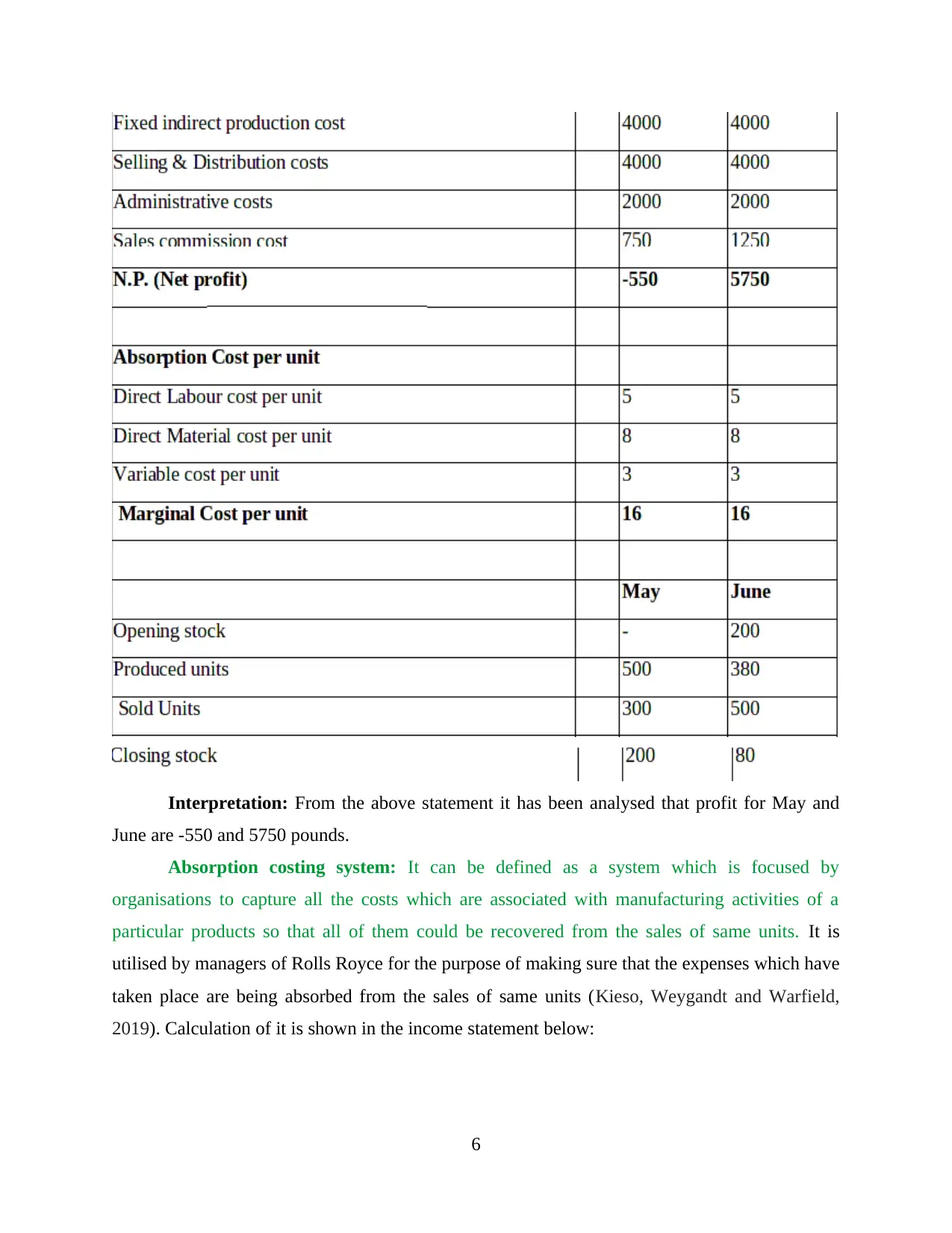

Interpretation: From the above statement it has been analysed that profit for May and

June are -550 and 5750 pounds.

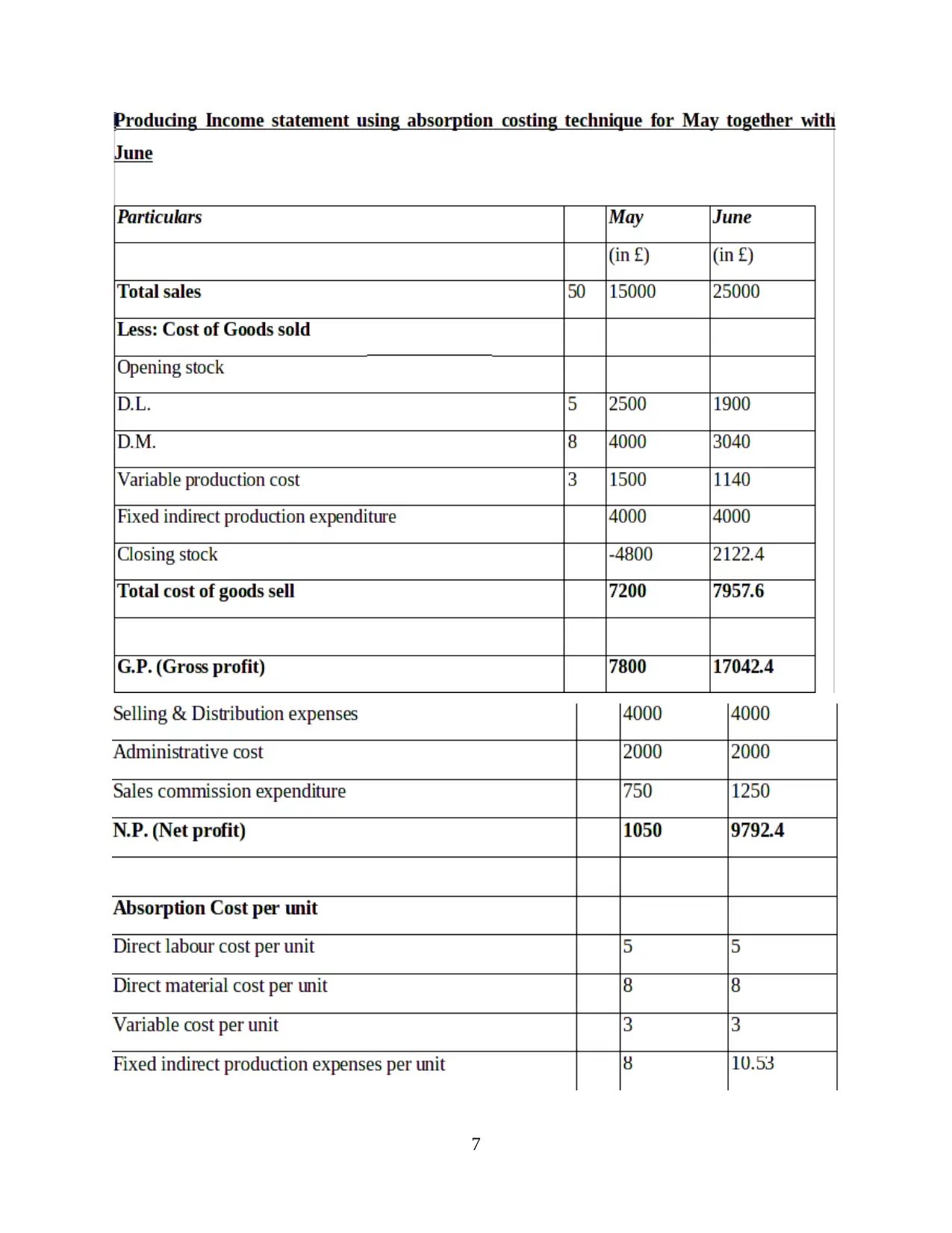

Absorption costing system: It can be defined as a system which is focused by

organisations to capture all the costs which are associated with manufacturing activities of a

particular products so that all of them could be recovered from the sales of same units. It is

utilised by managers of Rolls Royce for the purpose of making sure that the expenses which have

taken place are being absorbed from the sales of same units (Kieso, Weygandt and Warfield,

2019). Calculation of it is shown in the income statement below:

6

June are -550 and 5750 pounds.

Absorption costing system: It can be defined as a system which is focused by

organisations to capture all the costs which are associated with manufacturing activities of a

particular products so that all of them could be recovered from the sales of same units. It is

utilised by managers of Rolls Royce for the purpose of making sure that the expenses which have

taken place are being absorbed from the sales of same units (Kieso, Weygandt and Warfield,

2019). Calculation of it is shown in the income statement below:

6

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

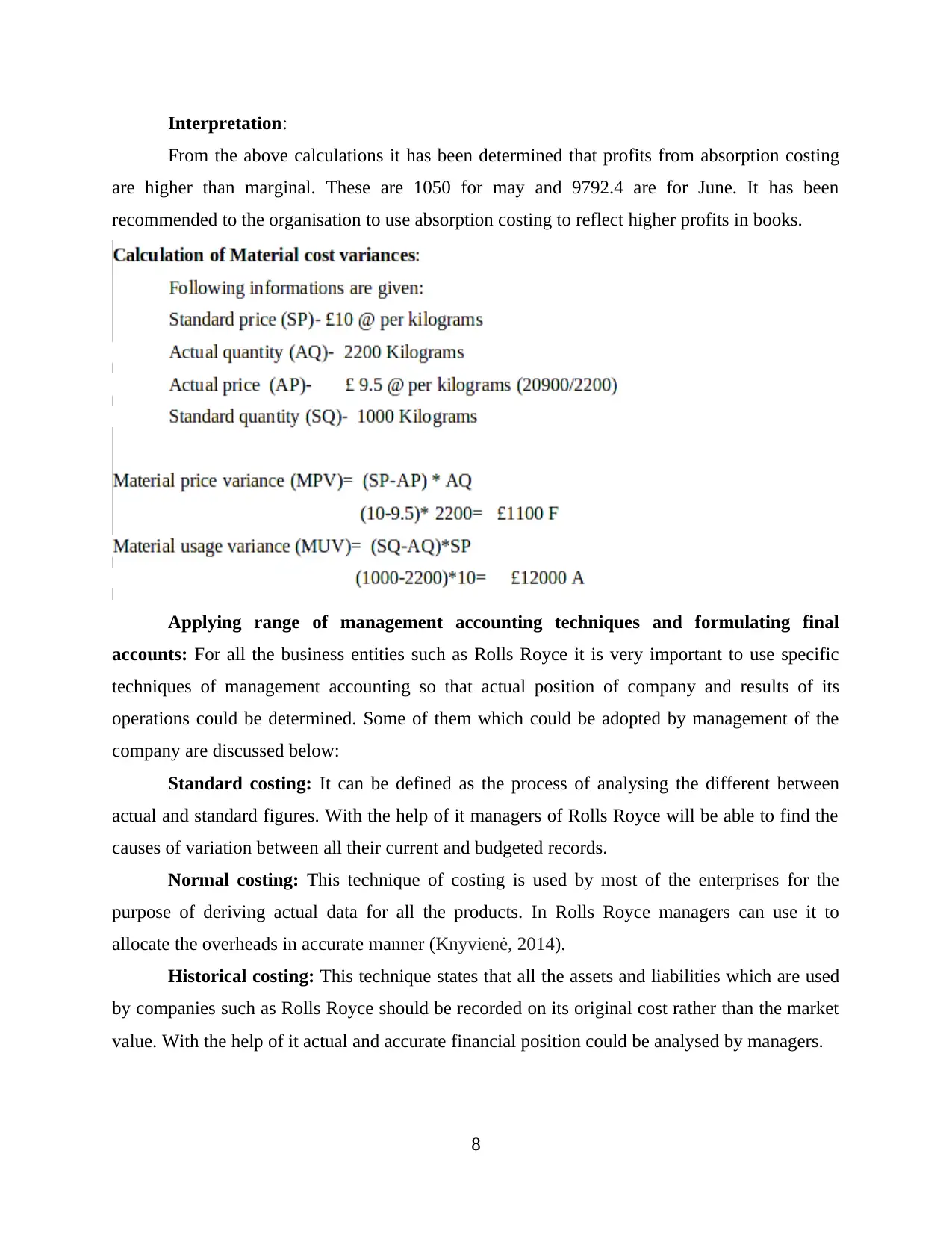

Interpretation:

From the above calculations it has been determined that profits from absorption costing

are higher than marginal. These are 1050 for may and 9792.4 are for June. It has been

recommended to the organisation to use absorption costing to reflect higher profits in books.

Applying range of management accounting techniques and formulating final

accounts: For all the business entities such as Rolls Royce it is very important to use specific

techniques of management accounting so that actual position of company and results of its

operations could be determined. Some of them which could be adopted by management of the

company are discussed below:

Standard costing: It can be defined as the process of analysing the different between

actual and standard figures. With the help of it managers of Rolls Royce will be able to find the

causes of variation between all their current and budgeted records.

Normal costing: This technique of costing is used by most of the enterprises for the

purpose of deriving actual data for all the products. In Rolls Royce managers can use it to

allocate the overheads in accurate manner (Knyvienė, 2014).

Historical costing: This technique states that all the assets and liabilities which are used

by companies such as Rolls Royce should be recorded on its original cost rather than the market

value. With the help of it actual and accurate financial position could be analysed by managers.

8

From the above calculations it has been determined that profits from absorption costing

are higher than marginal. These are 1050 for may and 9792.4 are for June. It has been

recommended to the organisation to use absorption costing to reflect higher profits in books.

Applying range of management accounting techniques and formulating final

accounts: For all the business entities such as Rolls Royce it is very important to use specific

techniques of management accounting so that actual position of company and results of its

operations could be determined. Some of them which could be adopted by management of the

company are discussed below:

Standard costing: It can be defined as the process of analysing the different between

actual and standard figures. With the help of it managers of Rolls Royce will be able to find the

causes of variation between all their current and budgeted records.

Normal costing: This technique of costing is used by most of the enterprises for the

purpose of deriving actual data for all the products. In Rolls Royce managers can use it to

allocate the overheads in accurate manner (Knyvienė, 2014).

Historical costing: This technique states that all the assets and liabilities which are used

by companies such as Rolls Royce should be recorded on its original cost rather than the market

value. With the help of it actual and accurate financial position could be analysed by managers.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LO 3

Different planning tools used in budgetary control with their advantages and disadvantages

Budget and budgetary control: In most of the business entities different plans and

strategies are formulated for the purpose of controlling expenses which are taking place due to

operational activities. Budget is also considered as one of them that guides management to find

that organisation's performance is being enhanced as compare to previous year or not. In Rolls

Royce different types of budgets such as zero based, operating and master are generated that

helps management to allocate funds to all the activities according to their requirements (Kraus,

Håkansson and Lind, 2015).

In order to facilitate the controlling procedures a specific procedure is followed by

managers of different companies which is known as budgetary control. With the help of it

actual performance of business could be enhanced because it helps managers to find the reasons

which are resulting in variation between actual and budgeted plans. In Rolls Royce it is also

focused by managers for the purpose of planning, coordinating and controlling the process of

allocation of budgets. All the planning tools which are used by management of the company are

described below:

Operational budgetary control: It is the combination of all the tools and techniques

which could be used by business entities for the purpose of taking control over all the operational

activities. Different elements of it are discussed below:

Forecasting: It is the process which is used by the companies to estimate future expenses

so that budgets to deal with them could be formulated in advance. It facilitates the

managers of the company to be prepare to face all the uncertain events which may take

place in future.

Standard costing: It is the costing technique in which difference between expected and

actual costs. With the help of it predetermined cost of executing operational activities.

Variance analysis: It is a technique which is used by companies such as Rolls Royce for

the purpose of determining the reason behind the variances which are taking place

between actual and budgeted figures. With the help of it the management will be able to

take effective decisions for future.

Flexible budget: In all the organisations different budgets are prepared on annual basis

for the purpose of keeping record of all the activities. Some of them which could be

9

Different planning tools used in budgetary control with their advantages and disadvantages

Budget and budgetary control: In most of the business entities different plans and

strategies are formulated for the purpose of controlling expenses which are taking place due to

operational activities. Budget is also considered as one of them that guides management to find

that organisation's performance is being enhanced as compare to previous year or not. In Rolls

Royce different types of budgets such as zero based, operating and master are generated that

helps management to allocate funds to all the activities according to their requirements (Kraus,

Håkansson and Lind, 2015).

In order to facilitate the controlling procedures a specific procedure is followed by

managers of different companies which is known as budgetary control. With the help of it

actual performance of business could be enhanced because it helps managers to find the reasons

which are resulting in variation between actual and budgeted plans. In Rolls Royce it is also

focused by managers for the purpose of planning, coordinating and controlling the process of

allocation of budgets. All the planning tools which are used by management of the company are

described below:

Operational budgetary control: It is the combination of all the tools and techniques

which could be used by business entities for the purpose of taking control over all the operational

activities. Different elements of it are discussed below:

Forecasting: It is the process which is used by the companies to estimate future expenses

so that budgets to deal with them could be formulated in advance. It facilitates the

managers of the company to be prepare to face all the uncertain events which may take

place in future.

Standard costing: It is the costing technique in which difference between expected and

actual costs. With the help of it predetermined cost of executing operational activities.

Variance analysis: It is a technique which is used by companies such as Rolls Royce for

the purpose of determining the reason behind the variances which are taking place

between actual and budgeted figures. With the help of it the management will be able to

take effective decisions for future.

Flexible budget: In all the organisations different budgets are prepared on annual basis

for the purpose of keeping record of all the activities. Some of them which could be

9

modified with changes in business figures then these are known as flexible budgets. In

rolls Royce these are used by managers to analyse actual position of business.

All the advantages and disadvantages of it are as follows:

Advantages Disadvantages

This planning tool keep accurate information

about all the costs which are related to

different operations which are carried out by

the company. It helps to make the process of

budget building more flexible because it

facilitates management to allocate resources

appropriately (Lapsley and Rekers, 2017).

If organisations such as Rolls Royce are

willing to use it for long term objectives then it

may not be the right choice because it is based

upon estimation.

It facilitates the communication between

different departments because it consolidates

information of all the operational activities.

The level of rigidity in the formulation of it is

very high for which an experienced employee

is required which may result in increased cost

for the company.

Capital budgeting: It is a budgeting technique which is used by organisations to

determine the best suitable investment from end number of alternatives. There are various types

of it which are used by managers of Rolls Royce while planning for making investment in a new

project. Description of all of them is as follows:

NPV: This technique of capital budgeting is used to determine the net present value o an

asset which could be acquired by an organisation after a certain period of time by making

investment in a business project.

ARR: With the help of it, organisations try to figure out average rate of return which will

be received by them from the projects in which investment is made. The higher rate

shows the investment decision of the organisation is very good.

IRR: It is the interest rate which works as a measure of determining interest rate of a

business project. With the help of it, attractiveness of different alternatives could be

determined.

10

rolls Royce these are used by managers to analyse actual position of business.

All the advantages and disadvantages of it are as follows:

Advantages Disadvantages

This planning tool keep accurate information

about all the costs which are related to

different operations which are carried out by

the company. It helps to make the process of

budget building more flexible because it

facilitates management to allocate resources

appropriately (Lapsley and Rekers, 2017).

If organisations such as Rolls Royce are

willing to use it for long term objectives then it

may not be the right choice because it is based

upon estimation.

It facilitates the communication between

different departments because it consolidates

information of all the operational activities.

The level of rigidity in the formulation of it is

very high for which an experienced employee

is required which may result in increased cost

for the company.

Capital budgeting: It is a budgeting technique which is used by organisations to

determine the best suitable investment from end number of alternatives. There are various types

of it which are used by managers of Rolls Royce while planning for making investment in a new

project. Description of all of them is as follows:

NPV: This technique of capital budgeting is used to determine the net present value o an

asset which could be acquired by an organisation after a certain period of time by making

investment in a business project.

ARR: With the help of it, organisations try to figure out average rate of return which will

be received by them from the projects in which investment is made. The higher rate

shows the investment decision of the organisation is very good.

IRR: It is the interest rate which works as a measure of determining interest rate of a

business project. With the help of it, attractiveness of different alternatives could be

determined.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.