Management Accounting Report: Ryanair Financial Problems and Solutions

VerifiedAdded on 2021/06/17

|16

|2875

|401

Report

AI Summary

This report provides a detailed analysis of management accounting practices within Ryanair, focusing on various aspects such as the definition and importance of management accounting, its differences from financial accounting, and different management accounting methods like job costing, contract costing, and service costing. The report explores the benefits of implementing a management accounting system in Ryanair, particularly in cost accounting and inventory management. It further examines product costing techniques, specifically absorption and marginal costing, highlighting their impact on profit and loss statements. The report also delves into the pros and cons of budgeting tools, application of planning tools, and the financial problems faced by Ryanair. Finally, it discusses financial governance, setting up an effective management accounting system, and implementing budgeting policies, providing a comprehensive overview of the financial management of the airline.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGEMENT ACCOUNTING

Table of Contents

Requirement of Task 1.....................................................................................................................2

Definition of Management Accounting.......................................................................................2

Importance of Management Accounting.....................................................................................2

Difference between Management Accounting and Financial Accounting..................................3

Different Types of Management Accounting Method.................................................................4

Benefits of Management Accounting System in Ryanair............................................................5

Integrating Management Accounting System and Report in Ryanair.........................................5

Requirement of Task 2.....................................................................................................................6

Product Cost Under Absorption and Marginal Costing Techniques...........................................6

Requirement of Task 3.....................................................................................................................8

Pros and Cons of Budgeting Tools..............................................................................................8

Application of Different Planning tools....................................................................................11

Requirement of Task 4...................................................................................................................12

Financial Problems of Ryanair and Southwest Airlines............................................................12

Financial Governance................................................................................................................12

Setting Up an Effective Management Accounting System and Strategies................................12

Implementation of the Budgeting policy...................................................................................13

Reference.......................................................................................................................................14

MANAGEMENT ACCOUNTING

Table of Contents

Requirement of Task 1.....................................................................................................................2

Definition of Management Accounting.......................................................................................2

Importance of Management Accounting.....................................................................................2

Difference between Management Accounting and Financial Accounting..................................3

Different Types of Management Accounting Method.................................................................4

Benefits of Management Accounting System in Ryanair............................................................5

Integrating Management Accounting System and Report in Ryanair.........................................5

Requirement of Task 2.....................................................................................................................6

Product Cost Under Absorption and Marginal Costing Techniques...........................................6

Requirement of Task 3.....................................................................................................................8

Pros and Cons of Budgeting Tools..............................................................................................8

Application of Different Planning tools....................................................................................11

Requirement of Task 4...................................................................................................................12

Financial Problems of Ryanair and Southwest Airlines............................................................12

Financial Governance................................................................................................................12

Setting Up an Effective Management Accounting System and Strategies................................12

Implementation of the Budgeting policy...................................................................................13

Reference.......................................................................................................................................14

2

MANAGEMENT ACCOUNTING

Requirement of Task 1

Definition of Management Accounting

Management Accounting is also considered as a part of accounting process which is

adopted by business to formulate internal management reports which can be used by the

businesses in order to take management decisions (Fullerton, Kennedy and Widener 2013).

Management accounting helps businesses to assist in day to day activities of the business.

Management accounting helps businesses to perform functions which are important for the

business, like planning, organizing, staffing, directing and controlling.

As per the Institute of Cost and Management Accountants, London, the preparation of

accounting information which can help the management in formulation of policies which can be

related to planning and control of business with the application of professional knowledge and

skills (Soin and Collier 2013).

The use of management accounting in modern times has become very much essential so

as to ensure that the effective management. Management Accounting is closely associated with

effective decision-making process and also strategic management of the business.

Importance of Management Accounting

The importance of the management accounting in a business is immense in today’s

dynamic environment. The management accounting processes links various level of management

that is top level, Middle level and lower level management with the each other and facilitates

effective communication between each level so that the policies and strategies are clearly

communicated among the executives of different levels (Juras 2014). Management Accounting

MANAGEMENT ACCOUNTING

Requirement of Task 1

Definition of Management Accounting

Management Accounting is also considered as a part of accounting process which is

adopted by business to formulate internal management reports which can be used by the

businesses in order to take management decisions (Fullerton, Kennedy and Widener 2013).

Management accounting helps businesses to assist in day to day activities of the business.

Management accounting helps businesses to perform functions which are important for the

business, like planning, organizing, staffing, directing and controlling.

As per the Institute of Cost and Management Accountants, London, the preparation of

accounting information which can help the management in formulation of policies which can be

related to planning and control of business with the application of professional knowledge and

skills (Soin and Collier 2013).

The use of management accounting in modern times has become very much essential so

as to ensure that the effective management. Management Accounting is closely associated with

effective decision-making process and also strategic management of the business.

Importance of Management Accounting

The importance of the management accounting in a business is immense in today’s

dynamic environment. The management accounting processes links various level of management

that is top level, Middle level and lower level management with the each other and facilitates

effective communication between each level so that the policies and strategies are clearly

communicated among the executives of different levels (Juras 2014). Management Accounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGEMENT ACCOUNTING

divides the entire business units into various sections, departments and divisions which can

effectively recognize the cost units. Management accounting system is also useful for

maintaining effective control in the business. Management accounting involves methods which

can be used by the management effectively for the purpose of setting of performance standards

and then measuring the actual performance of the business in terms of standard set and analyze

the cause of any variances which might have occurred (Ahmad 2013). In addition to this,

management accounting can be effectively used by the top-level management to take effective

management decisions.

Difference between Management Accounting and Financial Accounting

Point of Distinction Financial Accounting Management Accounting

Purpose Financial Accounting is used

for communication of

financial position of the

business (Scott 2015).

Management accounting is

mainly used for the purpose

of Decision Making process.

Primary Audience The primary audience of

financial accounts are

external parties such as

investors, debtors.

The primary audience of

management accounts are

internal users such as

management personnels.

Requirement This is to be prepared by the

company on a mandatory

basis

This is optional for the

business to prepare.

MANAGEMENT ACCOUNTING

divides the entire business units into various sections, departments and divisions which can

effectively recognize the cost units. Management accounting system is also useful for

maintaining effective control in the business. Management accounting involves methods which

can be used by the management effectively for the purpose of setting of performance standards

and then measuring the actual performance of the business in terms of standard set and analyze

the cause of any variances which might have occurred (Ahmad 2013). In addition to this,

management accounting can be effectively used by the top-level management to take effective

management decisions.

Difference between Management Accounting and Financial Accounting

Point of Distinction Financial Accounting Management Accounting

Purpose Financial Accounting is used

for communication of

financial position of the

business (Scott 2015).

Management accounting is

mainly used for the purpose

of Decision Making process.

Primary Audience The primary audience of

financial accounts are

external parties such as

investors, debtors.

The primary audience of

management accounts are

internal users such as

management personnels.

Requirement This is to be prepared by the

company on a mandatory

basis

This is optional for the

business to prepare.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGEMENT ACCOUNTING

Focus The focus of this type of

accounting is based on past

transactions.

The focus of this type of

accounting is to aid the

management to make future

decisions.

Different Types of Management Accounting Method

The different methods which are used by the management as a management accounting

tool are explained below:

Job Costing: This is a method which is sued by the management to allocate the costs

which are associated with the products on the basis of the job or batches in which the

product is produced (Braun 2013). The technique is used by businesses where there is a

number of products which are produced during the period.

Contract Costing: This is a method of costing which is mostly used by construction

business. The costing is done over a period of time and the costing is done on the basis of

the contract which is engaged between the client and the management. Contract costing

facilitates effective costing for construction industries (McLean 2013).

Service Costing: This is a costing technique which is used by business which are engaged

in providing services to the business. The method is also known as operating costing and

is very much effective in identifying the cost units of a service providing industry and

determining the costs which are to be allocated on such basis (Sakao and Lindahl 2015).

The management of service industry is effective in determining the price which is to be

charged for the services which is provided by the business.

MANAGEMENT ACCOUNTING

Focus The focus of this type of

accounting is based on past

transactions.

The focus of this type of

accounting is to aid the

management to make future

decisions.

Different Types of Management Accounting Method

The different methods which are used by the management as a management accounting

tool are explained below:

Job Costing: This is a method which is sued by the management to allocate the costs

which are associated with the products on the basis of the job or batches in which the

product is produced (Braun 2013). The technique is used by businesses where there is a

number of products which are produced during the period.

Contract Costing: This is a method of costing which is mostly used by construction

business. The costing is done over a period of time and the costing is done on the basis of

the contract which is engaged between the client and the management. Contract costing

facilitates effective costing for construction industries (McLean 2013).

Service Costing: This is a costing technique which is used by business which are engaged

in providing services to the business. The method is also known as operating costing and

is very much effective in identifying the cost units of a service providing industry and

determining the costs which are to be allocated on such basis (Sakao and Lindahl 2015).

The management of service industry is effective in determining the price which is to be

charged for the services which is provided by the business.

5

MANAGEMENT ACCOUNTING

Benefits of Management Accounting System in Ryanair

Ryanair is airline company which is engaged in flight services which are provided to the

customers of the business. The business model of the company is focused on low cost of the fare

which is charged by the business. This is one of the main reasons for which the business is

considered to be one of the successful brands of airline in UK. The benefits of management

accounting implementation are mention below:

Cost Accounting System: The airline business follows the business model of charging

low fares from the customers of the company. Management accounting techniques

specializes in maintenance of cost of the business and effective implementation of

strategies help business to maintain the cost of the business which is related to the flight

fares which are charged by the business. An effective cost accounting system not only

will help the business in maintaining the cost of the business but also help in forecasting

the expenses of the business.

Inventory management: Management Accounting methods also incorporate inventory

management system which will be useful in the case of Ryanair. The system facilitates

the business to effectively value the stocks of the business which are important in case of

an airline industry. In addition to this, the management will be able to compute the costs

which are associated with the inventory stocks of the business.

Integrating Management Accounting System and Report in Ryanair

It is recommended that Ryanair should incorporate management accounting techniques so

that it can lead to overall development of business processes and improvement in the internal

structure of the business. In addition to this, integrating such management accounting methods

MANAGEMENT ACCOUNTING

Benefits of Management Accounting System in Ryanair

Ryanair is airline company which is engaged in flight services which are provided to the

customers of the business. The business model of the company is focused on low cost of the fare

which is charged by the business. This is one of the main reasons for which the business is

considered to be one of the successful brands of airline in UK. The benefits of management

accounting implementation are mention below:

Cost Accounting System: The airline business follows the business model of charging

low fares from the customers of the company. Management accounting techniques

specializes in maintenance of cost of the business and effective implementation of

strategies help business to maintain the cost of the business which is related to the flight

fares which are charged by the business. An effective cost accounting system not only

will help the business in maintaining the cost of the business but also help in forecasting

the expenses of the business.

Inventory management: Management Accounting methods also incorporate inventory

management system which will be useful in the case of Ryanair. The system facilitates

the business to effectively value the stocks of the business which are important in case of

an airline industry. In addition to this, the management will be able to compute the costs

which are associated with the inventory stocks of the business.

Integrating Management Accounting System and Report in Ryanair

It is recommended that Ryanair should incorporate management accounting techniques so

that it can lead to overall development of business processes and improvement in the internal

structure of the business. In addition to this, integrating such management accounting methods

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGEMENT ACCOUNTING

will facilitate the business to take accurate management decisions and also help in forecasting of

results of business with the help of budgetary controls.

Requirement of Task 2

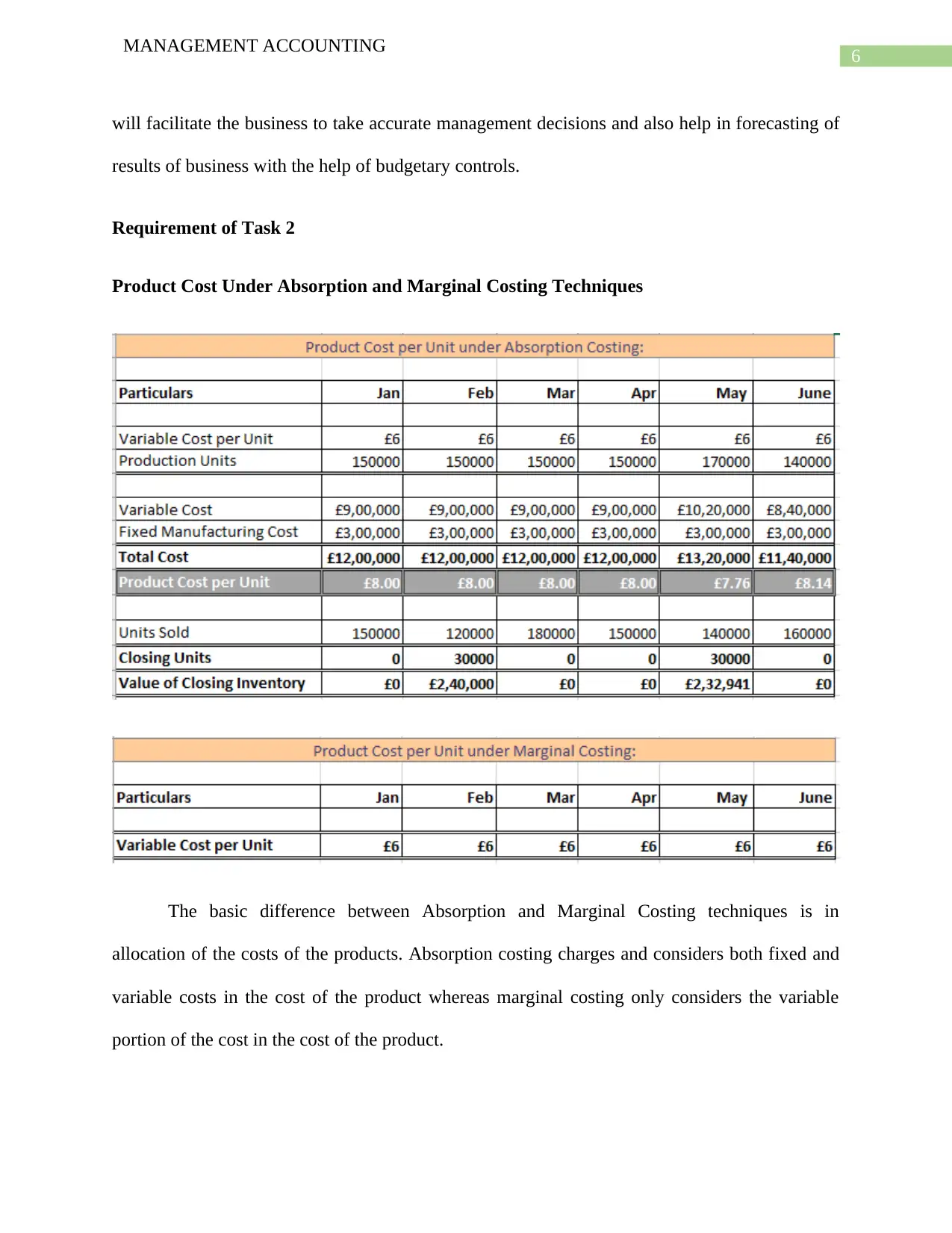

Product Cost Under Absorption and Marginal Costing Techniques

The basic difference between Absorption and Marginal Costing techniques is in

allocation of the costs of the products. Absorption costing charges and considers both fixed and

variable costs in the cost of the product whereas marginal costing only considers the variable

portion of the cost in the cost of the product.

MANAGEMENT ACCOUNTING

will facilitate the business to take accurate management decisions and also help in forecasting of

results of business with the help of budgetary controls.

Requirement of Task 2

Product Cost Under Absorption and Marginal Costing Techniques

The basic difference between Absorption and Marginal Costing techniques is in

allocation of the costs of the products. Absorption costing charges and considers both fixed and

variable costs in the cost of the product whereas marginal costing only considers the variable

portion of the cost in the cost of the product.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT ACCOUNTING

As shown in the above figure, the total cost of the product is arrived at by summing up

the fixed and variable costs of the business in the case of Absorption costing and the above table

also shows that the marginal costing techniques considers only the variable costs which are

associated with the products of the business.

The profit and loss account which is prepared by the business on the basis of the

absorption costing and marginal costing is distinct because of the treatment of fixed overhead

MANAGEMENT ACCOUNTING

As shown in the above figure, the total cost of the product is arrived at by summing up

the fixed and variable costs of the business in the case of Absorption costing and the above table

also shows that the marginal costing techniques considers only the variable costs which are

associated with the products of the business.

The profit and loss account which is prepared by the business on the basis of the

absorption costing and marginal costing is distinct because of the treatment of fixed overhead

8

MANAGEMENT ACCOUNTING

expenses of the business. In case of profit and loss account which is prepared under absorption

costing considers the fixed cost as a part of the cost of the production of the business which is

shown as a combined figure of $ 12,00,000 for the first four months and then it changes. The

above table shows that the business incurs losses for the month of March and June which can be

attributed to the high cost of products of the company. In case of profit and loss account which is

prepared on the basis of marginal costing system, the fixed costs do not form a part of the cost of

production as shown in the table above. The profits which are shown by the statement of profit

and loss account prepared under marginal costing system is $ 2,00,000 which is fixed for the first

four months and then the profits increases.

Requirement of Task 3

Pros and Cons of Budgeting Tools

The advantages of using budgets in the business of Ryanair are mentioned below in

details:

Budgets are regarded as an important tool in business as it helps the management to

effectively forecast important estimates such as net profit, sales turnover, growth and

similar other indicators of the business. It can be effectively used by the management to

estimate the income and expenses of the company and also estimate the costs of the

business department wise.

Budgets are an excellent way to communicate the plans of the top-level management of

the lower subordinates of the business. Budgets effective relay the plans or standards

which are set by the senior management to departmental heads so that all departments can

clearly understand the goals of the business and make efforts to achieve the same.

MANAGEMENT ACCOUNTING

expenses of the business. In case of profit and loss account which is prepared under absorption

costing considers the fixed cost as a part of the cost of the production of the business which is

shown as a combined figure of $ 12,00,000 for the first four months and then it changes. The

above table shows that the business incurs losses for the month of March and June which can be

attributed to the high cost of products of the company. In case of profit and loss account which is

prepared on the basis of marginal costing system, the fixed costs do not form a part of the cost of

production as shown in the table above. The profits which are shown by the statement of profit

and loss account prepared under marginal costing system is $ 2,00,000 which is fixed for the first

four months and then the profits increases.

Requirement of Task 3

Pros and Cons of Budgeting Tools

The advantages of using budgets in the business of Ryanair are mentioned below in

details:

Budgets are regarded as an important tool in business as it helps the management to

effectively forecast important estimates such as net profit, sales turnover, growth and

similar other indicators of the business. It can be effectively used by the management to

estimate the income and expenses of the company and also estimate the costs of the

business department wise.

Budgets are an excellent way to communicate the plans of the top-level management of

the lower subordinates of the business. Budgets effective relay the plans or standards

which are set by the senior management to departmental heads so that all departments can

clearly understand the goals of the business and make efforts to achieve the same.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGEMENT ACCOUNTING

Budgeting techniques can also be used for the purpose of supervising and controlling the

performance of the business effectively. This facilitates the management to measure the

performance of the business and that of the employees of the business effectively.

In addition to this, Budgets are also used in strategic management techniques such as

benchmarking and therefore it can be clearly be identified that Budgets are universally

applicable in the business and overall management of the company.

The disadvantages which is related to application of Budgetary control in a business are

discussed below:

Budgets are prepared forecasting changes in prices and also market fluctuations, however

budgets are not effective when there is change in the external factors such as new

technological development which will increase the level of production of the business

(Aminbakhsh, Gunduz and Sonmez 2013). In such a case, the budgets become obsolete.

The cost of setting up a budget and implementing the same is a costly process and

therefore it is not applicable to all organizations especially the small one.

The estimates of the budgets depend on the accuracy of the judgements of the business

and forecasting ability of the business.

Cash Budget

MANAGEMENT ACCOUNTING

Budgeting techniques can also be used for the purpose of supervising and controlling the

performance of the business effectively. This facilitates the management to measure the

performance of the business and that of the employees of the business effectively.

In addition to this, Budgets are also used in strategic management techniques such as

benchmarking and therefore it can be clearly be identified that Budgets are universally

applicable in the business and overall management of the company.

The disadvantages which is related to application of Budgetary control in a business are

discussed below:

Budgets are prepared forecasting changes in prices and also market fluctuations, however

budgets are not effective when there is change in the external factors such as new

technological development which will increase the level of production of the business

(Aminbakhsh, Gunduz and Sonmez 2013). In such a case, the budgets become obsolete.

The cost of setting up a budget and implementing the same is a costly process and

therefore it is not applicable to all organizations especially the small one.

The estimates of the budgets depend on the accuracy of the judgements of the business

and forecasting ability of the business.

Cash Budget

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGEMENT ACCOUNTING

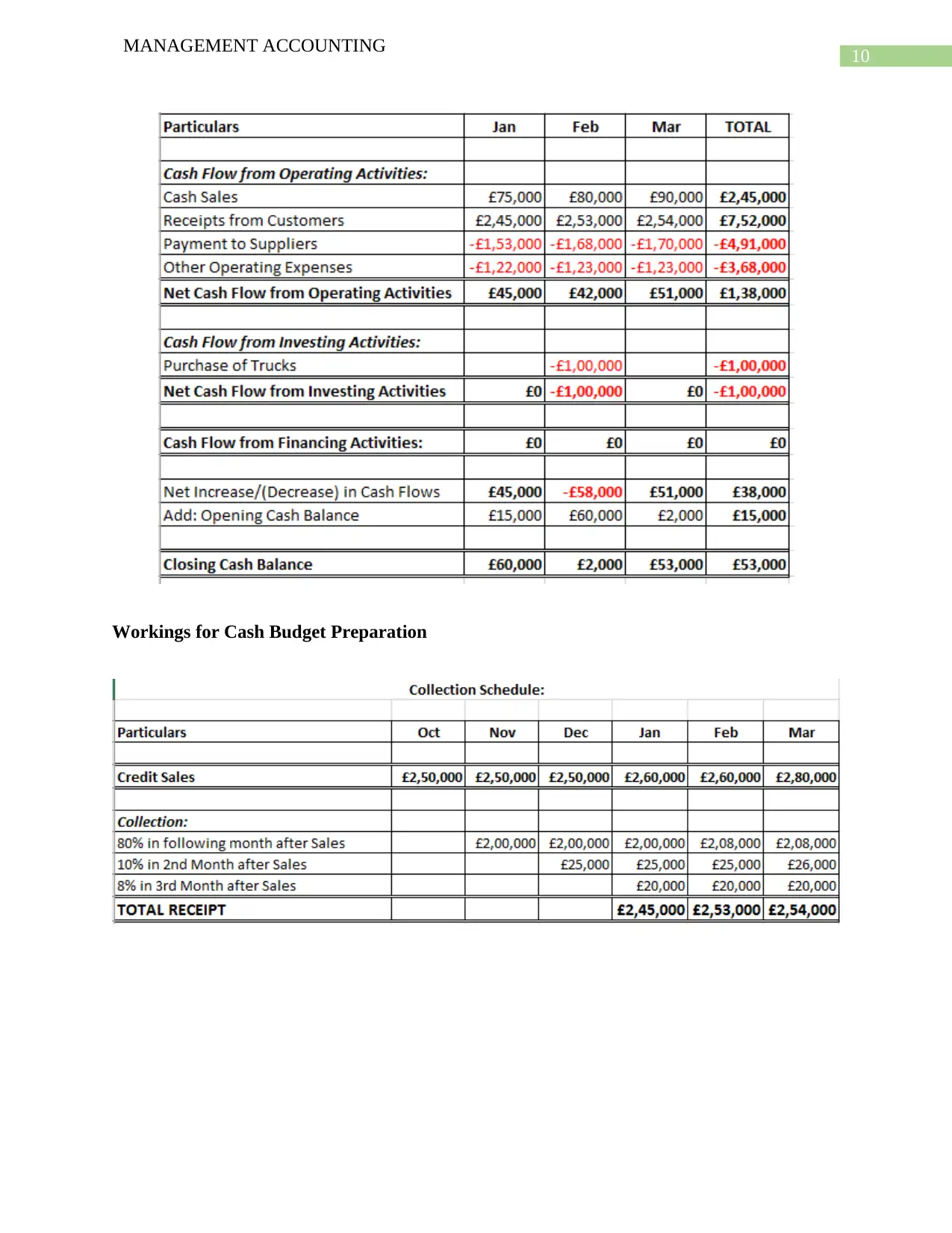

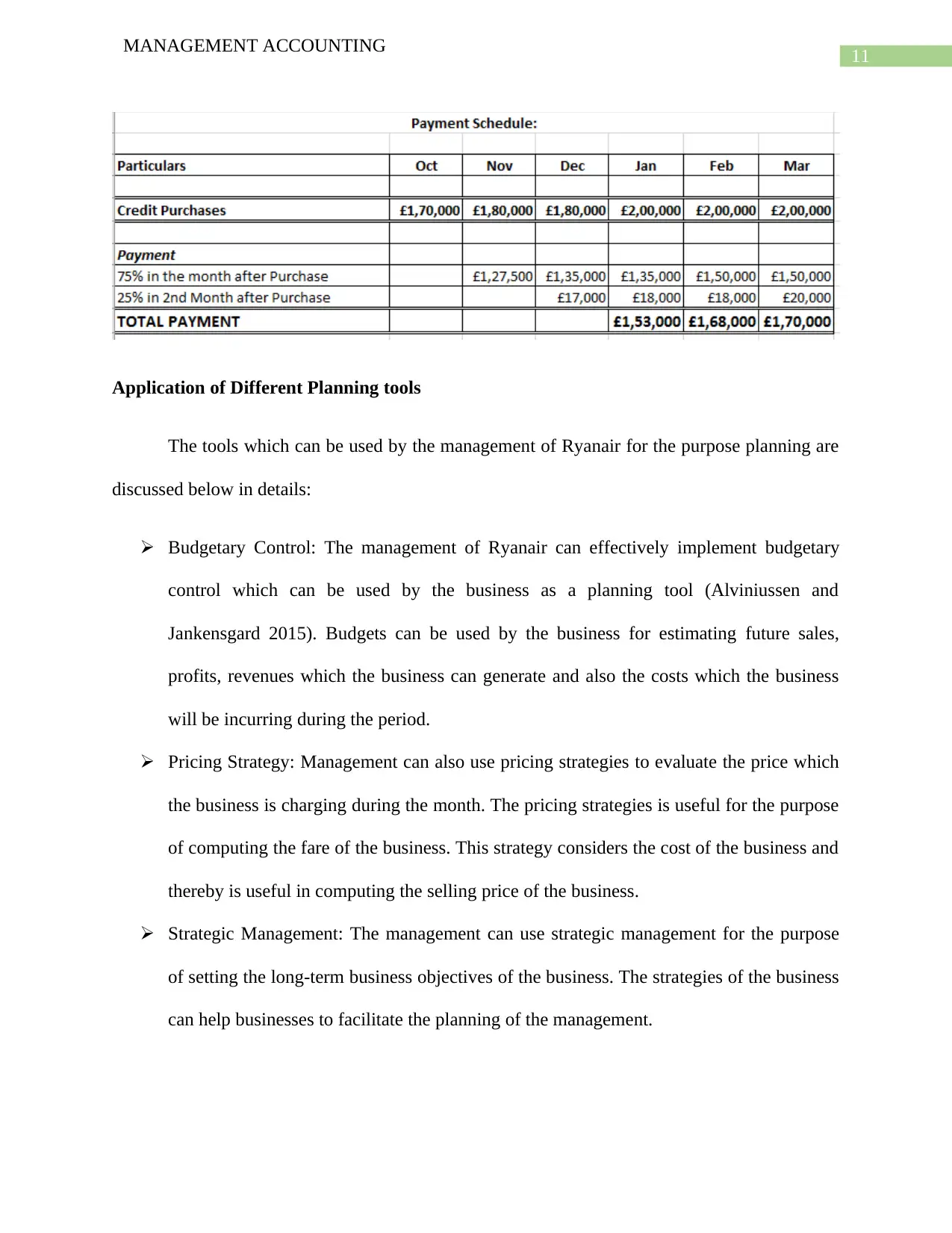

Workings for Cash Budget Preparation

MANAGEMENT ACCOUNTING

Workings for Cash Budget Preparation

11

MANAGEMENT ACCOUNTING

Application of Different Planning tools

The tools which can be used by the management of Ryanair for the purpose planning are

discussed below in details:

Budgetary Control: The management of Ryanair can effectively implement budgetary

control which can be used by the business as a planning tool (Alviniussen and

Jankensgard 2015). Budgets can be used by the business for estimating future sales,

profits, revenues which the business can generate and also the costs which the business

will be incurring during the period.

Pricing Strategy: Management can also use pricing strategies to evaluate the price which

the business is charging during the month. The pricing strategies is useful for the purpose

of computing the fare of the business. This strategy considers the cost of the business and

thereby is useful in computing the selling price of the business.

Strategic Management: The management can use strategic management for the purpose

of setting the long-term business objectives of the business. The strategies of the business

can help businesses to facilitate the planning of the management.

MANAGEMENT ACCOUNTING

Application of Different Planning tools

The tools which can be used by the management of Ryanair for the purpose planning are

discussed below in details:

Budgetary Control: The management of Ryanair can effectively implement budgetary

control which can be used by the business as a planning tool (Alviniussen and

Jankensgard 2015). Budgets can be used by the business for estimating future sales,

profits, revenues which the business can generate and also the costs which the business

will be incurring during the period.

Pricing Strategy: Management can also use pricing strategies to evaluate the price which

the business is charging during the month. The pricing strategies is useful for the purpose

of computing the fare of the business. This strategy considers the cost of the business and

thereby is useful in computing the selling price of the business.

Strategic Management: The management can use strategic management for the purpose

of setting the long-term business objectives of the business. The strategies of the business

can help businesses to facilitate the planning of the management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.