Management Accounting and Financial Analysis: A Samsung Case Study

VerifiedAdded on 2024/04/26

|23

|4023

|447

Report

AI Summary

This management accounting report provides a comprehensive analysis of Samsung's financial strategies and systems. It begins with an overview of management accounting, detailing its essential requirements and reporting methods. The report then delves into cost analysis, comparing absorption and marginal costing methods to prepare income statements and understand their differences. Furthermore, it explores various planning tools for budgetary control, evaluating their advantages and disadvantages. Finally, the report benchmarks Samsung against a competitor to assess how organizations adapt management accounting systems to address financial challenges, offering valuable insights into practical applications of management accounting principles. Desklib provides access to this and other solved assignments for students.

Applying expertise in Management

Accounting

1

Accounting

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction:....................................................................................................................................3

Task 1...............................................................................................................................................4

P1. Explain management accounting and give the essential requirements of different types of

management accounting systems.................................................................................................4

P2. Explain different methods used for management accounting reporting................................6

Task 2...............................................................................................................................................7

P3. Calculate cost per unit using absorption and marginal costing and explain why they differ.

Explain how they are used to prepare an income statement under Marginal costing and

absorption costing........................................................................................................................7

Task 3.............................................................................................................................................12

P4. Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.......................................................................................................................12

Task 4.............................................................................................................................................17

P5. Compare Samsung with one of its competitor in order to establish how organisations are

adapting management accounting systems to respond to financial problems...........................17

Conclusion:....................................................................................................................................20

References:....................................................................................................................................21

2

Introduction:....................................................................................................................................3

Task 1...............................................................................................................................................4

P1. Explain management accounting and give the essential requirements of different types of

management accounting systems.................................................................................................4

P2. Explain different methods used for management accounting reporting................................6

Task 2...............................................................................................................................................7

P3. Calculate cost per unit using absorption and marginal costing and explain why they differ.

Explain how they are used to prepare an income statement under Marginal costing and

absorption costing........................................................................................................................7

Task 3.............................................................................................................................................12

P4. Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.......................................................................................................................12

Task 4.............................................................................................................................................17

P5. Compare Samsung with one of its competitor in order to establish how organisations are

adapting management accounting systems to respond to financial problems...........................17

Conclusion:....................................................................................................................................20

References:....................................................................................................................................21

2

Introduction:

The management accounting report will be prepared here to gain knowledge about the various

uses and advantages of using management accounting system in context of an organisation

chosen in the given case. The various concepts regarding management accounting systems and

the relation of these systems with performance of the company will be evaluated in this report.

The report will contain a brief introduction about the management accounting definition along

with the types of reporting required in management accounting. The report will then include the

use of various types of costing methods in analysing the cost structure of the enterprise. The

various financial reports will be generated using marginal and absorption coting method. Further

the report will include the explanation of use of standard costing in responding to various

financial problems of the organisation. The types of management accounting tools will be

analysed in order to resolve these types of problems and gaining competitive edge in the market.

3

The management accounting report will be prepared here to gain knowledge about the various

uses and advantages of using management accounting system in context of an organisation

chosen in the given case. The various concepts regarding management accounting systems and

the relation of these systems with performance of the company will be evaluated in this report.

The report will contain a brief introduction about the management accounting definition along

with the types of reporting required in management accounting. The report will then include the

use of various types of costing methods in analysing the cost structure of the enterprise. The

various financial reports will be generated using marginal and absorption coting method. Further

the report will include the explanation of use of standard costing in responding to various

financial problems of the organisation. The types of management accounting tools will be

analysed in order to resolve these types of problems and gaining competitive edge in the market.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 1

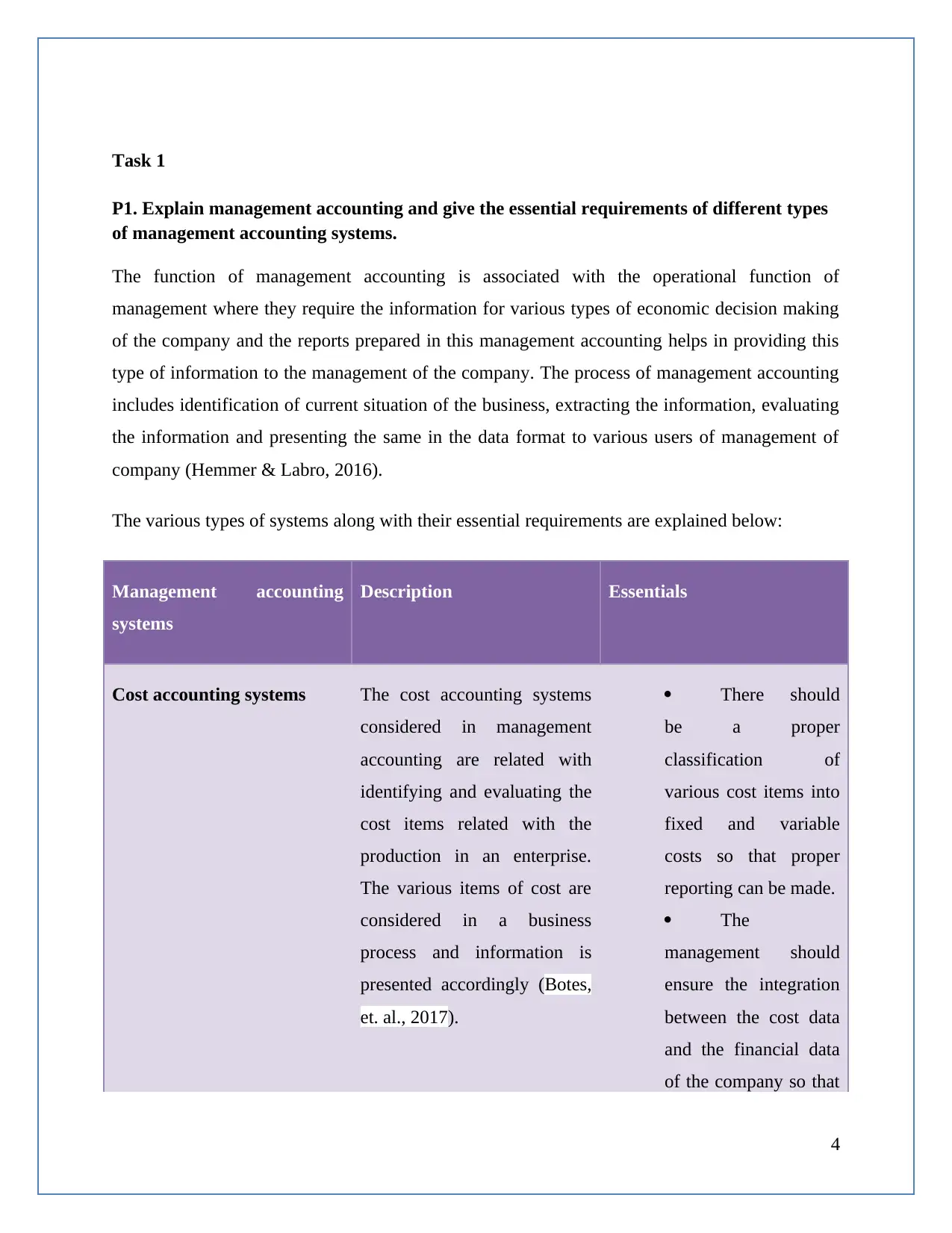

P1. Explain management accounting and give the essential requirements of different types

of management accounting systems.

The function of management accounting is associated with the operational function of

management where they require the information for various types of economic decision making

of the company and the reports prepared in this management accounting helps in providing this

type of information to the management of the company. The process of management accounting

includes identification of current situation of the business, extracting the information, evaluating

the information and presenting the same in the data format to various users of management of

company (Hemmer & Labro, 2016).

The various types of systems along with their essential requirements are explained below:

Management accounting

systems

Description Essentials

Cost accounting systems The cost accounting systems

considered in management

accounting are related with

identifying and evaluating the

cost items related with the

production in an enterprise.

The various items of cost are

considered in a business

process and information is

presented accordingly (Botes,

et. al., 2017).

There should

be a proper

classification of

various cost items into

fixed and variable

costs so that proper

reporting can be made.

The

management should

ensure the integration

between the cost data

and the financial data

of the company so that

4

P1. Explain management accounting and give the essential requirements of different types

of management accounting systems.

The function of management accounting is associated with the operational function of

management where they require the information for various types of economic decision making

of the company and the reports prepared in this management accounting helps in providing this

type of information to the management of the company. The process of management accounting

includes identification of current situation of the business, extracting the information, evaluating

the information and presenting the same in the data format to various users of management of

company (Hemmer & Labro, 2016).

The various types of systems along with their essential requirements are explained below:

Management accounting

systems

Description Essentials

Cost accounting systems The cost accounting systems

considered in management

accounting are related with

identifying and evaluating the

cost items related with the

production in an enterprise.

The various items of cost are

considered in a business

process and information is

presented accordingly (Botes,

et. al., 2017).

There should

be a proper

classification of

various cost items into

fixed and variable

costs so that proper

reporting can be made.

The

management should

ensure the integration

between the cost data

and the financial data

of the company so that

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

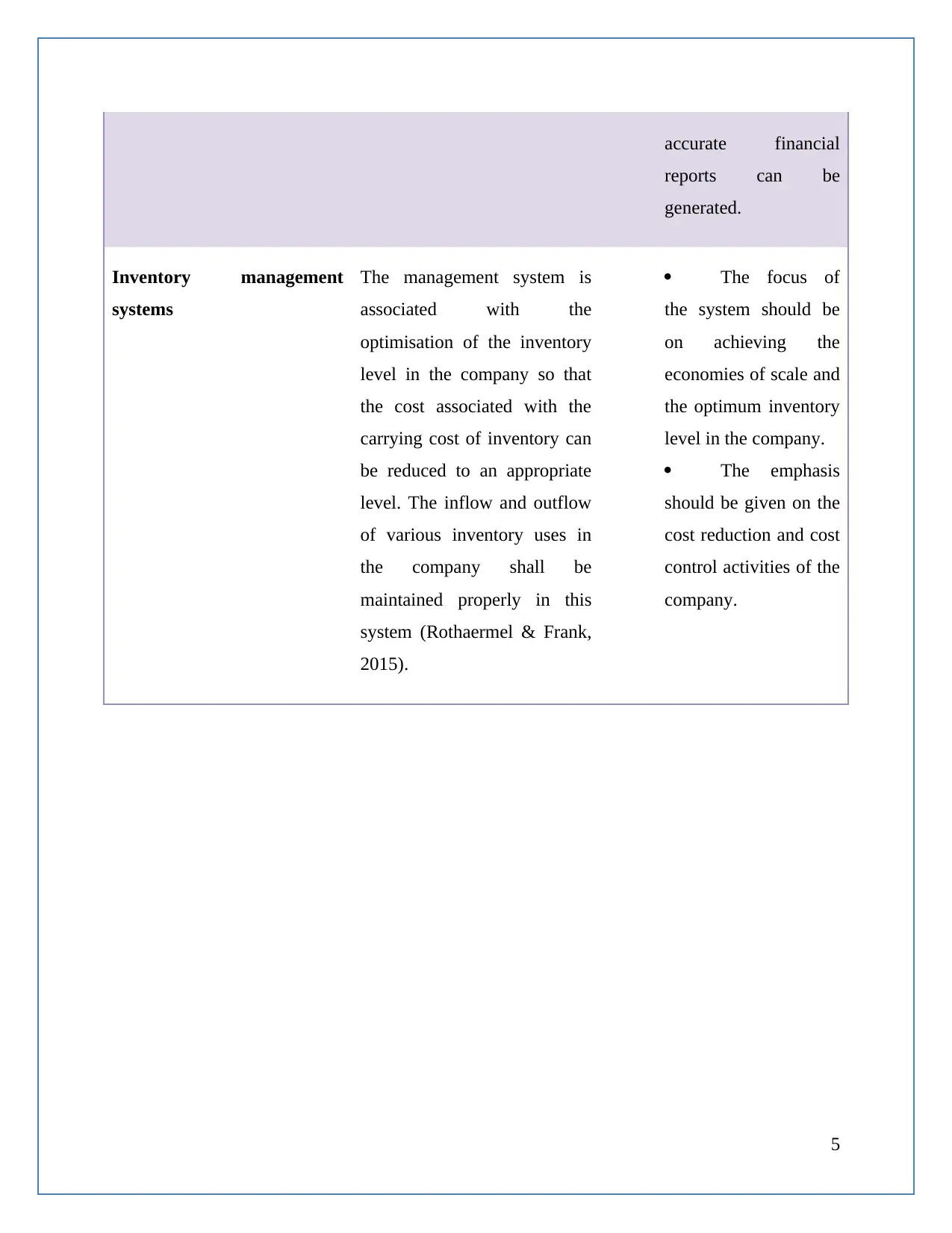

accurate financial

reports can be

generated.

Inventory management

systems

The management system is

associated with the

optimisation of the inventory

level in the company so that

the cost associated with the

carrying cost of inventory can

be reduced to an appropriate

level. The inflow and outflow

of various inventory uses in

the company shall be

maintained properly in this

system (Rothaermel & Frank,

2015).

The focus of

the system should be

on achieving the

economies of scale and

the optimum inventory

level in the company.

The emphasis

should be given on the

cost reduction and cost

control activities of the

company.

5

reports can be

generated.

Inventory management

systems

The management system is

associated with the

optimisation of the inventory

level in the company so that

the cost associated with the

carrying cost of inventory can

be reduced to an appropriate

level. The inflow and outflow

of various inventory uses in

the company shall be

maintained properly in this

system (Rothaermel & Frank,

2015).

The focus of

the system should be

on achieving the

economies of scale and

the optimum inventory

level in the company.

The emphasis

should be given on the

cost reduction and cost

control activities of the

company.

5

P2. Explain different methods used for management accounting reporting.

The different method and reports which can be used in Samsung for proper decision making and

financial reporting are as follows:

Inventory report – The inventory report of the company is concerned with maintaining

the records about the inflow and outflow of various items of inventory utilized and remaining

in the company for production of products and services of the company. The finished

products of the company along with the material remaining to be utilized in producing the

finished goods are recorded along with the prices associated with these products and material

in this report. The same can be used by the management of Samsung in order to reduce the

level of inventory and the carrying cost associate with it (Anderson, et. al., 2015).

Budgetary reports – The budgetary reports of the company are concerned with presenting

the budgeted results along with the comparison of these results with the actual results of the

company so that there can be identification of the deficiencies associated with the budgeted

performance of the company and the necessary measures can be taken accordingly. The same

can be used by Samsung in order to improve the efficiency and effectiveness of the activities

performed (Botes, et. al., 2017).

6

The different method and reports which can be used in Samsung for proper decision making and

financial reporting are as follows:

Inventory report – The inventory report of the company is concerned with maintaining

the records about the inflow and outflow of various items of inventory utilized and remaining

in the company for production of products and services of the company. The finished

products of the company along with the material remaining to be utilized in producing the

finished goods are recorded along with the prices associated with these products and material

in this report. The same can be used by the management of Samsung in order to reduce the

level of inventory and the carrying cost associate with it (Anderson, et. al., 2015).

Budgetary reports – The budgetary reports of the company are concerned with presenting

the budgeted results along with the comparison of these results with the actual results of the

company so that there can be identification of the deficiencies associated with the budgeted

performance of the company and the necessary measures can be taken accordingly. The same

can be used by Samsung in order to improve the efficiency and effectiveness of the activities

performed (Botes, et. al., 2017).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

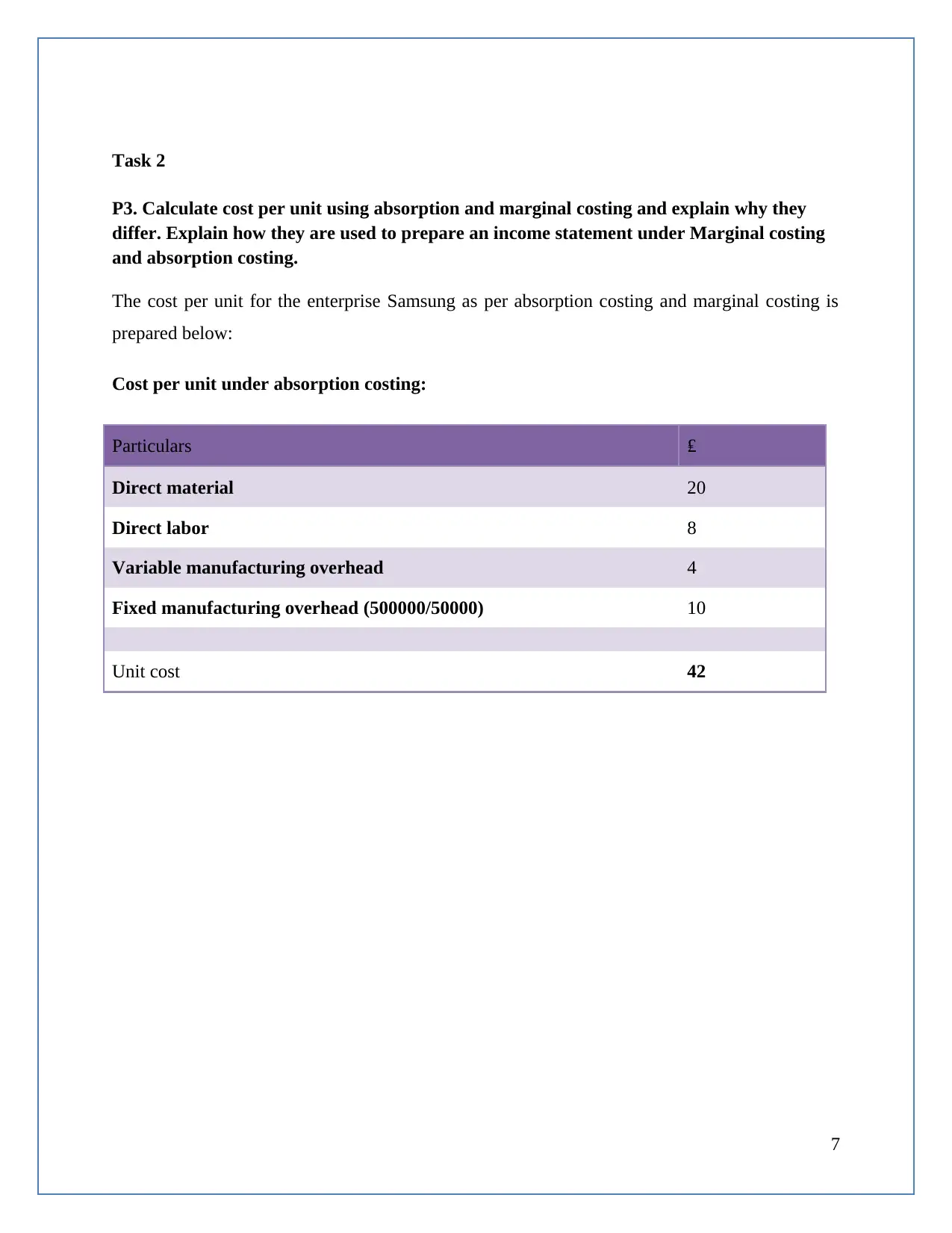

Task 2

P3. Calculate cost per unit using absorption and marginal costing and explain why they

differ. Explain how they are used to prepare an income statement under Marginal costing

and absorption costing.

The cost per unit for the enterprise Samsung as per absorption costing and marginal costing is

prepared below:

Cost per unit under absorption costing:

Particulars ₤

Direct material 20

Direct labor 8

Variable manufacturing overhead 4

Fixed manufacturing overhead (500000/50000) 10

Unit cost 42

7

P3. Calculate cost per unit using absorption and marginal costing and explain why they

differ. Explain how they are used to prepare an income statement under Marginal costing

and absorption costing.

The cost per unit for the enterprise Samsung as per absorption costing and marginal costing is

prepared below:

Cost per unit under absorption costing:

Particulars ₤

Direct material 20

Direct labor 8

Variable manufacturing overhead 4

Fixed manufacturing overhead (500000/50000) 10

Unit cost 42

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

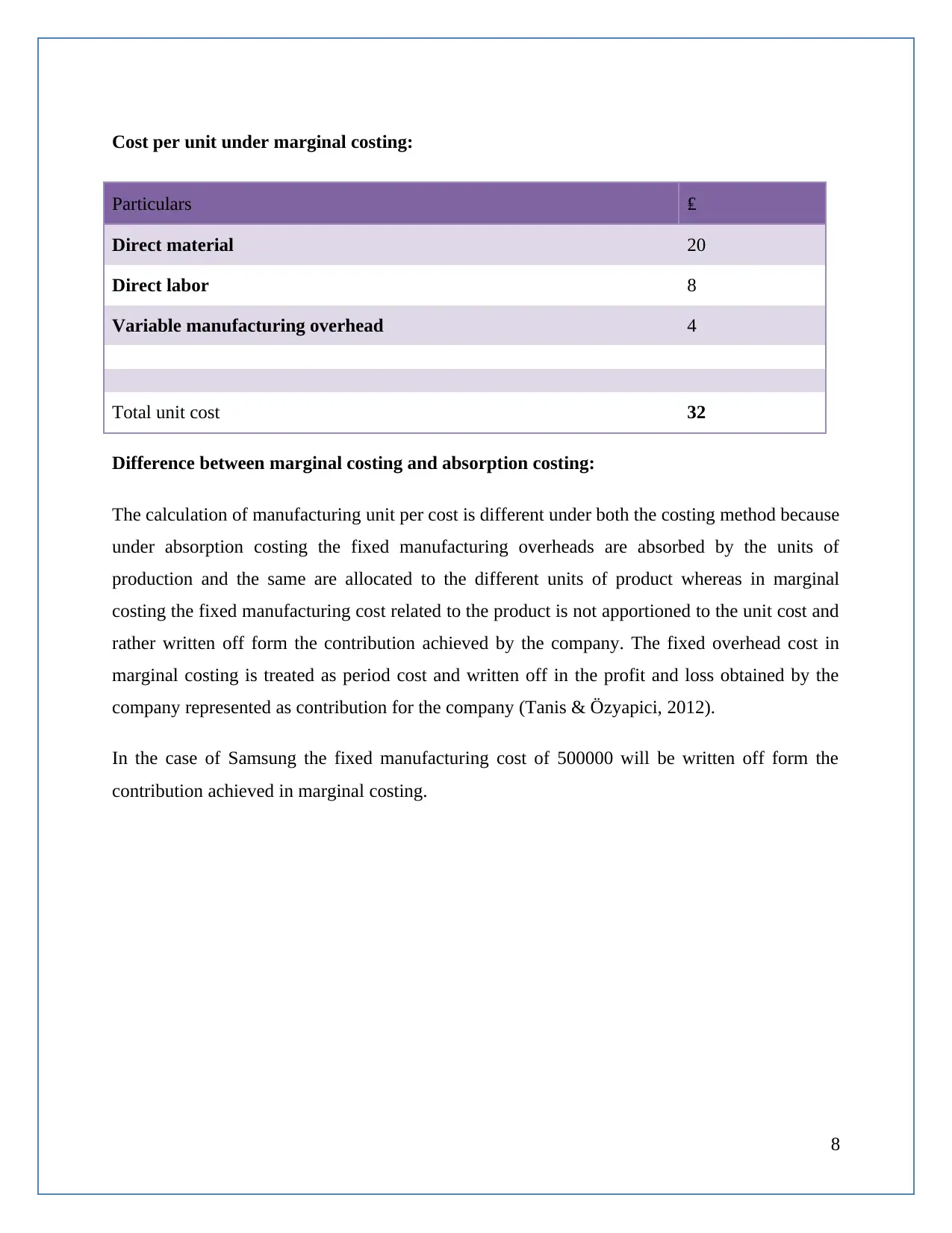

Cost per unit under marginal costing:

Particulars ₤

Direct material 20

Direct labor 8

Variable manufacturing overhead 4

Total unit cost 32

Difference between marginal costing and absorption costing:

The calculation of manufacturing unit per cost is different under both the costing method because

under absorption costing the fixed manufacturing overheads are absorbed by the units of

production and the same are allocated to the different units of product whereas in marginal

costing the fixed manufacturing cost related to the product is not apportioned to the unit cost and

rather written off form the contribution achieved by the company. The fixed overhead cost in

marginal costing is treated as period cost and written off in the profit and loss obtained by the

company represented as contribution for the company (Tanis & Özyapici, 2012).

In the case of Samsung the fixed manufacturing cost of 500000 will be written off form the

contribution achieved in marginal costing.

8

Particulars ₤

Direct material 20

Direct labor 8

Variable manufacturing overhead 4

Total unit cost 32

Difference between marginal costing and absorption costing:

The calculation of manufacturing unit per cost is different under both the costing method because

under absorption costing the fixed manufacturing overheads are absorbed by the units of

production and the same are allocated to the different units of product whereas in marginal

costing the fixed manufacturing cost related to the product is not apportioned to the unit cost and

rather written off form the contribution achieved by the company. The fixed overhead cost in

marginal costing is treated as period cost and written off in the profit and loss obtained by the

company represented as contribution for the company (Tanis & Özyapici, 2012).

In the case of Samsung the fixed manufacturing cost of 500000 will be written off form the

contribution achieved in marginal costing.

8

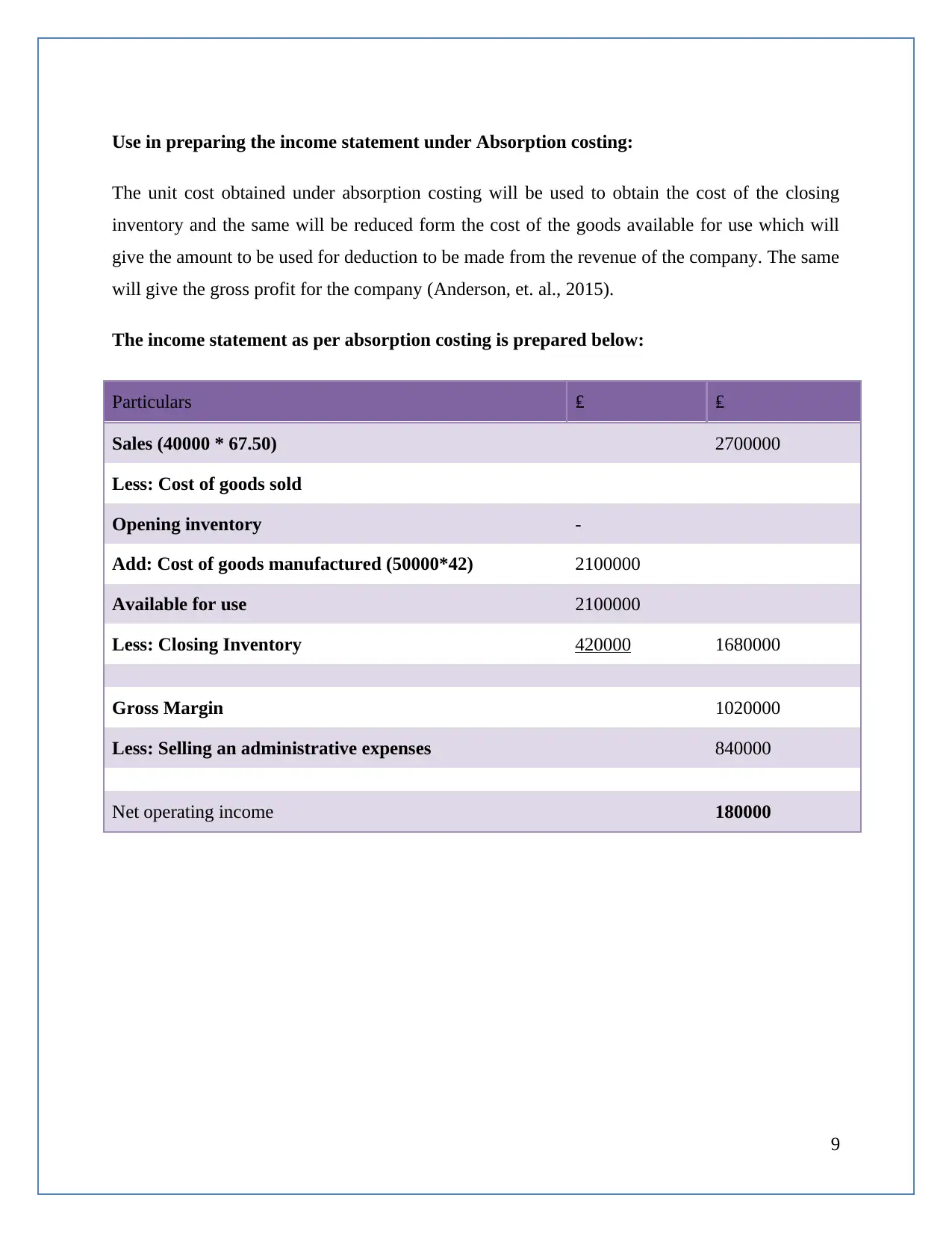

Use in preparing the income statement under Absorption costing:

The unit cost obtained under absorption costing will be used to obtain the cost of the closing

inventory and the same will be reduced form the cost of the goods available for use which will

give the amount to be used for deduction to be made from the revenue of the company. The same

will give the gross profit for the company (Anderson, et. al., 2015).

The income statement as per absorption costing is prepared below:

Particulars ₤ ₤

Sales (40000 * 67.50) 2700000

Less: Cost of goods sold

Opening inventory -

Add: Cost of goods manufactured (50000*42) 2100000

Available for use 2100000

Less: Closing Inventory 420000 1680000

Gross Margin 1020000

Less: Selling an administrative expenses 840000

Net operating income 180000

9

The unit cost obtained under absorption costing will be used to obtain the cost of the closing

inventory and the same will be reduced form the cost of the goods available for use which will

give the amount to be used for deduction to be made from the revenue of the company. The same

will give the gross profit for the company (Anderson, et. al., 2015).

The income statement as per absorption costing is prepared below:

Particulars ₤ ₤

Sales (40000 * 67.50) 2700000

Less: Cost of goods sold

Opening inventory -

Add: Cost of goods manufactured (50000*42) 2100000

Available for use 2100000

Less: Closing Inventory 420000 1680000

Gross Margin 1020000

Less: Selling an administrative expenses 840000

Net operating income 180000

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

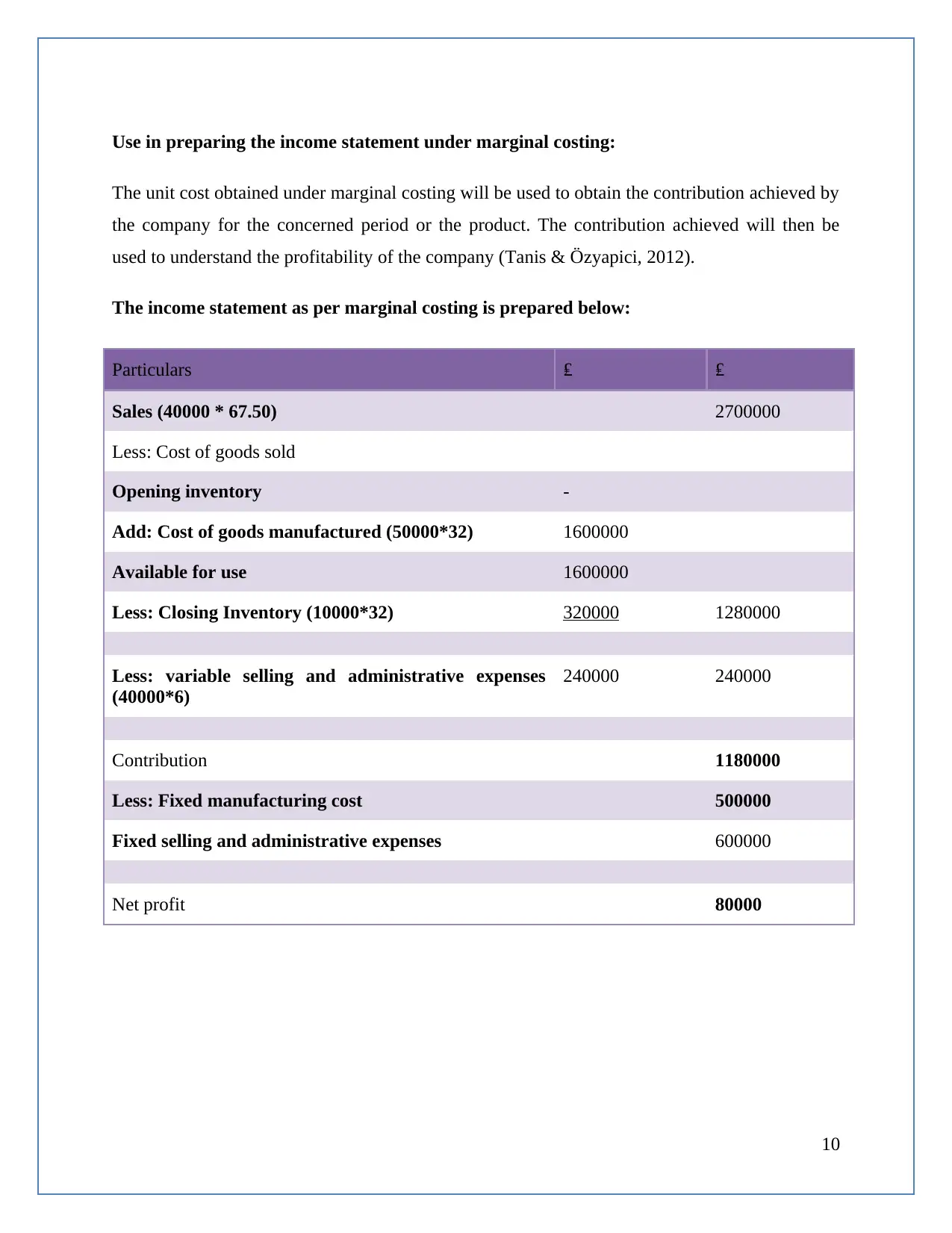

Use in preparing the income statement under marginal costing:

The unit cost obtained under marginal costing will be used to obtain the contribution achieved by

the company for the concerned period or the product. The contribution achieved will then be

used to understand the profitability of the company (Tanis & Özyapici, 2012).

The income statement as per marginal costing is prepared below:

Particulars ₤ ₤

Sales (40000 * 67.50) 2700000

Less: Cost of goods sold

Opening inventory -

Add: Cost of goods manufactured (50000*32) 1600000

Available for use 1600000

Less: Closing Inventory (10000*32) 320000 1280000

Less: variable selling and administrative expenses

(40000*6)

240000 240000

Contribution 1180000

Less: Fixed manufacturing cost 500000

Fixed selling and administrative expenses 600000

Net profit 80000

10

The unit cost obtained under marginal costing will be used to obtain the contribution achieved by

the company for the concerned period or the product. The contribution achieved will then be

used to understand the profitability of the company (Tanis & Özyapici, 2012).

The income statement as per marginal costing is prepared below:

Particulars ₤ ₤

Sales (40000 * 67.50) 2700000

Less: Cost of goods sold

Opening inventory -

Add: Cost of goods manufactured (50000*32) 1600000

Available for use 1600000

Less: Closing Inventory (10000*32) 320000 1280000

Less: variable selling and administrative expenses

(40000*6)

240000 240000

Contribution 1180000

Less: Fixed manufacturing cost 500000

Fixed selling and administrative expenses 600000

Net profit 80000

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reconciliation of net profits:

The difference in profits is due to the under absorption of fixed overheads in absorption costing

methods which amounted to ₤100000 and when the same is considered in marginal costing gives

the same net profit of ₤180000 (Cooper, 2017).

11

The difference in profits is due to the under absorption of fixed overheads in absorption costing

methods which amounted to ₤100000 and when the same is considered in marginal costing gives

the same net profit of ₤180000 (Cooper, 2017).

11

Task 3

P4. Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.

Budgetary control involves the preparation of various types of budget and comparison difference

between the actual cost and standard cost and identifying the variation between the actual cost

and standard cost. There are various tools and techniques of budgetary control. Each tool has its

own significance. As such, selection and implementation of various tools of budgetary control is

a very crucial decision and requires significant judgment. Some of the planning tools of

budgetary control are financial budget, Zero Based Budgeting and

Financial Budgets:

According to Amirya, et. al., (2014), different types of budgets are prepared under financial

budgets. Some of the most common types of budgets prepared by almost every organization are

cash budget, sales budget, expense budget, master budget and likewise (Amirya, et. al., 2014),.

Advantages of various types of financial budgets:

Preparation of cash budget is very crucial in the dynamic environment since it

forces the business enterprise to maintain a sufficient amount of cash to face any future

uncertainty. As such, the concerned organization controls their expense and accordingly

kept aside the reasonable cash.

According to Anna (2015), expenses budget preparation involves various

unreasonable assumptions and as such a significant change in any assumption may render

the budget useless. There can be a rise in the raw material prices by the supplier which

the expense budget fails to consider (Anna, 2015).

Disadvantages of various types of financial budgets:

12

P4. Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.

Budgetary control involves the preparation of various types of budget and comparison difference

between the actual cost and standard cost and identifying the variation between the actual cost

and standard cost. There are various tools and techniques of budgetary control. Each tool has its

own significance. As such, selection and implementation of various tools of budgetary control is

a very crucial decision and requires significant judgment. Some of the planning tools of

budgetary control are financial budget, Zero Based Budgeting and

Financial Budgets:

According to Amirya, et. al., (2014), different types of budgets are prepared under financial

budgets. Some of the most common types of budgets prepared by almost every organization are

cash budget, sales budget, expense budget, master budget and likewise (Amirya, et. al., 2014),.

Advantages of various types of financial budgets:

Preparation of cash budget is very crucial in the dynamic environment since it

forces the business enterprise to maintain a sufficient amount of cash to face any future

uncertainty. As such, the concerned organization controls their expense and accordingly

kept aside the reasonable cash.

According to Anna (2015), expenses budget preparation involves various

unreasonable assumptions and as such a significant change in any assumption may render

the budget useless. There can be a rise in the raw material prices by the supplier which

the expense budget fails to consider (Anna, 2015).

Disadvantages of various types of financial budgets:

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.