Management Accounting Report: Sewport and Financial Systems Analysis

VerifiedAdded on 2021/02/19

|17

|3111

|378

Report

AI Summary

This report delves into the realm of management accounting, presenting a comprehensive analysis through the lens of Alpha Financial Consultancy and its client, Sewport, a clothing manufacturer. The report explores the core principles of management accounting, contrasting it with financial accounting, and examines various management accounting systems such as cost accounting, job costing, and inventory management, highlighting their benefits and applications within Sewport. It then proceeds to analyze different types of management accounting reports, emphasizing the importance of reliable, accurate, and up-to-date information. The report further examines financial statements, including cost analysis, cost-volume-profit analysis, and costing methods like absorption and marginal costing. It also covers variance analysis, inventory valuation methods (LIFO, FIFO, and weighted average), and overhead allocation. Supporting calculations, including material variances and inventory valuations are provided. The report culminates in a detailed examination of the practical application of management accounting principles in a real-world business scenario.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

MA is an accounting which is based on monetary and non monetary information which

helps in internal management of the companies (Serena Chiucchi, 2013). Eventually, this

accounting system is applied without considering any accounting period and concepts. The

organisations implement it as per their needs. To understand in broad sense about the MA, Alpha

financial consultancy company has been chosen that provides consultancy services to different

companies which operates in manufacturing, construction etc. In the report their client company

is Sewport that operates in manufacture of clothes. Additionally, in the project report the first

scenario defines about different accounting systems and reports as well as it covers different

costing methods to prepare financial statements. While the second scenario includes different

kind of planning tools and role of MAS in response to financial problems.

TASK 1.

P1. Introduction to management accounting.

Management accounting- The MA is a typical part of accounting which is associated with

providing the financial information and suggestions to the companies for the purpose of effective

planning (Lindholm, Laine and Suomala, 2017). The above company applies this accounting for

integral management.

Management accounting system- MAS is a field of accounting that gather company's

quantitative and qualitative information for preparation of reports. The main purpose of these

reports is to helping the managers of companies to take suitable decisions.

Role of alignment of accounting systems to companies: Various accounting systems of

management accounting are very important because each of them have their own role. Like the

job costing system is useful in calculating the cost of job separately as well as inventory

management system is integrated with the solving the issues of stock management. Along with

the price optimisation system helps in determining the prices. Such as in Sewport they use these

accounting systems for purpose of effective management of cost regarding to jobs as well as for

better stock management of cloths.

Origin, role and principle of MAS:

MA is an accounting which is based on monetary and non monetary information which

helps in internal management of the companies (Serena Chiucchi, 2013). Eventually, this

accounting system is applied without considering any accounting period and concepts. The

organisations implement it as per their needs. To understand in broad sense about the MA, Alpha

financial consultancy company has been chosen that provides consultancy services to different

companies which operates in manufacturing, construction etc. In the report their client company

is Sewport that operates in manufacture of clothes. Additionally, in the project report the first

scenario defines about different accounting systems and reports as well as it covers different

costing methods to prepare financial statements. While the second scenario includes different

kind of planning tools and role of MAS in response to financial problems.

TASK 1.

P1. Introduction to management accounting.

Management accounting- The MA is a typical part of accounting which is associated with

providing the financial information and suggestions to the companies for the purpose of effective

planning (Lindholm, Laine and Suomala, 2017). The above company applies this accounting for

integral management.

Management accounting system- MAS is a field of accounting that gather company's

quantitative and qualitative information for preparation of reports. The main purpose of these

reports is to helping the managers of companies to take suitable decisions.

Role of alignment of accounting systems to companies: Various accounting systems of

management accounting are very important because each of them have their own role. Like the

job costing system is useful in calculating the cost of job separately as well as inventory

management system is integrated with the solving the issues of stock management. Along with

the price optimisation system helps in determining the prices. Such as in Sewport they use these

accounting systems for purpose of effective management of cost regarding to jobs as well as for

better stock management of cloths.

Origin, role and principle of MAS:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Origin- The term management accounting system was evolved by cost accounting

techniques which was developed in England during revolution of industry (Stechemesser and

Guenther, 2012).

Principles - The MAS is based on different principles such as influence, relevance, value

and trust. These principles are needed to be implemented for management accounting system.

Distinction between financial and management accounting system:

Basis Management accounting system Financial accounting system

Information This accounting system consists

both kind of accounting information

such as quantitative and qualitative

information.

While this contains only financial

information.

Accounting

principles

The management accounting does

not follow any accounting principle

and concepts

This accounting system is implemented as

per the accounting period and concepts.

Compulsory It is not necessary for the companies

to apply this accounting system.

On the other hand, it is essential for the

companies to adopt this accounting

system.

Different type of MAS- The MA includes a wide range of accounting systems and some of

them are mentioned below:

Cost accounting system- It related to computing total cost of different activities.

Eventually, it is important for controlling and managing overall cost. Such as in the

Sewport company, this system is important for in analysing cost of their different

operations.

Job costing system-It is related to the computing cost of job associated in of activities

(McVay, Kennedy and Fullerton, 2016). This helps in provide information about how

much cost is occurring in the process of job of various functions. In Sewport company,

they applies this accounting system is guidance of their consultancy company for the

purpose of getting information about job cost.

techniques which was developed in England during revolution of industry (Stechemesser and

Guenther, 2012).

Principles - The MAS is based on different principles such as influence, relevance, value

and trust. These principles are needed to be implemented for management accounting system.

Distinction between financial and management accounting system:

Basis Management accounting system Financial accounting system

Information This accounting system consists

both kind of accounting information

such as quantitative and qualitative

information.

While this contains only financial

information.

Accounting

principles

The management accounting does

not follow any accounting principle

and concepts

This accounting system is implemented as

per the accounting period and concepts.

Compulsory It is not necessary for the companies

to apply this accounting system.

On the other hand, it is essential for the

companies to adopt this accounting

system.

Different type of MAS- The MA includes a wide range of accounting systems and some of

them are mentioned below:

Cost accounting system- It related to computing total cost of different activities.

Eventually, it is important for controlling and managing overall cost. Such as in the

Sewport company, this system is important for in analysing cost of their different

operations.

Job costing system-It is related to the computing cost of job associated in of activities

(McVay, Kennedy and Fullerton, 2016). This helps in provide information about how

much cost is occurring in the process of job of various functions. In Sewport company,

they applies this accounting system is guidance of their consultancy company for the

purpose of getting information about job cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory management system- It is associated with management of the stocks such as

raw material, finished goods etc. In above respected company, they have implemented

this accounting system for managing raw material for production of cloths.

Price optimisation system- This is related to the determining the prices of products and

services at an accurate level. For example in the Sewport company, they implement this

system for fixing price of their cloths.

Benefits of management accounting systems- The management accounting systems are

beneficial in the different activities of the organisations. Herein, benefit of these systems is

mentioned below:

Management accounting

system

Benefits

Cost accounting system It is beneficial in computing total cost of activities. Like in the

Sewport clothing company, they measure the cost of different

activities of manufacturing of cloths.

Job costing system It is import for computing the cost of job of various activities. Such

as in the above mentioned company, it is beneficial in providing

information about cost of job of various activities.

Inventory management

system

It is beneficial in effective management of raw material so that

companies can make better use of resources. In the Sewport

company, this is useful in taking effective decision about production

of new cloths as per the information of available finished goods.

Price optimisation system This is important for determination of the price of products and

services (Schaltegger, 2012). In the above company, they use this

accounting system for fixing the price of their products at an

efficient level.

raw material, finished goods etc. In above respected company, they have implemented

this accounting system for managing raw material for production of cloths.

Price optimisation system- This is related to the determining the prices of products and

services at an accurate level. For example in the Sewport company, they implement this

system for fixing price of their cloths.

Benefits of management accounting systems- The management accounting systems are

beneficial in the different activities of the organisations. Herein, benefit of these systems is

mentioned below:

Management accounting

system

Benefits

Cost accounting system It is beneficial in computing total cost of activities. Like in the

Sewport clothing company, they measure the cost of different

activities of manufacturing of cloths.

Job costing system It is import for computing the cost of job of various activities. Such

as in the above mentioned company, it is beneficial in providing

information about cost of job of various activities.

Inventory management

system

It is beneficial in effective management of raw material so that

companies can make better use of resources. In the Sewport

company, this is useful in taking effective decision about production

of new cloths as per the information of available finished goods.

Price optimisation system This is important for determination of the price of products and

services (Schaltegger, 2012). In the above company, they use this

accounting system for fixing the price of their products at an

efficient level.

P2. Different kind of management accounting reports.

Characteristics of better information system- This is necessary that information which is used

in the management accounting reports. Some of the characteristics are as follows:

Reliability- It is associated with a kind of information which must be reliable with the

financial transaction of the organisations. So that they can take suitable decision for further

activities.

Accuracy-This is essential that information should be accurate as per the financial

transactions. Without accuracy it will be difficult for companies to make accurate financial

reports.

Up to date- The financial transactions of the companies can not be remain same. So it is

important that financial informations should be updated for better results.

Role of presenting the informations in an understanding manner: This is important that

financial information should be easy and understanding manner so that companies can make

crucial decisions. Without this, it will be difficult for the organisations to make financial reports

and due to this many other issues may arise. Eventually, the accurate financial information helps

in taking effective decisions so it is mandatory that financial information should be

understandable.

Various kind of managerial accounting reports-

Inventory management reports- These reports provide information about the stock

available in the warehouses (Schaltegger, 2012). It consists, quantity of RM , finished

goods etc. Due to this companies can take further decisions about the buying of new RM.

Such as in the Sewport company, they produce it for analysing the cost of storage and

need of RM.

Budget report- It is related to providing information about actual financial performance of

the company. By this report companies can measure their performance and can take

decisions accordingly. Like in the above respected company, they use it for analysing the

actual performance and make corrective changes accordingly.

Characteristics of better information system- This is necessary that information which is used

in the management accounting reports. Some of the characteristics are as follows:

Reliability- It is associated with a kind of information which must be reliable with the

financial transaction of the organisations. So that they can take suitable decision for further

activities.

Accuracy-This is essential that information should be accurate as per the financial

transactions. Without accuracy it will be difficult for companies to make accurate financial

reports.

Up to date- The financial transactions of the companies can not be remain same. So it is

important that financial informations should be updated for better results.

Role of presenting the informations in an understanding manner: This is important that

financial information should be easy and understanding manner so that companies can make

crucial decisions. Without this, it will be difficult for the organisations to make financial reports

and due to this many other issues may arise. Eventually, the accurate financial information helps

in taking effective decisions so it is mandatory that financial information should be

understandable.

Various kind of managerial accounting reports-

Inventory management reports- These reports provide information about the stock

available in the warehouses (Schaltegger, 2012). It consists, quantity of RM , finished

goods etc. Due to this companies can take further decisions about the buying of new RM.

Such as in the Sewport company, they produce it for analysing the cost of storage and

need of RM.

Budget report- It is related to providing information about actual financial performance of

the company. By this report companies can measure their performance and can take

decisions accordingly. Like in the above respected company, they use it for analysing the

actual performance and make corrective changes accordingly.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Account receivable ageing report- It provides detailed information about total collective

amount from different debtors (Rossing, 2013). With the help of this report companies

can check about how much collection they have in the market from the debtors. As well

as these reports consist about date on which payment is due by the debtors. Such as in

Sewport, company they use if for collecting the amount which is due by their debtors or

from credit sale.

Performance report- It is prepared for purpose of evaluating the actual performance of

employees and different activities. In this report, various kind of information is included

such as financial and non financial. In the Sewport company, they use it for evaluating

their actual performance.

TASK 2.

P3 Financial statements.

Cost- It can be defined as a combination of all the expenses which occurs in process of

operating different operations (Myers, 2013). Such as in the Sewport company, various kind of

cost occurs like cost of material, manufacturing etc. As well as some other costs like direct cost,

indirect cost, fixed and variable etc. While the cost analysis is related to calculating overall cost

of different activities so that financial position can be determined.

Cost volume profit- It is related to the determining variation in expenditures and

volume. Main purpose of it, is to evaluating financial performance on basis of change in

expenditure and volume. In Sewport they conduct this analysis for measure the variation in the

cost and profit.

Flexible budgeting- This is budgeting techniques in that budgets are being flexed or

changed if sales or volume changes. In Sewport company, they apply this budgeting for

evaluating the effect of sales and volume on the budgets.

Cost variance- In general terms, the cost variance is related to the difference between the

actual costs with the budgeted cost. Purpose of this is to finding the actual difference in the

costs. Like in the above respected company they calculate the actual variance in the costs for

minimising the cost of different activities.

Absorption & marginal costing:

amount from different debtors (Rossing, 2013). With the help of this report companies

can check about how much collection they have in the market from the debtors. As well

as these reports consist about date on which payment is due by the debtors. Such as in

Sewport, company they use if for collecting the amount which is due by their debtors or

from credit sale.

Performance report- It is prepared for purpose of evaluating the actual performance of

employees and different activities. In this report, various kind of information is included

such as financial and non financial. In the Sewport company, they use it for evaluating

their actual performance.

TASK 2.

P3 Financial statements.

Cost- It can be defined as a combination of all the expenses which occurs in process of

operating different operations (Myers, 2013). Such as in the Sewport company, various kind of

cost occurs like cost of material, manufacturing etc. As well as some other costs like direct cost,

indirect cost, fixed and variable etc. While the cost analysis is related to calculating overall cost

of different activities so that financial position can be determined.

Cost volume profit- It is related to the determining variation in expenditures and

volume. Main purpose of it, is to evaluating financial performance on basis of change in

expenditure and volume. In Sewport they conduct this analysis for measure the variation in the

cost and profit.

Flexible budgeting- This is budgeting techniques in that budgets are being flexed or

changed if sales or volume changes. In Sewport company, they apply this budgeting for

evaluating the effect of sales and volume on the budgets.

Cost variance- In general terms, the cost variance is related to the difference between the

actual costs with the budgeted cost. Purpose of this is to finding the actual difference in the

costs. Like in the above respected company they calculate the actual variance in the costs for

minimising the cost of different activities.

Absorption & marginal costing:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Absorption costing- In this variable and production costs are considered as product cost.

(Clinton and White, 2015).

Marginal costing- This is a kind of costing technique in that fixed cost is considered as

the period cost and variable cost as the product cost.

Cost allocation- It is related to assigning cost to different activities. Above mentioned

company, apply this for allocating the overheads to various kind activities.

Fixed cost- It is a cost that do not flex if output changes. Some example of fixed cost is

rent, telephone charges etc. Such as in the Sewport company, whether they may increase or

decrease the production but fixed cost will remain same. .

Variable cost-It is a cost which changes as the change in level of output. In the above

respected company, their variable costs are such as cost of labour, material etc.

Normal costing- This can be defined as the total cost of any particular commodity

including different costs like labour cost, overhead etc.

Standard costing- This is also known by the estimated costing. In this costing, cost is

estimated for the purpose of comparing the actual cost. For example, Sewport company, they

estimate future cost of activities.

Activity based costing- This is a kind of costing under that cost is assigned for different

activities separately. Like in above respected company, they accumulate the cost of various

activities individually.

Inventory cost- It is a type of cost that incurs in the process of storing the stock in the

warehouses. This includes cost of ordering, carrying etc. Such as mentioned company, they

calculates storage cost for the purpose of minimising the cost as much as possible.

Valuation methods- The stock is being valued by various kind of method. Some of these

methods are mentioned below:

LIFO- This is associated with the manufacturing of products with the use of raw material

that was brought last (Houghton, 2013). Like in the above respected company, apply this method

for clearing of their warehouse as well as to offer goods on demand.

FIFO- This is associated with the manufacturing of products with the use of raw material

that was brought first. Such as Sewport company use this method for those goods which are

needed to be consumed as soon as possible.

(Clinton and White, 2015).

Marginal costing- This is a kind of costing technique in that fixed cost is considered as

the period cost and variable cost as the product cost.

Cost allocation- It is related to assigning cost to different activities. Above mentioned

company, apply this for allocating the overheads to various kind activities.

Fixed cost- It is a cost that do not flex if output changes. Some example of fixed cost is

rent, telephone charges etc. Such as in the Sewport company, whether they may increase or

decrease the production but fixed cost will remain same. .

Variable cost-It is a cost which changes as the change in level of output. In the above

respected company, their variable costs are such as cost of labour, material etc.

Normal costing- This can be defined as the total cost of any particular commodity

including different costs like labour cost, overhead etc.

Standard costing- This is also known by the estimated costing. In this costing, cost is

estimated for the purpose of comparing the actual cost. For example, Sewport company, they

estimate future cost of activities.

Activity based costing- This is a kind of costing under that cost is assigned for different

activities separately. Like in above respected company, they accumulate the cost of various

activities individually.

Inventory cost- It is a type of cost that incurs in the process of storing the stock in the

warehouses. This includes cost of ordering, carrying etc. Such as mentioned company, they

calculates storage cost for the purpose of minimising the cost as much as possible.

Valuation methods- The stock is being valued by various kind of method. Some of these

methods are mentioned below:

LIFO- This is associated with the manufacturing of products with the use of raw material

that was brought last (Houghton, 2013). Like in the above respected company, apply this method

for clearing of their warehouse as well as to offer goods on demand.

FIFO- This is associated with the manufacturing of products with the use of raw material

that was brought first. Such as Sewport company use this method for those goods which are

needed to be consumed as soon as possible.

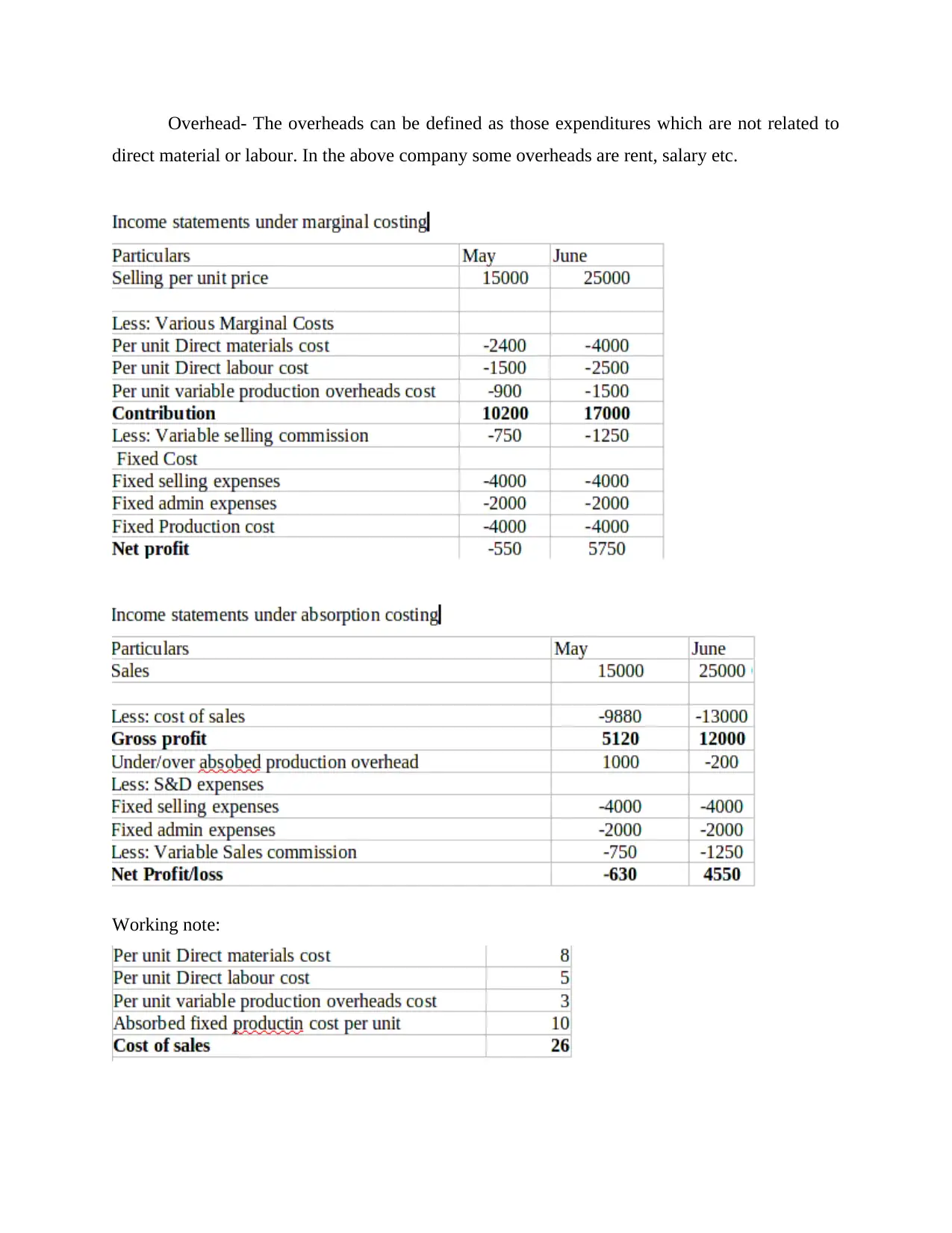

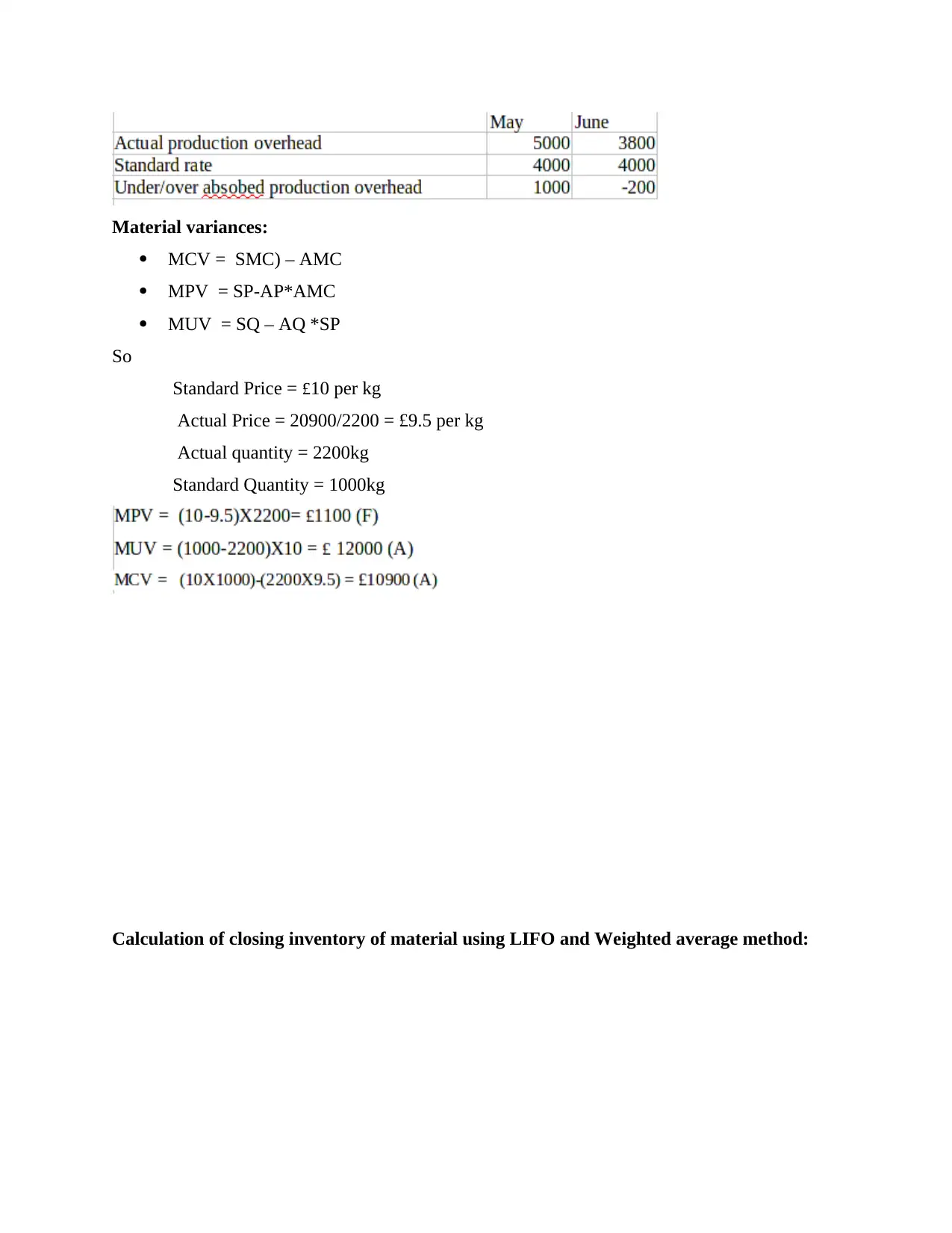

Overhead- The overheads can be defined as those expenditures which are not related to

direct material or labour. In the above company some overheads are rent, salary etc.

Working note:

direct material or labour. In the above company some overheads are rent, salary etc.

Working note:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Material variances:

MCV = SMC) – AMC

MPV = SP-AP*AMC

MUV = SQ – AQ *SP

So

Standard Price = £10 per kg

Actual Price = 20900/2200 = £9.5 per kg

Actual quantity = 2200kg

Standard Quantity = 1000kg

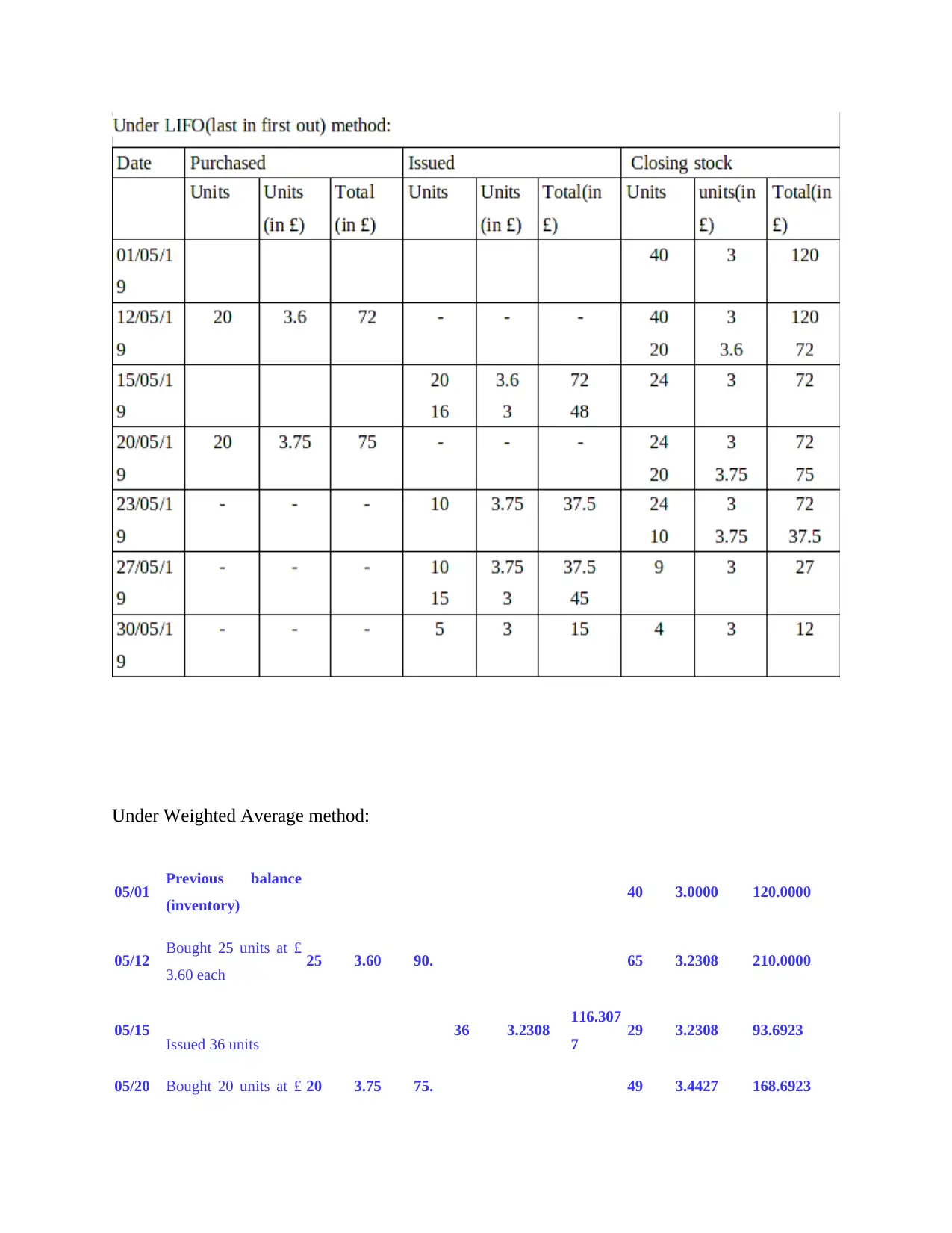

Calculation of closing inventory of material using LIFO and Weighted average method:

MCV = SMC) – AMC

MPV = SP-AP*AMC

MUV = SQ – AQ *SP

So

Standard Price = £10 per kg

Actual Price = 20900/2200 = £9.5 per kg

Actual quantity = 2200kg

Standard Quantity = 1000kg

Calculation of closing inventory of material using LIFO and Weighted average method:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Under Weighted Average method:

05/01 Previous balance

(inventory) 40 3.0000 120.0000

05/12 Bought 25 units at £

3.60 each 25 3.60 90. 65 3.2308 210.0000

05/15 Issued 36 units 36 3.2308 116.307

7 29 3.2308 93.6923

05/20 Bought 20 units at £ 20 3.75 75. 49 3.4427 168.6923

05/01 Previous balance

(inventory) 40 3.0000 120.0000

05/12 Bought 25 units at £

3.60 each 25 3.60 90. 65 3.2308 210.0000

05/15 Issued 36 units 36 3.2308 116.307

7 29 3.2308 93.6923

05/20 Bought 20 units at £ 20 3.75 75. 49 3.4427 168.6923

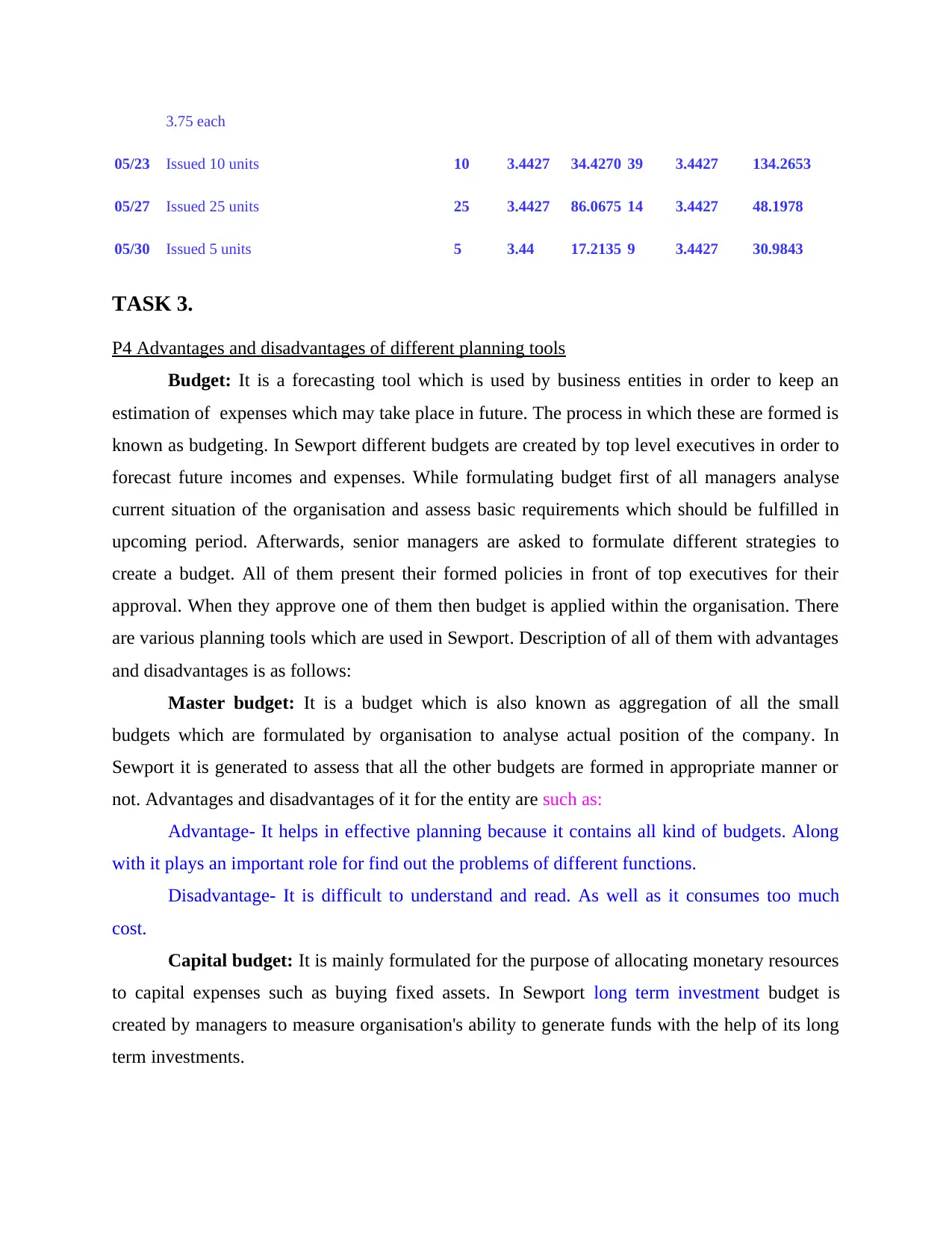

3.75 each

05/23 Issued 10 units 10 3.4427 34.4270 39 3.4427 134.2653

05/27 Issued 25 units 25 3.4427 86.0675 14 3.4427 48.1978

05/30 Issued 5 units 5 3.44 17.2135 9 3.4427 30.9843

TASK 3.

P4 Advantages and disadvantages of different planning tools

Budget: It is a forecasting tool which is used by business entities in order to keep an

estimation of expenses which may take place in future. The process in which these are formed is

known as budgeting. In Sewport different budgets are created by top level executives in order to

forecast future incomes and expenses. While formulating budget first of all managers analyse

current situation of the organisation and assess basic requirements which should be fulfilled in

upcoming period. Afterwards, senior managers are asked to formulate different strategies to

create a budget. All of them present their formed policies in front of top executives for their

approval. When they approve one of them then budget is applied within the organisation. There

are various planning tools which are used in Sewport. Description of all of them with advantages

and disadvantages is as follows:

Master budget: It is a budget which is also known as aggregation of all the small

budgets which are formulated by organisation to analyse actual position of the company. In

Sewport it is generated to assess that all the other budgets are formed in appropriate manner or

not. Advantages and disadvantages of it for the entity are such as:

Advantage- It helps in effective planning because it contains all kind of budgets. Along

with it plays an important role for find out the problems of different functions.

Disadvantage- It is difficult to understand and read. As well as it consumes too much

cost.

Capital budget: It is mainly formulated for the purpose of allocating monetary resources

to capital expenses such as buying fixed assets. In Sewport long term investment budget is

created by managers to measure organisation's ability to generate funds with the help of its long

term investments.

05/23 Issued 10 units 10 3.4427 34.4270 39 3.4427 134.2653

05/27 Issued 25 units 25 3.4427 86.0675 14 3.4427 48.1978

05/30 Issued 5 units 5 3.44 17.2135 9 3.4427 30.9843

TASK 3.

P4 Advantages and disadvantages of different planning tools

Budget: It is a forecasting tool which is used by business entities in order to keep an

estimation of expenses which may take place in future. The process in which these are formed is

known as budgeting. In Sewport different budgets are created by top level executives in order to

forecast future incomes and expenses. While formulating budget first of all managers analyse

current situation of the organisation and assess basic requirements which should be fulfilled in

upcoming period. Afterwards, senior managers are asked to formulate different strategies to

create a budget. All of them present their formed policies in front of top executives for their

approval. When they approve one of them then budget is applied within the organisation. There

are various planning tools which are used in Sewport. Description of all of them with advantages

and disadvantages is as follows:

Master budget: It is a budget which is also known as aggregation of all the small

budgets which are formulated by organisation to analyse actual position of the company. In

Sewport it is generated to assess that all the other budgets are formed in appropriate manner or

not. Advantages and disadvantages of it for the entity are such as:

Advantage- It helps in effective planning because it contains all kind of budgets. Along

with it plays an important role for find out the problems of different functions.

Disadvantage- It is difficult to understand and read. As well as it consumes too much

cost.

Capital budget: It is mainly formulated for the purpose of allocating monetary resources

to capital expenses such as buying fixed assets. In Sewport long term investment budget is

created by managers to measure organisation's ability to generate funds with the help of its long

term investments.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.