Management Accounting Report: Sewport Financial Analysis & Planning

VerifiedAdded on 2020/11/23

|20

|5172

|343

Report

AI Summary

This report delves into the realm of management accounting, emphasizing its crucial role in organizational decision-making and financial performance enhancement, specifically within the context of Sewport. It explores the core principles, diverse types of management accounting systems such as cost accounting and inventory management, and their seamless integration into business operations. The report critically evaluates the advantages of these systems and their reporting mechanisms within organizational processes, alongside the benefits of price optimization systems. Furthermore, it presents calculations and analyses related to financial statements and planning tools, including budgets, using the example of Nero Ltd. The report also highlights the significance of management accounting in addressing financial challenges and achieving sustainable success, offering valuable insights for students seeking a comprehensive understanding of this essential field. The report also encompasses the importance of management accounting in dealing with financial problems and achieving sustainable success.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

LO 1 and LO 2.................................................................................................................................1

1. Importance of management accounting for decision making process of company in

improving financial performance................................................................................................1

2. Different types of management accounting systems used in reporting and its integration in

business operations......................................................................................................................3

3. Critically evaluating the benefits of management accounting system and MA reporting with

organizational process ................................................................................................................4

4. Calculation of income statements...........................................................................................6

LO 3...............................................................................................................................................10

Comparing and analysing of different planning tools used in management accounting of Nero

Ltd.............................................................................................................................................10

LO 4...............................................................................................................................................12

Importance of management accounting in dealing financial problems and achieving

sustainable success....................................................................................................................12

CONCLUSIONS............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

LO 1 and LO 2.................................................................................................................................1

1. Importance of management accounting for decision making process of company in

improving financial performance................................................................................................1

2. Different types of management accounting systems used in reporting and its integration in

business operations......................................................................................................................3

3. Critically evaluating the benefits of management accounting system and MA reporting with

organizational process ................................................................................................................4

4. Calculation of income statements...........................................................................................6

LO 3...............................................................................................................................................10

Comparing and analysing of different planning tools used in management accounting of Nero

Ltd.............................................................................................................................................10

LO 4...............................................................................................................................................12

Importance of management accounting in dealing financial problems and achieving

sustainable success....................................................................................................................12

CONCLUSIONS............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is method which used by managers for the provision of

accounting information which helps in developing effective information for the maximization of

profit for entity. This present report provides an information related to management accounting

in context of company Sewport. In this report an explanation is to be provided on management

accounting and its importance on decision making process with types of management accounting

with its integration in business. Further, in this report calculations with the explanation of

different planning tools of budget is explained with view of Nero ltd. and importance of

management accounting in solving financial problems of the organisations.

LO 1 and LO 2

1. Importance of management accounting for decision making process of company in improving

financial performance

Management accounting is the process which is known for identifying, measuring,

analysing, interpreting and for communicating information of organisations to achieve overall

business goals (Importance of Management Accounting, 2018). It overall helps managers of

Sewport organisation to clarify the decision problems, specifying criteria and identifying

alternatives by which decision making model developed and to collect data which set an

alternative. This overall will lead to develop effective strategies and policies for improvement of

organisation.

Management accountant is the tool which is used to design and implement accounting

information system so that effective production, marketing and financial decision will get

developed to get better business operations. Another importance of management accounting is to

protect future of firm by developing effective competitive strategies for organisation.

Management accounting used by business organisation's for knowing overall amount of

money which has been spent in developing business operations. It is also used by management

just to analyse availability of resources which needs to develop for improving capabilities of

organisations (Kaplan and Atkinson, 2015). Therefore, not only managers used management

accounting but it is also important for stakeholders which helps in developing effective policies.

Importance of management accounting in decision making is as follows-

Analysing expenses and revenue:

1

Management accounting is method which used by managers for the provision of

accounting information which helps in developing effective information for the maximization of

profit for entity. This present report provides an information related to management accounting

in context of company Sewport. In this report an explanation is to be provided on management

accounting and its importance on decision making process with types of management accounting

with its integration in business. Further, in this report calculations with the explanation of

different planning tools of budget is explained with view of Nero ltd. and importance of

management accounting in solving financial problems of the organisations.

LO 1 and LO 2

1. Importance of management accounting for decision making process of company in improving

financial performance

Management accounting is the process which is known for identifying, measuring,

analysing, interpreting and for communicating information of organisations to achieve overall

business goals (Importance of Management Accounting, 2018). It overall helps managers of

Sewport organisation to clarify the decision problems, specifying criteria and identifying

alternatives by which decision making model developed and to collect data which set an

alternative. This overall will lead to develop effective strategies and policies for improvement of

organisation.

Management accountant is the tool which is used to design and implement accounting

information system so that effective production, marketing and financial decision will get

developed to get better business operations. Another importance of management accounting is to

protect future of firm by developing effective competitive strategies for organisation.

Management accounting used by business organisation's for knowing overall amount of

money which has been spent in developing business operations. It is also used by management

just to analyse availability of resources which needs to develop for improving capabilities of

organisations (Kaplan and Atkinson, 2015). Therefore, not only managers used management

accounting but it is also important for stakeholders which helps in developing effective policies.

Importance of management accounting in decision making is as follows-

Analysing expenses and revenue:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Revenue refers to money which is earned by company by their business operations. More

emphasis of company is to reduce their expenses and to increase its overall revenue because

revenue refers to profitability of company. Expenses of the company include salaries, rent,

payments and cost which incurred for developing effective production in company. Therefore,

management accounting helps managers in getting accurate figures of revenues and expenses.

This analysis of revenue and expenses helps managers in developing effective strategies for

reducing expenses and for generating better revenues.

Creating Budgets and Forecasting Ideas for growth:

Once analysis is done regarding revenue and expenses, role of management accounting is

to develop effective budget for forecasting business projects and operations with in organisation.

This development of budget will overall helps management in achieving long term growth and

profitability of organisation from business market. Management accounting provides accurate

figures and data's which overall helps in developing effective strategic policies. Policies are

developed by comparing previous year performance which result in getting effective sustainable

growth of the company (Otley, 2016).

Development of confidential information:

For the development of effective strategies, accounting managers will guide decision

makers of company regarding the raw data's and numbers for implementing changes in

organisation. This analysis of raw data, helps management in developing effective actionable

policies. Information generated in management accounting are provided to users of the company

which overall helps upper management in taking company in profitable situation which overall

result in developing competitive advantage of company in business market.

Helps in understanding performance variances:

Management accounting used by managers for developing variances which helps

managers on predicting goals which needs to achieved for developing better operations of

organisation. Therefore, role of management accounting is to analyse techniques which overall

helps management in building positive variance in achieving sustainable growth of the

organisation.

2

emphasis of company is to reduce their expenses and to increase its overall revenue because

revenue refers to profitability of company. Expenses of the company include salaries, rent,

payments and cost which incurred for developing effective production in company. Therefore,

management accounting helps managers in getting accurate figures of revenues and expenses.

This analysis of revenue and expenses helps managers in developing effective strategies for

reducing expenses and for generating better revenues.

Creating Budgets and Forecasting Ideas for growth:

Once analysis is done regarding revenue and expenses, role of management accounting is

to develop effective budget for forecasting business projects and operations with in organisation.

This development of budget will overall helps management in achieving long term growth and

profitability of organisation from business market. Management accounting provides accurate

figures and data's which overall helps in developing effective strategic policies. Policies are

developed by comparing previous year performance which result in getting effective sustainable

growth of the company (Otley, 2016).

Development of confidential information:

For the development of effective strategies, accounting managers will guide decision

makers of company regarding the raw data's and numbers for implementing changes in

organisation. This analysis of raw data, helps management in developing effective actionable

policies. Information generated in management accounting are provided to users of the company

which overall helps upper management in taking company in profitable situation which overall

result in developing competitive advantage of company in business market.

Helps in understanding performance variances:

Management accounting used by managers for developing variances which helps

managers on predicting goals which needs to achieved for developing better operations of

organisation. Therefore, role of management accounting is to analyse techniques which overall

helps management in building positive variance in achieving sustainable growth of the

organisation.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

These are the importance of management accounting which analyse resources and

strategies by which effective decisions will get developed for improving performance of

organisation. Specific data's are provided by management accountant for developing decision in

areas which needs to get improve in achieving future goals of the company (Fullerton, Kennedy

and Widener, 2014).

2. Different types of management accounting systems used in reporting and its integration in

business operations

Management accounting system is process which is used in decision making, devising

planning with emphasis on controlling objects of organisation. Management accounting report is

used as tools in understanding business operations of the organisation. Sewport is an enterprise

which will use this management accounting system for integrating effective business operations.

Different techniques of management accounting are used by accountant of organisation which

outline requirement of resources which needs to develop in improving financial capabilities of

organisation. Its techniques are as follows-

Cost accounting system: it is the system used by manufacturers which helps in recording

production activities of organisation using perpetual inventory system. This accounting system

used in organisation to measure the cost of products which provide sufficient profitability,

inventory valuation and cost control. This cost accounting system helps organisation in

evaluating product which is more profitable. This only possible when company will able to

measure correct cost of products. There are two cost accounting system that product costing and

job order costing (Höglund and et.al., 2016).

Job order costing helps Sewport organisations in accumulating manufacturing cost for

each job of the organisation. Entities which apply this type of costing evaluation are generally

ones which are engaged in the production of unique and special orders. For example:- event

management company are the one which used this costing technique in accumulating

manufacturing cost of organisation.

Process costing is the another cost accounting techniques which accumulate

manufacturing cost which is separate from each process of the Sewport company. This method is

generally appropriate for products whose productions are generally innovated in different

departments of organisation.

3

strategies by which effective decisions will get developed for improving performance of

organisation. Specific data's are provided by management accountant for developing decision in

areas which needs to get improve in achieving future goals of the company (Fullerton, Kennedy

and Widener, 2014).

2. Different types of management accounting systems used in reporting and its integration in

business operations

Management accounting system is process which is used in decision making, devising

planning with emphasis on controlling objects of organisation. Management accounting report is

used as tools in understanding business operations of the organisation. Sewport is an enterprise

which will use this management accounting system for integrating effective business operations.

Different techniques of management accounting are used by accountant of organisation which

outline requirement of resources which needs to develop in improving financial capabilities of

organisation. Its techniques are as follows-

Cost accounting system: it is the system used by manufacturers which helps in recording

production activities of organisation using perpetual inventory system. This accounting system

used in organisation to measure the cost of products which provide sufficient profitability,

inventory valuation and cost control. This cost accounting system helps organisation in

evaluating product which is more profitable. This only possible when company will able to

measure correct cost of products. There are two cost accounting system that product costing and

job order costing (Höglund and et.al., 2016).

Job order costing helps Sewport organisations in accumulating manufacturing cost for

each job of the organisation. Entities which apply this type of costing evaluation are generally

ones which are engaged in the production of unique and special orders. For example:- event

management company are the one which used this costing technique in accumulating

manufacturing cost of organisation.

Process costing is the another cost accounting techniques which accumulate

manufacturing cost which is separate from each process of the Sewport company. This method is

generally appropriate for products whose productions are generally innovated in different

departments of organisation.

3

Inventory management system: it is the method which used to measure which is used to

oversee the flow of inventory which comes and out from organisation. In this type of system,

management will ensure to keep right inventory at right place and at the right time by which

effective business operations will get developed in an entity. This system helps in developing

effective capabilities by which customers demand will get fulfilled in a proper delivery of time.

Sewport company generally follows inventory management systems are the one which

are engaged in retail business, service delivery and also in companies which track their produced

assets (Laudon and Laudon, 2016). These techniques used by organisation in providing their

services to customers in proper time. LIFO and FIFO method is also used in this system. LIFO

method is the assumption in which last item which purchase is sold first. FIFO method is the

assumption regarding first in first out means first purchased goods are sold first.

Price Optimization system: it is the process which is used by managers of organisation to

find that price of products which customers are willing to pay in business market. This is known

as effective tool for management accounting in deciding prices of the products of organisation.

This method used to calculate demand which varies at different price levels. This is the method

used to target customers of the market which overall helps in producing profitability in the

organisation.

Companies which follows price optimization model are the one which are engaged in

providing diversifies products among customers of business market. All these systems are used

by managers reporting and in integration in business operation is useful so that effective

strategies get developed in achieving future goals of Sewport organisation.

3. Critically evaluating the benefits of management accounting system and MA reporting with

organizational process

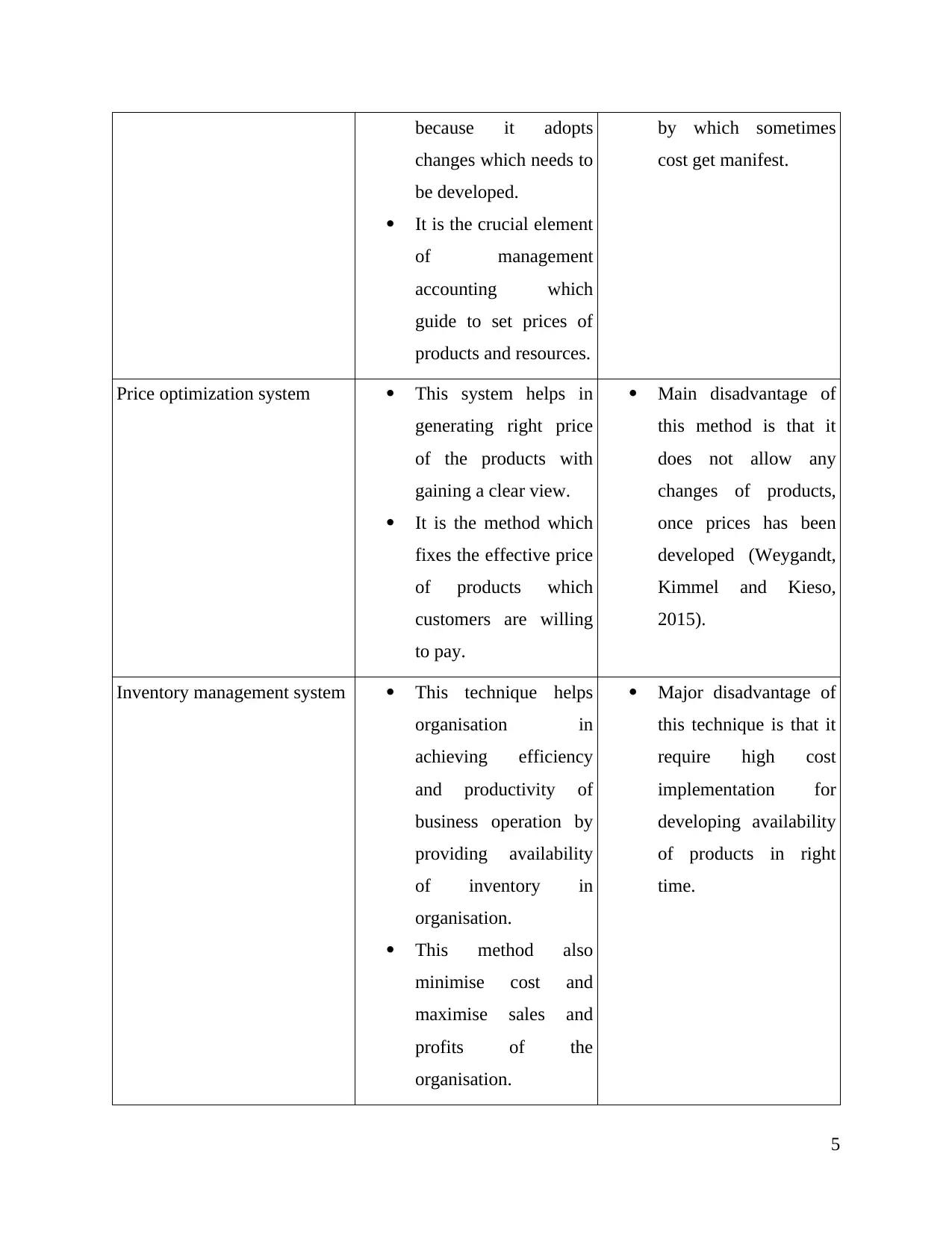

Importance of management accounting system

Management accounting system is important at all levels of management accounting. Above

discussed three management accounting systems are cost accounting system, price optimization

system and inventory management system. Its importance are as follows-

Methods Advantages disadvantages

Cost accounting system Cost accounting

appreciated by mangers

of the company

Cost accounting

method differ from one

organisation to another

4

oversee the flow of inventory which comes and out from organisation. In this type of system,

management will ensure to keep right inventory at right place and at the right time by which

effective business operations will get developed in an entity. This system helps in developing

effective capabilities by which customers demand will get fulfilled in a proper delivery of time.

Sewport company generally follows inventory management systems are the one which

are engaged in retail business, service delivery and also in companies which track their produced

assets (Laudon and Laudon, 2016). These techniques used by organisation in providing their

services to customers in proper time. LIFO and FIFO method is also used in this system. LIFO

method is the assumption in which last item which purchase is sold first. FIFO method is the

assumption regarding first in first out means first purchased goods are sold first.

Price Optimization system: it is the process which is used by managers of organisation to

find that price of products which customers are willing to pay in business market. This is known

as effective tool for management accounting in deciding prices of the products of organisation.

This method used to calculate demand which varies at different price levels. This is the method

used to target customers of the market which overall helps in producing profitability in the

organisation.

Companies which follows price optimization model are the one which are engaged in

providing diversifies products among customers of business market. All these systems are used

by managers reporting and in integration in business operation is useful so that effective

strategies get developed in achieving future goals of Sewport organisation.

3. Critically evaluating the benefits of management accounting system and MA reporting with

organizational process

Importance of management accounting system

Management accounting system is important at all levels of management accounting. Above

discussed three management accounting systems are cost accounting system, price optimization

system and inventory management system. Its importance are as follows-

Methods Advantages disadvantages

Cost accounting system Cost accounting

appreciated by mangers

of the company

Cost accounting

method differ from one

organisation to another

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

because it adopts

changes which needs to

be developed.

It is the crucial element

of management

accounting which

guide to set prices of

products and resources.

by which sometimes

cost get manifest.

Price optimization system This system helps in

generating right price

of the products with

gaining a clear view.

It is the method which

fixes the effective price

of products which

customers are willing

to pay.

Main disadvantage of

this method is that it

does not allow any

changes of products,

once prices has been

developed (Weygandt,

Kimmel and Kieso,

2015).

Inventory management system This technique helps

organisation in

achieving efficiency

and productivity of

business operation by

providing availability

of inventory in

organisation.

This method also

minimise cost and

maximise sales and

profits of the

organisation.

Major disadvantage of

this technique is that it

require high cost

implementation for

developing availability

of products in right

time.

5

changes which needs to

be developed.

It is the crucial element

of management

accounting which

guide to set prices of

products and resources.

by which sometimes

cost get manifest.

Price optimization system This system helps in

generating right price

of the products with

gaining a clear view.

It is the method which

fixes the effective price

of products which

customers are willing

to pay.

Main disadvantage of

this method is that it

does not allow any

changes of products,

once prices has been

developed (Weygandt,

Kimmel and Kieso,

2015).

Inventory management system This technique helps

organisation in

achieving efficiency

and productivity of

business operation by

providing availability

of inventory in

organisation.

This method also

minimise cost and

maximise sales and

profits of the

organisation.

Major disadvantage of

this technique is that it

require high cost

implementation for

developing availability

of products in right

time.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

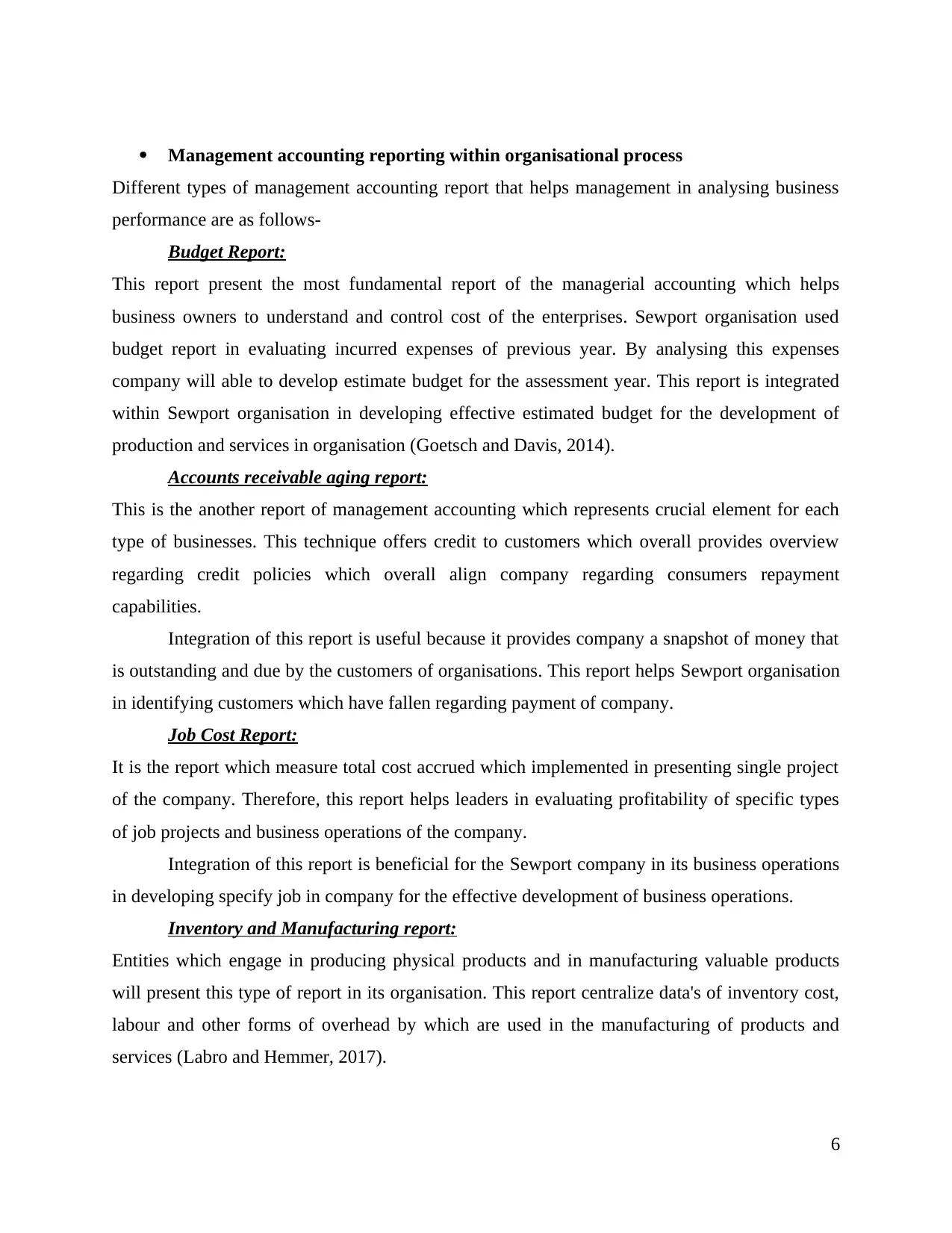

Management accounting reporting within organisational process

Different types of management accounting report that helps management in analysing business

performance are as follows-

Budget Report:

This report present the most fundamental report of the managerial accounting which helps

business owners to understand and control cost of the enterprises. Sewport organisation used

budget report in evaluating incurred expenses of previous year. By analysing this expenses

company will able to develop estimate budget for the assessment year. This report is integrated

within Sewport organisation in developing effective estimated budget for the development of

production and services in organisation (Goetsch and Davis, 2014).

Accounts receivable aging report:

This is the another report of management accounting which represents crucial element for each

type of businesses. This technique offers credit to customers which overall provides overview

regarding credit policies which overall align company regarding consumers repayment

capabilities.

Integration of this report is useful because it provides company a snapshot of money that

is outstanding and due by the customers of organisations. This report helps Sewport organisation

in identifying customers which have fallen regarding payment of company.

Job Cost Report:

It is the report which measure total cost accrued which implemented in presenting single project

of the company. Therefore, this report helps leaders in evaluating profitability of specific types

of job projects and business operations of the company.

Integration of this report is beneficial for the Sewport company in its business operations

in developing specify job in company for the effective development of business operations.

Inventory and Manufacturing report:

Entities which engage in producing physical products and in manufacturing valuable products

will present this type of report in its organisation. This report centralize data's of inventory cost,

labour and other forms of overhead by which are used in the manufacturing of products and

services (Labro and Hemmer, 2017).

6

Different types of management accounting report that helps management in analysing business

performance are as follows-

Budget Report:

This report present the most fundamental report of the managerial accounting which helps

business owners to understand and control cost of the enterprises. Sewport organisation used

budget report in evaluating incurred expenses of previous year. By analysing this expenses

company will able to develop estimate budget for the assessment year. This report is integrated

within Sewport organisation in developing effective estimated budget for the development of

production and services in organisation (Goetsch and Davis, 2014).

Accounts receivable aging report:

This is the another report of management accounting which represents crucial element for each

type of businesses. This technique offers credit to customers which overall provides overview

regarding credit policies which overall align company regarding consumers repayment

capabilities.

Integration of this report is useful because it provides company a snapshot of money that

is outstanding and due by the customers of organisations. This report helps Sewport organisation

in identifying customers which have fallen regarding payment of company.

Job Cost Report:

It is the report which measure total cost accrued which implemented in presenting single project

of the company. Therefore, this report helps leaders in evaluating profitability of specific types

of job projects and business operations of the company.

Integration of this report is beneficial for the Sewport company in its business operations

in developing specify job in company for the effective development of business operations.

Inventory and Manufacturing report:

Entities which engage in producing physical products and in manufacturing valuable products

will present this type of report in its organisation. This report centralize data's of inventory cost,

labour and other forms of overhead by which are used in the manufacturing of products and

services (Labro and Hemmer, 2017).

6

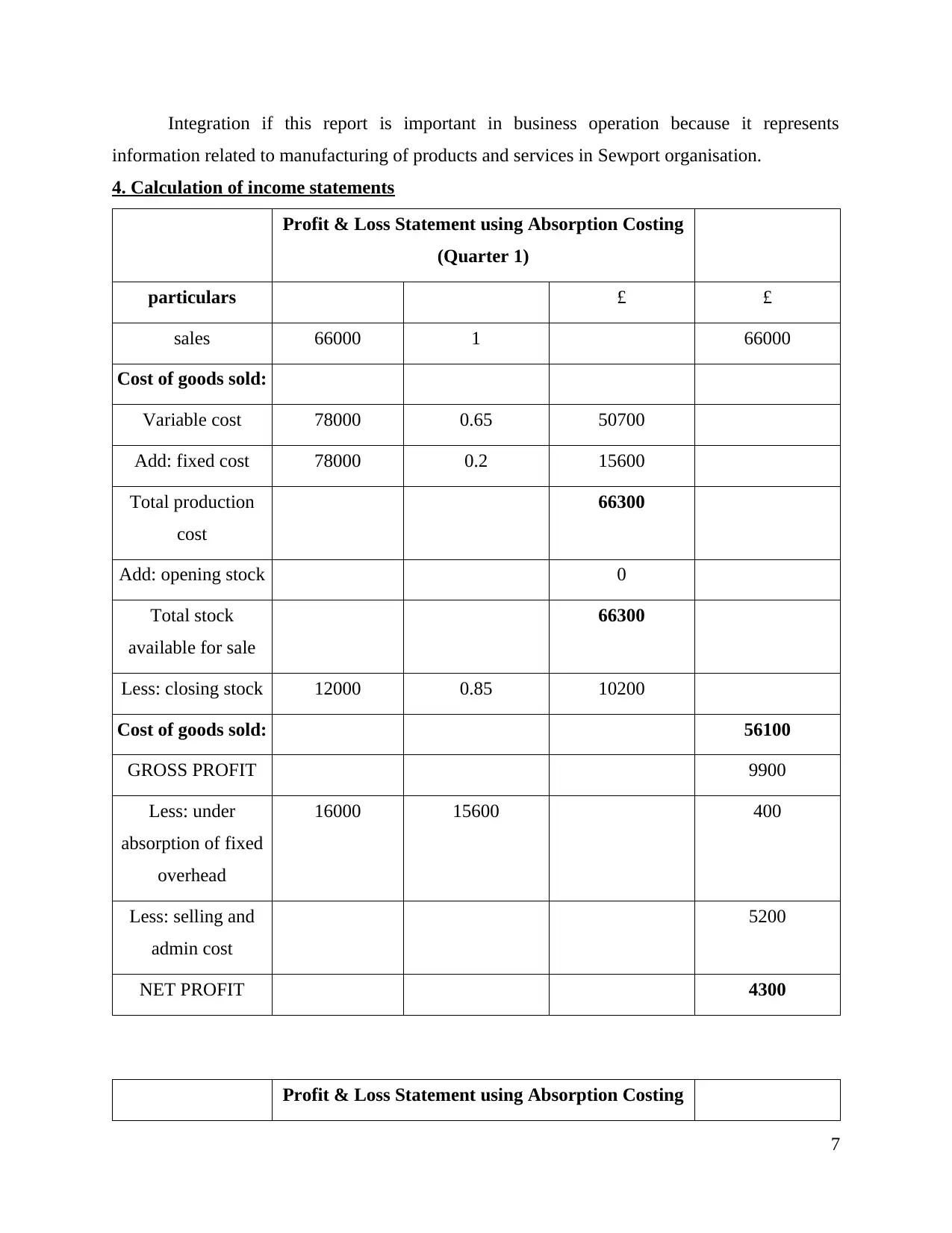

Integration if this report is important in business operation because it represents

information related to manufacturing of products and services in Sewport organisation.

4. Calculation of income statements

Profit & Loss Statement using Absorption Costing

(Quarter 1)

particulars £ £

sales 66000 1 66000

Cost of goods sold:

Variable cost 78000 0.65 50700

Add: fixed cost 78000 0.2 15600

Total production

cost

66300

Add: opening stock 0

Total stock

available for sale

66300

Less: closing stock 12000 0.85 10200

Cost of goods sold: 56100

GROSS PROFIT 9900

Less: under

absorption of fixed

overhead

16000 15600 400

Less: selling and

admin cost

5200

NET PROFIT 4300

Profit & Loss Statement using Absorption Costing

7

information related to manufacturing of products and services in Sewport organisation.

4. Calculation of income statements

Profit & Loss Statement using Absorption Costing

(Quarter 1)

particulars £ £

sales 66000 1 66000

Cost of goods sold:

Variable cost 78000 0.65 50700

Add: fixed cost 78000 0.2 15600

Total production

cost

66300

Add: opening stock 0

Total stock

available for sale

66300

Less: closing stock 12000 0.85 10200

Cost of goods sold: 56100

GROSS PROFIT 9900

Less: under

absorption of fixed

overhead

16000 15600 400

Less: selling and

admin cost

5200

NET PROFIT 4300

Profit & Loss Statement using Absorption Costing

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

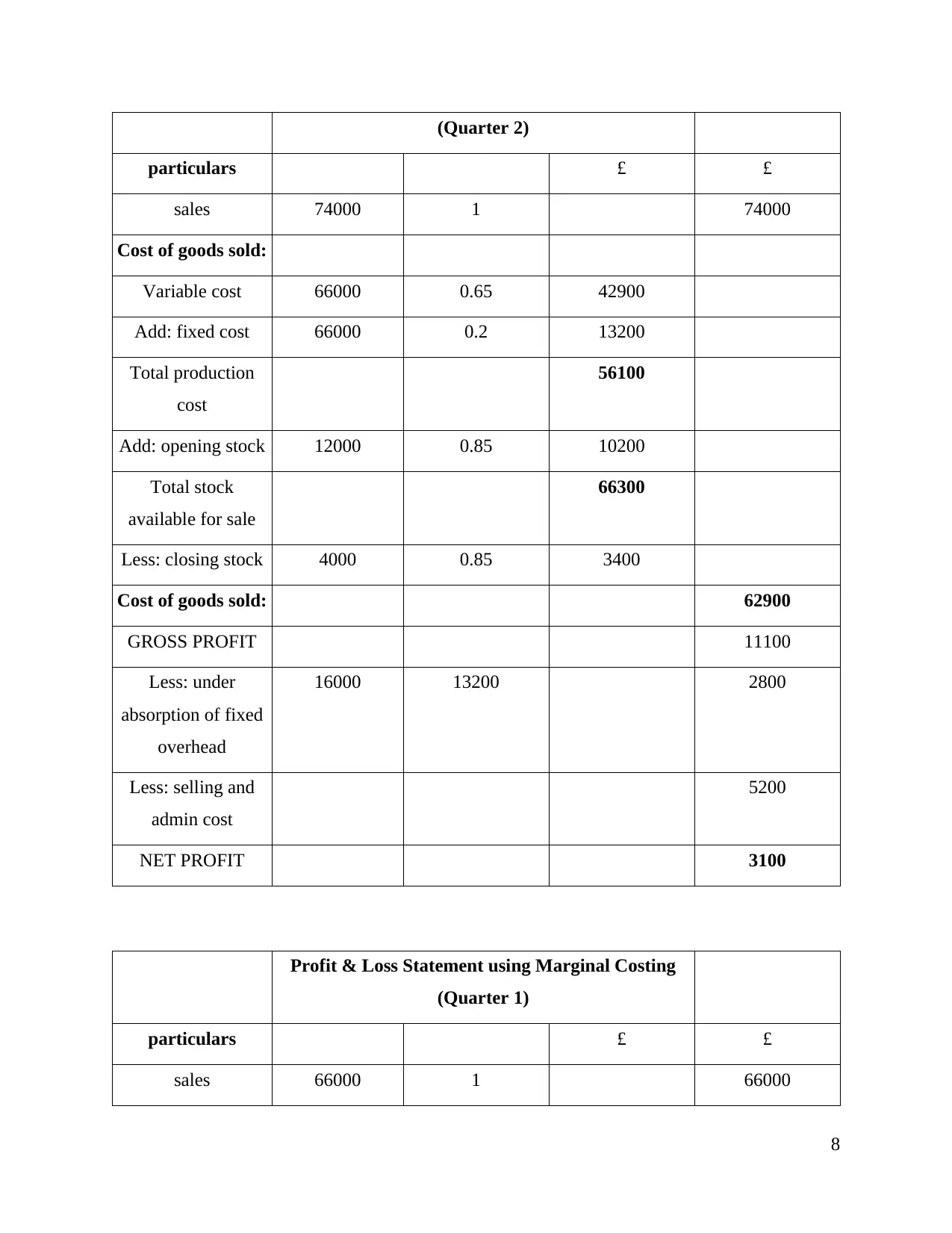

(Quarter 2)

particulars £ £

sales 74000 1 74000

Cost of goods sold:

Variable cost 66000 0.65 42900

Add: fixed cost 66000 0.2 13200

Total production

cost

56100

Add: opening stock 12000 0.85 10200

Total stock

available for sale

66300

Less: closing stock 4000 0.85 3400

Cost of goods sold: 62900

GROSS PROFIT 11100

Less: under

absorption of fixed

overhead

16000 13200 2800

Less: selling and

admin cost

5200

NET PROFIT 3100

Profit & Loss Statement using Marginal Costing

(Quarter 1)

particulars £ £

sales 66000 1 66000

8

particulars £ £

sales 74000 1 74000

Cost of goods sold:

Variable cost 66000 0.65 42900

Add: fixed cost 66000 0.2 13200

Total production

cost

56100

Add: opening stock 12000 0.85 10200

Total stock

available for sale

66300

Less: closing stock 4000 0.85 3400

Cost of goods sold: 62900

GROSS PROFIT 11100

Less: under

absorption of fixed

overhead

16000 13200 2800

Less: selling and

admin cost

5200

NET PROFIT 3100

Profit & Loss Statement using Marginal Costing

(Quarter 1)

particulars £ £

sales 66000 1 66000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Production cost:

Variable cost 78000 0.65 50700

Add: opening stock 0

Total stock

available for sale

50700

Less: closing stock 12000 0.65 7800

Cost of goods sold: 42900

Contribution

margin

23100

Less: fixed

manufacturing

overhead

16000 13200 16000

Less: selling and

admin cost

5200

NET PROFIT 19000

Profit & Loss Statement using Marginal Costing

(Quarter 2)

particulars £ £

sales 74000 1 74000

Production cost:

Variable cost 66000 0.65 42900

Add: opening stock 1200 0.65 7800

Total stock

available for sale

50700

9

Variable cost 78000 0.65 50700

Add: opening stock 0

Total stock

available for sale

50700

Less: closing stock 12000 0.65 7800

Cost of goods sold: 42900

Contribution

margin

23100

Less: fixed

manufacturing

overhead

16000 13200 16000

Less: selling and

admin cost

5200

NET PROFIT 19000

Profit & Loss Statement using Marginal Costing

(Quarter 2)

particulars £ £

sales 74000 1 74000

Production cost:

Variable cost 66000 0.65 42900

Add: opening stock 1200 0.65 7800

Total stock

available for sale

50700

9

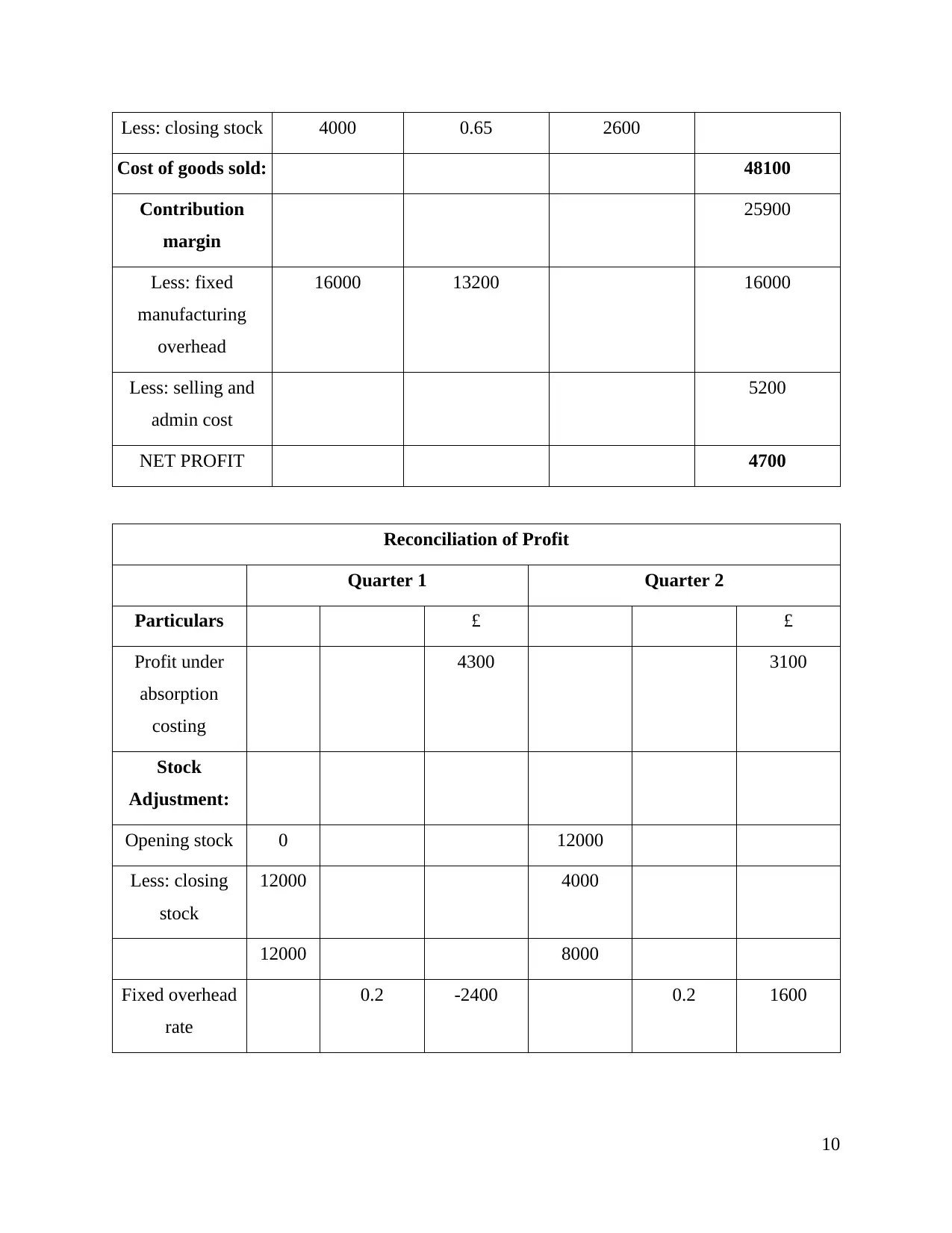

Less: closing stock 4000 0.65 2600

Cost of goods sold: 48100

Contribution

margin

25900

Less: fixed

manufacturing

overhead

16000 13200 16000

Less: selling and

admin cost

5200

NET PROFIT 4700

Reconciliation of Profit

Quarter 1 Quarter 2

Particulars £ £

Profit under

absorption

costing

4300 3100

Stock

Adjustment:

Opening stock 0 12000

Less: closing

stock

12000 4000

12000 8000

Fixed overhead

rate

0.2 -2400 0.2 1600

10

Cost of goods sold: 48100

Contribution

margin

25900

Less: fixed

manufacturing

overhead

16000 13200 16000

Less: selling and

admin cost

5200

NET PROFIT 4700

Reconciliation of Profit

Quarter 1 Quarter 2

Particulars £ £

Profit under

absorption

costing

4300 3100

Stock

Adjustment:

Opening stock 0 12000

Less: closing

stock

12000 4000

12000 8000

Fixed overhead

rate

0.2 -2400 0.2 1600

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.