Management Accounting Report: Financial Analysis of Shell Corporation

VerifiedAdded on 2023/01/13

|12

|3150

|77

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and systems, focusing on Shell Corporation's financial challenges. The report delves into the core concepts of management accounting, including its role in providing information for internal decision-making. It examines various management accounting systems such as inventory management, cost accounting, and price optimization, highlighting their importance in Shell's operations. The report also explores management accounting reporting, including cost reports, performance reports, and inventory reports. Furthermore, the report applies techniques like marginal and absorption costing to analyze income statements and evaluate financial performance. It examines planning tools of budgetary control, discussing the merits and demerits of zero-based budgeting, rolling budgets, and operating budgets. Finally, the report identifies financial problems faced by Shell and suggests appropriate management accounting systems, such as key performance indicators and benchmarking, to address these challenges and improve financial outcomes.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Management Accounting and Systems:......................................................................................3

Management Accounting Reporting...........................................................................................5

TASK 2............................................................................................................................................6

Using techniques for income statement......................................................................................6

TASK 3............................................................................................................................................7

Planning tools of budgetary control with merit and demerit.......................................................7

TASK 4............................................................................................................................................9

Financial provable of business and appropriate management accounting system.....................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Management Accounting and Systems:......................................................................................3

Management Accounting Reporting...........................................................................................5

TASK 2............................................................................................................................................6

Using techniques for income statement......................................................................................6

TASK 3............................................................................................................................................7

Planning tools of budgetary control with merit and demerit.......................................................7

TASK 4............................................................................................................................................9

Financial provable of business and appropriate management accounting system.....................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting is classified as procedures and methods that concentrate on use

of organizational resources in order to help management staff in their task of maximizing

customer satisfaction as well as shareholder wealth (Kumarasiri, 2017). This emphasises on

information and details for entity's internal users and support their decisions taken in relation to

entity. This study contains comprehensive discussion on multiple aspects and areas of

management accounting and concerned systems along with core requirements in context of

corporation Shell. Company is running around more than 1100 service stations all around the UK

and is in partnership with Costa Coffee and Deli2Go. It also consists explanations on techniques

of MA and comparison of manner of utilization of MA in responding to multiple fiscal problems.

TASK

Management Accounting and Systems:

Management accounting is set of approaches mainly used for evaluating and recording

information on financial activities within organisations, for managers to utilize in planning,

progress, control, measurement and decision-making. Key role of management accounting in

business is to provide and circulate information/data to managing officials within information

especially for managing tasks and decision-making. Management Accounting encompasses

numerous accounting method and techniques that may be beneficial to management staff in

carrying out its functions of planning, coordinating Interacting and other related staff. MA's

primary functions are to gather, analyse and report data regarding company's operations and

financial resources.

Management Accounting Principles: The Management Accounting Principles are

guidelines designed to meet the key requirements of organizational management to enhance the

strategies of decision making, internal business operations, resource use, customer satisfaction,

and capability utilization required to optimally meet organizational goals (Larmande, 2016).

Here are tow major principles of MA, as follows: Principle of Causality: Principle of Causality allows modelling corporation's costs

depended on critical relationship among organisational inputs as well as outputs of

multiple resources used in distinct-distinct functions of organisation.

Management accounting is classified as procedures and methods that concentrate on use

of organizational resources in order to help management staff in their task of maximizing

customer satisfaction as well as shareholder wealth (Kumarasiri, 2017). This emphasises on

information and details for entity's internal users and support their decisions taken in relation to

entity. This study contains comprehensive discussion on multiple aspects and areas of

management accounting and concerned systems along with core requirements in context of

corporation Shell. Company is running around more than 1100 service stations all around the UK

and is in partnership with Costa Coffee and Deli2Go. It also consists explanations on techniques

of MA and comparison of manner of utilization of MA in responding to multiple fiscal problems.

TASK

Management Accounting and Systems:

Management accounting is set of approaches mainly used for evaluating and recording

information on financial activities within organisations, for managers to utilize in planning,

progress, control, measurement and decision-making. Key role of management accounting in

business is to provide and circulate information/data to managing officials within information

especially for managing tasks and decision-making. Management Accounting encompasses

numerous accounting method and techniques that may be beneficial to management staff in

carrying out its functions of planning, coordinating Interacting and other related staff. MA's

primary functions are to gather, analyse and report data regarding company's operations and

financial resources.

Management Accounting Principles: The Management Accounting Principles are

guidelines designed to meet the key requirements of organizational management to enhance the

strategies of decision making, internal business operations, resource use, customer satisfaction,

and capability utilization required to optimally meet organizational goals (Larmande, 2016).

Here are tow major principles of MA, as follows: Principle of Causality: Principle of Causality allows modelling corporation's costs

depended on critical relationship among organisational inputs as well as outputs of

multiple resources used in distinct-distinct functions of organisation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Principle of Analogy: This principle regulate different users of managerial accounting

output information's quality to utilize involved knowledge or reviews through planning,

controls.

Management Accounting System: It regarded as specified frameworks utilised by

managing personnels to deal with different tasks of business and generate information for

managerial decision-making phase. In this regard following are several systems and their

requirements in context of Shell:

Inventory management system: It is a technique of management accounting which is

used to identify and monitoring each unit of product available in business entity. In other words,

inventory management system is the combination of hardware and software tools which helps

managers to analysing, controlling and maintaining stock level of the organisation. Managers

uses various technique to maintain stock level of their entity (Mkrtychev, Ochepovsky and Enik,

2018). They use ABC analysis, VED analysis, inventory management software’s to identify

minimum, maximum and dangerous level of their stock. Organisations apply this system in order

to effectively and efficiently manage operating cycle of their department.

Cost accounting system: It is a tool which is used by managers to identify cost of

manufacturing each product in order to control cost of inventory to maximize profitability level

of their organisation. Managers apply various techniques to calculate cost of each unite. Job

costing, process costing, and activity based costing are the part of this system. In this system

cost are calculated on the basis of allocation and absorption of expenses at each units.

Organisations uses this system to formulates polices and plans for optimum utilization of

resources through controlling cost incurred in manufacturing product.

Price optimization system: It is a framework of accounting system, managers uses this

system analyzing and selecting best price strategy for their product. This system helps to identify

factors affecting pricing policies of an organization. Managers take decision regarding selecting

price of product after analyzing market condition of their business environment. Managers uses

various techniques to maximize their profitability level through selling their product at best price.

Price strategy of an entity depends on the stage of their product life cycle (Ng and et.al., 2017).

Price optimization system also a part of management accounting which helps managers to take

best decision regarding selecting price which satisfied produces as well as customer also.

output information's quality to utilize involved knowledge or reviews through planning,

controls.

Management Accounting System: It regarded as specified frameworks utilised by

managing personnels to deal with different tasks of business and generate information for

managerial decision-making phase. In this regard following are several systems and their

requirements in context of Shell:

Inventory management system: It is a technique of management accounting which is

used to identify and monitoring each unit of product available in business entity. In other words,

inventory management system is the combination of hardware and software tools which helps

managers to analysing, controlling and maintaining stock level of the organisation. Managers

uses various technique to maintain stock level of their entity (Mkrtychev, Ochepovsky and Enik,

2018). They use ABC analysis, VED analysis, inventory management software’s to identify

minimum, maximum and dangerous level of their stock. Organisations apply this system in order

to effectively and efficiently manage operating cycle of their department.

Cost accounting system: It is a tool which is used by managers to identify cost of

manufacturing each product in order to control cost of inventory to maximize profitability level

of their organisation. Managers apply various techniques to calculate cost of each unite. Job

costing, process costing, and activity based costing are the part of this system. In this system

cost are calculated on the basis of allocation and absorption of expenses at each units.

Organisations uses this system to formulates polices and plans for optimum utilization of

resources through controlling cost incurred in manufacturing product.

Price optimization system: It is a framework of accounting system, managers uses this

system analyzing and selecting best price strategy for their product. This system helps to identify

factors affecting pricing policies of an organization. Managers take decision regarding selecting

price of product after analyzing market condition of their business environment. Managers uses

various techniques to maximize their profitability level through selling their product at best price.

Price strategy of an entity depends on the stage of their product life cycle (Ng and et.al., 2017).

Price optimization system also a part of management accounting which helps managers to take

best decision regarding selecting price which satisfied produces as well as customer also.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Integration of above specified systems within corporation's processes is quite necessary

for effective and systematised adoption of such systems as per organisation's needs and

requirements. As in Shell, managers can integrate accounting and financial processes with

inventory management and cost accounting for quick transmission and generation of systems.

Further some key processes which are relevant for extracting information for systems should also

be integrated with systems.

Management Accounting Reporting

MA's mechanism also contains several reports for reporting information and data for

managerial decision-making as well as to support other managerial functions. Here following are

several reports concerned with MA, as follows:

Cost report: It encompasses all the component of producing as well as selling a product

that involves all direct and indirect expenses (Nitzl, 2018). Executives of a manufacturing

organizations take decisions about product prices and reducing costs after analysing this report's

summery. In Shell, managing staff can use this report to take decision regarding controlling any

specific key expenses and allocate or recognise costs which are detrimental in corporation's

profit targets .

Performance report: Performance report is prepare to show quality state of employees

as well as the firm's division. It is essential reporting approach of MA as such reports help

managing personnels to identify/assess their workforces' performance level over particular time-

frame. In Shell this report can allow managers to determine payroll, wages and other incentives

as per employees' performance. Also it enable corporation to allot works and jobs per workers

and employees strengths and capabilities.

Inventory report: This report is a compilation of how much stock a company has on its

different sites and branches as on particular time. This report is tangible or electronic document

with numbers that reflect the product that organisation can deliver, inventory to be ordered, or

inventory for internal usage. In Shell, managers can apply this report to track usage and level of

inventories across different stations.

for effective and systematised adoption of such systems as per organisation's needs and

requirements. As in Shell, managers can integrate accounting and financial processes with

inventory management and cost accounting for quick transmission and generation of systems.

Further some key processes which are relevant for extracting information for systems should also

be integrated with systems.

Management Accounting Reporting

MA's mechanism also contains several reports for reporting information and data for

managerial decision-making as well as to support other managerial functions. Here following are

several reports concerned with MA, as follows:

Cost report: It encompasses all the component of producing as well as selling a product

that involves all direct and indirect expenses (Nitzl, 2018). Executives of a manufacturing

organizations take decisions about product prices and reducing costs after analysing this report's

summery. In Shell, managing staff can use this report to take decision regarding controlling any

specific key expenses and allocate or recognise costs which are detrimental in corporation's

profit targets .

Performance report: Performance report is prepare to show quality state of employees

as well as the firm's division. It is essential reporting approach of MA as such reports help

managing personnels to identify/assess their workforces' performance level over particular time-

frame. In Shell this report can allow managers to determine payroll, wages and other incentives

as per employees' performance. Also it enable corporation to allot works and jobs per workers

and employees strengths and capabilities.

Inventory report: This report is a compilation of how much stock a company has on its

different sites and branches as on particular time. This report is tangible or electronic document

with numbers that reflect the product that organisation can deliver, inventory to be ordered, or

inventory for internal usage. In Shell, managers can apply this report to track usage and level of

inventories across different stations.

TASK 2

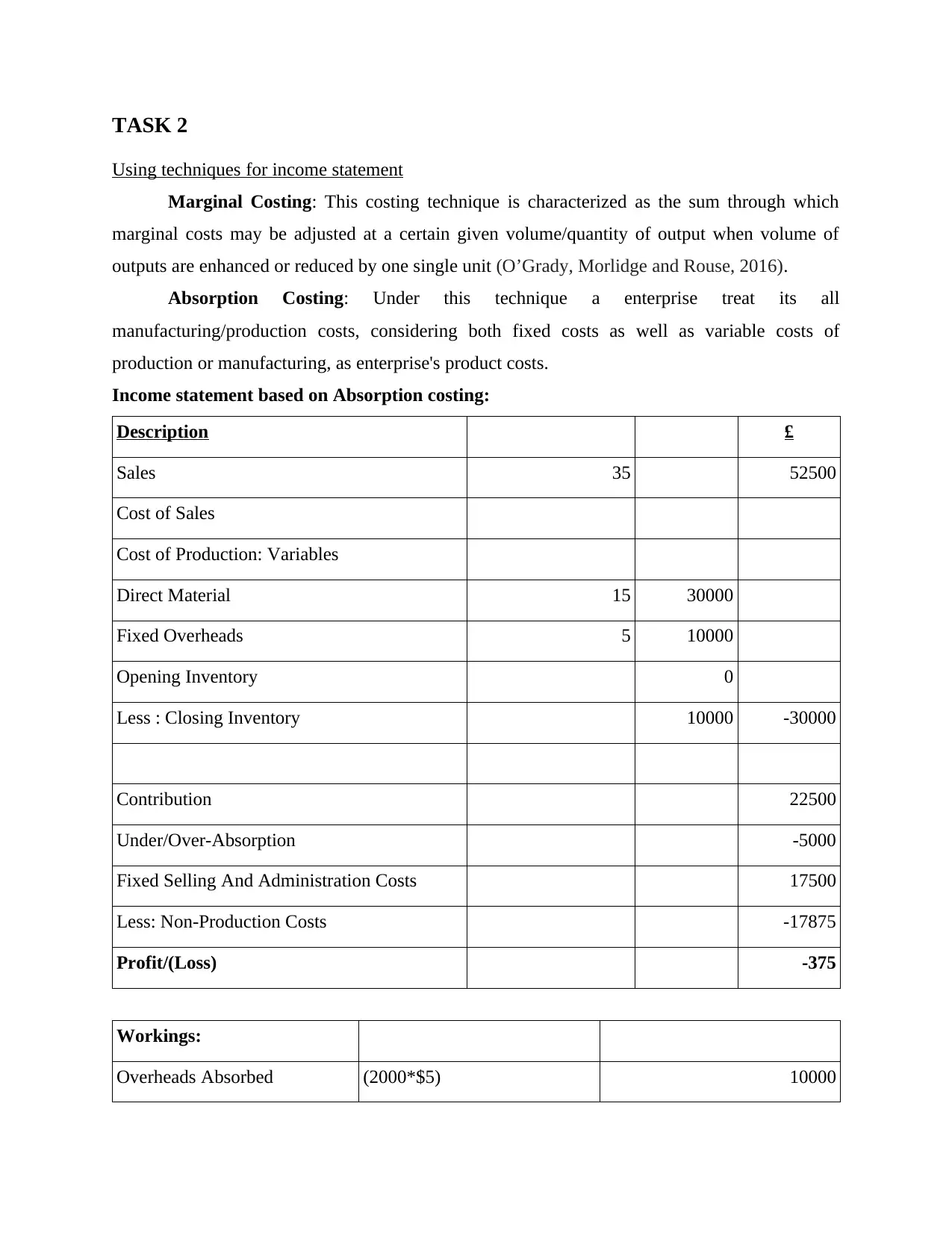

Using techniques for income statement

Marginal Costing: This costing technique is characterized as the sum through which

marginal costs may be adjusted at a certain given volume/quantity of output when volume of

outputs are enhanced or reduced by one single unit (O’Grady, Morlidge and Rouse, 2016).

Absorption Costing: Under this technique a enterprise treat its all

manufacturing/production costs, considering both fixed costs as well as variable costs of

production or manufacturing, as enterprise's product costs.

Income statement based on Absorption costing:

Description £

Sales 35 52500

Cost of Sales

Cost of Production: Variables

Direct Material 15 30000

Fixed Overheads 5 10000

Opening Inventory 0

Less : Closing Inventory 10000 -30000

Contribution 22500

Under/Over-Absorption -5000

Fixed Selling And Administration Costs 17500

Less: Non-Production Costs -17875

Profit/(Loss) -375

Workings:

Overheads Absorbed (2000*$5) 10000

Using techniques for income statement

Marginal Costing: This costing technique is characterized as the sum through which

marginal costs may be adjusted at a certain given volume/quantity of output when volume of

outputs are enhanced or reduced by one single unit (O’Grady, Morlidge and Rouse, 2016).

Absorption Costing: Under this technique a enterprise treat its all

manufacturing/production costs, considering both fixed costs as well as variable costs of

production or manufacturing, as enterprise's product costs.

Income statement based on Absorption costing:

Description £

Sales 35 52500

Cost of Sales

Cost of Production: Variables

Direct Material 15 30000

Fixed Overheads 5 10000

Opening Inventory 0

Less : Closing Inventory 10000 -30000

Contribution 22500

Under/Over-Absorption -5000

Fixed Selling And Administration Costs 17500

Less: Non-Production Costs -17875

Profit/(Loss) -375

Workings:

Overheads Absorbed (2000*$5) 10000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

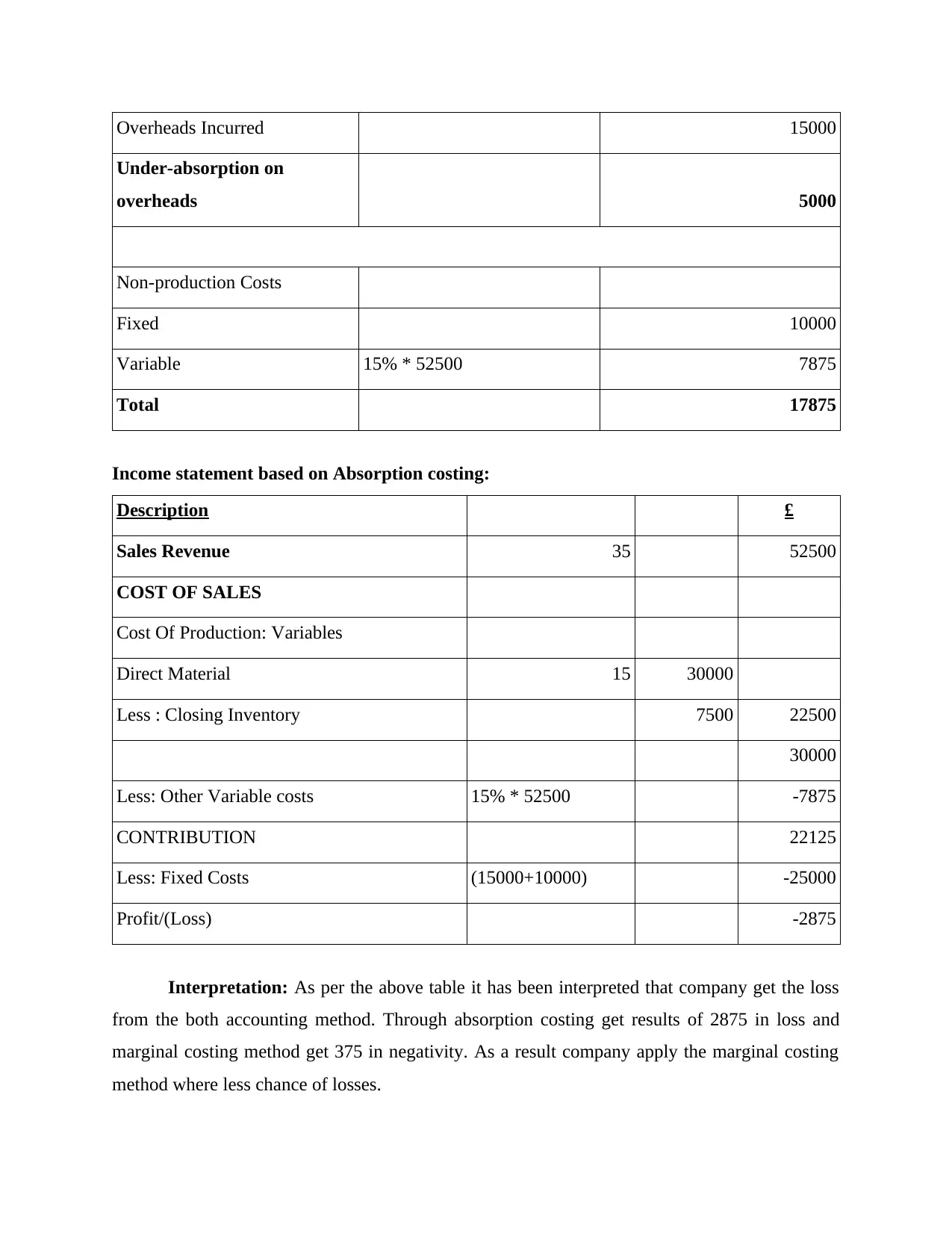

Overheads Incurred 15000

Under-absorption on

overheads 5000

Non-production Costs

Fixed 10000

Variable 15% * 52500 7875

Total 17875

Income statement based on Absorption costing:

Description £

Sales Revenue 35 52500

COST OF SALES

Cost Of Production: Variables

Direct Material 15 30000

Less : Closing Inventory 7500 22500

30000

Less: Other Variable costs 15% * 52500 -7875

CONTRIBUTION 22125

Less: Fixed Costs (15000+10000) -25000

Profit/(Loss) -2875

Interpretation: As per the above table it has been interpreted that company get the loss

from the both accounting method. Through absorption costing get results of 2875 in loss and

marginal costing method get 375 in negativity. As a result company apply the marginal costing

method where less chance of losses.

Under-absorption on

overheads 5000

Non-production Costs

Fixed 10000

Variable 15% * 52500 7875

Total 17875

Income statement based on Absorption costing:

Description £

Sales Revenue 35 52500

COST OF SALES

Cost Of Production: Variables

Direct Material 15 30000

Less : Closing Inventory 7500 22500

30000

Less: Other Variable costs 15% * 52500 -7875

CONTRIBUTION 22125

Less: Fixed Costs (15000+10000) -25000

Profit/(Loss) -2875

Interpretation: As per the above table it has been interpreted that company get the loss

from the both accounting method. Through absorption costing get results of 2875 in loss and

marginal costing method get 375 in negativity. As a result company apply the marginal costing

method where less chance of losses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

Planning tools of budgetary control with merit and demerit

Budgetary control: It is the process of identifying gap between actual performance and

standard performance and then make plans and polices to fulfil the gap in order to achieve

budgetary target of the organisation. Managers of Shell limited uses different planning tools to

effectively run their managerial process, these are mention as below:

Zero Based budget: In this technique managers prepared budget from initial level.

Managers built their budget after analysing all the factors of environment (Pavlatos and

Kostakis, 2018). They did not use historical data. It is an essential tool of budgetary

control, managers prepare statement of cash flow and other tools on the basis analysing

recent market conditions. Managers of Shell limited uses this tool for maintain efficiency

level of their new products.

Advantage:

It helps in effectively and efficiently utilization of resources.

It helps in provides better coordination and communication within organisation.

Disadvantage:

Cost of applying zero based budgeting method is too high.

It requires highly skilled employers for applying this technique for organisation.

Rolling budget: It is a technique of budgetary control in which managers prepared

budget for certain time period and after completion of the project they prepare another budget on

the basis of analysing data of past budget. Rolling budgets are prepared for short time period. It

is most effective planning tool of budgetary control. Managers of Shell limited uses rolling

budget to for optimum utilization of their resources and effectively achieve their goal (Pelz,

2019).

Advantage:

It uses as effective planning and controlling tool for organisation.

This technique helps organisation to spending their money on vital and essential

activities.

Disadvantage:

This method is applicable only for short run period.

It takes times in preparing and applying this budget

Planning tools of budgetary control with merit and demerit

Budgetary control: It is the process of identifying gap between actual performance and

standard performance and then make plans and polices to fulfil the gap in order to achieve

budgetary target of the organisation. Managers of Shell limited uses different planning tools to

effectively run their managerial process, these are mention as below:

Zero Based budget: In this technique managers prepared budget from initial level.

Managers built their budget after analysing all the factors of environment (Pavlatos and

Kostakis, 2018). They did not use historical data. It is an essential tool of budgetary

control, managers prepare statement of cash flow and other tools on the basis analysing

recent market conditions. Managers of Shell limited uses this tool for maintain efficiency

level of their new products.

Advantage:

It helps in effectively and efficiently utilization of resources.

It helps in provides better coordination and communication within organisation.

Disadvantage:

Cost of applying zero based budgeting method is too high.

It requires highly skilled employers for applying this technique for organisation.

Rolling budget: It is a technique of budgetary control in which managers prepared

budget for certain time period and after completion of the project they prepare another budget on

the basis of analysing data of past budget. Rolling budgets are prepared for short time period. It

is most effective planning tool of budgetary control. Managers of Shell limited uses rolling

budget to for optimum utilization of their resources and effectively achieve their goal (Pelz,

2019).

Advantage:

It uses as effective planning and controlling tool for organisation.

This technique helps organisation to spending their money on vital and essential

activities.

Disadvantage:

This method is applicable only for short run period.

It takes times in preparing and applying this budget

Operating budget: Organisation prepared operating budget to identifying income and

expenditure level at predetermined time period. It is an essential tool of budgetary control

managers use this tool to set target of selling products of the business entity at fixed time period.

Managers used this tool to identify causes of gap between achieved and standard budgetary

target then make strategic plans to achieve set future target.

Advantage:

It helps in identifying production level of organisation at different levels of economical

market conditions (Piontkewicz and et.al., 2016).

Operating budgeting useful in enhancing profitability level of an organisation.

Disadvantage:

It requires effective skilled workforce for the organisation which can easily adopt

changing polices of organisation.

This planning tool is only considered monetary outcomes, thus operating budgeting tool

is not providing accurate information regarding future earnings (Quinn and Hiebl, 2018).

TASK 4

Financial provable of business and appropriate management accounting system

Financial Problems: It is a situation at which organisations are unable to invest in any

security and pay debt liability of their creditors. Financial problems arise due to lack of financial

capital of the organisation. Shell limited is medium size enterprises at present the organisation is

suffering from financial problem due to lack of money managerial skills and decreases in sales.

Shell limited now apply techniques which helps them to detect and overcome their problems. Lack of money managerial Skill: In Shell people have not skill of proper utilisation of

money management that become reason of loss. As a result business face many problem

and impact on the financial condition on the business.

Decrease in sales: Now a days company face the problem of decreasing sales because of

company do not offer any discounts and prepare attractive strategies to influence people

for purchase their products & services. As a result it impact on the performance of

business in negative manner.

To overcome from these problems require to apply effective management too that help to

business to identify the financial problems and easily and these techniques are mention below:

expenditure level at predetermined time period. It is an essential tool of budgetary control

managers use this tool to set target of selling products of the business entity at fixed time period.

Managers used this tool to identify causes of gap between achieved and standard budgetary

target then make strategic plans to achieve set future target.

Advantage:

It helps in identifying production level of organisation at different levels of economical

market conditions (Piontkewicz and et.al., 2016).

Operating budgeting useful in enhancing profitability level of an organisation.

Disadvantage:

It requires effective skilled workforce for the organisation which can easily adopt

changing polices of organisation.

This planning tool is only considered monetary outcomes, thus operating budgeting tool

is not providing accurate information regarding future earnings (Quinn and Hiebl, 2018).

TASK 4

Financial provable of business and appropriate management accounting system

Financial Problems: It is a situation at which organisations are unable to invest in any

security and pay debt liability of their creditors. Financial problems arise due to lack of financial

capital of the organisation. Shell limited is medium size enterprises at present the organisation is

suffering from financial problem due to lack of money managerial skills and decreases in sales.

Shell limited now apply techniques which helps them to detect and overcome their problems. Lack of money managerial Skill: In Shell people have not skill of proper utilisation of

money management that become reason of loss. As a result business face many problem

and impact on the financial condition on the business.

Decrease in sales: Now a days company face the problem of decreasing sales because of

company do not offer any discounts and prepare attractive strategies to influence people

for purchase their products & services. As a result it impact on the performance of

business in negative manner.

To overcome from these problems require to apply effective management too that help to

business to identify the financial problems and easily and these techniques are mention below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Key Performance Indicator: It is a tool which helps to identifies how effectively and

efficiently an organisation achieve their goals. KPI helps mangers of Shell limited to

enhance their managerial skills. Directors of Shell limited increase managers skills of

their managers through provides them incentive and change their job designation,

Benchmarking: It is a process of comparing products, services and level of profitability

from another rivalry organisation. Manager of Shell limited uses this technique to

compare their profitability level from competitive industry. Benchmarking helps

managers to increase sales of their organisation through identifying strategies of

increasing profitability level of another organisation.

Financial governance: It is a effective tool which is applied by the business top sort out

the different financial problem that arise in the business and impact on the performance.

Through this tool find out solution of these problem there is require to offer proper

training to staff member to overcome from the lack of manage money skills. For the

decrease sales require to provide attractive to customer and implemented on them

(Szychta and Dobroszek, 2016).

Comparison of Shell and MQS organisation

Management

accounting

Shell MQS

Key performance

indicator

In this organisation through key

performance indicator indemnify

the decrease sales. To sort out this

problem require to apply cost

accounting system where set cost

as per the cash requirement.

There are management assure about

the right costs and circulated to all

the operational activities that

possible through overspending of

budget can be reduced. For this apply

the price optimization system to set

effective price in budget.

Benchmarking It is measurement tool which is

applied to identify the problem of

lack of money managerial skill

where compare with other business

and adopt their strategies

This technique utilised to find out the

all financial principle are complied

with management or not. For this

applied the job order costing system

to arrange management effectively

efficiently an organisation achieve their goals. KPI helps mangers of Shell limited to

enhance their managerial skills. Directors of Shell limited increase managers skills of

their managers through provides them incentive and change their job designation,

Benchmarking: It is a process of comparing products, services and level of profitability

from another rivalry organisation. Manager of Shell limited uses this technique to

compare their profitability level from competitive industry. Benchmarking helps

managers to increase sales of their organisation through identifying strategies of

increasing profitability level of another organisation.

Financial governance: It is a effective tool which is applied by the business top sort out

the different financial problem that arise in the business and impact on the performance.

Through this tool find out solution of these problem there is require to offer proper

training to staff member to overcome from the lack of manage money skills. For the

decrease sales require to provide attractive to customer and implemented on them

(Szychta and Dobroszek, 2016).

Comparison of Shell and MQS organisation

Management

accounting

Shell MQS

Key performance

indicator

In this organisation through key

performance indicator indemnify

the decrease sales. To sort out this

problem require to apply cost

accounting system where set cost

as per the cash requirement.

There are management assure about

the right costs and circulated to all

the operational activities that

possible through overspending of

budget can be reduced. For this apply

the price optimization system to set

effective price in budget.

Benchmarking It is measurement tool which is

applied to identify the problem of

lack of money managerial skill

where compare with other business

and adopt their strategies

This technique utilised to find out the

all financial principle are complied

with management or not. For this

applied the job order costing system

to arrange management effectively

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

effectively. For this apply the

inventory management system.

(Vetrov, Vandina and Galustov,

2017).

CONCLUSION

From above study it has been articulated that managerial accounting being a wider term

covers almost all key elements related to organisational and functional structure. Also its

multiple key systems enables managers to deal with different business and financial difficulties.

For different corporation manner of adoption of multiple systems may be different but overall

aim is to support management core tasks. In this report discuss about various system and reports

are cost accounting inventory management, price optimization and many others. These are

providing depth information in helps in decision making procedure. Along with various planning

tools with advantage and disadvantage that apply by business to get information about business.

Additionally, discuss about the financial problem that impact on the performance on apply

reliable system to sort out it.

inventory management system.

(Vetrov, Vandina and Galustov,

2017).

CONCLUSION

From above study it has been articulated that managerial accounting being a wider term

covers almost all key elements related to organisational and functional structure. Also its

multiple key systems enables managers to deal with different business and financial difficulties.

For different corporation manner of adoption of multiple systems may be different but overall

aim is to support management core tasks. In this report discuss about various system and reports

are cost accounting inventory management, price optimization and many others. These are

providing depth information in helps in decision making procedure. Along with various planning

tools with advantage and disadvantage that apply by business to get information about business.

Additionally, discuss about the financial problem that impact on the performance on apply

reliable system to sort out it.

REFERENCES

Books and Journal

Kumarasiri, J., 2017. Stakeholder pressure on carbon emissions: strategies and the use of

management accounting. Australasian Journal of Environmental Management. 24(4).

pp.339-354.

Larmande, L., 2016. Shareholders’ Demand for Conservatism? Accounting Conservatism,

Earnings Management, and the Stewardship Value of Information. (No. 1104). HEC

Paris.

Mkrtychev, S. V., Ochepovsky, A. V. and Enik, O. A., 2018, May. Configuration of management

accounting information system for multi-stage manufacturing. In Journal of Physics:

Conference Series. (Vol. 1015, No. 4, p. 042039). IOP Publishing.

Ng, Y. H. and et.al., 2017. Factors influencing accounting students’ career paths. Journal of

Management Development.

Nitzl, C., 2018. Management accounting and partial least squares-structural equation modelling

(PLS-SEM): Some illustrative examples. In Partial Least Squares Structural Equation

Modeling. (pp. 211-229). Springer, Cham.

O’Grady, W., Morlidge, S. and Rouse, P., 2016. Evaluating the completeness and effectiveness

of management control systems with cybernetic tools. Management Accounting

Research. 33. pp.1-15.

Pavlatos, O. and Kostakis, X., 2018. The impact of top management team characteristics and

historical financial performance on strategic management accounting. Journal of

Accounting & Organizational Change.

Pelz, M., 2019. Can Management Accounting Be Helpful for Young and Small Companies?

Systematic Review of a Paradox. International Journal of Management Reviews. 21(2).

pp.256-274.Ostapiuk, N., Karmaza, O., Kurylo, M. and Timchenko, G., 2017. Economic

security in investment projects management: convergence of accounting mechanisms.

Piontkewicz, R. and et.al., 2016, May. Management of intellectual capital in a system of

management accounting information. In 2016 6th International Conference on

Computers Communications and Control (ICCCC). (pp. 180-187). IEEE.

Quinn, M. and Hiebl, M. R., 2018. Management accounting routines: a framework on their

foundations. Qualitative Research in Accounting & Management.

Szychta, A. and Dobroszek, J., 2016, December. Perception of Management Accounting and

Controlling by Polish Authors in Publications in 1990-2016. In 5th International

Conference on Accounting, Auditing, and Taxation (ICAAT 2016). Atlantis Press.

Vetrov, Y. P., Vandina, O. G. and Galustov, A. R., 2017. Strategic management accounting in

organizations’ cash flow control. Journal of History Culture and Art Research. 6(4).

pp.425-435.

Books and Journal

Kumarasiri, J., 2017. Stakeholder pressure on carbon emissions: strategies and the use of

management accounting. Australasian Journal of Environmental Management. 24(4).

pp.339-354.

Larmande, L., 2016. Shareholders’ Demand for Conservatism? Accounting Conservatism,

Earnings Management, and the Stewardship Value of Information. (No. 1104). HEC

Paris.

Mkrtychev, S. V., Ochepovsky, A. V. and Enik, O. A., 2018, May. Configuration of management

accounting information system for multi-stage manufacturing. In Journal of Physics:

Conference Series. (Vol. 1015, No. 4, p. 042039). IOP Publishing.

Ng, Y. H. and et.al., 2017. Factors influencing accounting students’ career paths. Journal of

Management Development.

Nitzl, C., 2018. Management accounting and partial least squares-structural equation modelling

(PLS-SEM): Some illustrative examples. In Partial Least Squares Structural Equation

Modeling. (pp. 211-229). Springer, Cham.

O’Grady, W., Morlidge, S. and Rouse, P., 2016. Evaluating the completeness and effectiveness

of management control systems with cybernetic tools. Management Accounting

Research. 33. pp.1-15.

Pavlatos, O. and Kostakis, X., 2018. The impact of top management team characteristics and

historical financial performance on strategic management accounting. Journal of

Accounting & Organizational Change.

Pelz, M., 2019. Can Management Accounting Be Helpful for Young and Small Companies?

Systematic Review of a Paradox. International Journal of Management Reviews. 21(2).

pp.256-274.Ostapiuk, N., Karmaza, O., Kurylo, M. and Timchenko, G., 2017. Economic

security in investment projects management: convergence of accounting mechanisms.

Piontkewicz, R. and et.al., 2016, May. Management of intellectual capital in a system of

management accounting information. In 2016 6th International Conference on

Computers Communications and Control (ICCCC). (pp. 180-187). IEEE.

Quinn, M. and Hiebl, M. R., 2018. Management accounting routines: a framework on their

foundations. Qualitative Research in Accounting & Management.

Szychta, A. and Dobroszek, J., 2016, December. Perception of Management Accounting and

Controlling by Polish Authors in Publications in 1990-2016. In 5th International

Conference on Accounting, Auditing, and Taxation (ICAAT 2016). Atlantis Press.

Vetrov, Y. P., Vandina, O. G. and Galustov, A. R., 2017. Strategic management accounting in

organizations’ cash flow control. Journal of History Culture and Art Research. 6(4).

pp.425-435.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.