Management Accounting Report: Inventory and Budgeting for Smart Looks

VerifiedAdded on 2020/02/12

|24

|5145

|60

Report

AI Summary

This management accounting report analyzes the case of Smart Looks, a clothing retailer, covering various aspects of cost accounting and budgeting. The report begins by classifying costs (fixed, variable, semi-variable) and explores different cost classification methods. It then delves into inventory valuation using FIFO, LIFO, and average cost methods, calculating cost of goods sold under each method. The report also includes total and unit cost calculations at different production levels, with graphical presentations. Furthermore, it evaluates critical success factors and their associated performance indicators, along with strategies for cost reduction and quality enhancement. The report then examines budgeting techniques, including sales, production, raw materials, labor, and overhead budgets, culminating in the preparation of a cash budget. Finally, it addresses variance analysis, calculating budgeted and actual profit, and providing recommendations for improvement.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Question 1....................................................................................................................................3

a. Classifying cost in terms of fixed, variable and semi-variable................................................3

b. Explaining other ways of cost classification...........................................................................3

TASK 2............................................................................................................................................5

Question 2....................................................................................................................................5

a. Computing total and unit cost at different production level....................................................5

b. Analyzing cost data through graphical presentation................................................................6

Question 3....................................................................................................................................6

Computing inventory by using various methods.........................................................................6

a. First in, first out \.....................................................................................................................6

b. Last-in first out........................................................................................................................7

c. Average cost method................................................................................................................8

Question 4....................................................................................................................................9

Preparing a report of cost of goods sold in accordance with different methods..........................9

Question 5....................................................................................................................................9

a. Evaluating critical success factors and associated them with suitable performance indicators

.....................................................................................................................................................9

b.................................................................................................................................................10

1. Assessing the manner in which cost can be reduced.............................................................10

2. Presenting the ways to enhance quality.................................................................................11

TASK 2..........................................................................................................................................11

Question 6..................................................................................................................................11

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Question 1....................................................................................................................................3

a. Classifying cost in terms of fixed, variable and semi-variable................................................3

b. Explaining other ways of cost classification...........................................................................3

TASK 2............................................................................................................................................5

Question 2....................................................................................................................................5

a. Computing total and unit cost at different production level....................................................5

b. Analyzing cost data through graphical presentation................................................................6

Question 3....................................................................................................................................6

Computing inventory by using various methods.........................................................................6

a. First in, first out \.....................................................................................................................6

b. Last-in first out........................................................................................................................7

c. Average cost method................................................................................................................8

Question 4....................................................................................................................................9

Preparing a report of cost of goods sold in accordance with different methods..........................9

Question 5....................................................................................................................................9

a. Evaluating critical success factors and associated them with suitable performance indicators

.....................................................................................................................................................9

b.................................................................................................................................................10

1. Assessing the manner in which cost can be reduced.............................................................10

2. Presenting the ways to enhance quality.................................................................................11

TASK 2..........................................................................................................................................11

Question 6..................................................................................................................................11

a. Definition of budget...............................................................................................................11

b. Purpose of budgets.................................................................................................................12

c. Assessing the different methods of budget preparation and suggesting the most suitable one

for Smart looks..........................................................................................................................12

Question7...................................................................................................................................14

a. Sales budget...........................................................................................................................14

b. Production budget..................................................................................................................14

c. Raw material budgets.............................................................................................................14

d. Labor budgets........................................................................................................................15

e. Total overhead budget............................................................................................................15

Question 8..................................................................................................................................16

Preparing cash budget for Smart Looks for the year ended at 30th June 2017...........................16

TASK 3..........................................................................................................................................17

Question 9..................................................................................................................................17

a. Calculating budgeted profit for March 2017.........................................................................17

b. Computation of actual profit..................................................................................................17

c. Calculating material and labor sub-variances........................................................................17

d. Preparing an operating statement reconciled budget and actual profit..................................18

Question 10................................................................................................................................18

Explaining reason behind the deviations and giving recommendations for improvement........18

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................21

b. Purpose of budgets.................................................................................................................12

c. Assessing the different methods of budget preparation and suggesting the most suitable one

for Smart looks..........................................................................................................................12

Question7...................................................................................................................................14

a. Sales budget...........................................................................................................................14

b. Production budget..................................................................................................................14

c. Raw material budgets.............................................................................................................14

d. Labor budgets........................................................................................................................15

e. Total overhead budget............................................................................................................15

Question 8..................................................................................................................................16

Preparing cash budget for Smart Looks for the year ended at 30th June 2017...........................16

TASK 3..........................................................................................................................................17

Question 9..................................................................................................................................17

a. Calculating budgeted profit for March 2017.........................................................................17

b. Computation of actual profit..................................................................................................17

c. Calculating material and labor sub-variances........................................................................17

d. Preparing an operating statement reconciled budget and actual profit..................................18

Question 10................................................................................................................................18

Explaining reason behind the deviations and giving recommendations for improvement........18

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Management accounting may be served as a decision making tool which in turn provides

manager with the valuable input. Hence, by undertaking the reports of budget, cost and profit

business unit can develop highly strategic and competent policy framework. Managerial

accounting reports help in getting deeper insight about the monetary position and performance.

Hence, by making evaluation of the departmental performance in both monetary and non-

monetary terms higher management team can take significant action for improvement. This

project report is based on the case situation of Smart Looks that offers clothes or apparel to the

customers. In this, report will furnish information regarding the manner in which cost can be

classified and presented. Besides this, it will also shed light on the different types of inventory

valuation methods and techniques. Further, report also develops understanding about the various

budgeting tools and techniques which in turn facilitates optimum use of financial resources.

TASK 1

Question 1

a. Classifying cost in terms of fixed, variable and semi-variable

Categorization of costs incurred by Smart Looks is as follows:

Cost Category

Material for clothes Variable

Factory rent Fixed

Power for sewing machines in factory Semi-variable

Telephone expenses Semi-variable

Office rates Fixed

Delivery drivers Semi-variable

Factory heating Variable

Management accounting may be served as a decision making tool which in turn provides

manager with the valuable input. Hence, by undertaking the reports of budget, cost and profit

business unit can develop highly strategic and competent policy framework. Managerial

accounting reports help in getting deeper insight about the monetary position and performance.

Hence, by making evaluation of the departmental performance in both monetary and non-

monetary terms higher management team can take significant action for improvement. This

project report is based on the case situation of Smart Looks that offers clothes or apparel to the

customers. In this, report will furnish information regarding the manner in which cost can be

classified and presented. Besides this, it will also shed light on the different types of inventory

valuation methods and techniques. Further, report also develops understanding about the various

budgeting tools and techniques which in turn facilitates optimum use of financial resources.

TASK 1

Question 1

a. Classifying cost in terms of fixed, variable and semi-variable

Categorization of costs incurred by Smart Looks is as follows:

Cost Category

Material for clothes Variable

Factory rent Fixed

Power for sewing machines in factory Semi-variable

Telephone expenses Semi-variable

Office rates Fixed

Delivery drivers Semi-variable

Factory heating Variable

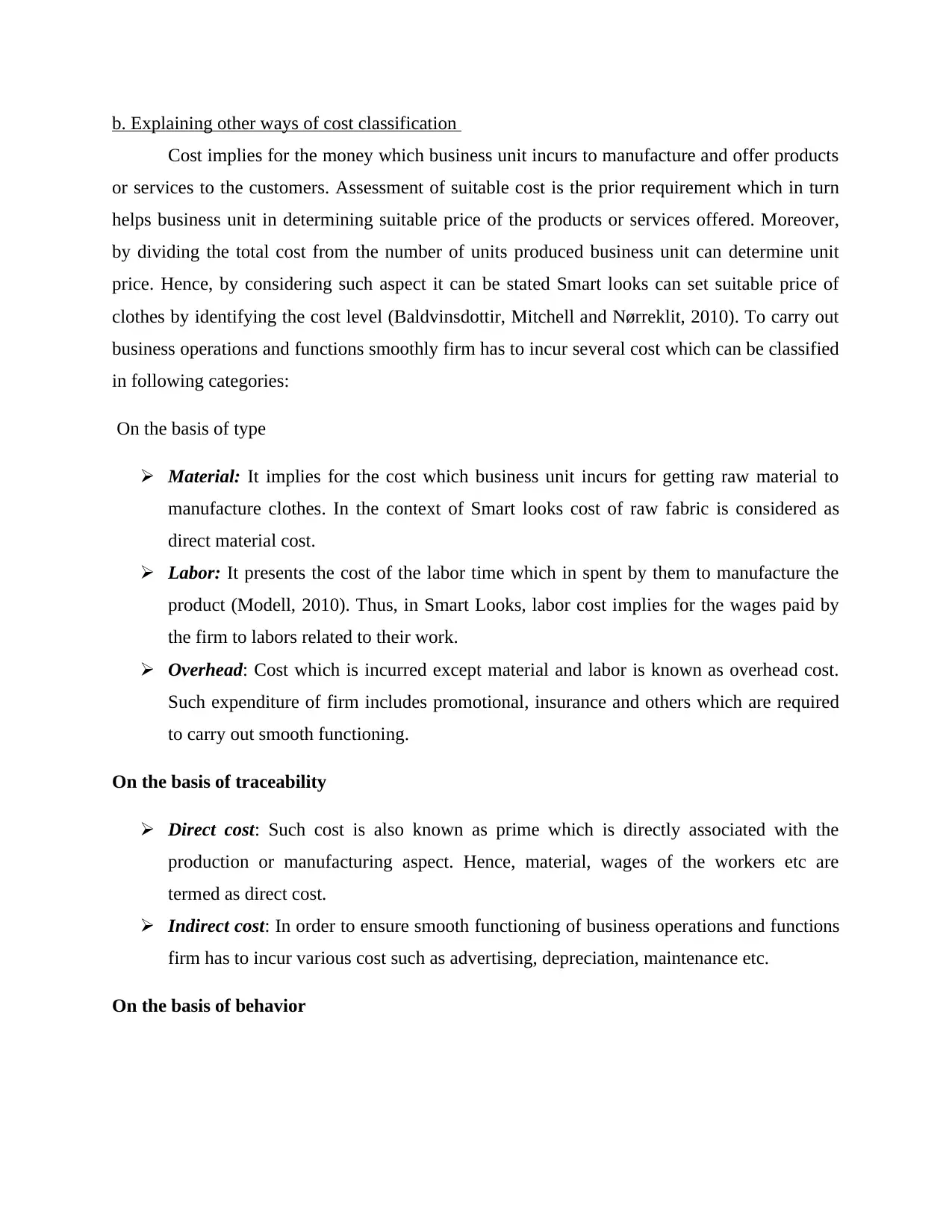

b. Explaining other ways of cost classification

Cost implies for the money which business unit incurs to manufacture and offer products

or services to the customers. Assessment of suitable cost is the prior requirement which in turn

helps business unit in determining suitable price of the products or services offered. Moreover,

by dividing the total cost from the number of units produced business unit can determine unit

price. Hence, by considering such aspect it can be stated Smart looks can set suitable price of

clothes by identifying the cost level (Baldvinsdottir, Mitchell and Nørreklit, 2010). To carry out

business operations and functions smoothly firm has to incur several cost which can be classified

in following categories:

On the basis of type

Material: It implies for the cost which business unit incurs for getting raw material to

manufacture clothes. In the context of Smart looks cost of raw fabric is considered as

direct material cost.

Labor: It presents the cost of the labor time which in spent by them to manufacture the

product (Modell, 2010). Thus, in Smart Looks, labor cost implies for the wages paid by

the firm to labors related to their work.

Overhead: Cost which is incurred except material and labor is known as overhead cost.

Such expenditure of firm includes promotional, insurance and others which are required

to carry out smooth functioning.

On the basis of traceability

Direct cost: Such cost is also known as prime which is directly associated with the

production or manufacturing aspect. Hence, material, wages of the workers etc are

termed as direct cost.

Indirect cost: In order to ensure smooth functioning of business operations and functions

firm has to incur various cost such as advertising, depreciation, maintenance etc.

On the basis of behavior

Cost implies for the money which business unit incurs to manufacture and offer products

or services to the customers. Assessment of suitable cost is the prior requirement which in turn

helps business unit in determining suitable price of the products or services offered. Moreover,

by dividing the total cost from the number of units produced business unit can determine unit

price. Hence, by considering such aspect it can be stated Smart looks can set suitable price of

clothes by identifying the cost level (Baldvinsdottir, Mitchell and Nørreklit, 2010). To carry out

business operations and functions smoothly firm has to incur several cost which can be classified

in following categories:

On the basis of type

Material: It implies for the cost which business unit incurs for getting raw material to

manufacture clothes. In the context of Smart looks cost of raw fabric is considered as

direct material cost.

Labor: It presents the cost of the labor time which in spent by them to manufacture the

product (Modell, 2010). Thus, in Smart Looks, labor cost implies for the wages paid by

the firm to labors related to their work.

Overhead: Cost which is incurred except material and labor is known as overhead cost.

Such expenditure of firm includes promotional, insurance and others which are required

to carry out smooth functioning.

On the basis of traceability

Direct cost: Such cost is also known as prime which is directly associated with the

production or manufacturing aspect. Hence, material, wages of the workers etc are

termed as direct cost.

Indirect cost: In order to ensure smooth functioning of business operations and functions

firm has to incur various cost such as advertising, depreciation, maintenance etc.

On the basis of behavior

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fixed cost: Rent of building, salaries of personnel etc. are the main examples of fixed

cost. Hence, fixed cost is the one which remains same at each level and does not affect

from the output produced.

Semi-variable cost: It may be served as one which remains fixed at specific at specific

level of production and becomes variable after certain level (Lukka and Modell, 2010).

Electricity, insurance expenses come under the category of semi-variable cost.

Variable cost: Unlike fixed cost, variable expenses are the one which in turn highly

influences from the output produced. Hence, electricity, material cost are the examples

of variable cost which in turn closely influences the cost on the basis of output and

thereby profitability aspect. Thus, variable costs closely affected in accordance with the

output level.

Hence, all such are the main costs which Smart Look has to incur for manufacturing the

clothes to the customers.

TASK 2

Question 2

a. Computing total and unit cost at different production level

Total cost assessment

Units

manufactured Material Labor Fixed cost

Total

cost

Unit cost

(TC/Units

produced)

15000 75000 90000 50000

21500

0

£215,000/15,00

0

= £14.33

20000 100000 120000 50000

27000

0

£270,000/20,00

0

= £13.50

25000 125000 150000 50000 32500

0

£325,000/25,00

0

cost. Hence, fixed cost is the one which remains same at each level and does not affect

from the output produced.

Semi-variable cost: It may be served as one which remains fixed at specific at specific

level of production and becomes variable after certain level (Lukka and Modell, 2010).

Electricity, insurance expenses come under the category of semi-variable cost.

Variable cost: Unlike fixed cost, variable expenses are the one which in turn highly

influences from the output produced. Hence, electricity, material cost are the examples

of variable cost which in turn closely influences the cost on the basis of output and

thereby profitability aspect. Thus, variable costs closely affected in accordance with the

output level.

Hence, all such are the main costs which Smart Look has to incur for manufacturing the

clothes to the customers.

TASK 2

Question 2

a. Computing total and unit cost at different production level

Total cost assessment

Units

manufactured Material Labor Fixed cost

Total

cost

Unit cost

(TC/Units

produced)

15000 75000 90000 50000

21500

0

£215,000/15,00

0

= £14.33

20000 100000 120000 50000

27000

0

£270,000/20,00

0

= £13.50

25000 125000 150000 50000 32500

0

£325,000/25,00

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= £13.00

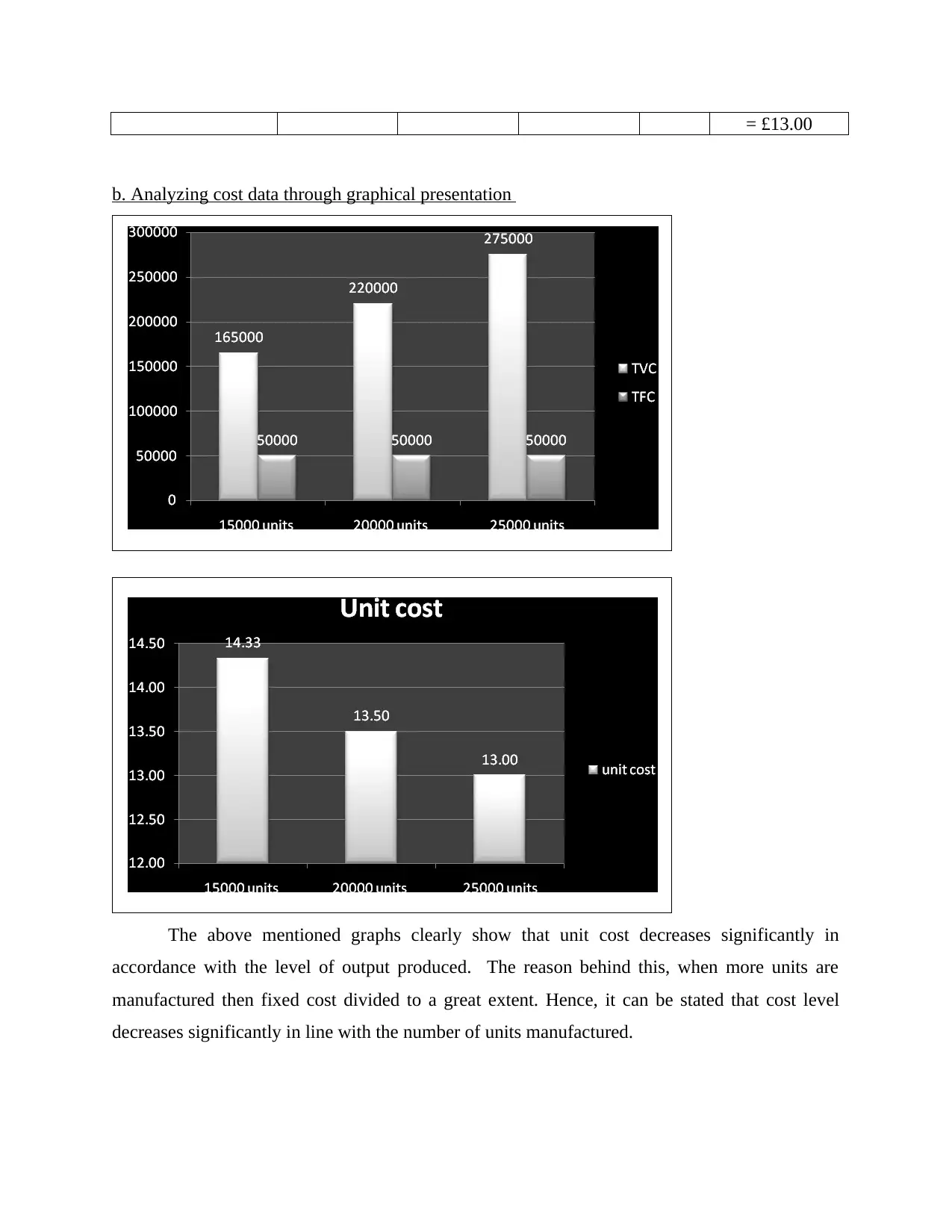

b. Analyzing cost data through graphical presentation

The above mentioned graphs clearly show that unit cost decreases significantly in

accordance with the level of output produced. The reason behind this, when more units are

manufactured then fixed cost divided to a great extent. Hence, it can be stated that cost level

decreases significantly in line with the number of units manufactured.

b. Analyzing cost data through graphical presentation

The above mentioned graphs clearly show that unit cost decreases significantly in

accordance with the level of output produced. The reason behind this, when more units are

manufactured then fixed cost divided to a great extent. Hence, it can be stated that cost level

decreases significantly in line with the number of units manufactured.

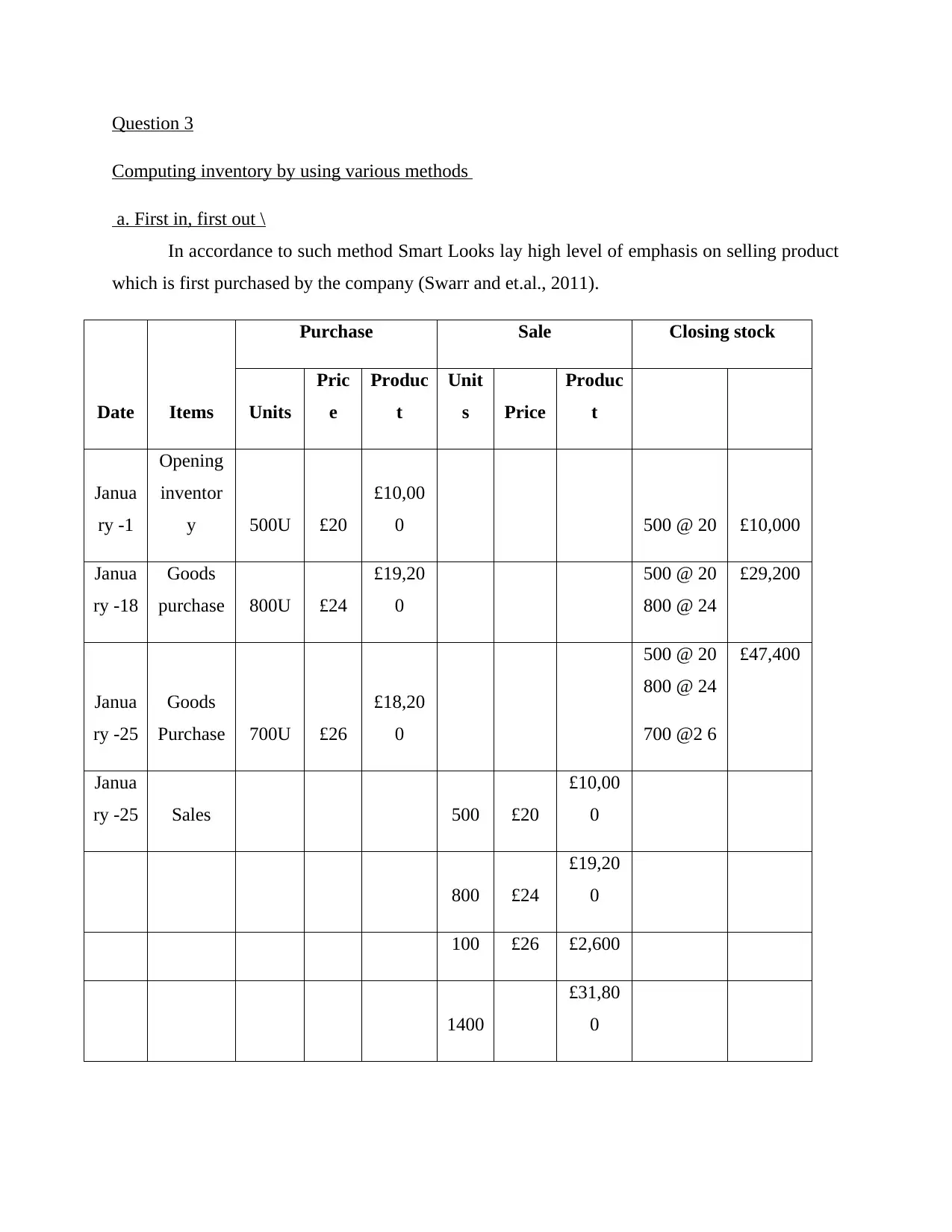

Question 3

Computing inventory by using various methods

a. First in, first out \

In accordance to such method Smart Looks lay high level of emphasis on selling product

which is first purchased by the company (Swarr and et.al., 2011).

Date Items

Purchase Sale Closing stock

Units

Pric

e

Produc

t

Unit

s Price

Produc

t

Janua

ry -1

Opening

inventor

y 500U £20

£10,00

0 500 @ 20 £10,000

Janua

ry -18

Goods

purchase 800U £24

£19,20

0

500 @ 20

800 @ 24

£29,200

Janua

ry -25

Goods

Purchase 700U £26

£18,20

0

500 @ 20

800 @ 24

700 @2 6

£47,400

Janua

ry -25 Sales 500 £20

£10,00

0

800 £24

£19,20

0

100 £26 £2,600

1400

£31,80

0

Computing inventory by using various methods

a. First in, first out \

In accordance to such method Smart Looks lay high level of emphasis on selling product

which is first purchased by the company (Swarr and et.al., 2011).

Date Items

Purchase Sale Closing stock

Units

Pric

e

Produc

t

Unit

s Price

Produc

t

Janua

ry -1

Opening

inventor

y 500U £20

£10,00

0 500 @ 20 £10,000

Janua

ry -18

Goods

purchase 800U £24

£19,20

0

500 @ 20

800 @ 24

£29,200

Janua

ry -25

Goods

Purchase 700U £26

£18,20

0

500 @ 20

800 @ 24

700 @2 6

£47,400

Janua

ry -25 Sales 500 £20

£10,00

0

800 £24

£19,20

0

100 £26 £2,600

1400

£31,80

0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Janua

ry -31

Ending

stock

600 @ 26 £15,600

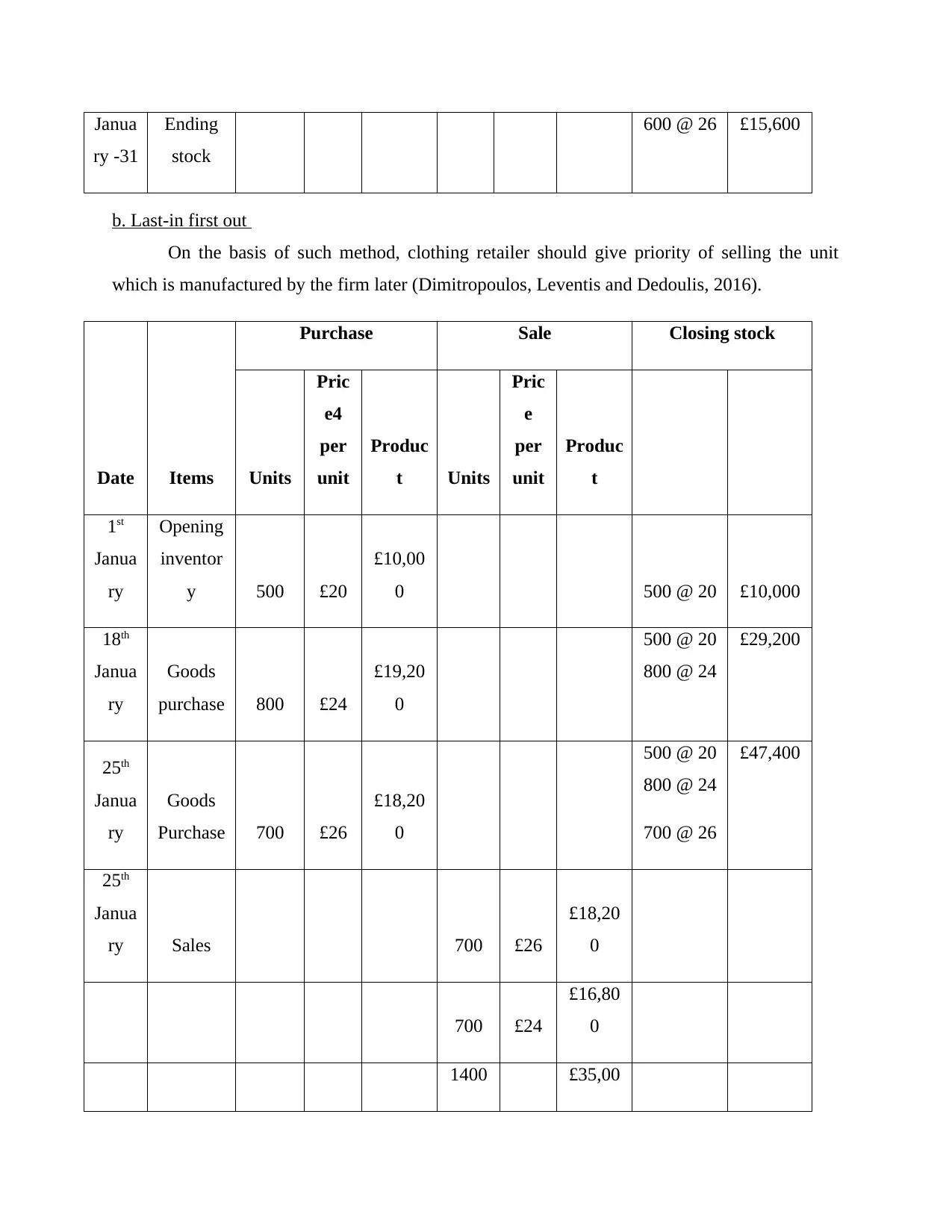

b. Last-in first out

On the basis of such method, clothing retailer should give priority of selling the unit

which is manufactured by the firm later (Dimitropoulos, Leventis and Dedoulis, 2016).

Date Items

Purchase Sale Closing stock

Units

Pric

e4

per

unit

Produc

t Units

Pric

e

per

unit

Produc

t

1st

Janua

ry

Opening

inventor

y 500 £20

£10,00

0 500 @ 20 £10,000

18th

Janua

ry

Goods

purchase 800 £24

£19,20

0

500 @ 20

800 @ 24

£29,200

25th

Janua

ry

Goods

Purchase 700 £26

£18,20

0

500 @ 20

800 @ 24

700 @ 26

£47,400

25th

Janua

ry Sales 700 £26

£18,20

0

700 £24

£16,80

0

1400 £35,00

ry -31

Ending

stock

600 @ 26 £15,600

b. Last-in first out

On the basis of such method, clothing retailer should give priority of selling the unit

which is manufactured by the firm later (Dimitropoulos, Leventis and Dedoulis, 2016).

Date Items

Purchase Sale Closing stock

Units

Pric

e4

per

unit

Produc

t Units

Pric

e

per

unit

Produc

t

1st

Janua

ry

Opening

inventor

y 500 £20

£10,00

0 500 @ 20 £10,000

18th

Janua

ry

Goods

purchase 800 £24

£19,20

0

500 @ 20

800 @ 24

£29,200

25th

Janua

ry

Goods

Purchase 700 £26

£18,20

0

500 @ 20

800 @ 24

700 @ 26

£47,400

25th

Janua

ry Sales 700 £26

£18,20

0

700 £24

£16,80

0

1400 £35,00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0

Jan-

31

Closing

stock

100 @ 24

500 @ 20

£12,400

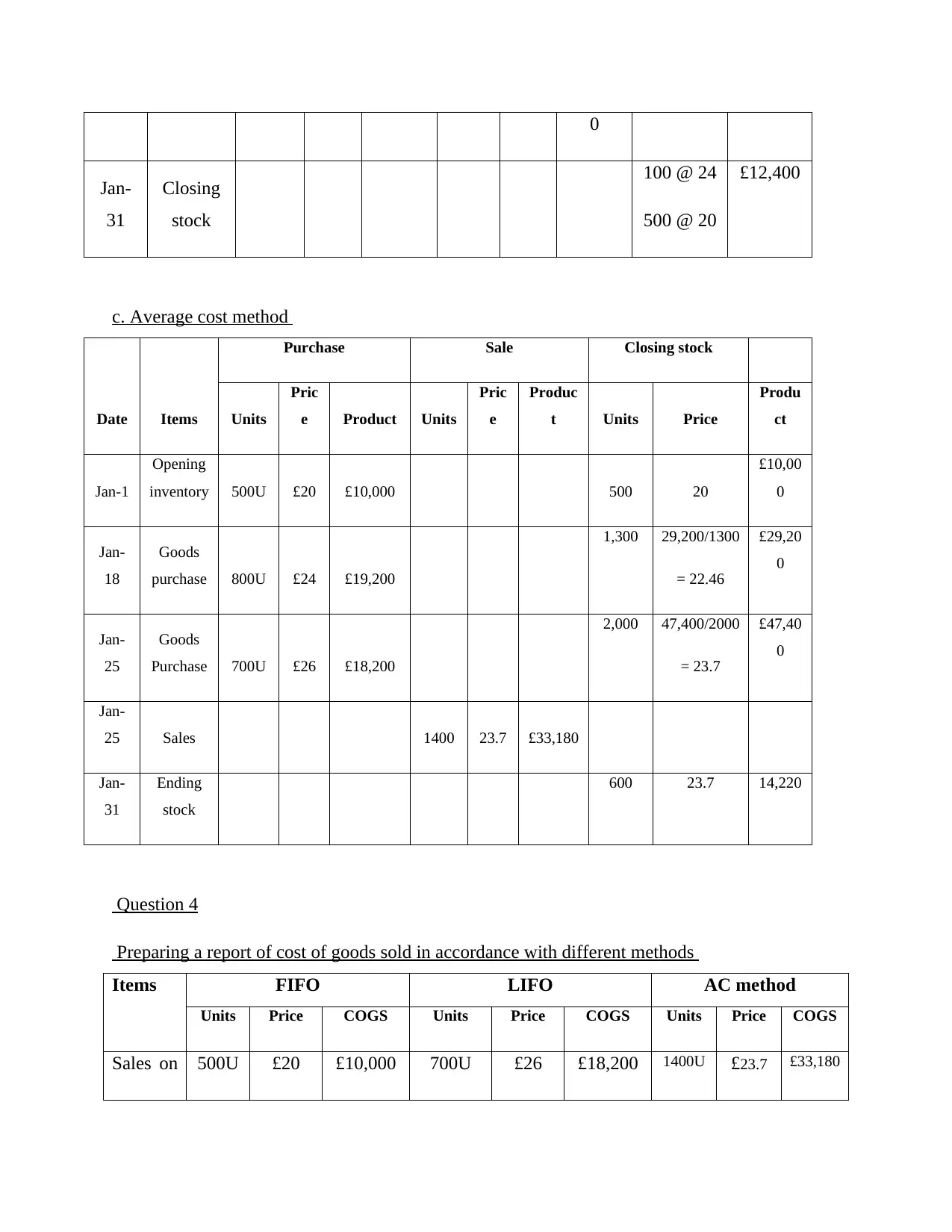

c. Average cost method

Date Items

Purchase Sale Closing stock

Units

Pric

e Product Units

Pric

e

Produc

t Units Price

Produ

ct

Jan-1

Opening

inventory 500U £20 £10,000 500 20

£10,00

0

Jan-

18

Goods

purchase 800U £24 £19,200

1,300 29,200/1300

= 22.46

£29,20

0

Jan-

25

Goods

Purchase 700U £26 £18,200

2,000 47,400/2000

= 23.7

£47,40

0

Jan-

25 Sales 1400 23.7 £33,180

Jan-

31

Ending

stock

600 23.7 14,220

Question 4

Preparing a report of cost of goods sold in accordance with different methods

Items FIFO LIFO AC method

Units Price COGS Units Price COGS Units Price COGS

Sales on 500U £20 £10,000 700U £26 £18,200 1400U £23.7 £33,180

Jan-

31

Closing

stock

100 @ 24

500 @ 20

£12,400

c. Average cost method

Date Items

Purchase Sale Closing stock

Units

Pric

e Product Units

Pric

e

Produc

t Units Price

Produ

ct

Jan-1

Opening

inventory 500U £20 £10,000 500 20

£10,00

0

Jan-

18

Goods

purchase 800U £24 £19,200

1,300 29,200/1300

= 22.46

£29,20

0

Jan-

25

Goods

Purchase 700U £26 £18,200

2,000 47,400/2000

= 23.7

£47,40

0

Jan-

25 Sales 1400 23.7 £33,180

Jan-

31

Ending

stock

600 23.7 14,220

Question 4

Preparing a report of cost of goods sold in accordance with different methods

Items FIFO LIFO AC method

Units Price COGS Units Price COGS Units Price COGS

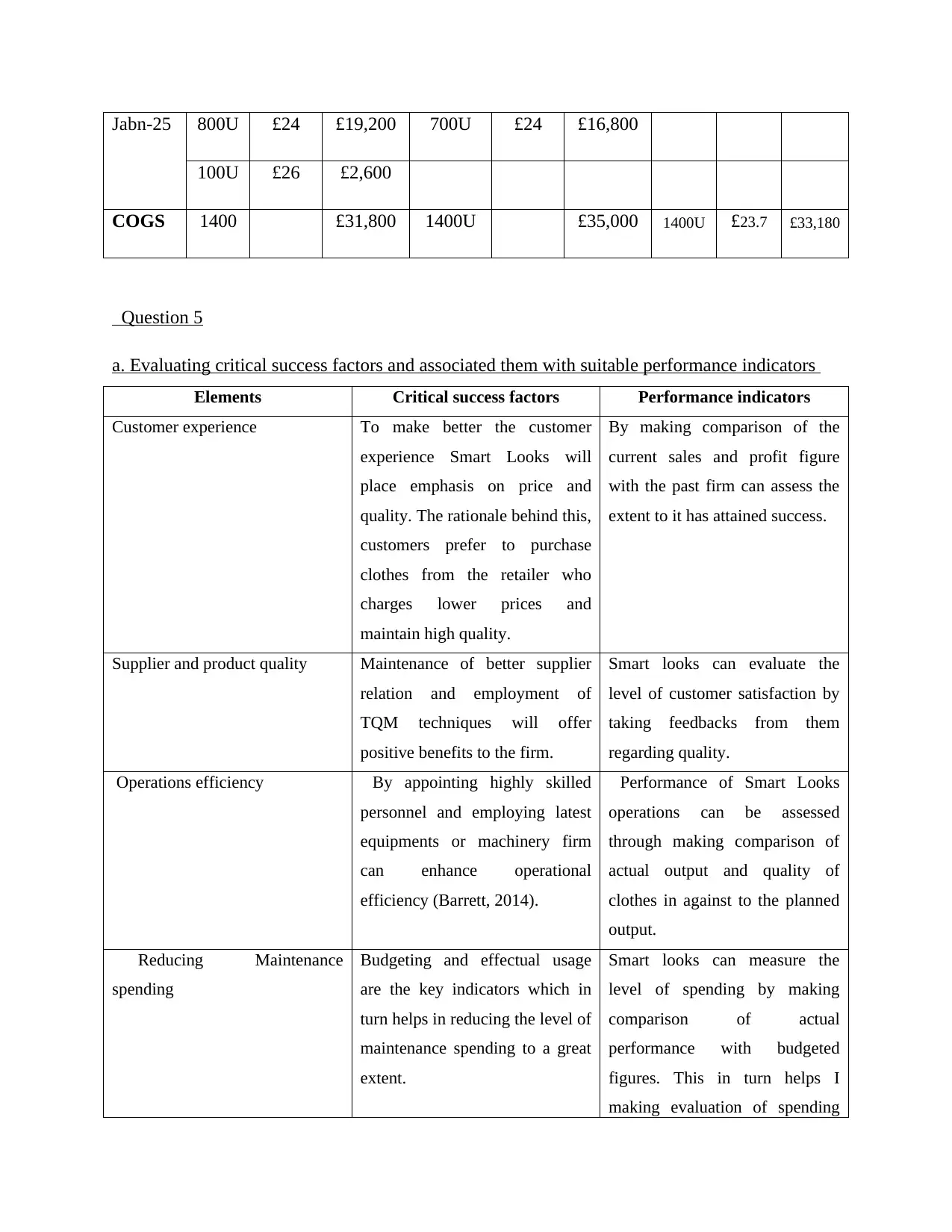

Sales on 500U £20 £10,000 700U £26 £18,200 1400U £23.7 £33,180

Jabn-25 800U £24 £19,200 700U £24 £16,800

100U £26 £2,600

COGS 1400 £31,800 1400U £35,000 1400U £23.7 £33,180

Question 5

a. Evaluating critical success factors and associated them with suitable performance indicators

Elements Critical success factors Performance indicators

Customer experience To make better the customer

experience Smart Looks will

place emphasis on price and

quality. The rationale behind this,

customers prefer to purchase

clothes from the retailer who

charges lower prices and

maintain high quality.

By making comparison of the

current sales and profit figure

with the past firm can assess the

extent to it has attained success.

Supplier and product quality Maintenance of better supplier

relation and employment of

TQM techniques will offer

positive benefits to the firm.

Smart looks can evaluate the

level of customer satisfaction by

taking feedbacks from them

regarding quality.

Operations efficiency By appointing highly skilled

personnel and employing latest

equipments or machinery firm

can enhance operational

efficiency (Barrett, 2014).

Performance of Smart Looks

operations can be assessed

through making comparison of

actual output and quality of

clothes in against to the planned

output.

Reducing Maintenance

spending

Budgeting and effectual usage

are the key indicators which in

turn helps in reducing the level of

maintenance spending to a great

extent.

Smart looks can measure the

level of spending by making

comparison of actual

performance with budgeted

figures. This in turn helps I

making evaluation of spending

100U £26 £2,600

COGS 1400 £31,800 1400U £35,000 1400U £23.7 £33,180

Question 5

a. Evaluating critical success factors and associated them with suitable performance indicators

Elements Critical success factors Performance indicators

Customer experience To make better the customer

experience Smart Looks will

place emphasis on price and

quality. The rationale behind this,

customers prefer to purchase

clothes from the retailer who

charges lower prices and

maintain high quality.

By making comparison of the

current sales and profit figure

with the past firm can assess the

extent to it has attained success.

Supplier and product quality Maintenance of better supplier

relation and employment of

TQM techniques will offer

positive benefits to the firm.

Smart looks can evaluate the

level of customer satisfaction by

taking feedbacks from them

regarding quality.

Operations efficiency By appointing highly skilled

personnel and employing latest

equipments or machinery firm

can enhance operational

efficiency (Barrett, 2014).

Performance of Smart Looks

operations can be assessed

through making comparison of

actual output and quality of

clothes in against to the planned

output.

Reducing Maintenance

spending

Budgeting and effectual usage

are the key indicators which in

turn helps in reducing the level of

maintenance spending to a great

extent.

Smart looks can measure the

level of spending by making

comparison of actual

performance with budgeted

figures. This in turn helps I

making evaluation of spending

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.