Examining Management Accounting Techniques in SMEs

VerifiedAdded on 2020/06/03

|16

|5502

|130

AI Summary

The text analyzes the use of management accounting techniques within small and medium-sized enterprises (SMEs), focusing on how these businesses apply financial strategies to improve efficiency and sustainability. Key themes include the implementation of environmental management accounting tools, which are crucial for fostering innovation and addressing ecological concerns. Several academic studies, such as those by Ferreira et al., Grabner and Moers, and Papaspyropoulos et al., provide empirical evidence on current practices and challenges faced by SMEs in adopting these techniques. The analysis highlights the gap between theoretical frameworks and practical applications, suggesting areas for further research to enhance the effectiveness of management accounting within smaller business contexts.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and essential requirements of its different types..........................1

P2 Methods used in management accounting reporting.............................................................3

M1 Evaluation of benefits of management accoutring within the organisation.........................5

D1 Integration of management accounting and management accounting reporting...................5

TASK 2............................................................................................................................................5

P3 Calculation of cost by using appropriate techniques.............................................................5

M2 Range of management accounting techniques......................................................................8

D2 Financial report with the interpretation of data.....................................................................8

P4 Advantages and disadvantages of various type of planning tools.........................................8

M3. Evaluation of planning tools..............................................................................................11

D3. Critical analysis of financial problem................................................................................11

TASK 3..........................................................................................................................................11

P5 Comparison of management accounting system subject to implanting in organisation......11

M4 management accounting as a leading factor.......................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and essential requirements of its different types..........................1

P2 Methods used in management accounting reporting.............................................................3

M1 Evaluation of benefits of management accoutring within the organisation.........................5

D1 Integration of management accounting and management accounting reporting...................5

TASK 2............................................................................................................................................5

P3 Calculation of cost by using appropriate techniques.............................................................5

M2 Range of management accounting techniques......................................................................8

D2 Financial report with the interpretation of data.....................................................................8

P4 Advantages and disadvantages of various type of planning tools.........................................8

M3. Evaluation of planning tools..............................................................................................11

D3. Critical analysis of financial problem................................................................................11

TASK 3..........................................................................................................................................11

P5 Comparison of management accounting system subject to implanting in organisation......11

M4 management accounting as a leading factor.......................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is one of the branches of accounting process used by managers

and senior level management of company (Otley and Emmanuel, 2013). This is the management

system which contains principles, standards, rules and guidelines in respect of managing

divisions and departments of an organisation. This report is made around management and

accounting process subject to small scale industry. Aspen travel and hospitality industry is the

chosen organisation in report to describe the meaning and scope of management accounting.

Different types of management accounting systems, methods and principles are used in

management accounting process elaborated briefly. Cost accounting process and systems are

discussed for reducing cost of company by applying absorption and marginal costing.

Advantages and disadvantages of various types of planning tools are used with respect to

budgetary control as well. There is a comparison made in respect of adapting management

accounting system in organisation.

TASK 1

P1. Management accounting and essential requirements of its different types

Management accounting

This is an accounting system used to provide information and data to managers and

senior authorises. Management accounting also considered as managerial account. Information

and data provided under this accounting system are useful for decision making process and

strategic planning. It is one of the practical approaches that is widely used in management and

operations (Papaspyropoulos and et. al., 2012). It works as a bridge to flow the information and

data in a systematic manner. Making plans, budgets, growth model and forecasting are the main

fields in which management accounting concept is used. To grab new growth opportunities and

adopting new techniques for better operations are the main objectives of organisation. Various

definitions are given with respect to management accounting. According to Institute of

Management Accountants (IMA), management accounting is a professional way to represent

accounting and financial details to the managers. It includes partnering in management decision

making, developing plans, performance analysis and management, financial reporting as well as

summarised report, implementation and formulation of organisation's strategy.

1

Management accounting is one of the branches of accounting process used by managers

and senior level management of company (Otley and Emmanuel, 2013). This is the management

system which contains principles, standards, rules and guidelines in respect of managing

divisions and departments of an organisation. This report is made around management and

accounting process subject to small scale industry. Aspen travel and hospitality industry is the

chosen organisation in report to describe the meaning and scope of management accounting.

Different types of management accounting systems, methods and principles are used in

management accounting process elaborated briefly. Cost accounting process and systems are

discussed for reducing cost of company by applying absorption and marginal costing.

Advantages and disadvantages of various types of planning tools are used with respect to

budgetary control as well. There is a comparison made in respect of adapting management

accounting system in organisation.

TASK 1

P1. Management accounting and essential requirements of its different types

Management accounting

This is an accounting system used to provide information and data to managers and

senior authorises. Management accounting also considered as managerial account. Information

and data provided under this accounting system are useful for decision making process and

strategic planning. It is one of the practical approaches that is widely used in management and

operations (Papaspyropoulos and et. al., 2012). It works as a bridge to flow the information and

data in a systematic manner. Making plans, budgets, growth model and forecasting are the main

fields in which management accounting concept is used. To grab new growth opportunities and

adopting new techniques for better operations are the main objectives of organisation. Various

definitions are given with respect to management accounting. According to Institute of

Management Accountants (IMA), management accounting is a professional way to represent

accounting and financial details to the managers. It includes partnering in management decision

making, developing plans, performance analysis and management, financial reporting as well as

summarised report, implementation and formulation of organisation's strategy.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As per the American Institute of Certified Public Accounts (AICPA), management

accounting works in three major areas such as strategic management, performance management

and risk management. It helps the organisation as a supporter to manage the operations and play

a role of a partner to make strategies and plans. It improves the process of decision making and

enhance credibility of financial statements and financial reports. It assists accountants and

managers to analyse the risk and forecasting of future opportunities. It is a way to produce

information for financial decisions and decision oriented information to make policies and

accounting compliance structure of company.

Person who manage all the accounting records are considered as value creators.

Knowledge and experience of management accounting can be obtained by management of

treasury, efficient and accurate auditing process, marketing and valuation of assets, analysis of

risk management, pricing and logistic and information system.

Different type of management accounting systems

Governmental accounting: accounting of legislations, legal rules and keeping legal

records are the main key work fields managed under this accounting system. This accounting

system also considered as federal accounting and public accounting system (Renz, 2016).

Governmental accounting system was implemented to separate accounting for public and private

sector. Determine aims and objective of private and public sector was the main reason to

introduce governmental accounting system in organisational context. This accounting tool is

beneficial to ascertain public and private organisation's financial position and performance and

bifurcate the rules and regulation are the

Financial accounting: Finance is a major requirement of any type and nature of

business. Finance is one of the sources which helps to execute the functions and operations in

smooth way. This is another branch of accounting helps to manage the requirement of finance in

organisation. Find out best option to generate finance and proper allocation and utilisation

examined in this accounting system. Financial statements, financial reports are made under this

accounting system to analyse the financial strength of company.

Tax accounting: payment of tax and calculate the amount of tax liability is one of the

major field of accounting system. Rules, standards, provisions and regulations are made in

respect of tax accounting. In large organisation there is a specific branch of accounting found in

which team of accountants works as charted accountants, company secretary and cost

2

accounting works in three major areas such as strategic management, performance management

and risk management. It helps the organisation as a supporter to manage the operations and play

a role of a partner to make strategies and plans. It improves the process of decision making and

enhance credibility of financial statements and financial reports. It assists accountants and

managers to analyse the risk and forecasting of future opportunities. It is a way to produce

information for financial decisions and decision oriented information to make policies and

accounting compliance structure of company.

Person who manage all the accounting records are considered as value creators.

Knowledge and experience of management accounting can be obtained by management of

treasury, efficient and accurate auditing process, marketing and valuation of assets, analysis of

risk management, pricing and logistic and information system.

Different type of management accounting systems

Governmental accounting: accounting of legislations, legal rules and keeping legal

records are the main key work fields managed under this accounting system. This accounting

system also considered as federal accounting and public accounting system (Renz, 2016).

Governmental accounting system was implemented to separate accounting for public and private

sector. Determine aims and objective of private and public sector was the main reason to

introduce governmental accounting system in organisational context. This accounting tool is

beneficial to ascertain public and private organisation's financial position and performance and

bifurcate the rules and regulation are the

Financial accounting: Finance is a major requirement of any type and nature of

business. Finance is one of the sources which helps to execute the functions and operations in

smooth way. This is another branch of accounting helps to manage the requirement of finance in

organisation. Find out best option to generate finance and proper allocation and utilisation

examined in this accounting system. Financial statements, financial reports are made under this

accounting system to analyse the financial strength of company.

Tax accounting: payment of tax and calculate the amount of tax liability is one of the

major field of accounting system. Rules, standards, provisions and regulations are made in

respect of tax accounting. In large organisation there is a specific branch of accounting found in

which team of accountants works as charted accountants, company secretary and cost

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accountants. They keep monitoring the legal actions and activities in respect of changing tax

rates. They follow the rules and standards given by GAAP which is known as Generally

Accepted Accounting Rules and analyse records to calculate tax liabilities or make provision for

taxation.

Forensic accounting: managing records of criminal disputes, contingent liabilities,

physical verification and valuation of assets and liabilities, fair and clean representation of

financial statements and reports are considered in forensic accounting system (Kotas, 2014).

Reports, informations and sources in this accounting system are considered as evidence and

witnesses proofs in disputes and fraud cases.

Project accounting: this accounting tool is used to measure future opportunities and

advantages for sustainable growth of company. Supervision of tasks and projects, accounting for

construction contracts and venture capital accounting are done in this accounting system. This

accounting system is know as forecasting system. Making financial budget, resources

management and analyse project requirement are the key factors analyse in project accounting

system.

Social accounting: Accounting of corporate social responsibilities, accounting for

research and development departments are the main aspects considered in this accounting

system. This is also known as ethical accounting system to analyse the environment and

geographical structure of organisation. There is an annual report is published by the auditors in

which the details of consumption of natural resources defined in report briefly.

P2 Methods used in management accounting reporting

Management accounting reporting

Accounting report are the essential part of making certain and accurate information

regarding functions and operations of business. These are the informations are used to produce

information and making effective strategies management for decision making (Lavia López and

Hiebl, 2014). Accounting reports provide an analysation report of performance, efficiency of

operations and functional department apart from it the financial strength also can be measured by

accounting management and reporting. There is a specific time duration is set to produce

accounting reports. Comprehensive accounting report is prepared specifically for critical

analysation of performance and efficiency level of organisation. These reports are prepared

3

rates. They follow the rules and standards given by GAAP which is known as Generally

Accepted Accounting Rules and analyse records to calculate tax liabilities or make provision for

taxation.

Forensic accounting: managing records of criminal disputes, contingent liabilities,

physical verification and valuation of assets and liabilities, fair and clean representation of

financial statements and reports are considered in forensic accounting system (Kotas, 2014).

Reports, informations and sources in this accounting system are considered as evidence and

witnesses proofs in disputes and fraud cases.

Project accounting: this accounting tool is used to measure future opportunities and

advantages for sustainable growth of company. Supervision of tasks and projects, accounting for

construction contracts and venture capital accounting are done in this accounting system. This

accounting system is know as forecasting system. Making financial budget, resources

management and analyse project requirement are the key factors analyse in project accounting

system.

Social accounting: Accounting of corporate social responsibilities, accounting for

research and development departments are the main aspects considered in this accounting

system. This is also known as ethical accounting system to analyse the environment and

geographical structure of organisation. There is an annual report is published by the auditors in

which the details of consumption of natural resources defined in report briefly.

P2 Methods used in management accounting reporting

Management accounting reporting

Accounting report are the essential part of making certain and accurate information

regarding functions and operations of business. These are the informations are used to produce

information and making effective strategies management for decision making (Lavia López and

Hiebl, 2014). Accounting reports provide an analysation report of performance, efficiency of

operations and functional department apart from it the financial strength also can be measured by

accounting management and reporting. There is a specific time duration is set to produce

accounting reports. Comprehensive accounting report is prepared specifically for critical

analysation of performance and efficiency level of organisation. These reports are prepared

3

quarterly, half yearly to analyse finance requirement in organisation. Below are type of

accounting report defined in respect of management accounting;

Budget reports: these reports are considered as fundamental reports helps to ascertain

further requirement of resources within the organisation. It is useful to business owners to

understand and control the cost of operations and management. Business structure is made of

multiple layers and levels (Morales and Lambert, 2013). Budget reports are helpful for small

scale organisation, analysation of performance of company. It is an estimation of information on

the basis of previous records and information. Actual expenses and incomes are considered while

making budget reports. Some fractional changes and adjustments are included in these reports as

inflation rates, increased rate of labour, material and overheads etc. budgets reports indicates

towards forecasting speciality and strength of company in respect of upcoming years. Budget

reports are considered as predetermined structure of operations which reduce the work load and

pressure from the shoulders of managers.

Job cost reports: large business structures operate multiple functions and job sectors. To

maintain accounting and financing records of particular job is considered in this repost. For

example an manufacturing company has three job departments such as casting, moulding and

designing. There is a separate accounts and measurement system are used to record informations

and transaction for every batch (Tucker and Lowe, 2014). Cost accountant provides all the

relevant informations from all the job departments and produce a summarised report to

managers. These reports help to understand the progress and status of a particular job or project.

It bifurcate the higher earning areas and helps to make separate accounting structure.

Accounts receivable reports: this is an analysis of collection from debtors, account

receivables, bills receivable and collection of cheque payments. These reports are prepared by

those organisations which deals in physical goods and products. There is a business cycle is

found in manufacturing industries. Calculation of operating cycle and cash conversion cycle are

the method which are used to analyse payback period of collection from debtors and account

receivables. These are the main informations used to frame accounts receivable reports for an

organisation. It defines the fluctuation of cash inflows and outflows in organisation. It helps to

set the calling period of getting cash from debtors. There are invoices maintained for 30 days, 90

days and 6 days.

4

accounting report defined in respect of management accounting;

Budget reports: these reports are considered as fundamental reports helps to ascertain

further requirement of resources within the organisation. It is useful to business owners to

understand and control the cost of operations and management. Business structure is made of

multiple layers and levels (Morales and Lambert, 2013). Budget reports are helpful for small

scale organisation, analysation of performance of company. It is an estimation of information on

the basis of previous records and information. Actual expenses and incomes are considered while

making budget reports. Some fractional changes and adjustments are included in these reports as

inflation rates, increased rate of labour, material and overheads etc. budgets reports indicates

towards forecasting speciality and strength of company in respect of upcoming years. Budget

reports are considered as predetermined structure of operations which reduce the work load and

pressure from the shoulders of managers.

Job cost reports: large business structures operate multiple functions and job sectors. To

maintain accounting and financing records of particular job is considered in this repost. For

example an manufacturing company has three job departments such as casting, moulding and

designing. There is a separate accounts and measurement system are used to record informations

and transaction for every batch (Tucker and Lowe, 2014). Cost accountant provides all the

relevant informations from all the job departments and produce a summarised report to

managers. These reports help to understand the progress and status of a particular job or project.

It bifurcate the higher earning areas and helps to make separate accounting structure.

Accounts receivable reports: this is an analysis of collection from debtors, account

receivables, bills receivable and collection of cheque payments. These reports are prepared by

those organisations which deals in physical goods and products. There is a business cycle is

found in manufacturing industries. Calculation of operating cycle and cash conversion cycle are

the method which are used to analyse payback period of collection from debtors and account

receivables. These are the main informations used to frame accounts receivable reports for an

organisation. It defines the fluctuation of cash inflows and outflows in organisation. It helps to

set the calling period of getting cash from debtors. There are invoices maintained for 30 days, 90

days and 6 days.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory and manufacturing reports: these reports also used in manufacturing and

retail industries. Management of inventories and stock is one of the essential requirement for

manufacturing and production organisation (van der Steen, 2011.). To manage the requirement

of raw material, labour and resources subject to manufacturing process, inventory and

manufacturing reports are prepared. Payment rates to labour, rates of wastage, cost per unit by

including overheads are the major factors which are considered in this report. It helps to

assemble the manufacturing departments related to producing different type of goods and

products. Managers would able to consolidate separate departmental and sectional informations

in single structure.

Other subquery reports: All other reports such as administrative reports, managing,

operating expenses and office charges reports, are considered in subsidiary reports. There is a

apart accounting system is used by organisations to record small expenses, records of

administrative and operating expenses. Subsidiary reports provides a conclusive reports of

various informations from small divisions and departments of company.

M1 Evaluation of benefits of management accoutring within the organisation

Decision making on of the scenario in which management accounting system plays vital

role (Lennox, Francis and Wang, 2011). Planning, forecasting, cost analyse, performance

management and analysation, making compliance strategies, consideration of incremental,

evaluation of opportunity and sunk cost are the types of scenarios in which management

accounting concepts are used widely.

D1 Integration of management accounting and management accounting reporting

Management of organisation depends upon management of accounting records, financial

informations, resources management (Grabner and Moers, 2013). Accounting is a process which

helps to record each and every transaction in structural format and helps to summarise the

information. Whereas accounting report is prepared on the basis of accounting records and

financial informations. These reports remain essential to senior level of management and

authorities.

TASK 2

P3 Calculation of cost by using appropriate techniques

There are various cost techniques are found in organisational context

5

retail industries. Management of inventories and stock is one of the essential requirement for

manufacturing and production organisation (van der Steen, 2011.). To manage the requirement

of raw material, labour and resources subject to manufacturing process, inventory and

manufacturing reports are prepared. Payment rates to labour, rates of wastage, cost per unit by

including overheads are the major factors which are considered in this report. It helps to

assemble the manufacturing departments related to producing different type of goods and

products. Managers would able to consolidate separate departmental and sectional informations

in single structure.

Other subquery reports: All other reports such as administrative reports, managing,

operating expenses and office charges reports, are considered in subsidiary reports. There is a

apart accounting system is used by organisations to record small expenses, records of

administrative and operating expenses. Subsidiary reports provides a conclusive reports of

various informations from small divisions and departments of company.

M1 Evaluation of benefits of management accoutring within the organisation

Decision making on of the scenario in which management accounting system plays vital

role (Lennox, Francis and Wang, 2011). Planning, forecasting, cost analyse, performance

management and analysation, making compliance strategies, consideration of incremental,

evaluation of opportunity and sunk cost are the types of scenarios in which management

accounting concepts are used widely.

D1 Integration of management accounting and management accounting reporting

Management of organisation depends upon management of accounting records, financial

informations, resources management (Grabner and Moers, 2013). Accounting is a process which

helps to record each and every transaction in structural format and helps to summarise the

information. Whereas accounting report is prepared on the basis of accounting records and

financial informations. These reports remain essential to senior level of management and

authorities.

TASK 2

P3 Calculation of cost by using appropriate techniques

There are various cost techniques are found in organisational context

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Uniform costing: this is the costing techniques is the application of the same accounting

and costing principle, procedures and methods applied in same type of business industry. This is

the technique which used usual accounting methods and principles to make accounting

informations approachable to managers and senior level management. It is a set of multiple

principles and procedures to calculate cost, targets and profitability of organisation. As per

CIMA, London technology elaborate the definition of uniform costing as common system of

evaluating cost of multiple sections and departments.

Marginal costing: this is one of the common cost evaluating technique used

manufacturing and production companies. This is the method which is used to calculate the cost

on per unit produced in organisation. This is the cost method help to ascertain the cost by

increasing and decreasing the volume of product. Analysation of cost is based upon variation of

production units. This cost method contains all the variable cost which incurred in manufacturing

and production process. Labour, raw material, overheads and direct expenses are the types of

variable cost considered in while calculating cost per unit.

Standard costing: It is considered as a practice to analyse the cost records for making a

projected report of production and sales units. There is a difference evaluated between actual

cost and expected cost under this cost evaluation method. Expected cost also known as cost

budgeted cost. Variance analysation is one of the factor which is analysed in respect of variation

in labour cost, direct material cost, finished goods cost and variances of production overheads.

This method is used to compare the difference between predicted cost and actual cost of product.

Historical costing: Measurement of cost based upon historical cost. This costing system

is basically used to record the assets in books on the amount when it was acquired in the

organisation (DRURY, 2013). Organisations use the guidelines and rules given by GAAP

regarding evaluating the cost of assets.

Direct costing: All the direct factors are considered in this accounting system to analyse

the cost of products. These are the cost directly incurred in manufacturing and production

process. This costing system is also used in decision making and strategic planning process.

Absorption costing: this is also one of the cost calculating techniques which helps to

evaluate overall production and manufacturing cost of product in organisation. This method is

considered relevant and appropriate to calculate the cost by considering variable and fixed cost.

This method is also known as full costing or overall evaluation of costing method. This method

6

and costing principle, procedures and methods applied in same type of business industry. This is

the technique which used usual accounting methods and principles to make accounting

informations approachable to managers and senior level management. It is a set of multiple

principles and procedures to calculate cost, targets and profitability of organisation. As per

CIMA, London technology elaborate the definition of uniform costing as common system of

evaluating cost of multiple sections and departments.

Marginal costing: this is one of the common cost evaluating technique used

manufacturing and production companies. This is the method which is used to calculate the cost

on per unit produced in organisation. This is the cost method help to ascertain the cost by

increasing and decreasing the volume of product. Analysation of cost is based upon variation of

production units. This cost method contains all the variable cost which incurred in manufacturing

and production process. Labour, raw material, overheads and direct expenses are the types of

variable cost considered in while calculating cost per unit.

Standard costing: It is considered as a practice to analyse the cost records for making a

projected report of production and sales units. There is a difference evaluated between actual

cost and expected cost under this cost evaluation method. Expected cost also known as cost

budgeted cost. Variance analysation is one of the factor which is analysed in respect of variation

in labour cost, direct material cost, finished goods cost and variances of production overheads.

This method is used to compare the difference between predicted cost and actual cost of product.

Historical costing: Measurement of cost based upon historical cost. This costing system

is basically used to record the assets in books on the amount when it was acquired in the

organisation (DRURY, 2013). Organisations use the guidelines and rules given by GAAP

regarding evaluating the cost of assets.

Direct costing: All the direct factors are considered in this accounting system to analyse

the cost of products. These are the cost directly incurred in manufacturing and production

process. This costing system is also used in decision making and strategic planning process.

Absorption costing: this is also one of the cost calculating techniques which helps to

evaluate overall production and manufacturing cost of product in organisation. This method is

considered relevant and appropriate to calculate the cost by considering variable and fixed cost.

This method is also known as full costing or overall evaluation of costing method. This method

6

is able to divide the variable and fixed factors incurred in manufacturing process. All the fixed

overhead and expenses also considered with variable expenses while calculating profit per

product.

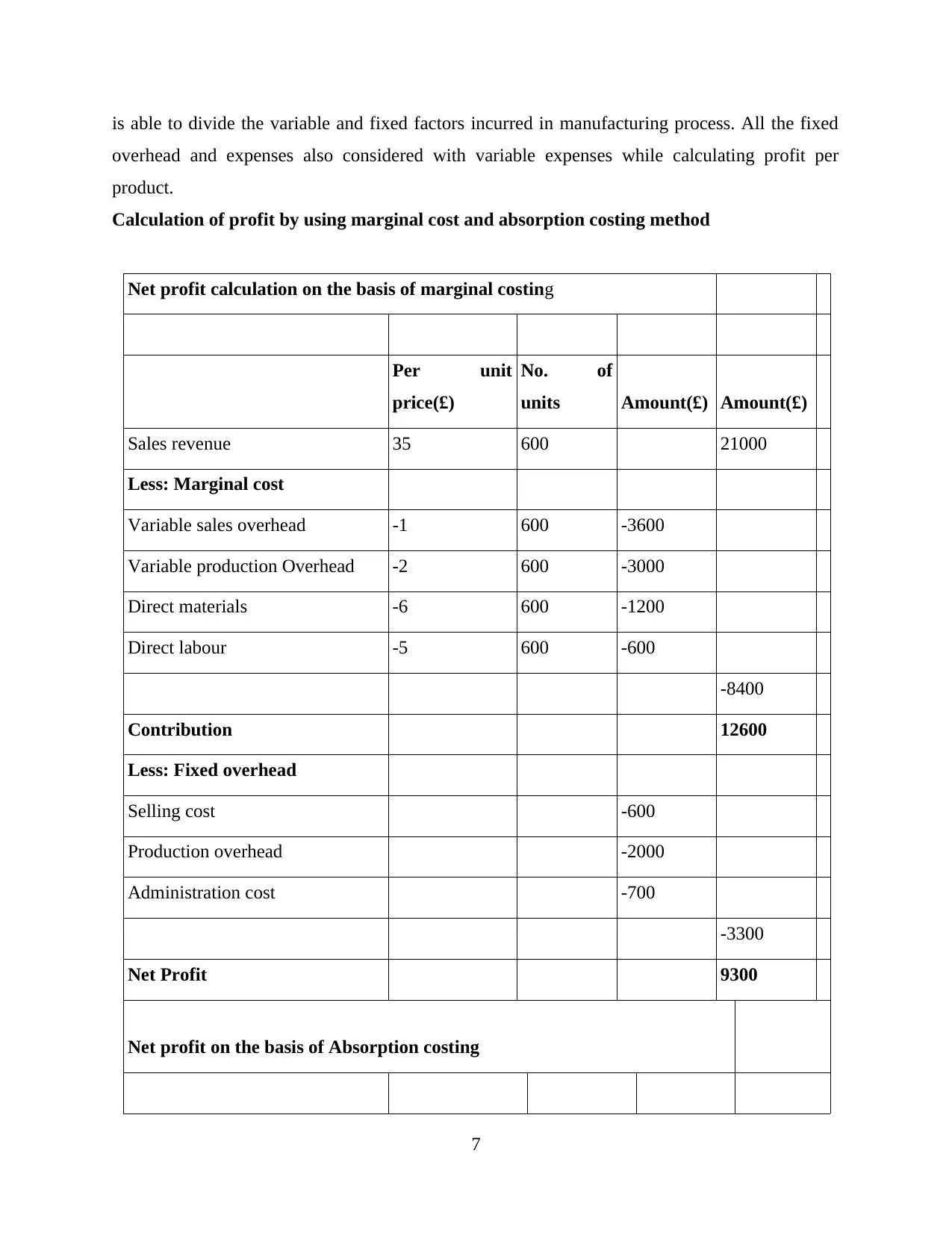

Calculation of profit by using marginal cost and absorption costing method

Net profit calculation on the basis of marginal costing

Per unit

price(£)

No. of

units Amount(£) Amount(£)

Sales revenue 35 600 21000

Less: Marginal cost

Variable sales overhead -1 600 -3600

Variable production Overhead -2 600 -3000

Direct materials -6 600 -1200

Direct labour -5 600 -600

-8400

Contribution 12600

Less: Fixed overhead

Selling cost -600

Production overhead -2000

Administration cost -700

-3300

Net Profit 9300

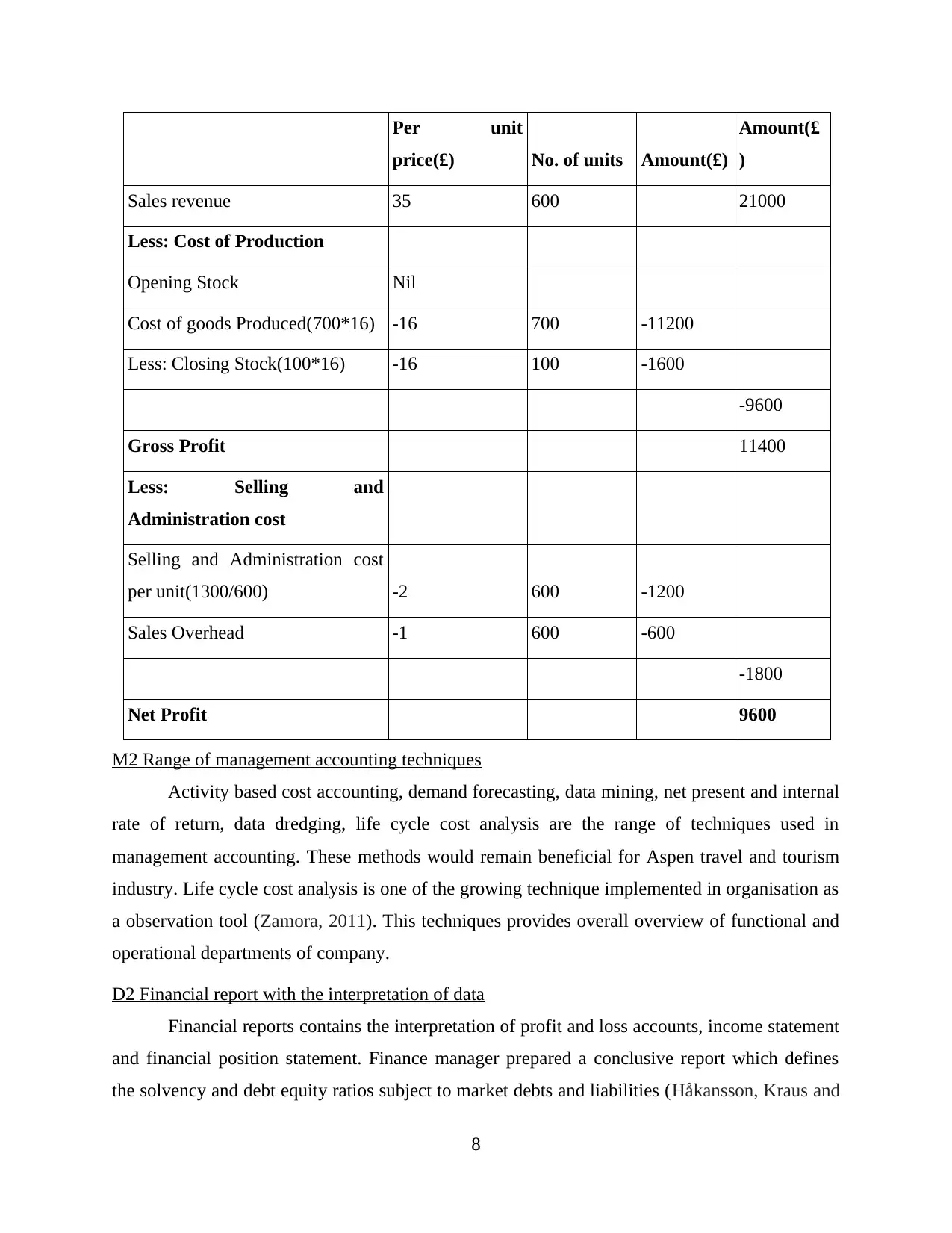

Net profit on the basis of Absorption costing

7

overhead and expenses also considered with variable expenses while calculating profit per

product.

Calculation of profit by using marginal cost and absorption costing method

Net profit calculation on the basis of marginal costing

Per unit

price(£)

No. of

units Amount(£) Amount(£)

Sales revenue 35 600 21000

Less: Marginal cost

Variable sales overhead -1 600 -3600

Variable production Overhead -2 600 -3000

Direct materials -6 600 -1200

Direct labour -5 600 -600

-8400

Contribution 12600

Less: Fixed overhead

Selling cost -600

Production overhead -2000

Administration cost -700

-3300

Net Profit 9300

Net profit on the basis of Absorption costing

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Per unit

price(£) No. of units Amount(£)

Amount(£

)

Sales revenue 35 600 21000

Less: Cost of Production

Opening Stock Nil

Cost of goods Produced(700*16) -16 700 -11200

Less: Closing Stock(100*16) -16 100 -1600

-9600

Gross Profit 11400

Less: Selling and

Administration cost

Selling and Administration cost

per unit(1300/600) -2 600 -1200

Sales Overhead -1 600 -600

-1800

Net Profit 9600

M2 Range of management accounting techniques

Activity based cost accounting, demand forecasting, data mining, net present and internal

rate of return, data dredging, life cycle cost analysis are the range of techniques used in

management accounting. These methods would remain beneficial for Aspen travel and tourism

industry. Life cycle cost analysis is one of the growing technique implemented in organisation as

a observation tool (Zamora, 2011). This techniques provides overall overview of functional and

operational departments of company.

D2 Financial report with the interpretation of data

Financial reports contains the interpretation of profit and loss accounts, income statement

and financial position statement. Finance manager prepared a conclusive report which defines

the solvency and debt equity ratios subject to market debts and liabilities (Håkansson, Kraus and

8

price(£) No. of units Amount(£)

Amount(£

)

Sales revenue 35 600 21000

Less: Cost of Production

Opening Stock Nil

Cost of goods Produced(700*16) -16 700 -11200

Less: Closing Stock(100*16) -16 100 -1600

-9600

Gross Profit 11400

Less: Selling and

Administration cost

Selling and Administration cost

per unit(1300/600) -2 600 -1200

Sales Overhead -1 600 -600

-1800

Net Profit 9600

M2 Range of management accounting techniques

Activity based cost accounting, demand forecasting, data mining, net present and internal

rate of return, data dredging, life cycle cost analysis are the range of techniques used in

management accounting. These methods would remain beneficial for Aspen travel and tourism

industry. Life cycle cost analysis is one of the growing technique implemented in organisation as

a observation tool (Zamora, 2011). This techniques provides overall overview of functional and

operational departments of company.

D2 Financial report with the interpretation of data

Financial reports contains the interpretation of profit and loss accounts, income statement

and financial position statement. Finance manager prepared a conclusive report which defines

the solvency and debt equity ratios subject to market debts and liabilities (Håkansson, Kraus and

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Lind, eds., 2010). This report also published in annual reports and remain helpful for

shareholders, stakeholders and investors.

P4 Advantages and disadvantages of various type of planning tools

Generally there are three important budgetary control techniques which are used by the

managers of Aspen Travel in order to make effective plans and strategies which also help them

in forecasting project activities. An organisation needs to prepare budget with a motive of

managing and utilising available resources in business operations which brings maximum

outcomes to company. Generally, budget is prepared for one year after forecasting cost in

incurred in future operational activities. It enables managers to evaluate and compare the actual

performance with standard performance and accordingly implement corrective measures in order

to eliminate deviations or problems if any occur during business operations. Utilising available

funds in an optimum manner is the prime objective of preparing budget. The manager needs to

this focus on allocating funds in such important areas of business operations through which they

get maximum positive results.

Budgetary control: The managers of Aspen Travel company is held responsible to

implement budget control techniques which help in managing and controlling financial resources

of company in such an effective manner that the chances of miss-utilisation of funds are

minimized (Moser, 2012). It is important for an organisation to allocate fund in different areas of

department which provide them positive outcomes.

Budgetary control: It is the process of preparing budget on the basis of forecasting and thereafter

making comparison of actual performance with standard one in order to find out the deviations if

any. It helps management to implement corrective actions in order to remove all such deviations

on time so as to achieve desired target.

Objectives of Budgetary control:

The main objective of this an effective tool is to define the goals that need to be achieved

by company in near future.

Formulating plans and strategies to achieve desired targeted within given time frame.

Coordinating the business activities of different departments.

Reduce wastage so as to earn huge profits.

Assigning roles and responsibilities to each individual in order to complete given in an

effective manner.

9

shareholders, stakeholders and investors.

P4 Advantages and disadvantages of various type of planning tools

Generally there are three important budgetary control techniques which are used by the

managers of Aspen Travel in order to make effective plans and strategies which also help them

in forecasting project activities. An organisation needs to prepare budget with a motive of

managing and utilising available resources in business operations which brings maximum

outcomes to company. Generally, budget is prepared for one year after forecasting cost in

incurred in future operational activities. It enables managers to evaluate and compare the actual

performance with standard performance and accordingly implement corrective measures in order

to eliminate deviations or problems if any occur during business operations. Utilising available

funds in an optimum manner is the prime objective of preparing budget. The manager needs to

this focus on allocating funds in such important areas of business operations through which they

get maximum positive results.

Budgetary control: The managers of Aspen Travel company is held responsible to

implement budget control techniques which help in managing and controlling financial resources

of company in such an effective manner that the chances of miss-utilisation of funds are

minimized (Moser, 2012). It is important for an organisation to allocate fund in different areas of

department which provide them positive outcomes.

Budgetary control: It is the process of preparing budget on the basis of forecasting and thereafter

making comparison of actual performance with standard one in order to find out the deviations if

any. It helps management to implement corrective actions in order to remove all such deviations

on time so as to achieve desired target.

Objectives of Budgetary control:

The main objective of this an effective tool is to define the goals that need to be achieved

by company in near future.

Formulating plans and strategies to achieve desired targeted within given time frame.

Coordinating the business activities of different departments.

Reduce wastage so as to earn huge profits.

Assigning roles and responsibilities to each individual in order to complete given in an

effective manner.

9

It also focuses on correcting variances from set standards and also concentrate on

centralising the control system.

Process of Budgetary control:

Discuss with managers to formulate effective strategy: In this step, the managers has

discuss with their staff members of company relating to expenses incurred in future business

activities and accordingly formulate effective strategy.

Record the actual performance: The manager first needs to analyse previous data and

information of different areas of department of company and accordingly, implement strategy

which brings them positive results.

Comparison of actual with the planned: At this stage, company needs to analyse and

compare actual performance with the desired performance in order to find out deviations, if any,

which restrict them in performing in an effective and efficient manner. It helps them in

determining various variable and standard cost of sales.

Determine difference or other variance: In this step, company has to select one qualified

person that effectively review the differences or deviations arise between actual and desired

performance. Appointed person needs to collect variance of actual budget with desired budgeted

and accordingly, review the same.

Respond immediately, if required: It is the last step process of budgetary control in

which the managers need to act immediately if any problems occur and accordingly make

changes that will help them in achieving desired targets.

Planning tools used by manager to control budget:

Forecasting tools: This tool is used in estimating cost which will be incurred in the

future business activities that will help them in getting better possible outcome. Forecasting helps

management to make effective planning and policies which may be useful in getting profitable

outcomes. The manager needs to first understand trends and happenings occurred in market due

to forecasting such as price, demand and labour and accordingly implement corrective actions in

order to achieve desired goals and objectives.

Scenario analysis tools: As there are many uncertainties and complexities that occur in

the business environment which affect the performance of an organisation and in order to face

such complex situation manager need to first identify those uncertainties and evaluate its impact

10

centralising the control system.

Process of Budgetary control:

Discuss with managers to formulate effective strategy: In this step, the managers has

discuss with their staff members of company relating to expenses incurred in future business

activities and accordingly formulate effective strategy.

Record the actual performance: The manager first needs to analyse previous data and

information of different areas of department of company and accordingly, implement strategy

which brings them positive results.

Comparison of actual with the planned: At this stage, company needs to analyse and

compare actual performance with the desired performance in order to find out deviations, if any,

which restrict them in performing in an effective and efficient manner. It helps them in

determining various variable and standard cost of sales.

Determine difference or other variance: In this step, company has to select one qualified

person that effectively review the differences or deviations arise between actual and desired

performance. Appointed person needs to collect variance of actual budget with desired budgeted

and accordingly, review the same.

Respond immediately, if required: It is the last step process of budgetary control in

which the managers need to act immediately if any problems occur and accordingly make

changes that will help them in achieving desired targets.

Planning tools used by manager to control budget:

Forecasting tools: This tool is used in estimating cost which will be incurred in the

future business activities that will help them in getting better possible outcome. Forecasting helps

management to make effective planning and policies which may be useful in getting profitable

outcomes. The manager needs to first understand trends and happenings occurred in market due

to forecasting such as price, demand and labour and accordingly implement corrective actions in

order to achieve desired goals and objectives.

Scenario analysis tools: As there are many uncertainties and complexities that occur in

the business environment which affect the performance of an organisation and in order to face

such complex situation manager need to first identify those uncertainties and evaluate its impact

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.