Management Accounting: Software Selection Case Study Analysis

VerifiedAdded on 2023/04/22

|7

|580

|201

Case Study

AI Summary

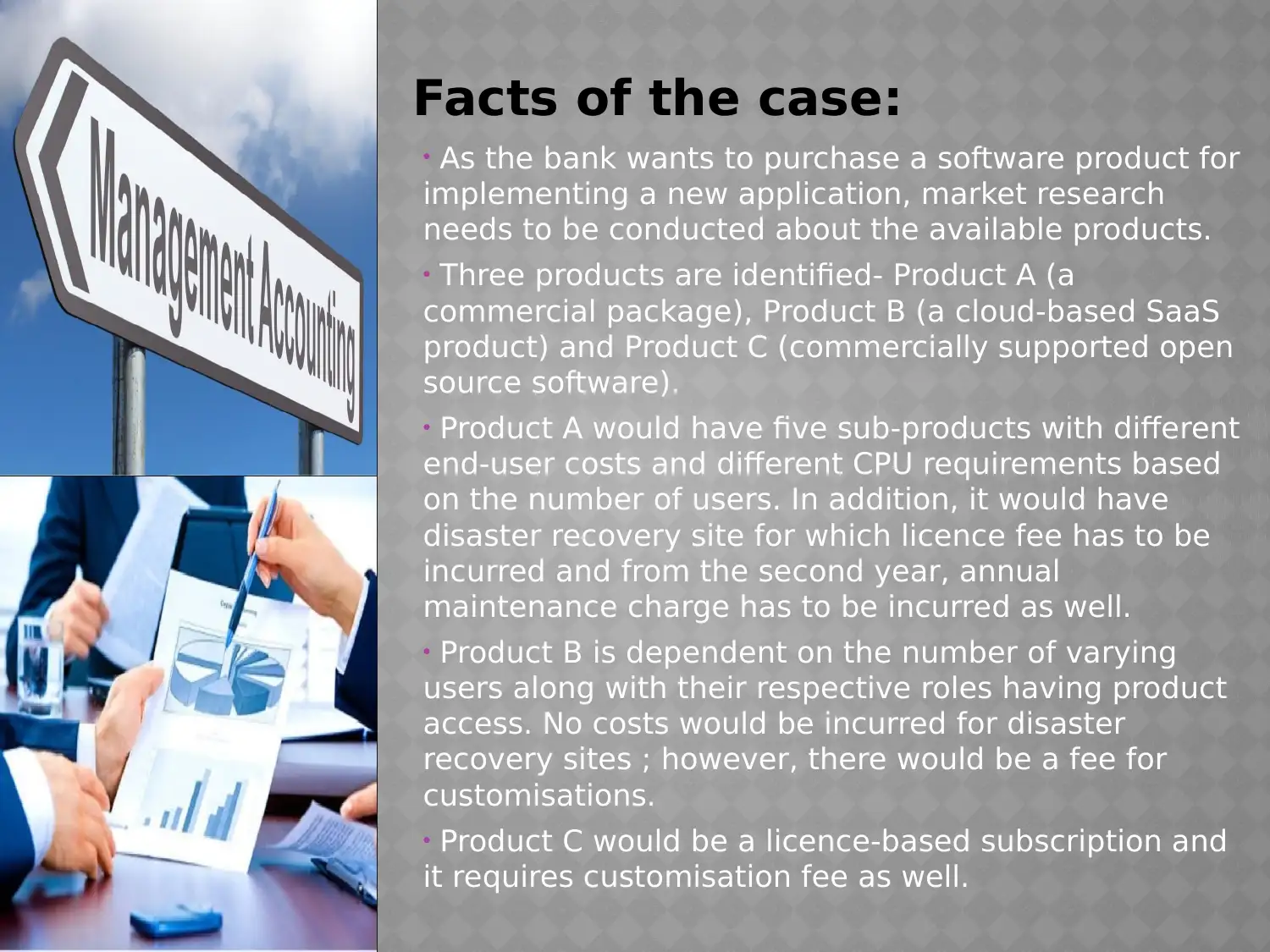

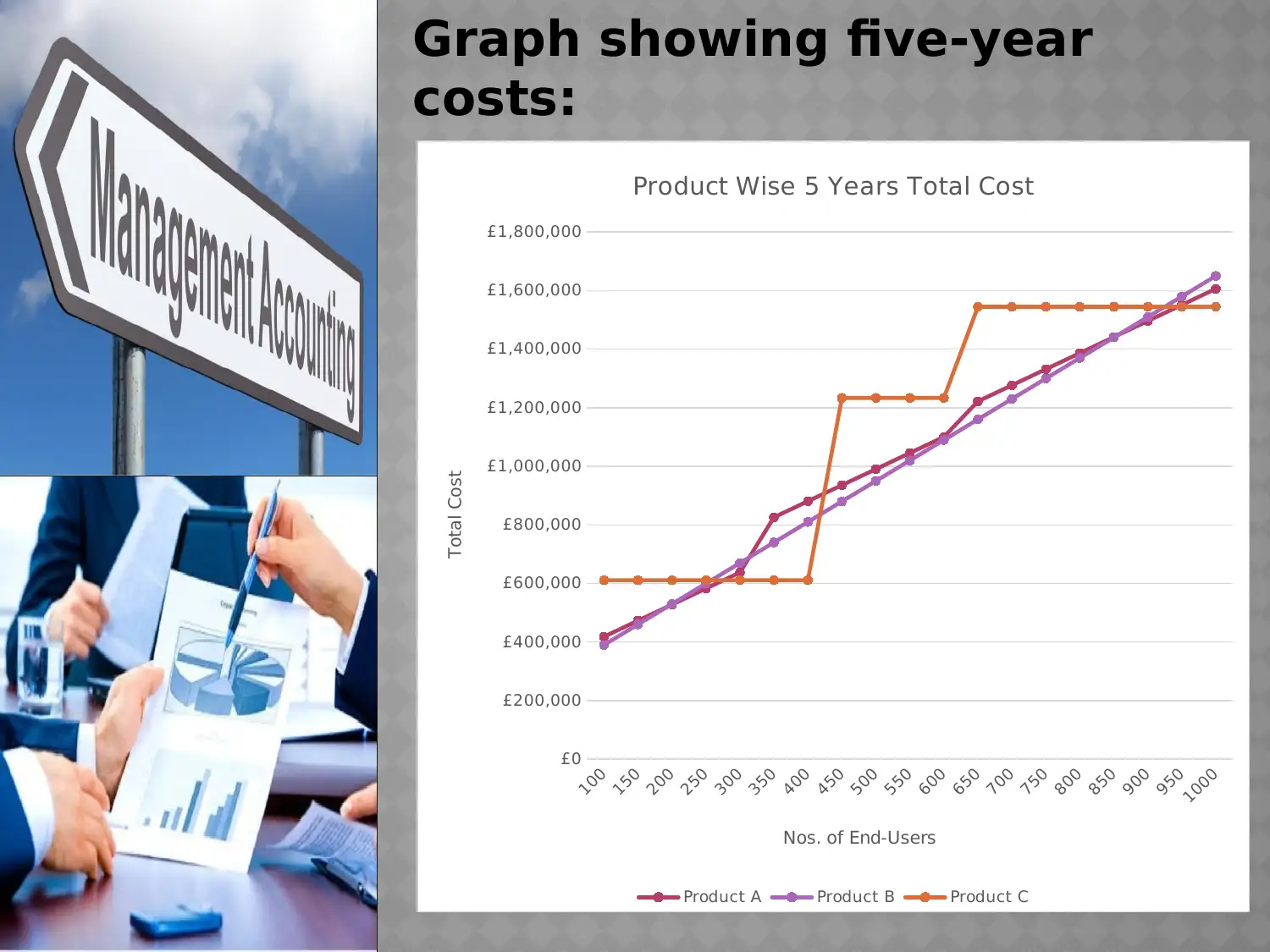

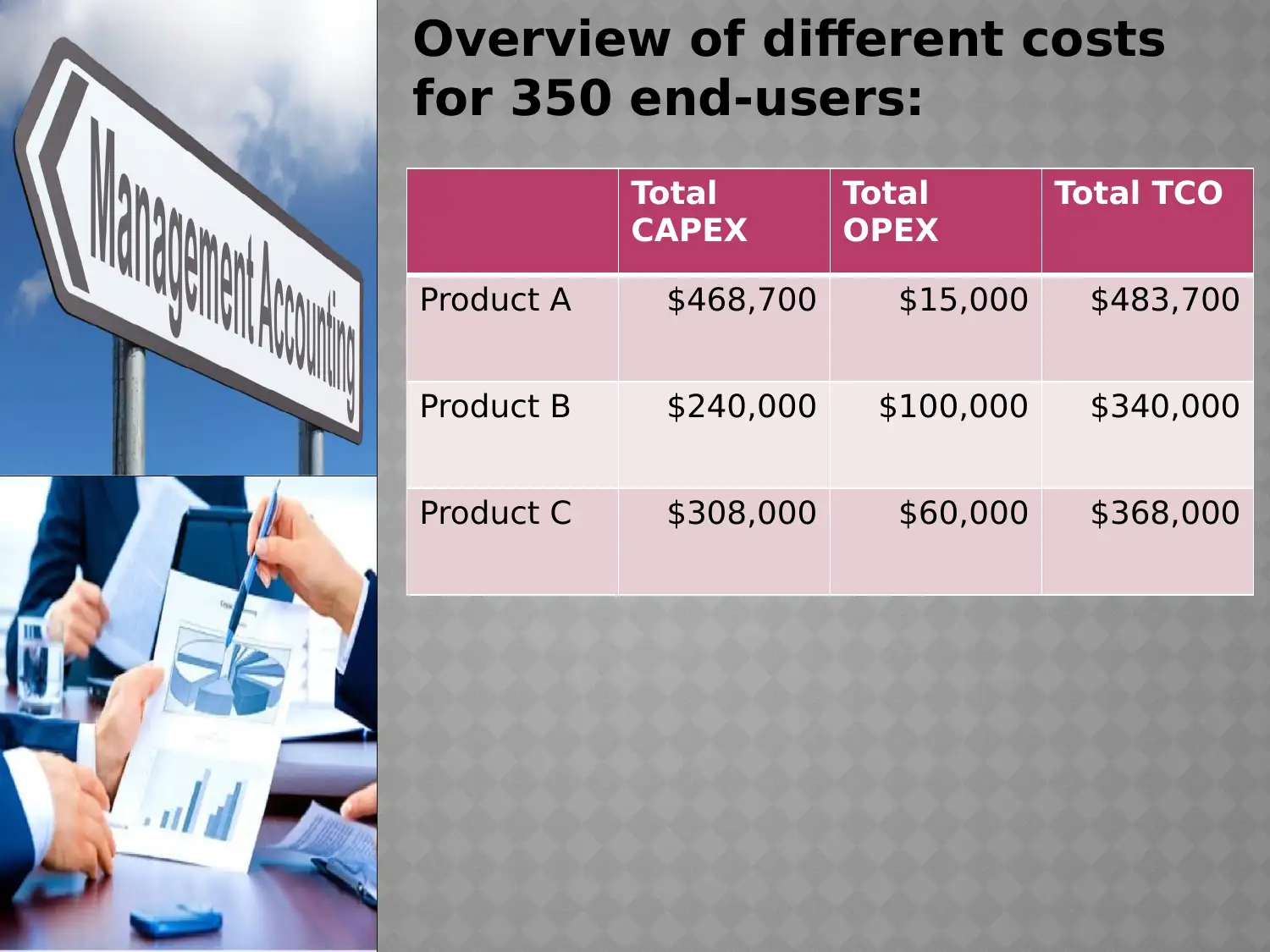

This case study examines a bank's decision-making process in selecting a software product for a new application, considering three options: Product A (a commercial package), Product B (a cloud-based SaaS product), and Product C (commercially supported open-source software). The analysis involves a comparison of total cost of ownership (TCO), capital expenditure (CAPEX), and operational expenditure (OPEX) for each product over a five-year period, considering factors like end-user costs, CPU requirements, disaster recovery, and customization fees. The study finds that Product B is the most cost-effective option based on TCO, despite having higher OPEX than Product A. Additional cost factors, including security, scalability, telecommunication costs, functionality, and ease of use, are also discussed. The case study concludes that Product B is the preferred choice due to its overall cost advantages. Desklib provides access to similar solved assignments and past papers for students.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.