Management Accounting Report: Analysis of Sollatek Company

VerifiedAdded on 2020/02/05

|18

|5489

|45

Report

AI Summary

This report examines management accounting principles through a case study of Sollatek, a company involved in manufacturing products for electrical and electronic equipment. The report explores various aspects of management accounting, including its definition, different types of systems like throughput and lean accounting, and traditional methods. It details the advantages of management accounting systems, such as cost reduction and improved decision-making. The report covers the preparation of performance reports, job costing reports, variable analysis reports, and budgets. It also analyzes the integration of management accounting systems and reports, along with the preparation of income statements using marginal and absorption costing. The report further discusses planning tools for budgetary control, the adoption of management accounting systems to address financial problems, and the role of management accounting in achieving sustainable success. Overall, the report provides a comprehensive overview of management accounting techniques and their application within a business context.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management accounting and essential requirement of different types of management

accounting systems......................................................................................................................3

M1 Advantages of management accounting systems and their application................................4

P2 Methods that are used for management accounting reporting...............................................5

D1 Evaluation of how management accounting systems and reports are integrated..................6

TASK 2............................................................................................................................................7

P3 Preparation of income statement using marginal and absorption costing..............................7

M2 Application of various management accounting techniques..............................................10

D2 Accurate interpretation of the data by production of the reports........................................11

TASK 3..........................................................................................................................................11

P4 Planning tools that can be used for Budgetary Control. .....................................................11

M3 Different types of planning tools and their application in the preparation of budgets.......13

P5 Adoption of management accounting systems to respond to financial problems................13

M4 Role of management accounting in sustainable success....................................................14

D3 Solving of financial problems by using planning tools.......................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management accounting and essential requirement of different types of management

accounting systems......................................................................................................................3

M1 Advantages of management accounting systems and their application................................4

P2 Methods that are used for management accounting reporting...............................................5

D1 Evaluation of how management accounting systems and reports are integrated..................6

TASK 2............................................................................................................................................7

P3 Preparation of income statement using marginal and absorption costing..............................7

M2 Application of various management accounting techniques..............................................10

D2 Accurate interpretation of the data by production of the reports........................................11

TASK 3..........................................................................................................................................11

P4 Planning tools that can be used for Budgetary Control. .....................................................11

M3 Different types of planning tools and their application in the preparation of budgets.......13

P5 Adoption of management accounting systems to respond to financial problems................13

M4 Role of management accounting in sustainable success....................................................14

D3 Solving of financial problems by using planning tools.......................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting is the process by which organisation goals and objectives that

are decided can be achieved (Ajibolade, Arowomole and Ojikutu, 2010). For this purpose it will

include various processes to be undertaken which will include identification, measurement,

analysation of the relevant information, and than on that basis interpretation will be carried out

and all the findings will be required to be communicated so that the goals can be achieved. The

main purpose of management accounting is to provide the required information to the managers

which will be helpful for them in their decision making process. This form of accounting focuses

on helping the internal managers of the company and in this no information is provided to the

outside parties. In this assignment various aspects in relation to management accounting such as

meaning of management accounting, types of management accounting systems, different

budgetary control techniques and costing methods will be discussed with reference Sollatek. This

company was founded in 1983 and is involved in manufacturing of products which are helpful in

protecting electrical and electronic equipments.

TASK 1

P1 Management accounting and essential requirement of different types of management

accounting systems.

In a business there are various decisions that are required to be taken for the attainment of

the objectives and goals that are set by the company (Albelda, 2011). In order to achieve this

sollatek will be required to prepare various reports that will help the management in acquiring all

the financial and statistical information on the timely basis and in accurate manner which will

help them in performing various decisions. This process of preparation of reports is known as

management accounting. These reports are made just for internal use and will not be provided to

anyone for external use. They will show various amounts in relation to cash available,

outstanding debts, sales revenue, variance analysis and many other figures. The main areas in

which management accounting can be used are risk management, performance management and

strategic management. There are different types of management accounting systems that can be

used by Sollatek which are described below :

1. Throughput Accounting : - In the production process of sollatek there are various

constraints that will be present and will be required to be identified. In the process of

Management accounting is the process by which organisation goals and objectives that

are decided can be achieved (Ajibolade, Arowomole and Ojikutu, 2010). For this purpose it will

include various processes to be undertaken which will include identification, measurement,

analysation of the relevant information, and than on that basis interpretation will be carried out

and all the findings will be required to be communicated so that the goals can be achieved. The

main purpose of management accounting is to provide the required information to the managers

which will be helpful for them in their decision making process. This form of accounting focuses

on helping the internal managers of the company and in this no information is provided to the

outside parties. In this assignment various aspects in relation to management accounting such as

meaning of management accounting, types of management accounting systems, different

budgetary control techniques and costing methods will be discussed with reference Sollatek. This

company was founded in 1983 and is involved in manufacturing of products which are helpful in

protecting electrical and electronic equipments.

TASK 1

P1 Management accounting and essential requirement of different types of management

accounting systems.

In a business there are various decisions that are required to be taken for the attainment of

the objectives and goals that are set by the company (Albelda, 2011). In order to achieve this

sollatek will be required to prepare various reports that will help the management in acquiring all

the financial and statistical information on the timely basis and in accurate manner which will

help them in performing various decisions. This process of preparation of reports is known as

management accounting. These reports are made just for internal use and will not be provided to

anyone for external use. They will show various amounts in relation to cash available,

outstanding debts, sales revenue, variance analysis and many other figures. The main areas in

which management accounting can be used are risk management, performance management and

strategic management. There are different types of management accounting systems that can be

used by Sollatek which are described below :

1. Throughput Accounting : - In the production process of sollatek there are various

constraints that will be present and will be required to be identified. In the process of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

throughput accounting focus will be given on identification of such constraints only. The

constraints can be various such as insufficiency of labour , material or any other facility.

These constraints are reduced in this system and this is achieved by increasing the

volume of production by which the per unit cost of the product will get reduced.

2. Lean accounting : - In case of lean accounting instead of giving importance to cost the

main focus is kept on formulation of different strategies that will be helpful in reduction

of cost (Arroyo, 2012). The objective of cost reduction will be achieved by reducing the

level of wastage that takes place in the production process carried on by sollatek. There

are various such irrelevant cost that can be eliminated from the production process and

for that purpose information will be required that will be available with the help of this

system. The information will be provided by the accountants on the immediate effect.

3. Traditional management accounting Systems : - the main focus of this system is on

tracking of the cost and that can be achieved by the use of various methods that will

include methods such as job order costing or process costing. With the help of these

methods the manner in which various cost are required to be allocated will be

determined. Job costing will be used in the case where individual allocation is possible

whereas process costing will be required where there are many processes involved in

production of the product.

4. Transfer Pricing : - in the system of transfer pricing cost of the product will be

calculated on the basis of the movement of the goods that takes place during the

production from the different departments included in production system (Bodie, 2013).

Variable cost and opportunity cost are the two main cost that are involved in the system

of transfer pricing. There will be addition at each stage and so the cost will also increase

in small portions.

A part from these there are various other management accounting systems which are available

and can be used. They include cost accounting systems, job order costing, inventory management

system and price optimisation systems.

Cost accounting method – It is the process of accounting in which recording of various

operations are done according to their actual cost incurred. It is a continuous process in which

recording, classification, analysing and summarising of various entries are made which is utilised

to manage the various activities of the given entity.

constraints can be various such as insufficiency of labour , material or any other facility.

These constraints are reduced in this system and this is achieved by increasing the

volume of production by which the per unit cost of the product will get reduced.

2. Lean accounting : - In case of lean accounting instead of giving importance to cost the

main focus is kept on formulation of different strategies that will be helpful in reduction

of cost (Arroyo, 2012). The objective of cost reduction will be achieved by reducing the

level of wastage that takes place in the production process carried on by sollatek. There

are various such irrelevant cost that can be eliminated from the production process and

for that purpose information will be required that will be available with the help of this

system. The information will be provided by the accountants on the immediate effect.

3. Traditional management accounting Systems : - the main focus of this system is on

tracking of the cost and that can be achieved by the use of various methods that will

include methods such as job order costing or process costing. With the help of these

methods the manner in which various cost are required to be allocated will be

determined. Job costing will be used in the case where individual allocation is possible

whereas process costing will be required where there are many processes involved in

production of the product.

4. Transfer Pricing : - in the system of transfer pricing cost of the product will be

calculated on the basis of the movement of the goods that takes place during the

production from the different departments included in production system (Bodie, 2013).

Variable cost and opportunity cost are the two main cost that are involved in the system

of transfer pricing. There will be addition at each stage and so the cost will also increase

in small portions.

A part from these there are various other management accounting systems which are available

and can be used. They include cost accounting systems, job order costing, inventory management

system and price optimisation systems.

Cost accounting method – It is the process of accounting in which recording of various

operations are done according to their actual cost incurred. It is a continuous process in which

recording, classification, analysing and summarising of various entries are made which is utilised

to manage the various activities of the given entity.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job costing – It is a different method in which recording of different entries are done according

to the cost of different jobs as distinct job incurs different cost and therefore through this cost of

each job can be identified.

Inventory management system – It is a method through which the total stock is maintained so

that both the situations of excess and deficit can be avoided as this has major impact on the total

productivity.

Prize optimization – Through this method of accounting management reach to the best price

which it can offer in the market as maximum care has to be given before fixing the price of the

commodity so that customers can accept the same.

M1 Advantages of management accounting systems and their application.

There are various benefits that company receives form management accounting systems.

Some of them are :

Reduction in expenses : With the help of management accounting systems Sollatek will be able

to know about those activities that are relevant and by this the expenditure that is incurred in

relation to irrelevant activities can be eliminated.

Making Decisions : The information that will be available with the use of various management

accounting systems will be helpful for managers to make correct decisions and by this if any

loopholes are present than they will be identified and removed.

P2 Methods that are used for management accounting reporting.

A part from normal financial statements there are prepared by every organisation there

are various other reports that are also required to be made and that includes the following reports

which are described below :

Performance reports : It is important for Sollatek to measure its performance and this

can be achieved only with the help of performance reports (Chenhall, 2012). For the

preparation of report it will be required that the actual and budgeted figures that are

available in the budget should be compared and on that basis variances will be required to

be identified. These variances will be considered by the management in the preparation of

new budgets. The performance can be evaluated with the help of performance report and

any limitation that are found in the report will have to be removed in order to improve the

overall performance of the company.

to the cost of different jobs as distinct job incurs different cost and therefore through this cost of

each job can be identified.

Inventory management system – It is a method through which the total stock is maintained so

that both the situations of excess and deficit can be avoided as this has major impact on the total

productivity.

Prize optimization – Through this method of accounting management reach to the best price

which it can offer in the market as maximum care has to be given before fixing the price of the

commodity so that customers can accept the same.

M1 Advantages of management accounting systems and their application.

There are various benefits that company receives form management accounting systems.

Some of them are :

Reduction in expenses : With the help of management accounting systems Sollatek will be able

to know about those activities that are relevant and by this the expenditure that is incurred in

relation to irrelevant activities can be eliminated.

Making Decisions : The information that will be available with the use of various management

accounting systems will be helpful for managers to make correct decisions and by this if any

loopholes are present than they will be identified and removed.

P2 Methods that are used for management accounting reporting.

A part from normal financial statements there are prepared by every organisation there

are various other reports that are also required to be made and that includes the following reports

which are described below :

Performance reports : It is important for Sollatek to measure its performance and this

can be achieved only with the help of performance reports (Chenhall, 2012). For the

preparation of report it will be required that the actual and budgeted figures that are

available in the budget should be compared and on that basis variances will be required to

be identified. These variances will be considered by the management in the preparation of

new budgets. The performance can be evaluated with the help of performance report and

any limitation that are found in the report will have to be removed in order to improve the

overall performance of the company.

Job Costing Reports : there are various costs that are involved in production of a

product such as production cost, labour cost, overhead cost and many other costs. For the

purpose of determination of the cost of the final product it will be required that all these

costs should be taken into consideration (France, 2010). By following this process the

total cost that have been incurred in the whole production process will be determined and

than with the help of it the cost of each product will be ascertained and that that will be

possible by dividing this total cost with the number of total products that have been

manufactured in the company. Than this report will be prepared with the help of the

information that has been collected and it will be beneficial for sollatek as with the help

of it managers will be able to compare the cost and selling price and on that basis they

will be able to control the profits of the company.

Variable Analysis Reports : In the production of a product there are various costs that

are incurred and one such cost is variable cost. It is that cost which is never fixed and it

depends on the number of units produced which mean it changes with change in single

unit in production. The profits of the company will be affected to a great extent due to

this cost and due to this reason it is necessary that this report should be prepared.

Management will study the report and with the help of it they will be able to improve the

profit levels of Sollatek.

Budgets : Budgets are most important in the management accounting as with the help of

it variances can be determined by comparing the actual figures with that of the budgeted

figures (Hiebl, 2014). For the preparation of the budget it will be required by the

company to take into consideration the past details or the previous budgets. Together with

the past budgets they are also required to use the variances that have been calculated and

the projections that have been made in relation to the future should also be considered.

All the targets are mentioned in the budget which are required to be achieved by the

company and so in order to achieve the targets it will be needed that all the amounts

mentioned in the budget should taken care of while performing the activities in the

company.

Inventory control Reports : In the production process inventory plays the most

important role so it will be needed that all the aspects in relation to it should be taken care

of and mentioned in this report. If there is any wastage that has been noticed than it

product such as production cost, labour cost, overhead cost and many other costs. For the

purpose of determination of the cost of the final product it will be required that all these

costs should be taken into consideration (France, 2010). By following this process the

total cost that have been incurred in the whole production process will be determined and

than with the help of it the cost of each product will be ascertained and that that will be

possible by dividing this total cost with the number of total products that have been

manufactured in the company. Than this report will be prepared with the help of the

information that has been collected and it will be beneficial for sollatek as with the help

of it managers will be able to compare the cost and selling price and on that basis they

will be able to control the profits of the company.

Variable Analysis Reports : In the production of a product there are various costs that

are incurred and one such cost is variable cost. It is that cost which is never fixed and it

depends on the number of units produced which mean it changes with change in single

unit in production. The profits of the company will be affected to a great extent due to

this cost and due to this reason it is necessary that this report should be prepared.

Management will study the report and with the help of it they will be able to improve the

profit levels of Sollatek.

Budgets : Budgets are most important in the management accounting as with the help of

it variances can be determined by comparing the actual figures with that of the budgeted

figures (Hiebl, 2014). For the preparation of the budget it will be required by the

company to take into consideration the past details or the previous budgets. Together with

the past budgets they are also required to use the variances that have been calculated and

the projections that have been made in relation to the future should also be considered.

All the targets are mentioned in the budget which are required to be achieved by the

company and so in order to achieve the targets it will be needed that all the amounts

mentioned in the budget should taken care of while performing the activities in the

company.

Inventory control Reports : In the production process inventory plays the most

important role so it will be needed that all the aspects in relation to it should be taken care

of and mentioned in this report. If there is any wastage that has been noticed than it

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

should be taken into consideration and reason of it should be identified and measures

should be taken to remove them. Sollatek will determine the inventory level which is

required to be maintained in order to avoid the problem of shortage or excess stock due to

which no irrelevant cost will be incurred and the profits of the company will be

maximised.

D1 Evaluation of how management accounting systems and reports are integrated.

Management accounting systems and management accounting reports are integrated as

with the help of various systems Sollatek will be able to collect the information which will be

further analysed and than that information will be required to be included in the reports (Hülle,

Kaspar and Möller, 2011). Both these will be beneficial for the company as with the help of them

it will be possible to find out the shortcomings and than on their identification management will

be able to make correct decision and also measures can be taken to overcome those

shortcomings. By performing all this the overall performance of the company will be increased.

TASK 2

P3 Preparation of income statement using marginal and absorption costing.

Absorption Costing : By using absorption costing it will be possible to ascertain the cost

of the product. In this costing method the cost of the product will be calculated taking into

consideration all the costs that have been incurred in relation to that product. It is immaterial in

this form of costing that whether the cost that has been incurred is fixed cost or a variable cost as

both will be included in the cost (Kaplan and Atkinson, 2015). The total cost that will be

ascertained by this method will be divided among all the units that have been manufactured. The

major advantage of using absorption costing is that in this while valuing inventory an element of

fixed overhead is also included in it and also the cost is controlled by analysing the over or under

absorption of overheads.

Marginal costing : in the case of marginal costing the cost of the product will change

with the change in single unit of production. This will be due to the reason that in this variable

cost are taken into consideration (Zang, 2011). while calculation of the marginal cost of any

product the cost that are directly related to the product such as direct material, direct labour or

the variable cost associated with that product will be taken into consideration. In this method

firstly contribution will be determined by deducting variable cost from the selling price and than

should be taken to remove them. Sollatek will determine the inventory level which is

required to be maintained in order to avoid the problem of shortage or excess stock due to

which no irrelevant cost will be incurred and the profits of the company will be

maximised.

D1 Evaluation of how management accounting systems and reports are integrated.

Management accounting systems and management accounting reports are integrated as

with the help of various systems Sollatek will be able to collect the information which will be

further analysed and than that information will be required to be included in the reports (Hülle,

Kaspar and Möller, 2011). Both these will be beneficial for the company as with the help of them

it will be possible to find out the shortcomings and than on their identification management will

be able to make correct decision and also measures can be taken to overcome those

shortcomings. By performing all this the overall performance of the company will be increased.

TASK 2

P3 Preparation of income statement using marginal and absorption costing.

Absorption Costing : By using absorption costing it will be possible to ascertain the cost

of the product. In this costing method the cost of the product will be calculated taking into

consideration all the costs that have been incurred in relation to that product. It is immaterial in

this form of costing that whether the cost that has been incurred is fixed cost or a variable cost as

both will be included in the cost (Kaplan and Atkinson, 2015). The total cost that will be

ascertained by this method will be divided among all the units that have been manufactured. The

major advantage of using absorption costing is that in this while valuing inventory an element of

fixed overhead is also included in it and also the cost is controlled by analysing the over or under

absorption of overheads.

Marginal costing : in the case of marginal costing the cost of the product will change

with the change in single unit of production. This will be due to the reason that in this variable

cost are taken into consideration (Zang, 2011). while calculation of the marginal cost of any

product the cost that are directly related to the product such as direct material, direct labour or

the variable cost associated with that product will be taken into consideration. In this method

firstly contribution will be determined by deducting variable cost from the selling price and than

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

after this the fixed cost will be considered and deducted from the contribution in order to arrive

at the final profit that is earned by the company.

There are various differences that can be noticed between marginal and absorption costing and

some of them are specified in the below presented comparison table :

Basis Absorption costing Marginal costing

Meaning In this method the cost of

product is determined by

dividing the total amount of

cost to the various cost centres

(Kinney, Raiborn and

Poznanski, 2011).

It is a decision making

technique which will be used

by Sollatek as by this the total

cost that have been incurred in

the production of a product

will be determined.

Classification of overheads In this overheads are classified

as administration, production

and selling and distribution

overheads.

In this overheads are classified

in two categories that are fixed

and variable overheads.

Recognition of cost In this method fixed cost and

variable cost both will be

treated as product cost.

In this variable cost will be

treated as product cost and

fixed cost will be treated as

period cost.

Measurement of profitability In this as the fixed cost is

considered so the profitability

will be affected.

In order to measure the

profitability, profit volume

ratio is used.

Unit cost The factor that affect the cost

per unit in this case is the

variance in the opening and the

closing stock.

In this the variance between

the opening and closing stock

has no impact on the cost of

the product.

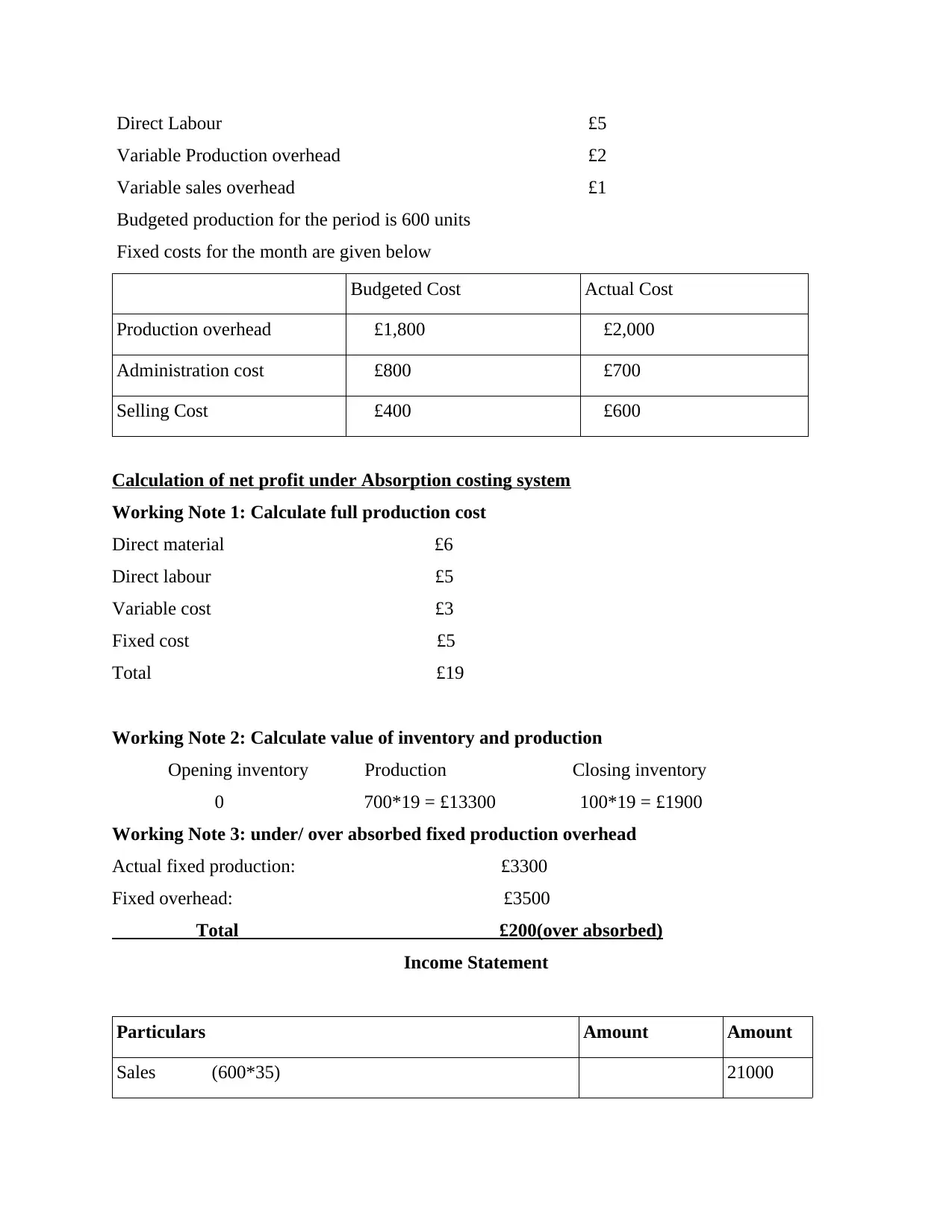

Selling price £35

Unit Costs

Direct materials £6

at the final profit that is earned by the company.

There are various differences that can be noticed between marginal and absorption costing and

some of them are specified in the below presented comparison table :

Basis Absorption costing Marginal costing

Meaning In this method the cost of

product is determined by

dividing the total amount of

cost to the various cost centres

(Kinney, Raiborn and

Poznanski, 2011).

It is a decision making

technique which will be used

by Sollatek as by this the total

cost that have been incurred in

the production of a product

will be determined.

Classification of overheads In this overheads are classified

as administration, production

and selling and distribution

overheads.

In this overheads are classified

in two categories that are fixed

and variable overheads.

Recognition of cost In this method fixed cost and

variable cost both will be

treated as product cost.

In this variable cost will be

treated as product cost and

fixed cost will be treated as

period cost.

Measurement of profitability In this as the fixed cost is

considered so the profitability

will be affected.

In order to measure the

profitability, profit volume

ratio is used.

Unit cost The factor that affect the cost

per unit in this case is the

variance in the opening and the

closing stock.

In this the variance between

the opening and closing stock

has no impact on the cost of

the product.

Selling price £35

Unit Costs

Direct materials £6

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed costs for the month are given below

Budgeted Cost Actual Cost

Production overhead £1,800 £2,000

Administration cost £800 £700

Selling Cost £400 £600

Calculation of net profit under Absorption costing system

Working Note 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £3

Fixed cost £5

Total £19

Working Note 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*19 = £1900

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £3300

Fixed overhead: £3500

Total £200(over absorbed)

Income Statement

Particulars Amount Amount

Sales (600*35) 21000

Variable Production overhead £2

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed costs for the month are given below

Budgeted Cost Actual Cost

Production overhead £1,800 £2,000

Administration cost £800 £700

Selling Cost £400 £600

Calculation of net profit under Absorption costing system

Working Note 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £3

Fixed cost £5

Total £19

Working Note 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*19 = £1900

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £3300

Fixed overhead: £3500

Total £200(over absorbed)

Income Statement

Particulars Amount Amount

Sales (600*35) 21000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

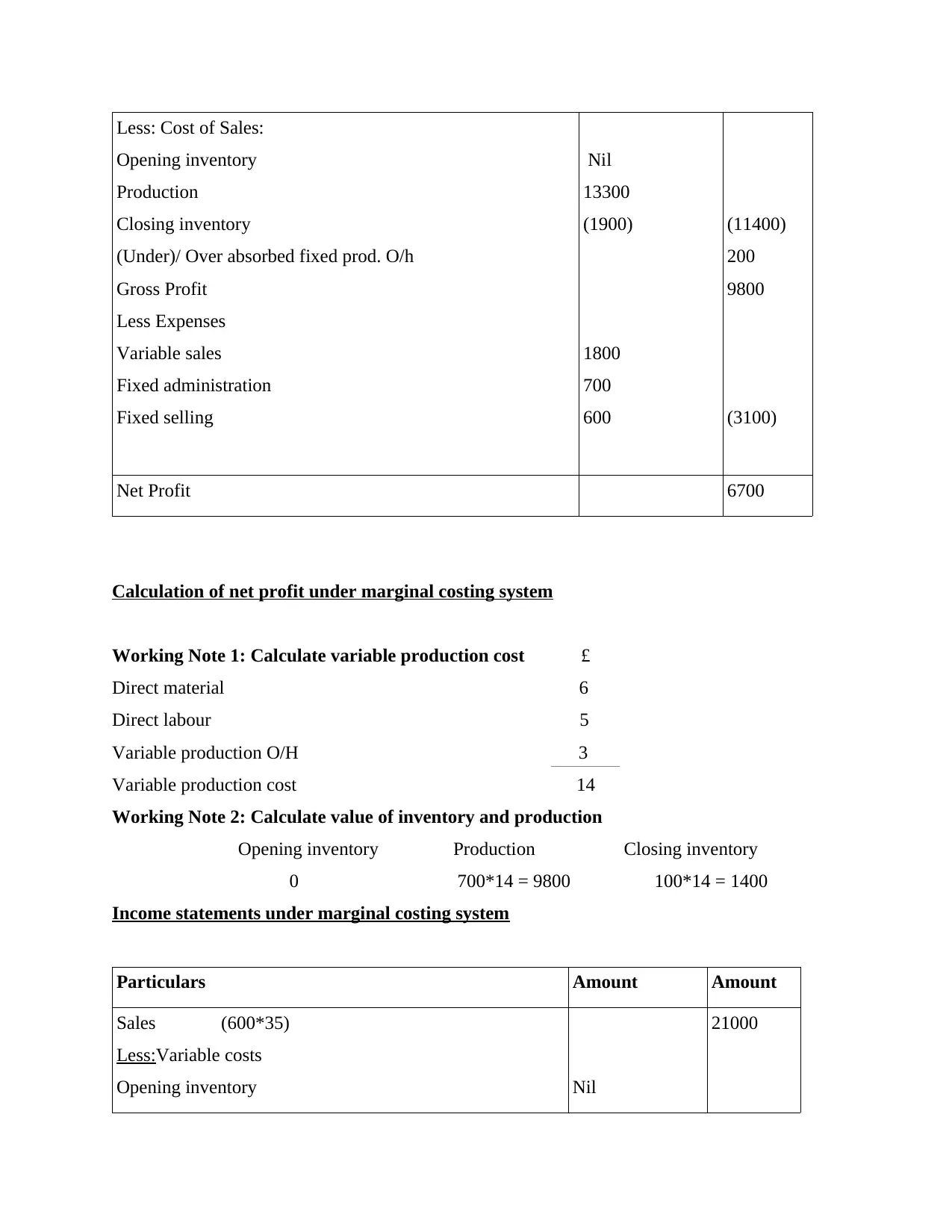

Less: Cost of Sales:

Opening inventory

Production

Closing inventory

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

Less Expenses

Variable sales

Fixed administration

Fixed selling

Nil

13300

(1900)

1800

700

600

(11400)

200

9800

(3100)

Net Profit 6700

Calculation of net profit under marginal costing system

Working Note 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/H 3

Variable production cost 14

Working Note 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Income statements under marginal costing system

Particulars Amount Amount

Sales (600*35)

Less:Variable costs

Opening inventory Nil

21000

Opening inventory

Production

Closing inventory

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

Less Expenses

Variable sales

Fixed administration

Fixed selling

Nil

13300

(1900)

1800

700

600

(11400)

200

9800

(3100)

Net Profit 6700

Calculation of net profit under marginal costing system

Working Note 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/H 3

Variable production cost 14

Working Note 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Income statements under marginal costing system

Particulars Amount Amount

Sales (600*35)

Less:Variable costs

Opening inventory Nil

21000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

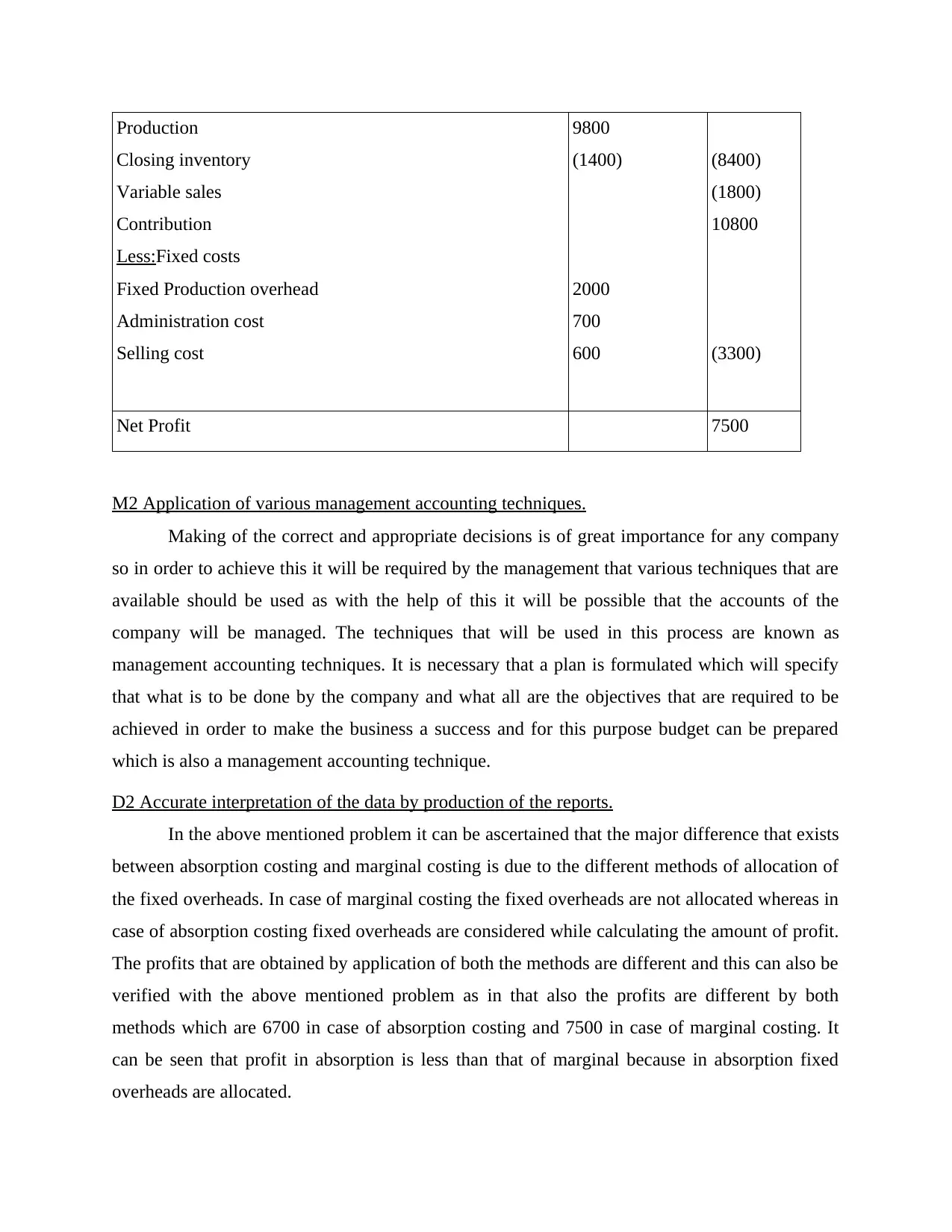

Production

Closing inventory

Variable sales

Contribution

Less:Fixed costs

Fixed Production overhead

Administration cost

Selling cost

9800

(1400)

2000

700

600

(8400)

(1800)

10800

(3300)

Net Profit 7500

M2 Application of various management accounting techniques.

Making of the correct and appropriate decisions is of great importance for any company

so in order to achieve this it will be required by the management that various techniques that are

available should be used as with the help of this it will be possible that the accounts of the

company will be managed. The techniques that will be used in this process are known as

management accounting techniques. It is necessary that a plan is formulated which will specify

that what is to be done by the company and what all are the objectives that are required to be

achieved in order to make the business a success and for this purpose budget can be prepared

which is also a management accounting technique.

D2 Accurate interpretation of the data by production of the reports.

In the above mentioned problem it can be ascertained that the major difference that exists

between absorption costing and marginal costing is due to the different methods of allocation of

the fixed overheads. In case of marginal costing the fixed overheads are not allocated whereas in

case of absorption costing fixed overheads are considered while calculating the amount of profit.

The profits that are obtained by application of both the methods are different and this can also be

verified with the above mentioned problem as in that also the profits are different by both

methods which are 6700 in case of absorption costing and 7500 in case of marginal costing. It

can be seen that profit in absorption is less than that of marginal because in absorption fixed

overheads are allocated.

Closing inventory

Variable sales

Contribution

Less:Fixed costs

Fixed Production overhead

Administration cost

Selling cost

9800

(1400)

2000

700

600

(8400)

(1800)

10800

(3300)

Net Profit 7500

M2 Application of various management accounting techniques.

Making of the correct and appropriate decisions is of great importance for any company

so in order to achieve this it will be required by the management that various techniques that are

available should be used as with the help of this it will be possible that the accounts of the

company will be managed. The techniques that will be used in this process are known as

management accounting techniques. It is necessary that a plan is formulated which will specify

that what is to be done by the company and what all are the objectives that are required to be

achieved in order to make the business a success and for this purpose budget can be prepared

which is also a management accounting technique.

D2 Accurate interpretation of the data by production of the reports.

In the above mentioned problem it can be ascertained that the major difference that exists

between absorption costing and marginal costing is due to the different methods of allocation of

the fixed overheads. In case of marginal costing the fixed overheads are not allocated whereas in

case of absorption costing fixed overheads are considered while calculating the amount of profit.

The profits that are obtained by application of both the methods are different and this can also be

verified with the above mentioned problem as in that also the profits are different by both

methods which are 6700 in case of absorption costing and 7500 in case of marginal costing. It

can be seen that profit in absorption is less than that of marginal because in absorption fixed

overheads are allocated.

TASK 3

P4 Planning tools that can be used for Budgetary Control.

The budget is considered as one of the major tools for the company as every company

plans for various operations according to the budget requirements and for this each and every

element of budget is taken into considerations and by the help of budget various operational,

managerial and technical aspects can be analysed for the effective development of products and

services (Macintosh and Quattrone, 2010). Budgets are the long term objectives that can be

evaluated at all the levels of operations that will help the organization to grow and develop on

the levels of successful growth and development.

Various objectives of Budget are : -

Budget is prepared for long term purpose and it caters to all the requirements that are

being implemented at the level of development.

Budget is prepared to check actual and necessary performance which are being analysed

so that if there is any disequilibrium between any of them then it can be over-crafted.

Advantages of Budgetary control are : -

It provides all the strategic policies with future considerations.

Employees development process takes place.

It helps in attaining the targets of the organization at the best suitable level.

Disadvantages of Budgetary control are : -

Provides economic pressure to all the employees of the organization.

It tends to create a managerial conflict among the employees of the organization.

Managers are made to form all the budgeted operations that include lot or high cost and

in making these types of operations an organization can suffer loss.

Different types of budgets are : -

Master Budget is the set of budgeted tools which helps any company to plan out operational

work in accordance with connected elements like sales, production cost, purchase incomes, etc.

and it includes all the practical aspects of making a budget that enables them to analyse all the

managerial and economical development (Quinn, 2011). The main advantage of master budget is

that while all the elements are included but they are coordinated in a proper way that enables the

development of managers in practical aspect. Disadvantage is that it always takes all the cost

related operations required for managerial development, not for individual development.

P4 Planning tools that can be used for Budgetary Control.

The budget is considered as one of the major tools for the company as every company

plans for various operations according to the budget requirements and for this each and every

element of budget is taken into considerations and by the help of budget various operational,

managerial and technical aspects can be analysed for the effective development of products and

services (Macintosh and Quattrone, 2010). Budgets are the long term objectives that can be

evaluated at all the levels of operations that will help the organization to grow and develop on

the levels of successful growth and development.

Various objectives of Budget are : -

Budget is prepared for long term purpose and it caters to all the requirements that are

being implemented at the level of development.

Budget is prepared to check actual and necessary performance which are being analysed

so that if there is any disequilibrium between any of them then it can be over-crafted.

Advantages of Budgetary control are : -

It provides all the strategic policies with future considerations.

Employees development process takes place.

It helps in attaining the targets of the organization at the best suitable level.

Disadvantages of Budgetary control are : -

Provides economic pressure to all the employees of the organization.

It tends to create a managerial conflict among the employees of the organization.

Managers are made to form all the budgeted operations that include lot or high cost and

in making these types of operations an organization can suffer loss.

Different types of budgets are : -

Master Budget is the set of budgeted tools which helps any company to plan out operational

work in accordance with connected elements like sales, production cost, purchase incomes, etc.

and it includes all the practical aspects of making a budget that enables them to analyse all the

managerial and economical development (Quinn, 2011). The main advantage of master budget is

that while all the elements are included but they are coordinated in a proper way that enables the

development of managers in practical aspect. Disadvantage is that it always takes all the cost

related operations required for managerial development, not for individual development.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.