University Finance Module: Management Accounting Assignment Analysis

VerifiedAdded on 2019/11/26

|7

|930

|313

Homework Assignment

AI Summary

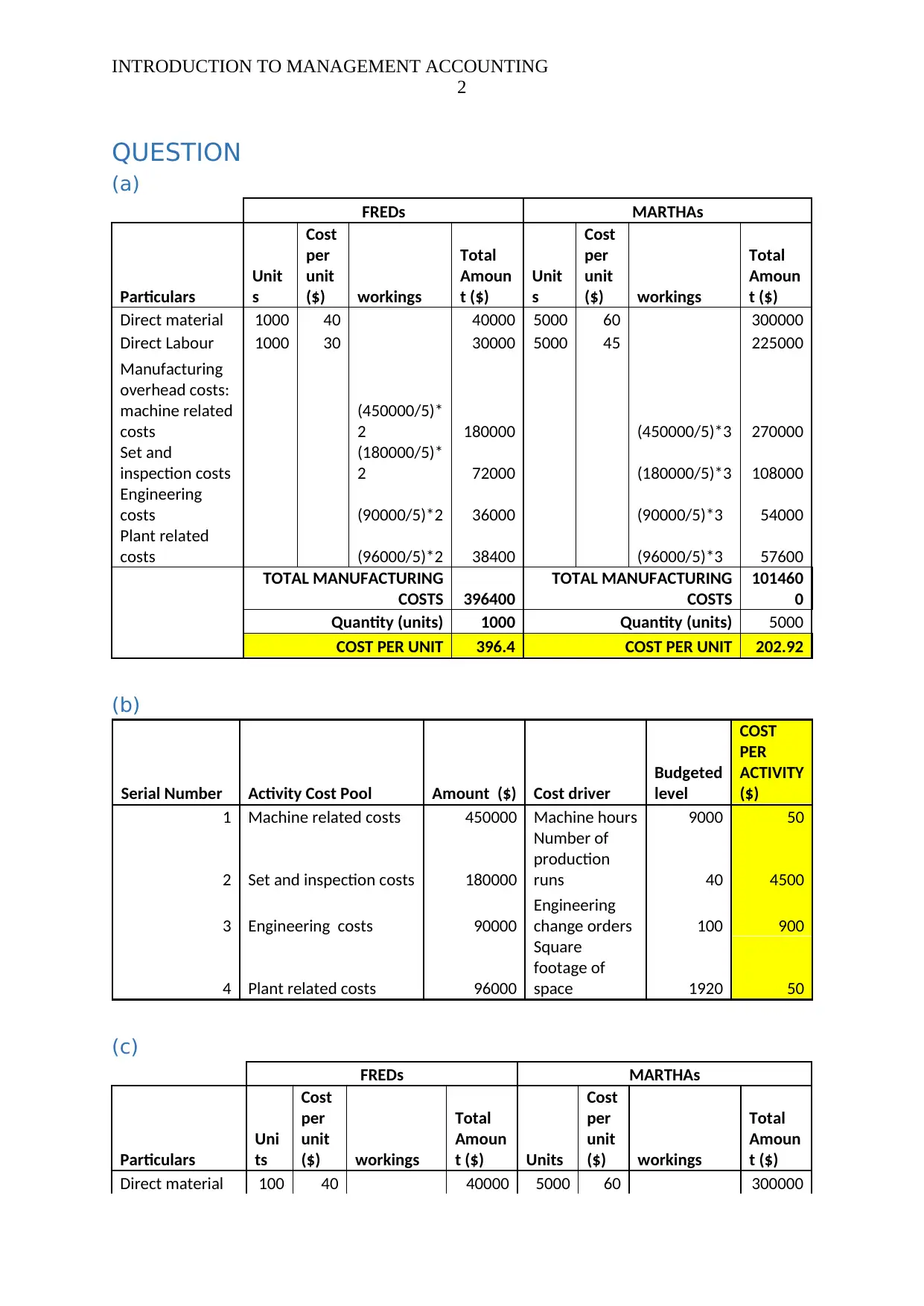

This assignment provides a comprehensive analysis of management accounting principles, specifically focusing on costing systems. The solution begins with a detailed calculation of manufacturing costs using traditional costing methods, comparing costs for two different production scenarios (FREDs and MARTHAs). It explores the calculation of direct materials, direct labor, and various manufacturing overhead costs. The assignment then delves into activity-based costing (ABC), outlining the cost drivers and budgeted levels for different activities. The solution includes a comparative analysis of the two costing systems, highlighting the differences in cost allocation and the impact on cost per unit. Furthermore, it discusses the advantages and disadvantages of both traditional and ABC costing methods, emphasizing the accuracy and decision-making implications of each approach. Finally, the solution provides a discussion of the benefits and drawbacks of using ABC costing systems, providing a well-rounded understanding of the topic.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.