Management Accounting Assignment - Finance Module Analysis

VerifiedAdded on 2020/03/28

|16

|1601

|93

Homework Assignment

AI Summary

This document presents a comprehensive solution to a management accounting assignment, addressing key concepts such as process costing, equivalent units, joint production costs, and variance analysis. The assignment explores the application of these concepts through several questions, including a comparison of cost management techniques in the context of the Great Pyramid of Giza and a detailed analysis of cost allocation and profit calculations. The solution includes calculations for equivalent units, cost per unit, and variance analysis, as well as discussions on budgeting and political factors influencing financial planning. The document also covers the impact of selling prices and the importance of variance analysis in business management.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGEMENT ACCOUNTING

Table of Contents

Answer to Question No 1................................................................................................................3

Requirement A:............................................................................................................................3

Requirement B:............................................................................................................................4

Answer to Question No 2................................................................................................................5

Answer to Question No 3................................................................................................................7

Requirement a:.............................................................................................................................7

Requirement b:.............................................................................................................................7

Answer to Question 4:.....................................................................................................................8

Requirement a:.............................................................................................................................8

Requirement b:...........................................................................................................................10

Answer to Question No 5..............................................................................................................12

Requirement A:..........................................................................................................................12

Requirement B:..........................................................................................................................13

Reference List................................................................................................................................15

MANAGEMENT ACCOUNTING

Table of Contents

Answer to Question No 1................................................................................................................3

Requirement A:............................................................................................................................3

Requirement B:............................................................................................................................4

Answer to Question No 2................................................................................................................5

Answer to Question No 3................................................................................................................7

Requirement a:.............................................................................................................................7

Requirement b:.............................................................................................................................7

Answer to Question 4:.....................................................................................................................8

Requirement a:.............................................................................................................................8

Requirement b:...........................................................................................................................10

Answer to Question No 5..............................................................................................................12

Requirement A:..........................................................................................................................12

Requirement B:..........................................................................................................................13

Reference List................................................................................................................................15

2

MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGEMENT ACCOUNTING

Answer to Question No 1

Requirement A:

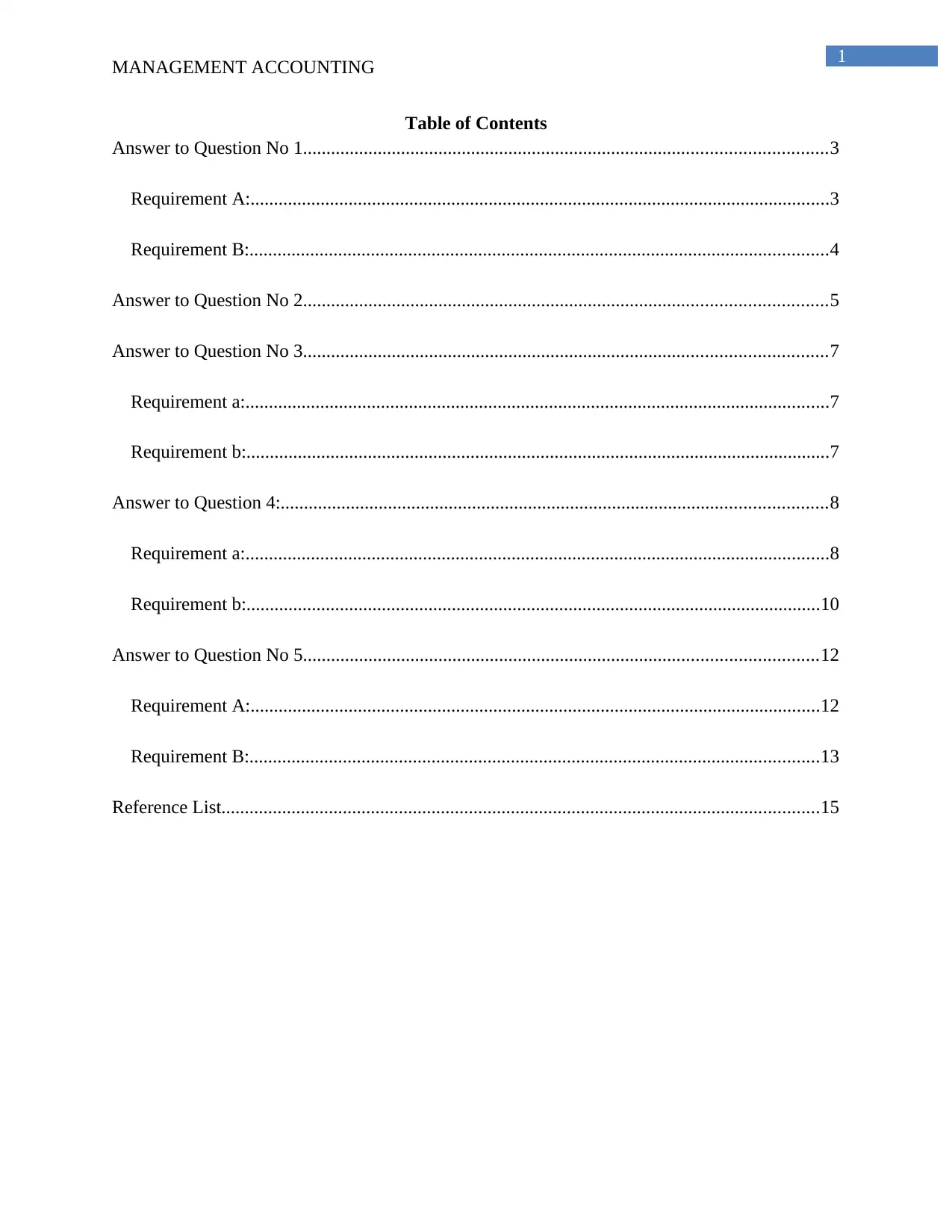

DR. CR.

Date Particulars Amount Date Particulars Amount

To, Balance b/d. 24855 31/8/14 By, Work-in-Process A/c. 6010

To, Accounts Payable A/c. 6155 By, Balance c/d 25000

31010 31010

DR. CR.

Date Particulars Amount Date Particulars Amount

1/8/X4 To, Balance b/d 8790 31/8/X4 By, Cost of Goods Sold A/c. 30000

31/8/X4 To, Work-in-Process A/c. 30110 By,Balance c/d 8900

38900 38900

DR. CR.

Date Particulars Amount Date Particulars Amount

31/8/X4 To, Finished Goods A/c. 30000 31/8/X4 By, Profit & Loss A/c. 32800

To, Manufacturing

Overhead A/c. 2800

32800 32800

Direct Material Account

Finished Goods

Cost of Goods Sold

MANAGEMENT ACCOUNTING

Answer to Question No 1

Requirement A:

DR. CR.

Date Particulars Amount Date Particulars Amount

To, Balance b/d. 24855 31/8/14 By, Work-in-Process A/c. 6010

To, Accounts Payable A/c. 6155 By, Balance c/d 25000

31010 31010

DR. CR.

Date Particulars Amount Date Particulars Amount

1/8/X4 To, Balance b/d 8790 31/8/X4 By, Cost of Goods Sold A/c. 30000

31/8/X4 To, Work-in-Process A/c. 30110 By,Balance c/d 8900

38900 38900

DR. CR.

Date Particulars Amount Date Particulars Amount

31/8/X4 To, Finished Goods A/c. 30000 31/8/X4 By, Profit & Loss A/c. 32800

To, Manufacturing

Overhead A/c. 2800

32800 32800

Direct Material Account

Finished Goods

Cost of Goods Sold

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGEMENT ACCOUNTING

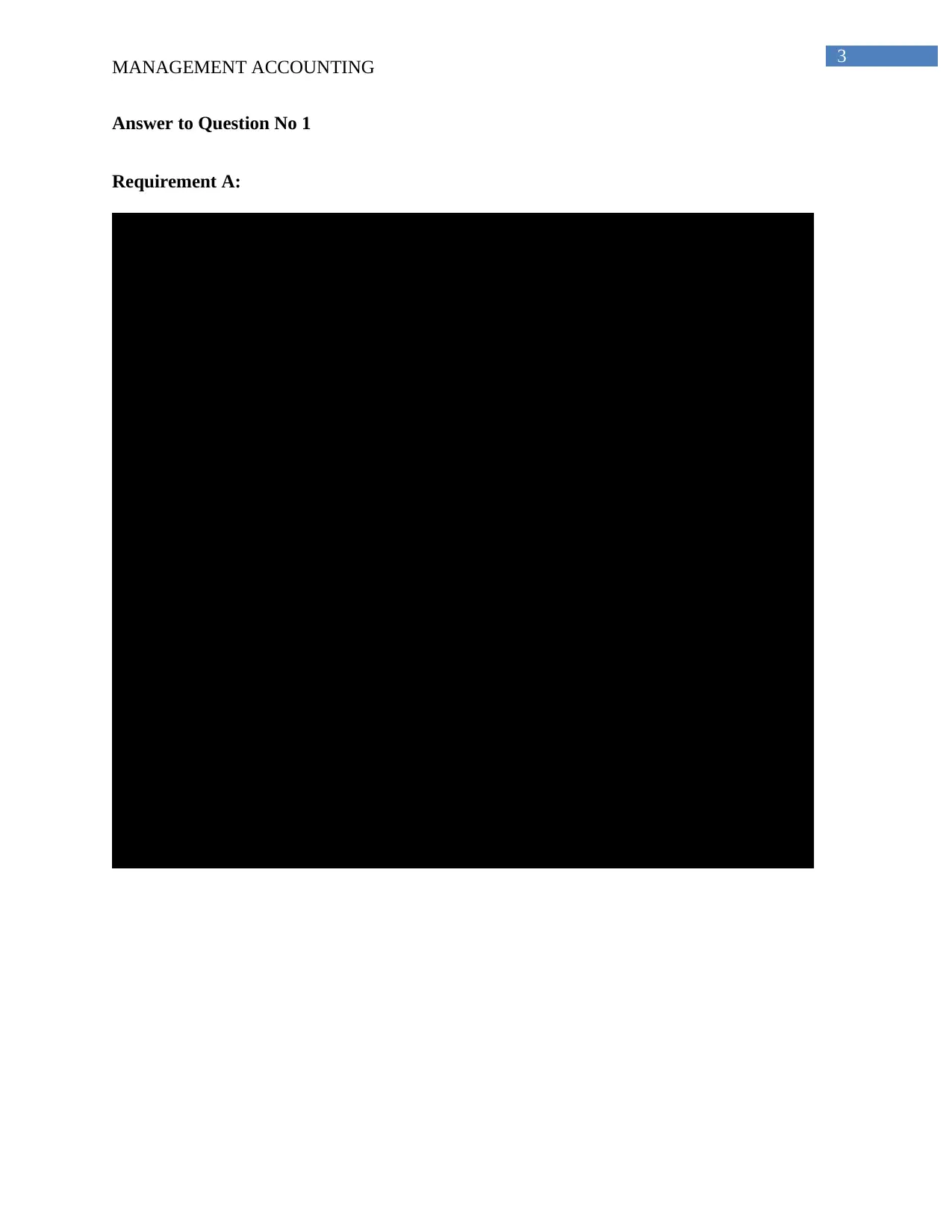

DR. CR.

Date Particulars Amount Date Particulars Amount

1/8/X4 To, Balance b/d 6700 31/8/X4 By, Finished Goods A/c. 30110

To, Direct Labor A/c. 14800 By, Balance c/d 9400

To, Manufacturing Overhead A/c. 12000

To, Direct Material A/c. 6010

39510 39510

DR. CR.

Date Particulars Amount Date Particulars Amount

31/8/X4 To, Bank A/c. 6700 1/8/X4 By, Balance b/d 2345

31/8/X4 To, Balance c/d 1800 By, Direct Material A/c. 6155

8500 8500

Work-in-Process

Accounts Payable

Requirement B:

There exists a huge difference in the construction of the great Pyramid of Giza during its

establishment 4500 years ago. The establishment of the pyramid involved the use of

conventional approaches that included various stages like the planning, execution, initiation,

designing and closing. During the construction of the great pyramid, certain limitations were

there that included cost, mechanisms and the resources (Tucker, & Schaltegger 2016). The

implementation of the new cost management accounting process would lead to a variation in the

difference within the techniques used for the purpose of construction along with the termination

of limitations discussed earlier.

In this respect, which is in relation to the construction of the great pyramid, the

implementation of the process costing would be ideal. It would be helpful for the segregation of

cost that would assist in handling the cost of construction. The cost per unit of the products has

been estimated to be the cost that is similar to the cost found to be in processed costing. The

MANAGEMENT ACCOUNTING

DR. CR.

Date Particulars Amount Date Particulars Amount

1/8/X4 To, Balance b/d 6700 31/8/X4 By, Finished Goods A/c. 30110

To, Direct Labor A/c. 14800 By, Balance c/d 9400

To, Manufacturing Overhead A/c. 12000

To, Direct Material A/c. 6010

39510 39510

DR. CR.

Date Particulars Amount Date Particulars Amount

31/8/X4 To, Bank A/c. 6700 1/8/X4 By, Balance b/d 2345

31/8/X4 To, Balance c/d 1800 By, Direct Material A/c. 6155

8500 8500

Work-in-Process

Accounts Payable

Requirement B:

There exists a huge difference in the construction of the great Pyramid of Giza during its

establishment 4500 years ago. The establishment of the pyramid involved the use of

conventional approaches that included various stages like the planning, execution, initiation,

designing and closing. During the construction of the great pyramid, certain limitations were

there that included cost, mechanisms and the resources (Tucker, & Schaltegger 2016). The

implementation of the new cost management accounting process would lead to a variation in the

difference within the techniques used for the purpose of construction along with the termination

of limitations discussed earlier.

In this respect, which is in relation to the construction of the great pyramid, the

implementation of the process costing would be ideal. It would be helpful for the segregation of

cost that would assist in handling the cost of construction. The cost per unit of the products has

been estimated to be the cost that is similar to the cost found to be in processed costing. The

5

MANAGEMENT ACCOUNTING

processed costing is dependent on the standard cost that is helpful when a wide range of products

is manufactured (Voußem et al., 2017). The construction of the pyramid would become very

complicated without explaining the real cost that is associated. Nevertheless, the introduction of

the processed costing would be helpful in allocating the real cost of the product.

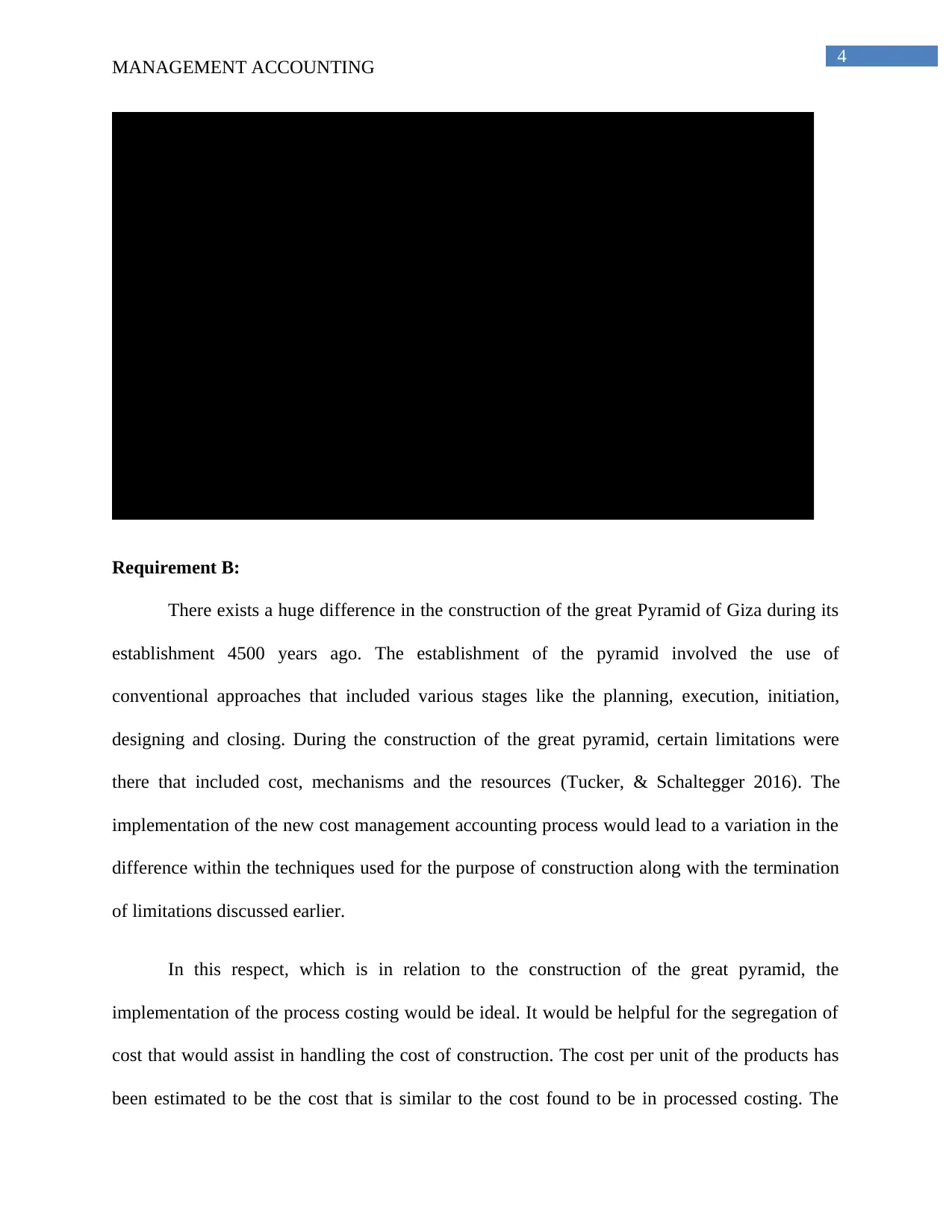

Answer to Question No 2

Computation of Equivalent Units:

Process 1 Physical Flow

Material Conversion

O/WIP 2000 0 1400

Started in May 6000

Total Production 8000

Completed in Process 7000 7000 7000

C/WIP 1000 1000 500

Total Equivalent Units 8000 7500

Process 2 Physical Flow

Material Conversion

O/WIP 1000 0 500

Started in May 7000

Total Production 8000

C/WIP 750 0 225

Completed I Process 7250 7250 7250

Total Equivalent Units 7250 7975

Equivalent Units

Equivalent Units

Cost per Equivalent Units:

MANAGEMENT ACCOUNTING

processed costing is dependent on the standard cost that is helpful when a wide range of products

is manufactured (Voußem et al., 2017). The construction of the pyramid would become very

complicated without explaining the real cost that is associated. Nevertheless, the introduction of

the processed costing would be helpful in allocating the real cost of the product.

Answer to Question No 2

Computation of Equivalent Units:

Process 1 Physical Flow

Material Conversion

O/WIP 2000 0 1400

Started in May 6000

Total Production 8000

Completed in Process 7000 7000 7000

C/WIP 1000 1000 500

Total Equivalent Units 8000 7500

Process 2 Physical Flow

Material Conversion

O/WIP 1000 0 500

Started in May 7000

Total Production 8000

C/WIP 750 0 225

Completed I Process 7250 7250 7250

Total Equivalent Units 7250 7975

Equivalent Units

Equivalent Units

Cost per Equivalent Units:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGEMENT ACCOUNTING

Particulars Material Coversion Transferred-in Total

Process 1:

O/WIP Cost $3,000 $2,000 $5,000

Current Cost $30,000 $60,000 $90,000

Total Production Cost of Process 1 $33,000 $62,000 $95,000

Total Equivalent Units 8000 7500

Cost per Equivalent Units of Process 1 $4.13 $8.27 $12.39

Process 2:

O/WIP Cost $3,000 $4,000 $8,000 $15,000

Current Cost $35,000 $45,000 $86,742 $166,742

Total Production Cost of Process 2 $38,000 $49,000 $94,742 $181,742

Total Equivalent Units 7250 7975 7000

Cost per Equivalent Units of Process 2 $5.24 $6.14 $13.53 $25

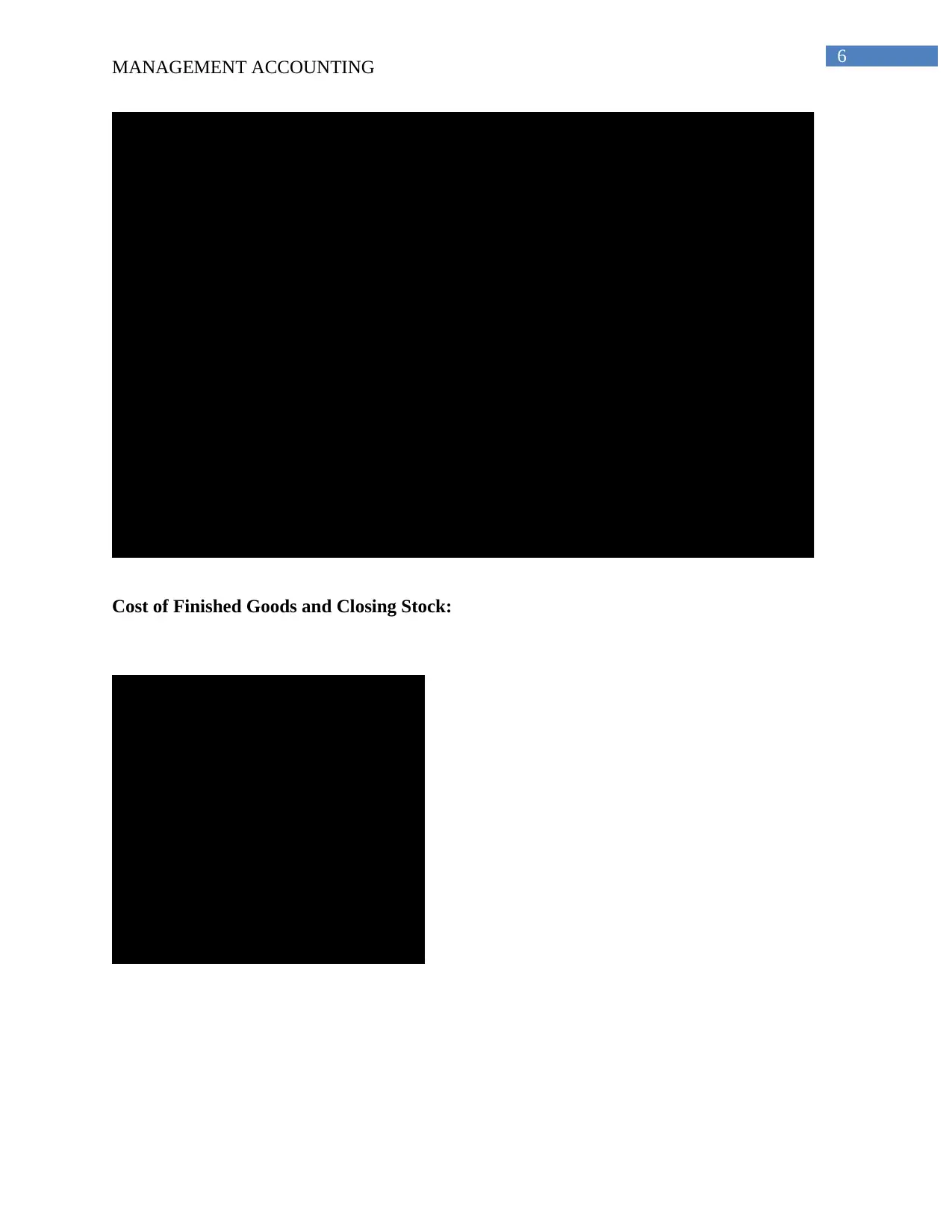

Cost of Finished Goods and Closing Stock:

Particulars Amount

Finished Goods Completed during May 7250

Cost per Equivalent Units $25

Cost of Finished Goods Completed $180,671

Closing Stock in Process 1 1000

Cost per Equivalent Units for Process 1 $12.39

Cost of Closing Stock in Process 1 $12,391.67

Closing Stock in Process 2 750

Cost per Equivalent Units for Process 1 $24.92

Cost of Closing Stock in Process 2 $18,690.08

MANAGEMENT ACCOUNTING

Particulars Material Coversion Transferred-in Total

Process 1:

O/WIP Cost $3,000 $2,000 $5,000

Current Cost $30,000 $60,000 $90,000

Total Production Cost of Process 1 $33,000 $62,000 $95,000

Total Equivalent Units 8000 7500

Cost per Equivalent Units of Process 1 $4.13 $8.27 $12.39

Process 2:

O/WIP Cost $3,000 $4,000 $8,000 $15,000

Current Cost $35,000 $45,000 $86,742 $166,742

Total Production Cost of Process 2 $38,000 $49,000 $94,742 $181,742

Total Equivalent Units 7250 7975 7000

Cost per Equivalent Units of Process 2 $5.24 $6.14 $13.53 $25

Cost of Finished Goods and Closing Stock:

Particulars Amount

Finished Goods Completed during May 7250

Cost per Equivalent Units $25

Cost of Finished Goods Completed $180,671

Closing Stock in Process 1 1000

Cost per Equivalent Units for Process 1 $12.39

Cost of Closing Stock in Process 1 $12,391.67

Closing Stock in Process 2 750

Cost per Equivalent Units for Process 1 $24.92

Cost of Closing Stock in Process 2 $18,690.08

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT ACCOUNTING

Answer to Question No 3

Requirement a:

Particulars Amount

Total Joint Production Cost A $250,000

Less: Joint Cost allocated to

A B $187,500

Joint Cost allocated to B C=A-B $62,500

Sales Volume of C (in kg.) D 60000

Selling Price per kg. of C E $4.50

Net Realisable Value of C F=DxE $270,000

Net Realisable Value of D

G=Fx(C/

B) $90,000

Sales Volume of D (in kg.) H 40000

Selling Price per kg. of D I=G/H $2.25

Requirement b:

The net profit, earned in general circumstances, are computed below:

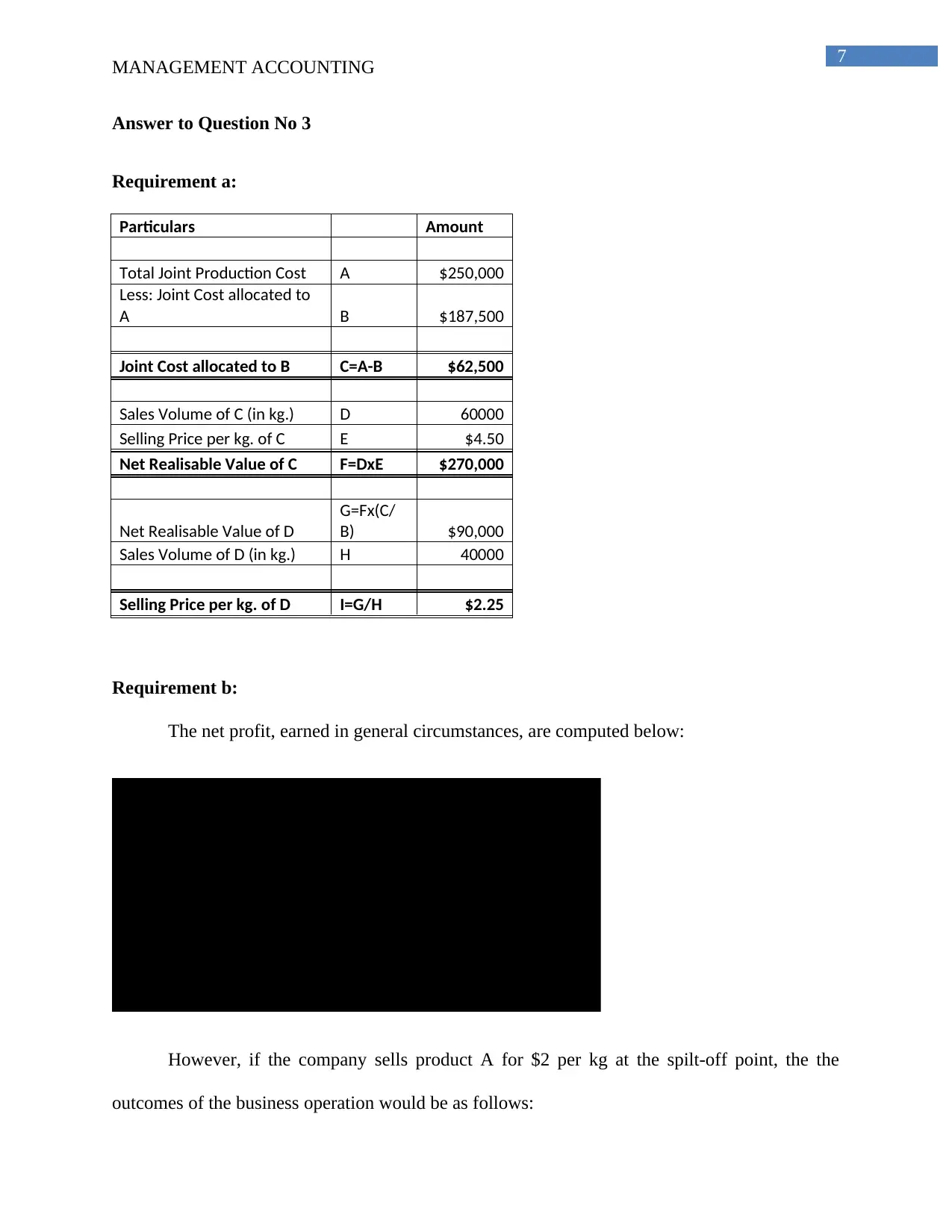

Particulars A B Total

Selling Price per unit $4.50 $2.25

Sales Volume 60000 40000 100000

Total Sale Revenue $270,000 $90,000 $360,000

Joint Cost Allocation ($187,500) ($62,500) ($250,000)

Further Processing Cost ($45,000) ($25,000) ($70,000)

Net Profit $37,500 $2,500 $40,000

However, if the company sells product A for $2 per kg at the spilt-off point, the the

outcomes of the business operation would be as follows:

MANAGEMENT ACCOUNTING

Answer to Question No 3

Requirement a:

Particulars Amount

Total Joint Production Cost A $250,000

Less: Joint Cost allocated to

A B $187,500

Joint Cost allocated to B C=A-B $62,500

Sales Volume of C (in kg.) D 60000

Selling Price per kg. of C E $4.50

Net Realisable Value of C F=DxE $270,000

Net Realisable Value of D

G=Fx(C/

B) $90,000

Sales Volume of D (in kg.) H 40000

Selling Price per kg. of D I=G/H $2.25

Requirement b:

The net profit, earned in general circumstances, are computed below:

Particulars A B Total

Selling Price per unit $4.50 $2.25

Sales Volume 60000 40000 100000

Total Sale Revenue $270,000 $90,000 $360,000

Joint Cost Allocation ($187,500) ($62,500) ($250,000)

Further Processing Cost ($45,000) ($25,000) ($70,000)

Net Profit $37,500 $2,500 $40,000

However, if the company sells product A for $2 per kg at the spilt-off point, the the

outcomes of the business operation would be as follows:

8

MANAGEMENT ACCOUNTING

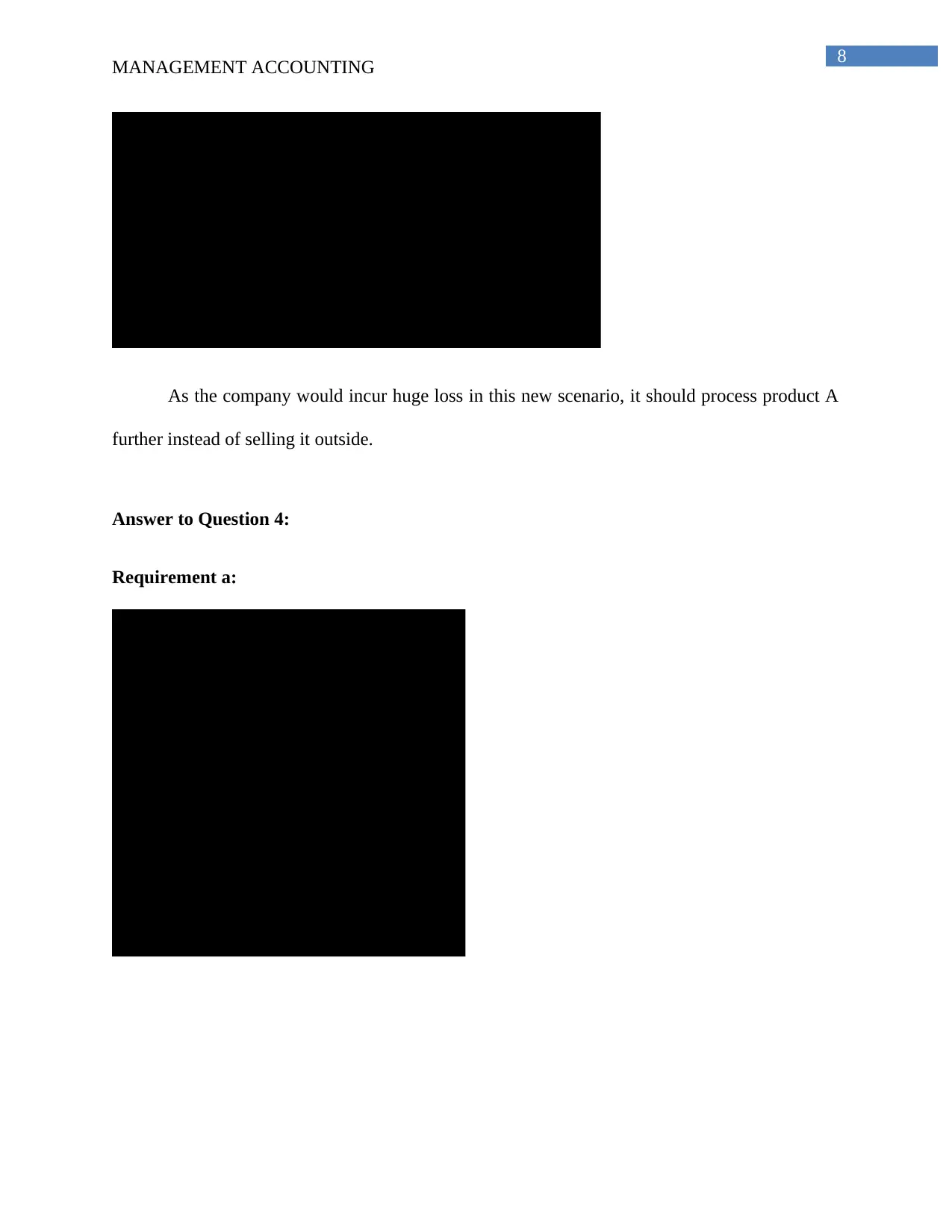

Particulars A B Total

Selling Price per unit $2.00 $2.25

Sales Volume 60000 40000 100000

Total Sale Revenue $120,000 $90,000 $210,000

Joint Cost Allocation ($142,857) ($107,143) ($250,000)

Further Processing Cost ($25,000) ($25,000)

Net Profit ($22,857) ($42,143) ($65,000)

As the company would incur huge loss in this new scenario, it should process product A

further instead of selling it outside.

Answer to Question 4:

Requirement a:

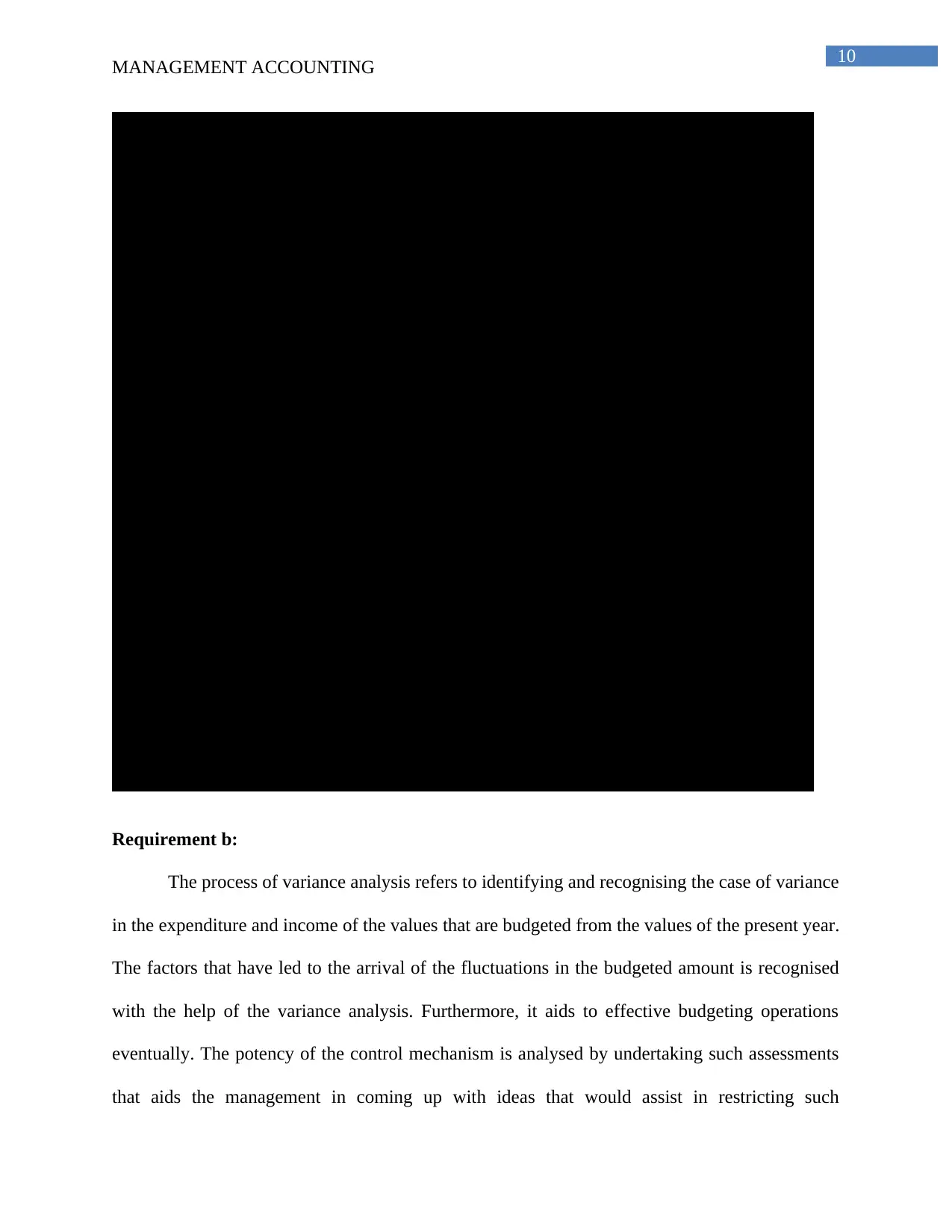

Particulars Amount

Material Purchased (in units) 220000

Standard Price per kg $6

Standard Cost for Actual Material

Purchased $1,320,000

Actual Cost of Actual Material

Purchased $1,364,000

Material Price Variance ($44,000)

Remarks Unfavorable

Material Price Variance:

MANAGEMENT ACCOUNTING

Particulars A B Total

Selling Price per unit $2.00 $2.25

Sales Volume 60000 40000 100000

Total Sale Revenue $120,000 $90,000 $210,000

Joint Cost Allocation ($142,857) ($107,143) ($250,000)

Further Processing Cost ($25,000) ($25,000)

Net Profit ($22,857) ($42,143) ($65,000)

As the company would incur huge loss in this new scenario, it should process product A

further instead of selling it outside.

Answer to Question 4:

Requirement a:

Particulars Amount

Material Purchased (in units) 220000

Standard Price per kg $6

Standard Cost for Actual Material

Purchased $1,320,000

Actual Cost of Actual Material

Purchased $1,364,000

Material Price Variance ($44,000)

Remarks Unfavorable

Material Price Variance:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGEMENT ACCOUNTING

Particulars Amount

Units Produced 19500

Standard Usage per unit of

production 11

Standard Usage for Actual

Production 214500

Actual Material Usage 197000

Standard price per kg. $6

Material Usage Variance $105,000

Remarks Favorable

Material Usage Variance:

Particulars Amount

Actual Production 19500

Standard Labor hour per unit 2

Standard Labor Hour for Actual

Production 39000

Actual Labor Hours 40000

Standard Labor Rate per hour $20

Direct Labor Efficiency Variance ($20,000)

Total Direct Labor Variance ($1,650)

Direct Labor Rate Variace $18,350

Standard Labor Cost for Actual

Labor Hours $800,000

Actual Labor Cost $781,650

Actual Direct Labor Rate per hour $19.54

Actual Direct Labor Rate per hour:

MANAGEMENT ACCOUNTING

Particulars Amount

Units Produced 19500

Standard Usage per unit of

production 11

Standard Usage for Actual

Production 214500

Actual Material Usage 197000

Standard price per kg. $6

Material Usage Variance $105,000

Remarks Favorable

Material Usage Variance:

Particulars Amount

Actual Production 19500

Standard Labor hour per unit 2

Standard Labor Hour for Actual

Production 39000

Actual Labor Hours 40000

Standard Labor Rate per hour $20

Direct Labor Efficiency Variance ($20,000)

Total Direct Labor Variance ($1,650)

Direct Labor Rate Variace $18,350

Standard Labor Cost for Actual

Labor Hours $800,000

Actual Labor Cost $781,650

Actual Direct Labor Rate per hour $19.54

Actual Direct Labor Rate per hour:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGEMENT ACCOUNTING

Dr. Cr.

Date Amount Amount

Direct Material A/c. Dr. $1,364,000

To, Accounts Payable A/c. $1,364,000

Work-in-Progress A/c. Dr. 1287000

To, Direct Material A/c. 1287000

Material Price Variance A/c. Dr. $44,000

To, Direct Material A/c. $44,000

Direct Material A/c. Dr. $105,000

To, Material Usage Variance A/c. $105,000

Direct Labor Cost A/c. Dr. $781,650

To, Accrued Payroll A/c. $781,650

Work-in-Progress A/c. Dr. 780000

To, Direct Labor Cost A/c. 780000

Direct Labor Cost A/c. Dr. $18,350

To, Direct Labor Rate Variance A/c. $18,350

Direct Labor Efficiency Variance A/c. Dr. $20,000

To, Direct Labor Cost A/c. $20,000

Material Usage Variance A/c. Dr. $105,000

Direct Labor Rate Variance A/c. Dr. $18,350

To, Cost of Goods Sold A/c. $59,350

To, Direct Labor Efficiency Variance A/c. $20,000

To, Material Price Variance A/c. $44,000

Particulars

Requirement b:

The process of variance analysis refers to identifying and recognising the case of variance

in the expenditure and income of the values that are budgeted from the values of the present year.

The factors that have led to the arrival of the fluctuations in the budgeted amount is recognised

with the help of the variance analysis. Furthermore, it aids to effective budgeting operations

eventually. The potency of the control mechanism is analysed by undertaking such assessments

that aids the management in coming up with ideas that would assist in restricting such

MANAGEMENT ACCOUNTING

Dr. Cr.

Date Amount Amount

Direct Material A/c. Dr. $1,364,000

To, Accounts Payable A/c. $1,364,000

Work-in-Progress A/c. Dr. 1287000

To, Direct Material A/c. 1287000

Material Price Variance A/c. Dr. $44,000

To, Direct Material A/c. $44,000

Direct Material A/c. Dr. $105,000

To, Material Usage Variance A/c. $105,000

Direct Labor Cost A/c. Dr. $781,650

To, Accrued Payroll A/c. $781,650

Work-in-Progress A/c. Dr. 780000

To, Direct Labor Cost A/c. 780000

Direct Labor Cost A/c. Dr. $18,350

To, Direct Labor Rate Variance A/c. $18,350

Direct Labor Efficiency Variance A/c. Dr. $20,000

To, Direct Labor Cost A/c. $20,000

Material Usage Variance A/c. Dr. $105,000

Direct Labor Rate Variance A/c. Dr. $18,350

To, Cost of Goods Sold A/c. $59,350

To, Direct Labor Efficiency Variance A/c. $20,000

To, Material Price Variance A/c. $44,000

Particulars

Requirement b:

The process of variance analysis refers to identifying and recognising the case of variance

in the expenditure and income of the values that are budgeted from the values of the present year.

The factors that have led to the arrival of the fluctuations in the budgeted amount is recognised

with the help of the variance analysis. Furthermore, it aids to effective budgeting operations

eventually. The potency of the control mechanism is analysed by undertaking such assessments

that aids the management in coming up with ideas that would assist in restricting such

11

MANAGEMENT ACCOUNTING

divergences (Alawattage et al., 2017). It aids in assisting during the allocation of the

responsibilities, which makes the departments occupied with the control methods.

The evaluation of the variance is regarded a vital equipment in business management and

is pertinent in the management accounting method. It aids in evaluating the reason for deviation

among the anticipated and the real values that aids in enhancing the efficiency and in that manner

assists in maintaining the command over the expenditure of the project by efficient supervising

of the planned versus and the real expenditure. The various issues, opportunities and the patterns

with respect to the short-term and the long-term accomplishment for any venture of the company

are discovered with the help of efficient variance evaluation. It aids in determining the variances

of cost and revenue.

The quantitative examination has been significant in several other locations like the

assessment of the performance, human resource department and organizational behaviour. It aids

in giving out open communication regarding the feedback expectation and the performance of

various other departments. The financial end result of the company is associated directly with the

performance of the human resource and the variance assessment aids in creating the relationship

between the changes in numerous departments (Van der Stede, 2015). The implementation of the

variance analysis aids in evaluating the responses of the employees in several aspects that will

assist in achieving the feedback. The managers at several levels functioning in various

departments utilise the variance evaluation that aids them in introducing the efficient

mechanisms and equipments of managing the costs. They look to obtain the maximum level of

benefit from the variance of material usage.

MANAGEMENT ACCOUNTING

divergences (Alawattage et al., 2017). It aids in assisting during the allocation of the

responsibilities, which makes the departments occupied with the control methods.

The evaluation of the variance is regarded a vital equipment in business management and

is pertinent in the management accounting method. It aids in evaluating the reason for deviation

among the anticipated and the real values that aids in enhancing the efficiency and in that manner

assists in maintaining the command over the expenditure of the project by efficient supervising

of the planned versus and the real expenditure. The various issues, opportunities and the patterns

with respect to the short-term and the long-term accomplishment for any venture of the company

are discovered with the help of efficient variance evaluation. It aids in determining the variances

of cost and revenue.

The quantitative examination has been significant in several other locations like the

assessment of the performance, human resource department and organizational behaviour. It aids

in giving out open communication regarding the feedback expectation and the performance of

various other departments. The financial end result of the company is associated directly with the

performance of the human resource and the variance assessment aids in creating the relationship

between the changes in numerous departments (Van der Stede, 2015). The implementation of the

variance analysis aids in evaluating the responses of the employees in several aspects that will

assist in achieving the feedback. The managers at several levels functioning in various

departments utilise the variance evaluation that aids them in introducing the efficient

mechanisms and equipments of managing the costs. They look to obtain the maximum level of

benefit from the variance of material usage.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.