Malaysia University of Science and Technology: Management Accounting

VerifiedAdded on 2022/12/19

|16

|3267

|71

Homework Assignment

AI Summary

This management accounting assignment solution provides a comprehensive analysis of various cost accounting concepts. The solution begins with an activity-based costing analysis, computing activity cost rates and assigning costs to different activities, including customer orders, complaints, and credit checks. It then proceeds to a break-even analysis, determining the sales levels required to achieve desired profit margins under single and double-shift operations. The assignment also covers budgeting, including sales, production, and component usage budgets, along with a production cost budget. Finally, it assesses financial feasibility based on the budget findings and presents a strategic plan for a university, focusing on operational improvements, student welfare, and strategic objectives. The solution demonstrates a strong understanding of cost accounting principles and their application in decision-making.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUSETION- 1.................................................................................................................................1

(a) Computation of the activity cost rate as per the traditional method of activity based costing

......................................................................................................................................................1

(b) Computation of the time-driven activity cost driver rates......................................................1

(c) Computation of the cost assigned to each activities...............................................................2

(d).................................................................................................................................................2

QUESTION- 2.................................................................................................................................3

(a) Contribution margin per capacitor in January........................................................................3

(b) Sales level at the desired profit of 20%..................................................................................3

(c) Break-even analysis of single shift operations.......................................................................4

Break-even analysis of double shift operations...........................................................................4

(d) Sales level at the desired profit of 10% in February at single shift of operation...................4

Sales level at the desired profit of 10% in February at double shift of operation........................5

QUESTION 3...................................................................................................................................6

a) .................................................................................................................................................6

b)..................................................................................................................................................7

QUESTION 4...................................................................................................................................7

REFERENCES..............................................................................................................................12

QUSETION- 1.................................................................................................................................1

(a) Computation of the activity cost rate as per the traditional method of activity based costing

......................................................................................................................................................1

(b) Computation of the time-driven activity cost driver rates......................................................1

(c) Computation of the cost assigned to each activities...............................................................2

(d).................................................................................................................................................2

QUESTION- 2.................................................................................................................................3

(a) Contribution margin per capacitor in January........................................................................3

(b) Sales level at the desired profit of 20%..................................................................................3

(c) Break-even analysis of single shift operations.......................................................................4

Break-even analysis of double shift operations...........................................................................4

(d) Sales level at the desired profit of 10% in February at single shift of operation...................4

Sales level at the desired profit of 10% in February at double shift of operation........................5

QUESTION 3...................................................................................................................................6

a) .................................................................................................................................................6

b)..................................................................................................................................................7

QUESTION 4...................................................................................................................................7

REFERENCES..............................................................................................................................12

QUSETION- 1

(a) Computation of the activity cost rate as per the traditional method of activity based costing

S.NO ACTIVITY

TIME

PERCENT

AGE

ASSIGNED

COST

ESTIMATED COST

DRIVER

QUANTITY

COST

DRIVER

RATE

1

Handle customer

orders 50.00% 300000 5000 customer orders

60 per customer

order

2

Process customer

complaints 35.00% 210000

700 customer

complaints

300 per

customer

complaint

3

Perform

customer credit

check 15.00% 90000 600 credit checks

150 per credit

checks

RM 600000

The total assigned cost to the various services is RM 600000 which is used by the service

personnels in three different types of services which are handling the customer orders, processing

the customer complaints and performing the customer credit check (Keel and et.al., 2017).

It can be assessed that the activity cost rate is RM 60 per customer order, RM 300 per customer

complaint and RM 150 per credit checks on the basis of their respective level of the actibvities

that are undertaken.

(b) Computation of the time-driven activity cost driver rates

Committed resource cost for

customer service 600000

Working hours 30000

Cost per hour 600000/30000

20

S.NO ACTIVITY

UNIT TIME

(HOURS)

ACTIVITY COST

DRIVER @ 20 PER

HOUR

1 Handle customer orders 2 40

2 Process customer complaints 7 140

3 Perform customer credit check 5 100

1

(a) Computation of the activity cost rate as per the traditional method of activity based costing

S.NO ACTIVITY

TIME

PERCENT

AGE

ASSIGNED

COST

ESTIMATED COST

DRIVER

QUANTITY

COST

DRIVER

RATE

1

Handle customer

orders 50.00% 300000 5000 customer orders

60 per customer

order

2

Process customer

complaints 35.00% 210000

700 customer

complaints

300 per

customer

complaint

3

Perform

customer credit

check 15.00% 90000 600 credit checks

150 per credit

checks

RM 600000

The total assigned cost to the various services is RM 600000 which is used by the service

personnels in three different types of services which are handling the customer orders, processing

the customer complaints and performing the customer credit check (Keel and et.al., 2017).

It can be assessed that the activity cost rate is RM 60 per customer order, RM 300 per customer

complaint and RM 150 per credit checks on the basis of their respective level of the actibvities

that are undertaken.

(b) Computation of the time-driven activity cost driver rates

Committed resource cost for

customer service 600000

Working hours 30000

Cost per hour 600000/30000

20

S.NO ACTIVITY

UNIT TIME

(HOURS)

ACTIVITY COST

DRIVER @ 20 PER

HOUR

1 Handle customer orders 2 40

2 Process customer complaints 7 140

3 Perform customer credit check 5 100

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The cost per hour is RM 20 based on the supplied resources and the actual working hours

that are undertaken by the company (Leahy and et.al., 2017). On the basis of the provided unit

time the activity cost driver per activity is ascertained which is RM 40 per hour for handling

customer orders. RM 140 per hour is for processing the customer complaints and RM 100 per

hour is for performing the credit checks.

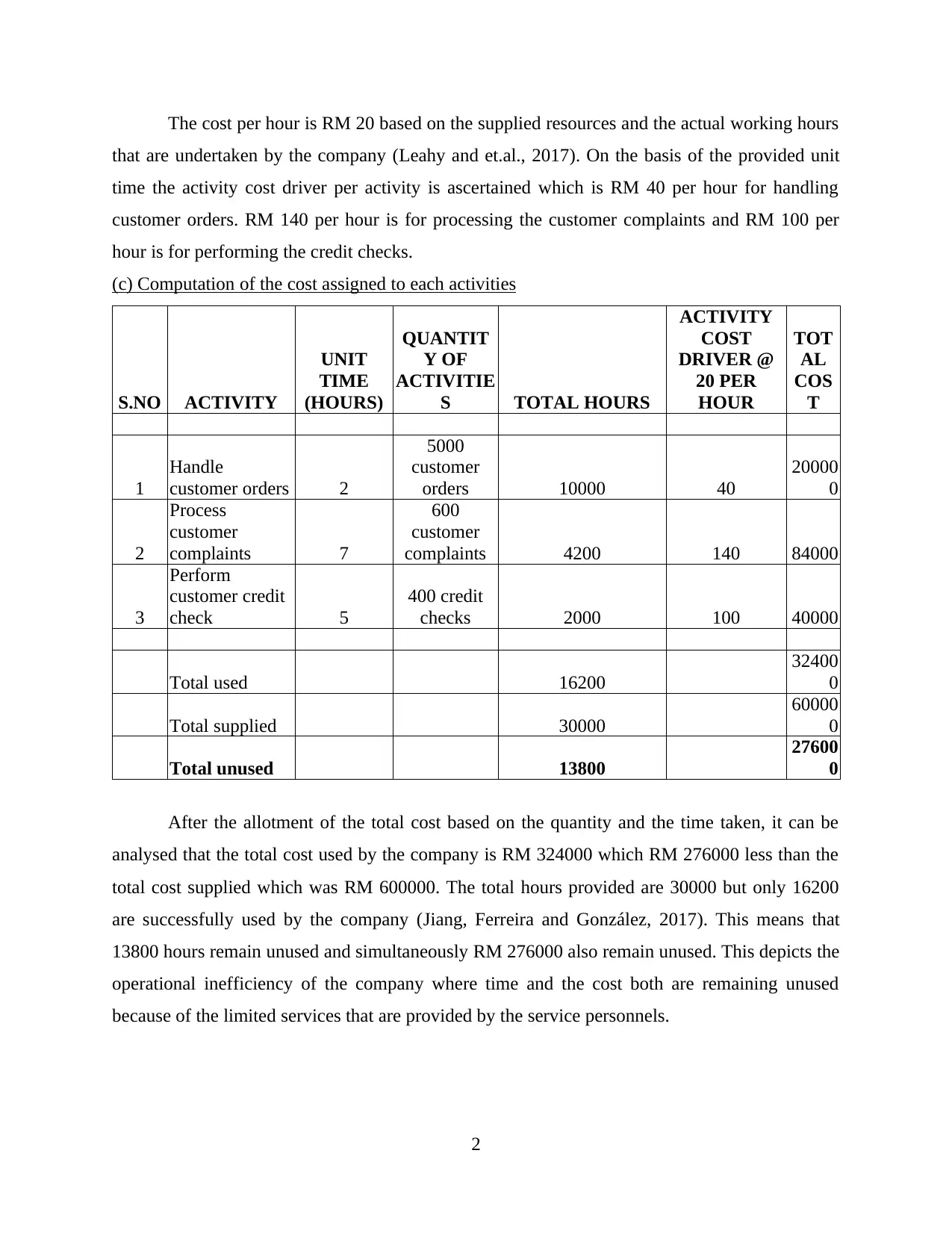

(c) Computation of the cost assigned to each activities

S.NO ACTIVITY

UNIT

TIME

(HOURS)

QUANTIT

Y OF

ACTIVITIE

S TOTAL HOURS

ACTIVITY

COST

DRIVER @

20 PER

HOUR

TOT

AL

COS

T

1

Handle

customer orders 2

5000

customer

orders 10000 40

20000

0

2

Process

customer

complaints 7

600

customer

complaints 4200 140 84000

3

Perform

customer credit

check 5

400 credit

checks 2000 100 40000

Total used 16200

32400

0

Total supplied 30000

60000

0

Total unused 13800

27600

0

After the allotment of the total cost based on the quantity and the time taken, it can be

analysed that the total cost used by the company is RM 324000 which RM 276000 less than the

total cost supplied which was RM 600000. The total hours provided are 30000 but only 16200

are successfully used by the company (Jiang, Ferreira and González, 2017). This means that

13800 hours remain unused and simultaneously RM 276000 also remain unused. This depicts the

operational inefficiency of the company where time and the cost both are remaining unused

because of the limited services that are provided by the service personnels.

2

that are undertaken by the company (Leahy and et.al., 2017). On the basis of the provided unit

time the activity cost driver per activity is ascertained which is RM 40 per hour for handling

customer orders. RM 140 per hour is for processing the customer complaints and RM 100 per

hour is for performing the credit checks.

(c) Computation of the cost assigned to each activities

S.NO ACTIVITY

UNIT

TIME

(HOURS)

QUANTIT

Y OF

ACTIVITIE

S TOTAL HOURS

ACTIVITY

COST

DRIVER @

20 PER

HOUR

TOT

AL

COS

T

1

Handle

customer orders 2

5000

customer

orders 10000 40

20000

0

2

Process

customer

complaints 7

600

customer

complaints 4200 140 84000

3

Perform

customer credit

check 5

400 credit

checks 2000 100 40000

Total used 16200

32400

0

Total supplied 30000

60000

0

Total unused 13800

27600

0

After the allotment of the total cost based on the quantity and the time taken, it can be

analysed that the total cost used by the company is RM 324000 which RM 276000 less than the

total cost supplied which was RM 600000. The total hours provided are 30000 but only 16200

are successfully used by the company (Jiang, Ferreira and González, 2017). This means that

13800 hours remain unused and simultaneously RM 276000 also remain unused. This depicts the

operational inefficiency of the company where time and the cost both are remaining unused

because of the limited services that are provided by the service personnels.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

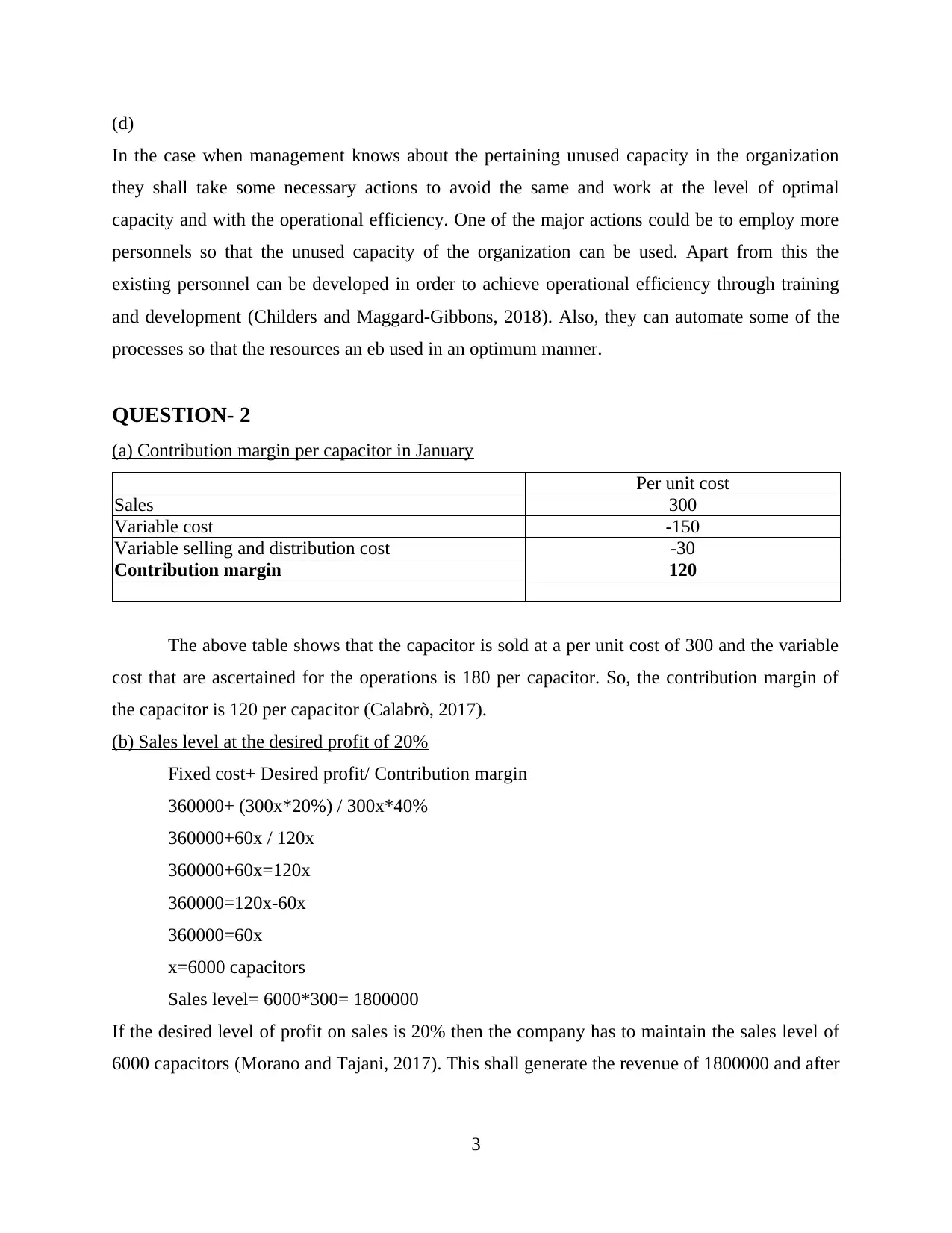

(d)

In the case when management knows about the pertaining unused capacity in the organization

they shall take some necessary actions to avoid the same and work at the level of optimal

capacity and with the operational efficiency. One of the major actions could be to employ more

personnels so that the unused capacity of the organization can be used. Apart from this the

existing personnel can be developed in order to achieve operational efficiency through training

and development (Childers and Maggard-Gibbons, 2018). Also, they can automate some of the

processes so that the resources an eb used in an optimum manner.

QUESTION- 2

(a) Contribution margin per capacitor in January

Per unit cost

Sales 300

Variable cost -150

Variable selling and distribution cost -30

Contribution margin 120

The above table shows that the capacitor is sold at a per unit cost of 300 and the variable

cost that are ascertained for the operations is 180 per capacitor. So, the contribution margin of

the capacitor is 120 per capacitor (Calabrò, 2017).

(b) Sales level at the desired profit of 20%

Fixed cost+ Desired profit/ Contribution margin

360000+ (300x*20%) / 300x*40%

360000+60x / 120x

360000+60x=120x

360000=120x-60x

360000=60x

x=6000 capacitors

Sales level= 6000*300= 1800000

If the desired level of profit on sales is 20% then the company has to maintain the sales level of

6000 capacitors (Morano and Tajani, 2017). This shall generate the revenue of 1800000 and after

3

In the case when management knows about the pertaining unused capacity in the organization

they shall take some necessary actions to avoid the same and work at the level of optimal

capacity and with the operational efficiency. One of the major actions could be to employ more

personnels so that the unused capacity of the organization can be used. Apart from this the

existing personnel can be developed in order to achieve operational efficiency through training

and development (Childers and Maggard-Gibbons, 2018). Also, they can automate some of the

processes so that the resources an eb used in an optimum manner.

QUESTION- 2

(a) Contribution margin per capacitor in January

Per unit cost

Sales 300

Variable cost -150

Variable selling and distribution cost -30

Contribution margin 120

The above table shows that the capacitor is sold at a per unit cost of 300 and the variable

cost that are ascertained for the operations is 180 per capacitor. So, the contribution margin of

the capacitor is 120 per capacitor (Calabrò, 2017).

(b) Sales level at the desired profit of 20%

Fixed cost+ Desired profit/ Contribution margin

360000+ (300x*20%) / 300x*40%

360000+60x / 120x

360000+60x=120x

360000=120x-60x

360000=60x

x=6000 capacitors

Sales level= 6000*300= 1800000

If the desired level of profit on sales is 20% then the company has to maintain the sales level of

6000 capacitors (Morano and Tajani, 2017). This shall generate the revenue of 1800000 and after

3

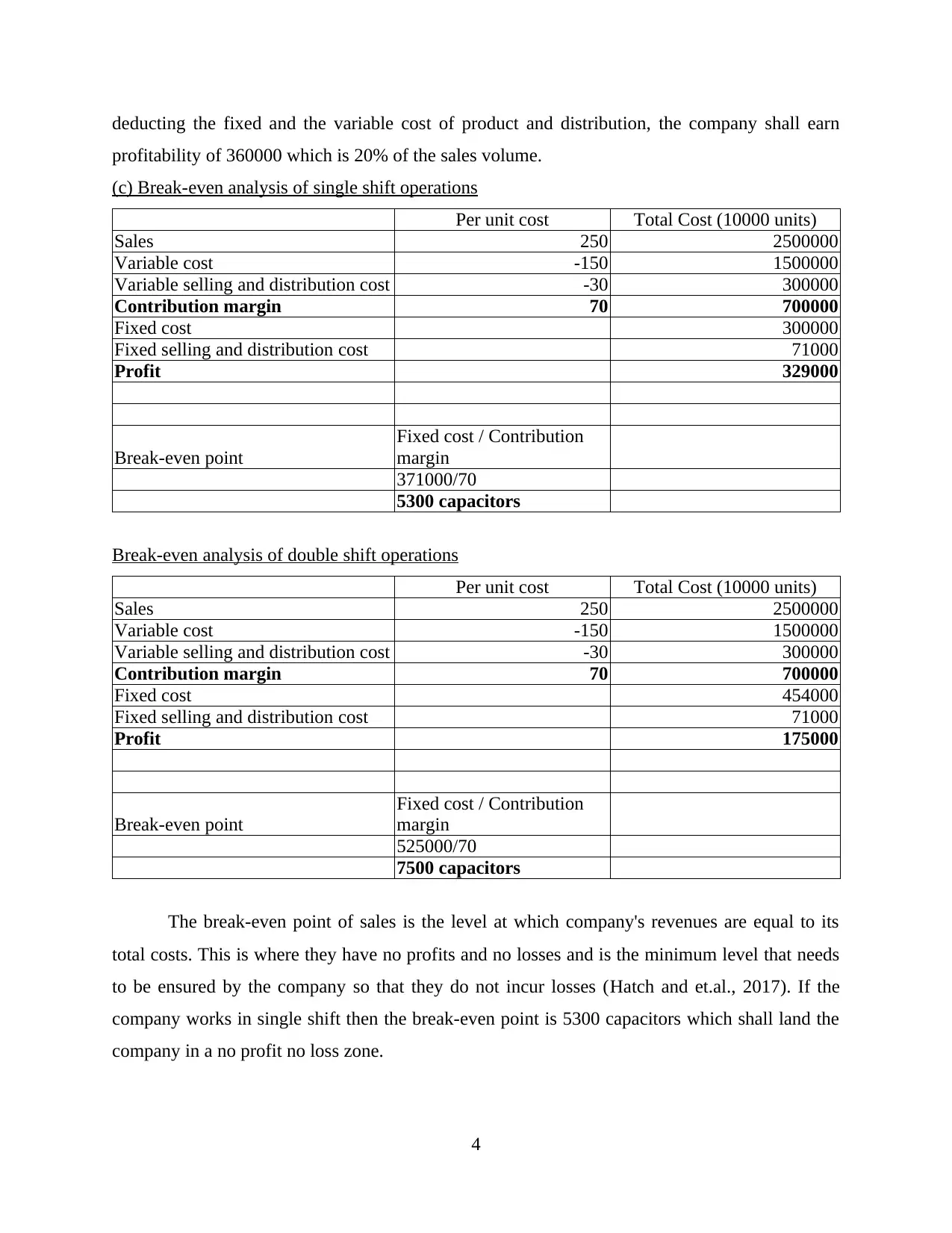

deducting the fixed and the variable cost of product and distribution, the company shall earn

profitability of 360000 which is 20% of the sales volume.

(c) Break-even analysis of single shift operations

Per unit cost Total Cost (10000 units)

Sales 250 2500000

Variable cost -150 1500000

Variable selling and distribution cost -30 300000

Contribution margin 70 700000

Fixed cost 300000

Fixed selling and distribution cost 71000

Profit 329000

Break-even point

Fixed cost / Contribution

margin

371000/70

5300 capacitors

Break-even analysis of double shift operations

Per unit cost Total Cost (10000 units)

Sales 250 2500000

Variable cost -150 1500000

Variable selling and distribution cost -30 300000

Contribution margin 70 700000

Fixed cost 454000

Fixed selling and distribution cost 71000

Profit 175000

Break-even point

Fixed cost / Contribution

margin

525000/70

7500 capacitors

The break-even point of sales is the level at which company's revenues are equal to its

total costs. This is where they have no profits and no losses and is the minimum level that needs

to be ensured by the company so that they do not incur losses (Hatch and et.al., 2017). If the

company works in single shift then the break-even point is 5300 capacitors which shall land the

company in a no profit no loss zone.

4

profitability of 360000 which is 20% of the sales volume.

(c) Break-even analysis of single shift operations

Per unit cost Total Cost (10000 units)

Sales 250 2500000

Variable cost -150 1500000

Variable selling and distribution cost -30 300000

Contribution margin 70 700000

Fixed cost 300000

Fixed selling and distribution cost 71000

Profit 329000

Break-even point

Fixed cost / Contribution

margin

371000/70

5300 capacitors

Break-even analysis of double shift operations

Per unit cost Total Cost (10000 units)

Sales 250 2500000

Variable cost -150 1500000

Variable selling and distribution cost -30 300000

Contribution margin 70 700000

Fixed cost 454000

Fixed selling and distribution cost 71000

Profit 175000

Break-even point

Fixed cost / Contribution

margin

525000/70

7500 capacitors

The break-even point of sales is the level at which company's revenues are equal to its

total costs. This is where they have no profits and no losses and is the minimum level that needs

to be ensured by the company so that they do not incur losses (Hatch and et.al., 2017). If the

company works in single shift then the break-even point is 5300 capacitors which shall land the

company in a no profit no loss zone.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

But if the company works in two shifts in that case the break-even point is at 7500

capacitors which is the minimum level of sales so that no losses are incurred to the company.

(d) Sales level at the desired profit of 10% in February at single shift of operation

Fixed cost+ Desired profit/ Contribution margin

371000+ (250x*10%) / 250x*28%

371000+25x / 70x

371000+25x=70x

371000=70x-25x

371000=45x

x=8244.44 capacitors

Sales level= 8244*250= 2061000

The sales level under the single shift system to earn the profitability of 10% is up-to 8244

capacitors (Van Asseldonk, Van Wagenberg and Wisselink, 2017).

Sales level at the desired profit of 10% in February at double shift of operation

Fixed cost+ Desired profit/ Contribution margin

525000+ (250x*10%) / 250x*28%

525000+25x / 70x

525000+25x=70x

525000=70x-25x

525000=45x

x=11666.66 capacitors

Sales level= 11667*250= 2916750

The sales level under the double shift system to earn the profitability of 10% is up-to 11667

capacitors.

5

capacitors which is the minimum level of sales so that no losses are incurred to the company.

(d) Sales level at the desired profit of 10% in February at single shift of operation

Fixed cost+ Desired profit/ Contribution margin

371000+ (250x*10%) / 250x*28%

371000+25x / 70x

371000+25x=70x

371000=70x-25x

371000=45x

x=8244.44 capacitors

Sales level= 8244*250= 2061000

The sales level under the single shift system to earn the profitability of 10% is up-to 8244

capacitors (Van Asseldonk, Van Wagenberg and Wisselink, 2017).

Sales level at the desired profit of 10% in February at double shift of operation

Fixed cost+ Desired profit/ Contribution margin

525000+ (250x*10%) / 250x*28%

525000+25x / 70x

525000+25x=70x

525000=70x-25x

525000=45x

x=11666.66 capacitors

Sales level= 11667*250= 2916750

The sales level under the double shift system to earn the profitability of 10% is up-to 11667

capacitors.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

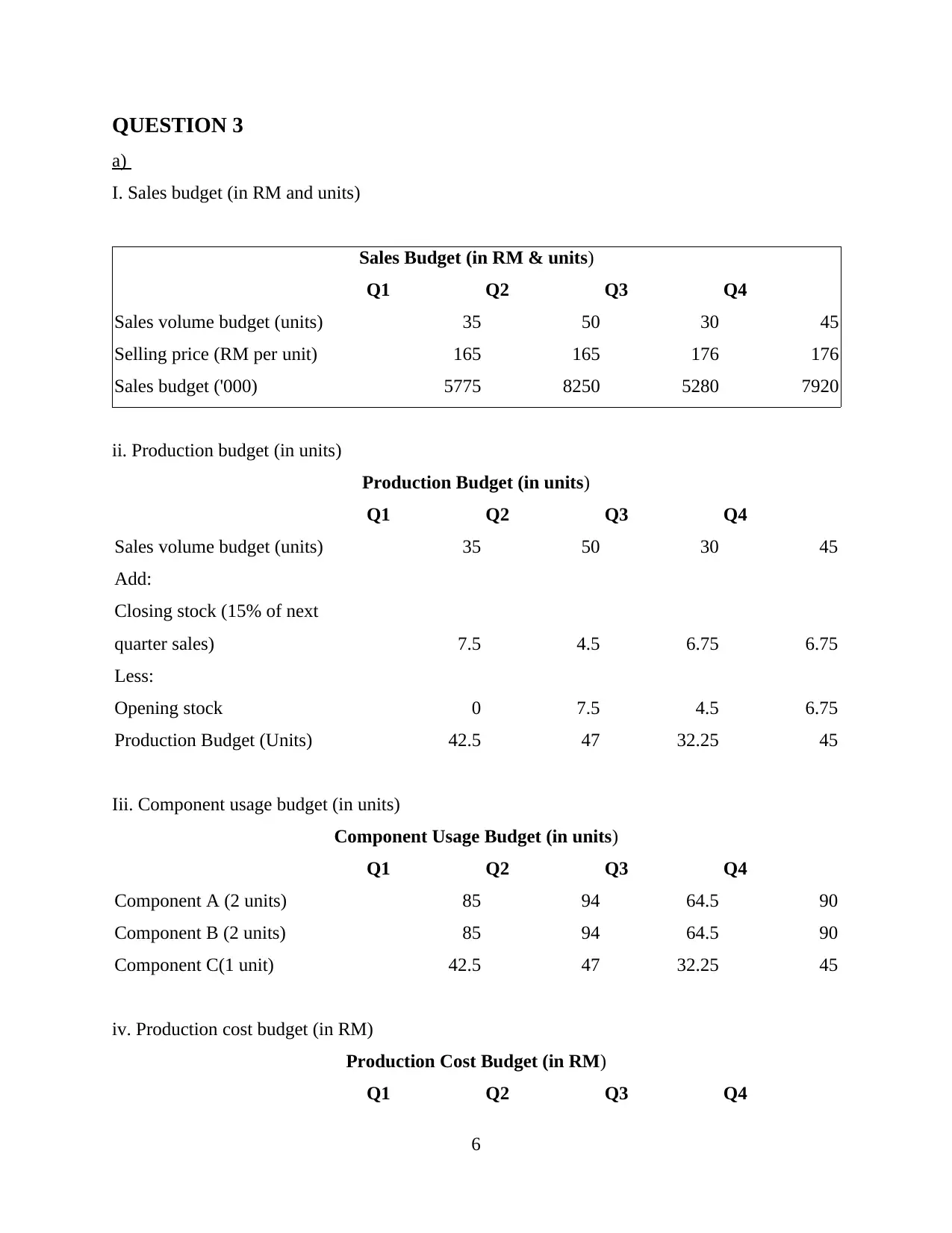

QUESTION 3

a)

I. Sales budget (in RM and units)

Sales Budget (in RM & units)

Q1 Q2 Q3 Q4

Sales volume budget (units) 35 50 30 45

Selling price (RM per unit) 165 165 176 176

Sales budget ('000) 5775 8250 5280 7920

ii. Production budget (in units)

Production Budget (in units)

Q1 Q2 Q3 Q4

Sales volume budget (units) 35 50 30 45

Add:

Closing stock (15% of next

quarter sales) 7.5 4.5 6.75 6.75

Less:

Opening stock 0 7.5 4.5 6.75

Production Budget (Units) 42.5 47 32.25 45

Iii. Component usage budget (in units)

Component Usage Budget (in units)

Q1 Q2 Q3 Q4

Component A (2 units) 85 94 64.5 90

Component B (2 units) 85 94 64.5 90

Component C(1 unit) 42.5 47 32.25 45

iv. Production cost budget (in RM)

Production Cost Budget (in RM)

Q1 Q2 Q3 Q4

6

a)

I. Sales budget (in RM and units)

Sales Budget (in RM & units)

Q1 Q2 Q3 Q4

Sales volume budget (units) 35 50 30 45

Selling price (RM per unit) 165 165 176 176

Sales budget ('000) 5775 8250 5280 7920

ii. Production budget (in units)

Production Budget (in units)

Q1 Q2 Q3 Q4

Sales volume budget (units) 35 50 30 45

Add:

Closing stock (15% of next

quarter sales) 7.5 4.5 6.75 6.75

Less:

Opening stock 0 7.5 4.5 6.75

Production Budget (Units) 42.5 47 32.25 45

Iii. Component usage budget (in units)

Component Usage Budget (in units)

Q1 Q2 Q3 Q4

Component A (2 units) 85 94 64.5 90

Component B (2 units) 85 94 64.5 90

Component C(1 unit) 42.5 47 32.25 45

iv. Production cost budget (in RM)

Production Cost Budget (in RM)

Q1 Q2 Q3 Q4

6

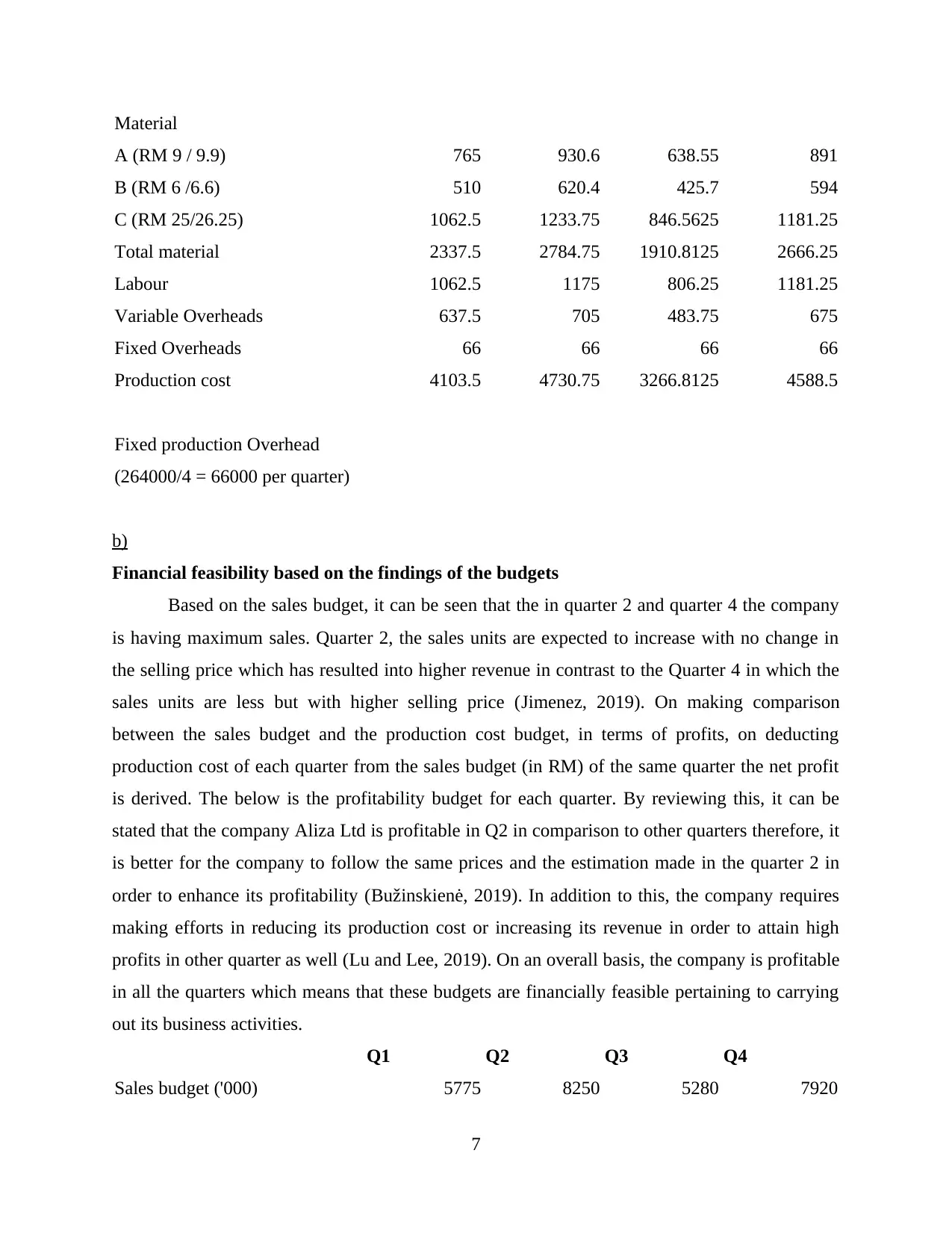

Material

A (RM 9 / 9.9) 765 930.6 638.55 891

B (RM 6 /6.6) 510 620.4 425.7 594

C (RM 25/26.25) 1062.5 1233.75 846.5625 1181.25

Total material 2337.5 2784.75 1910.8125 2666.25

Labour 1062.5 1175 806.25 1181.25

Variable Overheads 637.5 705 483.75 675

Fixed Overheads 66 66 66 66

Production cost 4103.5 4730.75 3266.8125 4588.5

Fixed production Overhead

(264000/4 = 66000 per quarter)

b)

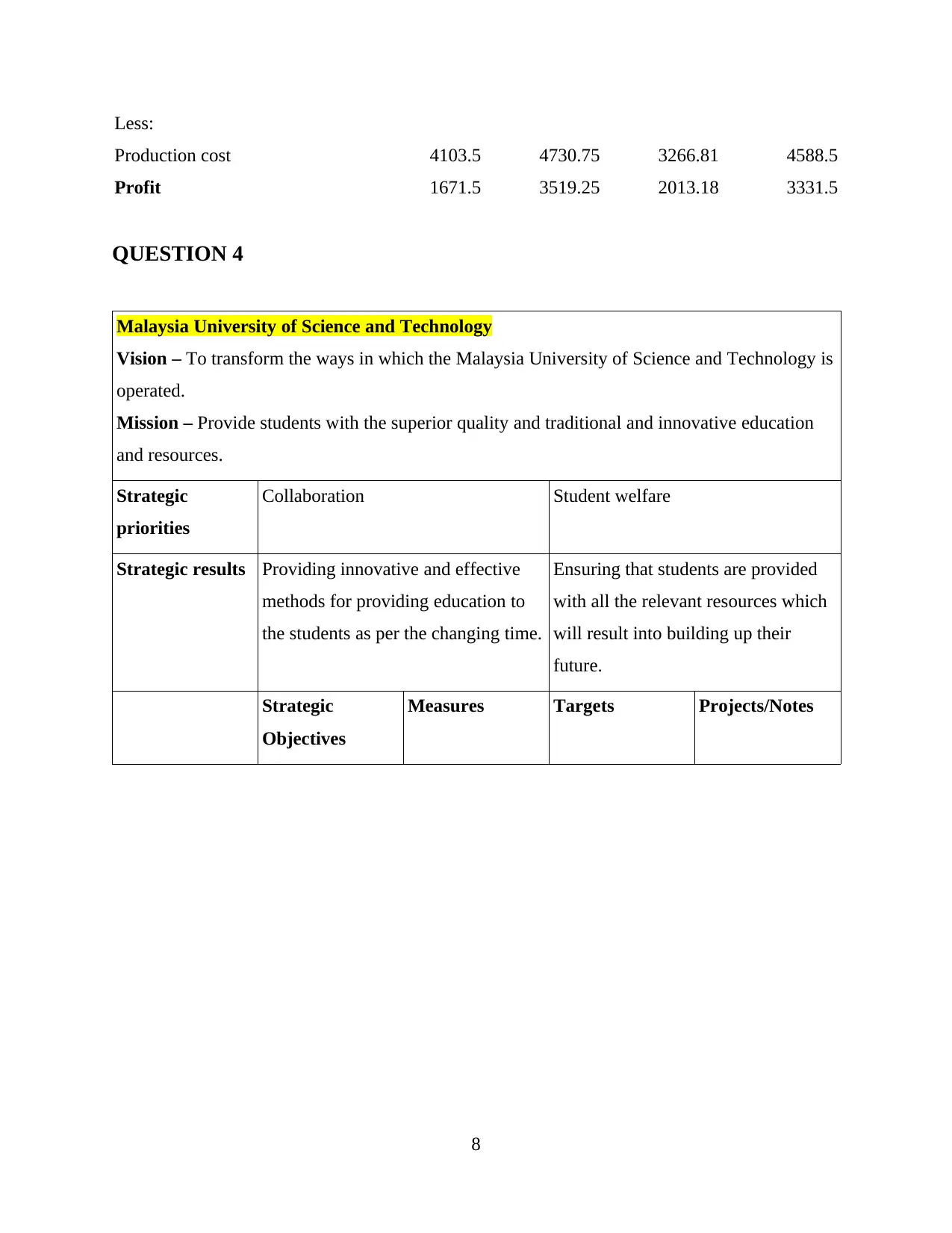

Financial feasibility based on the findings of the budgets

Based on the sales budget, it can be seen that the in quarter 2 and quarter 4 the company

is having maximum sales. Quarter 2, the sales units are expected to increase with no change in

the selling price which has resulted into higher revenue in contrast to the Quarter 4 in which the

sales units are less but with higher selling price (Jimenez, 2019). On making comparison

between the sales budget and the production cost budget, in terms of profits, on deducting

production cost of each quarter from the sales budget (in RM) of the same quarter the net profit

is derived. The below is the profitability budget for each quarter. By reviewing this, it can be

stated that the company Aliza Ltd is profitable in Q2 in comparison to other quarters therefore, it

is better for the company to follow the same prices and the estimation made in the quarter 2 in

order to enhance its profitability (Bužinskienė, 2019). In addition to this, the company requires

making efforts in reducing its production cost or increasing its revenue in order to attain high

profits in other quarter as well (Lu and Lee, 2019). On an overall basis, the company is profitable

in all the quarters which means that these budgets are financially feasible pertaining to carrying

out its business activities.

Q1 Q2 Q3 Q4

Sales budget ('000) 5775 8250 5280 7920

7

A (RM 9 / 9.9) 765 930.6 638.55 891

B (RM 6 /6.6) 510 620.4 425.7 594

C (RM 25/26.25) 1062.5 1233.75 846.5625 1181.25

Total material 2337.5 2784.75 1910.8125 2666.25

Labour 1062.5 1175 806.25 1181.25

Variable Overheads 637.5 705 483.75 675

Fixed Overheads 66 66 66 66

Production cost 4103.5 4730.75 3266.8125 4588.5

Fixed production Overhead

(264000/4 = 66000 per quarter)

b)

Financial feasibility based on the findings of the budgets

Based on the sales budget, it can be seen that the in quarter 2 and quarter 4 the company

is having maximum sales. Quarter 2, the sales units are expected to increase with no change in

the selling price which has resulted into higher revenue in contrast to the Quarter 4 in which the

sales units are less but with higher selling price (Jimenez, 2019). On making comparison

between the sales budget and the production cost budget, in terms of profits, on deducting

production cost of each quarter from the sales budget (in RM) of the same quarter the net profit

is derived. The below is the profitability budget for each quarter. By reviewing this, it can be

stated that the company Aliza Ltd is profitable in Q2 in comparison to other quarters therefore, it

is better for the company to follow the same prices and the estimation made in the quarter 2 in

order to enhance its profitability (Bužinskienė, 2019). In addition to this, the company requires

making efforts in reducing its production cost or increasing its revenue in order to attain high

profits in other quarter as well (Lu and Lee, 2019). On an overall basis, the company is profitable

in all the quarters which means that these budgets are financially feasible pertaining to carrying

out its business activities.

Q1 Q2 Q3 Q4

Sales budget ('000) 5775 8250 5280 7920

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less:

Production cost 4103.5 4730.75 3266.81 4588.5

Profit 1671.5 3519.25 2013.18 3331.5

QUESTION 4

Malaysia University of Science and Technology

Vision – To transform the ways in which the Malaysia University of Science and Technology is

operated.

Mission – Provide students with the superior quality and traditional and innovative education

and resources.

Strategic

priorities

Collaboration Student welfare

Strategic results Providing innovative and effective

methods for providing education to

the students as per the changing time.

Ensuring that students are provided

with all the relevant resources which

will result into building up their

future.

Strategic

Objectives

Measures Targets Projects/Notes

8

Production cost 4103.5 4730.75 3266.81 4588.5

Profit 1671.5 3519.25 2013.18 3331.5

QUESTION 4

Malaysia University of Science and Technology

Vision – To transform the ways in which the Malaysia University of Science and Technology is

operated.

Mission – Provide students with the superior quality and traditional and innovative education

and resources.

Strategic

priorities

Collaboration Student welfare

Strategic results Providing innovative and effective

methods for providing education to

the students as per the changing time.

Ensuring that students are provided

with all the relevant resources which

will result into building up their

future.

Strategic

Objectives

Measures Targets Projects/Notes

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To

increase

sales by

providing

relevant

and

differentia

ted

services.

To reduce

the cost of

operation

by

eliminatin

g

unnecessa

ry

expenditur

e.

Net profit

Operation

al cost

Attaining

target

revenue

10%

increase

20%

decrease

5%

increase

Implement

ing the

latest

accountin

g system.

Hiring

personnel

experience

d in

handling

finances

9

Financia

l

increase

sales by

providing

relevant

and

differentia

ted

services.

To reduce

the cost of

operation

by

eliminatin

g

unnecessa

ry

expenditur

e.

Net profit

Operation

al cost

Attaining

target

revenue

10%

increase

20%

decrease

5%

increase

Implement

ing the

latest

accountin

g system.

Hiring

personnel

experience

d in

handling

finances

9

Financia

l

Improving

the

students

experience

by

providing

clean and

hygienic

surroundin

g and

polite and

friendly

interaction

.

Retaining

students

by

recognizin

g their

achieveme

nt through

awards

and public

appreciati

on.

Student

satisfactio

n survey

Students

rating on

all

dimension

s

95%

student

satisfactio

n rating

Average

rating A

on all the

dimension

s

Creation

and

developm

ent of the

s

environme

nt which

will help

in

encouragi

ng and

motivating

the

students.

Offering

programm

es which

will help

in the

future.

Improving

the

efficiency

by

effectively

meeting

Meeting

with

student

queries

Pounds of

100%

accuracy

in

resolving

10%

reduction

Creating a

better

selection

process of

the

manageme

10

Custom

er/

student

Internal

process

es

the

students

experience

by

providing

clean and

hygienic

surroundin

g and

polite and

friendly

interaction

.

Retaining

students

by

recognizin

g their

achieveme

nt through

awards

and public

appreciati

on.

Student

satisfactio

n survey

Students

rating on

all

dimension

s

95%

student

satisfactio

n rating

Average

rating A

on all the

dimension

s

Creation

and

developm

ent of the

s

environme

nt which

will help

in

encouragi

ng and

motivating

the

students.

Offering

programm

es which

will help

in the

future.

Improving

the

efficiency

by

effectively

meeting

Meeting

with

student

queries

Pounds of

100%

accuracy

in

resolving

10%

reduction

Creating a

better

selection

process of

the

manageme

10

Custom

er/

student

Internal

process

es

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.