Management Accounting 3: Budgeting and Performance Analysis Solution

VerifiedAdded on 2021/06/16

|10

|2267

|16

Homework Assignment

AI Summary

This document presents a comprehensive solution to a management accounting assignment. Part A focuses on preparing a master budget, including manufacturing overhead, purchase, and direct material budgets. Part B provides an analysis of a new manufacturing facility investment, evaluating its impact on costs, sales, and cash flow through various budgets and financial statements, including a cost of goods manufactured statement and cash flow analysis. The analysis considers the financial implications of the investment for Heidegger Pty Ltd. Part C delves into the behavioral aspects of budgeting, comparing imposed and participatory budgeting approaches. It examines the implications of each approach on employee motivation, communication, and goal congruence, concluding that participatory budgeting is more effective in addressing behavioral concerns and promoting organizational performance. The solution utilizes flexible budgeting formulas and provides detailed calculations and analysis to support its conclusions.

Running head: MANAGEMENT ACCOUNTING

Management accounting

University Name

Student Name

Authors’ Note

Management accounting

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2MANAGEMENT ACCOUNTING

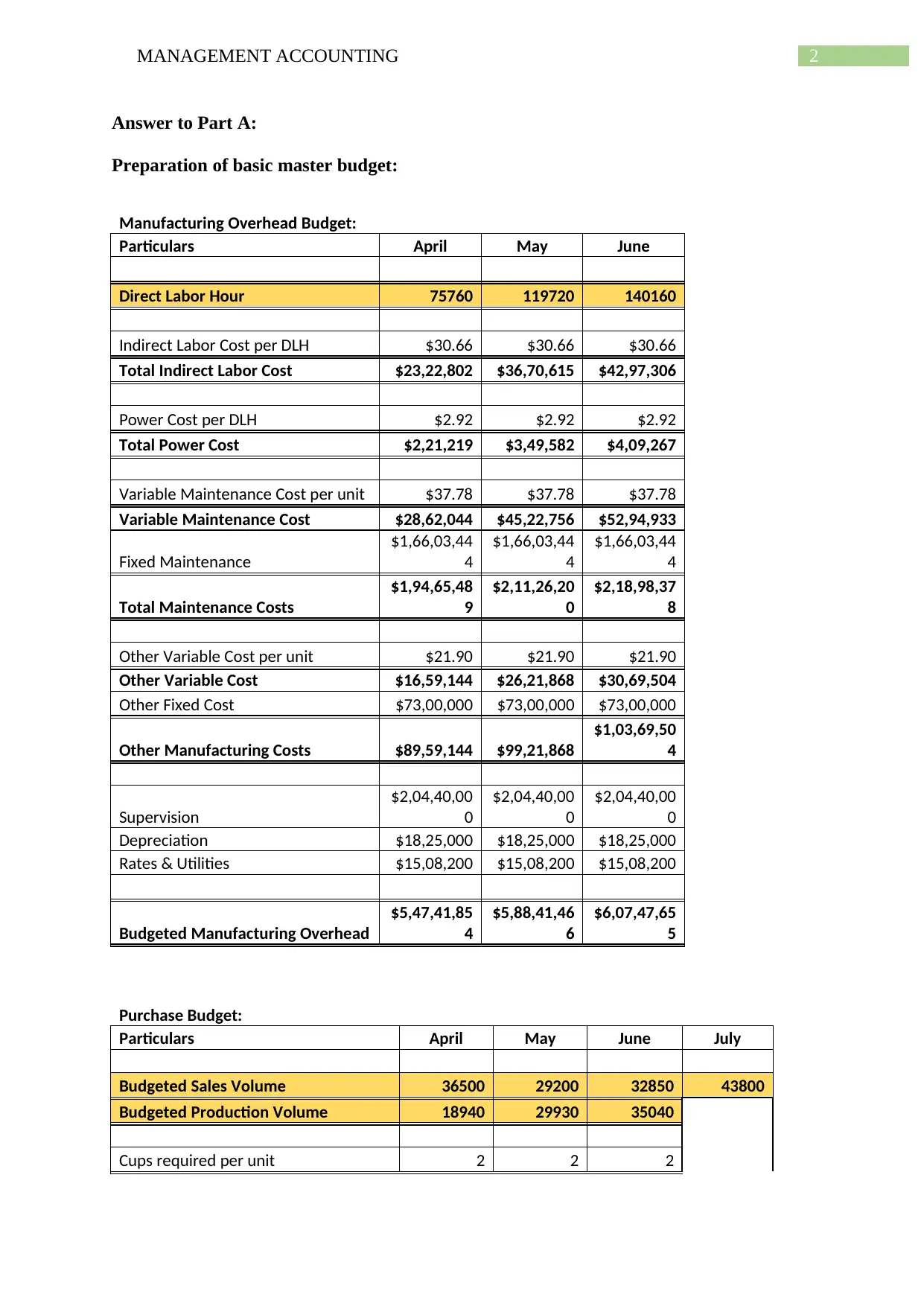

Answer to Part A:

Preparation of basic master budget:

Manufacturing Overhead Budget:

Particulars April May June

Direct Labor Hour 75760 119720 140160

Indirect Labor Cost per DLH $30.66 $30.66 $30.66

Total Indirect Labor Cost $23,22,802 $36,70,615 $42,97,306

Power Cost per DLH $2.92 $2.92 $2.92

Total Power Cost $2,21,219 $3,49,582 $4,09,267

Variable Maintenance Cost per unit $37.78 $37.78 $37.78

Variable Maintenance Cost $28,62,044 $45,22,756 $52,94,933

Fixed Maintenance

$1,66,03,44

4

$1,66,03,44

4

$1,66,03,44

4

Total Maintenance Costs

$1,94,65,48

9

$2,11,26,20

0

$2,18,98,37

8

Other Variable Cost per unit $21.90 $21.90 $21.90

Other Variable Cost $16,59,144 $26,21,868 $30,69,504

Other Fixed Cost $73,00,000 $73,00,000 $73,00,000

Other Manufacturing Costs $89,59,144 $99,21,868

$1,03,69,50

4

Supervision

$2,04,40,00

0

$2,04,40,00

0

$2,04,40,00

0

Depreciation $18,25,000 $18,25,000 $18,25,000

Rates & Utilities $15,08,200 $15,08,200 $15,08,200

Budgeted Manufacturing Overhead

$5,47,41,85

4

$5,88,41,46

6

$6,07,47,65

5

Purchase Budget:

Particulars April May June July

Budgeted Sales Volume 36500 29200 32850 43800

Budgeted Production Volume 18940 29930 35040

Cups required per unit 2 2 2

Answer to Part A:

Preparation of basic master budget:

Manufacturing Overhead Budget:

Particulars April May June

Direct Labor Hour 75760 119720 140160

Indirect Labor Cost per DLH $30.66 $30.66 $30.66

Total Indirect Labor Cost $23,22,802 $36,70,615 $42,97,306

Power Cost per DLH $2.92 $2.92 $2.92

Total Power Cost $2,21,219 $3,49,582 $4,09,267

Variable Maintenance Cost per unit $37.78 $37.78 $37.78

Variable Maintenance Cost $28,62,044 $45,22,756 $52,94,933

Fixed Maintenance

$1,66,03,44

4

$1,66,03,44

4

$1,66,03,44

4

Total Maintenance Costs

$1,94,65,48

9

$2,11,26,20

0

$2,18,98,37

8

Other Variable Cost per unit $21.90 $21.90 $21.90

Other Variable Cost $16,59,144 $26,21,868 $30,69,504

Other Fixed Cost $73,00,000 $73,00,000 $73,00,000

Other Manufacturing Costs $89,59,144 $99,21,868

$1,03,69,50

4

Supervision

$2,04,40,00

0

$2,04,40,00

0

$2,04,40,00

0

Depreciation $18,25,000 $18,25,000 $18,25,000

Rates & Utilities $15,08,200 $15,08,200 $15,08,200

Budgeted Manufacturing Overhead

$5,47,41,85

4

$5,88,41,46

6

$6,07,47,65

5

Purchase Budget:

Particulars April May June July

Budgeted Sales Volume 36500 29200 32850 43800

Budgeted Production Volume 18940 29930 35040

Cups required per unit 2 2 2

3MANAGEMENT ACCOUNTING

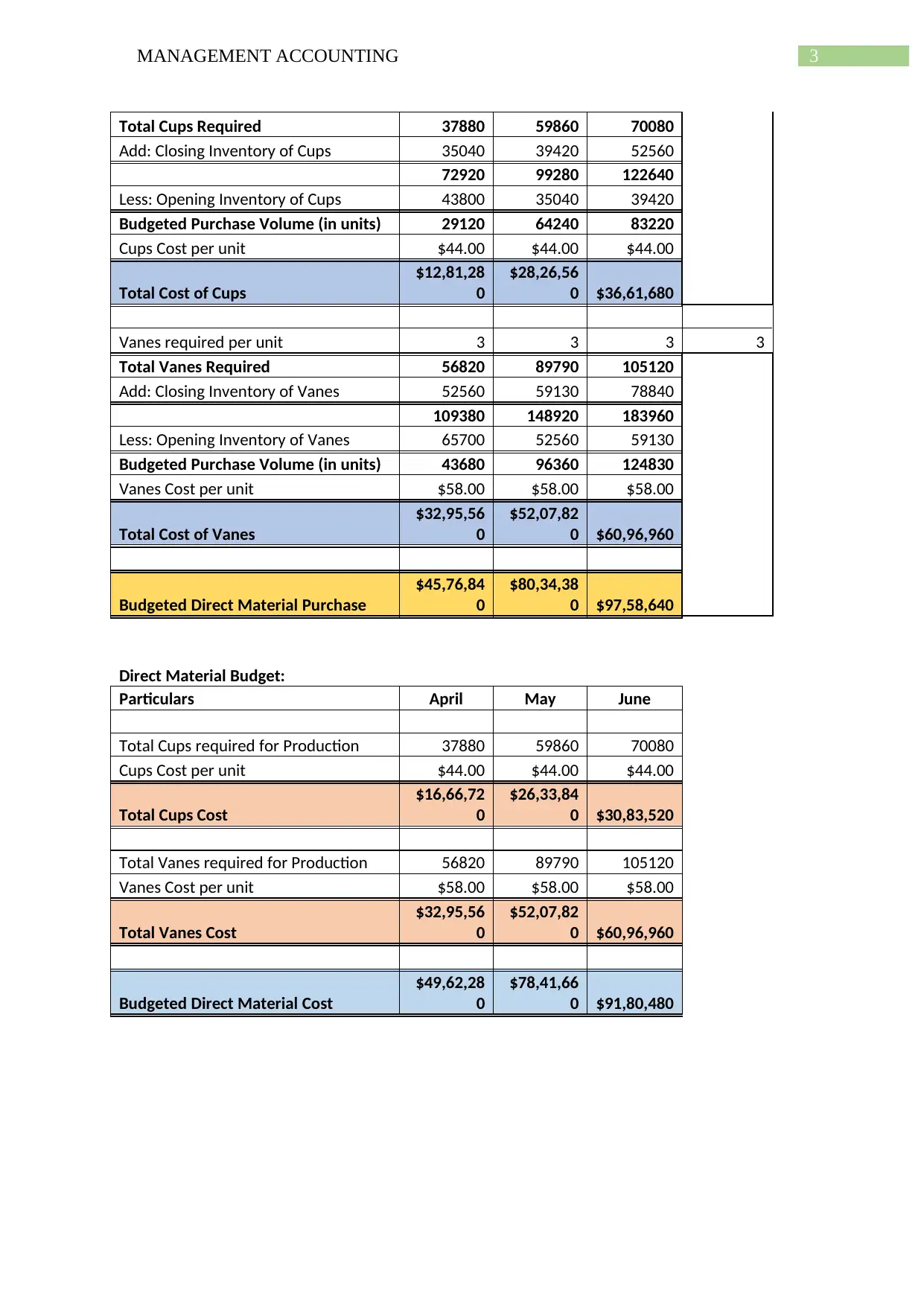

Total Cups Required 37880 59860 70080

Add: Closing Inventory of Cups 35040 39420 52560

72920 99280 122640

Less: Opening Inventory of Cups 43800 35040 39420

Budgeted Purchase Volume (in units) 29120 64240 83220

Cups Cost per unit $44.00 $44.00 $44.00

Total Cost of Cups

$12,81,28

0

$28,26,56

0 $36,61,680

Vanes required per unit 3 3 3 3

Total Vanes Required 56820 89790 105120

Add: Closing Inventory of Vanes 52560 59130 78840

109380 148920 183960

Less: Opening Inventory of Vanes 65700 52560 59130

Budgeted Purchase Volume (in units) 43680 96360 124830

Vanes Cost per unit $58.00 $58.00 $58.00

Total Cost of Vanes

$32,95,56

0

$52,07,82

0 $60,96,960

Budgeted Direct Material Purchase

$45,76,84

0

$80,34,38

0 $97,58,640

Direct Material Budget:

Particulars April May June

Total Cups required for Production 37880 59860 70080

Cups Cost per unit $44.00 $44.00 $44.00

Total Cups Cost

$16,66,72

0

$26,33,84

0 $30,83,520

Total Vanes required for Production 56820 89790 105120

Vanes Cost per unit $58.00 $58.00 $58.00

Total Vanes Cost

$32,95,56

0

$52,07,82

0 $60,96,960

Budgeted Direct Material Cost

$49,62,28

0

$78,41,66

0 $91,80,480

Total Cups Required 37880 59860 70080

Add: Closing Inventory of Cups 35040 39420 52560

72920 99280 122640

Less: Opening Inventory of Cups 43800 35040 39420

Budgeted Purchase Volume (in units) 29120 64240 83220

Cups Cost per unit $44.00 $44.00 $44.00

Total Cost of Cups

$12,81,28

0

$28,26,56

0 $36,61,680

Vanes required per unit 3 3 3 3

Total Vanes Required 56820 89790 105120

Add: Closing Inventory of Vanes 52560 59130 78840

109380 148920 183960

Less: Opening Inventory of Vanes 65700 52560 59130

Budgeted Purchase Volume (in units) 43680 96360 124830

Vanes Cost per unit $58.00 $58.00 $58.00

Total Cost of Vanes

$32,95,56

0

$52,07,82

0 $60,96,960

Budgeted Direct Material Purchase

$45,76,84

0

$80,34,38

0 $97,58,640

Direct Material Budget:

Particulars April May June

Total Cups required for Production 37880 59860 70080

Cups Cost per unit $44.00 $44.00 $44.00

Total Cups Cost

$16,66,72

0

$26,33,84

0 $30,83,520

Total Vanes required for Production 56820 89790 105120

Vanes Cost per unit $58.00 $58.00 $58.00

Total Vanes Cost

$32,95,56

0

$52,07,82

0 $60,96,960

Budgeted Direct Material Cost

$49,62,28

0

$78,41,66

0 $91,80,480

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4MANAGEMENT ACCOUNTING

Answer to Part B:

Introduction:

The report is prepared to address the concerns of the sales manager of Heidegger Pty

Ltd of the new manufacturing facility. Making investment in new production facility will

enable organization to manufacture anemometers that is used in the production of wind

power energy generated equipment. The current market for the equipment of alternative

power generation is uncertain and volatile and in light of this volatility and uncertainty,

introduction of new manufacturing facility will help in addressing such issues. There are two

parts in which the manufacturing will be carried out under this facility, the assembly will be

purchased and the assembly process that is somewhat labour intensive will be significantly

automated (Bromwic and Scapens 2016). Furthermore, the impact of intended investment in

the new production capacity has been evaluated that is supported by relevant calculations.

Discussion:

The new manufacturing facility is implemented with the deliberation of reduction in

material cost and direct labour cost. However, it is projected that the new manufacturing

facility will increase the fixed manufacturing overhead resulting from increased investment

made in the production facility. For the preparation of various budgets, Heidegger Pty Ltd

will make use of flexible budgeting formula. Some of the budgets that are prepared include

direct labour budget, direct material budget, direct labour budget, cost of goods manufactured

statement, cash collection from debtors account and budgetary income statement. There is

likelihood that fixed manufacturing overhead will increase by 50% and reduce labour and

direct cost by 25% due to increased investment in production capacity (Tappura et al. 2015).

From the sales budget, it can be seen that the budgeted sales revenue initially reduced

from $ 134685000 to $ 121216500 and thereafter it increased to $ 161622000. Volume of

Answer to Part B:

Introduction:

The report is prepared to address the concerns of the sales manager of Heidegger Pty

Ltd of the new manufacturing facility. Making investment in new production facility will

enable organization to manufacture anemometers that is used in the production of wind

power energy generated equipment. The current market for the equipment of alternative

power generation is uncertain and volatile and in light of this volatility and uncertainty,

introduction of new manufacturing facility will help in addressing such issues. There are two

parts in which the manufacturing will be carried out under this facility, the assembly will be

purchased and the assembly process that is somewhat labour intensive will be significantly

automated (Bromwic and Scapens 2016). Furthermore, the impact of intended investment in

the new production capacity has been evaluated that is supported by relevant calculations.

Discussion:

The new manufacturing facility is implemented with the deliberation of reduction in

material cost and direct labour cost. However, it is projected that the new manufacturing

facility will increase the fixed manufacturing overhead resulting from increased investment

made in the production facility. For the preparation of various budgets, Heidegger Pty Ltd

will make use of flexible budgeting formula. Some of the budgets that are prepared include

direct labour budget, direct material budget, direct labour budget, cost of goods manufactured

statement, cash collection from debtors account and budgetary income statement. There is

likelihood that fixed manufacturing overhead will increase by 50% and reduce labour and

direct cost by 25% due to increased investment in production capacity (Tappura et al. 2015).

From the sales budget, it can be seen that the budgeted sales revenue initially reduced

from $ 134685000 to $ 121216500 and thereafter it increased to $ 161622000. Volume of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5MANAGEMENT ACCOUNTING

budgeted production has increased significantly from 18940 in first month of operation to

35040 in third month of operation. In addition to this, there is considerable increase in

budgeted direct labour cost from $ 2272800 in month of April to $ 4204800 in month of June.

It is depicted from the production budget that the budgeted volume of production has

increased considerably. On other hand, the budgeted sales volume has initially reduced from

$ 36500 to $ 29200 and further the volume has increased significantly to $ 43800. The total

cost of cups has increased to $ 3661680 as against $ 1281280 initially. Furthermore, there has

been phenomenal increase in budgeted direct material purchase from $ 4576840 to $ 8034380

and further to $ 9758640. Therefore, it can be inferred from the analysis of several budgets

that with the introduction of new manufacturing facility, there is significant increase in direct

material cost, direct material purchase, direct labour cost, production volume and sales

volume (Mårtensson et al. 2016).

The budgeted manufacturing overhead has increased from $ 54741854 to $ 60747655

as revealed by the manufacturing overhead budget. It can also be noticed that direct labour

hour and indirect labour cost has increased since the month of operation (Kokubu and Kitada

2015). Furthermore, there has also been increase in total and variable maintenance cost.

In addition to this, the collection from debtors has initially increased from $

117073800 to $ 126603900 and thereafter the value has reduced to $ 108286470. The cash

payment for administration and selling expenses, the amount stood at $ 31031550 in first

month of operation to $ 23980500 in second month of operation and the amount stood at $

27853515 in third month of operation.

The cash budget prepared by organization depicts the net cash generated from

operating, financing and investing activities. Net cash flow from operating activities has

increased from $ 26275756 in first month of operation to $ 31545554 in second month of

budgeted production has increased significantly from 18940 in first month of operation to

35040 in third month of operation. In addition to this, there is considerable increase in

budgeted direct labour cost from $ 2272800 in month of April to $ 4204800 in month of June.

It is depicted from the production budget that the budgeted volume of production has

increased considerably. On other hand, the budgeted sales volume has initially reduced from

$ 36500 to $ 29200 and further the volume has increased significantly to $ 43800. The total

cost of cups has increased to $ 3661680 as against $ 1281280 initially. Furthermore, there has

been phenomenal increase in budgeted direct material purchase from $ 4576840 to $ 8034380

and further to $ 9758640. Therefore, it can be inferred from the analysis of several budgets

that with the introduction of new manufacturing facility, there is significant increase in direct

material cost, direct material purchase, direct labour cost, production volume and sales

volume (Mårtensson et al. 2016).

The budgeted manufacturing overhead has increased from $ 54741854 to $ 60747655

as revealed by the manufacturing overhead budget. It can also be noticed that direct labour

hour and indirect labour cost has increased since the month of operation (Kokubu and Kitada

2015). Furthermore, there has also been increase in total and variable maintenance cost.

In addition to this, the collection from debtors has initially increased from $

117073800 to $ 126603900 and thereafter the value has reduced to $ 108286470. The cash

payment for administration and selling expenses, the amount stood at $ 31031550 in first

month of operation to $ 23980500 in second month of operation and the amount stood at $

27853515 in third month of operation.

The cash budget prepared by organization depicts the net cash generated from

operating, financing and investing activities. Net cash flow from operating activities has

increased from $ 26275756 in first month of operation to $ 31545554 in second month of

6MANAGEMENT ACCOUNTING

operation and thereafter it has reduced drastically to $ 4807305. No cash flow has been

generated from financing activities in second and third month of operations. The closing cash

balance has increases month on month from $ 27454706 to $ 40020261 and further to $

44827566.

Now, the value of net operating income will form the basis whether the project should

be undertaken or not. It can be seen from cost of goods sold manufacturing statement that the

cost of goods manufactured has increased. However, the per unit cost of goods manufactured

has reduced. There has been increase in gross profit along with increase in net operating

income. Nevertheless, the total amount of net operating income is negative (Wouters and

Kirchberger 2015).

Conclusion:

From the evaluation of new manufacturing facility in terms of sales volume and

material and labour cost, it can be seen that there is no change in percentage of sales made.

Moreover, fixed manufacturing overhead has increased. Therefore, it would not be viable to

undertake investment in new manufacturing facility as the total net income generated is

negative.

Answer to Part C:

Budget preparation can have considerable impact on the behaviour of human

and overall performance of organization. The approach of imposed budgeting involve senior

level management who has the responsibility of facilitating the process of decision making by

setting parameters for achieving desirable targets. Lower or middle level employees are

involved in the computation of budgetary elements but have little say in the decision making.

Under this method, the management does not make effective human resource utilization.

operation and thereafter it has reduced drastically to $ 4807305. No cash flow has been

generated from financing activities in second and third month of operations. The closing cash

balance has increases month on month from $ 27454706 to $ 40020261 and further to $

44827566.

Now, the value of net operating income will form the basis whether the project should

be undertaken or not. It can be seen from cost of goods sold manufacturing statement that the

cost of goods manufactured has increased. However, the per unit cost of goods manufactured

has reduced. There has been increase in gross profit along with increase in net operating

income. Nevertheless, the total amount of net operating income is negative (Wouters and

Kirchberger 2015).

Conclusion:

From the evaluation of new manufacturing facility in terms of sales volume and

material and labour cost, it can be seen that there is no change in percentage of sales made.

Moreover, fixed manufacturing overhead has increased. Therefore, it would not be viable to

undertake investment in new manufacturing facility as the total net income generated is

negative.

Answer to Part C:

Budget preparation can have considerable impact on the behaviour of human

and overall performance of organization. The approach of imposed budgeting involve senior

level management who has the responsibility of facilitating the process of decision making by

setting parameters for achieving desirable targets. Lower or middle level employees are

involved in the computation of budgetary elements but have little say in the decision making.

Under this method, the management does not make effective human resource utilization.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7MANAGEMENT ACCOUNTING

Effective budget requires input in the form of financial and non financial information from all

the departments so that it covers broad range of aspects. This would make the budgetary

system reliable. Imposed budget might permit much budgetary slack if such budgets are not

properly scrutinized and such slack would create waste and inefficiency (Chiwamit et al.

2017). Therefore, before accepting the outcomes of such budgets, it is required that such

budgets should be reviewed carefully.

Participatory approach of budgeting on other hand involves active participation of

employees at all levels from different departments. Such budget intends to provide benefits in

terms attitude and performance of preparers of budgets. The implications of participatory

budget are measured in terms of congruency of goals, communication and motivation. There

is increased involvement from employees and increased flow of communication because of

participation of employees from different level of management. Organization is able to set

realistic targets by preparing a well designed budget involving employee’s participation.

Participatory budgetary approach helps in encouraging goals congruency and prevention of

any undesirable behaviour on part of employees (Chenhall & Moers 2015). Moreover,

behaviour implication in terms of motivation is generally higher when there is participation

from individual employees in setting his or her budgetary goals.

Analyzing both types of budget that is imposed as well as participatory budget, it can

be inferred that behavioural concerns of employee are addressed using the later budgetary

approach. The reason is attributable to the fact that the imposed budget does not facilitate

flow of communication between employees of different departments. Favourable outcome

will be produced by budget if the preparation of budget involves employees from upper to

lower level of management along with staffs and employees. Participatory budget will help in

addressing the issues experienced by the employees at behavioural level. In addition to this,

the performance of managers is evaluated by using the participative approach. Therefore, the

Effective budget requires input in the form of financial and non financial information from all

the departments so that it covers broad range of aspects. This would make the budgetary

system reliable. Imposed budget might permit much budgetary slack if such budgets are not

properly scrutinized and such slack would create waste and inefficiency (Chiwamit et al.

2017). Therefore, before accepting the outcomes of such budgets, it is required that such

budgets should be reviewed carefully.

Participatory approach of budgeting on other hand involves active participation of

employees at all levels from different departments. Such budget intends to provide benefits in

terms attitude and performance of preparers of budgets. The implications of participatory

budget are measured in terms of congruency of goals, communication and motivation. There

is increased involvement from employees and increased flow of communication because of

participation of employees from different level of management. Organization is able to set

realistic targets by preparing a well designed budget involving employee’s participation.

Participatory budgetary approach helps in encouraging goals congruency and prevention of

any undesirable behaviour on part of employees (Chenhall & Moers 2015). Moreover,

behaviour implication in terms of motivation is generally higher when there is participation

from individual employees in setting his or her budgetary goals.

Analyzing both types of budget that is imposed as well as participatory budget, it can

be inferred that behavioural concerns of employee are addressed using the later budgetary

approach. The reason is attributable to the fact that the imposed budget does not facilitate

flow of communication between employees of different departments. Favourable outcome

will be produced by budget if the preparation of budget involves employees from upper to

lower level of management along with staffs and employees. Participatory budget will help in

addressing the issues experienced by the employees at behavioural level. In addition to this,

the performance of managers is evaluated by using the participative approach. Therefore, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8MANAGEMENT ACCOUNTING

preparation of budget is considered desirable if it involves participation from top as well as

lower level of management. Budgets should be created in such a way that it receives

contribution from management in preparation of budget. Detailed budgeted data is provided

if the participation is sought from subordinates who are involved in day to day operations

(Cleary 2015).

Reference list:

Bromwich, M. and Scapens, R.W., 2016. Management accounting research: 25 years

on. Management Accounting Research, 31, pp.1-9.

preparation of budget is considered desirable if it involves participation from top as well as

lower level of management. Budgets should be created in such a way that it receives

contribution from management in preparation of budget. Detailed budgeted data is provided

if the participation is sought from subordinates who are involved in day to day operations

(Cleary 2015).

Reference list:

Bromwich, M. and Scapens, R.W., 2016. Management accounting research: 25 years

on. Management Accounting Research, 31, pp.1-9.

9MANAGEMENT ACCOUNTING

Chenhall, R. H., & Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, Organizations and

Society, 47, 1-13.

Chiwamit, P., Modell, S., & Scapens, R. W., 2017. Regulation and adaptation of management

accounting innovations: The case of economic value added in Thai state-owned

enterprises. Management Accounting Research, 37, 30-48.

Cleary, P., 2015. An empirical investigation of the impact of management accounting on

structural capital and business performance. Journal of Intellectual Capital, 16(3), pp.566-

586.

Fullerton, R. R., Kennedy, F. A., & Widener, S. K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7-8), 414-428.

Hopper, T., & Bui, B., 2016. Has management accounting research been

critical?. Management Accounting Research, 31, 10-30.

Horton, K.E. and de Araujo Wanderley, C., 2016. Identity conflict and the paradox of

embedded agency in the management accounting profession: adding a new piece to the

theoretical jigsaw. Management Accounting Research.

Kokubu, K. and Kitada, H., 2015. Material flow cost accounting and existing management

perspectives. Journal of Cleaner Production, 108, pp.1279-1288.

Mårtensson, M., Höglund, L., Holmgren Caicedo, M. and Svärdsten, F., 2016. Management

accounting of control practices: a matter of and for strategy. In the 9TH INTERNATIONAL

EIASM PUBLIC SECTOR CONFERENCE, held in LISBON, PORTUGAL, SEPTEMBER 6-

8, 2016..

Chenhall, R. H., & Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, Organizations and

Society, 47, 1-13.

Chiwamit, P., Modell, S., & Scapens, R. W., 2017. Regulation and adaptation of management

accounting innovations: The case of economic value added in Thai state-owned

enterprises. Management Accounting Research, 37, 30-48.

Cleary, P., 2015. An empirical investigation of the impact of management accounting on

structural capital and business performance. Journal of Intellectual Capital, 16(3), pp.566-

586.

Fullerton, R. R., Kennedy, F. A., & Widener, S. K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7-8), 414-428.

Hopper, T., & Bui, B., 2016. Has management accounting research been

critical?. Management Accounting Research, 31, 10-30.

Horton, K.E. and de Araujo Wanderley, C., 2016. Identity conflict and the paradox of

embedded agency in the management accounting profession: adding a new piece to the

theoretical jigsaw. Management Accounting Research.

Kokubu, K. and Kitada, H., 2015. Material flow cost accounting and existing management

perspectives. Journal of Cleaner Production, 108, pp.1279-1288.

Mårtensson, M., Höglund, L., Holmgren Caicedo, M. and Svärdsten, F., 2016. Management

accounting of control practices: a matter of and for strategy. In the 9TH INTERNATIONAL

EIASM PUBLIC SECTOR CONFERENCE, held in LISBON, PORTUGAL, SEPTEMBER 6-

8, 2016..

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10MANAGEMENT ACCOUNTING

McLean, T., McGovern, T. and Davie, S., 2015. Management accounting, engineering and

the management of company growth: Clarke Chapman, 1864–1914. The British Accounting

Review, 47(2), pp.177-190.

Messner, M., 2016. Does industry matter? How industry context shapes management

accounting practice. Management Accounting Research, 31, 103-111.

Tappura, S., Sievänen, M., Heikkilä, J., Jussila, A. and Nenonen, N., 2015. A management

accounting perspective on safety. Safety science, 71, pp.151-159.

Wouters, M. and Kirchberger, M.A., 2015. Customer value propositions as

interorganizational management accounting to support customer collaboration. Industrial

Marketing Management, 46, pp.54-67.

McLean, T., McGovern, T. and Davie, S., 2015. Management accounting, engineering and

the management of company growth: Clarke Chapman, 1864–1914. The British Accounting

Review, 47(2), pp.177-190.

Messner, M., 2016. Does industry matter? How industry context shapes management

accounting practice. Management Accounting Research, 31, 103-111.

Tappura, S., Sievänen, M., Heikkilä, J., Jussila, A. and Nenonen, N., 2015. A management

accounting perspective on safety. Safety science, 71, pp.151-159.

Wouters, M. and Kirchberger, M.A., 2015. Customer value propositions as

interorganizational management accounting to support customer collaboration. Industrial

Marketing Management, 46, pp.54-67.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.