Management Accounting Homework Solution: Costing and Statements

VerifiedAdded on 2023/04/06

|14

|1048

|317

Homework Assignment

AI Summary

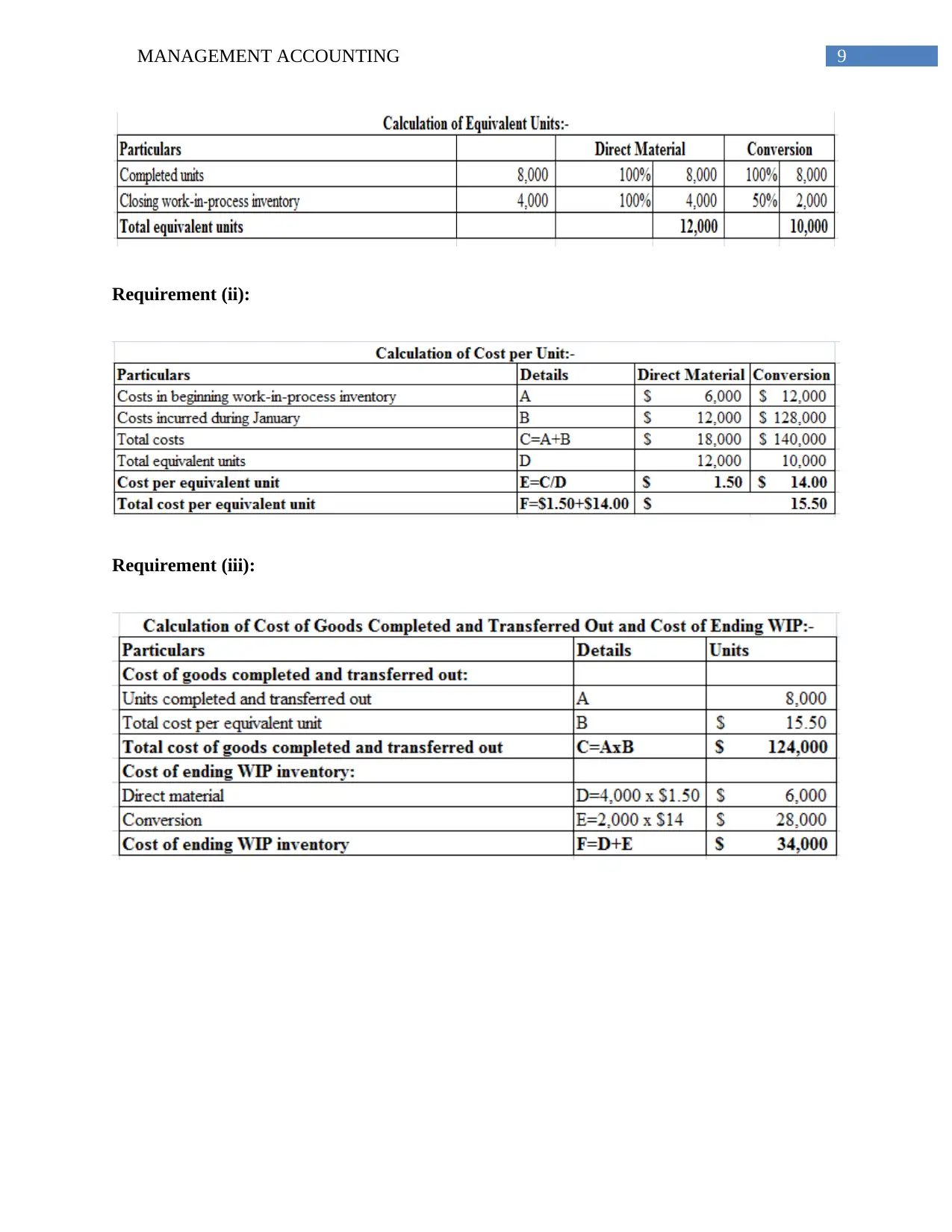

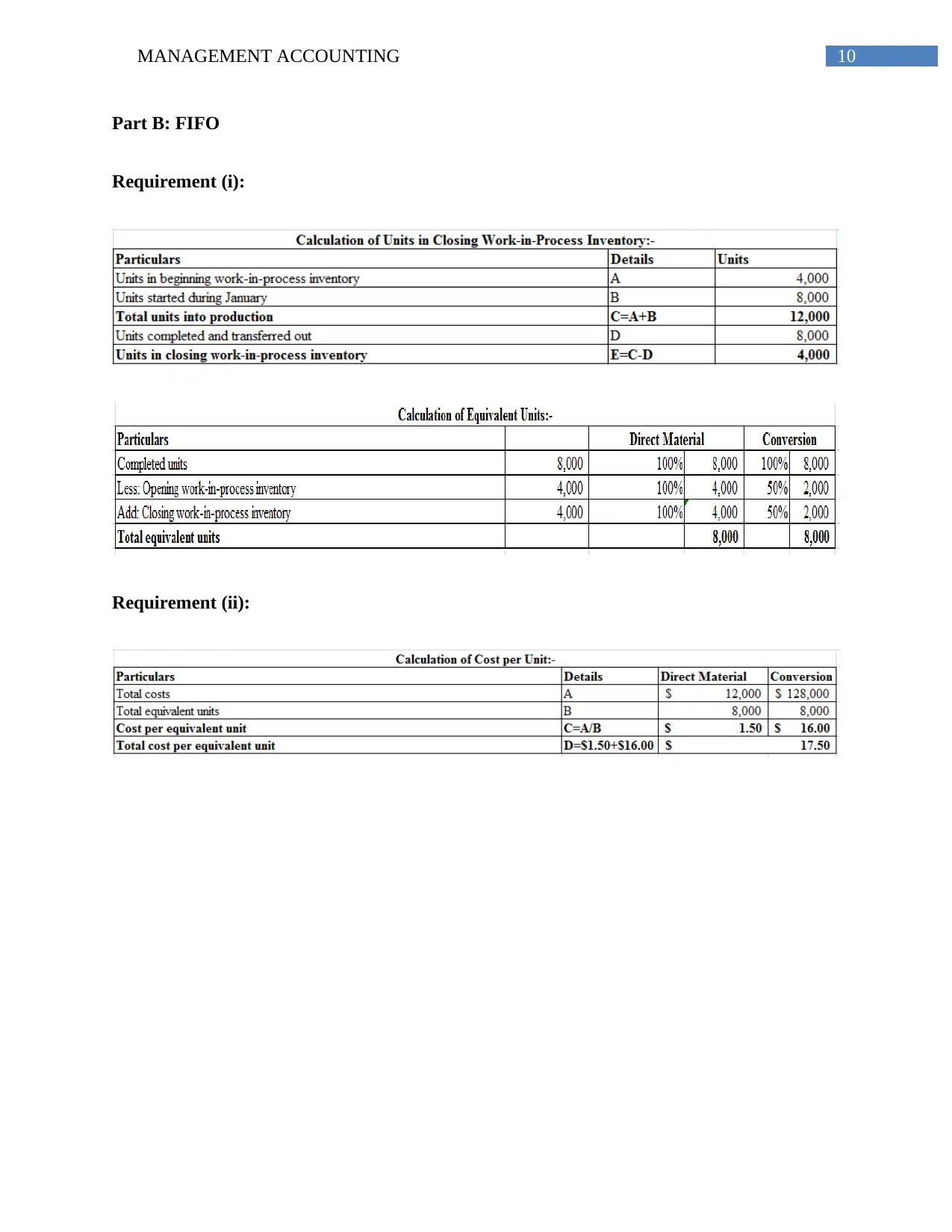

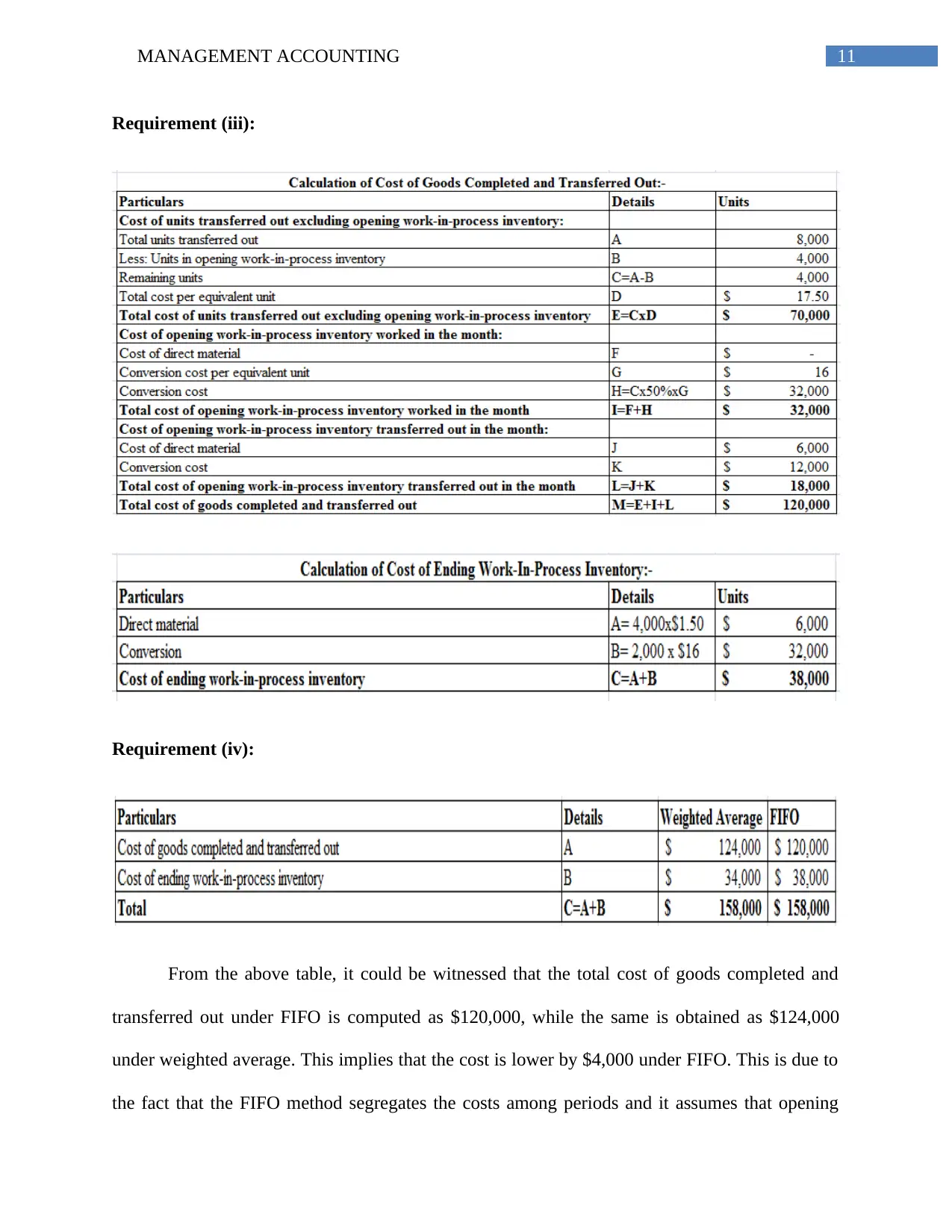

This management accounting assignment solution addresses key concepts including job costing, process costing (weighted average and FIFO methods), and the preparation and analysis of income statements. The assignment begins with an analysis of job costing, including calculations and explanations. It then delves into cost flows and the importance of proper cost classification in income statements for effective decision-making. The solution further explores process costing, comparing and contrasting the weighted average and FIFO methods, and provides detailed calculations and interpretations. The document also examines the impact of different costing methods on reported profits and provides recommendations based on the specific scenario. Overall, the assignment provides a comprehensive understanding of core management accounting principles and their application in various business contexts.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.