University Management Accounting Assignment Solution - Finance

VerifiedAdded on 2023/01/16

|14

|2282

|24

Homework Assignment

AI Summary

This management accounting assignment solution addresses several key concepts within the field. It begins by analyzing a quote from Richard Branson in the context of ethical standards outlined by the Institute of Management Accountants (IMA), specifically focusing on the standard of competence. The solution then delves into quality cost analysis, classifying various activities into prevention, appraisal, and failure costs, and examining their impact on overall costs. Further, the assignment explores variance analysis, identifying causes of cost discrepancies and their implications. It also covers manufacturing overhead, distinguishing between under-applied and over-applied overhead. Finally, the solution examines pricing strategies, comparing and contrasting cost-plus pricing and value-based pricing, highlighting their limitations and benefits, and discussing how quality conformance impacts pricing decisions.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING

Table of Contents

Question 1:.................................................................................................................................3

Question 2:.................................................................................................................................4

Requirement a:.......................................................................................................................4

Requirement b:.......................................................................................................................4

Requirement c:.......................................................................................................................4

Question 3:.................................................................................................................................5

Requirement a:.......................................................................................................................5

Requirement b:.......................................................................................................................5

Requirement c:.......................................................................................................................6

Requirement d:.......................................................................................................................6

Requirement e:.......................................................................................................................6

Question 4:.................................................................................................................................7

Requirement a:.......................................................................................................................7

Requirement b:.......................................................................................................................7

Requirement c:.......................................................................................................................8

Question 5:.................................................................................................................................8

Requirement a:.......................................................................................................................8

Requirement b:.......................................................................................................................8

Requirement c:.......................................................................................................................9

Question 6:.................................................................................................................................9

Table of Contents

Question 1:.................................................................................................................................3

Question 2:.................................................................................................................................4

Requirement a:.......................................................................................................................4

Requirement b:.......................................................................................................................4

Requirement c:.......................................................................................................................4

Question 3:.................................................................................................................................5

Requirement a:.......................................................................................................................5

Requirement b:.......................................................................................................................5

Requirement c:.......................................................................................................................6

Requirement d:.......................................................................................................................6

Requirement e:.......................................................................................................................6

Question 4:.................................................................................................................................7

Requirement a:.......................................................................................................................7

Requirement b:.......................................................................................................................7

Requirement c:.......................................................................................................................8

Question 5:.................................................................................................................................8

Requirement a:.......................................................................................................................8

Requirement b:.......................................................................................................................8

Requirement c:.......................................................................................................................9

Question 6:.................................................................................................................................9

2MANAGEMENT ACCOUNTING

Requirement a:.......................................................................................................................9

Requirement b:.....................................................................................................................11

References:...............................................................................................................................12

Requirement a:.......................................................................................................................9

Requirement b:.....................................................................................................................11

References:...............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING

Question 1:

The Institute of Management Accountants (IMA) is a governing body that assists the

business community in knowing about the overall professional ethics and the ways of

implementing the same. The standard, which the quote of Richard Branson has jeopardised, is

the standard related to competence. According to the standard, the professionals are needed to

possess the required skills and knowledge regarding the hob and they have to act

professionally to the matters. IMA has to provide its decision that needs to be supported by

recommendations and information, which have to be correct, timely and clear (Bromwich and

Scapens 2016).

According to the quote, an individual need not lose the opportunity of accepting an

offer and the same needs to be accepted even if the individual does not have the required

skills of performing job responsibilities. However, according to the IMA standard, an

individual has to possess the desired skills and knowledge for any position in an organisation

(Dekker 2016). Therefore, it could be seen that the quote has violated the competence

standard mentioned in IMA.

Question 1:

The Institute of Management Accountants (IMA) is a governing body that assists the

business community in knowing about the overall professional ethics and the ways of

implementing the same. The standard, which the quote of Richard Branson has jeopardised, is

the standard related to competence. According to the standard, the professionals are needed to

possess the required skills and knowledge regarding the hob and they have to act

professionally to the matters. IMA has to provide its decision that needs to be supported by

recommendations and information, which have to be correct, timely and clear (Bromwich and

Scapens 2016).

According to the quote, an individual need not lose the opportunity of accepting an

offer and the same needs to be accepted even if the individual does not have the required

skills of performing job responsibilities. However, according to the IMA standard, an

individual has to possess the desired skills and knowledge for any position in an organisation

(Dekker 2016). Therefore, it could be seen that the quote has violated the competence

standard mentioned in IMA.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING

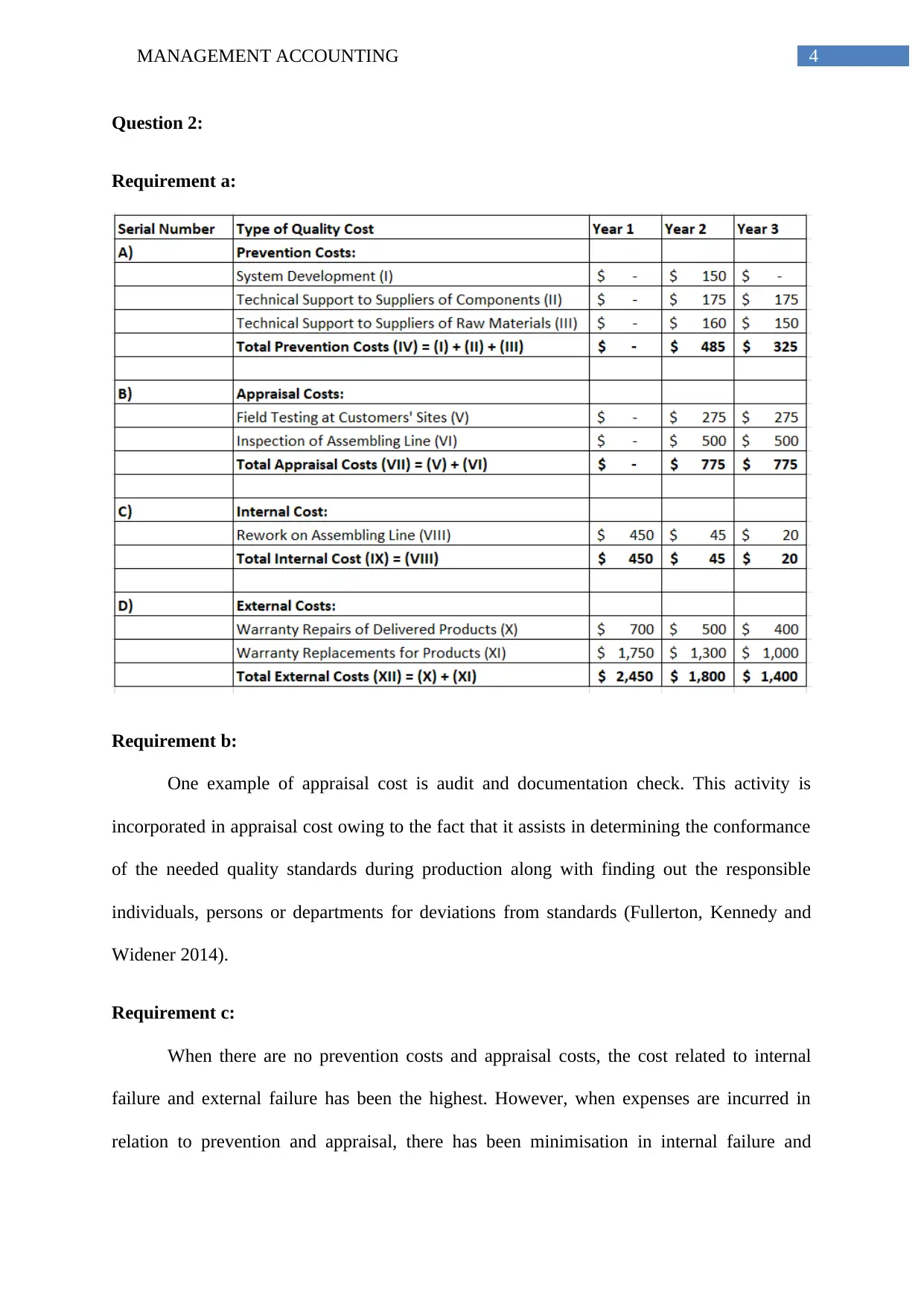

Question 2:

Requirement a:

Requirement b:

One example of appraisal cost is audit and documentation check. This activity is

incorporated in appraisal cost owing to the fact that it assists in determining the conformance

of the needed quality standards during production along with finding out the responsible

individuals, persons or departments for deviations from standards (Fullerton, Kennedy and

Widener 2014).

Requirement c:

When there are no prevention costs and appraisal costs, the cost related to internal

failure and external failure has been the highest. However, when expenses are incurred in

relation to prevention and appraisal, there has been minimisation in internal failure and

Question 2:

Requirement a:

Requirement b:

One example of appraisal cost is audit and documentation check. This activity is

incorporated in appraisal cost owing to the fact that it assists in determining the conformance

of the needed quality standards during production along with finding out the responsible

individuals, persons or departments for deviations from standards (Fullerton, Kennedy and

Widener 2014).

Requirement c:

When there are no prevention costs and appraisal costs, the cost related to internal

failure and external failure has been the highest. However, when expenses are incurred in

relation to prevention and appraisal, there has been minimisation in internal failure and

5MANAGEMENT ACCOUNTING

external failure costs. This implies that if an organisation concentrates on appraisal and

prevention, then the internal and external failures are minimised (Hopper and Bui 2016). If

the organisation focuses more on product quality, the quality cost could be minimised.

Internally, emphasis needs to be placed on the quality before sending products to the

customers. Therefore, if they are rectified, it would assist the organisation in maintaining

sound customer relationship. On the other hand, external failure costs are the minimum costs

to be maintained, since it comprises of cost defect in the product, as identified by the

customers.

Initially, in the first year, the organisation has not incurred expenses on appraisal and

prevention aspects, which have lead to increased internal and external failure costs. However,

in the second year and the third year, the organisation has incurred expenses on prevention

and appraisal aspects and this has minimised internal failure cost and external failure costs

drastically (Kaplan and Atkinson 2015). In case; the quality standard of the products would

decline, the impact would be adverse on brand value and goodwill of the organisation leading

to loss of market reputation.

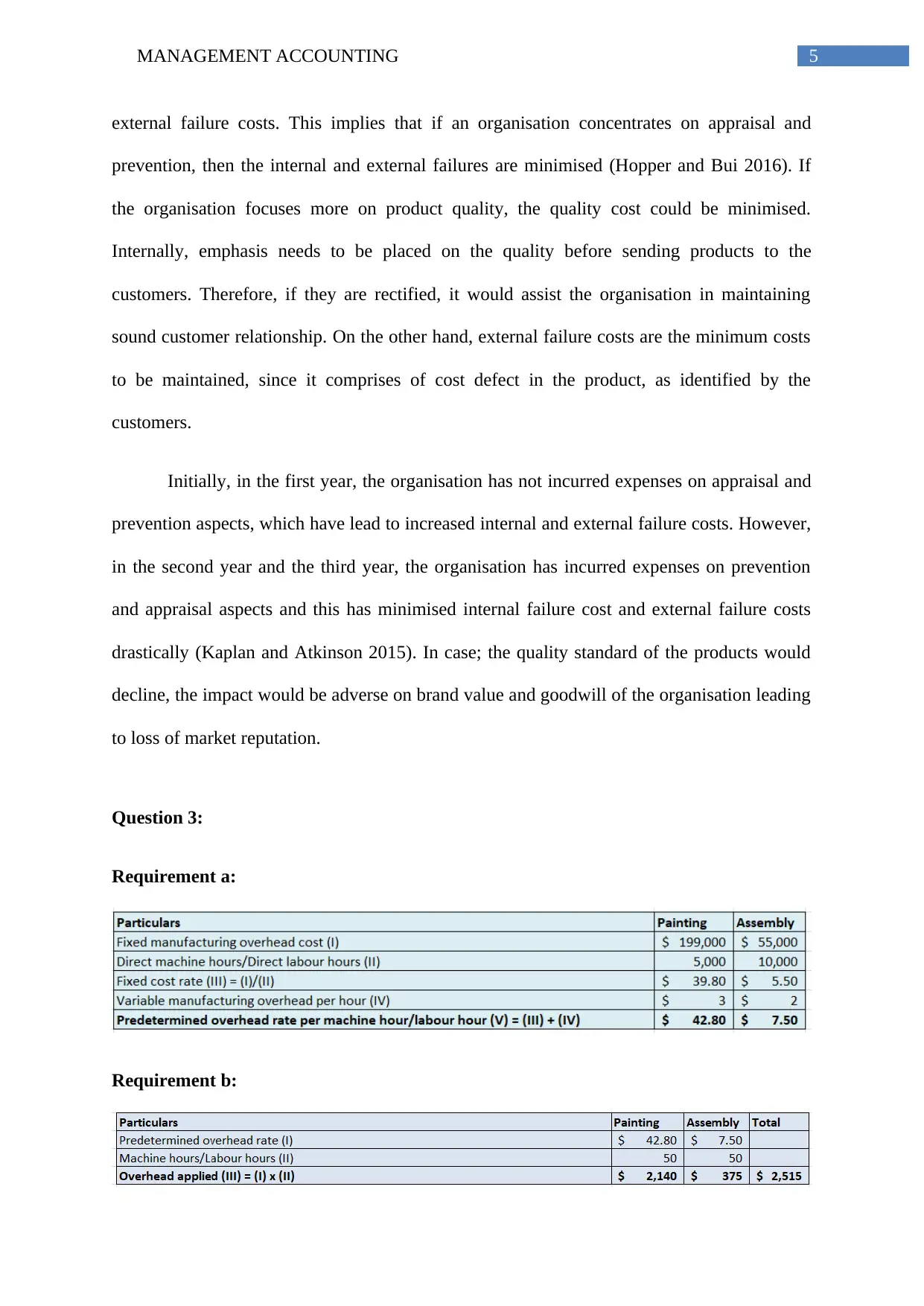

Question 3:

Requirement a:

Requirement b:

external failure costs. This implies that if an organisation concentrates on appraisal and

prevention, then the internal and external failures are minimised (Hopper and Bui 2016). If

the organisation focuses more on product quality, the quality cost could be minimised.

Internally, emphasis needs to be placed on the quality before sending products to the

customers. Therefore, if they are rectified, it would assist the organisation in maintaining

sound customer relationship. On the other hand, external failure costs are the minimum costs

to be maintained, since it comprises of cost defect in the product, as identified by the

customers.

Initially, in the first year, the organisation has not incurred expenses on appraisal and

prevention aspects, which have lead to increased internal and external failure costs. However,

in the second year and the third year, the organisation has incurred expenses on prevention

and appraisal aspects and this has minimised internal failure cost and external failure costs

drastically (Kaplan and Atkinson 2015). In case; the quality standard of the products would

decline, the impact would be adverse on brand value and goodwill of the organisation leading

to loss of market reputation.

Question 3:

Requirement a:

Requirement b:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING

Requirement c:

Requirement d:

Requirement e:

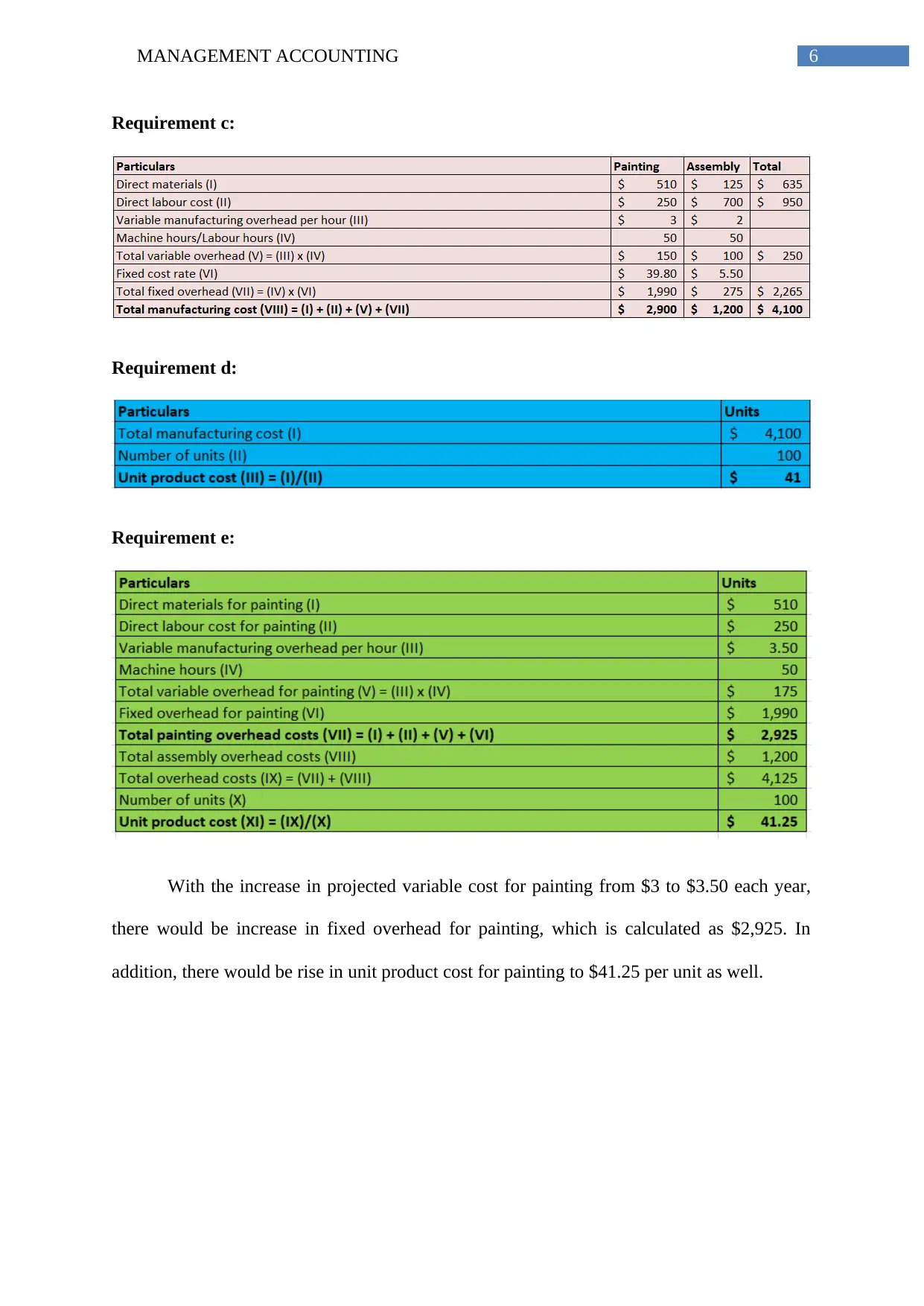

With the increase in projected variable cost for painting from $3 to $3.50 each year,

there would be increase in fixed overhead for painting, which is calculated as $2,925. In

addition, there would be rise in unit product cost for painting to $41.25 per unit as well.

Requirement c:

Requirement d:

Requirement e:

With the increase in projected variable cost for painting from $3 to $3.50 each year,

there would be increase in fixed overhead for painting, which is calculated as $2,925. In

addition, there would be rise in unit product cost for painting to $41.25 per unit as well.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING

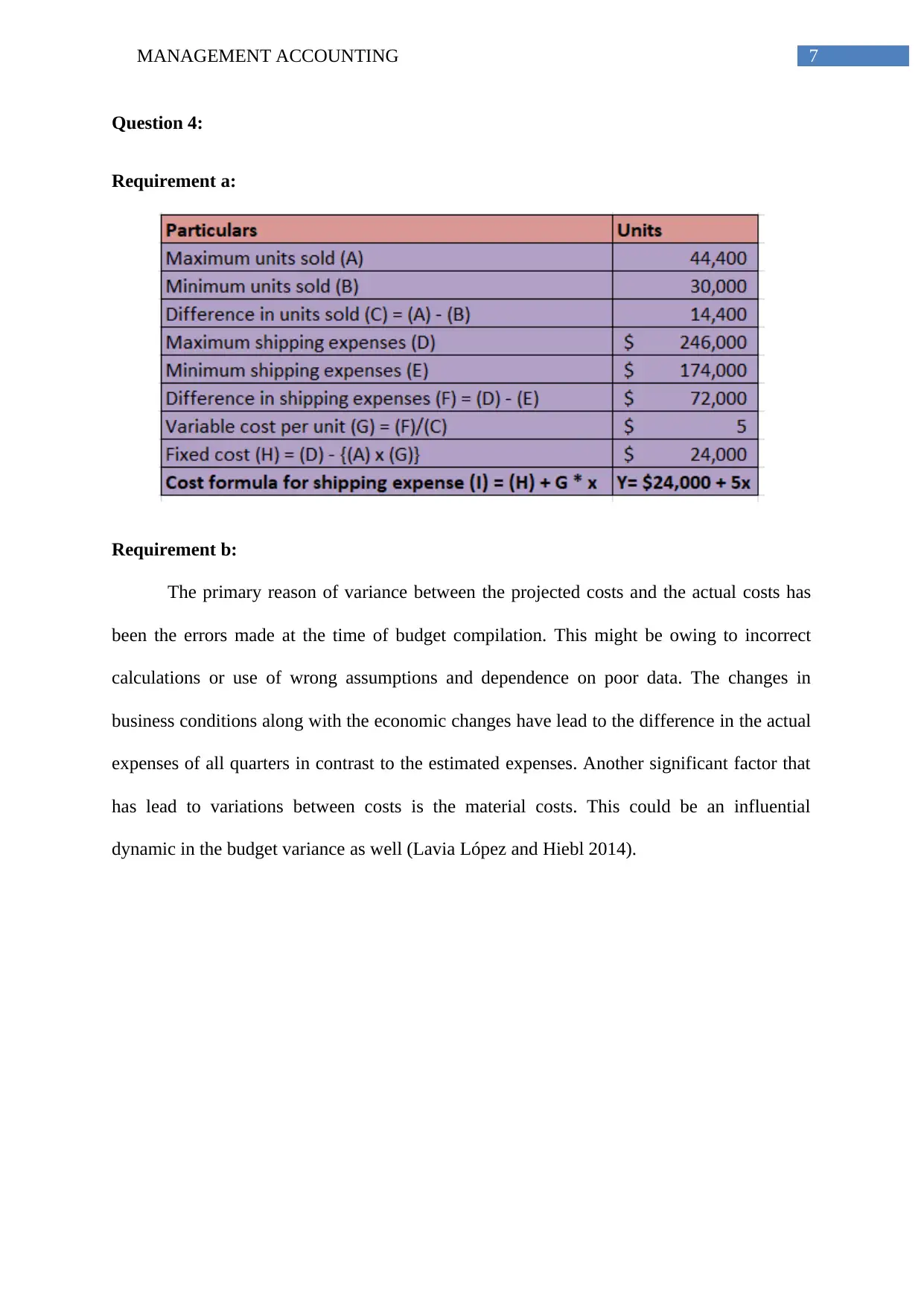

Question 4:

Requirement a:

Requirement b:

The primary reason of variance between the projected costs and the actual costs has

been the errors made at the time of budget compilation. This might be owing to incorrect

calculations or use of wrong assumptions and dependence on poor data. The changes in

business conditions along with the economic changes have lead to the difference in the actual

expenses of all quarters in contrast to the estimated expenses. Another significant factor that

has lead to variations between costs is the material costs. This could be an influential

dynamic in the budget variance as well (Lavia López and Hiebl 2014).

Question 4:

Requirement a:

Requirement b:

The primary reason of variance between the projected costs and the actual costs has

been the errors made at the time of budget compilation. This might be owing to incorrect

calculations or use of wrong assumptions and dependence on poor data. The changes in

business conditions along with the economic changes have lead to the difference in the actual

expenses of all quarters in contrast to the estimated expenses. Another significant factor that

has lead to variations between costs is the material costs. This could be an influential

dynamic in the budget variance as well (Lavia López and Hiebl 2014).

8MANAGEMENT ACCOUNTING

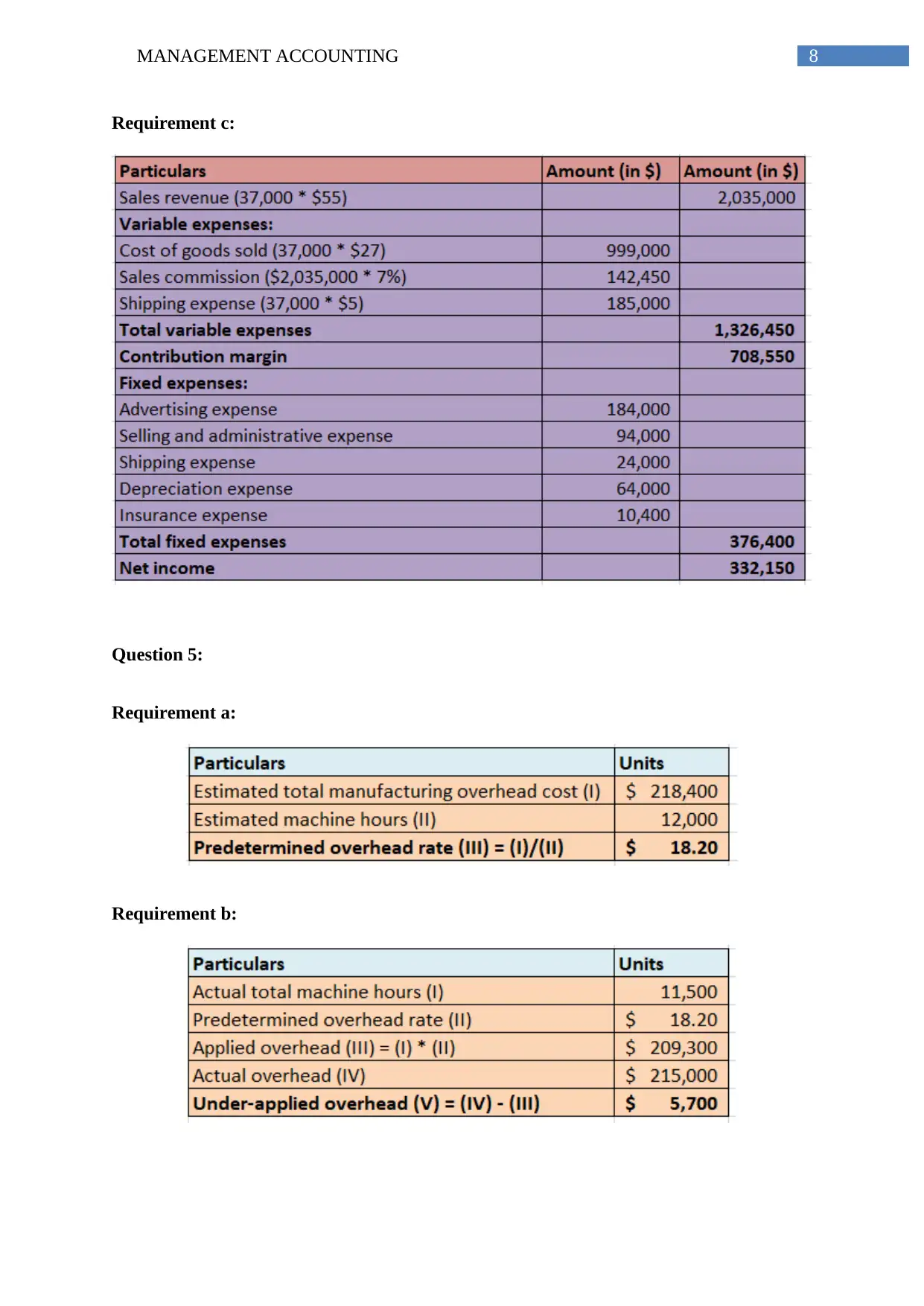

Requirement c:

Question 5:

Requirement a:

Requirement b:

Requirement c:

Question 5:

Requirement a:

Requirement b:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING

Requirement c:

Manufacturing overhead includes all cost of goods sold, which could not be attributed

to a particular product or service manufactured. This implies that it takes into account all

disparate items like utilities and other costs related to keep the production processes running

(Messner 2016). Under-applied and over-applied manufacturing overhead takes place at the

time the budgeted manufacturing overhead is not equal to the actual manufacturing overhead.

Under-applied overhead takes place at the time the actual manufacturing overhead

exceeds the budgeted manufacturing overhead incurred on production. For instance, if an

organisation makes a budget of $70,000 to be incurred on manufacturing overhead and it has

to incur $80,000 actually, the under-applied overhead amounts to $10,000 (Modell 2014).

This is recorded in the form of prepaid expense on balance sheet statement and after that, it is

rectified by increasing the cost of sales at the end of the period. On the other hand, if actual

overhead costs are lower than the budgeted overhead costs, it leads to over-applied overhead.

Thus, in case of under-application of overhead, it implies that additional actual

overhead expenses have been incurred than the budgeted expenses and the difference is

charged to expense as budgeted. This generally means that the realisation of expense is

accelerated into the existing period, which minimises the recognition of profit amount for the

organisation (Otley 2016).

Question 6:

Requirement a:

The main reason of using cost plus pricing is to find out the overall product cost. The

cost is computed based on the inclusion of all cost incurred on the product comprising of

variable and fixed costs. After this, mark-up is added to the total costs to obtain the overall

Requirement c:

Manufacturing overhead includes all cost of goods sold, which could not be attributed

to a particular product or service manufactured. This implies that it takes into account all

disparate items like utilities and other costs related to keep the production processes running

(Messner 2016). Under-applied and over-applied manufacturing overhead takes place at the

time the budgeted manufacturing overhead is not equal to the actual manufacturing overhead.

Under-applied overhead takes place at the time the actual manufacturing overhead

exceeds the budgeted manufacturing overhead incurred on production. For instance, if an

organisation makes a budget of $70,000 to be incurred on manufacturing overhead and it has

to incur $80,000 actually, the under-applied overhead amounts to $10,000 (Modell 2014).

This is recorded in the form of prepaid expense on balance sheet statement and after that, it is

rectified by increasing the cost of sales at the end of the period. On the other hand, if actual

overhead costs are lower than the budgeted overhead costs, it leads to over-applied overhead.

Thus, in case of under-application of overhead, it implies that additional actual

overhead expenses have been incurred than the budgeted expenses and the difference is

charged to expense as budgeted. This generally means that the realisation of expense is

accelerated into the existing period, which minimises the recognition of profit amount for the

organisation (Otley 2016).

Question 6:

Requirement a:

The main reason of using cost plus pricing is to find out the overall product cost. The

cost is computed based on the inclusion of all cost incurred on the product comprising of

variable and fixed costs. After this, mark-up is added to the total costs to obtain the overall

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING

cost of the product (Quattrone 2016). As per Dholakia, cost plus pricing suffers from three

major limitations, which are discussed briefly as follows:

Efficiency and low profit:

This pricing strategy constitutes of costing of all products, which relies on the cost of

the project. The lower budget cost project provides the organisation with minimum profit,

while high budget project fetches the organisation with increased profit (Shields 2015).

Hence, it minimises the efficiency of the organisation, since it would not be able to guide the

project properly leading to fall in income and the effect would be unfavourable on the

customers.

Covering project cost:

The selling price is forecasted and based on such forecast; the entire cost calculation

is conducted. The managers of the organisation estimate that it would be possible for them to

recover all costs and they would be able to generate the desired profit for the organisation.

However, on certain occasions, it is not possible for the organisation to achieve the desired

sales revenue and therefore, it has to experience increased cost burden ultimately resulting in

significant business losses. As a result, the impact would be adverse on business

sustainability (Tucker and Lowe 2014).

Ignoring the views of the competitors and customers:

Cost plus pricing only considers the cost side related to the product; however, it fails

to take into account the willingness of the customers to pay. For ensuring smooth running of

business operations, it is essential for an organisation to fulfil its cost needs according to the

needs of the customers. In case; the needs of the customers are not met, the organisation

would struggle for survival in the market. Moreover, this strategy does not consider the

cost of the product (Quattrone 2016). As per Dholakia, cost plus pricing suffers from three

major limitations, which are discussed briefly as follows:

Efficiency and low profit:

This pricing strategy constitutes of costing of all products, which relies on the cost of

the project. The lower budget cost project provides the organisation with minimum profit,

while high budget project fetches the organisation with increased profit (Shields 2015).

Hence, it minimises the efficiency of the organisation, since it would not be able to guide the

project properly leading to fall in income and the effect would be unfavourable on the

customers.

Covering project cost:

The selling price is forecasted and based on such forecast; the entire cost calculation

is conducted. The managers of the organisation estimate that it would be possible for them to

recover all costs and they would be able to generate the desired profit for the organisation.

However, on certain occasions, it is not possible for the organisation to achieve the desired

sales revenue and therefore, it has to experience increased cost burden ultimately resulting in

significant business losses. As a result, the impact would be adverse on business

sustainability (Tucker and Lowe 2014).

Ignoring the views of the competitors and customers:

Cost plus pricing only considers the cost side related to the product; however, it fails

to take into account the willingness of the customers to pay. For ensuring smooth running of

business operations, it is essential for an organisation to fulfil its cost needs according to the

needs of the customers. In case; the needs of the customers are not met, the organisation

would struggle for survival in the market. Moreover, this strategy does not consider the

11MANAGEMENT ACCOUNTING

perspectives of the competitors regarding product prices (Van Der Stede 2015). Since the

organisation has to match its price with the competitors’ prices, it needs to take into account

the views of the competitors while undertaking final product pricing decision.

Requirement b:

Value-based pricing strategy is a method where the cost is ascertained by considering

the perspectives of the customers; however, it fails to consider the historical cost method.

Each product cost varies from each other. The organisation could gain additional profit even

by selling lower product volumes, since it could charge greater prices. Therefore, the

organisation could gain profit from products. The method is utilised, in which the products

are priced based on the needs of the customers (Van Helden and Uddin 2016).

The quality of conformance in the products of the organisation implies that the

organisation could manufacture the product by using better quality of raw materials and due

to this; there would be increase in overall product quality.

The organisation could treat this in the form of investment, as manufacturing products

by considering the preferences and needs of the customers would increase the product

quality. Due to this, the organisation would be able to reduce the real cost of quality testing,

which it needs to perform for maintaining quality. The organisation could invest money saved

from quality cost to certain projects based on which it could generate a certain percentage of

return. With the help of this strategy, the organisation would have additional benefits owing

to the savings made out of quality cost along with earning some return on investment.

Therefore, it minimises the overall expenses and the interest revenue of the organisation is

increased.

perspectives of the competitors regarding product prices (Van Der Stede 2015). Since the

organisation has to match its price with the competitors’ prices, it needs to take into account

the views of the competitors while undertaking final product pricing decision.

Requirement b:

Value-based pricing strategy is a method where the cost is ascertained by considering

the perspectives of the customers; however, it fails to consider the historical cost method.

Each product cost varies from each other. The organisation could gain additional profit even

by selling lower product volumes, since it could charge greater prices. Therefore, the

organisation could gain profit from products. The method is utilised, in which the products

are priced based on the needs of the customers (Van Helden and Uddin 2016).

The quality of conformance in the products of the organisation implies that the

organisation could manufacture the product by using better quality of raw materials and due

to this; there would be increase in overall product quality.

The organisation could treat this in the form of investment, as manufacturing products

by considering the preferences and needs of the customers would increase the product

quality. Due to this, the organisation would be able to reduce the real cost of quality testing,

which it needs to perform for maintaining quality. The organisation could invest money saved

from quality cost to certain projects based on which it could generate a certain percentage of

return. With the help of this strategy, the organisation would have additional benefits owing

to the savings made out of quality cost along with earning some return on investment.

Therefore, it minimises the overall expenses and the interest revenue of the organisation is

increased.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.