Management Accounting for Cost and Control - Assignment Report

VerifiedAdded on 2023/01/17

|15

|1770

|60

Report

AI Summary

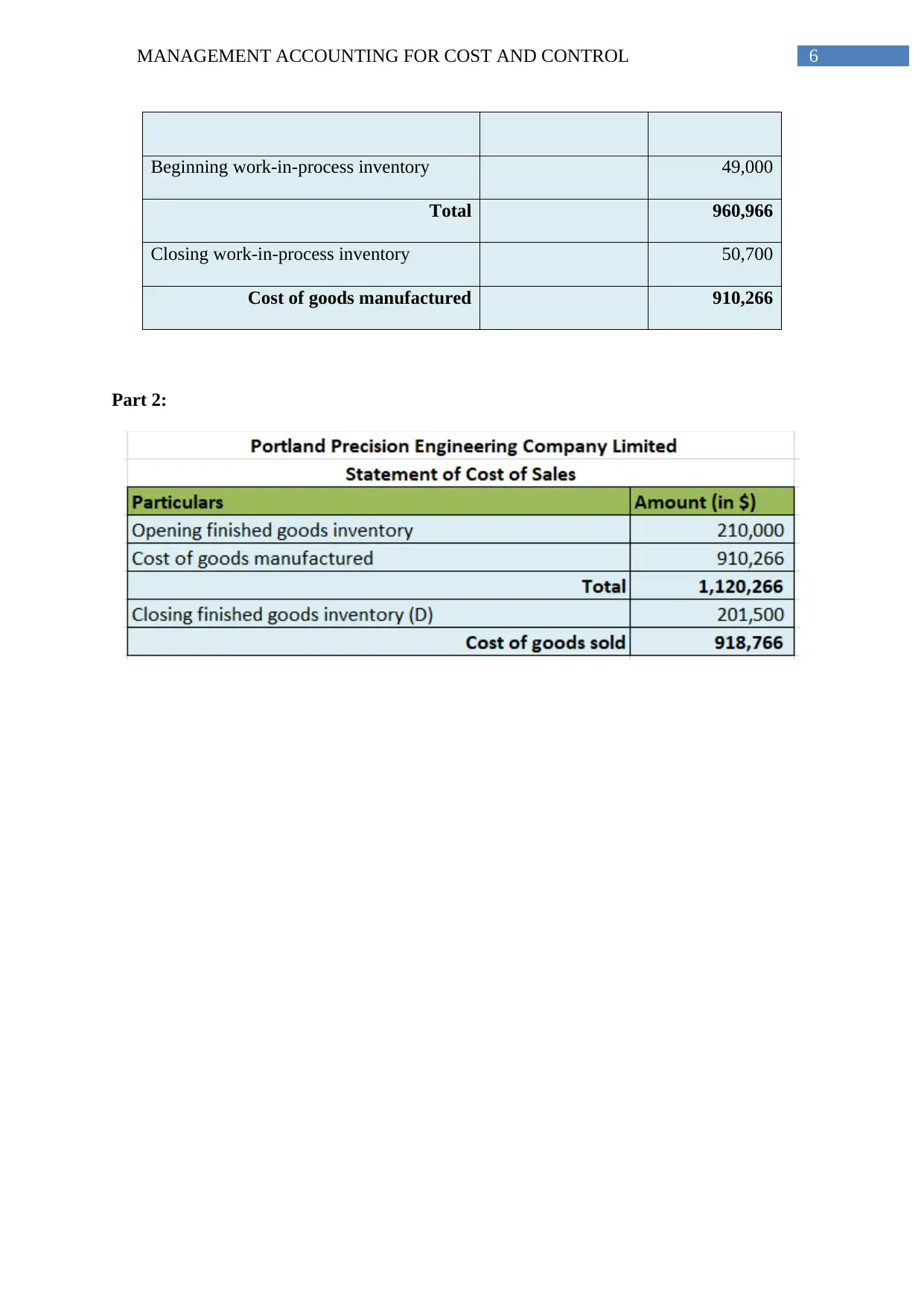

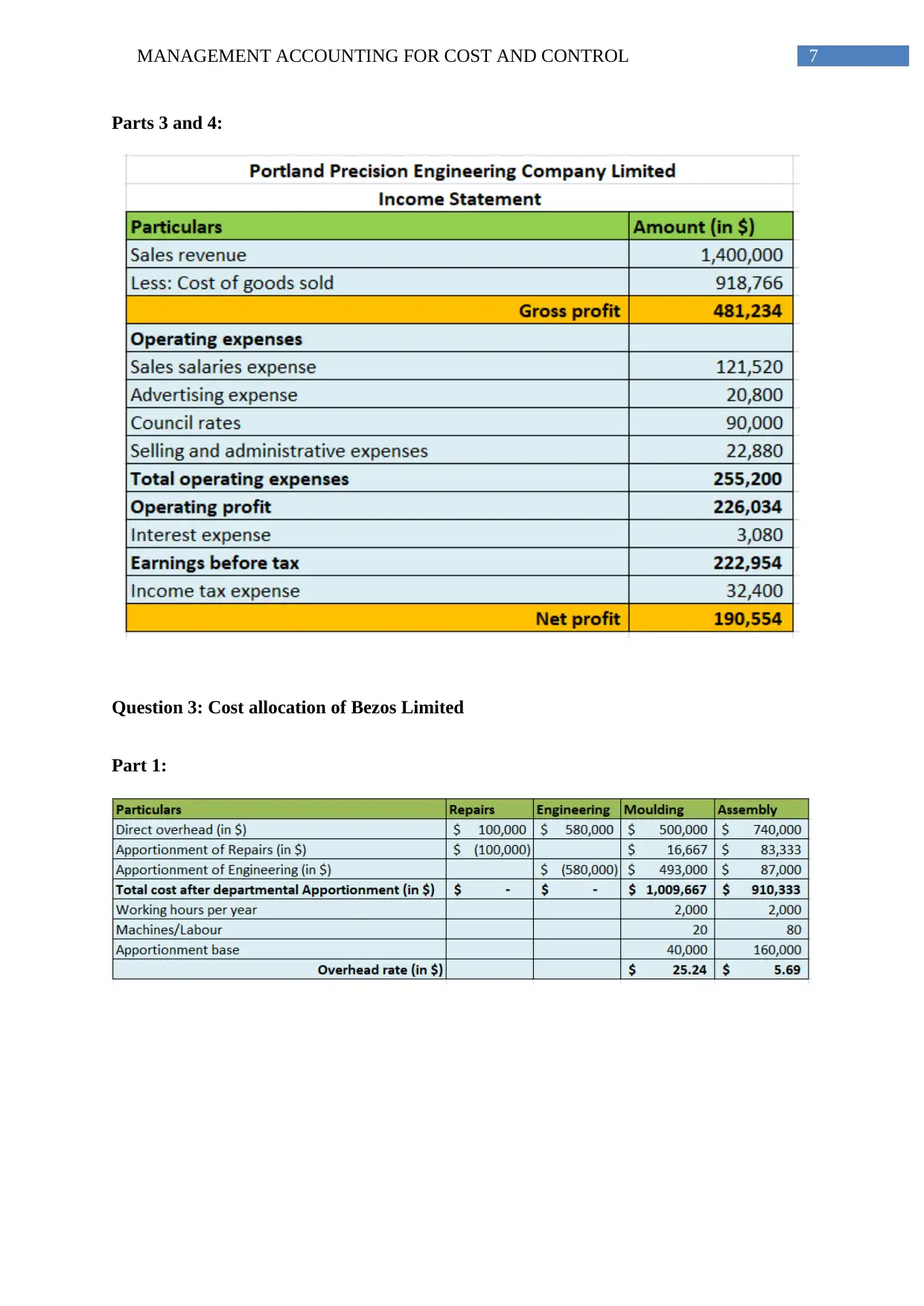

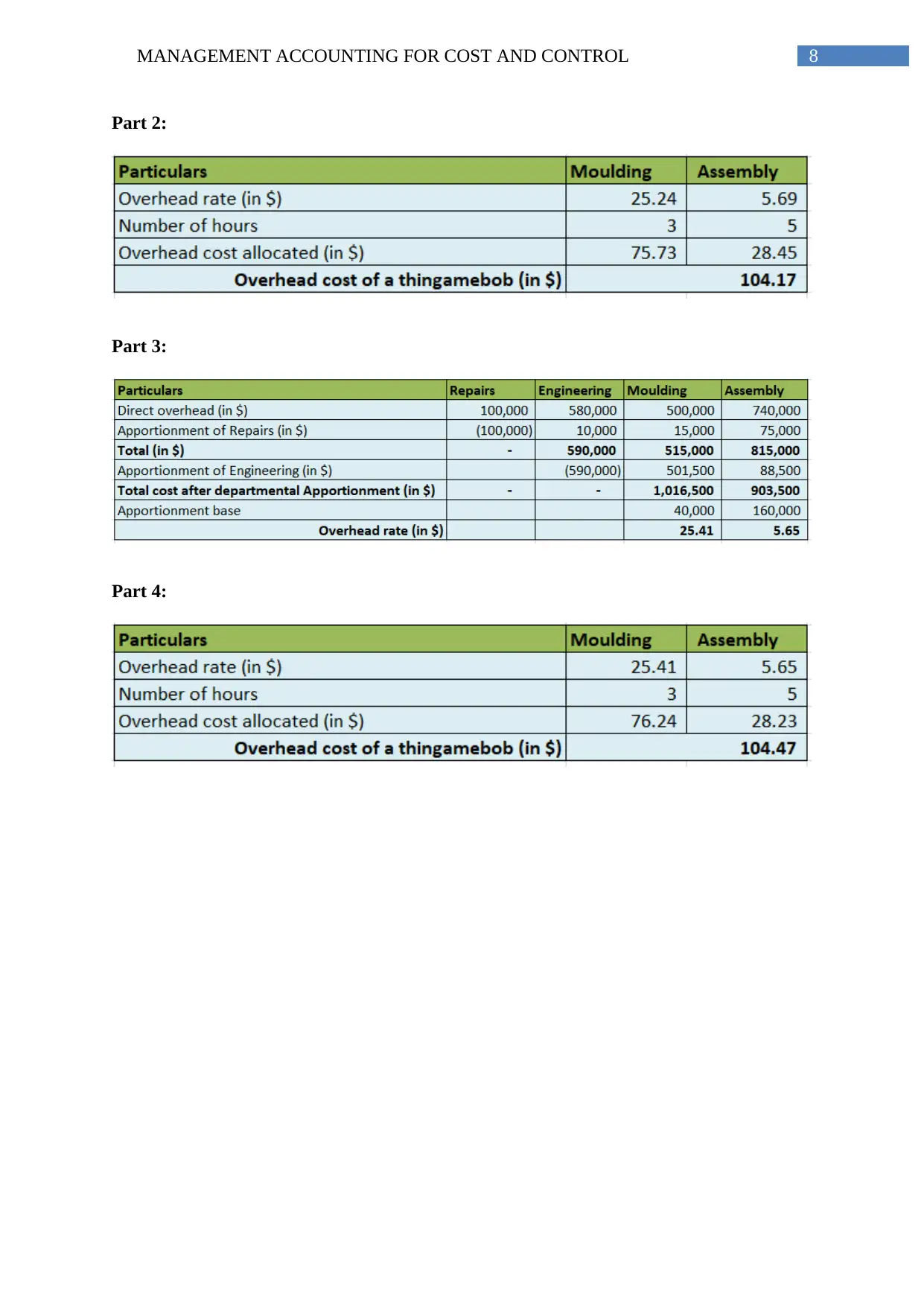

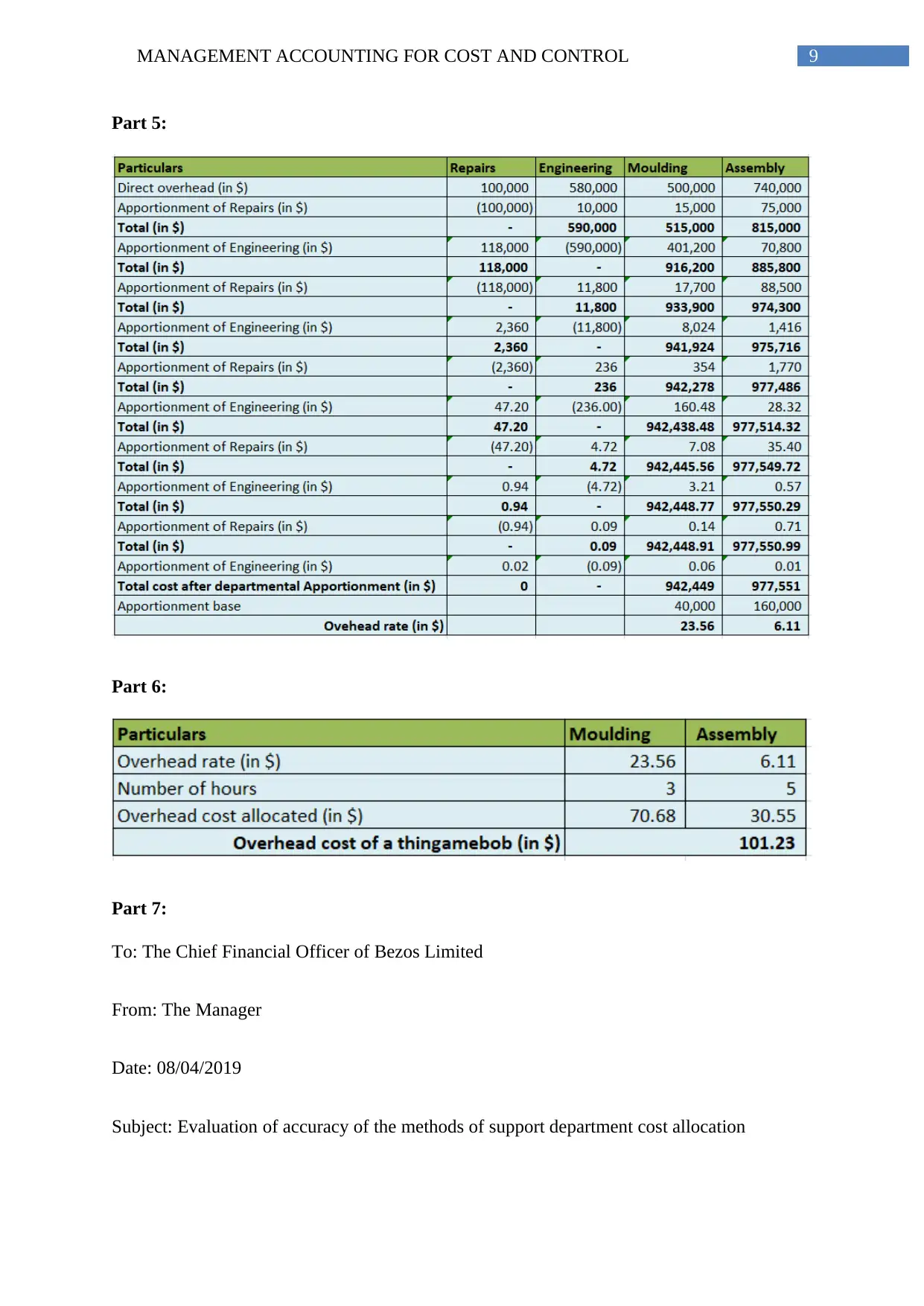

This document is a comprehensive report addressing a management accounting assignment, providing detailed solutions to various questions. The assignment covers a range of topics, including value chain analysis of Wesfarmers Limited, constructing a cost of manufacturing statement for Portland Precision Engineering Company Limited, cost allocation methods for Bezos Limited, job costing for Collaroy Products Limited, and process costing for Pure Cotton Limited. The report provides step-by-step calculations, explanations of different costing methods, and evaluations of their accuracy. It also includes discussions on key management accounting issues and the application of various techniques in real-world scenarios. The assignment showcases the application of accounting principles and techniques to solve practical business problems. The document also includes a memo to the Chief Financial Officer of Bezos Limited, evaluating the accuracy of support department cost allocation methods.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.