King's Own Institute ACC200 - Concetta Ltd Accounting Assignment

VerifiedAdded on 2023/03/17

|8

|1739

|56

Homework Assignment

AI Summary

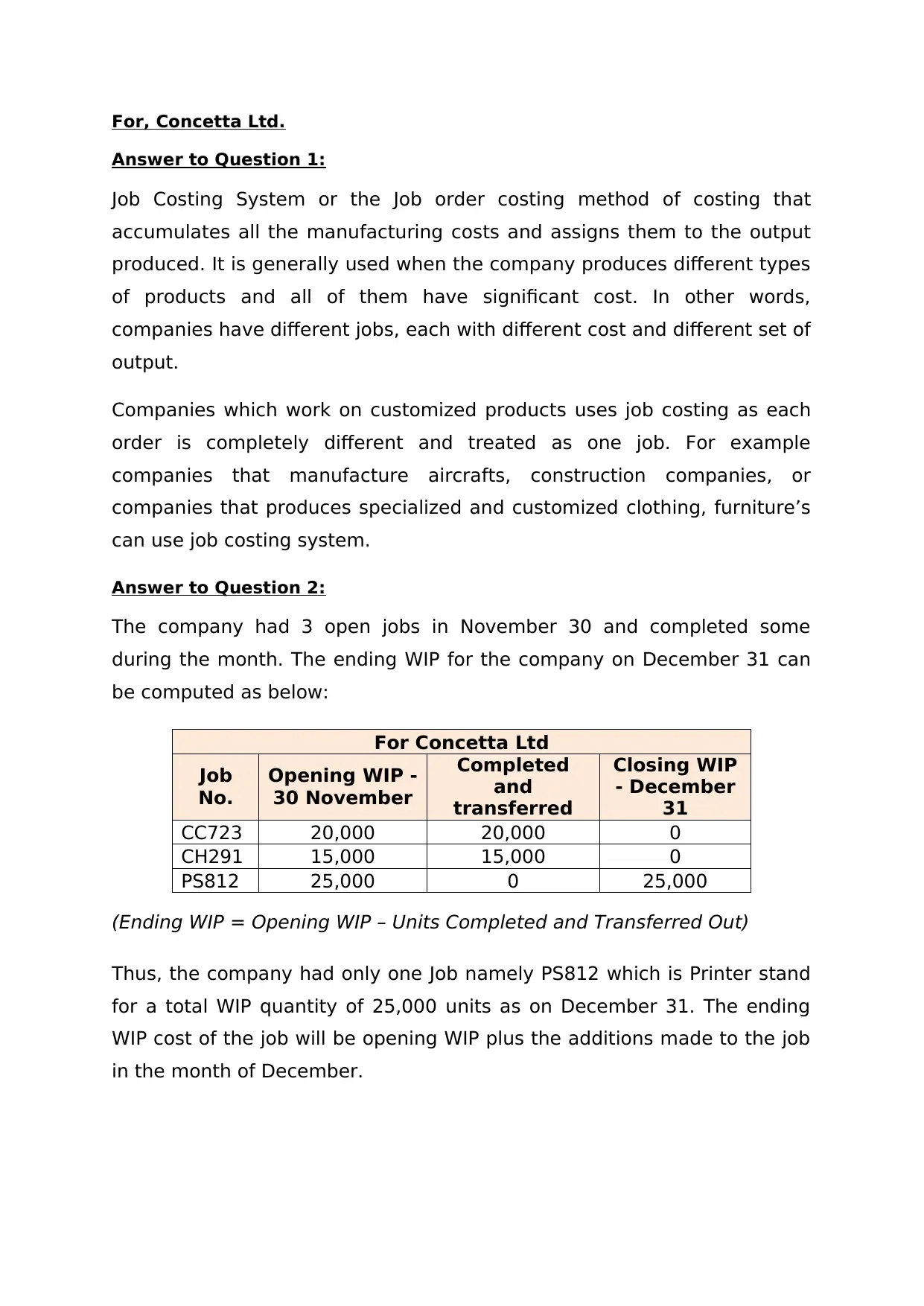

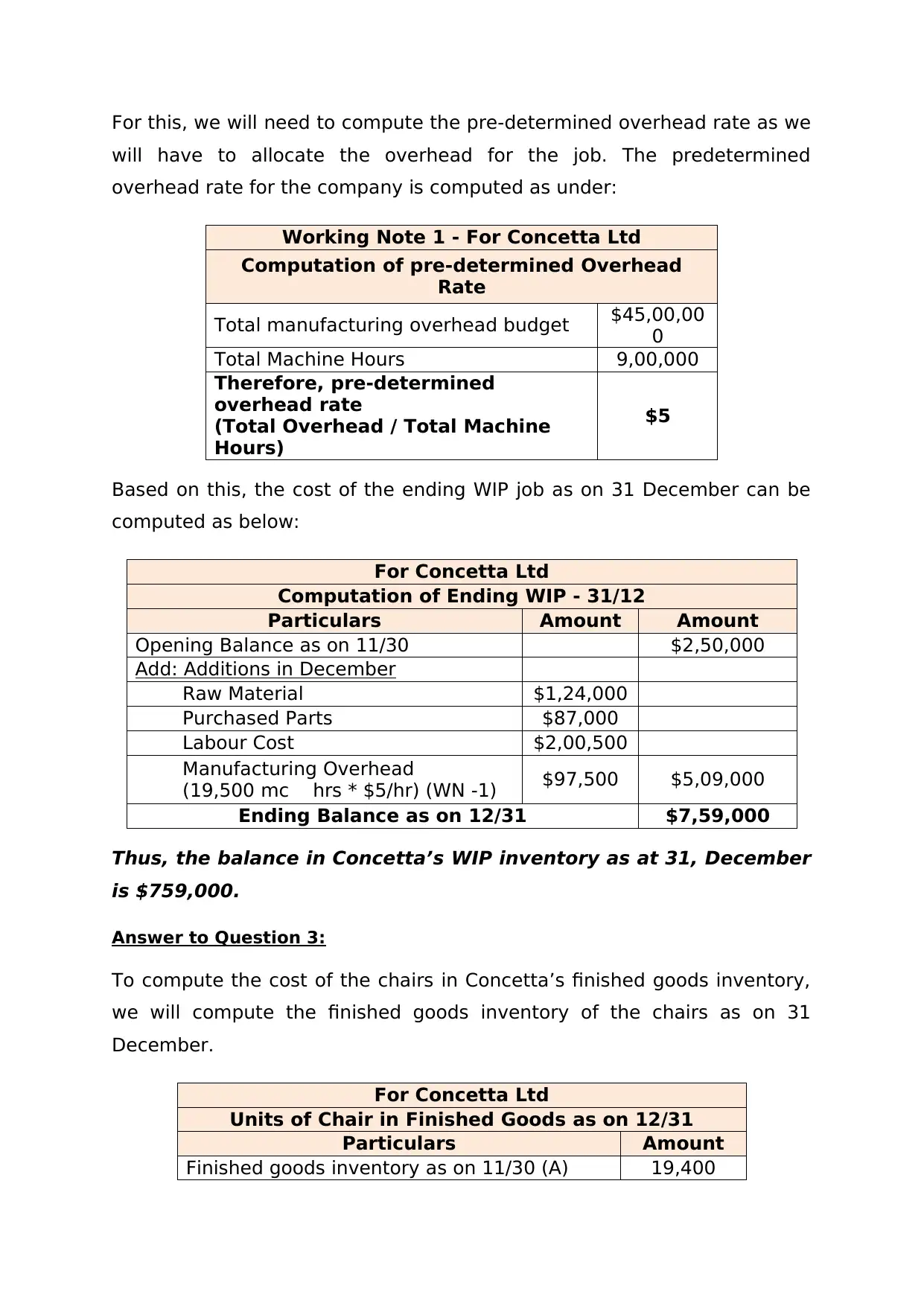

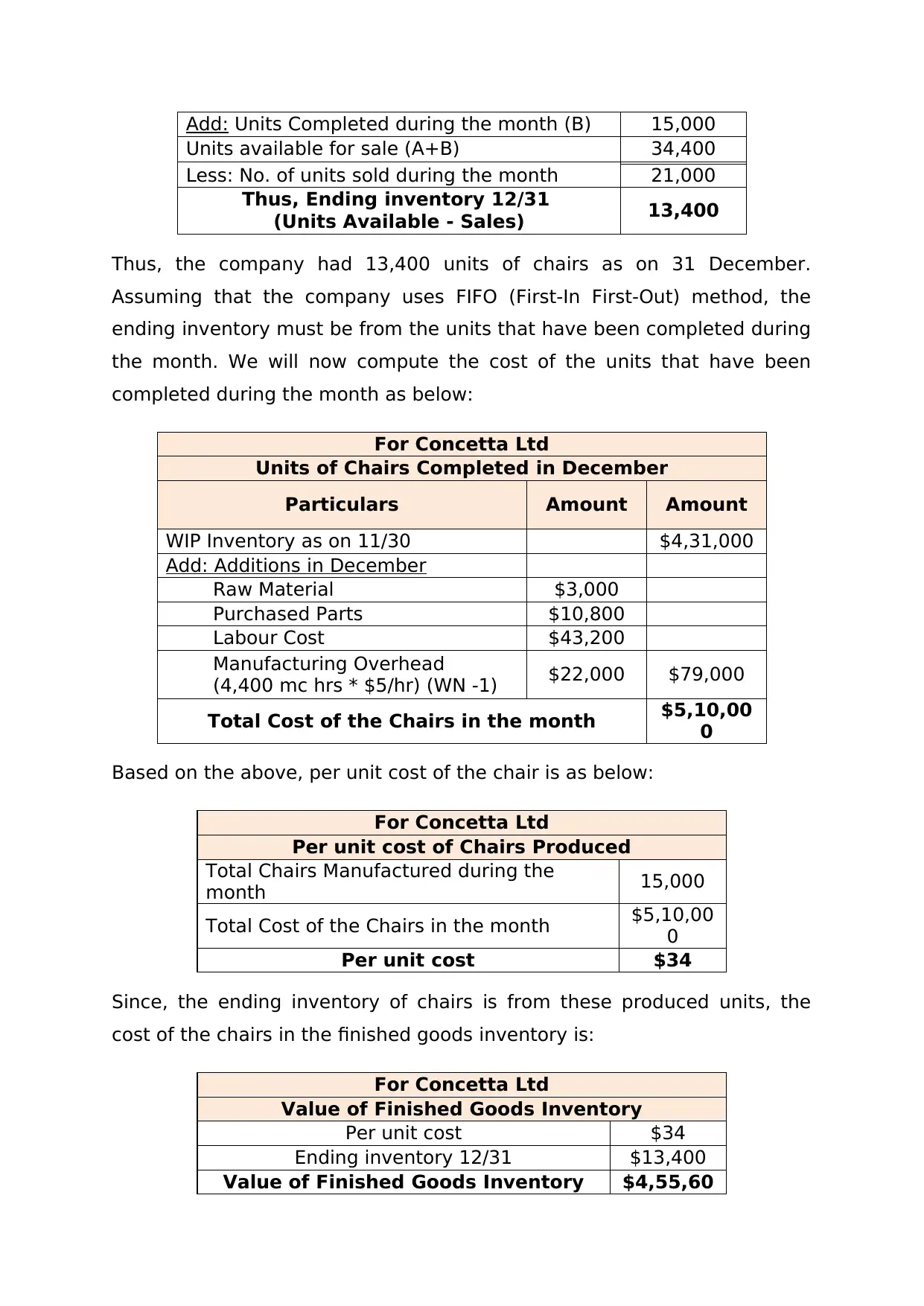

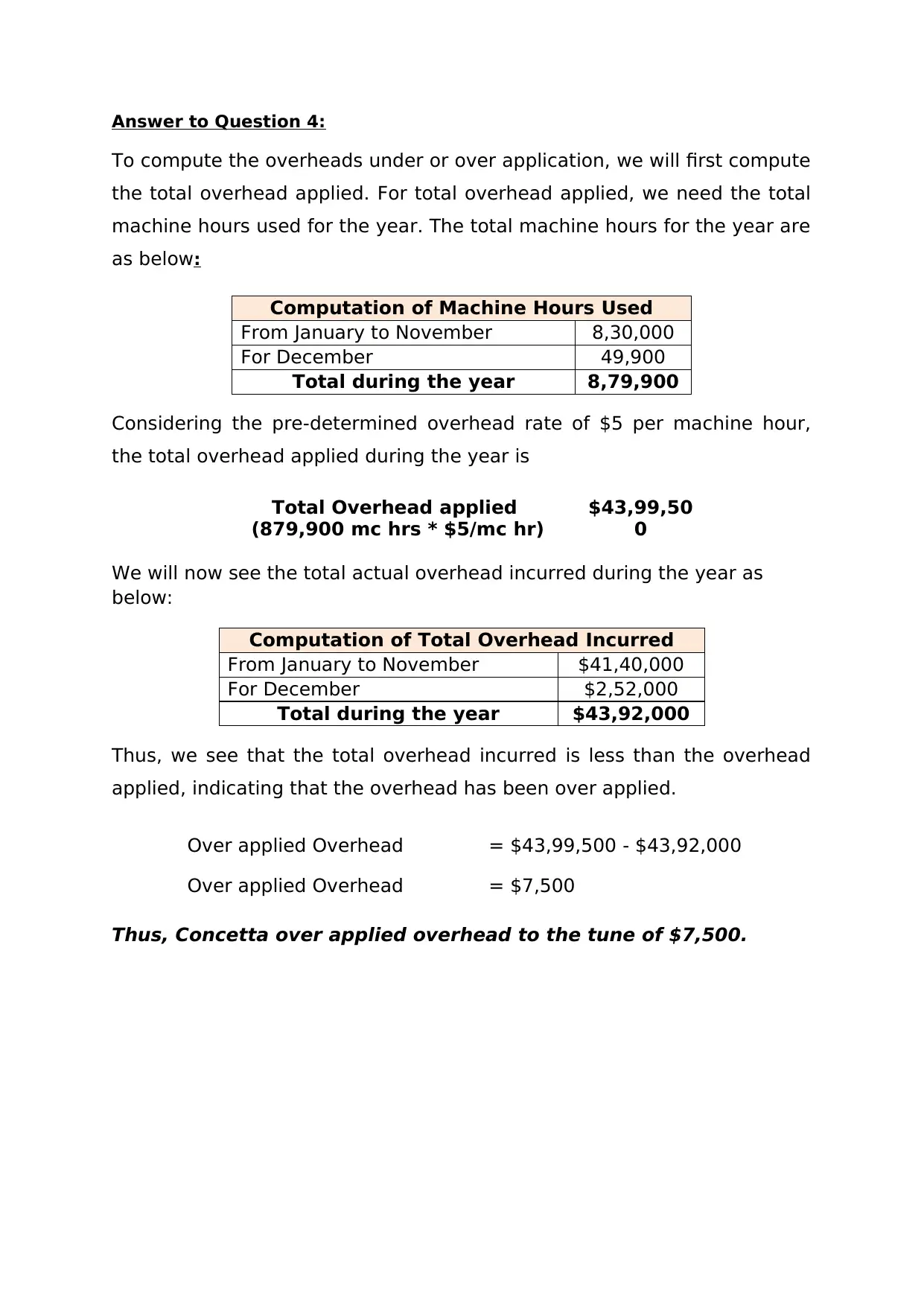

This assignment solution focuses on job costing for Concetta Ltd., addressing key aspects of management accounting. It begins by defining job costing and its application, followed by the calculation of Work-in-Progress (WIP) inventory and the cost of goods in finished goods inventory using the FIFO method. The solution includes computation of the predetermined overhead rate and the application of overheads, determining over or under application of overheads, and discussing the accounting treatment for such discrepancies. It also contrasts job costing with Activity Based Costing (ABC), highlighting the benefits of ABC in allocating costs more accurately. The assignment provides detailed calculations and explanations for each step, offering a comprehensive understanding of the concepts involved.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.