Comprehensive Analysis and Solution: Management Accounting Assignment

VerifiedAdded on 2022/11/25

|12

|2659

|238

Homework Assignment

AI Summary

This management accounting assignment solution provides a detailed analysis of various concepts and problems. It covers static and flexible budgeting, including variance analysis and the impact of budgetary slack. The solution delves into manufacturing overheads, explaining under-applied and over-applied overhead scenarios. Ethical considerations, based on the IMA Statement of Ethical Professional Practice, are presented, along with their application to pro bono work. The assignment further explores absorption and variable costing methods, comparing their impact on profit and inventory valuation. It also addresses strategies for improving operating profit through stock build-up and evaluates departmental performance using Return on Sales (ROS), Return on Investment (ROI), and Residual Income (RI) metrics. The solution concludes with an assessment of alternative measures for achieving a target return on investment.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1..................................................................................................................................1

a)..................................................................................................................................................1

b)..................................................................................................................................................1

c)..................................................................................................................................................1

d)..................................................................................................................................................1

QUESTION 2..................................................................................................................................2

a....................................................................................................................................................2

b...................................................................................................................................................2

C...................................................................................................................................................2

QUESTION 3..................................................................................................................................4

a) Presenting two ethical consideration provided by Institute of Management Accountants

(IMA) Statement of Ethical Professional practice.......................................................................4

b) Applying the principle for Pro bono work..............................................................................4

QUESTION 4..................................................................................................................................5

A Value of closing inventory under absorption costing..............................................................5

B Difference between profit in absorption and variable costing and which has higher profit

with reason...................................................................................................................................5

C Things management must do if they are planning on improving operation profit through

stock build up...............................................................................................................................6

QUESTION- 5.................................................................................................................................7

a)..................................................................................................................................................7

b) Assessing alternatives does the department have for attaining this return..............................8

QUESTION: 6.................................................................................................................................8

REFERENCES..............................................................................................................................10

QUESTION 1..................................................................................................................................1

a)..................................................................................................................................................1

b)..................................................................................................................................................1

c)..................................................................................................................................................1

d)..................................................................................................................................................1

QUESTION 2..................................................................................................................................2

a....................................................................................................................................................2

b...................................................................................................................................................2

C...................................................................................................................................................2

QUESTION 3..................................................................................................................................4

a) Presenting two ethical consideration provided by Institute of Management Accountants

(IMA) Statement of Ethical Professional practice.......................................................................4

b) Applying the principle for Pro bono work..............................................................................4

QUESTION 4..................................................................................................................................5

A Value of closing inventory under absorption costing..............................................................5

B Difference between profit in absorption and variable costing and which has higher profit

with reason...................................................................................................................................5

C Things management must do if they are planning on improving operation profit through

stock build up...............................................................................................................................6

QUESTION- 5.................................................................................................................................7

a)..................................................................................................................................................7

b) Assessing alternatives does the department have for attaining this return..............................8

QUESTION: 6.................................................................................................................................8

REFERENCES..............................................................................................................................10

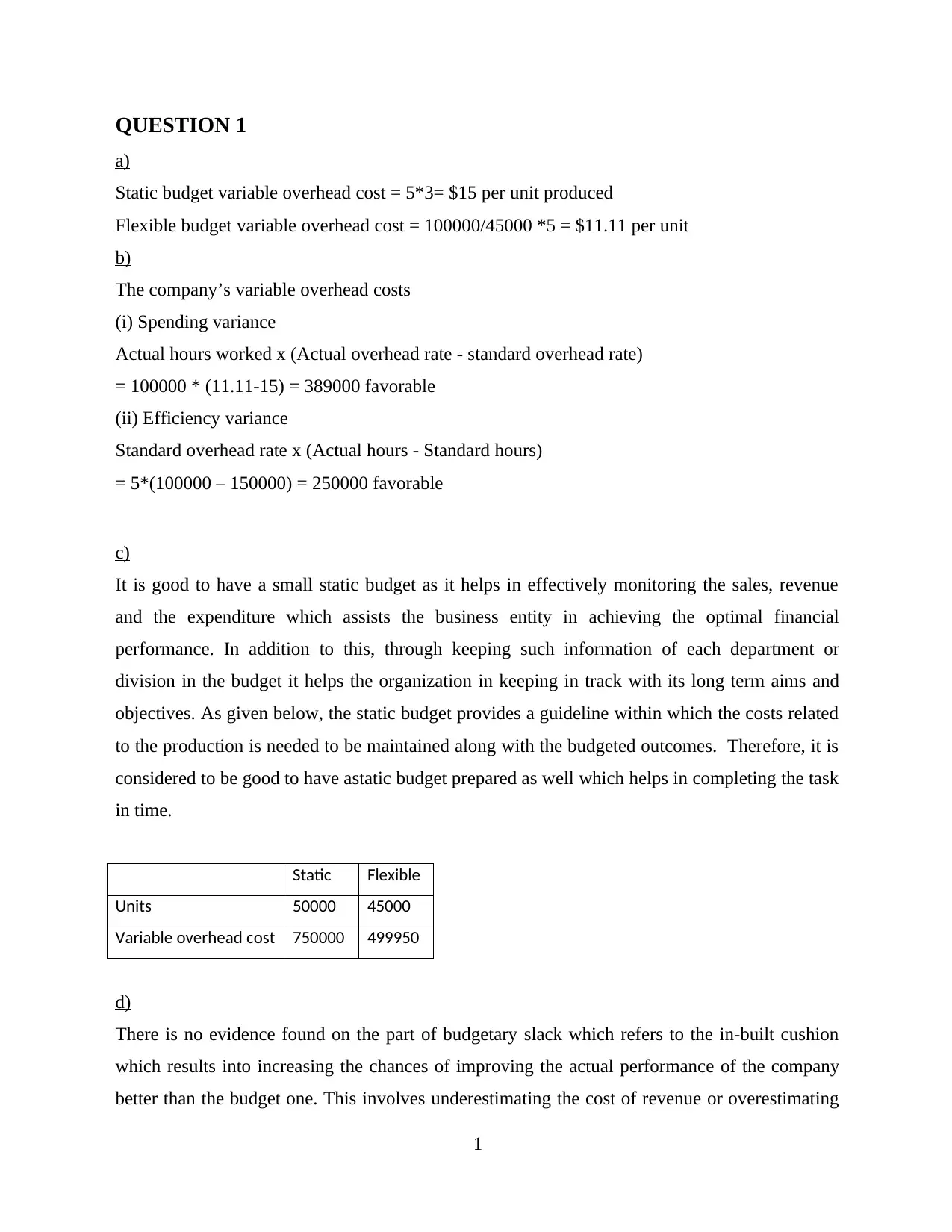

QUESTION 1

a)

Static budget variable overhead cost = 5*3= $15 per unit produced

Flexible budget variable overhead cost = 100000/45000 *5 = $11.11 per unit

b)

The company’s variable overhead costs

(i) Spending variance

Actual hours worked x (Actual overhead rate - standard overhead rate)

= 100000 * (11.11-15) = 389000 favorable

(ii) Efficiency variance

Standard overhead rate x (Actual hours - Standard hours)

= 5*(100000 – 150000) = 250000 favorable

c)

It is good to have a small static budget as it helps in effectively monitoring the sales, revenue

and the expenditure which assists the business entity in achieving the optimal financial

performance. In addition to this, through keeping such information of each department or

division in the budget it helps the organization in keeping in track with its long term aims and

objectives. As given below, the static budget provides a guideline within which the costs related

to the production is needed to be maintained along with the budgeted outcomes. Therefore, it is

considered to be good to have astatic budget prepared as well which helps in completing the task

in time.

Static Flexible

Units 50000 45000

Variable overhead cost 750000 499950

d)

There is no evidence found on the part of budgetary slack which refers to the in-built cushion

which results into increasing the chances of improving the actual performance of the company

better than the budget one. This involves underestimating the cost of revenue or overestimating

1

a)

Static budget variable overhead cost = 5*3= $15 per unit produced

Flexible budget variable overhead cost = 100000/45000 *5 = $11.11 per unit

b)

The company’s variable overhead costs

(i) Spending variance

Actual hours worked x (Actual overhead rate - standard overhead rate)

= 100000 * (11.11-15) = 389000 favorable

(ii) Efficiency variance

Standard overhead rate x (Actual hours - Standard hours)

= 5*(100000 – 150000) = 250000 favorable

c)

It is good to have a small static budget as it helps in effectively monitoring the sales, revenue

and the expenditure which assists the business entity in achieving the optimal financial

performance. In addition to this, through keeping such information of each department or

division in the budget it helps the organization in keeping in track with its long term aims and

objectives. As given below, the static budget provides a guideline within which the costs related

to the production is needed to be maintained along with the budgeted outcomes. Therefore, it is

considered to be good to have astatic budget prepared as well which helps in completing the task

in time.

Static Flexible

Units 50000 45000

Variable overhead cost 750000 499950

d)

There is no evidence found on the part of budgetary slack which refers to the in-built cushion

which results into increasing the chances of improving the actual performance of the company

better than the budget one. This involves underestimating the cost of revenue or overestimating

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the expenses which results into reducing the budget or making it less competitive in nature. This

leads to making it easy for the management or the divisions to enhance their performance. In the

given case, the actual outcome is less than the budgeted one which clearly states there is no such

thing like the budgetary slack is being done by the management of the company.

QUESTION 2

a.

Manufacturing overheads is relating with all indirect cost incurred during the production

process. It is included in unit produced within reporting period. In addition to this, it does not

comprise any selling & administration function of business. For example- salary of maintenance

personnel, rent of the factory building, property taxes on the production facility. These are

included in head of manufacturing overheads because it’s all are indirect expenses that is not

concerned with unit’s production cost therefore it is also known as factory overheads.

b.

It is identified that there is situation of under applied overhead which reflects that actual

cost to produce the goods sold was higher than anticipated. It presents that not enough cost has

been applied to jobs during the period & therefore COGS was understated. Its cause can be

found when overhead rate is not accurate. It mainly occurs in managerial process due to errors

in estimating the predetermined overhead rate which is crucial for deriving significant function

of company process. This can be easily identified by organization via focus on debit side which

is exceed than credits that is causing under applied situation in company (Under- or Over-

Applied Overhead, 2021). In order to make treatment regarding the under applied cost focus is

giving on actual cost as kit is recorded on debit side of manufacturing overhead account.

Increasing the expenses on the income statement and decreasing that period’s net income. In

cost of goods sold, under applied expenses are usually recorded by inputting a debit to COGS

section by the end of year. When there is any specific adjustment is made it is basically added to

cost of goods sold as in case of over applied it is reduced from COGS. Under applied are

basically disposed off by allocating to cost of goods sold account by transferring.

C.

From the evaluation of particular case it can be identified that there is situation of

overestimate as the budgeted cost for factory overhead is 90000 and actual given is 70000 that is

interpretation that company has over applied its cost. it can also be understood that labor hour

2

leads to making it easy for the management or the divisions to enhance their performance. In the

given case, the actual outcome is less than the budgeted one which clearly states there is no such

thing like the budgetary slack is being done by the management of the company.

QUESTION 2

a.

Manufacturing overheads is relating with all indirect cost incurred during the production

process. It is included in unit produced within reporting period. In addition to this, it does not

comprise any selling & administration function of business. For example- salary of maintenance

personnel, rent of the factory building, property taxes on the production facility. These are

included in head of manufacturing overheads because it’s all are indirect expenses that is not

concerned with unit’s production cost therefore it is also known as factory overheads.

b.

It is identified that there is situation of under applied overhead which reflects that actual

cost to produce the goods sold was higher than anticipated. It presents that not enough cost has

been applied to jobs during the period & therefore COGS was understated. Its cause can be

found when overhead rate is not accurate. It mainly occurs in managerial process due to errors

in estimating the predetermined overhead rate which is crucial for deriving significant function

of company process. This can be easily identified by organization via focus on debit side which

is exceed than credits that is causing under applied situation in company (Under- or Over-

Applied Overhead, 2021). In order to make treatment regarding the under applied cost focus is

giving on actual cost as kit is recorded on debit side of manufacturing overhead account.

Increasing the expenses on the income statement and decreasing that period’s net income. In

cost of goods sold, under applied expenses are usually recorded by inputting a debit to COGS

section by the end of year. When there is any specific adjustment is made it is basically added to

cost of goods sold as in case of over applied it is reduced from COGS. Under applied are

basically disposed off by allocating to cost of goods sold account by transferring.

C.

From the evaluation of particular case it can be identified that there is situation of

overestimate as the budgeted cost for factory overhead is 90000 and actual given is 70000 that is

interpretation that company has over applied its cost. it can also be understood that labor hour

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

given area s well very high than actual progress and utilization of labor in company. It becomes

crucial for giving concentration on over applied budgetary cost as it gives insights about way of

working of specified organization.

3

crucial for giving concentration on over applied budgetary cost as it gives insights about way of

working of specified organization.

3

QUESTION 3

a) Presenting two ethical consideration provided by Institute of Management Accountants (IMA)

Statement of Ethical Professional practice

Confidentiality: The information should be kept confidential that helps to protect the

overall sensitive data to being misused. Also, as per the IMA, it is necessary for the company to

keep the information confidential except when disclosure is authorized or legally required (IMA

Statement of ethical Professional Practice, 2020). Moreover, it is also necessary to inform

relevant parties regarding use of confidential information and also management should monitor

to ensure compliance. In addition to this, if such data cannot be kept confidential, then it will

lead to cause illegal advantage.

Credibility: It is necessary to communicate the information in accurate many and also

provide relevant information otherwise it would lead to influence the understanding of the

report. Further, management is also responsible to communicate entire professional limitation or

other constraints, otherwise it will lead to affect the performance of entire activity. Under this

standard, report any delays regarding information and internal control while implementing any

new law or policy, entire process should be communicated properly.

b) Applying the principle for Pro bono work

George also comply the two ethical standards and this is why, he did not disclose his

work experience in mining industry. He already knows the principle mentioned under IMA,

Statement of ethical professional practice and that is why, work for pro bono in order to get a

promotion (Lee, 2020). In the same way, George did not disclose the information about pro bono

work and as a result, the principle is compiled without any jeopardizing. Further, it has been

analyzed that the confidential information should not use for a personal advantage Apart from

this, credibility (another ethical standard) should also be complied and that is why, George

should properly communicate with their senior management about their working and do not

share any confidential data with anyone that might cause opposite impact. This further helps to

resolve the conflicts because it is the application of fundamental principle that improve the

performance of a business. Thus, adhering with such ethical consideration will help a George to

improve the growth as well.

4

a) Presenting two ethical consideration provided by Institute of Management Accountants (IMA)

Statement of Ethical Professional practice

Confidentiality: The information should be kept confidential that helps to protect the

overall sensitive data to being misused. Also, as per the IMA, it is necessary for the company to

keep the information confidential except when disclosure is authorized or legally required (IMA

Statement of ethical Professional Practice, 2020). Moreover, it is also necessary to inform

relevant parties regarding use of confidential information and also management should monitor

to ensure compliance. In addition to this, if such data cannot be kept confidential, then it will

lead to cause illegal advantage.

Credibility: It is necessary to communicate the information in accurate many and also

provide relevant information otherwise it would lead to influence the understanding of the

report. Further, management is also responsible to communicate entire professional limitation or

other constraints, otherwise it will lead to affect the performance of entire activity. Under this

standard, report any delays regarding information and internal control while implementing any

new law or policy, entire process should be communicated properly.

b) Applying the principle for Pro bono work

George also comply the two ethical standards and this is why, he did not disclose his

work experience in mining industry. He already knows the principle mentioned under IMA,

Statement of ethical professional practice and that is why, work for pro bono in order to get a

promotion (Lee, 2020). In the same way, George did not disclose the information about pro bono

work and as a result, the principle is compiled without any jeopardizing. Further, it has been

analyzed that the confidential information should not use for a personal advantage Apart from

this, credibility (another ethical standard) should also be complied and that is why, George

should properly communicate with their senior management about their working and do not

share any confidential data with anyone that might cause opposite impact. This further helps to

resolve the conflicts because it is the application of fundamental principle that improve the

performance of a business. Thus, adhering with such ethical consideration will help a George to

improve the growth as well.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

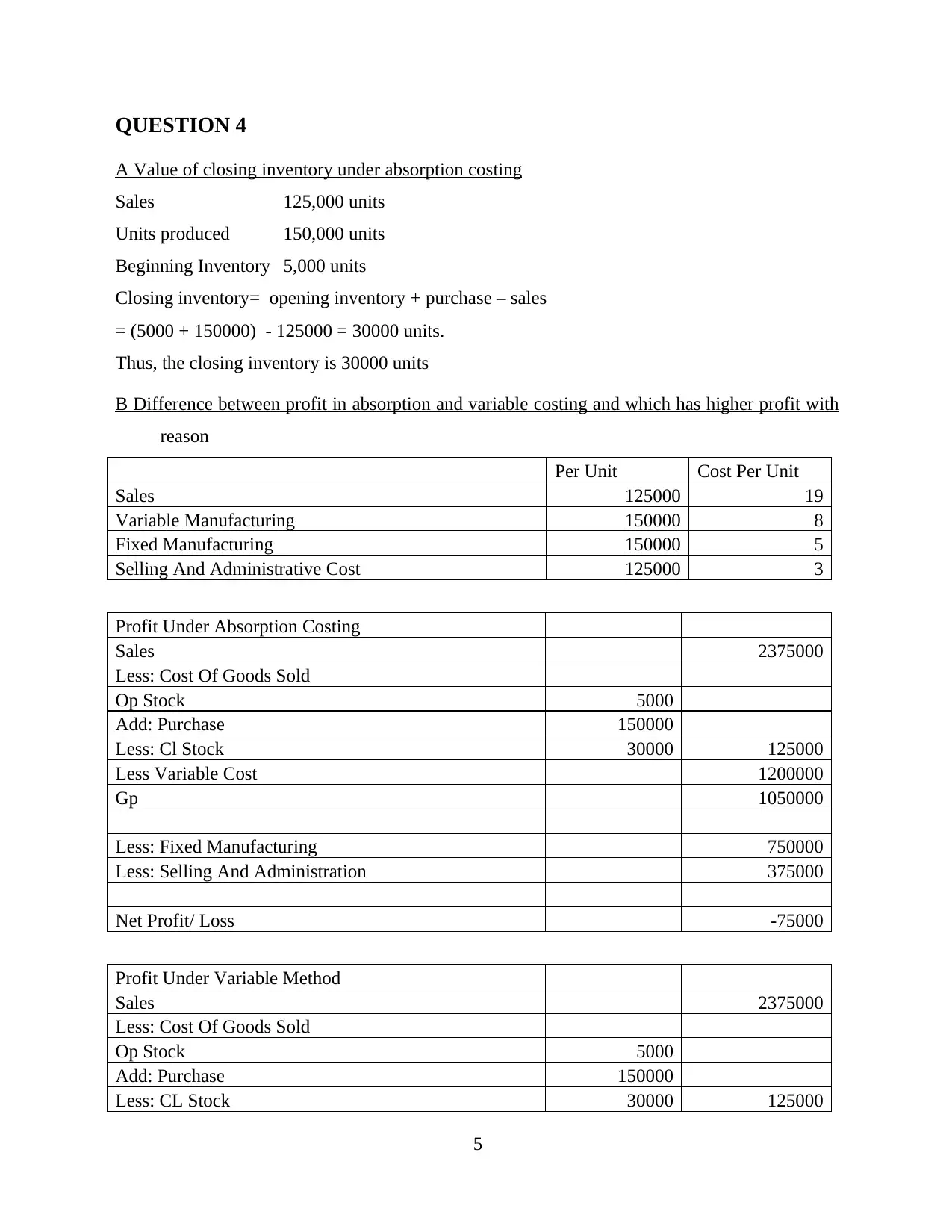

QUESTION 4

A Value of closing inventory under absorption costing

Sales 125,000 units

Units produced 150,000 units

Beginning Inventory 5,000 units

Closing inventory= opening inventory + purchase – sales

= (5000 + 150000) - 125000 = 30000 units.

Thus, the closing inventory is 30000 units

B Difference between profit in absorption and variable costing and which has higher profit with

reason

Per Unit Cost Per Unit

Sales 125000 19

Variable Manufacturing 150000 8

Fixed Manufacturing 150000 5

Selling And Administrative Cost 125000 3

Profit Under Absorption Costing

Sales 2375000

Less: Cost Of Goods Sold

Op Stock 5000

Add: Purchase 150000

Less: Cl Stock 30000 125000

Less Variable Cost 1200000

Gp 1050000

Less: Fixed Manufacturing 750000

Less: Selling And Administration 375000

Net Profit/ Loss -75000

Profit Under Variable Method

Sales 2375000

Less: Cost Of Goods Sold

Op Stock 5000

Add: Purchase 150000

Less: CL Stock 30000 125000

5

A Value of closing inventory under absorption costing

Sales 125,000 units

Units produced 150,000 units

Beginning Inventory 5,000 units

Closing inventory= opening inventory + purchase – sales

= (5000 + 150000) - 125000 = 30000 units.

Thus, the closing inventory is 30000 units

B Difference between profit in absorption and variable costing and which has higher profit with

reason

Per Unit Cost Per Unit

Sales 125000 19

Variable Manufacturing 150000 8

Fixed Manufacturing 150000 5

Selling And Administrative Cost 125000 3

Profit Under Absorption Costing

Sales 2375000

Less: Cost Of Goods Sold

Op Stock 5000

Add: Purchase 150000

Less: Cl Stock 30000 125000

Less Variable Cost 1200000

Gp 1050000

Less: Fixed Manufacturing 750000

Less: Selling And Administration 375000

Net Profit/ Loss -75000

Profit Under Variable Method

Sales 2375000

Less: Cost Of Goods Sold

Op Stock 5000

Add: Purchase 150000

Less: CL Stock 30000 125000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

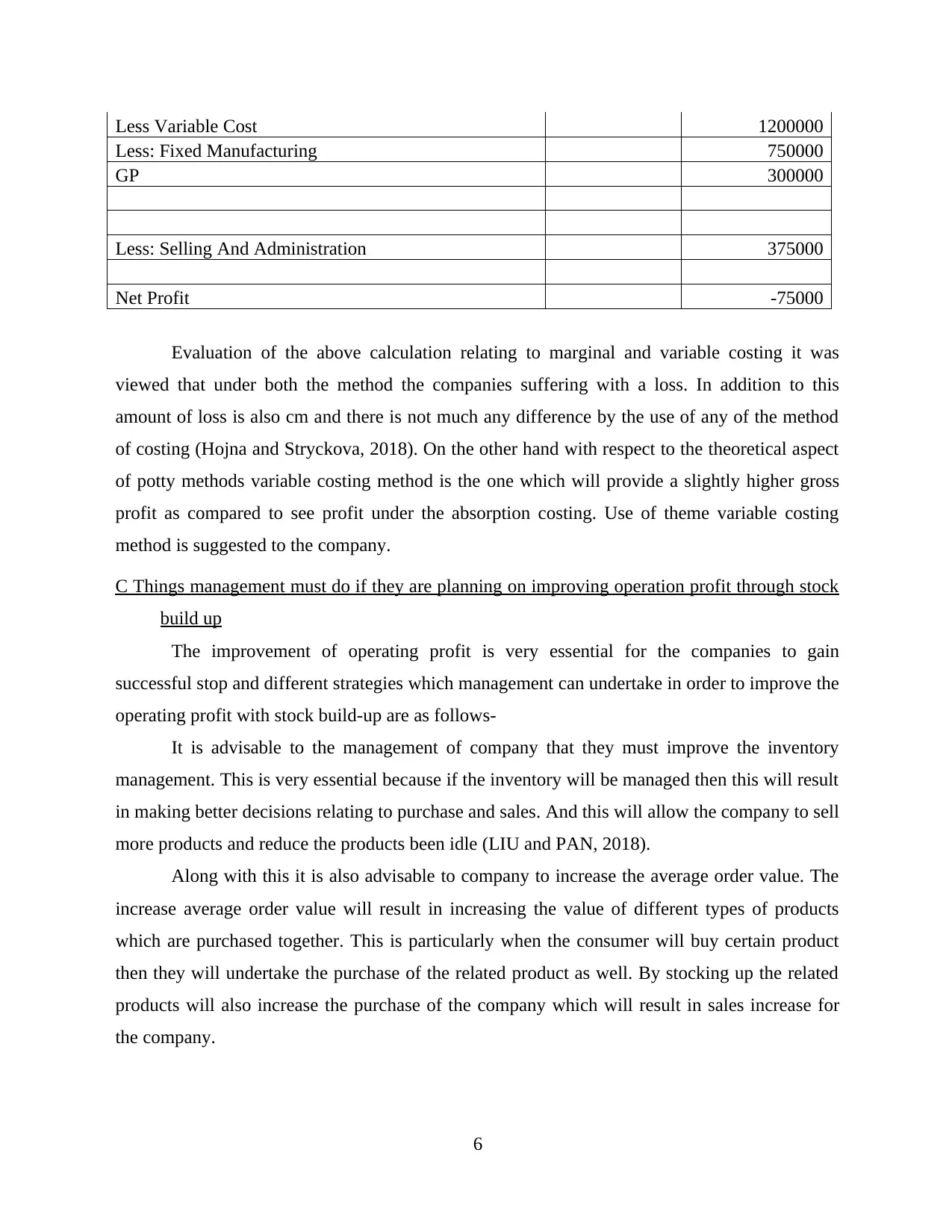

Less Variable Cost 1200000

Less: Fixed Manufacturing 750000

GP 300000

Less: Selling And Administration 375000

Net Profit -75000

Evaluation of the above calculation relating to marginal and variable costing it was

viewed that under both the method the companies suffering with a loss. In addition to this

amount of loss is also cm and there is not much any difference by the use of any of the method

of costing (Hojna and Stryckova, 2018). On the other hand with respect to the theoretical aspect

of potty methods variable costing method is the one which will provide a slightly higher gross

profit as compared to see profit under the absorption costing. Use of theme variable costing

method is suggested to the company.

C Things management must do if they are planning on improving operation profit through stock

build up

The improvement of operating profit is very essential for the companies to gain

successful stop and different strategies which management can undertake in order to improve the

operating profit with stock build-up are as follows-

It is advisable to the management of company that they must improve the inventory

management. This is very essential because if the inventory will be managed then this will result

in making better decisions relating to purchase and sales. And this will allow the company to sell

more products and reduce the products been idle (LIU and PAN, 2018).

Along with this it is also advisable to company to increase the average order value. The

increase average order value will result in increasing the value of different types of products

which are purchased together. This is particularly when the consumer will buy certain product

then they will undertake the purchase of the related product as well. By stocking up the related

products will also increase the purchase of the company which will result in sales increase for

the company.

6

Less: Fixed Manufacturing 750000

GP 300000

Less: Selling And Administration 375000

Net Profit -75000

Evaluation of the above calculation relating to marginal and variable costing it was

viewed that under both the method the companies suffering with a loss. In addition to this

amount of loss is also cm and there is not much any difference by the use of any of the method

of costing (Hojna and Stryckova, 2018). On the other hand with respect to the theoretical aspect

of potty methods variable costing method is the one which will provide a slightly higher gross

profit as compared to see profit under the absorption costing. Use of theme variable costing

method is suggested to the company.

C Things management must do if they are planning on improving operation profit through stock

build up

The improvement of operating profit is very essential for the companies to gain

successful stop and different strategies which management can undertake in order to improve the

operating profit with stock build-up are as follows-

It is advisable to the management of company that they must improve the inventory

management. This is very essential because if the inventory will be managed then this will result

in making better decisions relating to purchase and sales. And this will allow the company to sell

more products and reduce the products been idle (LIU and PAN, 2018).

Along with this it is also advisable to company to increase the average order value. The

increase average order value will result in increasing the value of different types of products

which are purchased together. This is particularly when the consumer will buy certain product

then they will undertake the purchase of the related product as well. By stocking up the related

products will also increase the purchase of the company which will result in sales increase for

the company.

6

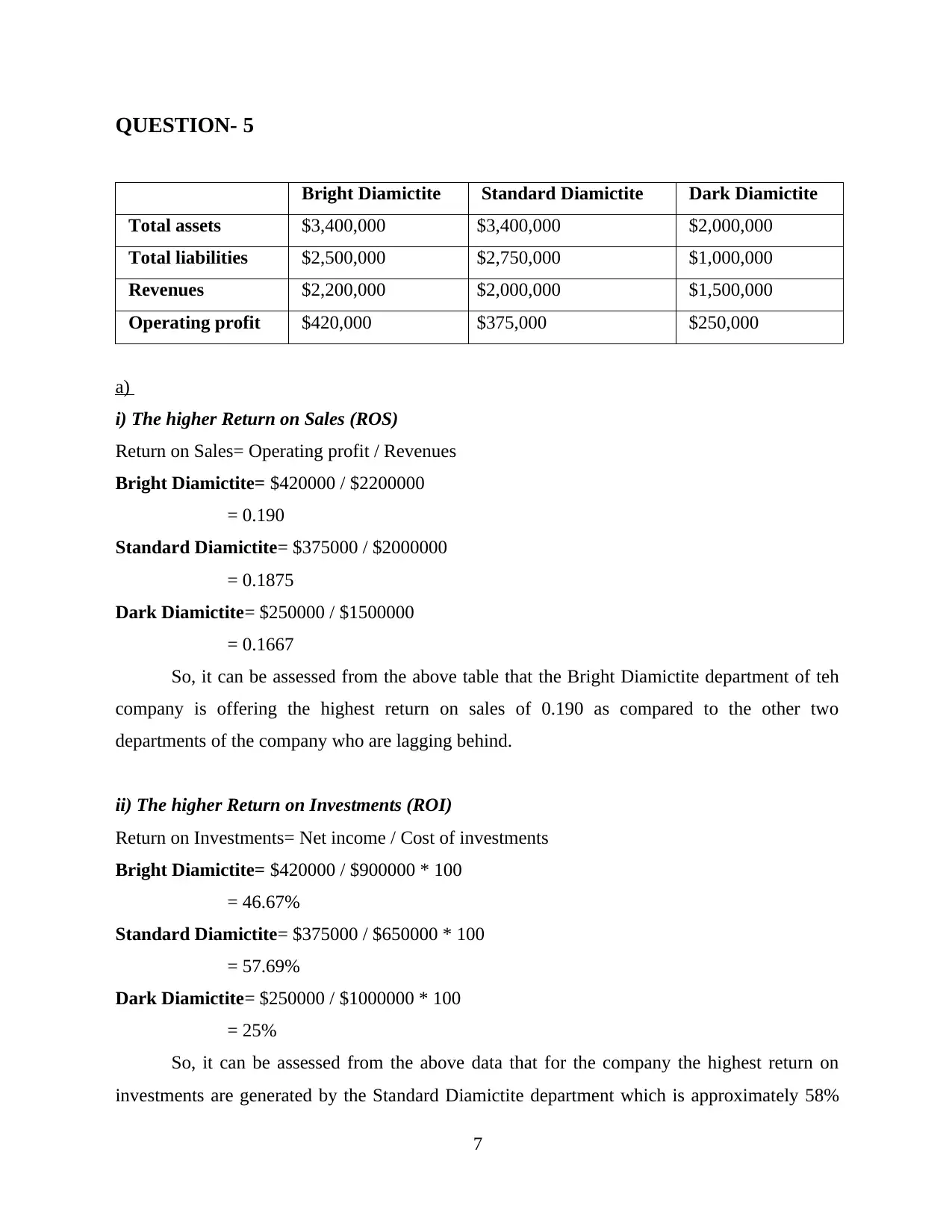

QUESTION- 5

Bright Diamictite Standard Diamictite Dark Diamictite

Total assets $3,400,000 $3,400,000 $2,000,000

Total liabilities $2,500,000 $2,750,000 $1,000,000

Revenues $2,200,000 $2,000,000 $1,500,000

Operating profit $420,000 $375,000 $250,000

a)

i) The higher Return on Sales (ROS)

Return on Sales= Operating profit / Revenues

Bright Diamictite= $420000 / $2200000

= 0.190

Standard Diamictite= $375000 / $2000000

= 0.1875

Dark Diamictite= $250000 / $1500000

= 0.1667

So, it can be assessed from the above table that the Bright Diamictite department of teh

company is offering the highest return on sales of 0.190 as compared to the other two

departments of the company who are lagging behind.

ii) The higher Return on Investments (ROI)

Return on Investments= Net income / Cost of investments

Bright Diamictite= $420000 / $900000 * 100

= 46.67%

Standard Diamictite= $375000 / $650000 * 100

= 57.69%

Dark Diamictite= $250000 / $1000000 * 100

= 25%

So, it can be assessed from the above data that for the company the highest return on

investments are generated by the Standard Diamictite department which is approximately 58%

7

Bright Diamictite Standard Diamictite Dark Diamictite

Total assets $3,400,000 $3,400,000 $2,000,000

Total liabilities $2,500,000 $2,750,000 $1,000,000

Revenues $2,200,000 $2,000,000 $1,500,000

Operating profit $420,000 $375,000 $250,000

a)

i) The higher Return on Sales (ROS)

Return on Sales= Operating profit / Revenues

Bright Diamictite= $420000 / $2200000

= 0.190

Standard Diamictite= $375000 / $2000000

= 0.1875

Dark Diamictite= $250000 / $1500000

= 0.1667

So, it can be assessed from the above table that the Bright Diamictite department of teh

company is offering the highest return on sales of 0.190 as compared to the other two

departments of the company who are lagging behind.

ii) The higher Return on Investments (ROI)

Return on Investments= Net income / Cost of investments

Bright Diamictite= $420000 / $900000 * 100

= 46.67%

Standard Diamictite= $375000 / $650000 * 100

= 57.69%

Dark Diamictite= $250000 / $1000000 * 100

= 25%

So, it can be assessed from the above data that for the company the highest return on

investments are generated by the Standard Diamictite department which is approximately 58%

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

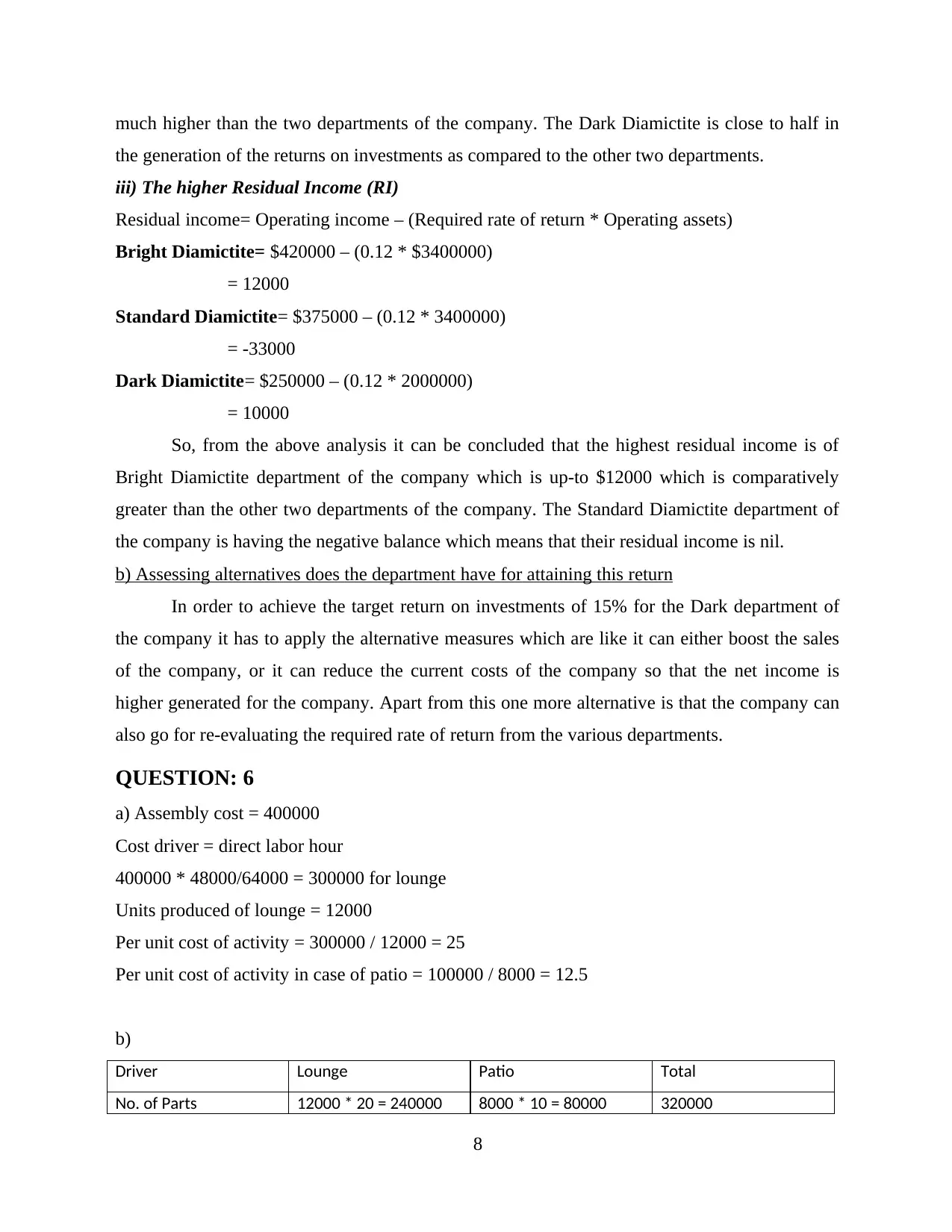

much higher than the two departments of the company. The Dark Diamictite is close to half in

the generation of the returns on investments as compared to the other two departments.

iii) The higher Residual Income (RI)

Residual income= Operating income – (Required rate of return * Operating assets)

Bright Diamictite= $420000 – (0.12 * $3400000)

= 12000

Standard Diamictite= $375000 – (0.12 * 3400000)

= -33000

Dark Diamictite= $250000 – (0.12 * 2000000)

= 10000

So, from the above analysis it can be concluded that the highest residual income is of

Bright Diamictite department of the company which is up-to $12000 which is comparatively

greater than the other two departments of the company. The Standard Diamictite department of

the company is having the negative balance which means that their residual income is nil.

b) Assessing alternatives does the department have for attaining this return

In order to achieve the target return on investments of 15% for the Dark department of

the company it has to apply the alternative measures which are like it can either boost the sales

of the company, or it can reduce the current costs of the company so that the net income is

higher generated for the company. Apart from this one more alternative is that the company can

also go for re-evaluating the required rate of return from the various departments.

QUESTION: 6

a) Assembly cost = 400000

Cost driver = direct labor hour

400000 * 48000/64000 = 300000 for lounge

Units produced of lounge = 12000

Per unit cost of activity = 300000 / 12000 = 25

Per unit cost of activity in case of patio = 100000 / 8000 = 12.5

b)

Driver Lounge Patio Total

No. of Parts 12000 * 20 = 240000 8000 * 10 = 80000 320000

8

the generation of the returns on investments as compared to the other two departments.

iii) The higher Residual Income (RI)

Residual income= Operating income – (Required rate of return * Operating assets)

Bright Diamictite= $420000 – (0.12 * $3400000)

= 12000

Standard Diamictite= $375000 – (0.12 * 3400000)

= -33000

Dark Diamictite= $250000 – (0.12 * 2000000)

= 10000

So, from the above analysis it can be concluded that the highest residual income is of

Bright Diamictite department of the company which is up-to $12000 which is comparatively

greater than the other two departments of the company. The Standard Diamictite department of

the company is having the negative balance which means that their residual income is nil.

b) Assessing alternatives does the department have for attaining this return

In order to achieve the target return on investments of 15% for the Dark department of

the company it has to apply the alternative measures which are like it can either boost the sales

of the company, or it can reduce the current costs of the company so that the net income is

higher generated for the company. Apart from this one more alternative is that the company can

also go for re-evaluating the required rate of return from the various departments.

QUESTION: 6

a) Assembly cost = 400000

Cost driver = direct labor hour

400000 * 48000/64000 = 300000 for lounge

Units produced of lounge = 12000

Per unit cost of activity = 300000 / 12000 = 25

Per unit cost of activity in case of patio = 100000 / 8000 = 12.5

b)

Driver Lounge Patio Total

No. of Parts 12000 * 20 = 240000 8000 * 10 = 80000 320000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

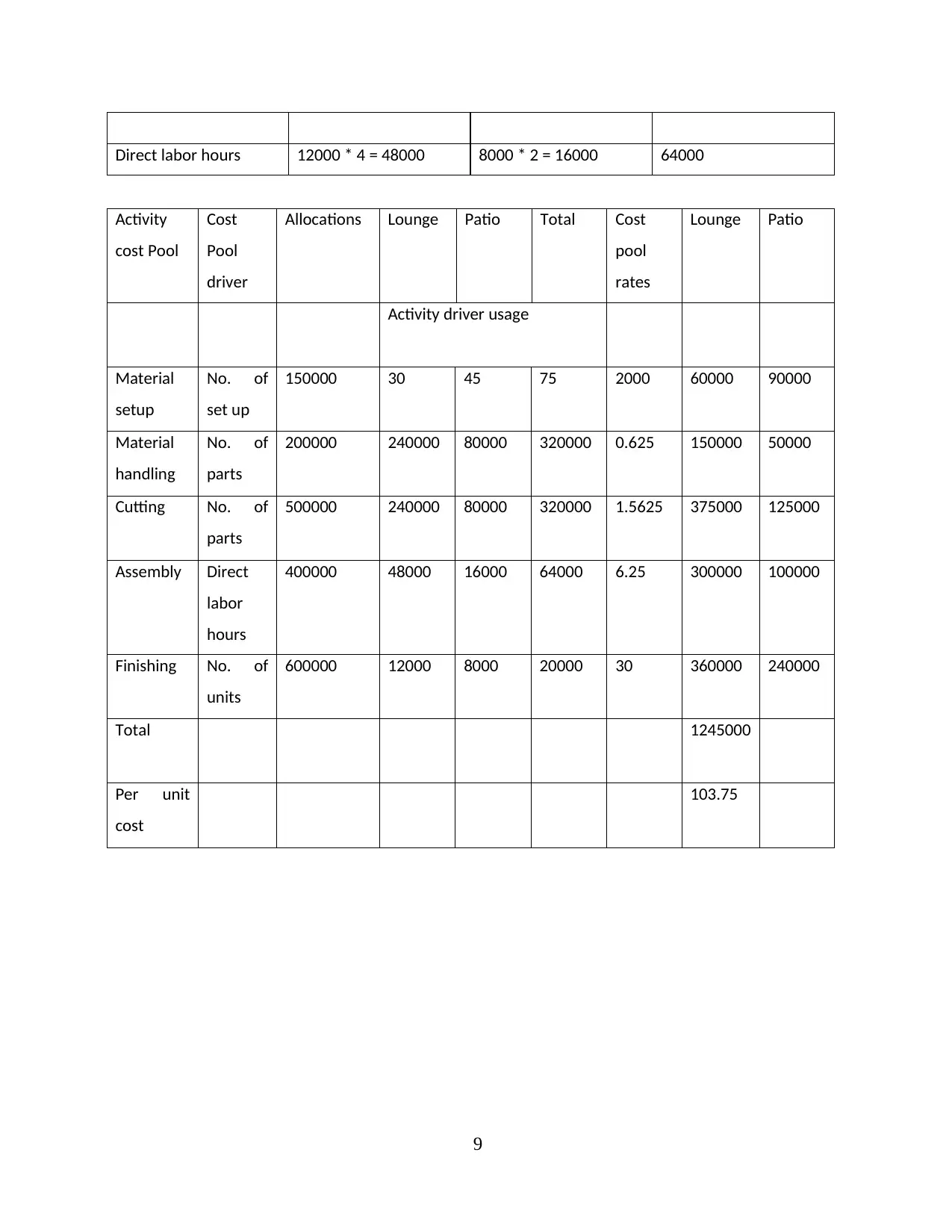

Direct labor hours 12000 * 4 = 48000 8000 * 2 = 16000 64000

Activity

cost Pool

Cost

Pool

driver

Allocations Lounge Patio Total Cost

pool

rates

Lounge Patio

Activity driver usage

Material

setup

No. of

set up

150000 30 45 75 2000 60000 90000

Material

handling

No. of

parts

200000 240000 80000 320000 0.625 150000 50000

Cutting No. of

parts

500000 240000 80000 320000 1.5625 375000 125000

Assembly Direct

labor

hours

400000 48000 16000 64000 6.25 300000 100000

Finishing No. of

units

600000 12000 8000 20000 30 360000 240000

Total 1245000

Per unit

cost

103.75

9

Activity

cost Pool

Cost

Pool

driver

Allocations Lounge Patio Total Cost

pool

rates

Lounge Patio

Activity driver usage

Material

setup

No. of

set up

150000 30 45 75 2000 60000 90000

Material

handling

No. of

parts

200000 240000 80000 320000 0.625 150000 50000

Cutting No. of

parts

500000 240000 80000 320000 1.5625 375000 125000

Assembly Direct

labor

hours

400000 48000 16000 64000 6.25 300000 100000

Finishing No. of

units

600000 12000 8000 20000 30 360000 240000

Total 1245000

Per unit

cost

103.75

9

REFERENCES

Books and Journals

Hojna, R. and Stryckova, L., 2018. ABSORPTION COSTING ANALYSIS AND ITS USE BY

CZECH MANUFACTURING COMPANIES. In 5th International Multidisciplinary

Scientific Conference on social sciences and arts SGEM 2018 (pp. 19-26).

Lee, J. J., 2020. Double Standards: An Empirical Study of Patent and Trademark

Discipline. BCL Rev.,61 p.1613.

LIU, B. and PAN, H.Q., 2018. Comparative Study of Absorption Costing and Variable Costing.

Journal of Qiqihar University (Philosophy & Social Science Edition), p.06.

Online

Under- or Over-Applied Overhead. 2021. Online. Available through:

<https://courses.lumenlearning.com/tcc-managacct/chapter/factory-overhead-calculations/>.

IMA Statement of ethical Professional Practice. 2020. [Online]. Available through:

<https://www.imanet.org/-/media/b6fbeeb74d964e6c9fe654c48456e61f.ashx?

la=en#:~:text=IMA's%20overarching%20ethical%20principles%20include,Fairness%2C

%20Objectivity%2C%20and%20Responsibility.&text=IMA%20members%20have%20a

%20responsibility,may%20result%20in%20disciplinary%20action.>.

10

Books and Journals

Hojna, R. and Stryckova, L., 2018. ABSORPTION COSTING ANALYSIS AND ITS USE BY

CZECH MANUFACTURING COMPANIES. In 5th International Multidisciplinary

Scientific Conference on social sciences and arts SGEM 2018 (pp. 19-26).

Lee, J. J., 2020. Double Standards: An Empirical Study of Patent and Trademark

Discipline. BCL Rev.,61 p.1613.

LIU, B. and PAN, H.Q., 2018. Comparative Study of Absorption Costing and Variable Costing.

Journal of Qiqihar University (Philosophy & Social Science Edition), p.06.

Online

Under- or Over-Applied Overhead. 2021. Online. Available through:

<https://courses.lumenlearning.com/tcc-managacct/chapter/factory-overhead-calculations/>.

IMA Statement of ethical Professional Practice. 2020. [Online]. Available through:

<https://www.imanet.org/-/media/b6fbeeb74d964e6c9fe654c48456e61f.ashx?

la=en#:~:text=IMA's%20overarching%20ethical%20principles%20include,Fairness%2C

%20Objectivity%2C%20and%20Responsibility.&text=IMA%20members%20have%20a

%20responsibility,may%20result%20in%20disciplinary%20action.>.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.