University Finance: Management Accounting Assignment Solution

VerifiedAdded on 2022/08/26

|8

|1270

|14

Homework Assignment

AI Summary

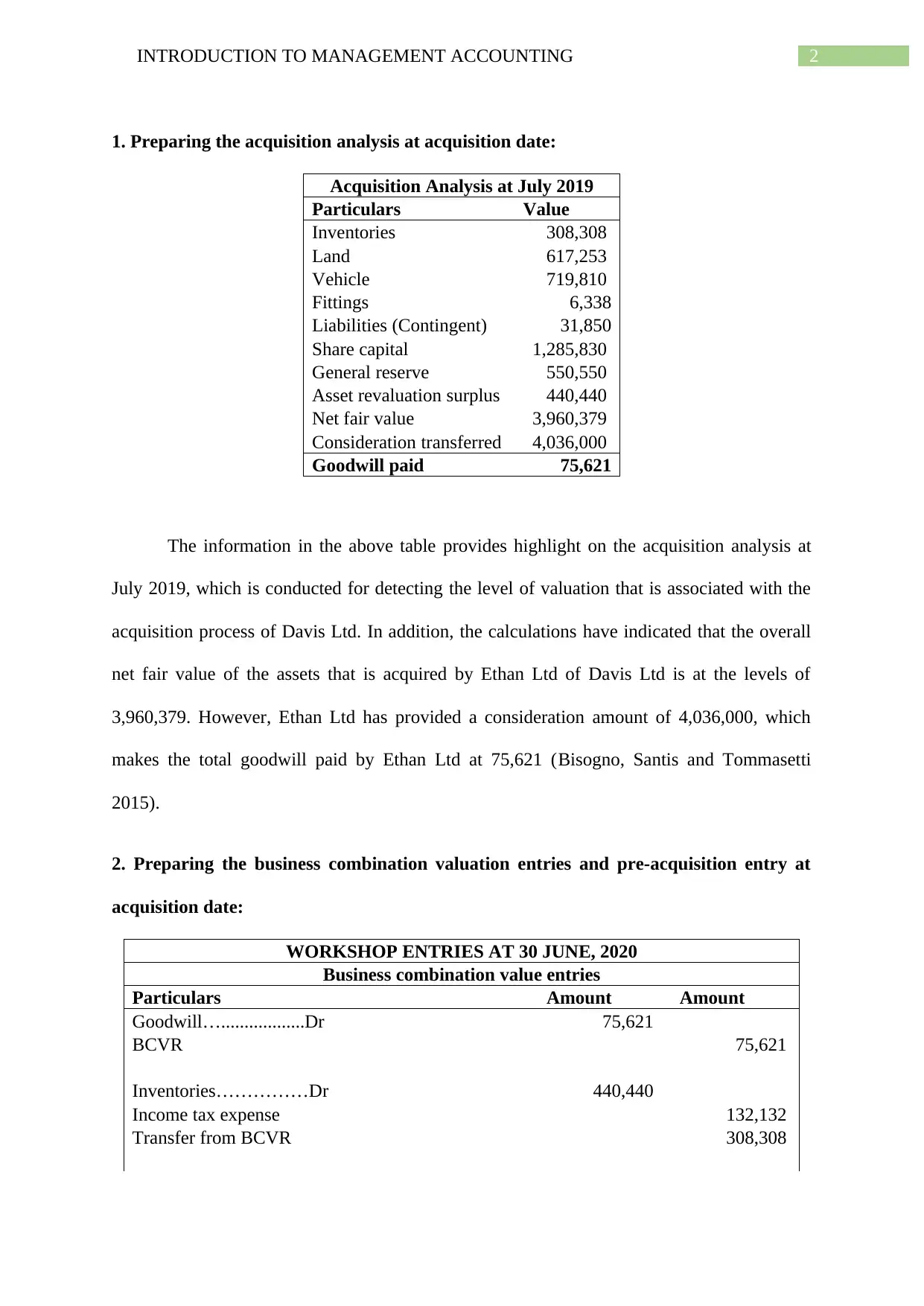

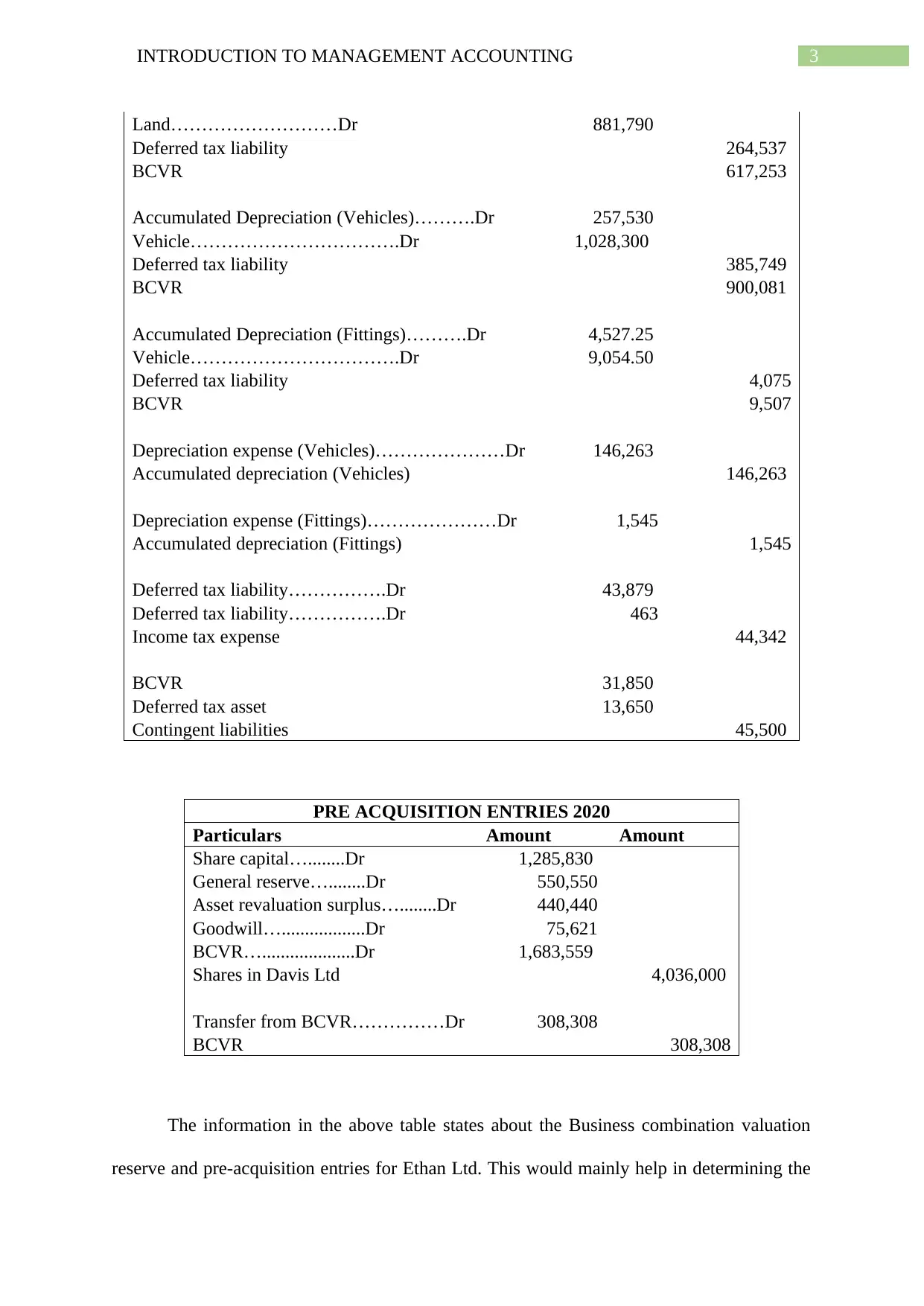

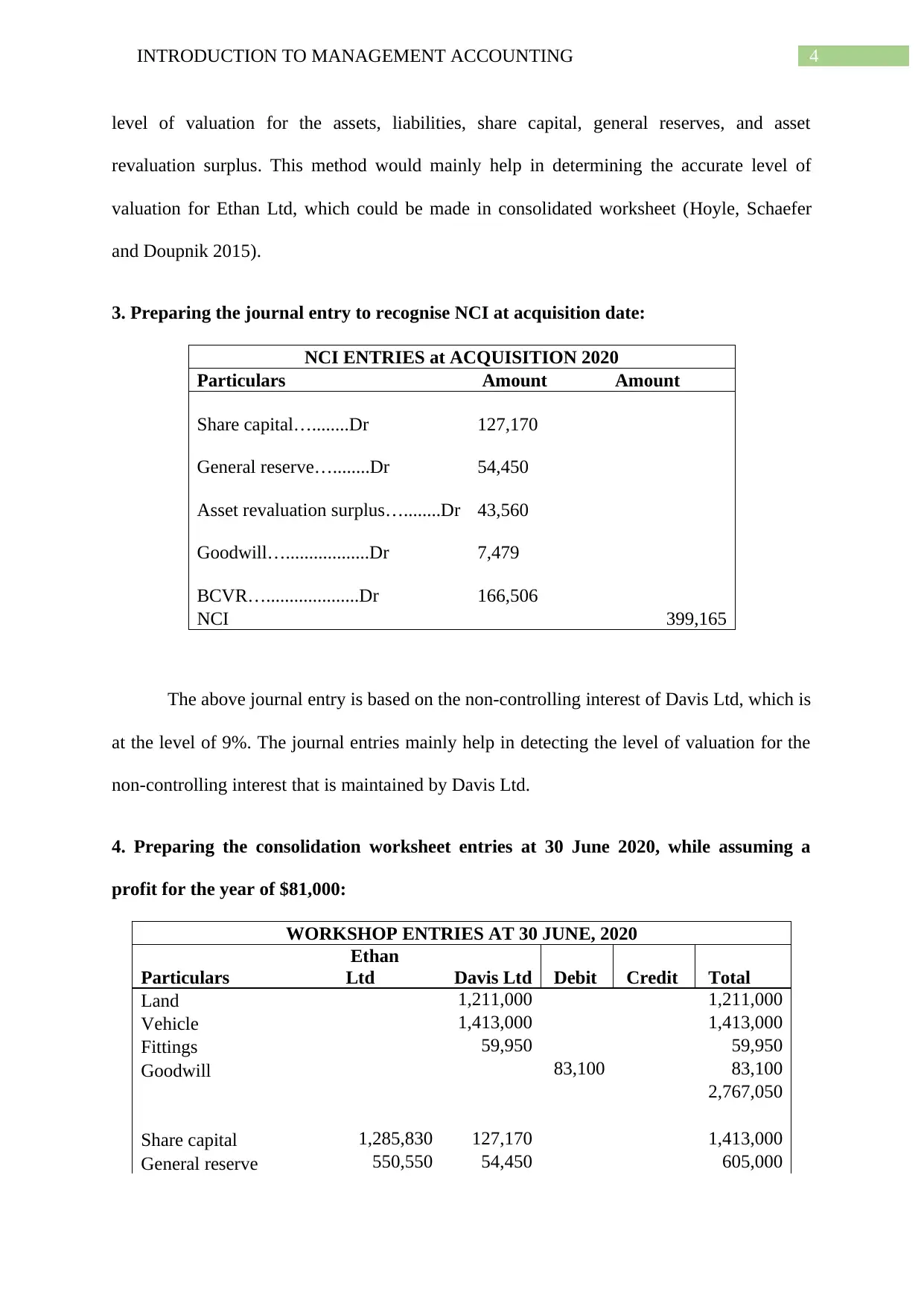

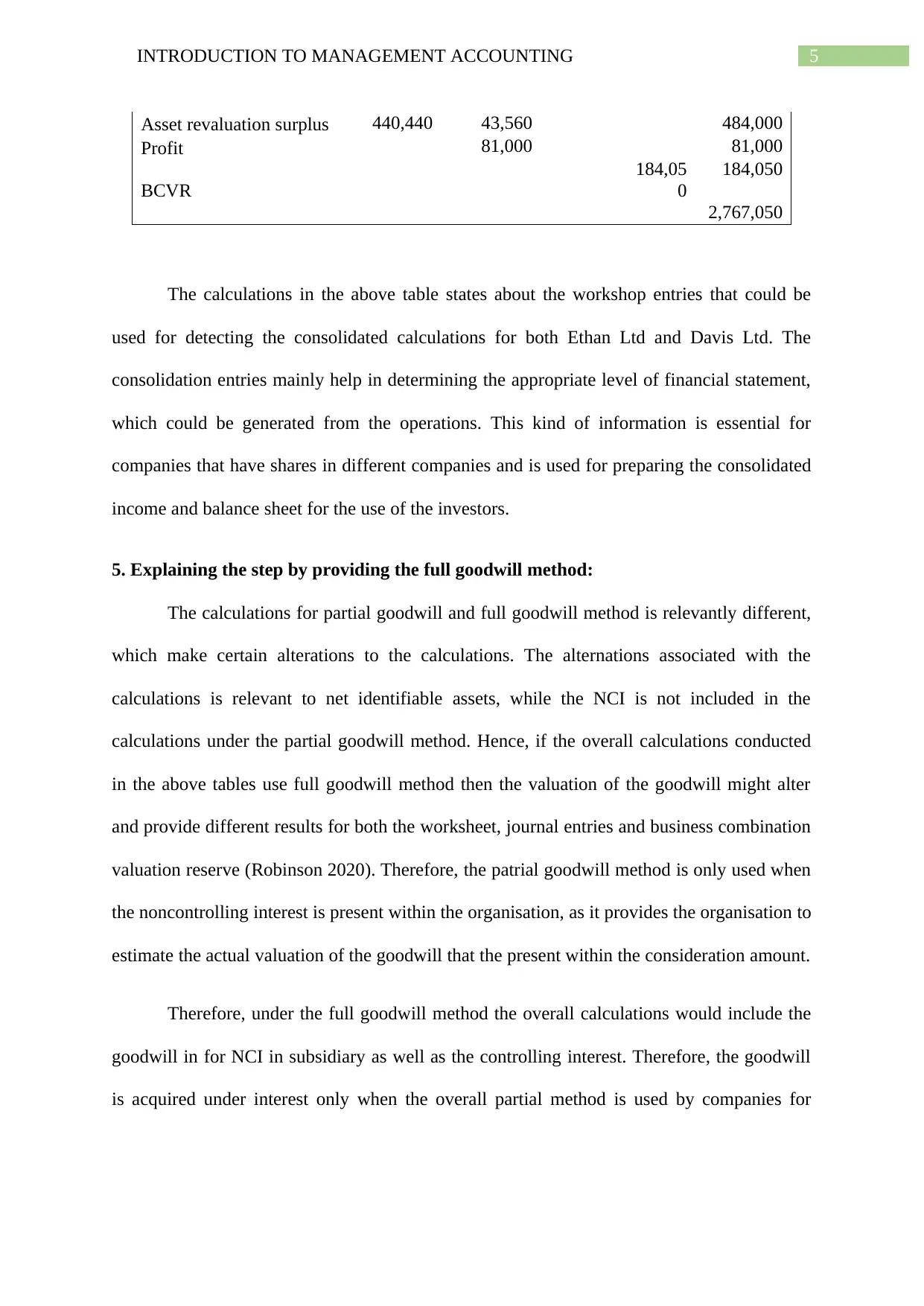

This management accounting assignment solution focuses on business combinations and consolidation. It begins with an acquisition analysis, detailing the valuation of assets and liabilities acquired by Ethan Ltd from Davis Ltd, including the calculation of goodwill. The solution then presents business combination valuation entries and pre-acquisition entries, followed by the journal entry to recognize Non-Controlling Interest (NCI). It provides consolidation worksheet entries, assuming a profit for the year, and explains the full goodwill method, highlighting its impact on goodwill valuation compared to the partial goodwill method. The assignment includes references to academic literature supporting the financial accounting concepts discussed, providing a comprehensive understanding of the topics covered.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.