MAA262 Management Accounting Assignment: Analysis of Stylish Chairs

VerifiedAdded on 2022/09/14

|12

|2132

|16

Homework Assignment

AI Summary

This assignment solution analyzes the case of Stylish Chairs, a company facing challenges in its management accounting processes, particularly cost accounting. The solution addresses several questions, including ethical violations related to the appointment of an unqualified management accountant. It provides detailed calculations and analyses of fixed and variable costs, product costs, and different costing methods, such as marginal and absorption costing. Furthermore, the solution explores the impact of production volume on costs and evaluates the financial implications of further processing options. The analysis also considers overhead allocation methods and their impact on cost management, offering insights into how the company can improve its financial decision-making and profitability. Finally, the assignment covers topics such as the impact of economies of scale and over-allocation of overhead costs.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note

Management Accounting

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGEMENT ACCOUNTING

Table of Contents

Answer to Question 1.....................................................................................................2

Answer to Question 2.....................................................................................................3

Answer to Question 3.....................................................................................................5

Answer to Question 4.....................................................................................................6

Answer to Question 5.....................................................................................................8

Answer to Question 6...................................................................................................10

Reference......................................................................................................................11

MANAGEMENT ACCOUNTING

Table of Contents

Answer to Question 1.....................................................................................................2

Answer to Question 2.....................................................................................................3

Answer to Question 3.....................................................................................................5

Answer to Question 4.....................................................................................................6

Answer to Question 5.....................................................................................................8

Answer to Question 6...................................................................................................10

Reference......................................................................................................................11

2

MANAGEMENT ACCOUNTING

Answer to Question 1

The main purpose of the analysis is proper study the case of Stylish Chairs which is

small company which is engaged in making and selling replicas of an 18th-century rococo chair. The

owners of the business Anni-Frid and Benny are having difficulties in appropriately handling

the management accounting process of the business mainly the cost accounting part and

therefore wishes to appoint an expert to look after the operational process of the business. As

per the case, Bjorn is appointed by the owners who are basically associates with each other.

The owners are expecting that Bjorn would bring about some transparency in the operational

process of the business (Rothaermel, 2016). However, it is to be noted that the competency of

Bjorn is a major issues which is not considered by the owners and this can create a conflict

with the ethical regulations which are applicable on the company. The provisions which are

stated by Competency standards reflects that a management accounting needs to have proper

training and knowledge to perform as a management accountant and the professional should

always thrive to continuous developments. The cases makes it clear that Bjorn does not have

any such skills or qualifications and therefore the company is in violation of the rules which

are formulated by the Institute of Management Accountants.

In pursuance of the duties of a management accountant, all relevant regulations must

be followed by the professional and it should also be ensured that a strict code of conduct is

maintained in the process of the entity (Namnai, Ussahawanitchakit & Janjarasjit, 2015).

Therefore, on an overall basis, it can be said that Bjorn and the company of Stylish chairs are

in violations of the competency standards.

Answer to Question 2

Part a

MANAGEMENT ACCOUNTING

Answer to Question 1

The main purpose of the analysis is proper study the case of Stylish Chairs which is

small company which is engaged in making and selling replicas of an 18th-century rococo chair. The

owners of the business Anni-Frid and Benny are having difficulties in appropriately handling

the management accounting process of the business mainly the cost accounting part and

therefore wishes to appoint an expert to look after the operational process of the business. As

per the case, Bjorn is appointed by the owners who are basically associates with each other.

The owners are expecting that Bjorn would bring about some transparency in the operational

process of the business (Rothaermel, 2016). However, it is to be noted that the competency of

Bjorn is a major issues which is not considered by the owners and this can create a conflict

with the ethical regulations which are applicable on the company. The provisions which are

stated by Competency standards reflects that a management accounting needs to have proper

training and knowledge to perform as a management accountant and the professional should

always thrive to continuous developments. The cases makes it clear that Bjorn does not have

any such skills or qualifications and therefore the company is in violation of the rules which

are formulated by the Institute of Management Accountants.

In pursuance of the duties of a management accountant, all relevant regulations must

be followed by the professional and it should also be ensured that a strict code of conduct is

maintained in the process of the entity (Namnai, Ussahawanitchakit & Janjarasjit, 2015).

Therefore, on an overall basis, it can be said that Bjorn and the company of Stylish chairs are

in violations of the competency standards.

Answer to Question 2

Part a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGEMENT ACCOUNTING

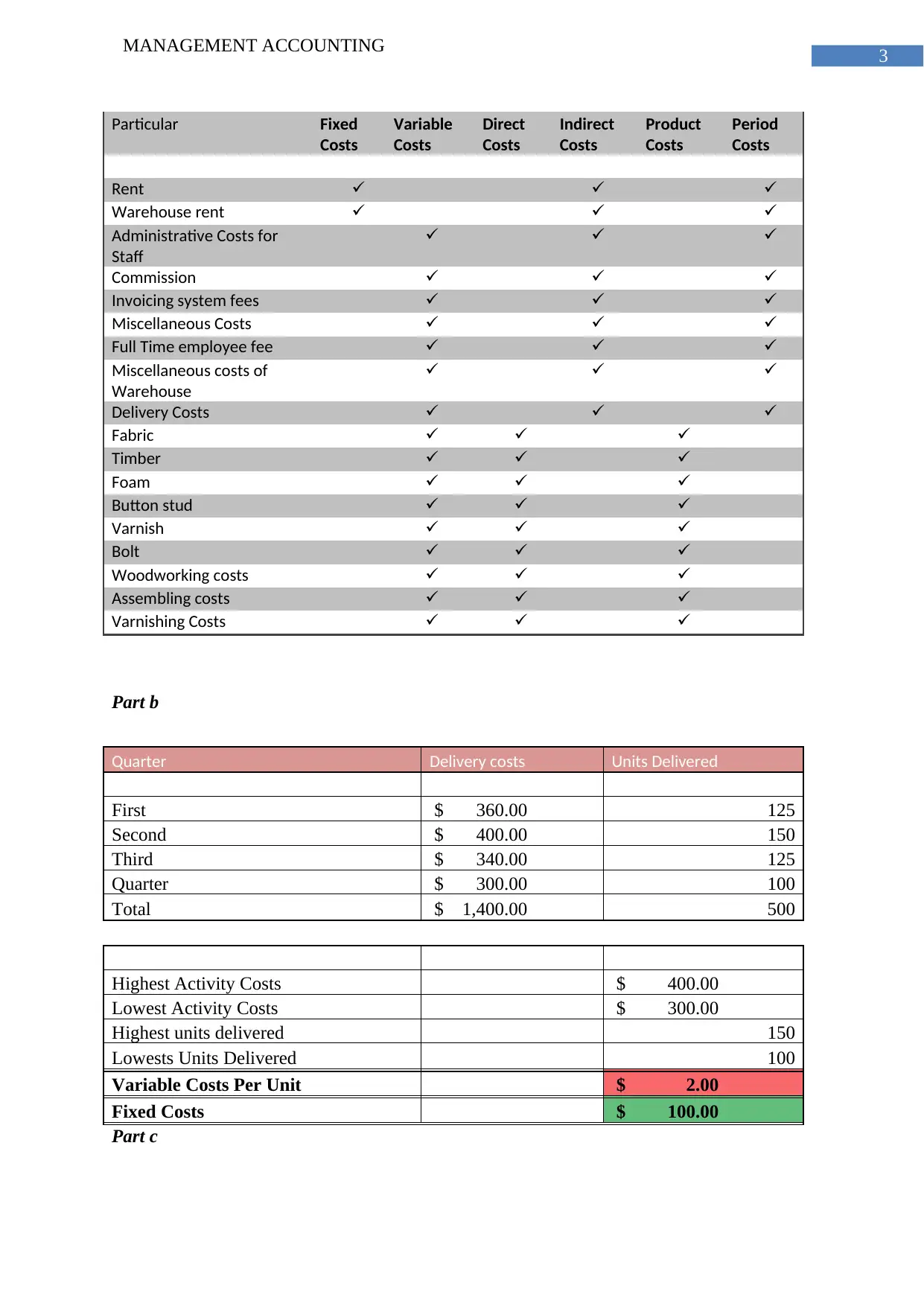

Particular Fixed

Costs

Variable

Costs

Direct

Costs

Indirect

Costs

Product

Costs

Period

Costs

Rent

Warehouse rent

Administrative Costs for

Staff

Commission

Invoicing system fees

Miscellaneous Costs

Full Time employee fee

Miscellaneous costs of

Warehouse

Delivery Costs

Fabric

Timber

Foam

Button stud

Varnish

Bolt

Woodworking costs

Assembling costs

Varnishing Costs

Part b

Quarter Delivery costs Units Delivered

First $ 360.00 125

Second $ 400.00 150

Third $ 340.00 125

Quarter $ 300.00 100

Total $ 1,400.00 500

Highest Activity Costs $ 400.00

Lowest Activity Costs $ 300.00

Highest units delivered 150

Lowests Units Delivered 100

Variable Costs Per Unit $ 2.00

Fixed Costs $ 100.00

Part c

MANAGEMENT ACCOUNTING

Particular Fixed

Costs

Variable

Costs

Direct

Costs

Indirect

Costs

Product

Costs

Period

Costs

Rent

Warehouse rent

Administrative Costs for

Staff

Commission

Invoicing system fees

Miscellaneous Costs

Full Time employee fee

Miscellaneous costs of

Warehouse

Delivery Costs

Fabric

Timber

Foam

Button stud

Varnish

Bolt

Woodworking costs

Assembling costs

Varnishing Costs

Part b

Quarter Delivery costs Units Delivered

First $ 360.00 125

Second $ 400.00 150

Third $ 340.00 125

Quarter $ 300.00 100

Total $ 1,400.00 500

Highest Activity Costs $ 400.00

Lowest Activity Costs $ 300.00

Highest units delivered 150

Lowests Units Delivered 100

Variable Costs Per Unit $ 2.00

Fixed Costs $ 100.00

Part c

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGEMENT ACCOUNTING

Computation of Total Product Costs

MANAGEMENT ACCOUNTING

Computation of Total Product Costs

5

MANAGEMENT ACCOUNTING

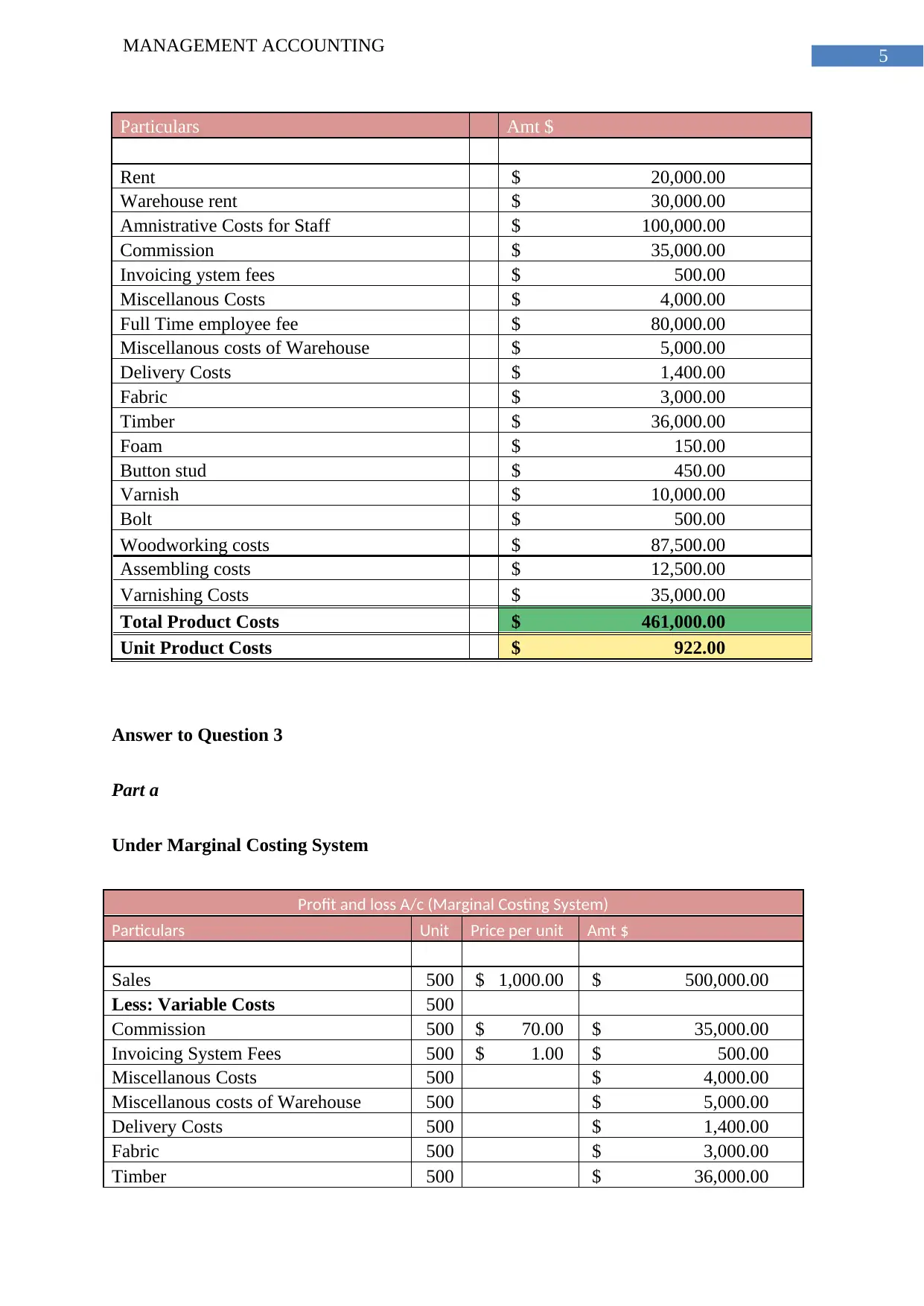

Particulars Amt $

Rent $ 20,000.00

Warehouse rent $ 30,000.00

Amnistrative Costs for Staff $ 100,000.00

Commission $ 35,000.00

Invoicing ystem fees $ 500.00

Miscellanous Costs $ 4,000.00

Full Time employee fee $ 80,000.00

Miscellanous costs of Warehouse $ 5,000.00

Delivery Costs $ 1,400.00

Fabric $ 3,000.00

Timber $ 36,000.00

Foam $ 150.00

Button stud $ 450.00

Varnish $ 10,000.00

Bolt $ 500.00

Woodworking costs $ 87,500.00

Assembling costs $ 12,500.00

Varnishing Costs $ 35,000.00

Total Product Costs $ 461,000.00

Unit Product Costs $ 922.00

Answer to Question 3

Part a

Under Marginal Costing System

Profit and loss A/c (Marginal Costing System)

Particulars Unit Price per unit Amt $

Sales 500 $ 1,000.00 $ 500,000.00

Less: Variable Costs 500

Commission 500 $ 70.00 $ 35,000.00

Invoicing System Fees 500 $ 1.00 $ 500.00

Miscellanous Costs 500 $ 4,000.00

Miscellanous costs of Warehouse 500 $ 5,000.00

Delivery Costs 500 $ 1,400.00

Fabric 500 $ 3,000.00

Timber 500 $ 36,000.00

MANAGEMENT ACCOUNTING

Particulars Amt $

Rent $ 20,000.00

Warehouse rent $ 30,000.00

Amnistrative Costs for Staff $ 100,000.00

Commission $ 35,000.00

Invoicing ystem fees $ 500.00

Miscellanous Costs $ 4,000.00

Full Time employee fee $ 80,000.00

Miscellanous costs of Warehouse $ 5,000.00

Delivery Costs $ 1,400.00

Fabric $ 3,000.00

Timber $ 36,000.00

Foam $ 150.00

Button stud $ 450.00

Varnish $ 10,000.00

Bolt $ 500.00

Woodworking costs $ 87,500.00

Assembling costs $ 12,500.00

Varnishing Costs $ 35,000.00

Total Product Costs $ 461,000.00

Unit Product Costs $ 922.00

Answer to Question 3

Part a

Under Marginal Costing System

Profit and loss A/c (Marginal Costing System)

Particulars Unit Price per unit Amt $

Sales 500 $ 1,000.00 $ 500,000.00

Less: Variable Costs 500

Commission 500 $ 70.00 $ 35,000.00

Invoicing System Fees 500 $ 1.00 $ 500.00

Miscellanous Costs 500 $ 4,000.00

Miscellanous costs of Warehouse 500 $ 5,000.00

Delivery Costs 500 $ 1,400.00

Fabric 500 $ 3,000.00

Timber 500 $ 36,000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGEMENT ACCOUNTING

Foam 500 $ 150.00

Button stud 500 $ 450.00

Varnish 500 $ 10,000.00

Bolt 500 $ 500.00

Woodworking costs 500 $ 35.00 $ 87,500.00

Assembling costs 500 $ 25.00 $ 12,500.00

Varnishing Costs 500 $ 35.00 $ 35,000.00

Total Variabke Costs 500 $ 231,000.00

Contribution Margin 500 $ 269,000.00

Less: Fixed Cpsts 500

Rent 500 $ 20,000.00

Warehouse rent 500 $ 30,000.00

Amnistrative Costs for Staff 500 $ 100,000.00

Full time employee wages 500 $ 80,000.00

Total Fixed Costs 500 $ 230,000.00

Profits 500 $ 39,000.00

Part b

Under Absorption Costing System

Profit and loss A/c Absorbtion Costing System)

Particulars Unit

Price per

unit Amt $

Sales 500 1000 $ 500,000.00

Direct Material Costs

Fabric 500 $ 3,000.00

Timber 500 $ 36,000.00

Foam 500 $ 150.00

Button stud 500 $ 450.00

Varnish 500 $ 10,000.00

Bolt 500 $ 500.00

Total Direct Material $ 50,100.00

Direct Labour costs

Woodworking costs 500

$

35.00 $ 87,500.00

Assembling costs 500

$

25.00 $ 12,500.00

Varnishing Costs 500

$

35.00 $ 35,000.00

MANAGEMENT ACCOUNTING

Foam 500 $ 150.00

Button stud 500 $ 450.00

Varnish 500 $ 10,000.00

Bolt 500 $ 500.00

Woodworking costs 500 $ 35.00 $ 87,500.00

Assembling costs 500 $ 25.00 $ 12,500.00

Varnishing Costs 500 $ 35.00 $ 35,000.00

Total Variabke Costs 500 $ 231,000.00

Contribution Margin 500 $ 269,000.00

Less: Fixed Cpsts 500

Rent 500 $ 20,000.00

Warehouse rent 500 $ 30,000.00

Amnistrative Costs for Staff 500 $ 100,000.00

Full time employee wages 500 $ 80,000.00

Total Fixed Costs 500 $ 230,000.00

Profits 500 $ 39,000.00

Part b

Under Absorption Costing System

Profit and loss A/c Absorbtion Costing System)

Particulars Unit

Price per

unit Amt $

Sales 500 1000 $ 500,000.00

Direct Material Costs

Fabric 500 $ 3,000.00

Timber 500 $ 36,000.00

Foam 500 $ 150.00

Button stud 500 $ 450.00

Varnish 500 $ 10,000.00

Bolt 500 $ 500.00

Total Direct Material $ 50,100.00

Direct Labour costs

Woodworking costs 500

$

35.00 $ 87,500.00

Assembling costs 500

$

25.00 $ 12,500.00

Varnishing Costs 500

$

35.00 $ 35,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT ACCOUNTING

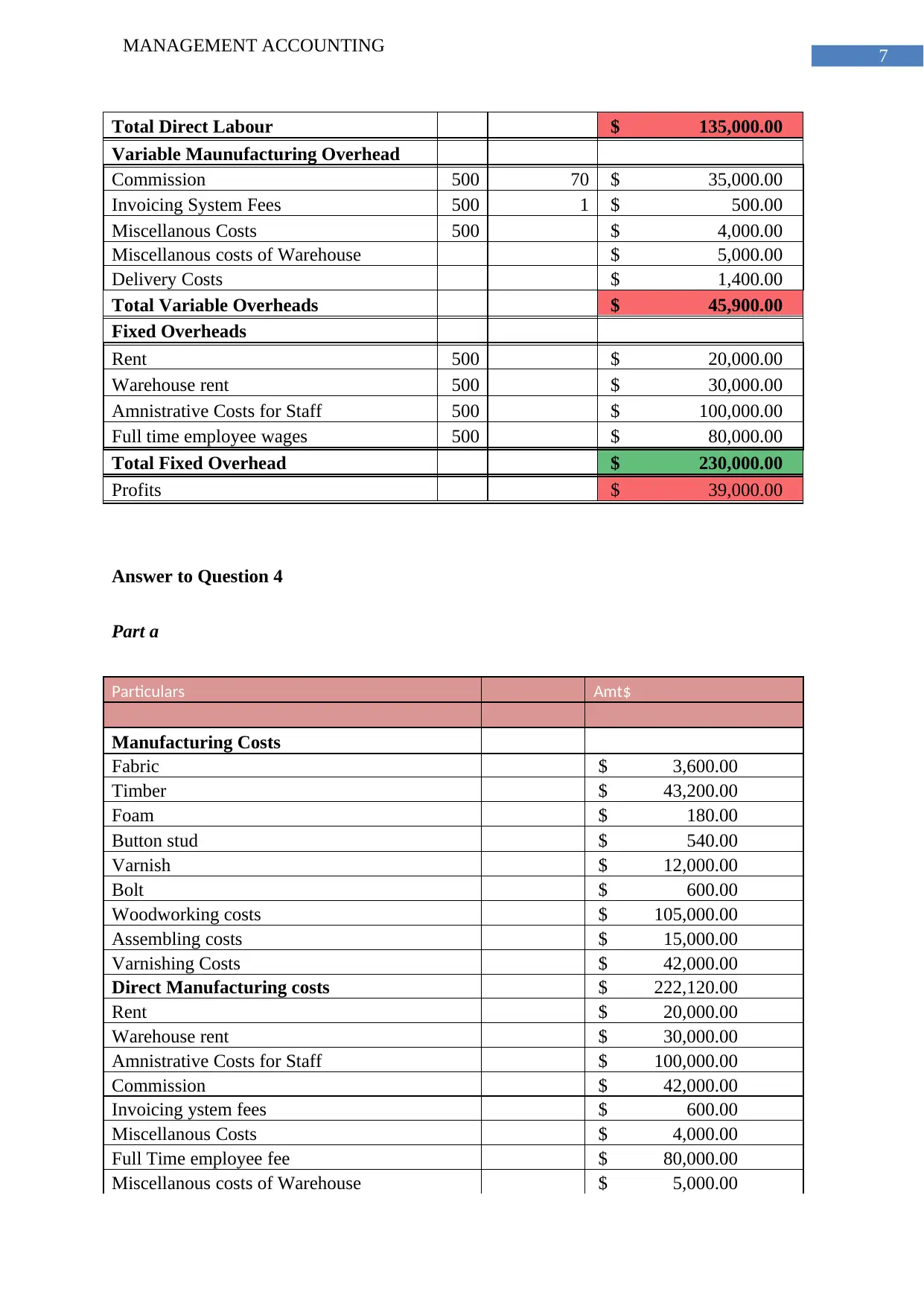

Total Direct Labour $ 135,000.00

Variable Maunufacturing Overhead

Commission 500 70 $ 35,000.00

Invoicing System Fees 500 1 $ 500.00

Miscellanous Costs 500 $ 4,000.00

Miscellanous costs of Warehouse $ 5,000.00

Delivery Costs $ 1,400.00

Total Variable Overheads $ 45,900.00

Fixed Overheads

Rent 500 $ 20,000.00

Warehouse rent 500 $ 30,000.00

Amnistrative Costs for Staff 500 $ 100,000.00

Full time employee wages 500 $ 80,000.00

Total Fixed Overhead $ 230,000.00

Profits $ 39,000.00

Answer to Question 4

Part a

Particulars Amt$

Manufacturing Costs

Fabric $ 3,600.00

Timber $ 43,200.00

Foam $ 180.00

Button stud $ 540.00

Varnish $ 12,000.00

Bolt $ 600.00

Woodworking costs $ 105,000.00

Assembling costs $ 15,000.00

Varnishing Costs $ 42,000.00

Direct Manufacturing costs $ 222,120.00

Rent $ 20,000.00

Warehouse rent $ 30,000.00

Amnistrative Costs for Staff $ 100,000.00

Commission $ 42,000.00

Invoicing ystem fees $ 600.00

Miscellanous Costs $ 4,000.00

Full Time employee fee $ 80,000.00

Miscellanous costs of Warehouse $ 5,000.00

MANAGEMENT ACCOUNTING

Total Direct Labour $ 135,000.00

Variable Maunufacturing Overhead

Commission 500 70 $ 35,000.00

Invoicing System Fees 500 1 $ 500.00

Miscellanous Costs 500 $ 4,000.00

Miscellanous costs of Warehouse $ 5,000.00

Delivery Costs $ 1,400.00

Total Variable Overheads $ 45,900.00

Fixed Overheads

Rent 500 $ 20,000.00

Warehouse rent 500 $ 30,000.00

Amnistrative Costs for Staff 500 $ 100,000.00

Full time employee wages 500 $ 80,000.00

Total Fixed Overhead $ 230,000.00

Profits $ 39,000.00

Answer to Question 4

Part a

Particulars Amt$

Manufacturing Costs

Fabric $ 3,600.00

Timber $ 43,200.00

Foam $ 180.00

Button stud $ 540.00

Varnish $ 12,000.00

Bolt $ 600.00

Woodworking costs $ 105,000.00

Assembling costs $ 15,000.00

Varnishing Costs $ 42,000.00

Direct Manufacturing costs $ 222,120.00

Rent $ 20,000.00

Warehouse rent $ 30,000.00

Amnistrative Costs for Staff $ 100,000.00

Commission $ 42,000.00

Invoicing ystem fees $ 600.00

Miscellanous Costs $ 4,000.00

Full Time employee fee $ 80,000.00

Miscellanous costs of Warehouse $ 5,000.00

8

MANAGEMENT ACCOUNTING

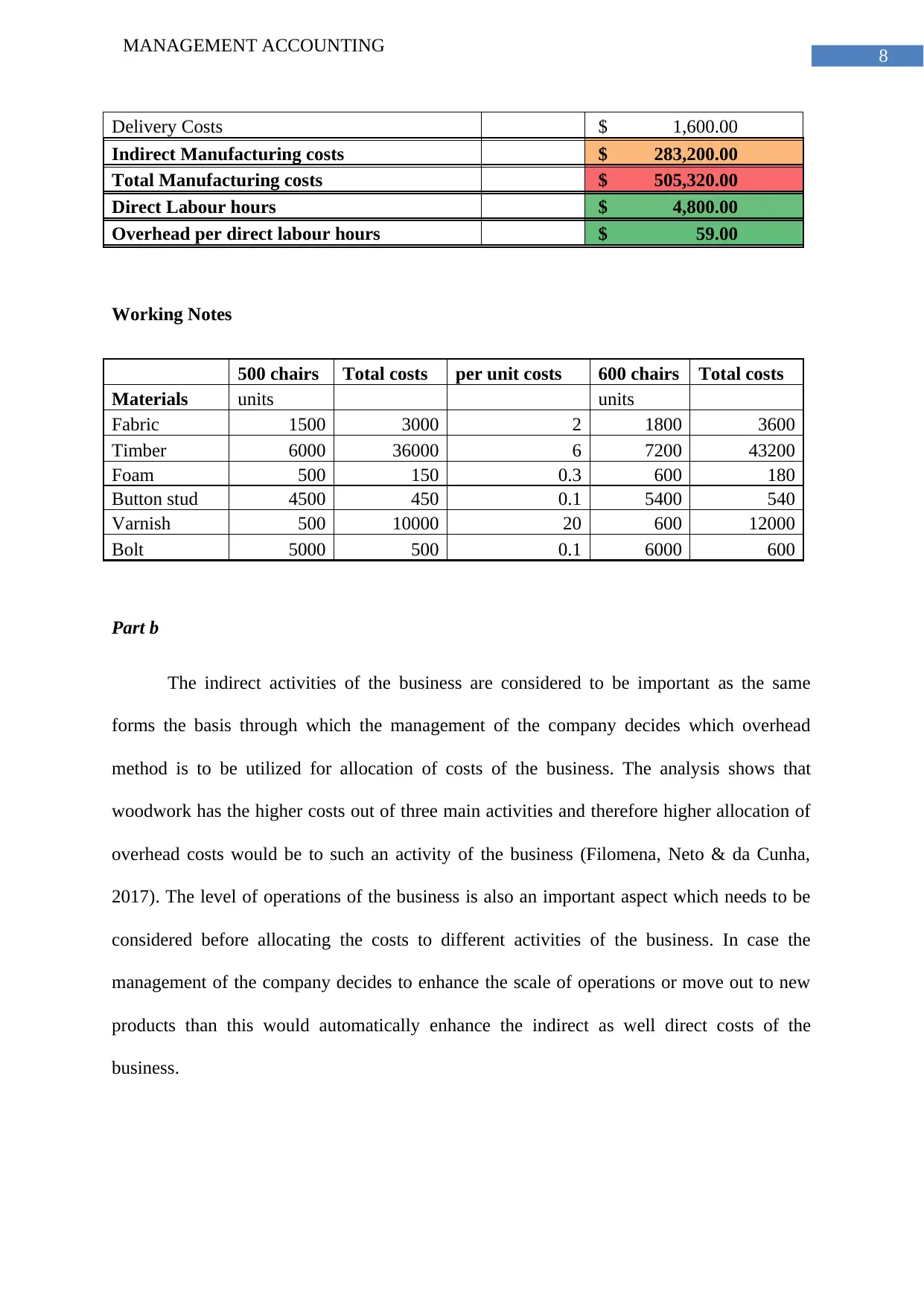

Delivery Costs $ 1,600.00

Indirect Manufacturing costs $ 283,200.00

Total Manufacturing costs $ 505,320.00

Direct Labour hours $ 4,800.00

Overhead per direct labour hours $ 59.00

Working Notes

500 chairs Total costs per unit costs 600 chairs Total costs

Materials units units

Fabric 1500 3000 2 1800 3600

Timber 6000 36000 6 7200 43200

Foam 500 150 0.3 600 180

Button stud 4500 450 0.1 5400 540

Varnish 500 10000 20 600 12000

Bolt 5000 500 0.1 6000 600

Part b

The indirect activities of the business are considered to be important as the same

forms the basis through which the management of the company decides which overhead

method is to be utilized for allocation of costs of the business. The analysis shows that

woodwork has the higher costs out of three main activities and therefore higher allocation of

overhead costs would be to such an activity of the business (Filomena, Neto & da Cunha,

2017). The level of operations of the business is also an important aspect which needs to be

considered before allocating the costs to different activities of the business. In case the

management of the company decides to enhance the scale of operations or move out to new

products than this would automatically enhance the indirect as well direct costs of the

business.

MANAGEMENT ACCOUNTING

Delivery Costs $ 1,600.00

Indirect Manufacturing costs $ 283,200.00

Total Manufacturing costs $ 505,320.00

Direct Labour hours $ 4,800.00

Overhead per direct labour hours $ 59.00

Working Notes

500 chairs Total costs per unit costs 600 chairs Total costs

Materials units units

Fabric 1500 3000 2 1800 3600

Timber 6000 36000 6 7200 43200

Foam 500 150 0.3 600 180

Button stud 4500 450 0.1 5400 540

Varnish 500 10000 20 600 12000

Bolt 5000 500 0.1 6000 600

Part b

The indirect activities of the business are considered to be important as the same

forms the basis through which the management of the company decides which overhead

method is to be utilized for allocation of costs of the business. The analysis shows that

woodwork has the higher costs out of three main activities and therefore higher allocation of

overhead costs would be to such an activity of the business (Filomena, Neto & da Cunha,

2017). The level of operations of the business is also an important aspect which needs to be

considered before allocating the costs to different activities of the business. In case the

management of the company decides to enhance the scale of operations or move out to new

products than this would automatically enhance the indirect as well direct costs of the

business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGEMENT ACCOUNTING

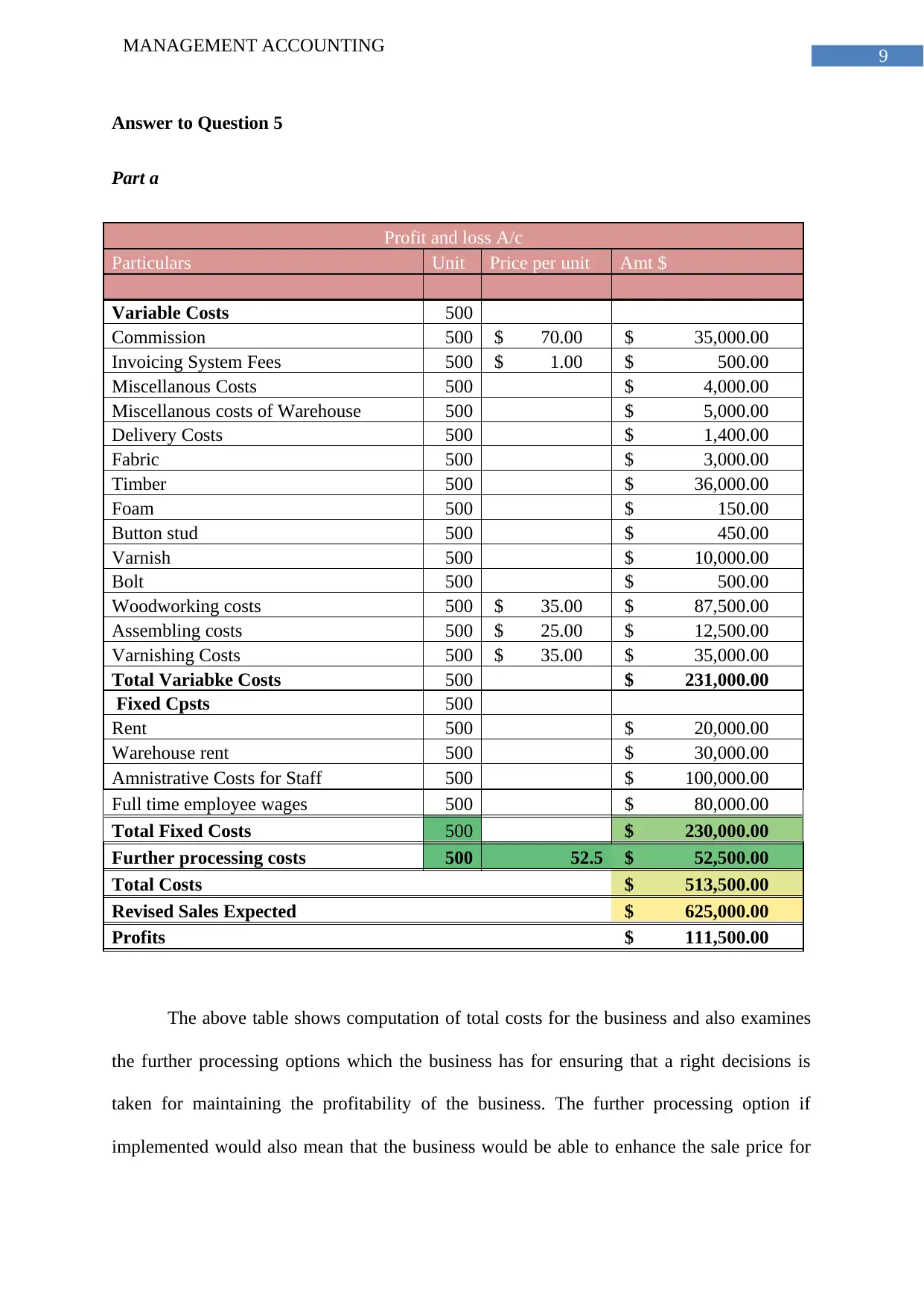

Answer to Question 5

Part a

Profit and loss A/c

Particulars Unit Price per unit Amt $

Variable Costs 500

Commission 500 $ 70.00 $ 35,000.00

Invoicing System Fees 500 $ 1.00 $ 500.00

Miscellanous Costs 500 $ 4,000.00

Miscellanous costs of Warehouse 500 $ 5,000.00

Delivery Costs 500 $ 1,400.00

Fabric 500 $ 3,000.00

Timber 500 $ 36,000.00

Foam 500 $ 150.00

Button stud 500 $ 450.00

Varnish 500 $ 10,000.00

Bolt 500 $ 500.00

Woodworking costs 500 $ 35.00 $ 87,500.00

Assembling costs 500 $ 25.00 $ 12,500.00

Varnishing Costs 500 $ 35.00 $ 35,000.00

Total Variabke Costs 500 $ 231,000.00

Fixed Cpsts 500

Rent 500 $ 20,000.00

Warehouse rent 500 $ 30,000.00

Amnistrative Costs for Staff 500 $ 100,000.00

Full time employee wages 500 $ 80,000.00

Total Fixed Costs 500 $ 230,000.00

Further processing costs 500 52.5 $ 52,500.00

Total Costs $ 513,500.00

Revised Sales Expected $ 625,000.00

Profits $ 111,500.00

The above table shows computation of total costs for the business and also examines

the further processing options which the business has for ensuring that a right decisions is

taken for maintaining the profitability of the business. The further processing option if

implemented would also mean that the business would be able to enhance the sale price for

MANAGEMENT ACCOUNTING

Answer to Question 5

Part a

Profit and loss A/c

Particulars Unit Price per unit Amt $

Variable Costs 500

Commission 500 $ 70.00 $ 35,000.00

Invoicing System Fees 500 $ 1.00 $ 500.00

Miscellanous Costs 500 $ 4,000.00

Miscellanous costs of Warehouse 500 $ 5,000.00

Delivery Costs 500 $ 1,400.00

Fabric 500 $ 3,000.00

Timber 500 $ 36,000.00

Foam 500 $ 150.00

Button stud 500 $ 450.00

Varnish 500 $ 10,000.00

Bolt 500 $ 500.00

Woodworking costs 500 $ 35.00 $ 87,500.00

Assembling costs 500 $ 25.00 $ 12,500.00

Varnishing Costs 500 $ 35.00 $ 35,000.00

Total Variabke Costs 500 $ 231,000.00

Fixed Cpsts 500

Rent 500 $ 20,000.00

Warehouse rent 500 $ 30,000.00

Amnistrative Costs for Staff 500 $ 100,000.00

Full time employee wages 500 $ 80,000.00

Total Fixed Costs 500 $ 230,000.00

Further processing costs 500 52.5 $ 52,500.00

Total Costs $ 513,500.00

Revised Sales Expected $ 625,000.00

Profits $ 111,500.00

The above table shows computation of total costs for the business and also examines

the further processing options which the business has for ensuring that a right decisions is

taken for maintaining the profitability of the business. The further processing option if

implemented would also mean that the business would be able to enhance the sale price for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGEMENT ACCOUNTING

the products as more value is being added to the products and also ensure that the same

enhances the sales of the business (Bjørnenak & Helgesen, 2013). As per the case, further

processing would only require additional varnishing which would provide a stylish coat to the

chairs and make the same 21st style chairs which are comparatively new to the market. It is

therefore for such reasons that it is anticipated that chair prices can be increased to $ 1250 per

chair.

The above computation shows that the management can proceed with new venture as

the same would generate appropriate profits which is beneficial for the business from the

perspective of long run. As per the analysis the increase in the expenses which can be

anticipated is the varnishing costs for the rich coat to the chairs considering the scale of

operations remains the same and there is no hike in other costs of the business (Wynn et al.,

2014). Hence, it can be said that the owners should implement the new processes so that the

entity is able to generate more revenue and rediscover itself in the market and also attract

more customers.

Answer to Question 6

Part a

The analysis of the costs shows that with the increase in the production of chair units,

the overall per unit costs for the product would be reduced. This can be due to variety of

factors which has an influence on the operational process of the business. The analysis can be

attributed to the concept of economies of scale as it states that when a business is able to

enhance the production in terms of units produced than the entity can also systematically

reduce the overall per unit costs (Lee et al., 2015). Therefore, it can be justified that a hike in

the sales of the entity would increase the number of units products and this would result in

decline in the costs of operations of the business/.

MANAGEMENT ACCOUNTING

the products as more value is being added to the products and also ensure that the same

enhances the sales of the business (Bjørnenak & Helgesen, 2013). As per the case, further

processing would only require additional varnishing which would provide a stylish coat to the

chairs and make the same 21st style chairs which are comparatively new to the market. It is

therefore for such reasons that it is anticipated that chair prices can be increased to $ 1250 per

chair.

The above computation shows that the management can proceed with new venture as

the same would generate appropriate profits which is beneficial for the business from the

perspective of long run. As per the analysis the increase in the expenses which can be

anticipated is the varnishing costs for the rich coat to the chairs considering the scale of

operations remains the same and there is no hike in other costs of the business (Wynn et al.,

2014). Hence, it can be said that the owners should implement the new processes so that the

entity is able to generate more revenue and rediscover itself in the market and also attract

more customers.

Answer to Question 6

Part a

The analysis of the costs shows that with the increase in the production of chair units,

the overall per unit costs for the product would be reduced. This can be due to variety of

factors which has an influence on the operational process of the business. The analysis can be

attributed to the concept of economies of scale as it states that when a business is able to

enhance the production in terms of units produced than the entity can also systematically

reduce the overall per unit costs (Lee et al., 2015). Therefore, it can be justified that a hike in

the sales of the entity would increase the number of units products and this would result in

decline in the costs of operations of the business/.

11

MANAGEMENT ACCOUNTING

Part b

In case there is a fall in the scale of production for the business and the same is not

according to the plans of the business than a situation may arise where there is over allocation

of overhead costs. This would hamper the costs analysis and influence the price which is to

be set for the product considering the market trends. The management of Stylish chairs in

such a case needs to make necessary adjustments to the cost statement so that proper

presentation can be made of the costs structure and proper analysis can also be conducted in

respect of the same.

Reference

Bjørnenak, T., & Helgesen, Ø. (2013). Customer relations and cost management. The

Routledge Companion to Cost Management, 250-266.

MANAGEMENT ACCOUNTING

Part b

In case there is a fall in the scale of production for the business and the same is not

according to the plans of the business than a situation may arise where there is over allocation

of overhead costs. This would hamper the costs analysis and influence the price which is to

be set for the product considering the market trends. The management of Stylish chairs in

such a case needs to make necessary adjustments to the cost statement so that proper

presentation can be made of the costs structure and proper analysis can also be conducted in

respect of the same.

Reference

Bjørnenak, T., & Helgesen, Ø. (2013). Customer relations and cost management. The

Routledge Companion to Cost Management, 250-266.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.