Comprehensive Analysis of Management Accounting Cost Solutions

VerifiedAdded on 2021/06/17

|11

|1351

|35

Homework Assignment

AI Summary

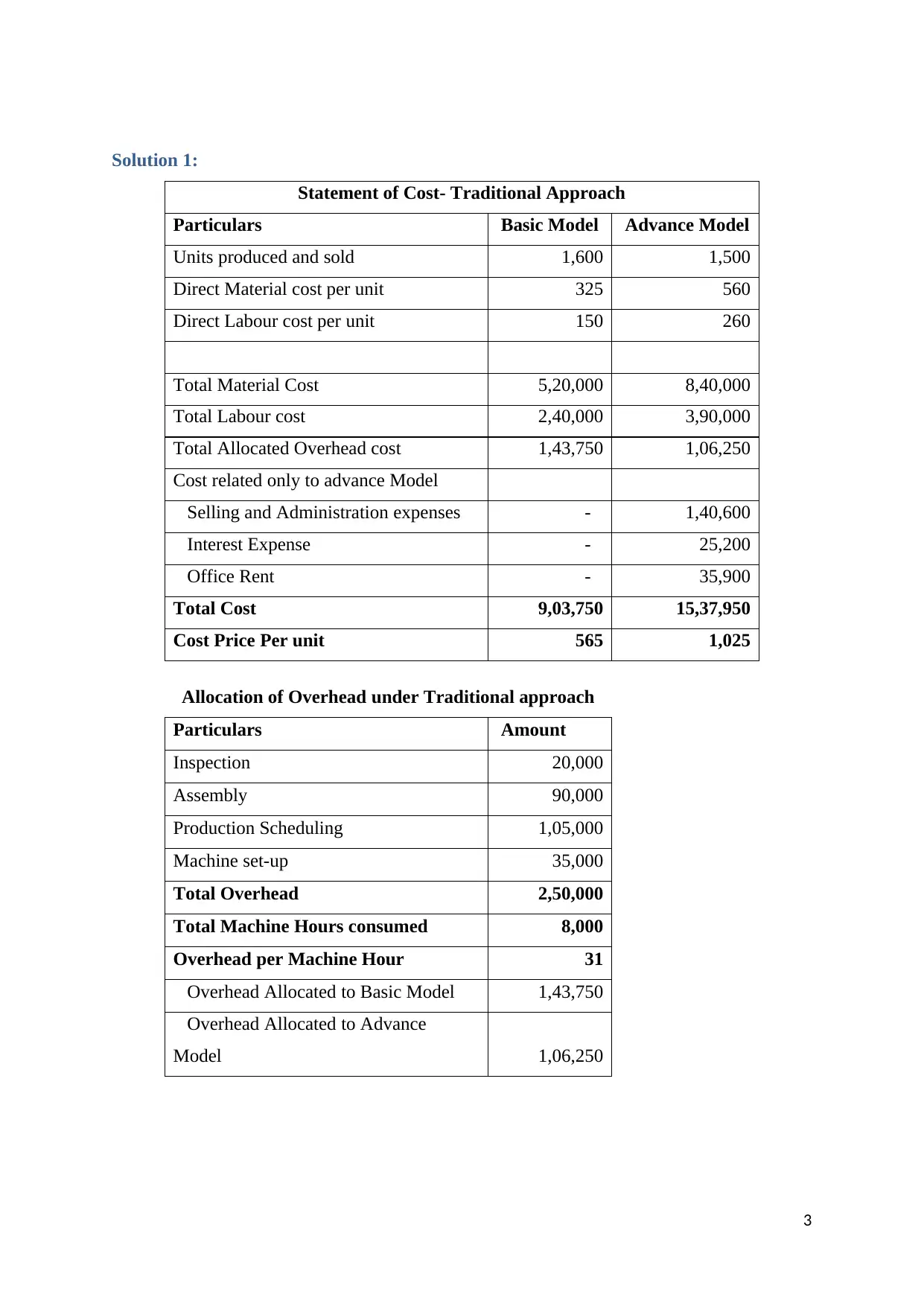

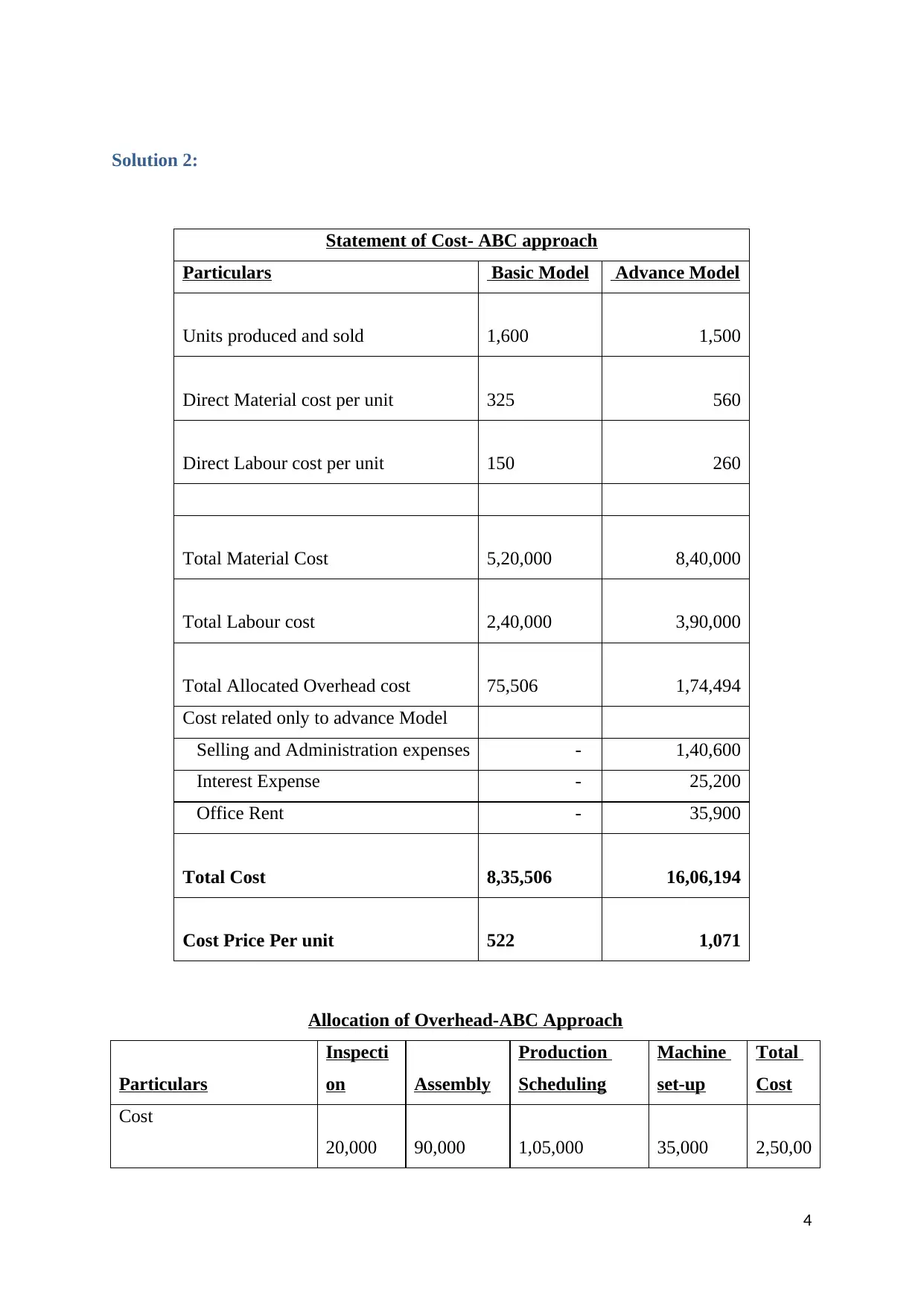

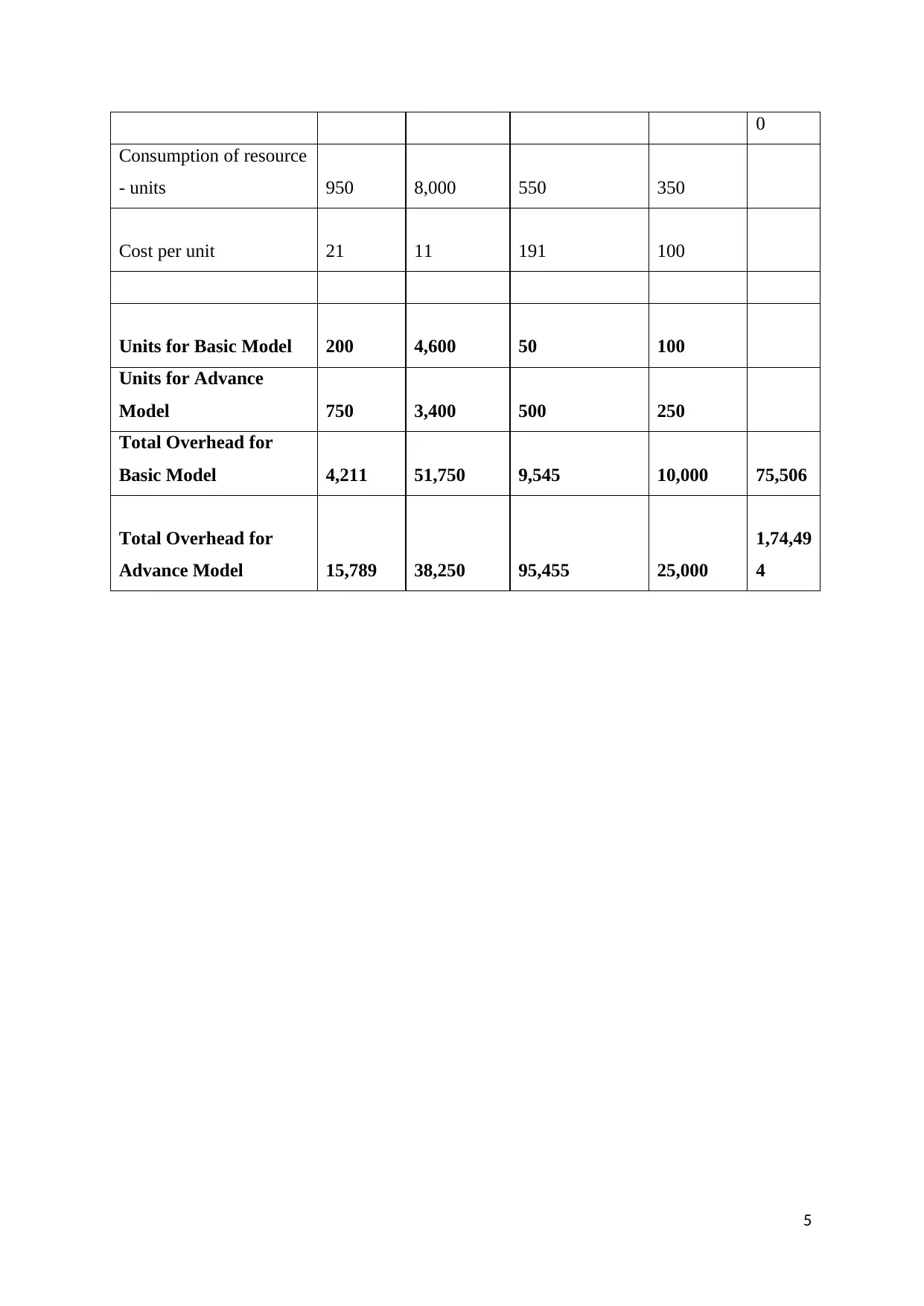

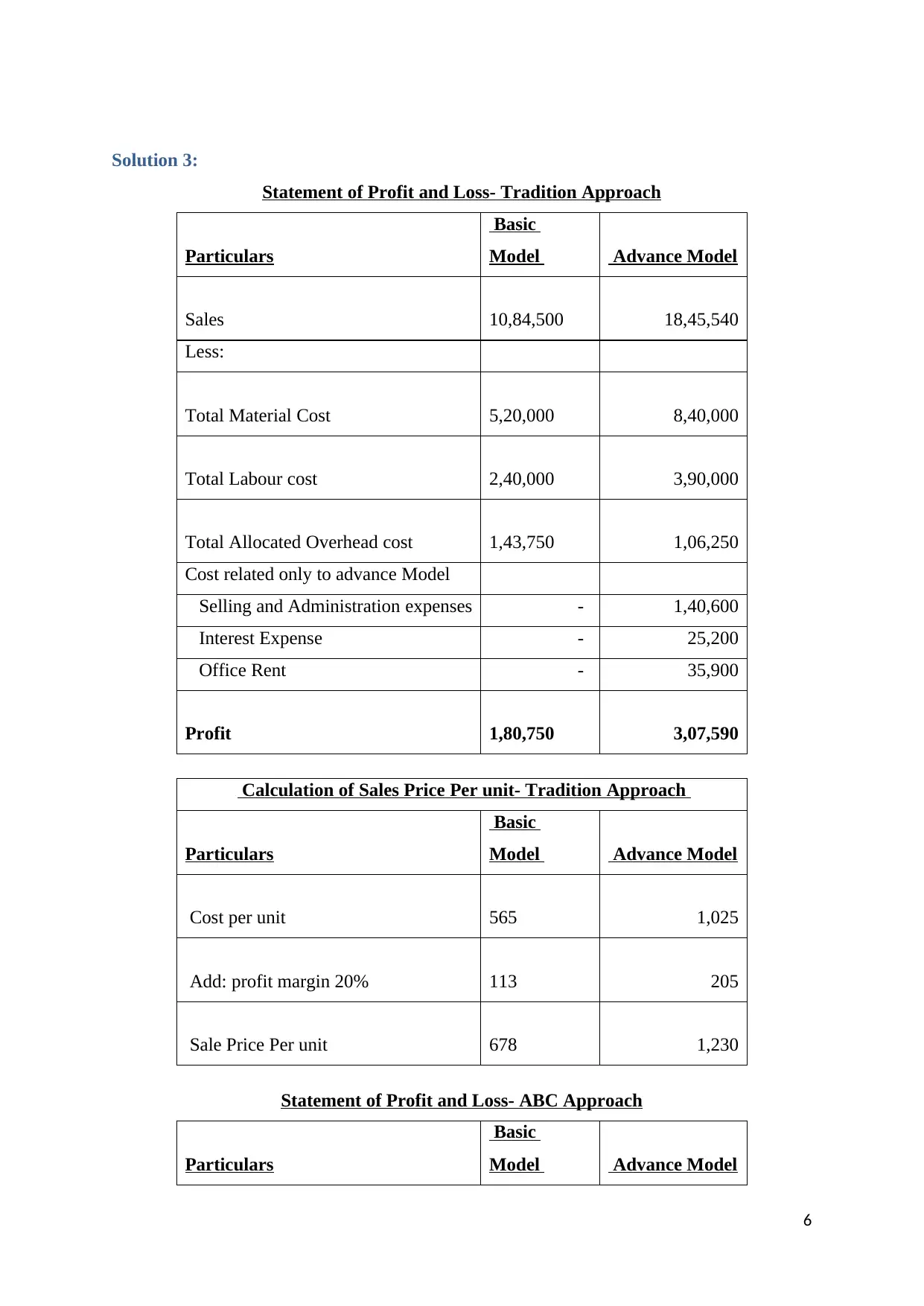

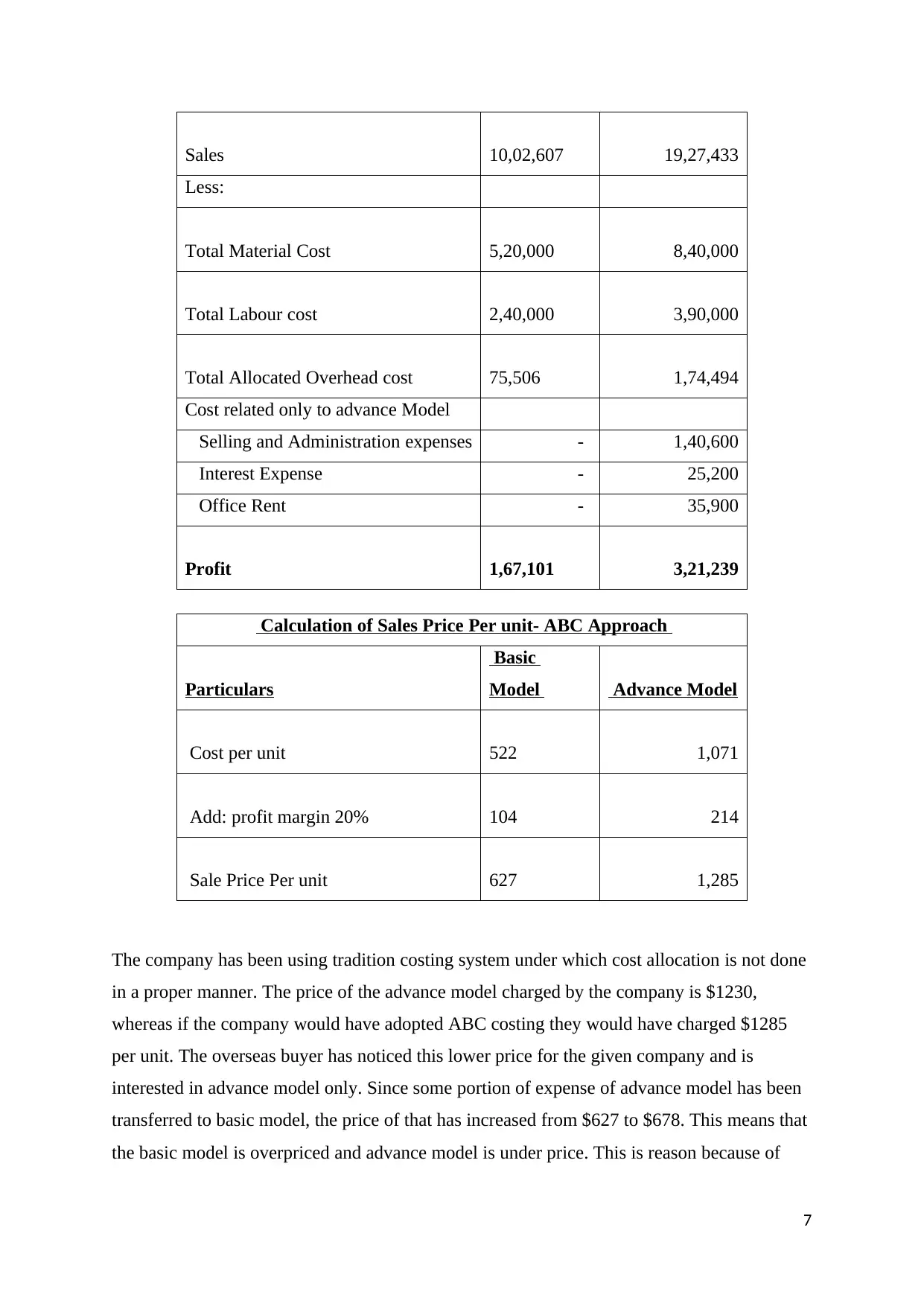

This document offers a detailed analysis of management accounting solutions, encompassing various costing methods and financial statement analysis. It begins with a comprehensive comparison of traditional and Activity-Based Costing (ABC) approaches, presenting detailed calculations for unit costs, total costs, and profit and loss statements for both basic and advanced models. The document highlights the impact of different costing methods on pricing decisions, explaining why an overseas buyer is interested in a specific model due to pricing discrepancies caused by overhead allocation. Furthermore, it addresses overhead variance treatment, exploring methods like carrying forward, writing off in the profit and loss account, and adjusting in the current year with existing units. Finally, the document provides a detailed overview of Activity-Based Costing, outlining its advantages, such as improved data analysis and cost allocation, and disadvantages, including data collection complexity and implementation costs. The solutions cover various aspects of cost accounting, including direct materials, direct labor, overhead allocation, and sales price calculations.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.