Management Accounting Homework: Special Order & Production Analysis

VerifiedAdded on 2020/05/08

|5

|689

|143

Homework Assignment

AI Summary

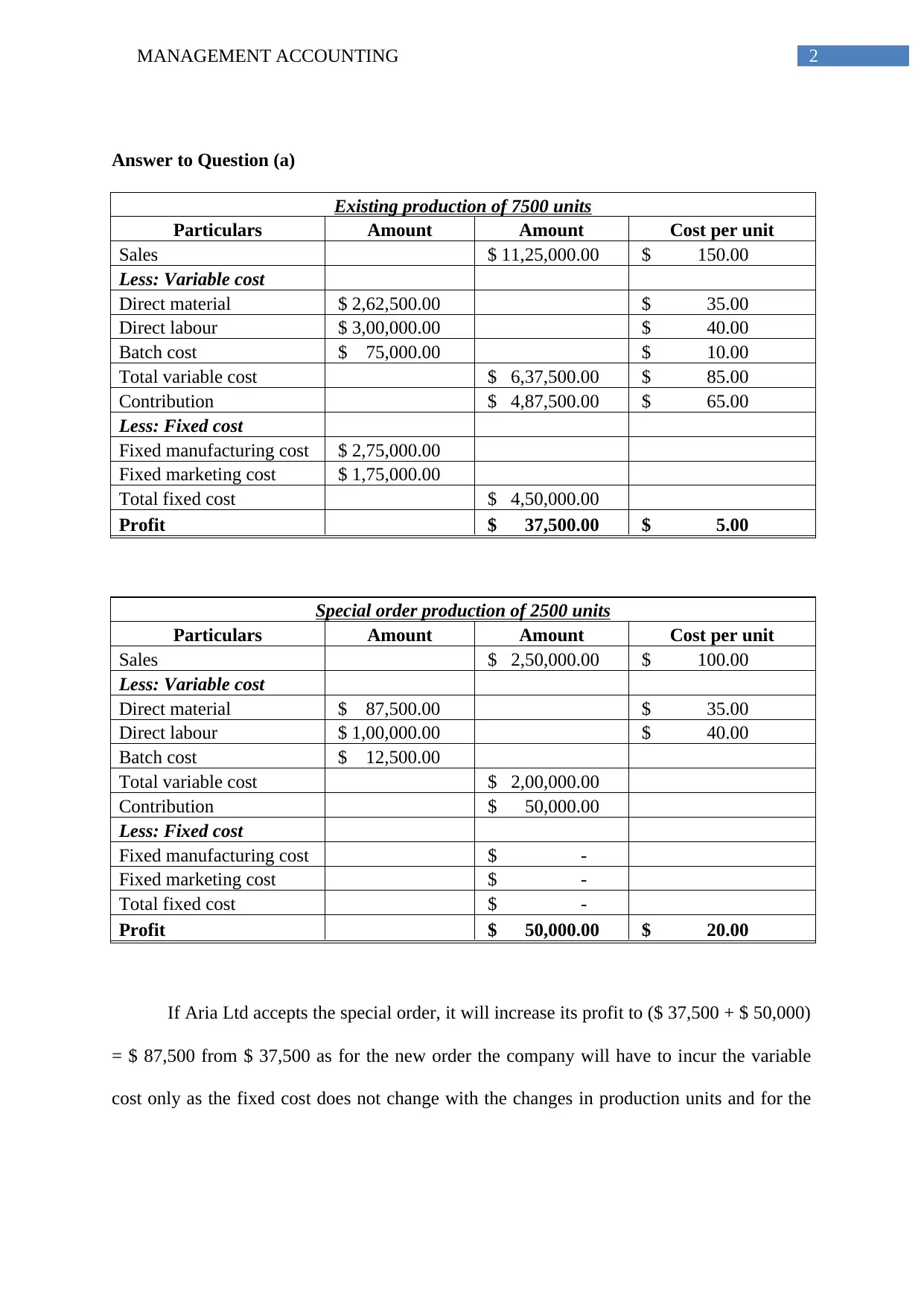

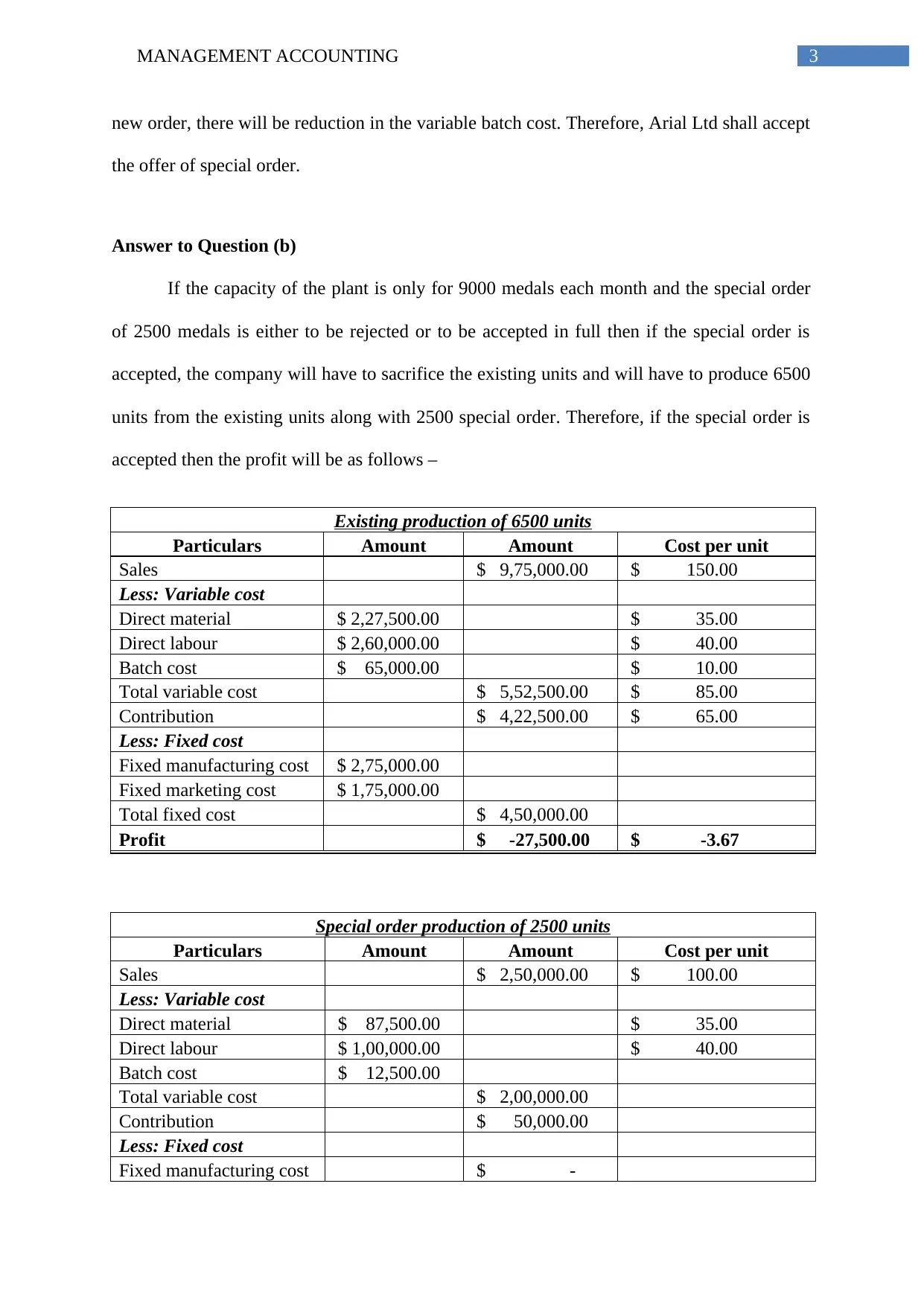

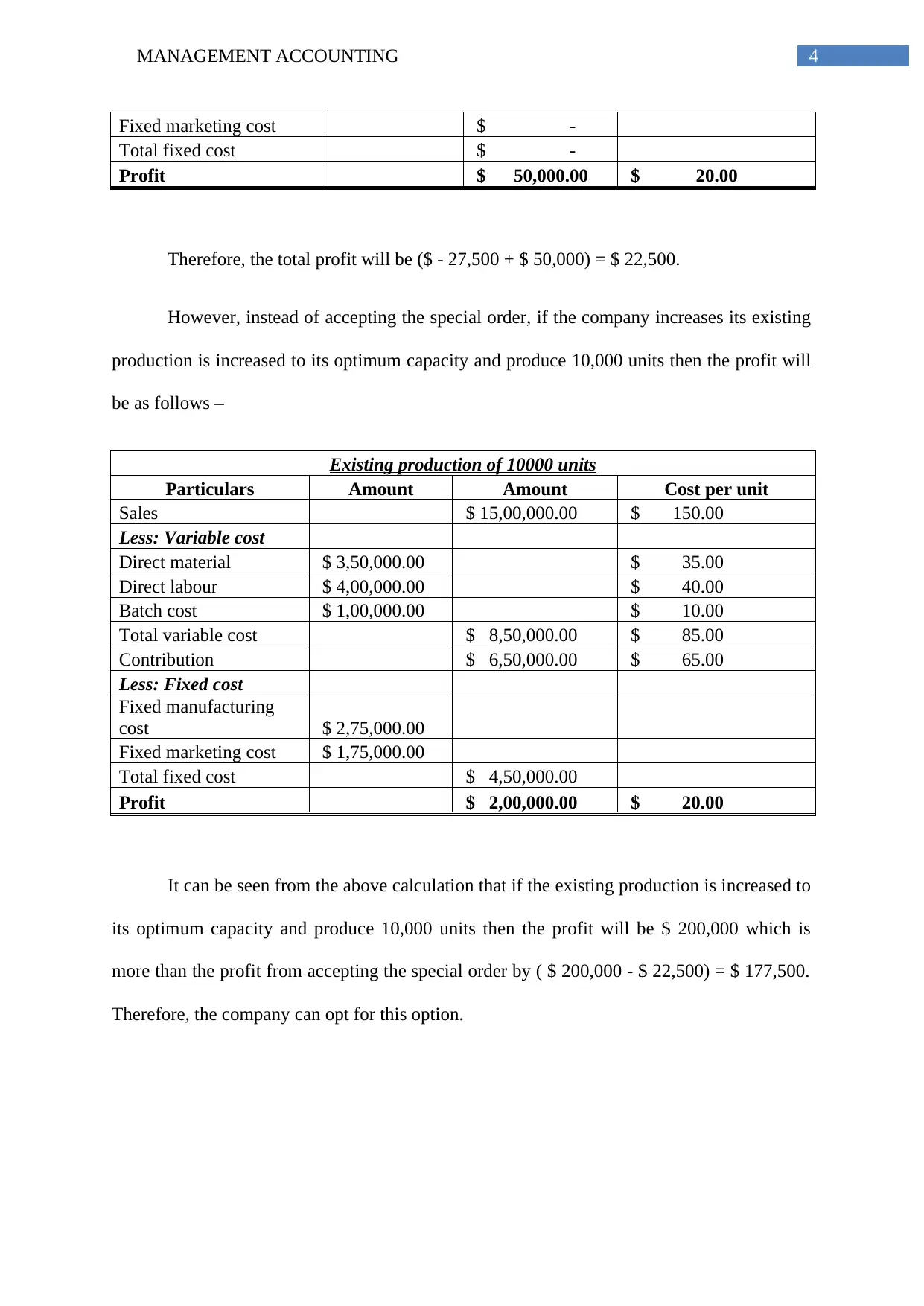

This management accounting assignment analyzes a company's production and profit scenarios, specifically focusing on the decision of whether to accept a special order. The solution begins by calculating the profit generated from existing production levels and then evaluates the profitability of a special order, considering variable and fixed costs. The analysis extends to a scenario where plant capacity is limited, forcing a trade-off between existing production and the special order. The assignment concludes by comparing the profits from accepting the special order versus increasing existing production to its maximum capacity. The solution includes detailed calculations of sales, variable costs (direct materials, labor, and batch costs), contribution margins, fixed costs, and overall profit, providing a clear framework for making informed financial decisions. The analysis highlights the impact of capacity constraints and the importance of considering both short-term and long-term profitability in production planning.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.