Management Accounting: System, Techniques, and Budgetary Control

VerifiedAdded on 2020/10/05

|15

|3339

|119

Report

AI Summary

This report provides a comprehensive overview of management accounting, encompassing its core principles, systems, and reporting methodologies. The introduction establishes the significance of management accounting in business decision-making, highlighting its role in providing financial and statistical data to management. Task 1 delves into the management accounting system, differentiating it from financial accounting and outlining various system types, such as cost accounting, inventory management, and job costing. The benefits of each system are explored. Task 2 focuses on management accounting reporting methods, emphasizing the importance of accurate and reliable information. It also presents different methods, including cost reports, inventory reports, and job costing reports. Furthermore, the report illustrates the preparation of income statements using different techniques like absorption costing, variable costing, and cost-volume-profit analysis. It also covers planning tools of budgetary control, such as cash budgets, sales budgets, and activity-based budgeting, alongside their advantages and disadvantages. The report concludes with a discussion on how management accounting systems can be adopted to address financial problems.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting system and its requirement in business.........................................1

P2 Methods of management accounting reporting......................................................................3

P2 Preparation of income statement using different techniques.................................................4

TASK 2............................................................................................................................................8

P4 Various planning tools of budgetary control and their advantages and disadvantages.........8

P5 Adoption of management accounting system as to responding to various financial

problems......................................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting system and its requirement in business.........................................1

P2 Methods of management accounting reporting......................................................................3

P2 Preparation of income statement using different techniques.................................................4

TASK 2............................................................................................................................................8

P4 Various planning tools of budgetary control and their advantages and disadvantages.........8

P5 Adoption of management accounting system as to responding to various financial

problems......................................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting is a branch of management which concerns with the preparation

of financial and statistical report of the business and making it available to management

whenever it is required. This report includes importance of management accounting in decision

making process, brief discussion about various management accounting system along with their

benefits. The study also shows preparation of income statement using different techniques of

management accounting. The report includes a brief comparison of different planning tools of

budgetary control and their importance in solving financial problem.

TASK 1

P1 Management accounting system and its requirement in business.

“Management accounting is a technique of management in which managers uses their

professional knowledge and skills for the preparation of data showing information relating to

accounts and statics of business for the purpose of using them in formulation of strategies and

plans for the business organization.”

It is an important part of decision making process as managers uses past informations for

taking better decisions for the business, and management accounting provides all major

information relating to cost, efficiency, financial data, financial performance, etc. to managers.

All these informations helps managers in taking the best decisions for the business and

developing the best strategies and plans for the business as per its past performance of business

in order to improve them and increasing overall performance and profitability of business

(Höglund, 2016).

There is major difference between management accounting and financial accounting like:

Basis Management accounting Financial accounting

Objectives Its main objective is to provide

relevant information to internal

members of business.

Its objective is to provide

information to the investors

and other outsiders of

business.

Mandatory Its preparation is optional for

any business

Business need to prepare

financial accounting reports

each year.

1

Management accounting is a branch of management which concerns with the preparation

of financial and statistical report of the business and making it available to management

whenever it is required. This report includes importance of management accounting in decision

making process, brief discussion about various management accounting system along with their

benefits. The study also shows preparation of income statement using different techniques of

management accounting. The report includes a brief comparison of different planning tools of

budgetary control and their importance in solving financial problem.

TASK 1

P1 Management accounting system and its requirement in business.

“Management accounting is a technique of management in which managers uses their

professional knowledge and skills for the preparation of data showing information relating to

accounts and statics of business for the purpose of using them in formulation of strategies and

plans for the business organization.”

It is an important part of decision making process as managers uses past informations for

taking better decisions for the business, and management accounting provides all major

information relating to cost, efficiency, financial data, financial performance, etc. to managers.

All these informations helps managers in taking the best decisions for the business and

developing the best strategies and plans for the business as per its past performance of business

in order to improve them and increasing overall performance and profitability of business

(Höglund, 2016).

There is major difference between management accounting and financial accounting like:

Basis Management accounting Financial accounting

Objectives Its main objective is to provide

relevant information to internal

members of business.

Its objective is to provide

information to the investors

and other outsiders of

business.

Mandatory Its preparation is optional for

any business

Business need to prepare

financial accounting reports

each year.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Users Management and other internal

members of business.

It is useful fot outsiders of

business like investors,

creditors, competitors, etc.

Management accounting system

Management accounting system is an integral part of planning and controlling process

which helps the managers in managing financial position of business. It is a technique of

management that provides help in enhancing profitability and financial position of business by

increasing its efficiency in investment of cash, preparation of budgets, etc (Otley, 2016).

Types of management accounting system:

1. Cost accounting system: this system helps the management in managing cost efficiency

in the business. It provides methods of estimation of cost of various departments of

business. This technique is beneficial for manufacturing concerns.

Benefits:

With the help of this technique, management can estimate cost of various

manufacturing processes.

It enables management to make strategies to eliminate wastage of cost at each stage

of manufacturing process in order to develop the business as more cost efficient.

It provides help in analyzing of cost control and efficiency, inventory management

and profitability of business.

2. Inventory management system: Inventory management refers to using different

techniques and methods for having an effective control in the business in order to avoid

shortage or excess of inventory in business. It is beneficial for every business whether it

is manufacturing concern, retail business, wholesale business or any other business.

Benefits:

It helps management in tracking the data relating to receiving and outgoing of inventory.

With this information, business enables to maintain appropriate amount of inventory in

the business.

With the use of this technique, management can minimize wastage of inventory.

It helps in having effective control over maintaining appropriate amount of inventory in

organization.

2

members of business.

It is useful fot outsiders of

business like investors,

creditors, competitors, etc.

Management accounting system

Management accounting system is an integral part of planning and controlling process

which helps the managers in managing financial position of business. It is a technique of

management that provides help in enhancing profitability and financial position of business by

increasing its efficiency in investment of cash, preparation of budgets, etc (Otley, 2016).

Types of management accounting system:

1. Cost accounting system: this system helps the management in managing cost efficiency

in the business. It provides methods of estimation of cost of various departments of

business. This technique is beneficial for manufacturing concerns.

Benefits:

With the help of this technique, management can estimate cost of various

manufacturing processes.

It enables management to make strategies to eliminate wastage of cost at each stage

of manufacturing process in order to develop the business as more cost efficient.

It provides help in analyzing of cost control and efficiency, inventory management

and profitability of business.

2. Inventory management system: Inventory management refers to using different

techniques and methods for having an effective control in the business in order to avoid

shortage or excess of inventory in business. It is beneficial for every business whether it

is manufacturing concern, retail business, wholesale business or any other business.

Benefits:

It helps management in tracking the data relating to receiving and outgoing of inventory.

With this information, business enables to maintain appropriate amount of inventory in

the business.

With the use of this technique, management can minimize wastage of inventory.

It helps in having effective control over maintaining appropriate amount of inventory in

organization.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Job costing system: job accounting system includes gathering information about cost

incurred in manufacture of each product or services. This system is helpful for those

business concerns which provides product or services as per the requirement of customers

(Maas, Schaltegger and Crutzen, 2016). This system can be used by event management

organizations, hotels, etc.

Benefits:

Through this technique, business can identify cost incurred on production of particular

product or services.

Business can use this technique when they provide customized goods or services to its

customers.

Through this management accounting system, management can easily track the accuracy

of budgetary control system of the business concern.

P2 Methods of management accounting reporting

Management accounting reporting can be defined as a system of management of

providing relevant report to the management including financial, statistical and cost related datas

in order to help them in developing better strategies and plans for the business and taking the

best decisions for the business as well through which profitability and efficiency of the business

can be enhanced over the year. Although, informations provided by the management need to be

relevant accurate, as wrong information may result in taking wrong decisions and development

of ineffective strategies by the management, which would directly affect the efficiency of the

business in negative way.

Through management accounting reporting, managers provides information related to the

financial position of the business, through which management enables to take appropriate actions

to develop and enhance the financial position of the business in competitive market. In case,

management accountant provides any wrong or non reliable information to the internal manager,

it would result in suffering loss by the whole organisation due to wrong decisions and strategies

of the business. Therefore, informations provided by the management need to be reliable and

accurate (Kwarteng, 2018).

All the reports made by the management accountant must be realiable in easily

understandable by the internal management of the business as in case management could

3

incurred in manufacture of each product or services. This system is helpful for those

business concerns which provides product or services as per the requirement of customers

(Maas, Schaltegger and Crutzen, 2016). This system can be used by event management

organizations, hotels, etc.

Benefits:

Through this technique, business can identify cost incurred on production of particular

product or services.

Business can use this technique when they provide customized goods or services to its

customers.

Through this management accounting system, management can easily track the accuracy

of budgetary control system of the business concern.

P2 Methods of management accounting reporting

Management accounting reporting can be defined as a system of management of

providing relevant report to the management including financial, statistical and cost related datas

in order to help them in developing better strategies and plans for the business and taking the

best decisions for the business as well through which profitability and efficiency of the business

can be enhanced over the year. Although, informations provided by the management need to be

relevant accurate, as wrong information may result in taking wrong decisions and development

of ineffective strategies by the management, which would directly affect the efficiency of the

business in negative way.

Through management accounting reporting, managers provides information related to the

financial position of the business, through which management enables to take appropriate actions

to develop and enhance the financial position of the business in competitive market. In case,

management accountant provides any wrong or non reliable information to the internal manager,

it would result in suffering loss by the whole organisation due to wrong decisions and strategies

of the business. Therefore, informations provided by the management need to be reliable and

accurate (Kwarteng, 2018).

All the reports made by the management accountant must be realiable in easily

understandable by the internal management of the business as in case management could

3

understand the report, and wrongly interpret any information, it would result in taking wrong

decisions by them which would lead in enhancement of inefficiency in the business and suffering

loss by the company.

Methods of management accounting reporting:

there are numerous methods available for the management accountant to prepare

management accounting reporting like:

Cost reports: this report includes information and data related to total cost incurred in

manufacture of any product or services including cost of direct material, labour,

electricity, and other overheads, etc. all these cost information helps management ion

having cost control by eliminating wastage and determining appropriate sales price of the

product or services as well.

Inventory report: it includes all the information relating to purchase and sale of

inventory along with the quantity and rate of inventory purchased or sold by the business.

With the help of these informations, management can have effective control over

management by eliminating excess or shortage of inventory in the business. This report

may provide wrong information to the management in case of any wrong entry made by

the accountant.

Job costing report: it includes the cost incurred in manufacture of each product or

services as per the demand of customer. It helps management in determining the selling

price of different jobs as per the cost incurred by the business in manufacturing the

customized product or services and amount of profit to be gained by the business from a

particular job. Although this report is of no use for those organizations which

manufactures same products and services for all customers and earns same profit from

them as well.

P2 Preparation of income statement using different techniques

Microeconomics techniques

Cost: it means amount paid by the business to produce any product or render any service to th

customer. It is a sum total of amount paid by the business for running its normal course of

actions.

4

decisions by them which would lead in enhancement of inefficiency in the business and suffering

loss by the company.

Methods of management accounting reporting:

there are numerous methods available for the management accountant to prepare

management accounting reporting like:

Cost reports: this report includes information and data related to total cost incurred in

manufacture of any product or services including cost of direct material, labour,

electricity, and other overheads, etc. all these cost information helps management ion

having cost control by eliminating wastage and determining appropriate sales price of the

product or services as well.

Inventory report: it includes all the information relating to purchase and sale of

inventory along with the quantity and rate of inventory purchased or sold by the business.

With the help of these informations, management can have effective control over

management by eliminating excess or shortage of inventory in the business. This report

may provide wrong information to the management in case of any wrong entry made by

the accountant.

Job costing report: it includes the cost incurred in manufacture of each product or

services as per the demand of customer. It helps management in determining the selling

price of different jobs as per the cost incurred by the business in manufacturing the

customized product or services and amount of profit to be gained by the business from a

particular job. Although this report is of no use for those organizations which

manufactures same products and services for all customers and earns same profit from

them as well.

P2 Preparation of income statement using different techniques

Microeconomics techniques

Cost: it means amount paid by the business to produce any product or render any service to th

customer. It is a sum total of amount paid by the business for running its normal course of

actions.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

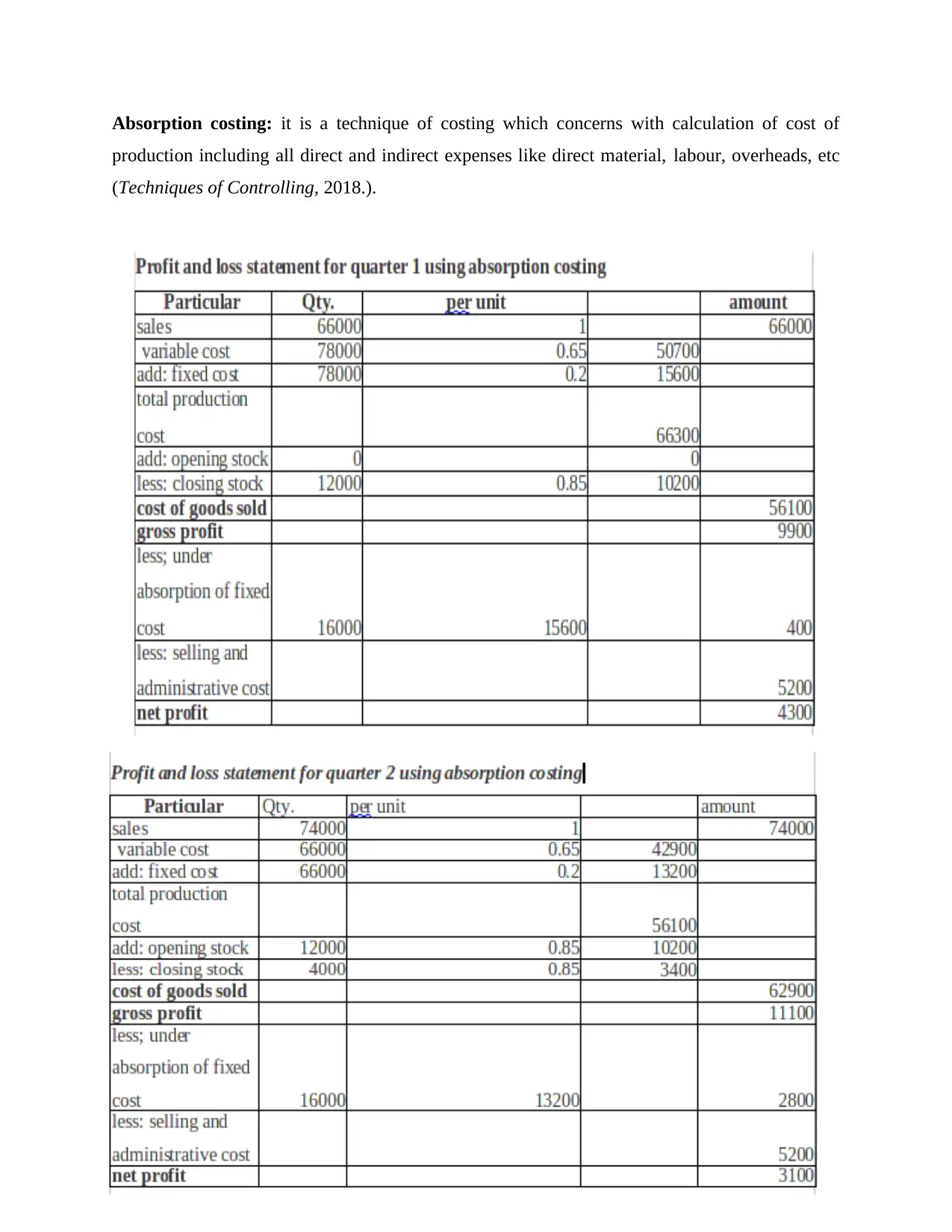

Absorption costing: it is a technique of costing which concerns with calculation of cost of

production including all direct and indirect expenses like direct material, labour, overheads, etc

(Techniques of Controlling, 2018.).

5

production including all direct and indirect expenses like direct material, labour, overheads, etc

(Techniques of Controlling, 2018.).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

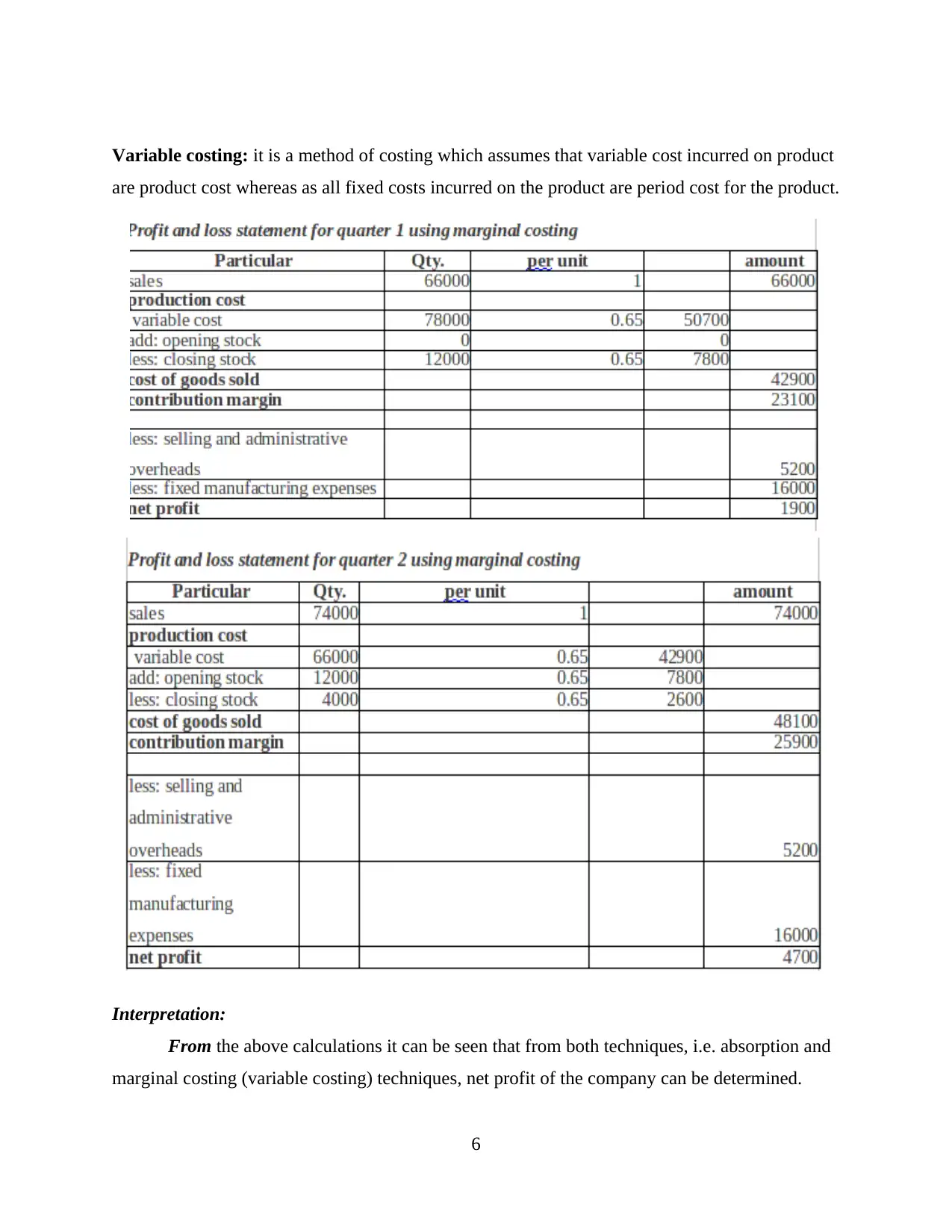

Variable costing: it is a method of costing which assumes that variable cost incurred on product

are product cost whereas as all fixed costs incurred on the product are period cost for the product.

Interpretation:

From the above calculations it can be seen that from both techniques, i.e. absorption and

marginal costing (variable costing) techniques, net profit of the company can be determined.

6

are product cost whereas as all fixed costs incurred on the product are period cost for the product.

Interpretation:

From the above calculations it can be seen that from both techniques, i.e. absorption and

marginal costing (variable costing) techniques, net profit of the company can be determined.

6

Absorption costing provides lower profit than marginal costing technique as it also includes

under or over absorption of cost by the mangers.

Cost volume profit:

This technique shows variation of cost at various levels of production. It is used to

determine break even point to evaluate selling price of product for gaining specific profit.

Flexible budgeting:

It shows the need of cost at different level of production level. It helps mangers in

determining the optimistic level of production at which it will need to incur minimum cost for

maximum output (Cool, Stouthuysen and Van den Abbeele, 2017).

Cost variance:

It shows the difference between budgeted cost and cost incurred by business. It majorly

helps management in determining cost efficiency of business, through which managers can take

appropriate action as to enhance the efficiency and having better control over business.

Product costing:

Cost allocation:

It includes bifurcation of various costs incurred in business operations at different level of

business. This process is used by management while preparing financial reports of company. It

helps in determining cost efficiency of all levels of business.

Standard costing:

This technique of costing helps in identifying efficiency of business' overall performance.

It includes various formulas which helps in comparing budgeted costs of business with actual

cost incurred during business operations.

Role of costing setting price:

Costing provides some methods and techniques which helps management in determining

actual cost of production through which they can determine selling price of product as to gain

reasonable profit from it:

It helps in determining actual cost incurred bu the business for production of particular

product through which company can determine selling price by adding set profit of

management (THE ROLE OF COSTS IN PRICING, 2019).

In case of production of customized product or services, through costing technique,

managers can determine cost incurred on each product which helps the company in

7

under or over absorption of cost by the mangers.

Cost volume profit:

This technique shows variation of cost at various levels of production. It is used to

determine break even point to evaluate selling price of product for gaining specific profit.

Flexible budgeting:

It shows the need of cost at different level of production level. It helps mangers in

determining the optimistic level of production at which it will need to incur minimum cost for

maximum output (Cool, Stouthuysen and Van den Abbeele, 2017).

Cost variance:

It shows the difference between budgeted cost and cost incurred by business. It majorly

helps management in determining cost efficiency of business, through which managers can take

appropriate action as to enhance the efficiency and having better control over business.

Product costing:

Cost allocation:

It includes bifurcation of various costs incurred in business operations at different level of

business. This process is used by management while preparing financial reports of company. It

helps in determining cost efficiency of all levels of business.

Standard costing:

This technique of costing helps in identifying efficiency of business' overall performance.

It includes various formulas which helps in comparing budgeted costs of business with actual

cost incurred during business operations.

Role of costing setting price:

Costing provides some methods and techniques which helps management in determining

actual cost of production through which they can determine selling price of product as to gain

reasonable profit from it:

It helps in determining actual cost incurred bu the business for production of particular

product through which company can determine selling price by adding set profit of

management (THE ROLE OF COSTS IN PRICING, 2019).

In case of production of customized product or services, through costing technique,

managers can determine cost incurred on each product which helps the company in

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

estimating selling price of product after adding profit as to be gained by business to fulfill

organization goals.

TASK 2

P4 Various planning tools of budgetary control and their advantages and disadvantages

Budgetary control

It is a technique of costing though which management predicts costs which would be

incurred by organisation in its normal course of action. Reports of budgetary control helps

management in having better control over efficiency of business .

Planning tools of budgetary control

Planning tools helps management in taking various decisions for business with the help

of various budgets like operating budget, financial budgets, etc. some planning tool are:

Cash budget: cash budget predicts receipts and payments of business in particular time

period. It helps in managing source of finance in advance which provides smoothness in

financial activities of business.

Pros Cons

It enables management to identify source of

finance in advance

Prediction of cost is uncertain, therefore, it

may provide wrong result

It helps in smooth running of normal course of

business.

It can be prepared for short period only.

Sale budget: it shows the expected sales to be made by business in order to gain

organizational goals. It makes management to fully utilize the resources for achieving

selling objectives (Budgetary Controlling Techniques, 2018).

Pros Cons

It shows management how the resources need

to be utilize to achieve predetermined sales.

It requires lots of informations to prepare sales

budget.

It helps in forecasting profit for the year. In case of wrong sales budget, whole

production and profit of business may suffer.

8

organization goals.

TASK 2

P4 Various planning tools of budgetary control and their advantages and disadvantages

Budgetary control

It is a technique of costing though which management predicts costs which would be

incurred by organisation in its normal course of action. Reports of budgetary control helps

management in having better control over efficiency of business .

Planning tools of budgetary control

Planning tools helps management in taking various decisions for business with the help

of various budgets like operating budget, financial budgets, etc. some planning tool are:

Cash budget: cash budget predicts receipts and payments of business in particular time

period. It helps in managing source of finance in advance which provides smoothness in

financial activities of business.

Pros Cons

It enables management to identify source of

finance in advance

Prediction of cost is uncertain, therefore, it

may provide wrong result

It helps in smooth running of normal course of

business.

It can be prepared for short period only.

Sale budget: it shows the expected sales to be made by business in order to gain

organizational goals. It makes management to fully utilize the resources for achieving

selling objectives (Budgetary Controlling Techniques, 2018).

Pros Cons

It shows management how the resources need

to be utilize to achieve predetermined sales.

It requires lots of informations to prepare sales

budget.

It helps in forecasting profit for the year. In case of wrong sales budget, whole

production and profit of business may suffer.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity based budget: it includes identifying, recording and analyzing of various

activities related to cost. It helps Nero ltd. In analyzing relation between various activities

of business.

Pros Cons

It enables management to analyse the actual

performance of business

Company needs numerous sources to prepare

activity based budget.

It helps managers in having effective

management of planning, controlling and

decision making process

It is a costly tool of budgeting, therefore every

company can not use it.

Evaluation of using different planning tools of budget for solving various financial

problems:

Above mentioned planning tools helps management in solving various financial problems

of business. Being a manufacturing concern, Nero ltd. Uses activity based planning tool for

solving its financial problems. With the help of it, company effectively predicts its cost to be

incurred in various activities through which it enables to identify sources of fund and being able

to eliminate financial problems in business.

Use of budget

Pricing: Through determining exact cost, organisation enables to set appropriate price of product

by adding reasonable profit in it.

Common costing system: it helps business in becoming more cost effective through comparing

budgeted cost with actual cost incurred.

Strategic planning: through budget, company enables to analyse various financial factors of

business with the help of PESTLE and SWOT analysis, company can effectively manage all the

factors influencing business of company.

P5 Adoption of management accounting system as to responding to various financial problems

Management accounting systems are to be used by managers in order to solving various

financial problems in effective way. Companies can use management accounting to solve

financial problems and grab success as under:

key performance indicator:

9

activities related to cost. It helps Nero ltd. In analyzing relation between various activities

of business.

Pros Cons

It enables management to analyse the actual

performance of business

Company needs numerous sources to prepare

activity based budget.

It helps managers in having effective

management of planning, controlling and

decision making process

It is a costly tool of budgeting, therefore every

company can not use it.

Evaluation of using different planning tools of budget for solving various financial

problems:

Above mentioned planning tools helps management in solving various financial problems

of business. Being a manufacturing concern, Nero ltd. Uses activity based planning tool for

solving its financial problems. With the help of it, company effectively predicts its cost to be

incurred in various activities through which it enables to identify sources of fund and being able

to eliminate financial problems in business.

Use of budget

Pricing: Through determining exact cost, organisation enables to set appropriate price of product

by adding reasonable profit in it.

Common costing system: it helps business in becoming more cost effective through comparing

budgeted cost with actual cost incurred.

Strategic planning: through budget, company enables to analyse various financial factors of

business with the help of PESTLE and SWOT analysis, company can effectively manage all the

factors influencing business of company.

P5 Adoption of management accounting system as to responding to various financial problems

Management accounting systems are to be used by managers in order to solving various

financial problems in effective way. Companies can use management accounting to solve

financial problems and grab success as under:

key performance indicator:

9

This system of accounting analyses overall performance of business. Company's

management can identify performance of each department of the organisaion and effectively

monitor them in order to enhance efficiency in their performance (Parmenter, 2015)).

` through monitoring performance of all departments, management of company enables to

estimate its future problems and can find their solution in advance, and also by effective control

over each department, company grows rapidly.

Bench marking:

While using this system, company selects few major factors which influences overall

performance of business. Management analyses those factors only for analysing overall business

performance.

It enables management in developing efficiency in key operations of business which

reduces the work of management through which their efficiency of management can be

improved. Which directly helps the company in having sustainable growth by its effective plans

and strategies (Lubis, Torong and Muda, 2016).

Balance score card:

Balance scorecard technique enables the mangers to link and interrelate all the factors of

business to develop a strong control over all business operations like, consumers, sales, purchase,

profit, etc. this management helps the company in determining the actual problem in a particular

activity, through which company can manage all the operations of business in effective way.

When business have control over all business operations, it automatically helps the company in

having sustainable growth in the market.

Financial governance:

It means collecting various informations to monitor financial activities of business as to

having an effective control over them. Through effective monitor over all financial activities,

company also enables to detect all the possible problems that can be arisen in the future. It helps

management in identifying their solutions in advance and help company in having smooth

growth in the future.

Identification of problems and effectively solving them

All management accounting techniques help management in detecting financial problems

in advance and determining their solutions as to have sustainable growth. Nero ltd. Adopts

balance score card technique, through which its managers develops a strong perspective over all

10

management can identify performance of each department of the organisaion and effectively

monitor them in order to enhance efficiency in their performance (Parmenter, 2015)).

` through monitoring performance of all departments, management of company enables to

estimate its future problems and can find their solution in advance, and also by effective control

over each department, company grows rapidly.

Bench marking:

While using this system, company selects few major factors which influences overall

performance of business. Management analyses those factors only for analysing overall business

performance.

It enables management in developing efficiency in key operations of business which

reduces the work of management through which their efficiency of management can be

improved. Which directly helps the company in having sustainable growth by its effective plans

and strategies (Lubis, Torong and Muda, 2016).

Balance score card:

Balance scorecard technique enables the mangers to link and interrelate all the factors of

business to develop a strong control over all business operations like, consumers, sales, purchase,

profit, etc. this management helps the company in determining the actual problem in a particular

activity, through which company can manage all the operations of business in effective way.

When business have control over all business operations, it automatically helps the company in

having sustainable growth in the market.

Financial governance:

It means collecting various informations to monitor financial activities of business as to

having an effective control over them. Through effective monitor over all financial activities,

company also enables to detect all the possible problems that can be arisen in the future. It helps

management in identifying their solutions in advance and help company in having smooth

growth in the future.

Identification of problems and effectively solving them

All management accounting techniques help management in detecting financial problems

in advance and determining their solutions as to have sustainable growth. Nero ltd. Adopts

balance score card technique, through which its managers develops a strong perspective over all

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.