Detailed Report on Management Accounting System and Financial Issues

VerifiedAdded on 2021/02/22

|19

|5440

|100

Report

AI Summary

This report delves into the multifaceted world of management accounting, exploring its core functions and various accounting systems, including cost accounting, inventory management, job costing, and price optimization. It examines different methods of management accounting reporting, such as cost accounting reports, inventory reports, and performance reports, providing a comprehensive overview of their purposes and applications. The report also analyzes the advantages and disadvantages of planning tools like budgetary control, comparing organizations and demonstrating how management accounting can resolve financial issues, ultimately contributing to organizational success. The report provides a detailed examination of the subject matter, including practical examples and real-world applications, making it a valuable resource for students studying finance and accounting.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

PART (A).........................................................................................................................................3

1. Explanation of management accounting..................................................................................3

2. Role of management accounting system along with various kind of accounting systems......4

3. Different method of management accounting reporting..........................................................6

4. Evaluation of management accounting system is integrated with the organisation................8

5. Evaluation of benefits of management accounting system......................................................8

6. Conclusions that reflect about the application of management accounting system.................9

PART (B).........................................................................................................................................9

(a) Advantages and disadvantages of different kind of planning tools of budgetary control......9

(b) Analysis of use of various planning tools and their application for preparing and

forecasting the budgets..............................................................................................................10

(c) Comparison of two organisations to resolve the financial issue by adapting the

management accounting system................................................................................................10

(d) Management accounting system to solve the financial issue that leads to organisational

success........................................................................................................................................12

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION ..........................................................................................................................3

PART (A).........................................................................................................................................3

1. Explanation of management accounting..................................................................................3

2. Role of management accounting system along with various kind of accounting systems......4

3. Different method of management accounting reporting..........................................................6

4. Evaluation of management accounting system is integrated with the organisation................8

5. Evaluation of benefits of management accounting system......................................................8

6. Conclusions that reflect about the application of management accounting system.................9

PART (B).........................................................................................................................................9

(a) Advantages and disadvantages of different kind of planning tools of budgetary control......9

(b) Analysis of use of various planning tools and their application for preparing and

forecasting the budgets..............................................................................................................10

(c) Comparison of two organisations to resolve the financial issue by adapting the

management accounting system................................................................................................10

(d) Management accounting system to solve the financial issue that leads to organisational

success........................................................................................................................................12

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is an accounting system which provides financial and non

financial information to the managers to make internal decisions (Arnaboldi, Lapsley,

Steccolini, 2015). In other words, this accounting system is related to the collecting, preparing,

summarising and interpreting the monetary and non monetary information. Herein, the project

report management accounting system and its types are mentioned as well as different method of

management accounting reporting are also described. Apart from it, advantages and

disadvantages of planning tools of budgetary control is also described along with role of

management accounting in solving the financial issues. To understand in detail about the

management accounting system, TPG processing company is selected that operates in

manufacturing sector.

PART (A)

1. Explanation of management accounting.

Management accounting system is an accounting system, that provides necessary and

needed information to the managers for internal management of the organisations (Sisaye,

Birnberg, 2012). Herein, some definition of management accounting system are mentioned

below:

According to the IMA (Institute of management accountants), “The management

accounting can be defined as a kind of profession that includes partnering in the management

decision making, planning, performance management and expertise in financial reporting”

(Jakobsen, 2012).

Comment- As per the above mentioned definition it can be comment that management

accounting system is very crucial for management of the organisations. On this accounting

system, managers can relay for decision making. Like in the TPG processing company, this

accounting system can be very beneficial for them in making planning and strategies for future.

According to the CIMA (Charted institute of management accountants), “ The

management accounting system can be defined as a process of measuring, accumulating,

preparing and communicating the information to managers so that they can take important

decisions” (Gibassier, 2017).

Management accounting is an accounting system which provides financial and non

financial information to the managers to make internal decisions (Arnaboldi, Lapsley,

Steccolini, 2015). In other words, this accounting system is related to the collecting, preparing,

summarising and interpreting the monetary and non monetary information. Herein, the project

report management accounting system and its types are mentioned as well as different method of

management accounting reporting are also described. Apart from it, advantages and

disadvantages of planning tools of budgetary control is also described along with role of

management accounting in solving the financial issues. To understand in detail about the

management accounting system, TPG processing company is selected that operates in

manufacturing sector.

PART (A)

1. Explanation of management accounting.

Management accounting system is an accounting system, that provides necessary and

needed information to the managers for internal management of the organisations (Sisaye,

Birnberg, 2012). Herein, some definition of management accounting system are mentioned

below:

According to the IMA (Institute of management accountants), “The management

accounting can be defined as a kind of profession that includes partnering in the management

decision making, planning, performance management and expertise in financial reporting”

(Jakobsen, 2012).

Comment- As per the above mentioned definition it can be comment that management

accounting system is very crucial for management of the organisations. On this accounting

system, managers can relay for decision making. Like in the TPG processing company, this

accounting system can be very beneficial for them in making planning and strategies for future.

According to the CIMA (Charted institute of management accountants), “ The

management accounting system can be defined as a process of measuring, accumulating,

preparing and communicating the information to managers so that they can take important

decisions” (Gibassier, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Comment- As per the above mentioned definition of CIMA, it can be comment that this

accounting system contains a wide and detailed process of presenting the financial and non

financial data. On the basis of this analysed information, companies take many important

decisions. Same as in the the TPG processing company, the management accounting system can

help them in making effective plans and policies for further decision making related to the

manufacturing system.

2. Role of management accounting system along with various kind of accounting systems.

The management accounting system plays an important role for management of the

companies (Schaltegger and Zvezdov, 2015). Due to this accounting system, organisations can

make further plans, policies and strategies. Herein, the context of TPG processing company, the

management accounting system is very important. This is why because, they are operating in the

manufacturing sector and various kind of accounting system helps them. Herein, some function

of the management accounting system are mentioned below:

Planning- This is the first and important function of the management accounting. In this

all needed information and authentic data is collected for planning. For example, in the

Starbucks company, they make planning related to the manufacturing of the products and

services which helps in important decision making.

Controlling- In this function of the management accounting system, it is being ensured

by the manager of the organisation that all available resources are effectively allocated or

not. Such as in the Starbucks company, their managers use this function of management

accounting in controlling the use of various kind of resources.

Cost accounting- As the name assists, this function of management accounting helps to

the organisations in controlling and predicting the future cost of different kind of

activities (Soltes, 2014). Like in the Starbucks company, they can use this function in

forecasting the cost of manufacturing.

Financial management- This is the function of management accounting which is related

to the collecting, analysing and managing of the financial information. With the help of

this function, the accountant of the Starbucks company manage all the financial

transactions effectively.

Auditing- This function of the management accounting is very important for the

companies. It is related with the inspection of the various kind of financial statements. In

accounting system contains a wide and detailed process of presenting the financial and non

financial data. On the basis of this analysed information, companies take many important

decisions. Same as in the the TPG processing company, the management accounting system can

help them in making effective plans and policies for further decision making related to the

manufacturing system.

2. Role of management accounting system along with various kind of accounting systems.

The management accounting system plays an important role for management of the

companies (Schaltegger and Zvezdov, 2015). Due to this accounting system, organisations can

make further plans, policies and strategies. Herein, the context of TPG processing company, the

management accounting system is very important. This is why because, they are operating in the

manufacturing sector and various kind of accounting system helps them. Herein, some function

of the management accounting system are mentioned below:

Planning- This is the first and important function of the management accounting. In this

all needed information and authentic data is collected for planning. For example, in the

Starbucks company, they make planning related to the manufacturing of the products and

services which helps in important decision making.

Controlling- In this function of the management accounting system, it is being ensured

by the manager of the organisation that all available resources are effectively allocated or

not. Such as in the Starbucks company, their managers use this function of management

accounting in controlling the use of various kind of resources.

Cost accounting- As the name assists, this function of management accounting helps to

the organisations in controlling and predicting the future cost of different kind of

activities (Soltes, 2014). Like in the Starbucks company, they can use this function in

forecasting the cost of manufacturing.

Financial management- This is the function of management accounting which is related

to the collecting, analysing and managing of the financial information. With the help of

this function, the accountant of the Starbucks company manage all the financial

transactions effectively.

Auditing- This function of the management accounting is very important for the

companies. It is related with the inspection of the various kind of financial statements. In

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the Starbucks, they can check the efficiency of the prepared financial statements by this

function.

So these are the main function of the management accounting system. Apart from it, various

types of management accounting system are mentioned below:

Cost accounting system- It is a kind of accounting system that provides a detailed

framework for estimating overall cost of products and services (Evans and Guthrie,

2013). On the basis of this accounting system, organisation can analyse about which

activities are consuming higher costs and which ones are not. So it is essential for

calculating overall cost that occurs due to different activities and operations. Along with

it is important in the better allocation of costs so that companies can find out about each

activity's cost separately. Herein, the context of TPG processing company this accounting

system can help them in computing the cost of manufacturing of different products.

Inventory management system- As the name assists, this accounting system is related

with the management of available stock in the organisation. In broad sense, this system

tracks the available quantity of raw material and finished goods in the stores. So it is

essential for making decisions regarding to the purchasing of raw material and

manufacturing of products. In the TPG, processing company they are involved in the

manufacturing sector so this accounting system can help them in making suitable

decision related to the production of new stock. Apart from it, this accounting system

includes various kind of methods to valuation of the stocks such as LIFO, FIFO etc. On

the basis of it organisations can decide about how much quantity of raw material is

needed to buy. If there is enough available stock in the warehouses then they will not

produce in higher quantity as well as if there is lack of goods in the store then they will

manufacture. So overall, it depends on the inventory management system. Job costing system- The job costing system is a kind of accounting system which tracks

the cost of revenues by specific job and provides reports on profitability by job (Morillo,

J.G., Díaz, J.A.R., Camacho, E. and Montesinos, 2015). In other words, this accounting

system provides detailed information about the cost by analysing cost associated with the

particular job. Eventually, the job costing system contains three types of information

which are as follows:

function.

So these are the main function of the management accounting system. Apart from it, various

types of management accounting system are mentioned below:

Cost accounting system- It is a kind of accounting system that provides a detailed

framework for estimating overall cost of products and services (Evans and Guthrie,

2013). On the basis of this accounting system, organisation can analyse about which

activities are consuming higher costs and which ones are not. So it is essential for

calculating overall cost that occurs due to different activities and operations. Along with

it is important in the better allocation of costs so that companies can find out about each

activity's cost separately. Herein, the context of TPG processing company this accounting

system can help them in computing the cost of manufacturing of different products.

Inventory management system- As the name assists, this accounting system is related

with the management of available stock in the organisation. In broad sense, this system

tracks the available quantity of raw material and finished goods in the stores. So it is

essential for making decisions regarding to the purchasing of raw material and

manufacturing of products. In the TPG, processing company they are involved in the

manufacturing sector so this accounting system can help them in making suitable

decision related to the production of new stock. Apart from it, this accounting system

includes various kind of methods to valuation of the stocks such as LIFO, FIFO etc. On

the basis of it organisations can decide about how much quantity of raw material is

needed to buy. If there is enough available stock in the warehouses then they will not

produce in higher quantity as well as if there is lack of goods in the store then they will

manufacture. So overall, it depends on the inventory management system. Job costing system- The job costing system is a kind of accounting system which tracks

the cost of revenues by specific job and provides reports on profitability by job (Morillo,

J.G., Díaz, J.A.R., Camacho, E. and Montesinos, 2015). In other words, this accounting

system provides detailed information about the cost by analysing cost associated with the

particular job. Eventually, the job costing system contains three types of information

which are as follows:

Direct material- This costing system, tracks the cost of material which is being used

during the course of job.

Direct labour- The job costing system evaluates the cost of labour that is used on a job.

Overhead- This costing system allocates the cost of overhead to different kind of cost

pools. After the end of the accounting period, the total cost of all cost pools allocated to

each involved job.

So the job costing system includes above mentioned information as well as on the basis

of it each involved job's cost is calculated separately. Basically, this accounting system is

essential for the companies in allocating each cost to septate job as well as to compute the total

cost of job. In the TPG processing company, this costing system can play an important role in the

proper management of the cost by assigning each job's cost separately.

Price optimisation system- The price optimisation system is an important part of the

management accounting system. This accounting system provides a kind of framework

which helps in determining the right pricing of the products and services. As well as on

the basis of this accounting system, companies can evaluate customer's reaction on

different pricing and accordingly they can fluctuate the prices. The big advantage of this

accounting system is that it determines pricing level at a level which is suitable for both

to the customers and company. Eventually, the price optimisation system is essential for

the companies in assigning the price at accurate level. In the TPG processing company,

this accounting system can be very crucial because with the help of this, they can fix their

manufactured product's price. As well as they can evaluate their customer's reaction on

different pricing stages and can modify accordingly.

So these are the types of management accounting systems which have their own benefits. As

well as in the TPG processing company, this system helps them at various stage of the

manufacturing process.

3. Different method of management accounting reporting.

Management accounting reporting- The management accounting reporting is different

from the financial accounting reporting. This kind of reporting consists both financial and non

financial information which becomes useful for the internal stakeholders. There are different

during the course of job.

Direct labour- The job costing system evaluates the cost of labour that is used on a job.

Overhead- This costing system allocates the cost of overhead to different kind of cost

pools. After the end of the accounting period, the total cost of all cost pools allocated to

each involved job.

So the job costing system includes above mentioned information as well as on the basis

of it each involved job's cost is calculated separately. Basically, this accounting system is

essential for the companies in allocating each cost to septate job as well as to compute the total

cost of job. In the TPG processing company, this costing system can play an important role in the

proper management of the cost by assigning each job's cost separately.

Price optimisation system- The price optimisation system is an important part of the

management accounting system. This accounting system provides a kind of framework

which helps in determining the right pricing of the products and services. As well as on

the basis of this accounting system, companies can evaluate customer's reaction on

different pricing and accordingly they can fluctuate the prices. The big advantage of this

accounting system is that it determines pricing level at a level which is suitable for both

to the customers and company. Eventually, the price optimisation system is essential for

the companies in assigning the price at accurate level. In the TPG processing company,

this accounting system can be very crucial because with the help of this, they can fix their

manufactured product's price. As well as they can evaluate their customer's reaction on

different pricing stages and can modify accordingly.

So these are the types of management accounting systems which have their own benefits. As

well as in the TPG processing company, this system helps them at various stage of the

manufacturing process.

3. Different method of management accounting reporting.

Management accounting reporting- The management accounting reporting is different

from the financial accounting reporting. This kind of reporting consists both financial and non

financial information which becomes useful for the internal stakeholders. There are different

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

kind of accounting reports that have multi-pal purposes. In the TPG processing company, they

prepares various kind of reports which are mentioned below:

Cost accounting reports- These reports are being prepared with the use of cost

accounting systems (ieckhof, Bergmann and Guenther, 2015). Under the cost accounting

reports detailed information related to the various kind of costs of different activities

includes. On the basis of these reports, companies can get needed information regarding

to the overall cost and take important decision about the cost control and management.

Eventually, in the absence of these reports, it becomes difficult for the companies to

estimate about the actual cost. The main purpose of this report is to get knowledge and

information about the cost of various operations and activities. The cost accounting

reports are prepared after the completion of an accounting period. For TPG processing

company, this accounting system can be very beneficial and useful because they are

operating in the manufacturing sector and it is necessary for a manufacturing entity to

have information about the cost. With the use of this accounting system, they can control

those activities which are consuming higher cost.

Inventory reports- The inventory reports includes the information regarding to quantity

of available raw material and finished goods at the warehouses. Due to this report

companies can manage the quantity of material as well as can take suitable decisions.

Apart from it, these reports also useful in providing information related to the cost of

inventory such as ordering cost, storing cost etc. The main purpose of this report is to

helping companies in taking decisions related to the purchasing of new raw material

according to the available stock in the stores. Eventually, this report is prepared as per the

need of organisation or at the end of month. Like in the TPG processing company, these

reports can help them in effective management of the available raw material and finished

products.

Performance report- As the name assist, the performance reports are those reports

which consists information regarding to the performance of various kind of activities. In

these reports, the actual profits and costs are compared with the budgeted profits and

costs. If actual income is more then budgeted income then performance will be rated as

good and vice versa. So basically, main purpose of this report is to provide actual

information about the performance. This report is prepared as per the end of budgeted

prepares various kind of reports which are mentioned below:

Cost accounting reports- These reports are being prepared with the use of cost

accounting systems (ieckhof, Bergmann and Guenther, 2015). Under the cost accounting

reports detailed information related to the various kind of costs of different activities

includes. On the basis of these reports, companies can get needed information regarding

to the overall cost and take important decision about the cost control and management.

Eventually, in the absence of these reports, it becomes difficult for the companies to

estimate about the actual cost. The main purpose of this report is to get knowledge and

information about the cost of various operations and activities. The cost accounting

reports are prepared after the completion of an accounting period. For TPG processing

company, this accounting system can be very beneficial and useful because they are

operating in the manufacturing sector and it is necessary for a manufacturing entity to

have information about the cost. With the use of this accounting system, they can control

those activities which are consuming higher cost.

Inventory reports- The inventory reports includes the information regarding to quantity

of available raw material and finished goods at the warehouses. Due to this report

companies can manage the quantity of material as well as can take suitable decisions.

Apart from it, these reports also useful in providing information related to the cost of

inventory such as ordering cost, storing cost etc. The main purpose of this report is to

helping companies in taking decisions related to the purchasing of new raw material

according to the available stock in the stores. Eventually, this report is prepared as per the

need of organisation or at the end of month. Like in the TPG processing company, these

reports can help them in effective management of the available raw material and finished

products.

Performance report- As the name assist, the performance reports are those reports

which consists information regarding to the performance of various kind of activities. In

these reports, the actual profits and costs are compared with the budgeted profits and

costs. If actual income is more then budgeted income then performance will be rated as

good and vice versa. So basically, main purpose of this report is to provide actual

information about the performance. This report is prepared as per the end of budgeted

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

time period. In the TPG processing company, this report can be useful in providing

information about the actual performance of their. Due to this report they can evaluate

about how much profit they are earning from different activities and they can make

suitable changes accordingly.

Budget reports- The budget reports are those reports which are being used by the

companies to compare the actual performance number with the budgeted projection

(Derchi, Burkert and Oyon, 2013). This report's concept is similar to the performance

report. The difference is that in this report both the data includes budgeted and actual.

While in the performance report only information related to the comparison of actual and

budgeted activities includes. So the main purpose of this report is to provide detailed

information regarding to the actual and budgeted performance. This type of report is

prepared after the end of budgeted time period. In the TPG processing company, this

report can be useful for the making further decision on the basis of comparison between

actual performance and budgeted projection.

Account receivable ageing report- It is a kind of report which provides detailed

information about the unpaid debtors by date range. Eventually, this report is suitable for

those companies who deals in credit basis. With the help of this report companies can

keep the record about their unpaid debtors. The main purpose of this report is to helping

the companies in collection of payment from the creditors. In the absence of this report, it

will be difficult for the accountant to remember about the creditors with date. Basically,

this report is prepared at the end of an accounting period. In the TPG processing

company, their accountant can collect the cash easily with interest from the buyers.

4. Evaluation of management accounting system is integrated with the organisation.

The management accounting system is aligned with the different activities and operations

of the organisations. This is why different types of management accounting systems like cost

accounting system, inventory management system etc. help in managing the functions. Such as

in the TPG processing company, they use inventory management system for the managing the

stock and raw material. As well as cost accounting system is aligned with the controlling of

different costs. So overall, management accounting system is linked with the different functions

of the organisation.

information about the actual performance of their. Due to this report they can evaluate

about how much profit they are earning from different activities and they can make

suitable changes accordingly.

Budget reports- The budget reports are those reports which are being used by the

companies to compare the actual performance number with the budgeted projection

(Derchi, Burkert and Oyon, 2013). This report's concept is similar to the performance

report. The difference is that in this report both the data includes budgeted and actual.

While in the performance report only information related to the comparison of actual and

budgeted activities includes. So the main purpose of this report is to provide detailed

information regarding to the actual and budgeted performance. This type of report is

prepared after the end of budgeted time period. In the TPG processing company, this

report can be useful for the making further decision on the basis of comparison between

actual performance and budgeted projection.

Account receivable ageing report- It is a kind of report which provides detailed

information about the unpaid debtors by date range. Eventually, this report is suitable for

those companies who deals in credit basis. With the help of this report companies can

keep the record about their unpaid debtors. The main purpose of this report is to helping

the companies in collection of payment from the creditors. In the absence of this report, it

will be difficult for the accountant to remember about the creditors with date. Basically,

this report is prepared at the end of an accounting period. In the TPG processing

company, their accountant can collect the cash easily with interest from the buyers.

4. Evaluation of management accounting system is integrated with the organisation.

The management accounting system is aligned with the different activities and operations

of the organisations. This is why different types of management accounting systems like cost

accounting system, inventory management system etc. help in managing the functions. Such as

in the TPG processing company, they use inventory management system for the managing the

stock and raw material. As well as cost accounting system is aligned with the controlling of

different costs. So overall, management accounting system is linked with the different functions

of the organisation.

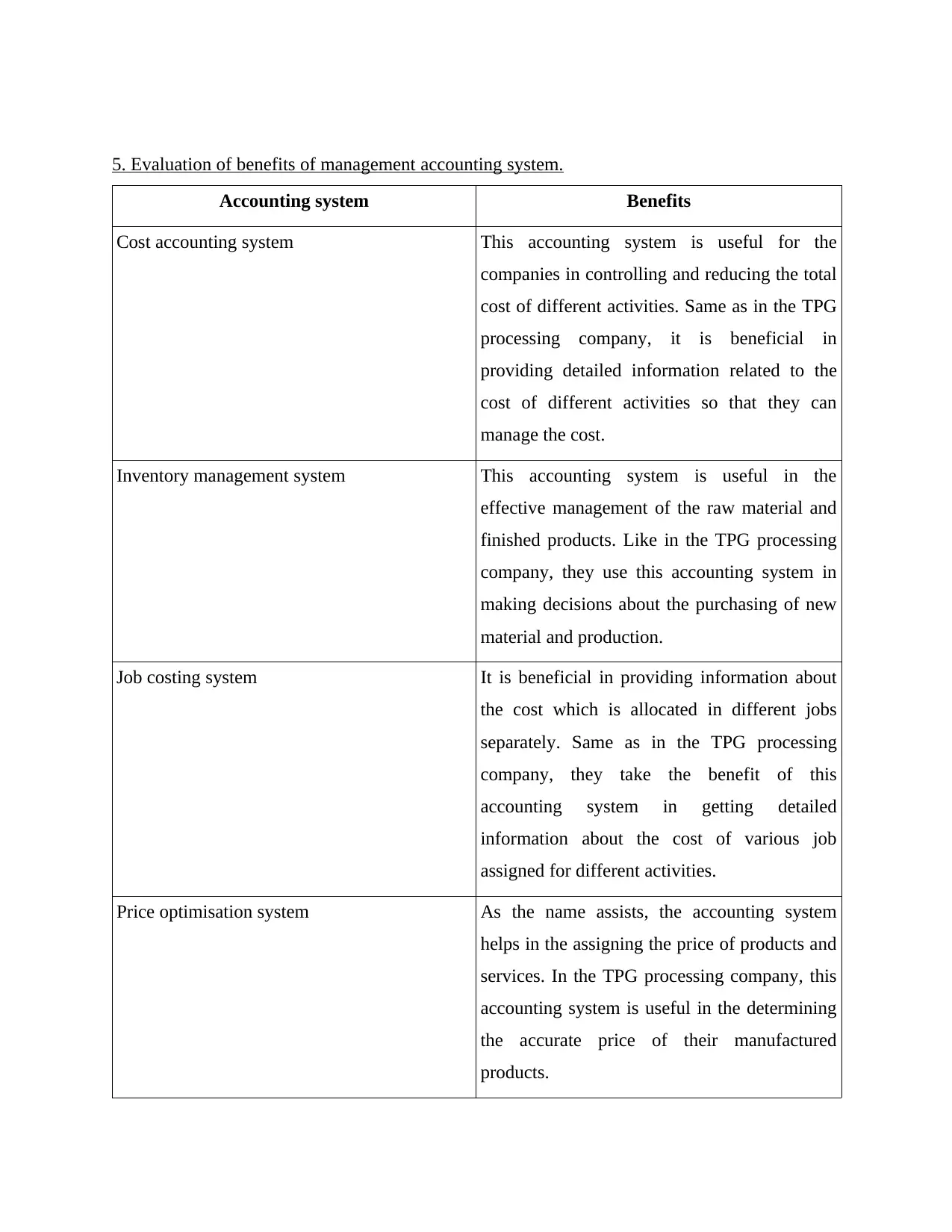

5. Evaluation of benefits of management accounting system.

Accounting system Benefits

Cost accounting system This accounting system is useful for the

companies in controlling and reducing the total

cost of different activities. Same as in the TPG

processing company, it is beneficial in

providing detailed information related to the

cost of different activities so that they can

manage the cost.

Inventory management system This accounting system is useful in the

effective management of the raw material and

finished products. Like in the TPG processing

company, they use this accounting system in

making decisions about the purchasing of new

material and production.

Job costing system It is beneficial in providing information about

the cost which is allocated in different jobs

separately. Same as in the TPG processing

company, they take the benefit of this

accounting system in getting detailed

information about the cost of various job

assigned for different activities.

Price optimisation system As the name assists, the accounting system

helps in the assigning the price of products and

services. In the TPG processing company, this

accounting system is useful in the determining

the accurate price of their manufactured

products.

Accounting system Benefits

Cost accounting system This accounting system is useful for the

companies in controlling and reducing the total

cost of different activities. Same as in the TPG

processing company, it is beneficial in

providing detailed information related to the

cost of different activities so that they can

manage the cost.

Inventory management system This accounting system is useful in the

effective management of the raw material and

finished products. Like in the TPG processing

company, they use this accounting system in

making decisions about the purchasing of new

material and production.

Job costing system It is beneficial in providing information about

the cost which is allocated in different jobs

separately. Same as in the TPG processing

company, they take the benefit of this

accounting system in getting detailed

information about the cost of various job

assigned for different activities.

Price optimisation system As the name assists, the accounting system

helps in the assigning the price of products and

services. In the TPG processing company, this

accounting system is useful in the determining

the accurate price of their manufactured

products.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

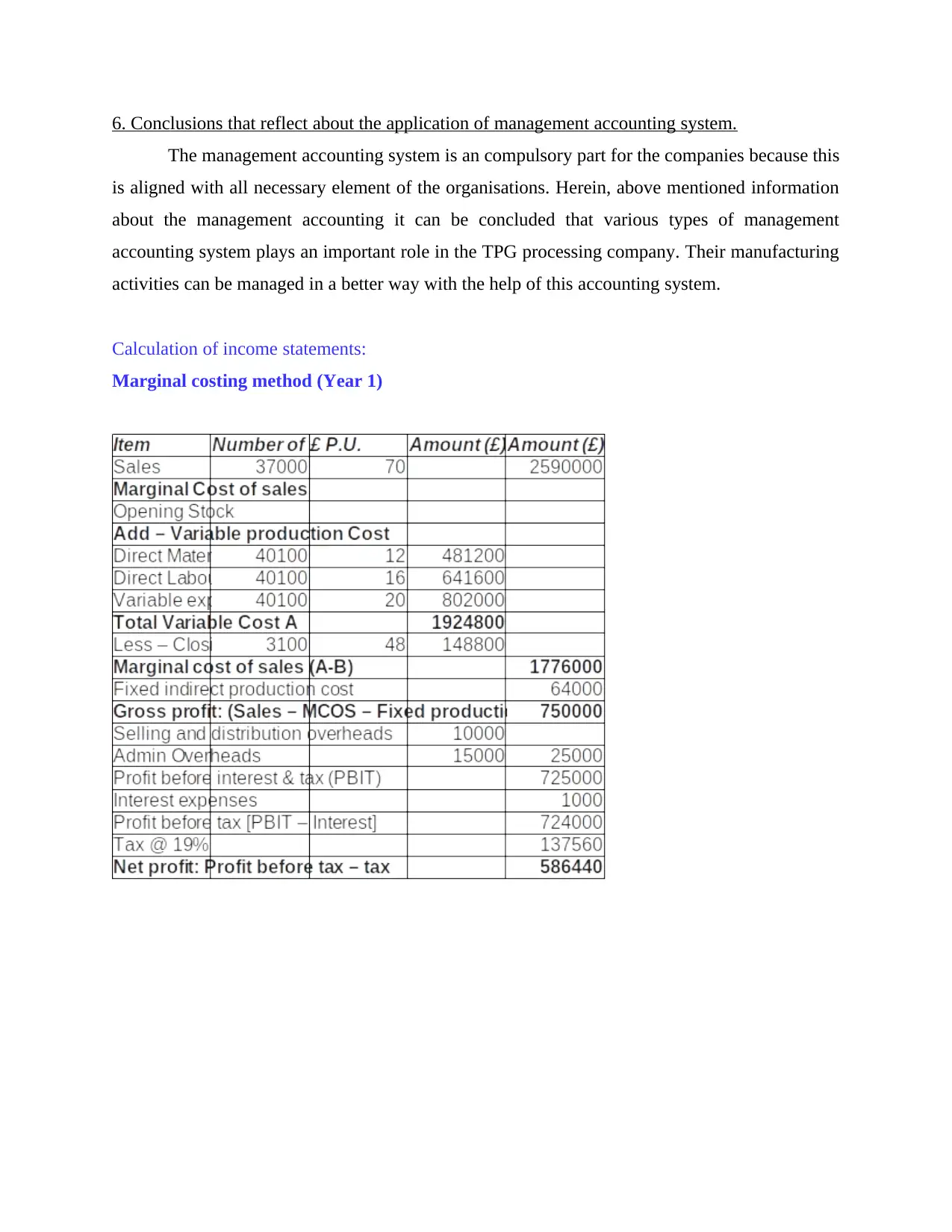

6. Conclusions that reflect about the application of management accounting system.

The management accounting system is an compulsory part for the companies because this

is aligned with all necessary element of the organisations. Herein, above mentioned information

about the management accounting it can be concluded that various types of management

accounting system plays an important role in the TPG processing company. Their manufacturing

activities can be managed in a better way with the help of this accounting system.

Calculation of income statements:

Marginal costing method (Year 1)

The management accounting system is an compulsory part for the companies because this

is aligned with all necessary element of the organisations. Herein, above mentioned information

about the management accounting it can be concluded that various types of management

accounting system plays an important role in the TPG processing company. Their manufacturing

activities can be managed in a better way with the help of this accounting system.

Calculation of income statements:

Marginal costing method (Year 1)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Marginal Costing method (Year 2)

Item Number of units£ P.U. Amount (£) Amount (£)

Sales 41000 70 2870000

Marginal Cost of sales

Opening Stock 3100 48 148800

Add – Variable production Cost

Direct Material 48100 12 577200

Direct Labour 48100 16 769600

Variable expenses48100 20 962000

Total Variable Cost A 2457600

Less – Closing stock – end of year 1 B [opening stock units + Units produced – units sold]10200 48 489600

Marginal cost of sales (A-B) 1968000

Fixed indirect production cost 64000

Gross profit: (Sales – MCOS – Fixed production cost )838000

Selling and distribution overheads 10500

Admin Overheads 15000

Profit before interest & tax (PBIT) 812500

Interest expenses 1250

Profit before tax [PBIT – Interest] 811250

Tax @ 19% 154137.5

Net profit: Profit before tax – tax 657112.5

Marginal Costing method (Year 3)

Item Number of units£ P.U. Amount (£) Amount (£)

Sales 61000 70 4270000

Marginal Cost of sales

Opening Stock 10200 48 489600

Add – Variable production Cost

Direct Material 51100 12 613200

Direct Labour 51100 16 817600

Variable expenses51100 20 1022000

Total Variable Cost A 2942400

Less – Closing stock – end of year 1 B [opening stock units + Units produced – units sold]300 48 14400

Marginal cost of sales (A-B) 2928000

Fixed indirect production cost 64000

Gross profit: (Sales – MCOS – Fixed production cost )1278000

Selling and distribution overheads 11000

Admin Overheads 15000

Profit before interest & tax (PBIT) 1252000

Interest expenses 1500

Profit before tax [PBIT – Interest] 1250500

Tax @ 19% 237595

Net profit: Profit before tax – tax 1012905

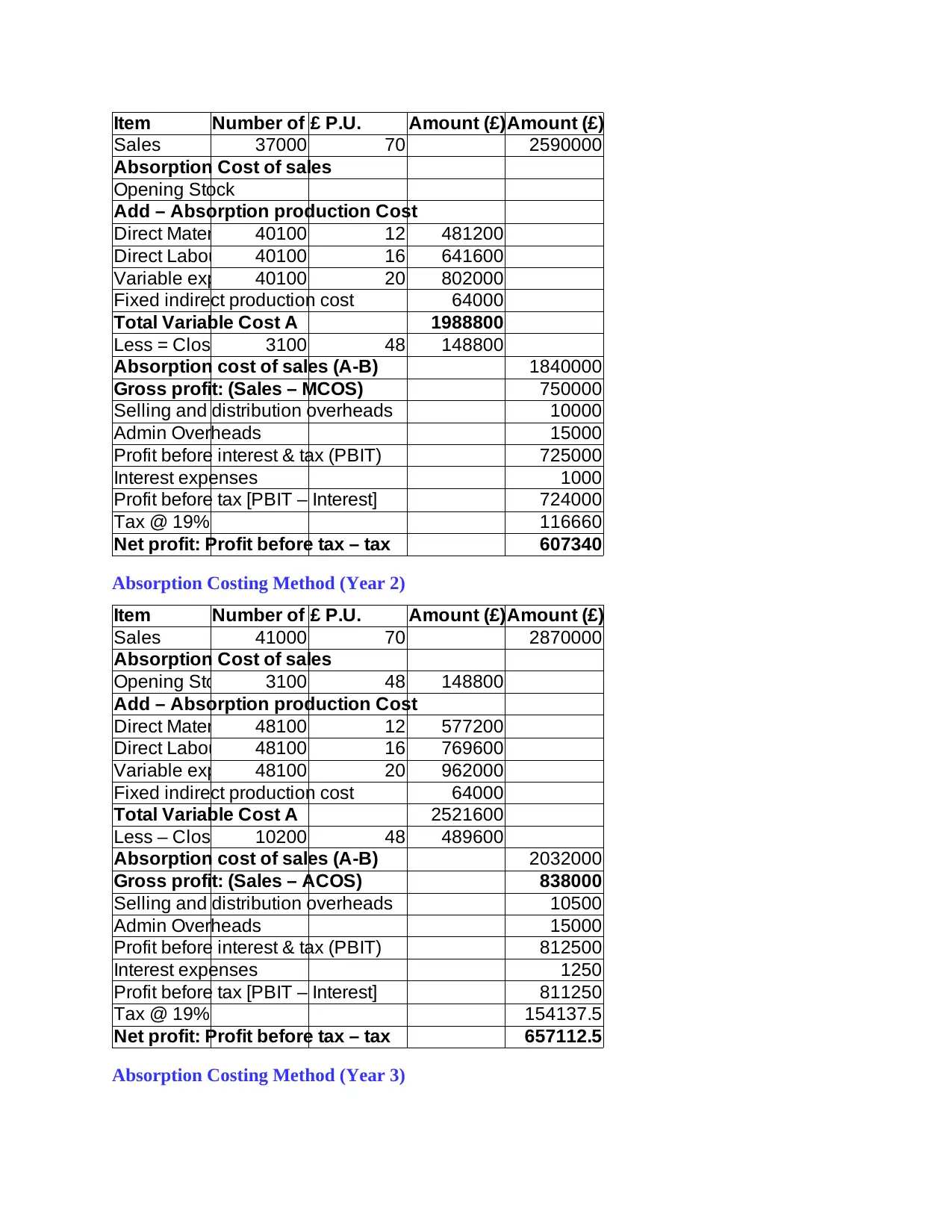

Absorption Costing method (Year 1)

Item Number of units£ P.U. Amount (£) Amount (£)

Sales 41000 70 2870000

Marginal Cost of sales

Opening Stock 3100 48 148800

Add – Variable production Cost

Direct Material 48100 12 577200

Direct Labour 48100 16 769600

Variable expenses48100 20 962000

Total Variable Cost A 2457600

Less – Closing stock – end of year 1 B [opening stock units + Units produced – units sold]10200 48 489600

Marginal cost of sales (A-B) 1968000

Fixed indirect production cost 64000

Gross profit: (Sales – MCOS – Fixed production cost )838000

Selling and distribution overheads 10500

Admin Overheads 15000

Profit before interest & tax (PBIT) 812500

Interest expenses 1250

Profit before tax [PBIT – Interest] 811250

Tax @ 19% 154137.5

Net profit: Profit before tax – tax 657112.5

Marginal Costing method (Year 3)

Item Number of units£ P.U. Amount (£) Amount (£)

Sales 61000 70 4270000

Marginal Cost of sales

Opening Stock 10200 48 489600

Add – Variable production Cost

Direct Material 51100 12 613200

Direct Labour 51100 16 817600

Variable expenses51100 20 1022000

Total Variable Cost A 2942400

Less – Closing stock – end of year 1 B [opening stock units + Units produced – units sold]300 48 14400

Marginal cost of sales (A-B) 2928000

Fixed indirect production cost 64000

Gross profit: (Sales – MCOS – Fixed production cost )1278000

Selling and distribution overheads 11000

Admin Overheads 15000

Profit before interest & tax (PBIT) 1252000

Interest expenses 1500

Profit before tax [PBIT – Interest] 1250500

Tax @ 19% 237595

Net profit: Profit before tax – tax 1012905

Absorption Costing method (Year 1)

Item Number of units£ P.U. Amount (£) Amount (£)

Sales 37000 70 2590000

Absorption Cost of sales

Opening Stock

Add – Absorption production Cost

Direct Material 40100 12 481200

Direct Labour 40100 16 641600

Variable expenses40100 20 802000

Fixed indirect production cost 64000

Total Variable Cost A 1988800

Less = Closing stock – end of year 1 B [opening stock units + Units produced – units sold]3100 48 148800

Absorption cost of sales (A-B) 1840000

Gross profit: (Sales – MCOS) 750000

Selling and distribution overheads 10000

Admin Overheads 15000

Profit before interest & tax (PBIT) 725000

Interest expenses 1000

Profit before tax [PBIT – Interest] 724000

Tax @ 19% 116660

Net profit: Profit before tax – tax 607340

Absorption Costing Method (Year 2)

Item Number of units£ P.U. Amount (£) Amount (£)

Sales 41000 70 2870000

Absorption Cost of sales

Opening Stock 3100 48 148800

Add – Absorption production Cost

Direct Material 48100 12 577200

Direct Labour 48100 16 769600

Variable expenses48100 20 962000

Fixed indirect production cost 64000

Total Variable Cost A 2521600

Less – Closing stock – end of year 1 B [opening stock units + Units produced – units sold]10200 48 489600

Absorption cost of sales (A-B) 2032000

Gross profit: (Sales – ACOS) 838000

Selling and distribution overheads 10500

Admin Overheads 15000

Profit before interest & tax (PBIT) 812500

Interest expenses 1250

Profit before tax [PBIT – Interest] 811250

Tax @ 19% 154137.5

Net profit: Profit before tax – tax 657112.5

Absorption Costing Method (Year 3)

Sales 37000 70 2590000

Absorption Cost of sales

Opening Stock

Add – Absorption production Cost

Direct Material 40100 12 481200

Direct Labour 40100 16 641600

Variable expenses40100 20 802000

Fixed indirect production cost 64000

Total Variable Cost A 1988800

Less = Closing stock – end of year 1 B [opening stock units + Units produced – units sold]3100 48 148800

Absorption cost of sales (A-B) 1840000

Gross profit: (Sales – MCOS) 750000

Selling and distribution overheads 10000

Admin Overheads 15000

Profit before interest & tax (PBIT) 725000

Interest expenses 1000

Profit before tax [PBIT – Interest] 724000

Tax @ 19% 116660

Net profit: Profit before tax – tax 607340

Absorption Costing Method (Year 2)

Item Number of units£ P.U. Amount (£) Amount (£)

Sales 41000 70 2870000

Absorption Cost of sales

Opening Stock 3100 48 148800

Add – Absorption production Cost

Direct Material 48100 12 577200

Direct Labour 48100 16 769600

Variable expenses48100 20 962000

Fixed indirect production cost 64000

Total Variable Cost A 2521600

Less – Closing stock – end of year 1 B [opening stock units + Units produced – units sold]10200 48 489600

Absorption cost of sales (A-B) 2032000

Gross profit: (Sales – ACOS) 838000

Selling and distribution overheads 10500

Admin Overheads 15000

Profit before interest & tax (PBIT) 812500

Interest expenses 1250

Profit before tax [PBIT – Interest] 811250

Tax @ 19% 154137.5

Net profit: Profit before tax – tax 657112.5

Absorption Costing Method (Year 3)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.