Management Accounting System and Techniques Report for Capital Joinery

VerifiedAdded on 2023/01/05

|19

|5435

|27

Report

AI Summary

This report provides a comprehensive analysis of management accounting systems and techniques, focusing on Capital Joinery Ltd. It explores various types of management accounting systems, including cost-accounting and inventory management systems, and their application within an organization. The report also delves into different methods for management accounting reporting, such as budgetary reports and performance management reports, and their significance. Furthermore, it examines cost analysis techniques to prepare an income statement, including variable and fixed costs, cost-volume-profit analysis, and marginal costing. Additionally, the report discusses planning tools and their advantages and disadvantages, along with their applications for forecasting and budgeting. Finally, it addresses how organizations adapt management accounting systems in response to financial problems, analyzing how planning tools help in solving these issues and leading to sustainable success. The report is a valuable resource for understanding the practical application of management accounting principles.

MANAGEMENT

ACCOUNTING

SYSTEM AND

TECHNIQUES

ACCOUNTING

SYSTEM AND

TECHNIQUES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and different types of management accounting systems:..............1

P2: Different methods for management accounting reporting:....................................................3

M1: Benefits of management accounting system and their application within an organisation: 7

D1: How management accounting system and management accounting reports are integrated

within an organisation:.................................................................................................................8

TASK 2............................................................................................................................................8

P3: Techniques of cost analysis to prepare an income statement:...............................................8

M2: Range of management accounting techniques for financial reporting:..............................10

D2: Explanation of financial reports in range of business activities:........................................10

TASK 3..........................................................................................................................................10

P4: Different types of planning tool and their advantages or disadvantages:............................10

M3: Planning tools and their applications for forecasting and preparing budget:.....................12

TASK 4..........................................................................................................................................12

P5: How organisations are adapting management accounting systems in respond to financial

problems:....................................................................................................................................12

M4: Analyse financial problems in management accounting can lead organisation to

sustainable success:....................................................................................................................14

D3: How planning tools helps in to solving financial problems:...............................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and different types of management accounting systems:..............1

P2: Different methods for management accounting reporting:....................................................3

M1: Benefits of management accounting system and their application within an organisation: 7

D1: How management accounting system and management accounting reports are integrated

within an organisation:.................................................................................................................8

TASK 2............................................................................................................................................8

P3: Techniques of cost analysis to prepare an income statement:...............................................8

M2: Range of management accounting techniques for financial reporting:..............................10

D2: Explanation of financial reports in range of business activities:........................................10

TASK 3..........................................................................................................................................10

P4: Different types of planning tool and their advantages or disadvantages:............................10

M3: Planning tools and their applications for forecasting and preparing budget:.....................12

TASK 4..........................................................................................................................................12

P5: How organisations are adapting management accounting systems in respond to financial

problems:....................................................................................................................................12

M4: Analyse financial problems in management accounting can lead organisation to

sustainable success:....................................................................................................................14

D3: How planning tools helps in to solving financial problems:...............................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is an internal system that provides critical information to firm's

management so that it can used in operations decision making. Organisations uses it to measure

and evaluate its performance according to information. It involves preparation of financial

reports, decision making and activities within an organisation. Company which is selected for

this report is Capital joinery Ltd. It is firm that specialised in windows, doors and stairs. It was

founded in 2008, situated in London UK (Vetrov and 2017). This report covers various topics

such as requirement of different types of management accounting systems, method for used

management accounting reports and different cost techniques to prepare an income statement.

Apart from this it also covers different planning tools and their advantages or disadvantages and

the ways in which organisations adapting management accounting system to respond to financial

problems.

TASK 1

P1: Management accounting and different types of management accounting systems:

Management accounting is refers to preparation of business reports that helps

management to generate its business operations and helps in short term and long term decision

making. It helps in planning, managing, measuring, evaluating and interpreting information to

managers.

Management accounting system is an internal system of any firm that an organisation

used to measure and evaluate its operations or activities for the management of the entity. In

context to Capital joinery Ltd., management team of the firm uses this system to evaluate firm's

operations so that it can achieve its goals or objective in efficient manner. It provides an insight

towards organisations decisions that helps managers to take corrective actions. It also provide

financial health and statical information assist by strong software that supports an organisations

decision making. It divides overall business unit into different departments on the basis of

production and functions so that it will be easy for Capital joinery to evaluate its performance.

Management accounting principles that company used are influence, relevance, value and

trust. Influence means it provides an insight that is influential, Relevance it gives relevant

information, value is analysed and in context to trust is it generates trust by providing overview

and relevance information.

1

Management accounting is an internal system that provides critical information to firm's

management so that it can used in operations decision making. Organisations uses it to measure

and evaluate its performance according to information. It involves preparation of financial

reports, decision making and activities within an organisation. Company which is selected for

this report is Capital joinery Ltd. It is firm that specialised in windows, doors and stairs. It was

founded in 2008, situated in London UK (Vetrov and 2017). This report covers various topics

such as requirement of different types of management accounting systems, method for used

management accounting reports and different cost techniques to prepare an income statement.

Apart from this it also covers different planning tools and their advantages or disadvantages and

the ways in which organisations adapting management accounting system to respond to financial

problems.

TASK 1

P1: Management accounting and different types of management accounting systems:

Management accounting is refers to preparation of business reports that helps

management to generate its business operations and helps in short term and long term decision

making. It helps in planning, managing, measuring, evaluating and interpreting information to

managers.

Management accounting system is an internal system of any firm that an organisation

used to measure and evaluate its operations or activities for the management of the entity. In

context to Capital joinery Ltd., management team of the firm uses this system to evaluate firm's

operations so that it can achieve its goals or objective in efficient manner. It provides an insight

towards organisations decisions that helps managers to take corrective actions. It also provide

financial health and statical information assist by strong software that supports an organisations

decision making. It divides overall business unit into different departments on the basis of

production and functions so that it will be easy for Capital joinery to evaluate its performance.

Management accounting principles that company used are influence, relevance, value and

trust. Influence means it provides an insight that is influential, Relevance it gives relevant

information, value is analysed and in context to trust is it generates trust by providing overview

and relevance information.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Basis Financial Accounting Management accounting

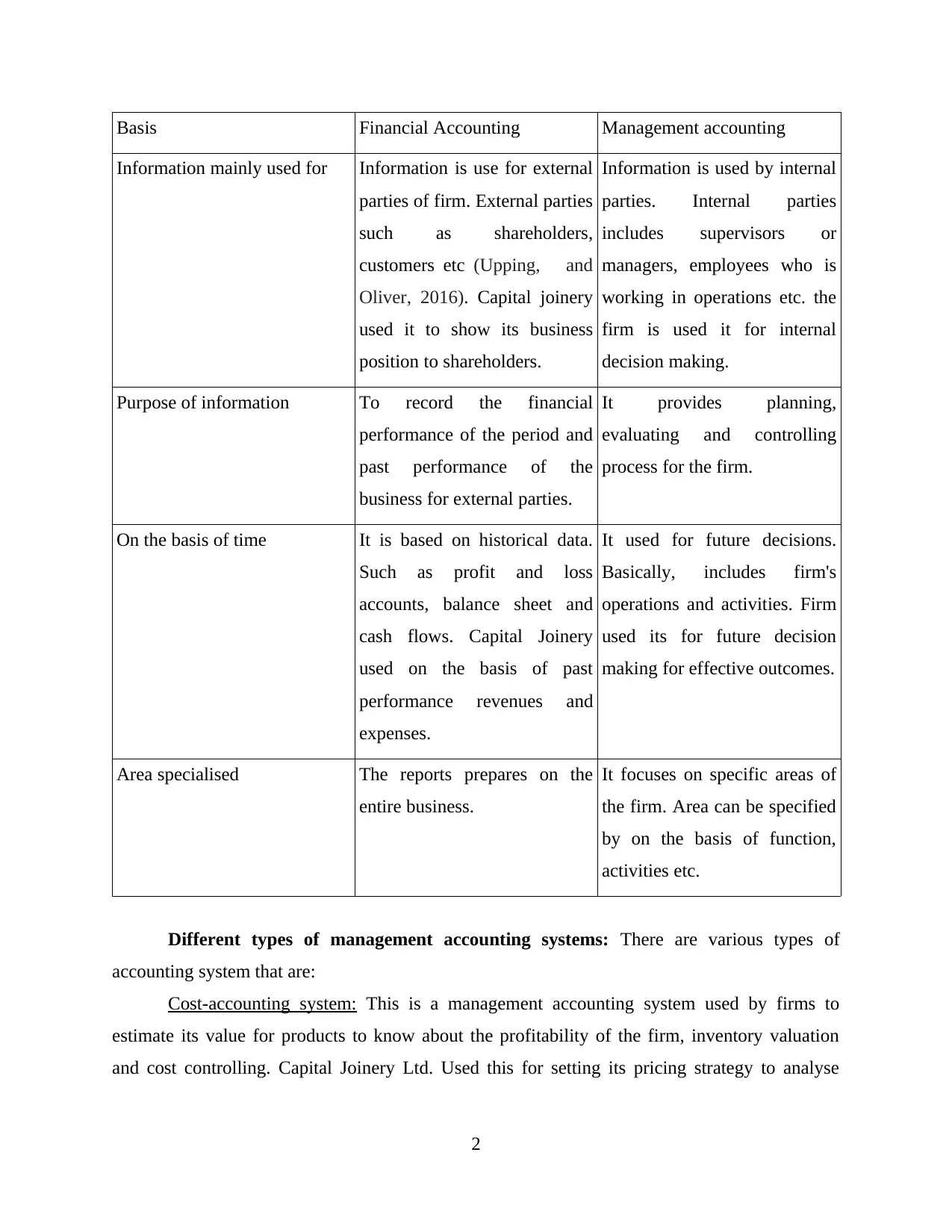

Information mainly used for Information is use for external

parties of firm. External parties

such as shareholders,

customers etc (Upping, and

Oliver, 2016). Capital joinery

used it to show its business

position to shareholders.

Information is used by internal

parties. Internal parties

includes supervisors or

managers, employees who is

working in operations etc. the

firm is used it for internal

decision making.

Purpose of information To record the financial

performance of the period and

past performance of the

business for external parties.

It provides planning,

evaluating and controlling

process for the firm.

On the basis of time It is based on historical data.

Such as profit and loss

accounts, balance sheet and

cash flows. Capital Joinery

used on the basis of past

performance revenues and

expenses.

It used for future decisions.

Basically, includes firm's

operations and activities. Firm

used its for future decision

making for effective outcomes.

Area specialised The reports prepares on the

entire business.

It focuses on specific areas of

the firm. Area can be specified

by on the basis of function,

activities etc.

Different types of management accounting systems: There are various types of

accounting system that are:

Cost-accounting system: This is a management accounting system used by firms to

estimate its value for products to know about the profitability of the firm, inventory valuation

and cost controlling. Capital Joinery Ltd. Used this for setting its pricing strategy to analyse

2

Information mainly used for Information is use for external

parties of firm. External parties

such as shareholders,

customers etc (Upping, and

Oliver, 2016). Capital joinery

used it to show its business

position to shareholders.

Information is used by internal

parties. Internal parties

includes supervisors or

managers, employees who is

working in operations etc. the

firm is used it for internal

decision making.

Purpose of information To record the financial

performance of the period and

past performance of the

business for external parties.

It provides planning,

evaluating and controlling

process for the firm.

On the basis of time It is based on historical data.

Such as profit and loss

accounts, balance sheet and

cash flows. Capital Joinery

used on the basis of past

performance revenues and

expenses.

It used for future decisions.

Basically, includes firm's

operations and activities. Firm

used its for future decision

making for effective outcomes.

Area specialised The reports prepares on the

entire business.

It focuses on specific areas of

the firm. Area can be specified

by on the basis of function,

activities etc.

Different types of management accounting systems: There are various types of

accounting system that are:

Cost-accounting system: This is a management accounting system used by firms to

estimate its value for products to know about the profitability of the firm, inventory valuation

and cost controlling. Capital Joinery Ltd. Used this for setting its pricing strategy to analyse

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profitability of firm. It is helpful to identify where the firm is spending its money and from where

it earn. It leads to analyse and report for improvement of internal cost control and efficiency.

Essential requirements: For the cost accounting system the actual costs occurs by the

different manufacturing activities are required. The information is requires for managers and

operational level employees in order to short term and long term decision-making.

Inventory management system: This is a system for tracking inventory levels, sales and

orders. In Capital Joinery Ltd., the firm used in it's production sector for create a work order and

analysis of raw material requirement. It helps firm for knowing its position regarding inventory

so that it helps its producers to know about the orders.

Essential requirements: This requires for stock level information such as sales orders,

storage costs etc. The managers and higher authorities are required for it in order to maintaining

costs of production for setting prices. It helps organisations for maintaining its cots for higher

probability.

Job-costing system: Job costing is refers to analysis of procedure of company where job

is different and performed according to consumers demand (Wahyuni and Triatmanto, 2020).

The firm is used this system for analysing firm's operations according to consumers demand so

that it can control it by time. In context to Capital Joinery firm used it for analyse its procedure

according to users wants.

Essential requirements: It is required information such as how consumers demand

affects by firms pricing strategy. It is required by higher level authorities for managing firms

operations and sales. It helps organisation by setting prices in such manner so that it can satisfied

customers and helps to maintain firms probability.

Price-optimising system: This is a customer oriented system that utilization of

mathematical process to know different prices firm's products and services through various

channels. Capital Joinery used this system to know customers willingness to pay for its products

or services. It helps firm to set optimum price for its products or service so that it can achieve its

objective and maximize its profits.

Essential requirements: Firm collecting information related to the costs involves in its

goods and services. It is required by higher authorities for short term and long term decision

making. It helps it to managing profits and controlling higher expensive activities.

3

it earn. It leads to analyse and report for improvement of internal cost control and efficiency.

Essential requirements: For the cost accounting system the actual costs occurs by the

different manufacturing activities are required. The information is requires for managers and

operational level employees in order to short term and long term decision-making.

Inventory management system: This is a system for tracking inventory levels, sales and

orders. In Capital Joinery Ltd., the firm used in it's production sector for create a work order and

analysis of raw material requirement. It helps firm for knowing its position regarding inventory

so that it helps its producers to know about the orders.

Essential requirements: This requires for stock level information such as sales orders,

storage costs etc. The managers and higher authorities are required for it in order to maintaining

costs of production for setting prices. It helps organisations for maintaining its cots for higher

probability.

Job-costing system: Job costing is refers to analysis of procedure of company where job

is different and performed according to consumers demand (Wahyuni and Triatmanto, 2020).

The firm is used this system for analysing firm's operations according to consumers demand so

that it can control it by time. In context to Capital Joinery firm used it for analyse its procedure

according to users wants.

Essential requirements: It is required information such as how consumers demand

affects by firms pricing strategy. It is required by higher level authorities for managing firms

operations and sales. It helps organisation by setting prices in such manner so that it can satisfied

customers and helps to maintain firms probability.

Price-optimising system: This is a customer oriented system that utilization of

mathematical process to know different prices firm's products and services through various

channels. Capital Joinery used this system to know customers willingness to pay for its products

or services. It helps firm to set optimum price for its products or service so that it can achieve its

objective and maximize its profits.

Essential requirements: Firm collecting information related to the costs involves in its

goods and services. It is required by higher authorities for short term and long term decision

making. It helps it to managing profits and controlling higher expensive activities.

3

P2: Different methods for management accounting reporting:

Management Accounting Reports: It compiles information gained through financial

accounting of business. It is used to identify, measure, analyse, interpret and communicate

financial status of an organization to its manager. Motive of preparing such reports is to achieve

organization's set goals (Speckbacher, 2017). It can be done by assessing and informing

company's decision makers which will ultimately guide them is preparing efficient plans for

business operations. Different types of management accounting reports and importance of

preparing these reports for Capital Joinery Ltd. are discussed below:

Budgetary report: It is prepared to analyse how business manages its funding. It is an

estimation of revenues and expenditure of business. Capital Joinery Ltd. Should prepare this

report to investigate whether its estimated financial projections match with its actual

performance. By analysis such reports company can keep track of its expenditures which will

encourage business managers to increase savings which can be further utilised for firm's

expansion plan.

Inventory management report: This report is composed to examine about inventory stock

of business. Firm should prepare it to monitor its inventory status on regular basis. It prevents

any kind of stock outs, ensures management of safety stocks, and encourages record keeping and

results in on-time ordering of stock. It will also reduce extra maintenance expenses that firm will

bear on ordering more than required inventory.

Performance management report: Progress of employees of organization is reported and

measured by formulating this report. It is a worthwhile report which Capital Joinery Ltd. should

prepare to keep track of performance of their workforce (Imionescu and Bica, 2016). It will

ensure aligning of their performance with strategic goals of organization to increase profitability

and smooth functioning. Key improvement areas can also be identified by composing such

reports.

Account receivable report: It contains record of receivables of business. Capital Joinery

Ltd. Can prepare this report to ensure that debtors had paid their invoices on time. This will

reduce probability of bad debts. It will also verify smooth cash flow in firm to avoid hinders in

business operations.

4

Management Accounting Reports: It compiles information gained through financial

accounting of business. It is used to identify, measure, analyse, interpret and communicate

financial status of an organization to its manager. Motive of preparing such reports is to achieve

organization's set goals (Speckbacher, 2017). It can be done by assessing and informing

company's decision makers which will ultimately guide them is preparing efficient plans for

business operations. Different types of management accounting reports and importance of

preparing these reports for Capital Joinery Ltd. are discussed below:

Budgetary report: It is prepared to analyse how business manages its funding. It is an

estimation of revenues and expenditure of business. Capital Joinery Ltd. Should prepare this

report to investigate whether its estimated financial projections match with its actual

performance. By analysis such reports company can keep track of its expenditures which will

encourage business managers to increase savings which can be further utilised for firm's

expansion plan.

Inventory management report: This report is composed to examine about inventory stock

of business. Firm should prepare it to monitor its inventory status on regular basis. It prevents

any kind of stock outs, ensures management of safety stocks, and encourages record keeping and

results in on-time ordering of stock. It will also reduce extra maintenance expenses that firm will

bear on ordering more than required inventory.

Performance management report: Progress of employees of organization is reported and

measured by formulating this report. It is a worthwhile report which Capital Joinery Ltd. should

prepare to keep track of performance of their workforce (Imionescu and Bica, 2016). It will

ensure aligning of their performance with strategic goals of organization to increase profitability

and smooth functioning. Key improvement areas can also be identified by composing such

reports.

Account receivable report: It contains record of receivables of business. Capital Joinery

Ltd. Can prepare this report to ensure that debtors had paid their invoices on time. This will

reduce probability of bad debts. It will also verify smooth cash flow in firm to avoid hinders in

business operations.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M1: Benefits of management accounting system and their application within an organisation:

It is a process of providing financial resources or data to manager for decision making. It

is generally conduct by internally team, in this statistical data is used for a better decision. In the

Capital joinery limited, this system helps in increase efficiency of the firm by better operation

and compare the performance with their competitor (Schaltegger, 2018). Company can

maximise their profitability. Apart from these manager simplify the financial statement for

taking managerial decision. It also help in controlling the cash flow so that there is no misuse of

money is done. Through this organization run effectively in a productive manner.

D1: How management accounting system and management accounting reports are integrated

within an organisation:

Management accounting systems and reports are used in an organization to keep track

about financial status of business (Posch, 2017). It will provide key insights to managers which

will enhance their decision making and efficient functioning of Capital Joinery Ltd.'s business

operations.

TASK 2

P3: Techniques of cost analysis to prepare an income statement:

Cost: Monitory value of business expenses or spendings on production and selling of its

products and services is termed as 'cost'. It can be categorized in mainly three types which are

described below:

Variable cost: These costs are effected by the change in level of output in production. In

context to Capital Joinery Ltd., these are the variable costs incurred- cost of raw materials

purchased for producing windows, stairs, and doors or wages of labour employed in business,

etc.

Fixed cost: These costs have no effect of output level of firm. It includes, cost of

machinery and equipment purchased, land or building cost etc.

Semi variable cost: It consists components of both fixed and variable costs. These costs

fixed till certain level of production and becomes variable when it exceeds. For example,

commissions.

Cost analysis: Categorizing, studying and analysing cost incurred in business is defined

as 'cost analysis (ewo, Ajibolade and Obazee, 2019)'.

5

It is a process of providing financial resources or data to manager for decision making. It

is generally conduct by internally team, in this statistical data is used for a better decision. In the

Capital joinery limited, this system helps in increase efficiency of the firm by better operation

and compare the performance with their competitor (Schaltegger, 2018). Company can

maximise their profitability. Apart from these manager simplify the financial statement for

taking managerial decision. It also help in controlling the cash flow so that there is no misuse of

money is done. Through this organization run effectively in a productive manner.

D1: How management accounting system and management accounting reports are integrated

within an organisation:

Management accounting systems and reports are used in an organization to keep track

about financial status of business (Posch, 2017). It will provide key insights to managers which

will enhance their decision making and efficient functioning of Capital Joinery Ltd.'s business

operations.

TASK 2

P3: Techniques of cost analysis to prepare an income statement:

Cost: Monitory value of business expenses or spendings on production and selling of its

products and services is termed as 'cost'. It can be categorized in mainly three types which are

described below:

Variable cost: These costs are effected by the change in level of output in production. In

context to Capital Joinery Ltd., these are the variable costs incurred- cost of raw materials

purchased for producing windows, stairs, and doors or wages of labour employed in business,

etc.

Fixed cost: These costs have no effect of output level of firm. It includes, cost of

machinery and equipment purchased, land or building cost etc.

Semi variable cost: It consists components of both fixed and variable costs. These costs

fixed till certain level of production and becomes variable when it exceeds. For example,

commissions.

Cost analysis: Categorizing, studying and analysing cost incurred in business is defined

as 'cost analysis (ewo, Ajibolade and Obazee, 2019)'.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost volume profit: it evaluates impact of volume and cost on operating profit of Capital

Joinery Ltd.

Flexible budgeting: On current level of output when revenue and expenditure of

business is forecasted, it is defined as 'flexible budgeting'.

Cost variances: It is difference between actual and estimated cost of an organization.

Absorption and marginal costing: Marginal cost indicates cost per additional unit of

production. It is a variable cost. On the contrary absorption cost is a total cost that involves both

fixed and variable cost.

Inventory cost: It refers to overall cost of products and services, not only the cost of

manufacturing but also refers to cost of keeping goods such as warehouse cost and maintaining

cost. It includes price from the manufacturing to delivered to customers. Inventory cost can be

divide into three parts such as order cost, carrying cost and shortage cost. Capital joinery used

this to recover its all over cost and maximise its profits ( Ojua, 2016).

Ordering costs: This cost refers to paying cost by customer that involves order cost,

delivery product cost and stock inventory. Capital joinery splits inventory into two parts:

The cost of ordering process itself: It involves the cost of producing products as fixed

cost and independent of the number of unit cost.

The inbound logistics costs: The cost is related to transportation and delivery of the

product that is variable in nature.

Carrying costs: Carrying cost of inventory is refers keeping cost or holding cost of

products in the warehouse. It includes warehouse cost such as rent, wages, opportunity cost,

insurance etc.

Shortage costs: It refers that cost that are occurs when a firm runs out of stock. In Capital

joinery firm faces this problem in reference to less stock availability in order to customers

demand. In this situation customers place orders but firm has not sufficient stock in their

warehouse or procedure.

Reducing in inventory cost leads to cost benefits to firm and probability maximisation of

the firm. Although it affects the pricing strategy of the firm (uhu and 2017). It helps in reducing

waste, improve supply chain management, demand forecasting, shorten the product life cycle or

distribution channel. It helps firm to maintain its warehousing cost and transportation cost. In

6

Joinery Ltd.

Flexible budgeting: On current level of output when revenue and expenditure of

business is forecasted, it is defined as 'flexible budgeting'.

Cost variances: It is difference between actual and estimated cost of an organization.

Absorption and marginal costing: Marginal cost indicates cost per additional unit of

production. It is a variable cost. On the contrary absorption cost is a total cost that involves both

fixed and variable cost.

Inventory cost: It refers to overall cost of products and services, not only the cost of

manufacturing but also refers to cost of keeping goods such as warehouse cost and maintaining

cost. It includes price from the manufacturing to delivered to customers. Inventory cost can be

divide into three parts such as order cost, carrying cost and shortage cost. Capital joinery used

this to recover its all over cost and maximise its profits ( Ojua, 2016).

Ordering costs: This cost refers to paying cost by customer that involves order cost,

delivery product cost and stock inventory. Capital joinery splits inventory into two parts:

The cost of ordering process itself: It involves the cost of producing products as fixed

cost and independent of the number of unit cost.

The inbound logistics costs: The cost is related to transportation and delivery of the

product that is variable in nature.

Carrying costs: Carrying cost of inventory is refers keeping cost or holding cost of

products in the warehouse. It includes warehouse cost such as rent, wages, opportunity cost,

insurance etc.

Shortage costs: It refers that cost that are occurs when a firm runs out of stock. In Capital

joinery firm faces this problem in reference to less stock availability in order to customers

demand. In this situation customers place orders but firm has not sufficient stock in their

warehouse or procedure.

Reducing in inventory cost leads to cost benefits to firm and probability maximisation of

the firm. Although it affects the pricing strategy of the firm (uhu and 2017). It helps in reducing

waste, improve supply chain management, demand forecasting, shorten the product life cycle or

distribution channel. It helps firm to maintain its warehousing cost and transportation cost. In

6

context to Capital joinery Ltd. Reducing inventory cost will help firm for cost benefits and

maximising its profits.

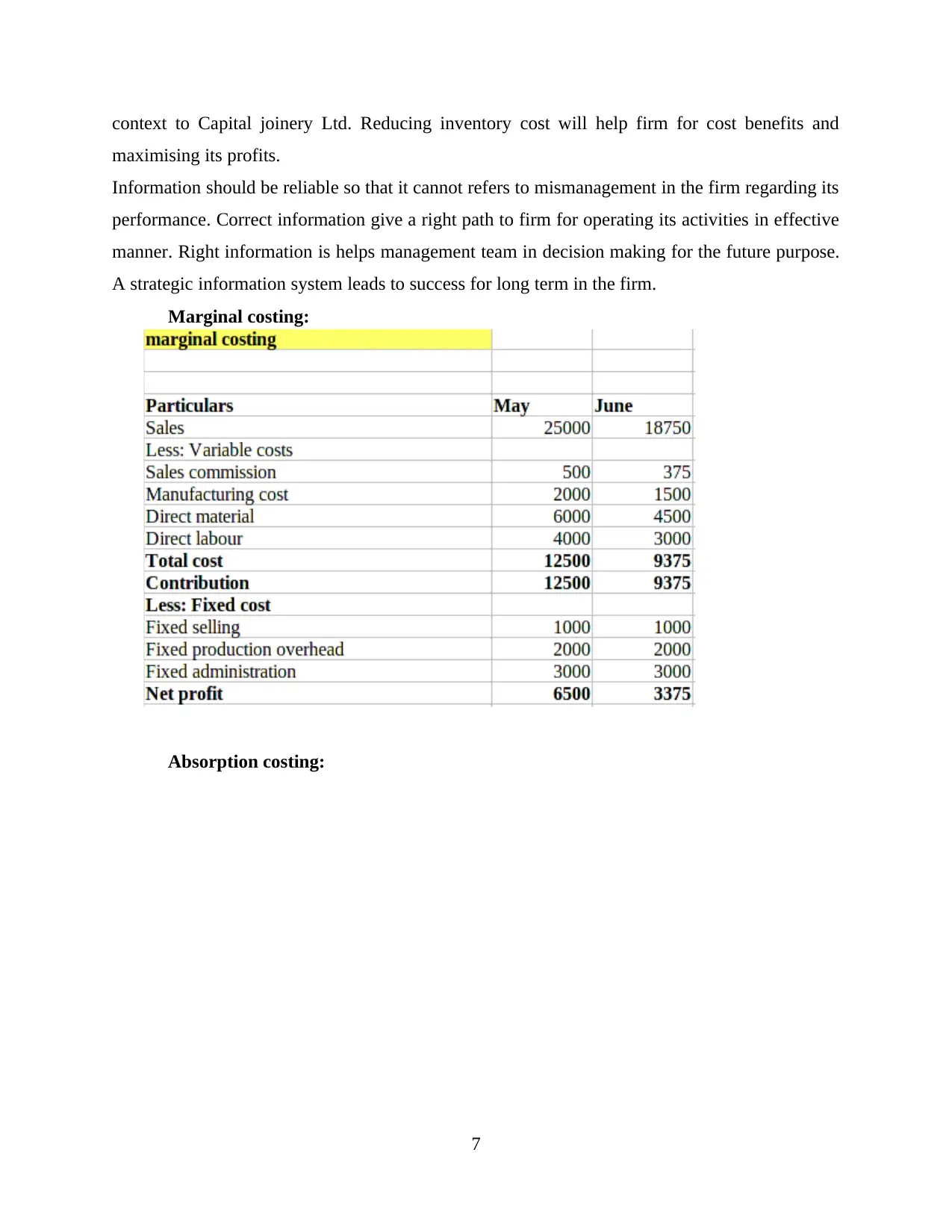

Information should be reliable so that it cannot refers to mismanagement in the firm regarding its

performance. Correct information give a right path to firm for operating its activities in effective

manner. Right information is helps management team in decision making for the future purpose.

A strategic information system leads to success for long term in the firm.

Marginal costing:

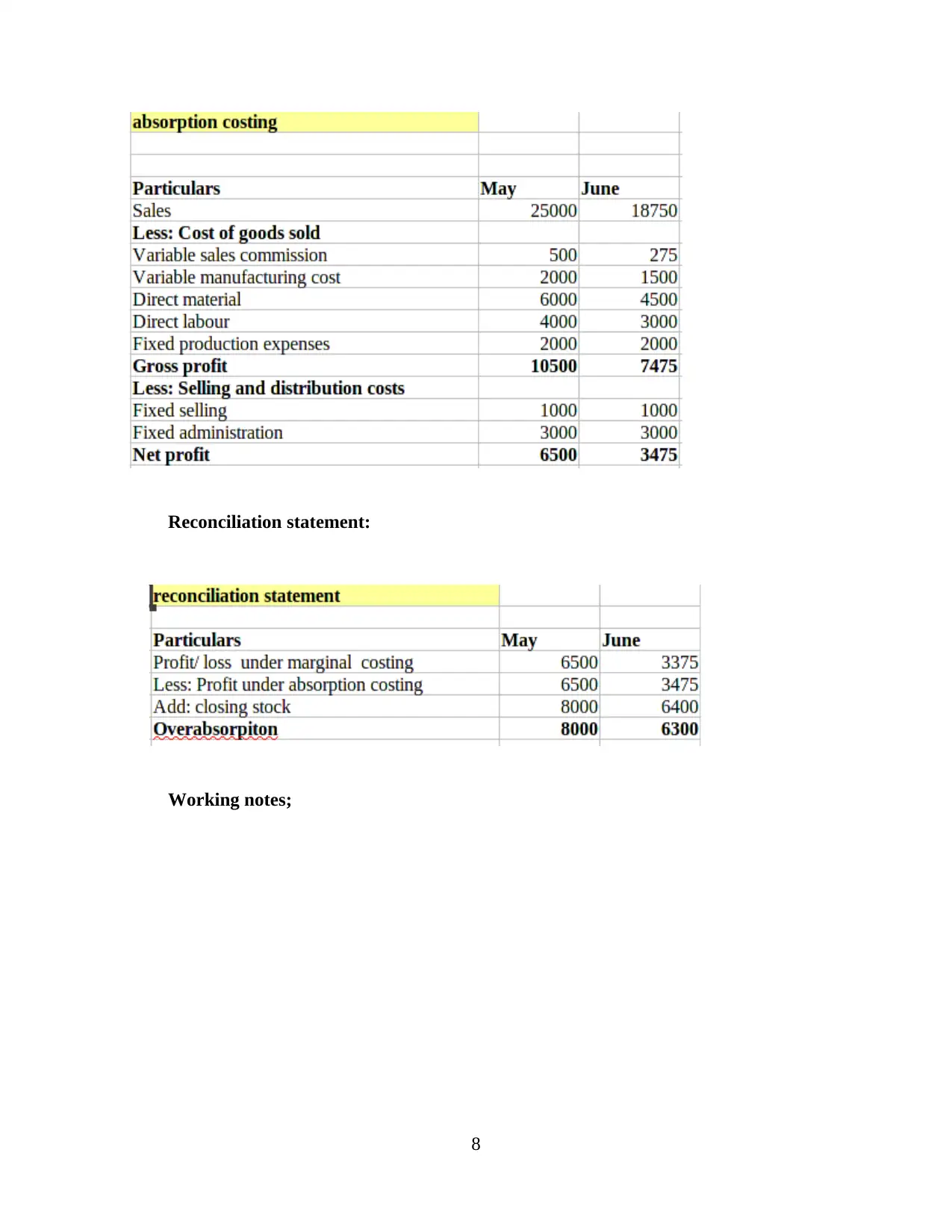

Absorption costing:

7

maximising its profits.

Information should be reliable so that it cannot refers to mismanagement in the firm regarding its

performance. Correct information give a right path to firm for operating its activities in effective

manner. Right information is helps management team in decision making for the future purpose.

A strategic information system leads to success for long term in the firm.

Marginal costing:

Absorption costing:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reconciliation statement:

Working notes;

8

Working notes;

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

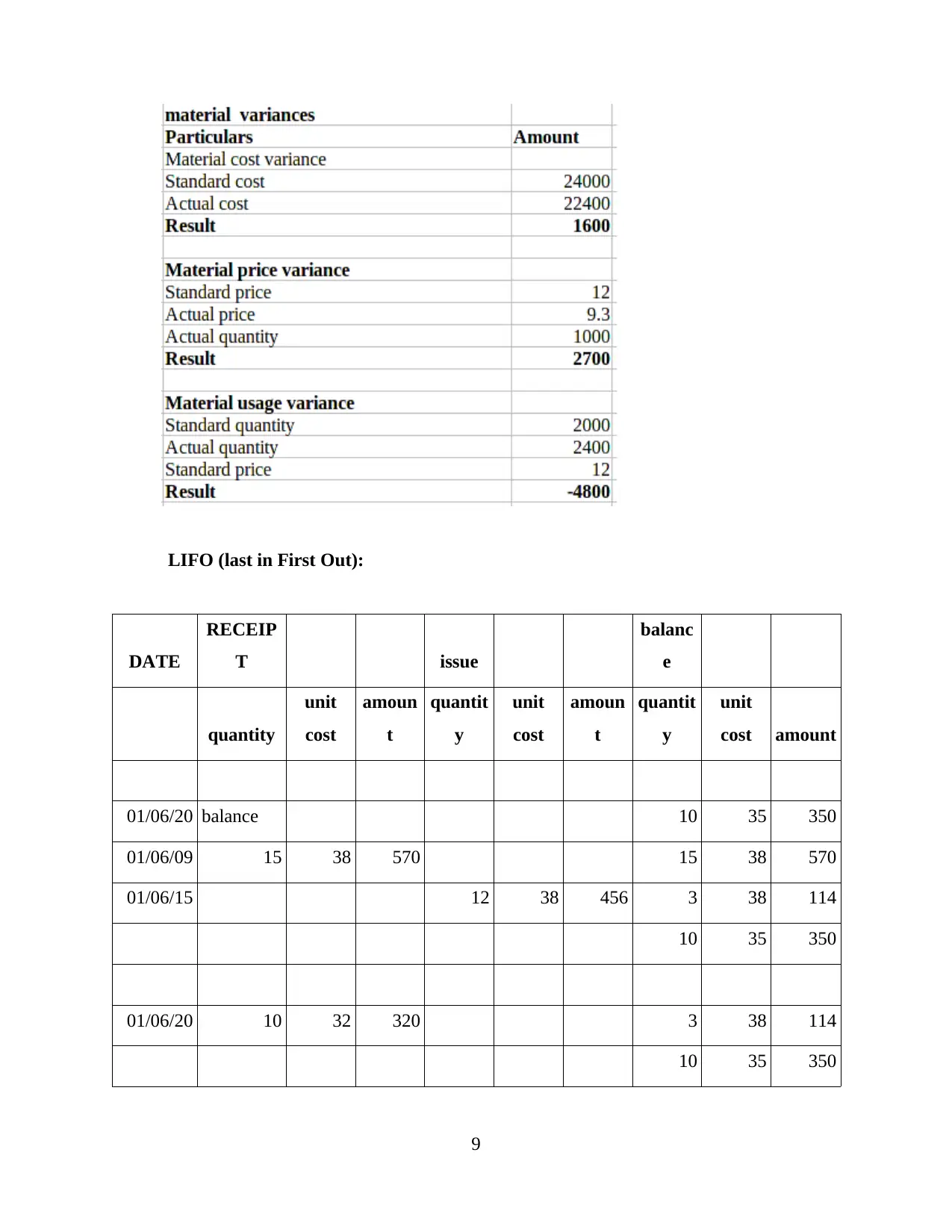

LIFO (last in First Out):

DATE

RECEIP

T issue

balanc

e

quantity

unit

cost

amoun

t

quantit

y

unit

cost

amoun

t

quantit

y

unit

cost amount

01/06/20 balance 10 35 350

01/06/09 15 38 570 15 38 570

01/06/15 12 38 456 3 38 114

10 35 350

01/06/20 10 32 320 3 38 114

10 35 350

9

DATE

RECEIP

T issue

balanc

e

quantity

unit

cost

amoun

t

quantit

y

unit

cost

amoun

t

quantit

y

unit

cost amount

01/06/20 balance 10 35 350

01/06/09 15 38 570 15 38 570

01/06/15 12 38 456 3 38 114

10 35 350

01/06/20 10 32 320 3 38 114

10 35 350

9

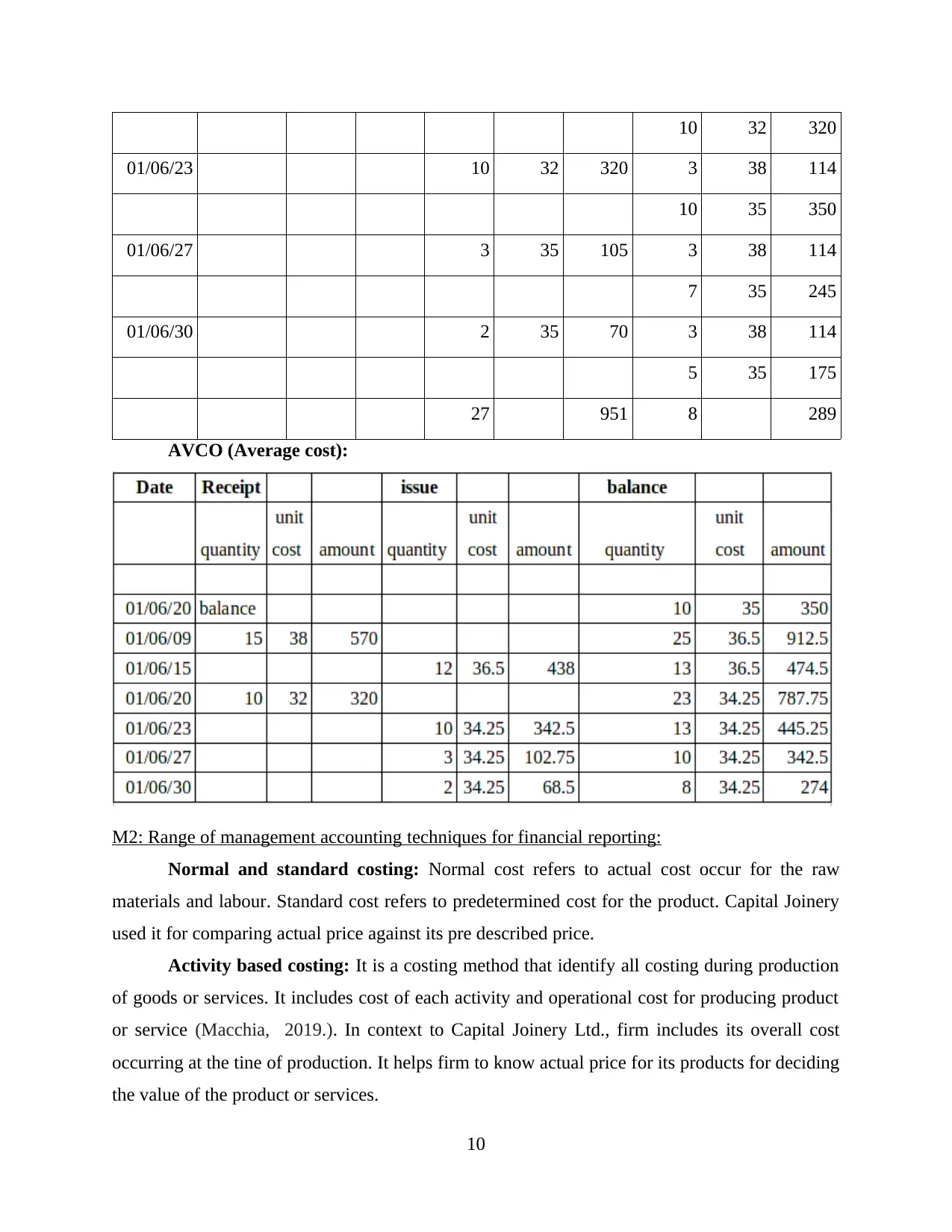

10 32 320

01/06/23 10 32 320 3 38 114

10 35 350

01/06/27 3 35 105 3 38 114

7 35 245

01/06/30 2 35 70 3 38 114

5 35 175

27 951 8 289

AVCO (Average cost):

M2: Range of management accounting techniques for financial reporting:

Normal and standard costing: Normal cost refers to actual cost occur for the raw

materials and labour. Standard cost refers to predetermined cost for the product. Capital Joinery

used it for comparing actual price against its pre described price.

Activity based costing: It is a costing method that identify all costing during production

of goods or services. It includes cost of each activity and operational cost for producing product

or service (Macchia, 2019.). In context to Capital Joinery Ltd., firm includes its overall cost

occurring at the tine of production. It helps firm to know actual price for its products for deciding

the value of the product or services.

10

01/06/23 10 32 320 3 38 114

10 35 350

01/06/27 3 35 105 3 38 114

7 35 245

01/06/30 2 35 70 3 38 114

5 35 175

27 951 8 289

AVCO (Average cost):

M2: Range of management accounting techniques for financial reporting:

Normal and standard costing: Normal cost refers to actual cost occur for the raw

materials and labour. Standard cost refers to predetermined cost for the product. Capital Joinery

used it for comparing actual price against its pre described price.

Activity based costing: It is a costing method that identify all costing during production

of goods or services. It includes cost of each activity and operational cost for producing product

or service (Macchia, 2019.). In context to Capital Joinery Ltd., firm includes its overall cost

occurring at the tine of production. It helps firm to know actual price for its products for deciding

the value of the product or services.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.