Management Accounting for Financial Problem Solving at NERO Ltd

VerifiedAdded on 2020/06/06

|17

|4900

|56

Report

AI Summary

This report delves into the core concepts of management accounting, exploring various systems, costing approaches, and budgetary control methods. It begins by defining management accounting and its different types, such as job costing and cost accounting systems. The report then examines methods used in management accounting reports, including accounts receivable alignment, job cost reports, and performance reports, all crucial for informed decision-making. A key section focuses on cost analysis techniques, comparing absorption costing and marginal costing through detailed calculations and income statements for NERO Ltd. Furthermore, the report evaluates the benefits of management accounting systems and assesses the impact of these systems and reporting within organizational processes. Finally, it explores planning tools for budgetary control and how organizations like NERO Ltd can leverage management accounting to address financial challenges and achieve success.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Define management accounting and different type of management accounting system.......1

P2 Explain various methods used for management accounting report.......................................3

M 1 Benefits of management accounting system and their application .....................................4

D1 Evaluate management accounting systems and reporting within organisational process ...4

TASK 2............................................................................................................................................4

P3 Calculate costs using techniques of cost analysis to prepare an income statement...............4

M 2 Range of management accounting techniques and produce financial report .....................8

D 2 Planning tools for accounting in respond to solving financial problems lead to success . . .8

TASK 3............................................................................................................................................8

P4 Explain the pros and cons of various kinds of planning tools used for budgetary control ...8

M 3 Examine use of various planning tools and their prepared application for budget ..........10

TASK 4..........................................................................................................................................10

P5 Organisations adopting management accounting system to respond financial problems....10

M 4 Respond to financial problem, accounting can lead organisation to success ...................12

CONCLUSION .............................................................................................................................12

.......................................................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Define management accounting and different type of management accounting system.......1

P2 Explain various methods used for management accounting report.......................................3

M 1 Benefits of management accounting system and their application .....................................4

D1 Evaluate management accounting systems and reporting within organisational process ...4

TASK 2............................................................................................................................................4

P3 Calculate costs using techniques of cost analysis to prepare an income statement...............4

M 2 Range of management accounting techniques and produce financial report .....................8

D 2 Planning tools for accounting in respond to solving financial problems lead to success . . .8

TASK 3............................................................................................................................................8

P4 Explain the pros and cons of various kinds of planning tools used for budgetary control ...8

M 3 Examine use of various planning tools and their prepared application for budget ..........10

TASK 4..........................................................................................................................................10

P5 Organisations adopting management accounting system to respond financial problems....10

M 4 Respond to financial problem, accounting can lead organisation to success ...................12

CONCLUSION .............................................................................................................................12

.......................................................................................................................................................12

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In the enterprises there are various objectives which is set by the organization and they

have to be attain all of them in order to meet the goals and target. There are several procedure

which will be interpreted such as measurement, identification, analysation of respective data,

interpretation and many more. There are more structured data which will be gathered with the

support of several tools (Macintosh and Quattrone, 2010). So through that they can use and help

to the management in the process of decision making. This assignment is going to present

various system, costing approaches and budgetary control along with appropriate understanding.

TASK 1

P1 Define management accounting and different type of management accounting system

Basically, management accounting is one of the important system it includes taxation

accounting, financial, managerial and internal auditing of company (Management accounting,

2017). This method can be used for identifying and collecting actual and reliable information

about organisation. It helps to take corrective and appropriate decision in the context of

enterprise. Management accounting has several objectives, which can explain such as:

It helps in interpretation of financial information and data

It aids in controlling and managing performance of organisation

It can be used for solving strategic business problems in effective and efficient manner.

Additionally, different type of management accounting system can be used for identify

issues and gathering actual information such as follows:

Job costing: A job costing system can be known as a process of collecting information

about costs within specific job task and production (Baldvinsdottir, Mitchell and

Nørreklit, 2010). Additionally, gathered data can be used to submit cost information to

customers while preparing a contract. This system can be accumulate different type of

informations such as follows:

1. Direct material

2. Direct labour

3. Overhead costs

Cost accounting system: This system can also known as product costing system it can be

used by every organisation to estimate and identify cost and charges of products and

1

In the enterprises there are various objectives which is set by the organization and they

have to be attain all of them in order to meet the goals and target. There are several procedure

which will be interpreted such as measurement, identification, analysation of respective data,

interpretation and many more. There are more structured data which will be gathered with the

support of several tools (Macintosh and Quattrone, 2010). So through that they can use and help

to the management in the process of decision making. This assignment is going to present

various system, costing approaches and budgetary control along with appropriate understanding.

TASK 1

P1 Define management accounting and different type of management accounting system

Basically, management accounting is one of the important system it includes taxation

accounting, financial, managerial and internal auditing of company (Management accounting,

2017). This method can be used for identifying and collecting actual and reliable information

about organisation. It helps to take corrective and appropriate decision in the context of

enterprise. Management accounting has several objectives, which can explain such as:

It helps in interpretation of financial information and data

It aids in controlling and managing performance of organisation

It can be used for solving strategic business problems in effective and efficient manner.

Additionally, different type of management accounting system can be used for identify

issues and gathering actual information such as follows:

Job costing: A job costing system can be known as a process of collecting information

about costs within specific job task and production (Baldvinsdottir, Mitchell and

Nørreklit, 2010). Additionally, gathered data can be used to submit cost information to

customers while preparing a contract. This system can be accumulate different type of

informations such as follows:

1. Direct material

2. Direct labour

3. Overhead costs

Cost accounting system: This system can also known as product costing system it can be

used by every organisation to estimate and identify cost and charges of products and

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

goods for profitability evaluation, cost management and so more. In the context of this

system, cost allocation of company's services and products which is based on traditional

costing system. With the help of this, effectively will set and allocate cost of services as

well as will take corrective decision. Basically, there are two type of cost accounting

system such as:

1. Job order costing

2. Process costing

Inventory management system: Basically, inventory shows a company's stock level of

products, goods, material and so more. With the help of inventory management system

can easy to identify and determine actual position or status of company's stock. Inventory

can be used while working in a company, in a production process of products and

services sold to customers as per their requirements. Apart from this, inventory

management system considered the use of software, barcode printers, scanner,

techniques, mobile systems and so more (Lukka and Modell, 2010). It helps to manage

and control inventory of company in a appropriate manner. Therefore, inventory

management system has several functions such as:

1. Prepare effective purchases orders

2. Received, managed, relocate, control, adjust inventory of the company

3. Develop appropriate sales orders

4. Pick, pack and shipped at right place and on right time.

Price optimization: Mainly this system is a mathematical tool or technique it helps to

calculate, how demand can changed at different level of product's price. After that, on the

basis of collected information company can manage cost and inventory in effective

manner due to organisation's profit level will improve. Furthermore, in this system three

factors are included such as:

1. Pricing strategies and methods

2. Value of goods to both buyer and seller

3. Approaches that manage and control all contents which impacting on company's

profitability.

2

system, cost allocation of company's services and products which is based on traditional

costing system. With the help of this, effectively will set and allocate cost of services as

well as will take corrective decision. Basically, there are two type of cost accounting

system such as:

1. Job order costing

2. Process costing

Inventory management system: Basically, inventory shows a company's stock level of

products, goods, material and so more. With the help of inventory management system

can easy to identify and determine actual position or status of company's stock. Inventory

can be used while working in a company, in a production process of products and

services sold to customers as per their requirements. Apart from this, inventory

management system considered the use of software, barcode printers, scanner,

techniques, mobile systems and so more (Lukka and Modell, 2010). It helps to manage

and control inventory of company in a appropriate manner. Therefore, inventory

management system has several functions such as:

1. Prepare effective purchases orders

2. Received, managed, relocate, control, adjust inventory of the company

3. Develop appropriate sales orders

4. Pick, pack and shipped at right place and on right time.

Price optimization: Mainly this system is a mathematical tool or technique it helps to

calculate, how demand can changed at different level of product's price. After that, on the

basis of collected information company can manage cost and inventory in effective

manner due to organisation's profit level will improve. Furthermore, in this system three

factors are included such as:

1. Pricing strategies and methods

2. Value of goods to both buyer and seller

3. Approaches that manage and control all contents which impacting on company's

profitability.

2

P2 Explain various methods used for management accounting report

Management accounting report refers to, it is a final part of collected information also it

can be known as a final picture of organisation which represent how business is performing and

operating their work. In every organisation it is necessary to be produced accounting report on

the quarterly basis, because with the help of this effectively will analyse and evaluate the actual

financial status or position of NERO Ltd company (Parker, 2012).

Apart from this, there are different type of reports that helps for protecting a business

firm in effective and efficient manner. Therefore, management accounting report helps in

decision making, planning and performance management system. With the help of company's

accounting statement, will significantly identify the actual position and status of firm also can

determine financial strength of organisation. Basically, there are different type of management

accounting reports but their working style and system different from each other. Due to, NERO

Ltd. can use various methods for preparing report in systematic manner such as follows: Accounts receivable align report: Basically, this report is co-related with credit offers

which is provided by the company to customers. This report can be known as a perfect

overview of credit balance of the organisation which is categorised as per the age of

consumers. Apart from this, accounting receivable align report aids to maintain and

control credit polices of organisation in effective and efficient manner. Job cost report: This report provide a overview of total cost which is accrued in a signal

project. With the help of this, systematically analyse and compare with actual cost to

expected revenue of project. This report helps to company because while using this

statement effectively determine and evaluate actual profitability level of specific job. In

this addition, with the help of this report will identify which types of jobs are profitable

for organisation (Renz, 2016).

Inventory and manufacturing report: Some companies are provides physical products

and goods to customers as per their requirements. But specially those products and

services are manufacturing with low fault tolerance, their a effective report or statement

is valuable for company. Because it helps to centralised the data and information, which

is related to inventory cost, labour and other things. All these contents are included in

manufacturing process of products. With the help of this report, company can manage

3

Management accounting report refers to, it is a final part of collected information also it

can be known as a final picture of organisation which represent how business is performing and

operating their work. In every organisation it is necessary to be produced accounting report on

the quarterly basis, because with the help of this effectively will analyse and evaluate the actual

financial status or position of NERO Ltd company (Parker, 2012).

Apart from this, there are different type of reports that helps for protecting a business

firm in effective and efficient manner. Therefore, management accounting report helps in

decision making, planning and performance management system. With the help of company's

accounting statement, will significantly identify the actual position and status of firm also can

determine financial strength of organisation. Basically, there are different type of management

accounting reports but their working style and system different from each other. Due to, NERO

Ltd. can use various methods for preparing report in systematic manner such as follows: Accounts receivable align report: Basically, this report is co-related with credit offers

which is provided by the company to customers. This report can be known as a perfect

overview of credit balance of the organisation which is categorised as per the age of

consumers. Apart from this, accounting receivable align report aids to maintain and

control credit polices of organisation in effective and efficient manner. Job cost report: This report provide a overview of total cost which is accrued in a signal

project. With the help of this, systematically analyse and compare with actual cost to

expected revenue of project. This report helps to company because while using this

statement effectively determine and evaluate actual profitability level of specific job. In

this addition, with the help of this report will identify which types of jobs are profitable

for organisation (Renz, 2016).

Inventory and manufacturing report: Some companies are provides physical products

and goods to customers as per their requirements. But specially those products and

services are manufacturing with low fault tolerance, their a effective report or statement

is valuable for company. Because it helps to centralised the data and information, which

is related to inventory cost, labour and other things. All these contents are included in

manufacturing process of products. With the help of this report, company can manage

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and control manufacturing cost of products as well as collect reliable information about

producing products and goods which produced for consumers.

Performance report: Basically, every business firms are using budget for identifying

actual expenditure and revenue of their organisation. On that basis will be prepared a

effective performance report which should be prepared in every year on the basis of

monthly or quarterly. With the help of performance report of company, managers will

make a effective plan for future requirements in manufacturing process in effective and

efficient manner.

M 1 Benefits of management accounting system and their application

There are the several advantages of the Gethsemane accounting which help in developing

their organisational vision and targets by measuring their goals and objectives. It reduces the

costs which is somewhere advantageous for there management accounting. They decrease their

expenditure of there operation of business which is important in accomplishing their economic

resources (Cinquini and Tenucci, 2010).

D1 Evaluate management accounting systems and reporting within organisational process

There is the utilization of the management accounting in the enterprise so they can

accomplish better interpretation of their demands and needs of the customers. There are several

tools which control their operational business which the aid of accounting. The relevant cost

analysis determine their report functional activity which assist to take their relevant cost in

decision in various business operations.

TASK 2

P3 Calculate costs using techniques of cost analysis to prepare an income statement

In the context of cost analysis, NERO Ltd. can be used different type of methods or

techniques such as follows: Absorption costing: This method can be define actual manufacturing cost which

absorbed by units manufactured. As well as, absorption costing approach related to the

cost of finished unity of stock. In includes direct material, direct labour, fixed and

variable manufacturing overheads. In other words, it is method which is related with the

final product cost. With the help of this, effectively analyse and identify actual cost in

producing products, sales, profit and loss of selected organisation. Apart from this, it

4

producing products and goods which produced for consumers.

Performance report: Basically, every business firms are using budget for identifying

actual expenditure and revenue of their organisation. On that basis will be prepared a

effective performance report which should be prepared in every year on the basis of

monthly or quarterly. With the help of performance report of company, managers will

make a effective plan for future requirements in manufacturing process in effective and

efficient manner.

M 1 Benefits of management accounting system and their application

There are the several advantages of the Gethsemane accounting which help in developing

their organisational vision and targets by measuring their goals and objectives. It reduces the

costs which is somewhere advantageous for there management accounting. They decrease their

expenditure of there operation of business which is important in accomplishing their economic

resources (Cinquini and Tenucci, 2010).

D1 Evaluate management accounting systems and reporting within organisational process

There is the utilization of the management accounting in the enterprise so they can

accomplish better interpretation of their demands and needs of the customers. There are several

tools which control their operational business which the aid of accounting. The relevant cost

analysis determine their report functional activity which assist to take their relevant cost in

decision in various business operations.

TASK 2

P3 Calculate costs using techniques of cost analysis to prepare an income statement

In the context of cost analysis, NERO Ltd. can be used different type of methods or

techniques such as follows: Absorption costing: This method can be define actual manufacturing cost which

absorbed by units manufactured. As well as, absorption costing approach related to the

cost of finished unity of stock. In includes direct material, direct labour, fixed and

variable manufacturing overheads. In other words, it is method which is related with the

final product cost. With the help of this, effectively analyse and identify actual cost in

producing products, sales, profit and loss of selected organisation. Apart from this, it

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

helps to define actual financial status or position in effective and efficient manner

(Fullerton, Kennedy and Widener, 2013).

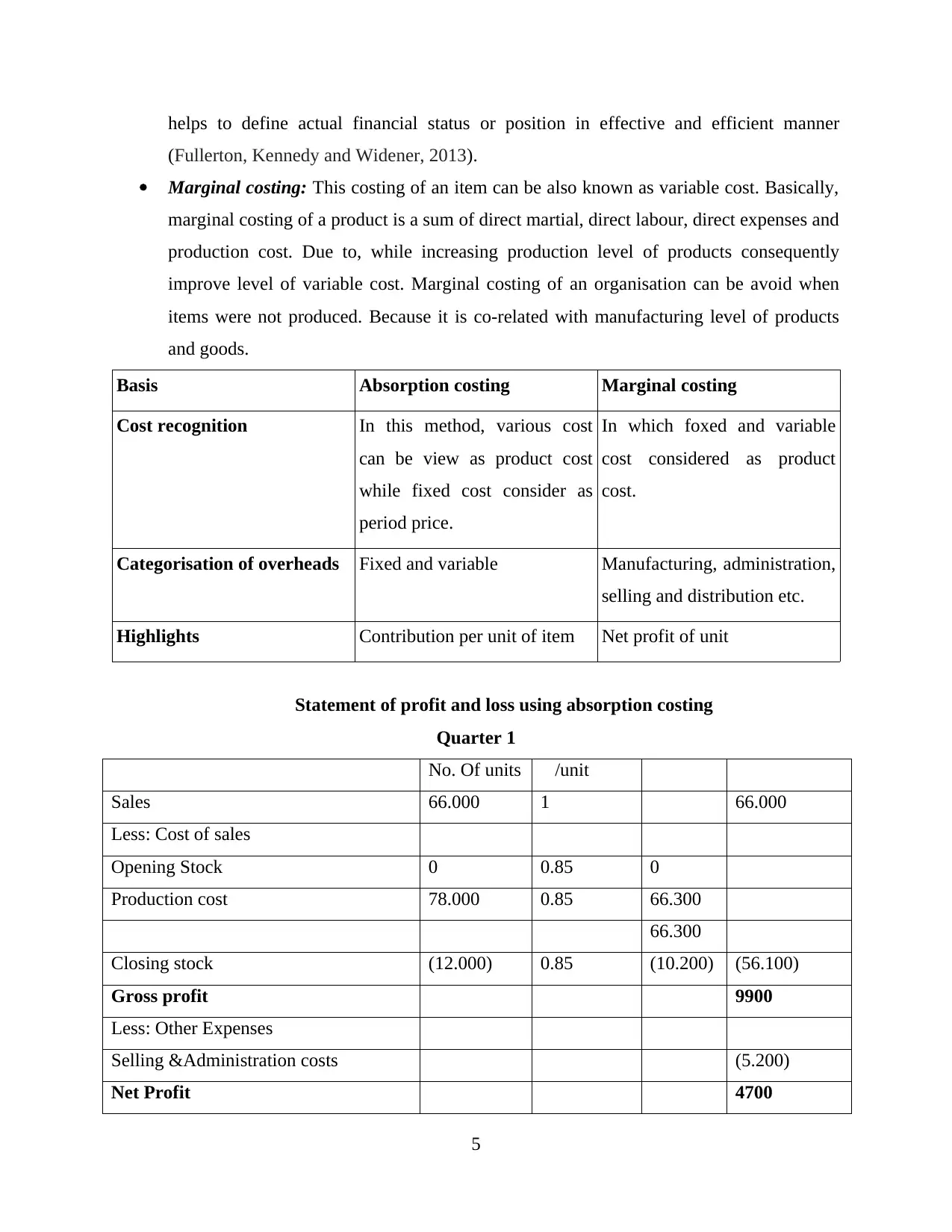

Marginal costing: This costing of an item can be also known as variable cost. Basically,

marginal costing of a product is a sum of direct martial, direct labour, direct expenses and

production cost. Due to, while increasing production level of products consequently

improve level of variable cost. Marginal costing of an organisation can be avoid when

items were not produced. Because it is co-related with manufacturing level of products

and goods.

Basis Absorption costing Marginal costing

Cost recognition In this method, various cost

can be view as product cost

while fixed cost consider as

period price.

In which foxed and variable

cost considered as product

cost.

Categorisation of overheads Fixed and variable Manufacturing, administration,

selling and distribution etc.

Highlights Contribution per unit of item Net profit of unit

Statement of profit and loss using absorption costing

Quarter 1

No. Of units £/unit £ £

Sales 66.000 1 66.000

Less: Cost of sales

Opening Stock 0 0.85 0

Production cost 78.000 0.85 66.300

66.300

Closing stock (12.000) 0.85 (10.200) (56.100)

Gross profit 9900

Less: Other Expenses

Selling &Administration costs (5.200)

Net Profit 4700

5

(Fullerton, Kennedy and Widener, 2013).

Marginal costing: This costing of an item can be also known as variable cost. Basically,

marginal costing of a product is a sum of direct martial, direct labour, direct expenses and

production cost. Due to, while increasing production level of products consequently

improve level of variable cost. Marginal costing of an organisation can be avoid when

items were not produced. Because it is co-related with manufacturing level of products

and goods.

Basis Absorption costing Marginal costing

Cost recognition In this method, various cost

can be view as product cost

while fixed cost consider as

period price.

In which foxed and variable

cost considered as product

cost.

Categorisation of overheads Fixed and variable Manufacturing, administration,

selling and distribution etc.

Highlights Contribution per unit of item Net profit of unit

Statement of profit and loss using absorption costing

Quarter 1

No. Of units £/unit £ £

Sales 66.000 1 66.000

Less: Cost of sales

Opening Stock 0 0.85 0

Production cost 78.000 0.85 66.300

66.300

Closing stock (12.000) 0.85 (10.200) (56.100)

Gross profit 9900

Less: Other Expenses

Selling &Administration costs (5.200)

Net Profit 4700

5

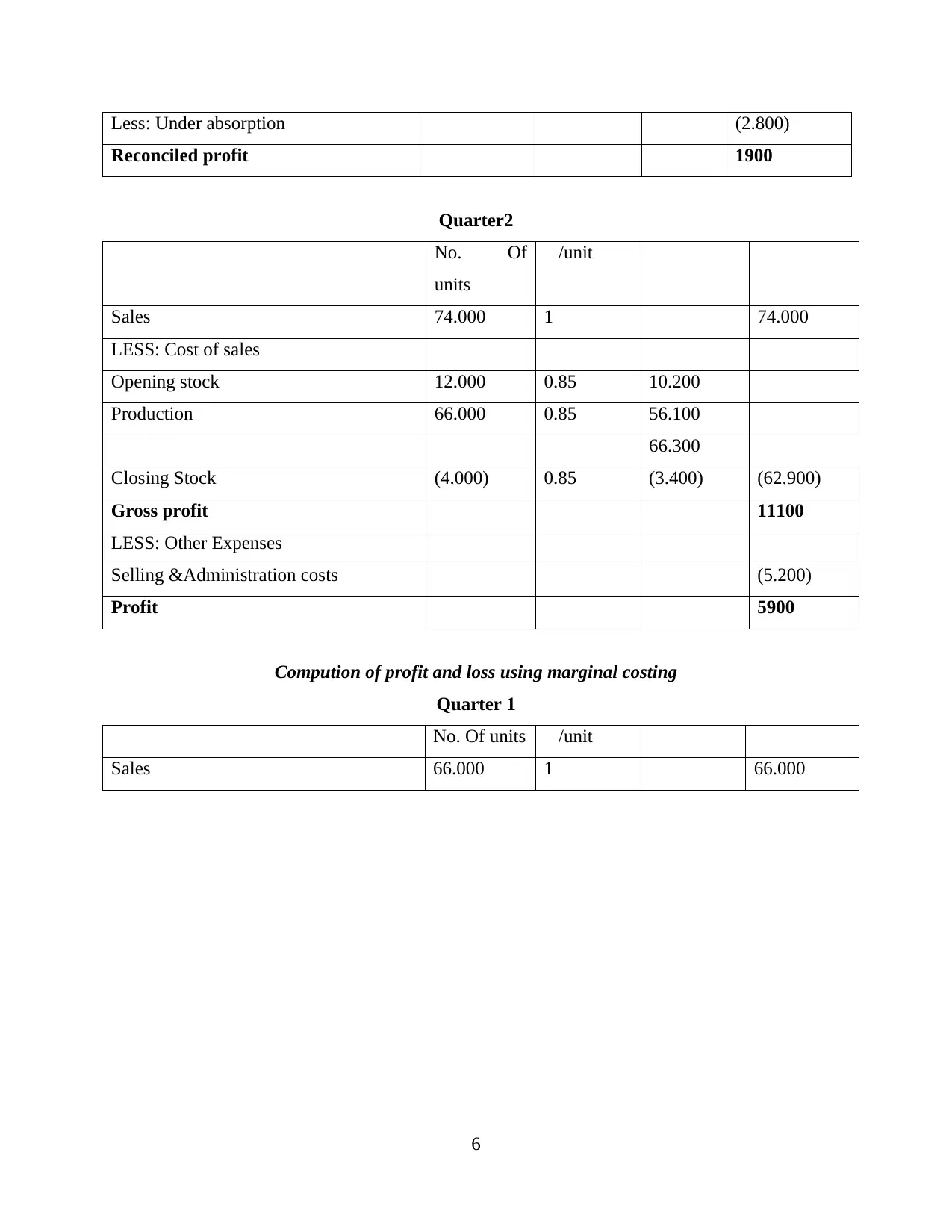

Less: Under absorption (2.800)

Reconciled profit 1900

Quarter2

No. Of

units

£/unit £ £

Sales 74.000 1 74.000

LESS: Cost of sales

Opening stock 12.000 0.85 10.200

Production 66.000 0.85 56.100

66.300

Closing Stock (4.000) 0.85 (3.400) (62.900)

Gross profit 11100

LESS: Other Expenses

Selling &Administration costs (5.200)

Profit 5900

Compution of profit and loss using marginal costing

Quarter 1

No. Of units £/unit £ £

Sales 66.000 1 66.000

6

Reconciled profit 1900

Quarter2

No. Of

units

£/unit £ £

Sales 74.000 1 74.000

LESS: Cost of sales

Opening stock 12.000 0.85 10.200

Production 66.000 0.85 56.100

66.300

Closing Stock (4.000) 0.85 (3.400) (62.900)

Gross profit 11100

LESS: Other Expenses

Selling &Administration costs (5.200)

Profit 5900

Compution of profit and loss using marginal costing

Quarter 1

No. Of units £/unit £ £

Sales 66.000 1 66.000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

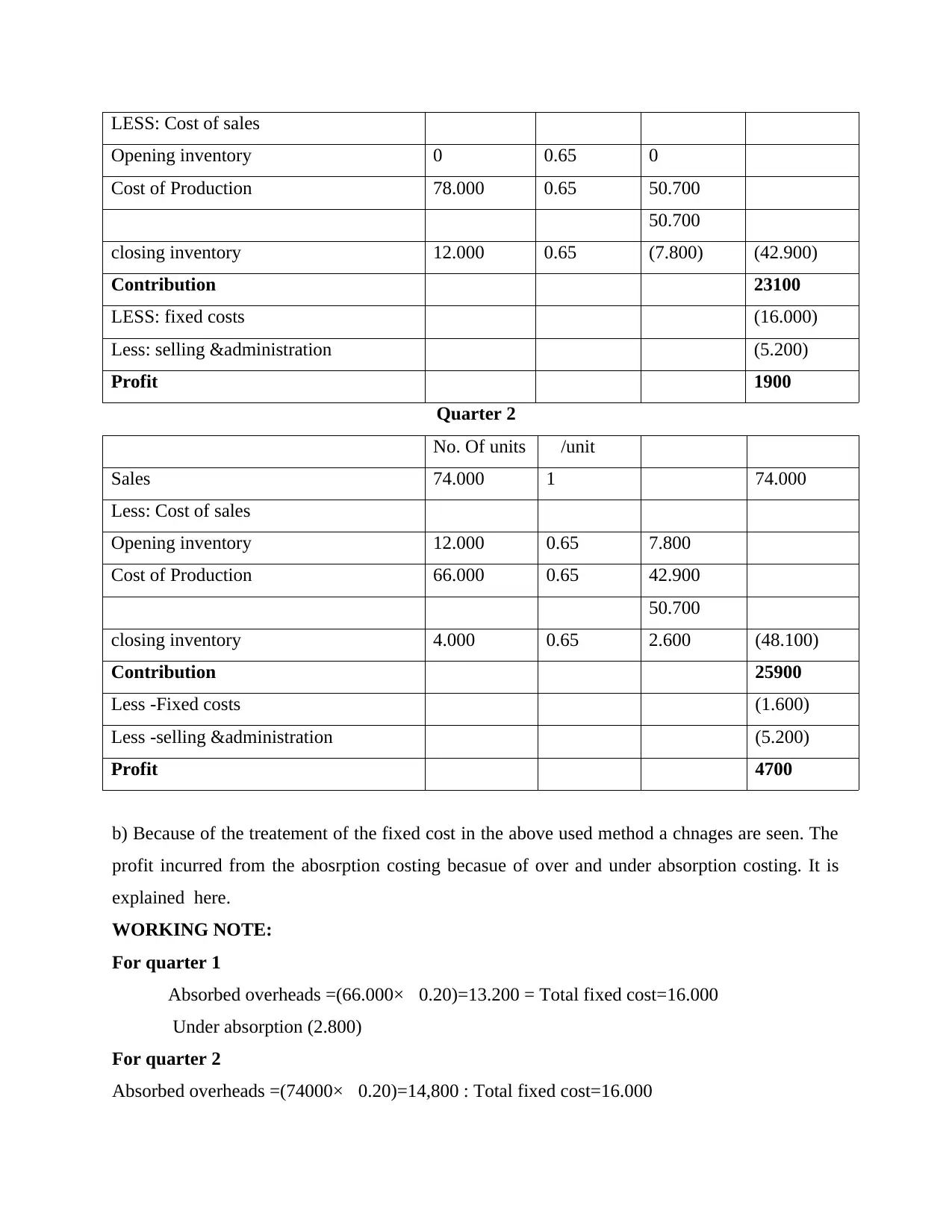

LESS: Cost of sales

Opening inventory 0 0.65 0

Cost of Production 78.000 0.65 50.700

50.700

closing inventory 12.000 0.65 (7.800) (42.900)

Contribution 23100

LESS: fixed costs (16.000)

Less: selling &administration (5.200)

Profit 1900

Quarter 2

No. Of units £/unit £ £

Sales 74.000 1 74.000

Less: Cost of sales

Opening inventory 12.000 0.65 7.800

Cost of Production 66.000 0.65 42.900

50.700

closing inventory 4.000 0.65 2.600 (48.100)

Contribution 25900

Less -Fixed costs (1.600)

Less -selling &administration (5.200)

Profit 4700

b) Because of the treatement of the fixed cost in the above used method a chnages are seen. The

profit incurred from the abosrption costing becasue of over and under absorption costing. It is

explained here.

WORKING NOTE:

For quarter 1

Absorbed overheads =(66.000×£0.20)=13.200 = Total fixed cost=16.000

Under absorption (2.800)

For quarter 2

Absorbed overheads =(74000×£0.20)=14,800 : Total fixed cost=16.000

Opening inventory 0 0.65 0

Cost of Production 78.000 0.65 50.700

50.700

closing inventory 12.000 0.65 (7.800) (42.900)

Contribution 23100

LESS: fixed costs (16.000)

Less: selling &administration (5.200)

Profit 1900

Quarter 2

No. Of units £/unit £ £

Sales 74.000 1 74.000

Less: Cost of sales

Opening inventory 12.000 0.65 7.800

Cost of Production 66.000 0.65 42.900

50.700

closing inventory 4.000 0.65 2.600 (48.100)

Contribution 25900

Less -Fixed costs (1.600)

Less -selling &administration (5.200)

Profit 4700

b) Because of the treatement of the fixed cost in the above used method a chnages are seen. The

profit incurred from the abosrption costing becasue of over and under absorption costing. It is

explained here.

WORKING NOTE:

For quarter 1

Absorbed overheads =(66.000×£0.20)=13.200 = Total fixed cost=16.000

Under absorption (2.800)

For quarter 2

Absorbed overheads =(74000×£0.20)=14,800 : Total fixed cost=16.000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Under absorption(1.200)

c) Reconciliation statements.

It is prepared in order to determine the profit for the company through using both the

costing methods:

8

c) Reconciliation statements.

It is prepared in order to determine the profit for the company through using both the

costing methods:

8

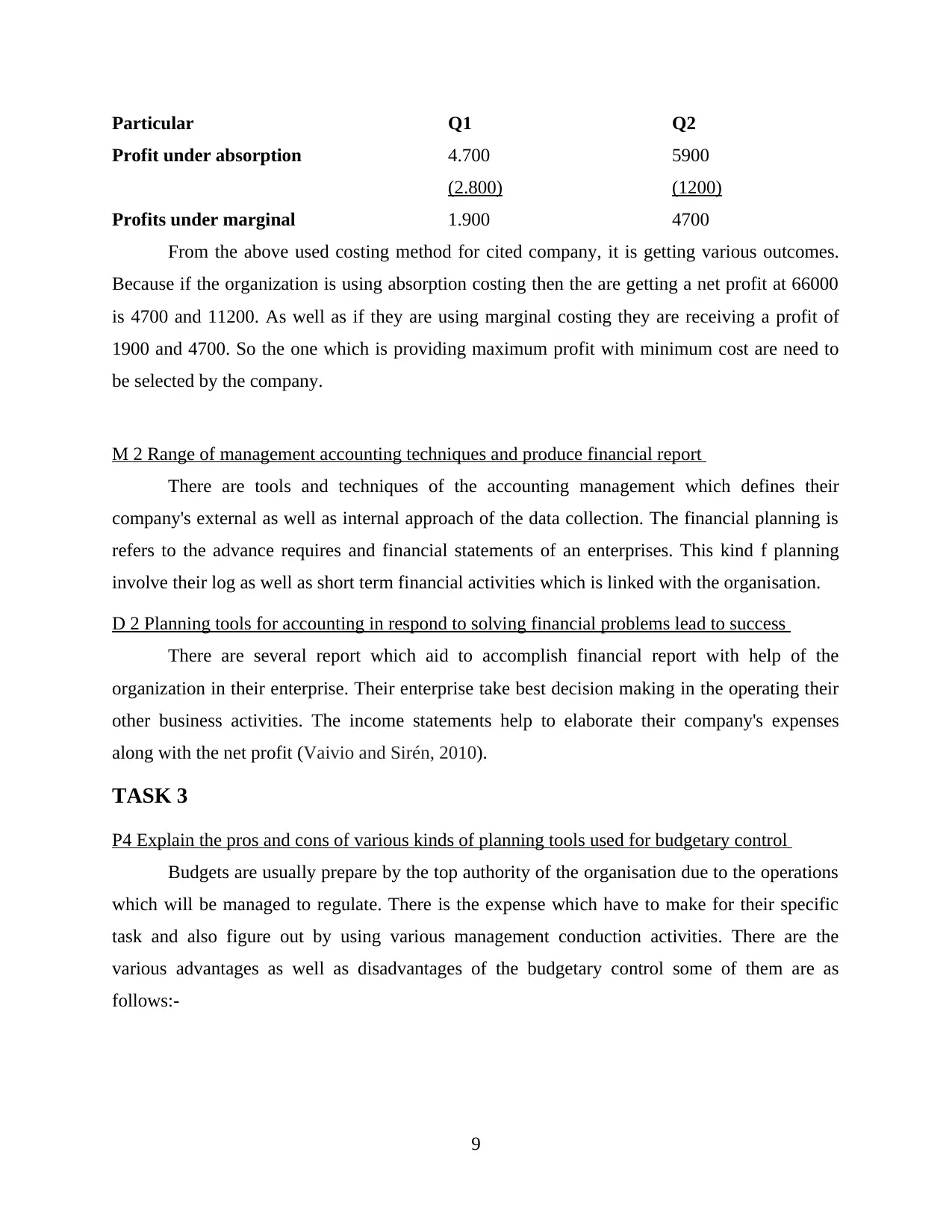

Particular Q1 Q2

Profit under absorption 4.700 5900

(2.800) (1200)

Profits under marginal 1.900 4700

From the above used costing method for cited company, it is getting various outcomes.

Because if the organization is using absorption costing then the are getting a net profit at 66000

is 4700 and 11200. As well as if they are using marginal costing they are receiving a profit of

1900 and 4700. So the one which is providing maximum profit with minimum cost are need to

be selected by the company.

M 2 Range of management accounting techniques and produce financial report

There are tools and techniques of the accounting management which defines their

company's external as well as internal approach of the data collection. The financial planning is

refers to the advance requires and financial statements of an enterprises. This kind f planning

involve their log as well as short term financial activities which is linked with the organisation.

D 2 Planning tools for accounting in respond to solving financial problems lead to success

There are several report which aid to accomplish financial report with help of the

organization in their enterprise. Their enterprise take best decision making in the operating their

other business activities. The income statements help to elaborate their company's expenses

along with the net profit (Vaivio and Sirén, 2010).

TASK 3

P4 Explain the pros and cons of various kinds of planning tools used for budgetary control

Budgets are usually prepare by the top authority of the organisation due to the operations

which will be managed to regulate. There is the expense which have to make for their specific

task and also figure out by using various management conduction activities. There are the

various advantages as well as disadvantages of the budgetary control some of them are as

follows:-

9

Profit under absorption 4.700 5900

(2.800) (1200)

Profits under marginal 1.900 4700

From the above used costing method for cited company, it is getting various outcomes.

Because if the organization is using absorption costing then the are getting a net profit at 66000

is 4700 and 11200. As well as if they are using marginal costing they are receiving a profit of

1900 and 4700. So the one which is providing maximum profit with minimum cost are need to

be selected by the company.

M 2 Range of management accounting techniques and produce financial report

There are tools and techniques of the accounting management which defines their

company's external as well as internal approach of the data collection. The financial planning is

refers to the advance requires and financial statements of an enterprises. This kind f planning

involve their log as well as short term financial activities which is linked with the organisation.

D 2 Planning tools for accounting in respond to solving financial problems lead to success

There are several report which aid to accomplish financial report with help of the

organization in their enterprise. Their enterprise take best decision making in the operating their

other business activities. The income statements help to elaborate their company's expenses

along with the net profit (Vaivio and Sirén, 2010).

TASK 3

P4 Explain the pros and cons of various kinds of planning tools used for budgetary control

Budgets are usually prepare by the top authority of the organisation due to the operations

which will be managed to regulate. There is the expense which have to make for their specific

task and also figure out by using various management conduction activities. There are the

various advantages as well as disadvantages of the budgetary control some of them are as

follows:-

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.