Management Accounting Systems, Costing, Planning and Financial Report

VerifiedAdded on 2021/02/19

|16

|5248

|44

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on various systems, methodologies, and their applications within an organizational context. It delves into different management accounting systems such as price optimization, cost accounting, inventory management, and job costing, examining their benefits and drawbacks. The report also explores different management accounting reporting methodologies, including performance reports, budget reports, and inventory management reports. It applies marginal and absorption costing techniques to prepare financial income statements for Oshodi Plc, a manufacturing entity. Furthermore, it analyzes the advantages and disadvantages of various planning tools utilized for budgetary control and evaluates how companies adapt management systems in the face of financial issues, culminating in an assessment of how management accounting systems contribute to sustainable organizational success.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

P1. Various Management Accounting Systems and their essential requirements:......................4

P2. Different Methodologies utilised in Management Accounting Reporting:...........................6

M1. Evaluating benefits of Management Accounting Systems and their application in

organisational context..................................................................................................................7

D1. Critically evaluate how management accounting systems and management accounting

reporting is integrated within organisational processes;..............................................................8

TASK 2............................................................................................................................................8

P3. Computing Costs through Marginal and Absorption Costing to prepare financial income

statements:....................................................................................................................................8

Marginal Costing ............................................................................................................................8

M2. Application of management accounting techniques to produce appropriate financial

reporting documents...................................................................................................................10

D2. Produce financial reports that accurately apply and interpret data for a range of business

activities:....................................................................................................................................10

TASK 3..........................................................................................................................................10

P4. Advantages and Disadvantages of various planning tools utilised to exercise budgetary

control:.......................................................................................................................................10

M3. Analysing use of different planning tools and their application for developing and

forecasting budgets....................................................................................................................12

TASK 4..........................................................................................................................................13

P5. Examining how companies adapt to management systems in the face of financial issues. 13

M4. Analysing how management accounting systems contribute towards sustainable

organisational success................................................................................................................15

D3. Evaluating how accounting planning tools help in resolving financial problems:.............15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

P1. Various Management Accounting Systems and their essential requirements:......................4

P2. Different Methodologies utilised in Management Accounting Reporting:...........................6

M1. Evaluating benefits of Management Accounting Systems and their application in

organisational context..................................................................................................................7

D1. Critically evaluate how management accounting systems and management accounting

reporting is integrated within organisational processes;..............................................................8

TASK 2............................................................................................................................................8

P3. Computing Costs through Marginal and Absorption Costing to prepare financial income

statements:....................................................................................................................................8

Marginal Costing ............................................................................................................................8

M2. Application of management accounting techniques to produce appropriate financial

reporting documents...................................................................................................................10

D2. Produce financial reports that accurately apply and interpret data for a range of business

activities:....................................................................................................................................10

TASK 3..........................................................................................................................................10

P4. Advantages and Disadvantages of various planning tools utilised to exercise budgetary

control:.......................................................................................................................................10

M3. Analysing use of different planning tools and their application for developing and

forecasting budgets....................................................................................................................12

TASK 4..........................................................................................................................................13

P5. Examining how companies adapt to management systems in the face of financial issues. 13

M4. Analysing how management accounting systems contribute towards sustainable

organisational success................................................................................................................15

D3. Evaluating how accounting planning tools help in resolving financial problems:.............15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The concept and notion of 'Management Accounting' is directly linked to the procedures

and structures taken by the organizations to guarantee that their inner activities function

smoothly. It therefore involves processes/tasks that recognize, appropriately measure, controls,

assess, explicate and transmit to executives at all levels crucial data about corporate operations.

This enables them to make informed choices and facilitates the effective fulfilment of

organizational objectives within a specified time-frame or period (Achleitner and et.al, 2014).

The study explains management accounting's concepts and its purpose, ways through

which management accounting's system contributes in success of entity, planning tools and

costing techniques in context of Oshodi Plc. It is manufacturing entity, engaged in production of

fruit juice under the brand name JOJO fruit-juice, for all age of customers. Using data of

respective company, applying Marginal and Absorption method's of costing net income is

generated. This study also describes how advantageous or disadvantageous planning tools are for

company and compares distinct business entities embracing systems to react to different

economic and financial issues.

TASK 1

P1. Various Management Accounting Systems and their essential requirements:

Management Accounting can be described as a processes that facilitates the evaluation of

different corporate operations in order to allow business personnels to make better choices from

a short/long-term view. In this context, to transform raw or unclassified data into meaningful or

useful information, it is vital for a manager and some other personnels to analyse their trade

environment's internal and external elements effectively. It finally assist business to attain

benefits in competitive environment (Aouni, McGillis and Abdulkarim, 2017). As Oshodi Plc is

selling its fruit juice with brand label of JOJO fruit-juice so adopting management accounting

can help company's owners to achieve targeted expansion. Company being a production oriented

entity carrying on wide processes and tasks which useful in accomplishment of goals. Below

discussed are important management accounting systems used by respective company, as

follows:

Price Optimisation System: Price determination is part of management's strategies and

they make changes in prices to set a most effective value of product while maintaining profit

The concept and notion of 'Management Accounting' is directly linked to the procedures

and structures taken by the organizations to guarantee that their inner activities function

smoothly. It therefore involves processes/tasks that recognize, appropriately measure, controls,

assess, explicate and transmit to executives at all levels crucial data about corporate operations.

This enables them to make informed choices and facilitates the effective fulfilment of

organizational objectives within a specified time-frame or period (Achleitner and et.al, 2014).

The study explains management accounting's concepts and its purpose, ways through

which management accounting's system contributes in success of entity, planning tools and

costing techniques in context of Oshodi Plc. It is manufacturing entity, engaged in production of

fruit juice under the brand name JOJO fruit-juice, for all age of customers. Using data of

respective company, applying Marginal and Absorption method's of costing net income is

generated. This study also describes how advantageous or disadvantageous planning tools are for

company and compares distinct business entities embracing systems to react to different

economic and financial issues.

TASK 1

P1. Various Management Accounting Systems and their essential requirements:

Management Accounting can be described as a processes that facilitates the evaluation of

different corporate operations in order to allow business personnels to make better choices from

a short/long-term view. In this context, to transform raw or unclassified data into meaningful or

useful information, it is vital for a manager and some other personnels to analyse their trade

environment's internal and external elements effectively. It finally assist business to attain

benefits in competitive environment (Aouni, McGillis and Abdulkarim, 2017). As Oshodi Plc is

selling its fruit juice with brand label of JOJO fruit-juice so adopting management accounting

can help company's owners to achieve targeted expansion. Company being a production oriented

entity carrying on wide processes and tasks which useful in accomplishment of goals. Below

discussed are important management accounting systems used by respective company, as

follows:

Price Optimisation System: Price determination is part of management's strategies and

they make changes in prices to set a most effective value of product while maintaining profit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

margin. Price optimisation system evaluates effect on demand of company's items and product

with planned fluctuation in prices. Customers compare various companies' product on the basis

of prices, so company prepare strategies to determine prices to face competition. Through it

Oshodi Plc determines price of fruit-juice at different market segments. Managers in respective

company analyses the relation of product's demand and supply with price of its different fruit-

juice. This system not only help in maintaining effects of market competitiveness, but also

generates comparative benefits for improving share in market. Ultimate aim of such system is to

increase productivity in producing products while increasing demand.

Cost Accounting System: Every manufacturing concern like Oshodi Plc internally

analyse its incurred costs and expenses with aim to evaluate whether company is effectively able

to control its costs to make targeted profits. Adapting this system facilitates company to organise

its costs and develop a base for making reliable estimation of costs to manage budget. As a

manufacturer, the Cost accounting system adopted by respective organisation has paramount

significance for company as it determines general pricing policies and strategies while

combining its goals. Annual budgets are formulated by corporates applying information of this

system.

Inventory Management System: Handling of stock is significant practice for business

entities because companies specially production units have large quantity and variety of

inventories. A ineffective stock managing can results in excessive loss of stock-items, storing

costs and handing expenses etc. It help to evaluate how effectively inventory is utilised by

company (Datar and Rajan, 2014). Oshodi Plc by inventory management system managing its

inventories like raw items to prepare fruit-juice, items in production processes, closing

inventories, finished products etc. It is required to organise company's inventories because it can

result in profit graph of company. Recognising elements leading to increase in inventory's costs

can be easily done through this system.

Job Costing System: This includes the process of collecting cost data specifically related

to the manufacturing and delivery of such costs to specific work or task. To determine

accountability in operations this system is placed by company by summarising and allocating

expenses to particular work or job. Direct materials, overheads and labour are required

information in adaption of Job Costing System. In such context, following is discussion:

with planned fluctuation in prices. Customers compare various companies' product on the basis

of prices, so company prepare strategies to determine prices to face competition. Through it

Oshodi Plc determines price of fruit-juice at different market segments. Managers in respective

company analyses the relation of product's demand and supply with price of its different fruit-

juice. This system not only help in maintaining effects of market competitiveness, but also

generates comparative benefits for improving share in market. Ultimate aim of such system is to

increase productivity in producing products while increasing demand.

Cost Accounting System: Every manufacturing concern like Oshodi Plc internally

analyse its incurred costs and expenses with aim to evaluate whether company is effectively able

to control its costs to make targeted profits. Adapting this system facilitates company to organise

its costs and develop a base for making reliable estimation of costs to manage budget. As a

manufacturer, the Cost accounting system adopted by respective organisation has paramount

significance for company as it determines general pricing policies and strategies while

combining its goals. Annual budgets are formulated by corporates applying information of this

system.

Inventory Management System: Handling of stock is significant practice for business

entities because companies specially production units have large quantity and variety of

inventories. A ineffective stock managing can results in excessive loss of stock-items, storing

costs and handing expenses etc. It help to evaluate how effectively inventory is utilised by

company (Datar and Rajan, 2014). Oshodi Plc by inventory management system managing its

inventories like raw items to prepare fruit-juice, items in production processes, closing

inventories, finished products etc. It is required to organise company's inventories because it can

result in profit graph of company. Recognising elements leading to increase in inventory's costs

can be easily done through this system.

Job Costing System: This includes the process of collecting cost data specifically related

to the manufacturing and delivery of such costs to specific work or task. To determine

accountability in operations this system is placed by company by summarising and allocating

expenses to particular work or job. Direct materials, overheads and labour are required

information in adaption of Job Costing System. In such context, following is discussion:

Direct Material: Tractability of direct components of material and labour, particularly

those discarded or used during accomplishing tasks, must be simple for an ideal job costing

system. Enabling business officials to match expenses with their respective tasks in effectively

way.

Direct Labour: It provide data for labour expenses incurred by entity to complete any

job. It help to asses how much costs are incurred on different tasks

Overheads: These are overall expensed sum by entity to complete any specific job task.

Combining overheads information with direct labour and materials provides entire cost of work

task.

P2. Different Methodologies utilised in Management Accounting Reporting:

Management Accounting Reporting relates to trade practices which enables managing

officials to report fiscal and other monetary informations to top level personnels of company's

management structure. Customised reports are also used by company to target any particular

problem. Reporting process is wholly based on report preparing task using systems' informations

(Ge and Kim, 2014). Two major requirement of reporting is accuracy and understandability,

fulfilment of these key requirement can provide reliable and trustworthy reports to stakeholders.

For internal and external assessment different sort of reports are used by corporates. Oshodi Plc

reports its fiscal results for attacking stakeholders. It also reports matters for internal analysis of

company's operating efficiencies. Following discussed are major reports framed by respective

organisation, as follows:

Performance Report: This report facilitate assessment of company's performance while

covering its employees and labour performance. A continuous review of employees is necessary

to asses employee's efficiencies and get them benefits for their performances in order to promote

them. In Oshodi Plc, company set targets for employees and evaluates how effectively they are

attaining set tasks and targets. It assures proper utilization of company's human resources with

objective of achieving predetermined productivity level. Incorporation of such reports can allow

management to recognize star employees of entity and determine reward for personnels who are

performing fabulous within entity and in their particular fields. Encouraging employees is aim of

this report to increase overall efficiency.

Budget report: A reliable forecast of company's fiscal data is significant to take instant

and important managing decisions. For this budget reports are considerable reports which also

those discarded or used during accomplishing tasks, must be simple for an ideal job costing

system. Enabling business officials to match expenses with their respective tasks in effectively

way.

Direct Labour: It provide data for labour expenses incurred by entity to complete any

job. It help to asses how much costs are incurred on different tasks

Overheads: These are overall expensed sum by entity to complete any specific job task.

Combining overheads information with direct labour and materials provides entire cost of work

task.

P2. Different Methodologies utilised in Management Accounting Reporting:

Management Accounting Reporting relates to trade practices which enables managing

officials to report fiscal and other monetary informations to top level personnels of company's

management structure. Customised reports are also used by company to target any particular

problem. Reporting process is wholly based on report preparing task using systems' informations

(Ge and Kim, 2014). Two major requirement of reporting is accuracy and understandability,

fulfilment of these key requirement can provide reliable and trustworthy reports to stakeholders.

For internal and external assessment different sort of reports are used by corporates. Oshodi Plc

reports its fiscal results for attacking stakeholders. It also reports matters for internal analysis of

company's operating efficiencies. Following discussed are major reports framed by respective

organisation, as follows:

Performance Report: This report facilitate assessment of company's performance while

covering its employees and labour performance. A continuous review of employees is necessary

to asses employee's efficiencies and get them benefits for their performances in order to promote

them. In Oshodi Plc, company set targets for employees and evaluates how effectively they are

attaining set tasks and targets. It assures proper utilization of company's human resources with

objective of achieving predetermined productivity level. Incorporation of such reports can allow

management to recognize star employees of entity and determine reward for personnels who are

performing fabulous within entity and in their particular fields. Encouraging employees is aim of

this report to increase overall efficiency.

Budget report: A reliable forecast of company's fiscal data is significant to take instant

and important managing decisions. For this budget reports are considerable reports which also

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

facilitates a comparison. A budget of entity includes all data about company's sales, incomes and

expenses along with estimation bases on past scenarios. In Oshodi Plc, to take long and short

term decisions manufacturing process and other processes heads form budgets and send these

reports to higher managing officials. Sometime to asses the root-cause of any problem

management directs to prepare budgets (Guragai and et.al, 2015). Budgets can be prepared for

each material or significant element of entity as sales budgets, overhead budget, labour budget,

purchase budget etc. It brings easiness in formulating charts, graphs and other graphical

presentation.

Account Receivable Ageing Report: It is major report which exhibits about how much

time entity's debtors normally takes to make payment of their dues and debts. Its break downs the

the ageing cycle of company's account receivables. Recognisance of suspicious debtors who may

be insolvent, can be easily traced with this report. It simply determines the status of company 's

all debtors. Manufacturing corporates like Oshodi Plc classifies their debtors as per their ageing

of payment and recognise any possible bed debts using this report. Thus, it is essential for entity

to formulate such accounts to ensure that its present short term debt strategies are powerful

enough for the lending parties to adhere to them or not.

Inventory Management Report: Inventory reports are vital practice which assist in

fixing economic stock quantity in respect of company, re-order levels presented in report ensure

easy trace of stocks. In Osholdi PLC, such assist in organising record of raw items and materials

used and other expense or overheads in context of them in a complete comprehensive manner.

This report complaisant for business entity as it provide ease in finding the actual or real status of

stocks in warehouse, goods which are in transit or that delivered to different clients effectively.

M1. Evaluating benefits of Management Accounting Systems and their application in

organisational context

Different accounting systems Advantages Disadvantages

Inventory Management

System

It prevents loss of theft of

goods and waste.

Safety stock calculation and re

order level, practically do

not provide realistic

results (Hiebl and

Mayrleitner, 2017).

expenses along with estimation bases on past scenarios. In Oshodi Plc, to take long and short

term decisions manufacturing process and other processes heads form budgets and send these

reports to higher managing officials. Sometime to asses the root-cause of any problem

management directs to prepare budgets (Guragai and et.al, 2015). Budgets can be prepared for

each material or significant element of entity as sales budgets, overhead budget, labour budget,

purchase budget etc. It brings easiness in formulating charts, graphs and other graphical

presentation.

Account Receivable Ageing Report: It is major report which exhibits about how much

time entity's debtors normally takes to make payment of their dues and debts. Its break downs the

the ageing cycle of company's account receivables. Recognisance of suspicious debtors who may

be insolvent, can be easily traced with this report. It simply determines the status of company 's

all debtors. Manufacturing corporates like Oshodi Plc classifies their debtors as per their ageing

of payment and recognise any possible bed debts using this report. Thus, it is essential for entity

to formulate such accounts to ensure that its present short term debt strategies are powerful

enough for the lending parties to adhere to them or not.

Inventory Management Report: Inventory reports are vital practice which assist in

fixing economic stock quantity in respect of company, re-order levels presented in report ensure

easy trace of stocks. In Osholdi PLC, such assist in organising record of raw items and materials

used and other expense or overheads in context of them in a complete comprehensive manner.

This report complaisant for business entity as it provide ease in finding the actual or real status of

stocks in warehouse, goods which are in transit or that delivered to different clients effectively.

M1. Evaluating benefits of Management Accounting Systems and their application in

organisational context

Different accounting systems Advantages Disadvantages

Inventory Management

System

It prevents loss of theft of

goods and waste.

Safety stock calculation and re

order level, practically do

not provide realistic

results (Hiebl and

Mayrleitner, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price optimisation system Its beneficial in Increasing

entity's customer base.

Analysing effects on demand

at different price label can

lead to shift in customer

base.

Job Costing System It provide proper

accountability in different

works.

Simultaneous use of job

costing and other normal

processes creates conflicts.

Cost accounting system It act as raw material for

preparation of annual

budgets.

An inappropriate assumption

in can results in wrong

decisions.

D1. Critically evaluate how management accounting systems and management accounting

reporting is integrated within organisational processes;

All the process heads are responsible for providing information for management

accounting's systems. By doing this they provides easiness in implementation of such systems

(Hrasky and Jones, 2016). As in Oshodi Plc accountants providers fiscal data to managing

personnels which is further applied by them to prepare budgets and in different systems. While

effectively adapting, different systems managers directly gathers relevant data to formulate

strategies for operating processes in business entity.

TASK 2

P3. Computing Costs through Marginal and Absorption Costing to prepare financial income

statements:

Marginal Costing:

As per this technique, contribution per unit is ascertained by taking into account only the

variable costs incurred on the production of an additional unit of output.

Particulars November (£)

Sales 500000

Less: Cost of sales

Direct Material Costs -180000

Direct Labor costs -40000

Variable Production Overheads -30000

Contribution 250000

entity's customer base.

Analysing effects on demand

at different price label can

lead to shift in customer

base.

Job Costing System It provide proper

accountability in different

works.

Simultaneous use of job

costing and other normal

processes creates conflicts.

Cost accounting system It act as raw material for

preparation of annual

budgets.

An inappropriate assumption

in can results in wrong

decisions.

D1. Critically evaluate how management accounting systems and management accounting

reporting is integrated within organisational processes;

All the process heads are responsible for providing information for management

accounting's systems. By doing this they provides easiness in implementation of such systems

(Hrasky and Jones, 2016). As in Oshodi Plc accountants providers fiscal data to managing

personnels which is further applied by them to prepare budgets and in different systems. While

effectively adapting, different systems managers directly gathers relevant data to formulate

strategies for operating processes in business entity.

TASK 2

P3. Computing Costs through Marginal and Absorption Costing to prepare financial income

statements:

Marginal Costing:

As per this technique, contribution per unit is ascertained by taking into account only the

variable costs incurred on the production of an additional unit of output.

Particulars November (£)

Sales 500000

Less: Cost of sales

Direct Material Costs -180000

Direct Labor costs -40000

Variable Production Overheads -30000

Contribution 250000

Less:

Variable selling overheads (10% sale value) -50000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Fixed production overheads -99000

Net Profit 61000

Particulars December (£)

Sales 600000

Less: cost of sale

Direct Material Costs -216000

Direct Labour costs -48000

Variable Production Overheads -36000

Contribution 300000

Less:

Variable selling overheads (10% sale value) -60000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Fixed production overheads -99000

Net Profit 101000

Absorption Costing:

Under this costing technique, both fixed and variable costs are taken into account

that facilitate the determination of net profit earned per unit on an output by a business

(Hu and et.al, 2015).

Particulars November (£)

Sales 50 500000

Less: Cost of sales -340000

Gross profit 160000

Variable selling overheads (10% sale value) 10000*5 -50000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Under/over absorbed prod expenses 9000

Net Profit 79000

Particulars December (£)

Sales 50 600000

Less: Cost of sales -408000

Variable selling overheads (10% sale value) -50000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Fixed production overheads -99000

Net Profit 61000

Particulars December (£)

Sales 600000

Less: cost of sale

Direct Material Costs -216000

Direct Labour costs -48000

Variable Production Overheads -36000

Contribution 300000

Less:

Variable selling overheads (10% sale value) -60000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Fixed production overheads -99000

Net Profit 101000

Absorption Costing:

Under this costing technique, both fixed and variable costs are taken into account

that facilitate the determination of net profit earned per unit on an output by a business

(Hu and et.al, 2015).

Particulars November (£)

Sales 50 500000

Less: Cost of sales -340000

Gross profit 160000

Variable selling overheads (10% sale value) 10000*5 -50000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Under/over absorbed prod expenses 9000

Net Profit 79000

Particulars December (£)

Sales 50 600000

Less: Cost of sales -408000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

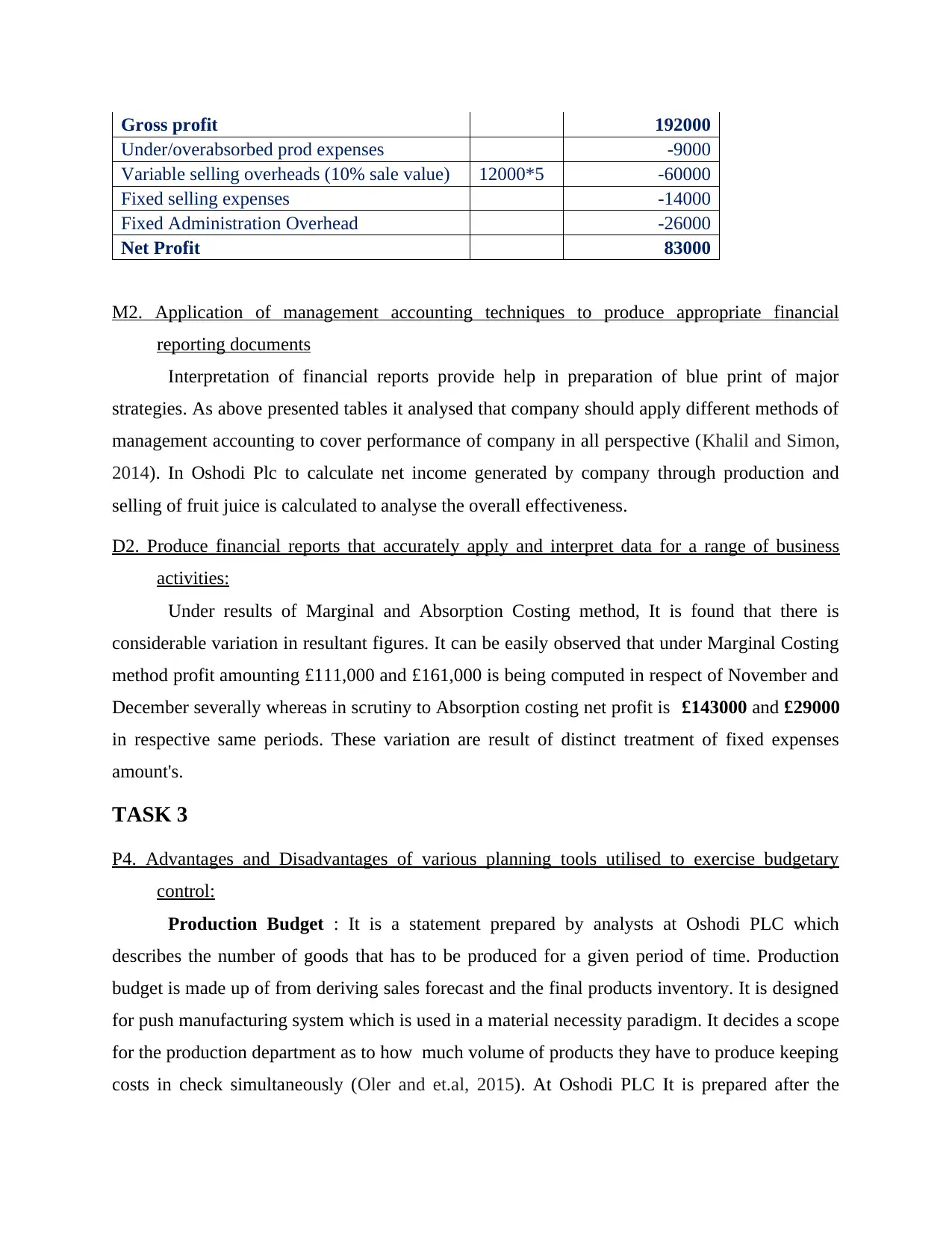

Gross profit 192000

Under/overabsorbed prod expenses -9000

Variable selling overheads (10% sale value) 12000*5 -60000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Net Profit 83000

M2. Application of management accounting techniques to produce appropriate financial

reporting documents

Interpretation of financial reports provide help in preparation of blue print of major

strategies. As above presented tables it analysed that company should apply different methods of

management accounting to cover performance of company in all perspective (Khalil and Simon,

2014). In Oshodi Plc to calculate net income generated by company through production and

selling of fruit juice is calculated to analyse the overall effectiveness.

D2. Produce financial reports that accurately apply and interpret data for a range of business

activities:

Under results of Marginal and Absorption Costing method, It is found that there is

considerable variation in resultant figures. It can be easily observed that under Marginal Costing

method profit amounting £111,000 and £161,000 is being computed in respect of November and

December severally whereas in scrutiny to Absorption costing net profit is £143000 and £29000

in respective same periods. These variation are result of distinct treatment of fixed expenses

amount's.

TASK 3

P4. Advantages and Disadvantages of various planning tools utilised to exercise budgetary

control:

Production Budget : It is a statement prepared by analysts at Oshodi PLC which

describes the number of goods that has to be produced for a given period of time. Production

budget is made up of from deriving sales forecast and the final products inventory. It is designed

for push manufacturing system which is used in a material necessity paradigm. It decides a scope

for the production department as to how much volume of products they have to produce keeping

costs in check simultaneously (Oler and et.al, 2015). At Oshodi PLC It is prepared after the

Under/overabsorbed prod expenses -9000

Variable selling overheads (10% sale value) 12000*5 -60000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Net Profit 83000

M2. Application of management accounting techniques to produce appropriate financial

reporting documents

Interpretation of financial reports provide help in preparation of blue print of major

strategies. As above presented tables it analysed that company should apply different methods of

management accounting to cover performance of company in all perspective (Khalil and Simon,

2014). In Oshodi Plc to calculate net income generated by company through production and

selling of fruit juice is calculated to analyse the overall effectiveness.

D2. Produce financial reports that accurately apply and interpret data for a range of business

activities:

Under results of Marginal and Absorption Costing method, It is found that there is

considerable variation in resultant figures. It can be easily observed that under Marginal Costing

method profit amounting £111,000 and £161,000 is being computed in respect of November and

December severally whereas in scrutiny to Absorption costing net profit is £143000 and £29000

in respective same periods. These variation are result of distinct treatment of fixed expenses

amount's.

TASK 3

P4. Advantages and Disadvantages of various planning tools utilised to exercise budgetary

control:

Production Budget : It is a statement prepared by analysts at Oshodi PLC which

describes the number of goods that has to be produced for a given period of time. Production

budget is made up of from deriving sales forecast and the final products inventory. It is designed

for push manufacturing system which is used in a material necessity paradigm. It decides a scope

for the production department as to how much volume of products they have to produce keeping

costs in check simultaneously (Oler and et.al, 2015). At Oshodi PLC It is prepared after the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

preparation of sales budget. The advantage of a production budget is that the plant and

machineries can be used to their full potential. And the disadvantage of this budget is that it

doesn't include the qualitative factors of producing a good like work conditions, level of hazards

etc.

Purchase budget : It contains figures about the inventory which needs to be purchased

by the procurement department of Oshodi PLC during a budget period. The purchase budget

outlines the scope for the company to purchase sufficient amount of inventory required to

produce goods to the satisfaction of the clientele. A typical budget has to consider beginning

balance, service levels, product terminations, cash usage as its core to draw a map for the budget.

It is most preferred by retailers or wholesalers who refrain from manufacturing their own

products. Its advantage is that it saves money from being wasted by creating a boundary line on

spending and its disadvantage is that it restricts the scope of procurement because of which

important things needed could not be purchased.

Sales budget : A sales budget made by Oshodi PLC's management to estimate the sales

per unit of a budgeted period and the expected revenue to be generated from the sales.

Meanwhile, the company produces a large variety of products, it segregates its total expected

sales into minimized quantities of product categories or regional division (Ponisciakova,

Gogolova and Ivankova, 2015). A sales budget is prepared quarterly as well as monthly at

oshodi. Making a yearly sales budget would make it too cumbersome to take constructive actions

on it. It benefits are that it decides sales targets for each period which gives a vision, It greatest

short coming is that it sometimes sets figures which may be very harsh on employees to achieve.

Labour budget : It is a quantitative statement which is needed to evaluate the number of

man labour hours needed to produce the number of units of the products identified in the

production budget. A comprehensive labour along with calculating labour hours per unit also

provides manned information by breaking down the work in labour category. It is useful for

Oshodi's management in forecasting the number of workers who will needed to be staffed in

order to fulfil the requirements of the manufacturing department. It helps in designing job hours,

overtime schedule and lay off policy. It helps in deciding hourly wages for the workers .

Meanwhile its drawback is that depreciates the human element out of the budget which can't be

quantified.

machineries can be used to their full potential. And the disadvantage of this budget is that it

doesn't include the qualitative factors of producing a good like work conditions, level of hazards

etc.

Purchase budget : It contains figures about the inventory which needs to be purchased

by the procurement department of Oshodi PLC during a budget period. The purchase budget

outlines the scope for the company to purchase sufficient amount of inventory required to

produce goods to the satisfaction of the clientele. A typical budget has to consider beginning

balance, service levels, product terminations, cash usage as its core to draw a map for the budget.

It is most preferred by retailers or wholesalers who refrain from manufacturing their own

products. Its advantage is that it saves money from being wasted by creating a boundary line on

spending and its disadvantage is that it restricts the scope of procurement because of which

important things needed could not be purchased.

Sales budget : A sales budget made by Oshodi PLC's management to estimate the sales

per unit of a budgeted period and the expected revenue to be generated from the sales.

Meanwhile, the company produces a large variety of products, it segregates its total expected

sales into minimized quantities of product categories or regional division (Ponisciakova,

Gogolova and Ivankova, 2015). A sales budget is prepared quarterly as well as monthly at

oshodi. Making a yearly sales budget would make it too cumbersome to take constructive actions

on it. It benefits are that it decides sales targets for each period which gives a vision, It greatest

short coming is that it sometimes sets figures which may be very harsh on employees to achieve.

Labour budget : It is a quantitative statement which is needed to evaluate the number of

man labour hours needed to produce the number of units of the products identified in the

production budget. A comprehensive labour along with calculating labour hours per unit also

provides manned information by breaking down the work in labour category. It is useful for

Oshodi's management in forecasting the number of workers who will needed to be staffed in

order to fulfil the requirements of the manufacturing department. It helps in designing job hours,

overtime schedule and lay off policy. It helps in deciding hourly wages for the workers .

Meanwhile its drawback is that depreciates the human element out of the budget which can't be

quantified.

Capital budget : A capital budget is prepared to create a scope for the acquisition of

capital assets in a year. It defines the border line for the management on proposing fixed assets.

It helps the management in acquiring profitable fixed assets and declining loss making entities.

Capital budgets are of great importance to corporations at they mark up in the balance sheet as

long term asset (Rampini, Sufi and Viswanathan, 2014). And their impact can be so large that a

good capital budget has the capacity to decide the future of any organisation. Since they are

irreversible in nature so it will very costly if it fails. It is crucial budget and if implemented well

it would bear handsome profits, It drawbacks are that it very static and rigid in nature.

Marketing budget : Marketing budget is an estimate of the funds required to promote

products via various marketing channels like media, newspapers, advertising campaigns, online

marketing etc. it includes all the costs which are needed to grow the product in the market and

among the customers. It is always consistent because a product has to be promoted throughout.

Marketing budget at Oshodi Plc is made according to the percentage of sales or revenue. It is a

very critically important budget for the organisation as this ensures that adequate money is being

spent on promoting the products which will eventually bring profits. It is beneficial to the

business in a way that it is only activity through which profits can be secured whereas its

drawback is that it doesn't guarantee returns in comparison to the level of money invested.

Cash budget : It determines the net inflow-outflow of cash transactions which will take

place in a period at Oshodi plc. This budget is prepared to ensure the liquidity position of the

company. The cash inflow & outflow includes revenues received, expenses incurred and loan

details of the business. Its advantage is that it defines the liquid position of the firm and gives

data about liquidity whereas its disadvantage is that it lowers the credit limit of the organisation.

M3. Analysing use of different planning tools and their application for developing and

forecasting budgets

Different sort of planning tools assisting in formulating different report budgets that

provide way to plan organisation's activities. These described budgets also help to set norms to

improve and maintain the efficiency of staff and whole company (Seal and Mattimoe, 2016). The

Oshodi Plc also using these as managerial process to face economic difficulties. Budgets defines

organisation's tasks and structures as per company's goals. As master budget, is prepared at the

end of accounting period to determine objectives of company and compute vital results.

capital assets in a year. It defines the border line for the management on proposing fixed assets.

It helps the management in acquiring profitable fixed assets and declining loss making entities.

Capital budgets are of great importance to corporations at they mark up in the balance sheet as

long term asset (Rampini, Sufi and Viswanathan, 2014). And their impact can be so large that a

good capital budget has the capacity to decide the future of any organisation. Since they are

irreversible in nature so it will very costly if it fails. It is crucial budget and if implemented well

it would bear handsome profits, It drawbacks are that it very static and rigid in nature.

Marketing budget : Marketing budget is an estimate of the funds required to promote

products via various marketing channels like media, newspapers, advertising campaigns, online

marketing etc. it includes all the costs which are needed to grow the product in the market and

among the customers. It is always consistent because a product has to be promoted throughout.

Marketing budget at Oshodi Plc is made according to the percentage of sales or revenue. It is a

very critically important budget for the organisation as this ensures that adequate money is being

spent on promoting the products which will eventually bring profits. It is beneficial to the

business in a way that it is only activity through which profits can be secured whereas its

drawback is that it doesn't guarantee returns in comparison to the level of money invested.

Cash budget : It determines the net inflow-outflow of cash transactions which will take

place in a period at Oshodi plc. This budget is prepared to ensure the liquidity position of the

company. The cash inflow & outflow includes revenues received, expenses incurred and loan

details of the business. Its advantage is that it defines the liquid position of the firm and gives

data about liquidity whereas its disadvantage is that it lowers the credit limit of the organisation.

M3. Analysing use of different planning tools and their application for developing and

forecasting budgets

Different sort of planning tools assisting in formulating different report budgets that

provide way to plan organisation's activities. These described budgets also help to set norms to

improve and maintain the efficiency of staff and whole company (Seal and Mattimoe, 2016). The

Oshodi Plc also using these as managerial process to face economic difficulties. Budgets defines

organisation's tasks and structures as per company's goals. As master budget, is prepared at the

end of accounting period to determine objectives of company and compute vital results.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.