Management Accounting: Systems, Reports, Costing, and Budgetary Tools

VerifiedAdded on 2020/07/23

|14

|3737

|43

Report

AI Summary

This report provides a comprehensive overview of management accounting, encompassing its systems, reports, and various costing methods. It begins by defining management accounting and its importance in organizational decision-making, emphasizing its distinction from financial accounting. The report then delves into the core components of management accounting systems, including cost accounting, inventory management, and value estimation frameworks. It explores different types of management accounting reports, such as performance reports, financial reports, and inventory management reports, highlighting their roles in evaluation, financial analysis, and operational control. Furthermore, the report offers a detailed comparison of marginal and absorption costing techniques, elucidating their applications in cost calculation and profit analysis. The report also examines budgetary tools and techniques to improve final outputs. Overall, the report aims to enhance the reader's understanding of management accounting principles and their practical applications in achieving organizational goals and objectives.

Management Accounting

Systems and its Applications

Systems and its Applications

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

P1. Management accounting and its systems..............................................................................1

P2 Management accounting reports............................................................................................3

P3 Marginal and absorption costing............................................................................................4

SECTION 2......................................................................................................................................7

P4 Budgetary tools......................................................................................................................7

P5 Techniques to improve final outputs.....................................................................................9

CONCLUSION..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

P1. Management accounting and its systems..............................................................................1

P2 Management accounting reports............................................................................................3

P3 Marginal and absorption costing............................................................................................4

SECTION 2......................................................................................................................................7

P4 Budgetary tools......................................................................................................................7

P5 Techniques to improve final outputs.....................................................................................9

CONCLUSION..............................................................................................................................10

INTRODUCTION

Management or managerial accounting is the process of recognising, classifying

recording and meditating the required information of company’s financial and non-financial

status to its different users. This data is provided by different managers that is further utilised by

management in the process of decision making. It is a distinct concept of financial accountancy

as it only gives the financial information to its user (Bodie, 2013). This system of accounting

ensures expertise in different reporting systems which further helps in achieving organisational

goals and objectives. The present report will discuss the related concepts of management

accounting which will enhance the knowledge of user regarding how it works and assist the firm

in reaching at desired standards. Apart from this, practical knowledge of how tools like marginal

and absorption costing help in formulating the financial statements will also be discussed in this

report.

SECTION 1

P1. Management accounting and its systems

Management accounting can be termed as a system that helps an organisation in carrying

out its operations with high efficiency and effectiveness. Through this system, the most suitable

options are selected from different alternatives which are implemented at workplace with a prime

goal of achieving competitive advantage (Otley, and Emmanuel, 2013). With the help of

different tools and techniques, evaluation and controlling process is carried out which ensures

optimum utilisation of resources. Its importance can be better understood in the following

manner:

Helps in taking judgements – While carrying out the daily operations, situation arises

where the authority needs to select one option from various available solutions. In this, it

has to be ensured that selected decision is the best among all others and should give

maximum advantage to the enterprise. System of administration accountancy plays a

great role in this. Information provided by it can assist concerned authority in knowing

the best suitable option that can give long term benefit to the firm.

Achieving task by setting targets through using budgetary tool – Under the system of

management accounting, different budgetary tools are used which further minimise the

1

Management or managerial accounting is the process of recognising, classifying

recording and meditating the required information of company’s financial and non-financial

status to its different users. This data is provided by different managers that is further utilised by

management in the process of decision making. It is a distinct concept of financial accountancy

as it only gives the financial information to its user (Bodie, 2013). This system of accounting

ensures expertise in different reporting systems which further helps in achieving organisational

goals and objectives. The present report will discuss the related concepts of management

accounting which will enhance the knowledge of user regarding how it works and assist the firm

in reaching at desired standards. Apart from this, practical knowledge of how tools like marginal

and absorption costing help in formulating the financial statements will also be discussed in this

report.

SECTION 1

P1. Management accounting and its systems

Management accounting can be termed as a system that helps an organisation in carrying

out its operations with high efficiency and effectiveness. Through this system, the most suitable

options are selected from different alternatives which are implemented at workplace with a prime

goal of achieving competitive advantage (Otley, and Emmanuel, 2013). With the help of

different tools and techniques, evaluation and controlling process is carried out which ensures

optimum utilisation of resources. Its importance can be better understood in the following

manner:

Helps in taking judgements – While carrying out the daily operations, situation arises

where the authority needs to select one option from various available solutions. In this, it

has to be ensured that selected decision is the best among all others and should give

maximum advantage to the enterprise. System of administration accountancy plays a

great role in this. Information provided by it can assist concerned authority in knowing

the best suitable option that can give long term benefit to the firm.

Achieving task by setting targets through using budgetary tool – Under the system of

management accounting, different budgetary tools are used which further minimise the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

total cost of company. Employees learn to work with the available resources which

further leads to optimum utilisation of finance and other material (Renz, 2016).

Different systems which work towards achieving the above mentioned advantages are as

follows:

Cost accounting framework: The main aim of an organisation is to use its finance in

such a manner that desired results are achieved as it has direct impact on the growth of an

organisation. Hence, this system is utilized so that improvements are done so effective

that working is made conceivable. The initial step is to quantify the stock by which its

worth can be determined. This will assist in cost keeping the cost related records that will

be recorded by supervisors further. This is helpful in controlling the general cost of item,

which is very much necessary in order to keep the total cost of production to minimum.

Stock administration system: Manufacturing process is carried out with the help of

stock and thus, it turns out to be particularly essential that it must be controlled by Nero

ltd. By this, change in operations will be accomplished and thus, it is required that stock

should be kept at the required level. For this financial request amount is to be computed

with the goal that most extreme preferred standpoint can be achieved. Both the situation

of excess and deficit is managed in an appropriate way with utilizing this framework

(Bodie, 2013).

Value estimating framework: This is critical as by the same, the cost to be charged is

estimated under this system. So it is important that appropriate investigation of different

components must be done and after that accordingly selection of alternative should be

done. The principle viewpoint to be included is what should be the apt price of a product

or service. This is on account of cost that might be such by which request can be

expanded and as there is opposite connection so on the off chance price needs to be kept

low so that costumers do not get effected much (Otley, and Emmanuel, 2013).

Job costing: In an organisation different functions are undertaken and for that it will be

required that recognizable importance should be analysed that what are most important

departments that cannot be discontinued. Few such perspectives which can be

disregarded and the cost which is caused in connection to them can be spared by

discontinuing same. The price shall be computed in total and after that, portion will be

made to each task which is performed in an organisation.

2

further leads to optimum utilisation of finance and other material (Renz, 2016).

Different systems which work towards achieving the above mentioned advantages are as

follows:

Cost accounting framework: The main aim of an organisation is to use its finance in

such a manner that desired results are achieved as it has direct impact on the growth of an

organisation. Hence, this system is utilized so that improvements are done so effective

that working is made conceivable. The initial step is to quantify the stock by which its

worth can be determined. This will assist in cost keeping the cost related records that will

be recorded by supervisors further. This is helpful in controlling the general cost of item,

which is very much necessary in order to keep the total cost of production to minimum.

Stock administration system: Manufacturing process is carried out with the help of

stock and thus, it turns out to be particularly essential that it must be controlled by Nero

ltd. By this, change in operations will be accomplished and thus, it is required that stock

should be kept at the required level. For this financial request amount is to be computed

with the goal that most extreme preferred standpoint can be achieved. Both the situation

of excess and deficit is managed in an appropriate way with utilizing this framework

(Bodie, 2013).

Value estimating framework: This is critical as by the same, the cost to be charged is

estimated under this system. So it is important that appropriate investigation of different

components must be done and after that accordingly selection of alternative should be

done. The principle viewpoint to be included is what should be the apt price of a product

or service. This is on account of cost that might be such by which request can be

expanded and as there is opposite connection so on the off chance price needs to be kept

low so that costumers do not get effected much (Otley, and Emmanuel, 2013).

Job costing: In an organisation different functions are undertaken and for that it will be

required that recognizable importance should be analysed that what are most important

departments that cannot be discontinued. Few such perspectives which can be

disregarded and the cost which is caused in connection to them can be spared by

discontinuing same. The price shall be computed in total and after that, portion will be

made to each task which is performed in an organisation.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2 Management accounting reports

Each department of an institution needs to prepare different reports which are a kind of

written document which contain all the quality information related to a particular section of an

organisation (Lee, 2011). It helps the management in taking different judgements at various

level which further contributes in better productivity by the whole organisation. Some of the

major reports prepared by the given enterprise are discussed below:

Execution report: In order to check the performance of different departmental sections

these reports are prepared which help in the process of evaluation. Through this it is

analysed that which section is performing good and which needs to be developed. This

way the overall productivity of an enterprise increases and hence growth can be

experienced.

Financial reports – It is another report which contain the detail of use of finance of a

particular period. Through this document it is identified that how much amount is

invested in a particular section and hence can be recognised that effective returns are

achieved or not.

Bills receivable report – This is a crucial record which has the information regarding the

present payments which are due but not received. Through this it can be given care that

from what all customers amount has to be collected and also helps in checking the credit

worthiness of different clients.

Inventory management report - In order to carry out daily operations stock needs to be

maintained. It is that report which keeps the record of present status of inventory with the

management. It is an important data as this helps management in taking decisions

regarding the future purchase of inventory. Apart from this situation related to the deficit

or excess can also be avoided through this which is very much necessary in order to

maintain the controlled cost of production (Burritt, and et.al., 2013).

Budget report – It is a written document that has the data for management so that it can

design budgets for different departments. It act as a guideline where need of each

function is given which is necessary to be analysed before setting limit for any particular

institution. Once the budget is prepared it is communicated to all so that accordingly

work cane be carried out by every departmental head (Nixon and Burns, 2012).

3

Each department of an institution needs to prepare different reports which are a kind of

written document which contain all the quality information related to a particular section of an

organisation (Lee, 2011). It helps the management in taking different judgements at various

level which further contributes in better productivity by the whole organisation. Some of the

major reports prepared by the given enterprise are discussed below:

Execution report: In order to check the performance of different departmental sections

these reports are prepared which help in the process of evaluation. Through this it is

analysed that which section is performing good and which needs to be developed. This

way the overall productivity of an enterprise increases and hence growth can be

experienced.

Financial reports – It is another report which contain the detail of use of finance of a

particular period. Through this document it is identified that how much amount is

invested in a particular section and hence can be recognised that effective returns are

achieved or not.

Bills receivable report – This is a crucial record which has the information regarding the

present payments which are due but not received. Through this it can be given care that

from what all customers amount has to be collected and also helps in checking the credit

worthiness of different clients.

Inventory management report - In order to carry out daily operations stock needs to be

maintained. It is that report which keeps the record of present status of inventory with the

management. It is an important data as this helps management in taking decisions

regarding the future purchase of inventory. Apart from this situation related to the deficit

or excess can also be avoided through this which is very much necessary in order to

maintain the controlled cost of production (Burritt, and et.al., 2013).

Budget report – It is a written document that has the data for management so that it can

design budgets for different departments. It act as a guideline where need of each

function is given which is necessary to be analysed before setting limit for any particular

institution. Once the budget is prepared it is communicated to all so that accordingly

work cane be carried out by every departmental head (Nixon and Burns, 2012).

3

Variance report – It is a special type of study which has the details of variations

observed in the final results. In order to minimise the deviations these reports are

prepared so that the changes can be identified and are minimised to minimum in future.

This way the results are achieved with greater efficiency

P3 Marginal and absorption costing

The procedure by which cost of any item might be computed is vital thus it is required

that the strategy that should be utilized for this ought to be chosen subsequent to making

legitimate investigation. The fundamental procedures which are determined in this regard are

marginal and absorption techniques. The cost which will be computed by them is extraordinary

and because of this reasons benefit that will be acquired by both is additionally unique as cost is

utilized as a part of the putting forth of expressions of wage. Both are strategies should be

appropriately comprehended by administration with the goal that they can be utilized as a part of

compelling way and for this clarification of same is given underneath:

Marginal costing: In this strategy just those parts of costs are considered which will vary

with the adjustment in units that are delivered (Ward, 2012). Such cost are known as

minor or changeable cost. Because of this they are gone up against per unit premise and

their impact can likewise be seen with only a unit change. Under this method cost which

can be designated on amount premise will be considered and ought to be deducted from

the estimation of offers which will give unicorn basic need the sum that has been earned

in type of commitment . The execution of organization can be checked with the thought

of it and afterwards so as to know the last pay that has been earned it is required that all

the cost that are settled and won't veer off should be decreased from the ascertained

esteem. There is immediate connection which exist among the two perspective that are

units and cost. It implies that if the creation is expanded by organization at that point cost

that will be brought about in type of variable components is additionally raised. So the

benefit is influenced to extraordinary degree by this and along these lines it is critical to

implement it in procedure of basic leadership (Parker, 2012).

Absorption costing: This is the system in which cost is divided on the premise of

permanent and variable cost is not made as all the settled cost will likewise be

apportioned on per unit premise and they are incorporated alongside the cost that are

evolving. As they are incorporated into regard of every unit so the sum utilized as a part

4

observed in the final results. In order to minimise the deviations these reports are

prepared so that the changes can be identified and are minimised to minimum in future.

This way the results are achieved with greater efficiency

P3 Marginal and absorption costing

The procedure by which cost of any item might be computed is vital thus it is required

that the strategy that should be utilized for this ought to be chosen subsequent to making

legitimate investigation. The fundamental procedures which are determined in this regard are

marginal and absorption techniques. The cost which will be computed by them is extraordinary

and because of this reasons benefit that will be acquired by both is additionally unique as cost is

utilized as a part of the putting forth of expressions of wage. Both are strategies should be

appropriately comprehended by administration with the goal that they can be utilized as a part of

compelling way and for this clarification of same is given underneath:

Marginal costing: In this strategy just those parts of costs are considered which will vary

with the adjustment in units that are delivered (Ward, 2012). Such cost are known as

minor or changeable cost. Because of this they are gone up against per unit premise and

their impact can likewise be seen with only a unit change. Under this method cost which

can be designated on amount premise will be considered and ought to be deducted from

the estimation of offers which will give unicorn basic need the sum that has been earned

in type of commitment . The execution of organization can be checked with the thought

of it and afterwards so as to know the last pay that has been earned it is required that all

the cost that are settled and won't veer off should be decreased from the ascertained

esteem. There is immediate connection which exist among the two perspective that are

units and cost. It implies that if the creation is expanded by organization at that point cost

that will be brought about in type of variable components is additionally raised. So the

benefit is influenced to extraordinary degree by this and along these lines it is critical to

implement it in procedure of basic leadership (Parker, 2012).

Absorption costing: This is the system in which cost is divided on the premise of

permanent and variable cost is not made as all the settled cost will likewise be

apportioned on per unit premise and they are incorporated alongside the cost that are

evolving. As they are incorporated into regard of every unit so the sum utilized as a part

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

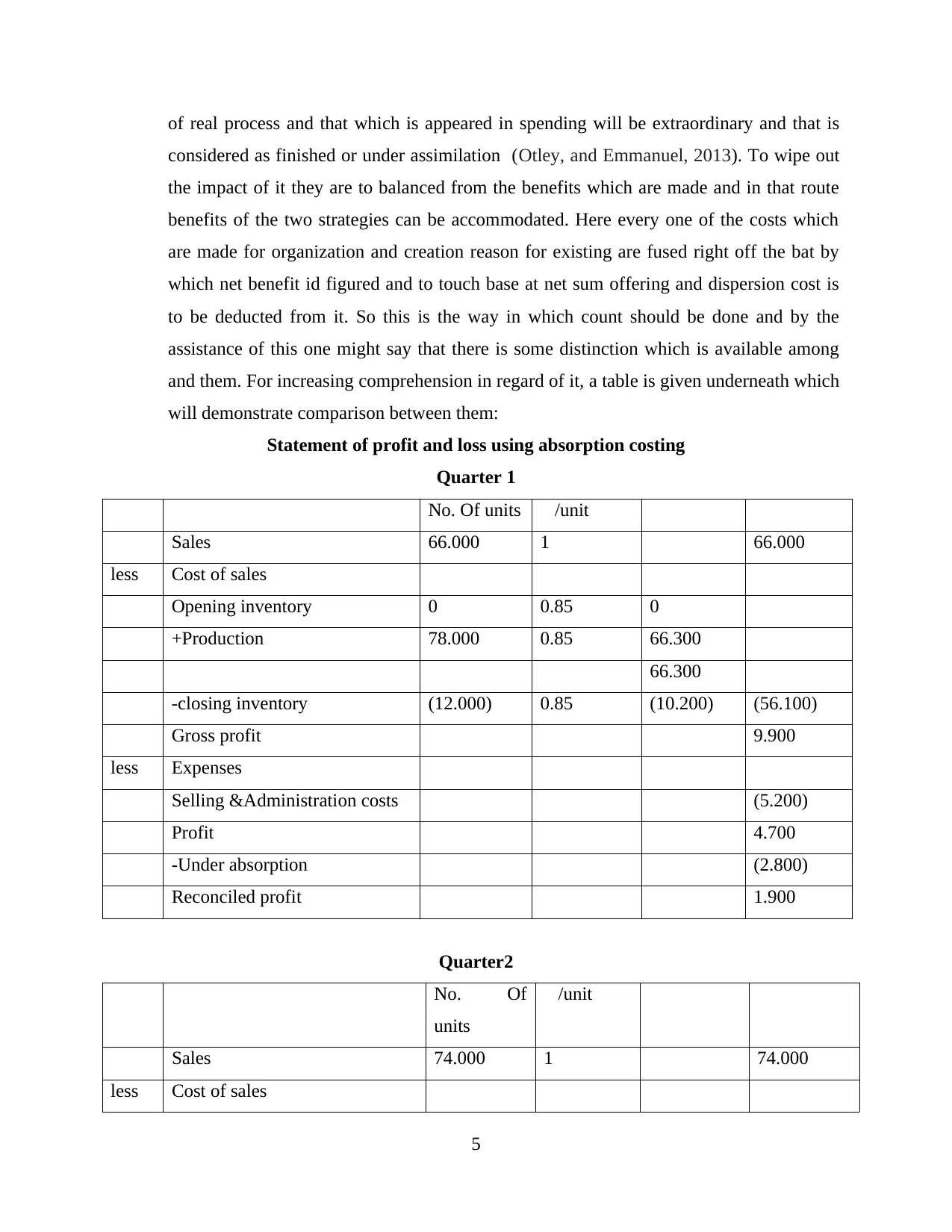

of real process and that which is appeared in spending will be extraordinary and that is

considered as finished or under assimilation (Otley, and Emmanuel, 2013). To wipe out

the impact of it they are to balanced from the benefits which are made and in that route

benefits of the two strategies can be accommodated. Here every one of the costs which

are made for organization and creation reason for existing are fused right off the bat by

which net benefit id figured and to touch base at net sum offering and dispersion cost is

to be deducted from it. So this is the way in which count should be done and by the

assistance of this one might say that there is some distinction which is available among

and them. For increasing comprehension in regard of it, a table is given underneath which

will demonstrate comparison between them:

Statement of profit and loss using absorption costing

Quarter 1

No. Of units £/unit £ £

Sales 66.000 1 66.000

less Cost of sales

Opening inventory 0 0.85 0

+Production 78.000 0.85 66.300

66.300

-closing inventory (12.000) 0.85 (10.200) (56.100)

Gross profit 9.900

less Expenses

Selling &Administration costs (5.200)

Profit 4.700

-Under absorption (2.800)

Reconciled profit 1.900

Quarter2

No. Of

units

£/unit £ £

Sales 74.000 1 74.000

less Cost of sales

5

considered as finished or under assimilation (Otley, and Emmanuel, 2013). To wipe out

the impact of it they are to balanced from the benefits which are made and in that route

benefits of the two strategies can be accommodated. Here every one of the costs which

are made for organization and creation reason for existing are fused right off the bat by

which net benefit id figured and to touch base at net sum offering and dispersion cost is

to be deducted from it. So this is the way in which count should be done and by the

assistance of this one might say that there is some distinction which is available among

and them. For increasing comprehension in regard of it, a table is given underneath which

will demonstrate comparison between them:

Statement of profit and loss using absorption costing

Quarter 1

No. Of units £/unit £ £

Sales 66.000 1 66.000

less Cost of sales

Opening inventory 0 0.85 0

+Production 78.000 0.85 66.300

66.300

-closing inventory (12.000) 0.85 (10.200) (56.100)

Gross profit 9.900

less Expenses

Selling &Administration costs (5.200)

Profit 4.700

-Under absorption (2.800)

Reconciled profit 1.900

Quarter2

No. Of

units

£/unit £ £

Sales 74.000 1 74.000

less Cost of sales

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

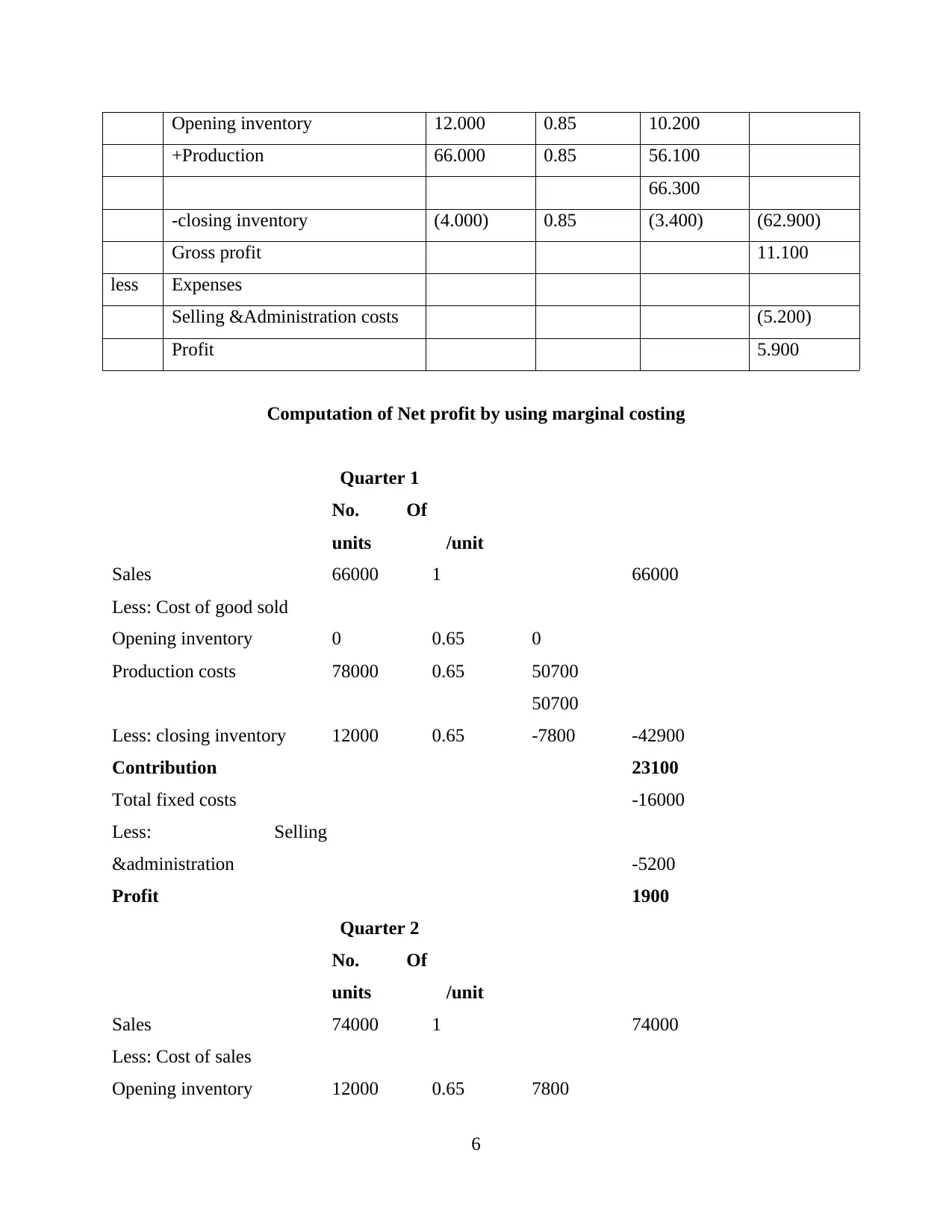

Opening inventory 12.000 0.85 10.200

+Production 66.000 0.85 56.100

66.300

-closing inventory (4.000) 0.85 (3.400) (62.900)

Gross profit 11.100

less Expenses

Selling &Administration costs (5.200)

Profit 5.900

Computation of Net profit by using marginal costing

Quarter 1

No. Of

units £/unit £ £

Sales 66000 1 66000

Less: Cost of good sold

Opening inventory 0 0.65 0

Production costs 78000 0.65 50700

50700

Less: closing inventory 12000 0.65 -7800 -42900

Contribution 23100

Total fixed costs -16000

Less: Selling

&administration -5200

Profit 1900

Quarter 2

No. Of

units £/unit £ £

Sales 74000 1 74000

Less: Cost of sales

Opening inventory 12000 0.65 7800

6

+Production 66.000 0.85 56.100

66.300

-closing inventory (4.000) 0.85 (3.400) (62.900)

Gross profit 11.100

less Expenses

Selling &Administration costs (5.200)

Profit 5.900

Computation of Net profit by using marginal costing

Quarter 1

No. Of

units £/unit £ £

Sales 66000 1 66000

Less: Cost of good sold

Opening inventory 0 0.65 0

Production costs 78000 0.65 50700

50700

Less: closing inventory 12000 0.65 -7800 -42900

Contribution 23100

Total fixed costs -16000

Less: Selling

&administration -5200

Profit 1900

Quarter 2

No. Of

units £/unit £ £

Sales 74000 1 74000

Less: Cost of sales

Opening inventory 12000 0.65 7800

6

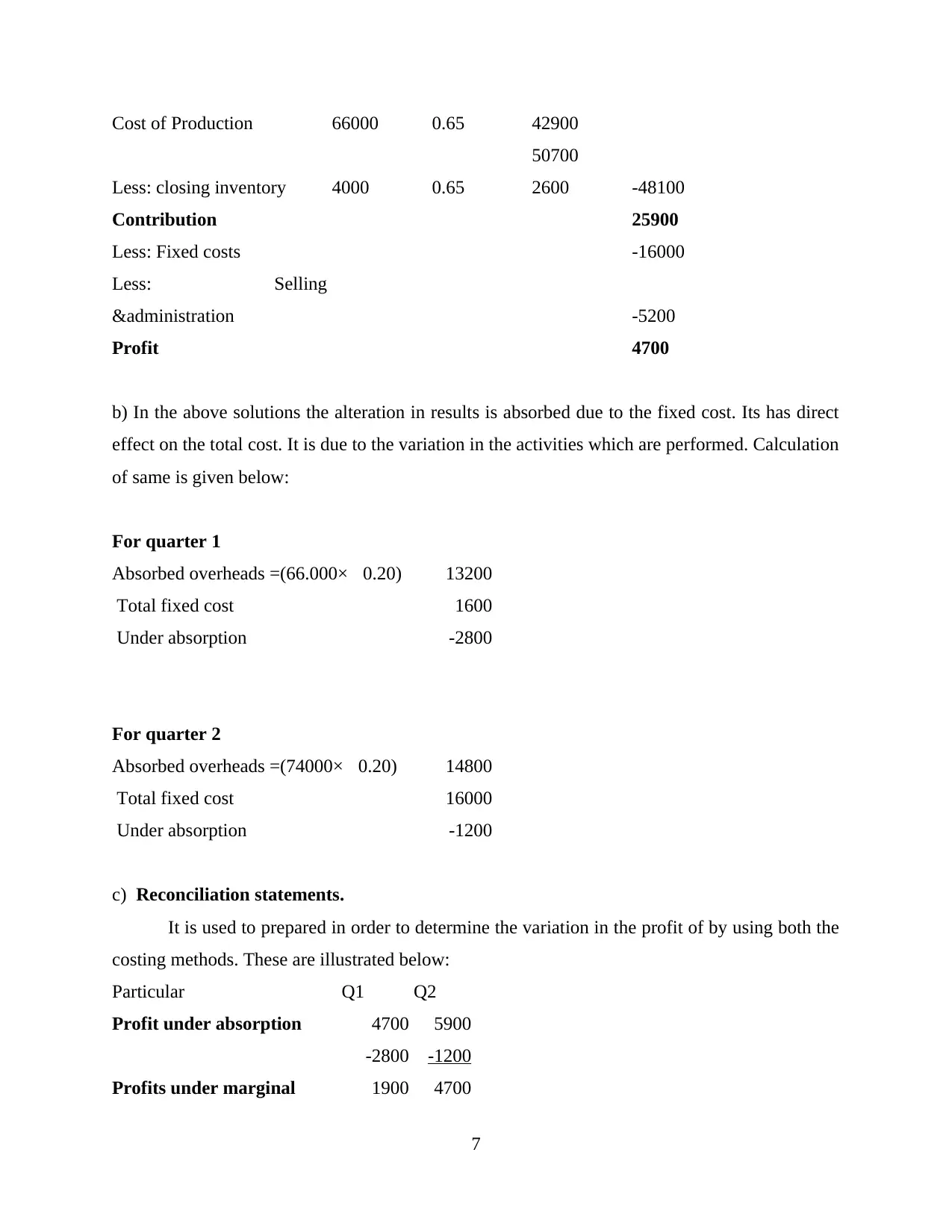

Cost of Production 66000 0.65 42900

50700

Less: closing inventory 4000 0.65 2600 -48100

Contribution 25900

Less: Fixed costs -16000

Less: Selling

&administration -5200

Profit 4700

b) In the above solutions the alteration in results is absorbed due to the fixed cost. Its has direct

effect on the total cost. It is due to the variation in the activities which are performed. Calculation

of same is given below:

For quarter 1

Absorbed overheads =(66.000×£0.20) 13200

Total fixed cost 1600

Under absorption -2800

For quarter 2

Absorbed overheads =(74000×£0.20) 14800

Total fixed cost 16000

Under absorption -1200

c) Reconciliation statements.

It is used to prepared in order to determine the variation in the profit of by using both the

costing methods. These are illustrated below:

Particular Q1 Q2

Profit under absorption 4700 5900

-2800 -1200

Profits under marginal 1900 4700

7

50700

Less: closing inventory 4000 0.65 2600 -48100

Contribution 25900

Less: Fixed costs -16000

Less: Selling

&administration -5200

Profit 4700

b) In the above solutions the alteration in results is absorbed due to the fixed cost. Its has direct

effect on the total cost. It is due to the variation in the activities which are performed. Calculation

of same is given below:

For quarter 1

Absorbed overheads =(66.000×£0.20) 13200

Total fixed cost 1600

Under absorption -2800

For quarter 2

Absorbed overheads =(74000×£0.20) 14800

Total fixed cost 16000

Under absorption -1200

c) Reconciliation statements.

It is used to prepared in order to determine the variation in the profit of by using both the

costing methods. These are illustrated below:

Particular Q1 Q2

Profit under absorption 4700 5900

-2800 -1200

Profits under marginal 1900 4700

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Working Note

a) Fixed cost =16.000 Total units = 66.000×0.20=13.200

Under absorption = (2.800)

b) With the same fixed cost of 16000 , total units of 74.000×0.20=14.800

Under absorption=1.200

SECTION 2

P4 Budgetary tools

In an organisation finance is the most important factor. Therefore, in order to take the

best use of same budgetary tools are utilised which helps in controlling the flow of cash in an

organisation. It is a best technique through which comparison is made possible which is crucial

for achieving the desired objectives and goals (Renz, 2016). There are a number of budgets

which are formed among which the most common one are as follows:

Income spending plan: This is made to recognize the requirements in regard of assets.

By this every one of the sources which are there and can be utilized to obtain money will

be utilized. The sum which is required is recognized ahead of time and by this issues

won't be confronted. All the work will be directed in way chose and furthermore

distribution will be made in viable way in which division is made on premise of need.

Static spending plan: This is the financial plan in which every one of the angles which

are incorporated will be settled that implies that all will stay same at any level of creation.

It won't be required to be altered as there are no progressions which are to be

consolidated under it. The measure of offers or some other wages and costs all will be

steady in it.

Zero based planning: The making of this includes every one of the sections should be

made, for example, they are from beginning stage (Bodie, 2013). It implies that every

one of the information will be expected to included from beginning and accordingly

parcel of research will be required as no data of past years is considered under it.

The negatives of the above given variety of budgets are as follows:

8

a) Fixed cost =16.000 Total units = 66.000×0.20=13.200

Under absorption = (2.800)

b) With the same fixed cost of 16000 , total units of 74.000×0.20=14.800

Under absorption=1.200

SECTION 2

P4 Budgetary tools

In an organisation finance is the most important factor. Therefore, in order to take the

best use of same budgetary tools are utilised which helps in controlling the flow of cash in an

organisation. It is a best technique through which comparison is made possible which is crucial

for achieving the desired objectives and goals (Renz, 2016). There are a number of budgets

which are formed among which the most common one are as follows:

Income spending plan: This is made to recognize the requirements in regard of assets.

By this every one of the sources which are there and can be utilized to obtain money will

be utilized. The sum which is required is recognized ahead of time and by this issues

won't be confronted. All the work will be directed in way chose and furthermore

distribution will be made in viable way in which division is made on premise of need.

Static spending plan: This is the financial plan in which every one of the angles which

are incorporated will be settled that implies that all will stay same at any level of creation.

It won't be required to be altered as there are no progressions which are to be

consolidated under it. The measure of offers or some other wages and costs all will be

steady in it.

Zero based planning: The making of this includes every one of the sections should be

made, for example, they are from beginning stage (Bodie, 2013). It implies that every

one of the information will be expected to included from beginning and accordingly

parcel of research will be required as no data of past years is considered under it.

The negatives of the above given variety of budgets are as follows:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. Complex process - The procedure which is included under it is exceptionally tedious as

extremely serious research is to be performed for this. Likewise part of assets are utilized

which could have been used for some other reason.

2. Risk of failure - The arrangement is made on premise of evaluations and there is no

surety that they will be precise so risks are there that wrong choices are made and this

expands the danger of business. The arrangement improves the situation for little period

thus this additionally may have negative mark as entire year is excluded. It might happen

that every one of the costs are excluded and some might be left for which no bookkeeping

is finished.

3. Reduces flexibility - There is no adaptability under this which is its bad mark as though

any extra deals is made then likewise no allotment is made for additional assets that are

required for it. The choice can't be taken to assign some extra assets to such range which

is in require and by this improvement of that section is hampered.

Apart from having the negatives this system has many positive effect too like:

1. Helps in planning for future - The principle justify is that every one of the necessities

which can emerge in not so distant future are resolved ahead of time thus assessment can

be made of different sources, for example, credits. By this it will likewise be

distinguished that whether there are any assets which are not used and afterwards

measures will be taken with the goal that they can be utilized as a part of best way by

putting them in some gainful viewpoint by which extra income will be made.

2. Allocation of resources - The information which is entered in this is most precise as all

is gathered from dependable sources and is than analysed. The assets under it are

designated in most legitimate way by which proficiency will be expanded. The level of

correspondence which is kept up among divisions will be enhanced with the utilization of

it.

3. Facilitates comparison – With the help of different accounting tools it become easy to

do the compression among the actual and desired results. When the final output is

received it is compared with the set standards through which deviations are observed

which further helps in evaluating the possible reasons of change in final output.

9

extremely serious research is to be performed for this. Likewise part of assets are utilized

which could have been used for some other reason.

2. Risk of failure - The arrangement is made on premise of evaluations and there is no

surety that they will be precise so risks are there that wrong choices are made and this

expands the danger of business. The arrangement improves the situation for little period

thus this additionally may have negative mark as entire year is excluded. It might happen

that every one of the costs are excluded and some might be left for which no bookkeeping

is finished.

3. Reduces flexibility - There is no adaptability under this which is its bad mark as though

any extra deals is made then likewise no allotment is made for additional assets that are

required for it. The choice can't be taken to assign some extra assets to such range which

is in require and by this improvement of that section is hampered.

Apart from having the negatives this system has many positive effect too like:

1. Helps in planning for future - The principle justify is that every one of the necessities

which can emerge in not so distant future are resolved ahead of time thus assessment can

be made of different sources, for example, credits. By this it will likewise be

distinguished that whether there are any assets which are not used and afterwards

measures will be taken with the goal that they can be utilized as a part of best way by

putting them in some gainful viewpoint by which extra income will be made.

2. Allocation of resources - The information which is entered in this is most precise as all

is gathered from dependable sources and is than analysed. The assets under it are

designated in most legitimate way by which proficiency will be expanded. The level of

correspondence which is kept up among divisions will be enhanced with the utilization of

it.

3. Facilitates comparison – With the help of different accounting tools it become easy to

do the compression among the actual and desired results. When the final output is

received it is compared with the set standards through which deviations are observed

which further helps in evaluating the possible reasons of change in final output.

9

P5 Techniques to improve final outputs

Business is completed and in that different operations are influenced so there are

constantly a few or different issues which to emerge and should be thought about (Lavia López

and Hiebl, 2014). The primary issues which are confronted will be identified with generation

productivity, or nature of items that are fabricated. Additionally at times issues emerge that are

identified with back. So keeping in mind the end goal to manage them it is required that every

one of the apparatuses and methods which are there might be assessed and afterward best among

them should be been utilized with the goal that appropriate arrangements can be made. Spending

plans is one such strategy that can be embraced as by that a level is settled by which organization

might play out its exercises and all the required subtle elements in regard of it are clarified

previously. Notwithstanding this there are some different instruments additionally which can be

utilized and they are as per the following:

Financial governance: There are some danger which are identified with finance and

each one of them will be taken care under this. The way in which reserves should be

taken into utilization will be distinguished and for this choices will be made. The

arrangements are detailed with the goal that they can be utilized and issues can be settled.

Benchmarks: The principles under this will be distinguished by making correlation with

those elements that are effective and have built up their position. The distinction will be

recognized and regions in which change is required will be as per the distinguished

guidelines.

Key performance indicators: In this representatives are furnished with specific targets

which are to be accomplished by them and along these lines they should work as per

them and this will build their productivity. Additionally there execution will be assessed

and if not discovered acceptable then new people will be enlisted.

CONCLUSION

From above report it has been summarised that effective management can be done with

the help of accounting system and goals can be achieved using tools and techniques provided

under management accounting system. Effective solutions are provided by the reports discussed

above and hence standard of output can be raised to a great level.

10

Business is completed and in that different operations are influenced so there are

constantly a few or different issues which to emerge and should be thought about (Lavia López

and Hiebl, 2014). The primary issues which are confronted will be identified with generation

productivity, or nature of items that are fabricated. Additionally at times issues emerge that are

identified with back. So keeping in mind the end goal to manage them it is required that every

one of the apparatuses and methods which are there might be assessed and afterward best among

them should be been utilized with the goal that appropriate arrangements can be made. Spending

plans is one such strategy that can be embraced as by that a level is settled by which organization

might play out its exercises and all the required subtle elements in regard of it are clarified

previously. Notwithstanding this there are some different instruments additionally which can be

utilized and they are as per the following:

Financial governance: There are some danger which are identified with finance and

each one of them will be taken care under this. The way in which reserves should be

taken into utilization will be distinguished and for this choices will be made. The

arrangements are detailed with the goal that they can be utilized and issues can be settled.

Benchmarks: The principles under this will be distinguished by making correlation with

those elements that are effective and have built up their position. The distinction will be

recognized and regions in which change is required will be as per the distinguished

guidelines.

Key performance indicators: In this representatives are furnished with specific targets

which are to be accomplished by them and along these lines they should work as per

them and this will build their productivity. Additionally there execution will be assessed

and if not discovered acceptable then new people will be enlisted.

CONCLUSION

From above report it has been summarised that effective management can be done with

the help of accounting system and goals can be achieved using tools and techniques provided

under management accounting system. Effective solutions are provided by the reports discussed

above and hence standard of output can be raised to a great level.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.