Management Accounting Report: R.L. Maynard Ltd. Financial Strategies

VerifiedAdded on 2020/10/22

|15

|5083

|343

Report

AI Summary

This report provides a detailed analysis of management accounting principles and their application within the context of R.L. Maynard Ltd., a construction and development company. The report covers various aspects of management accounting, including the essential requirements of management accounting systems, such as cost accounting, inventory management, and price optimization. It explores different types of management accounting reporting, including budget reports, account receivable reports, job cost reports, and inventory and manufacturing reports. The report also discusses the benefits of a management accounting system, emphasizing its role in improving efficiency, increasing profitability, and aiding in decision-making. Furthermore, it delves into the integration of management accounting systems and reporting, highlighting their importance in financial planning and performance evaluation. The report also calculates costs using marginal and absorption costing methods and analyzes budgetary control planning tools. Finally, it compares management accounting systems to resolve financial problems, analyzes financial problems leading to sustainable success, and evaluates financial planning tools for responding to financial issues.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting system and essential requirements of its types..............................1

P2 Management accounting reporting and its methods..............................................................2

M1 Benefits of management accounting system and application within the organisation.........4

D1 Integration of management accounting system and management accounting reporting.......4

TASK 2............................................................................................................................................5

P3: Calculation of cost using an appropriate techniques............................................................5

M2: Various types of accounting techniques..............................................................................7

D2: Data interpretation................................................................................................................8

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of Budgetary- control planning tools...................................8

M3 Analysis of different planning tools and their application for preparing and forecasting

budgets......................................................................................................................................10

TASK 4..........................................................................................................................................10

P5 comparison between organisations management accounting system to resolve financial

problems....................................................................................................................................10

M4 Analysing financial problem that can lead organisations to sustainable success...............11

D3: Evaluation of financial planning tools for responding financial issues.............................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting system and essential requirements of its types..............................1

P2 Management accounting reporting and its methods..............................................................2

M1 Benefits of management accounting system and application within the organisation.........4

D1 Integration of management accounting system and management accounting reporting.......4

TASK 2............................................................................................................................................5

P3: Calculation of cost using an appropriate techniques............................................................5

M2: Various types of accounting techniques..............................................................................7

D2: Data interpretation................................................................................................................8

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of Budgetary- control planning tools...................................8

M3 Analysis of different planning tools and their application for preparing and forecasting

budgets......................................................................................................................................10

TASK 4..........................................................................................................................................10

P5 comparison between organisations management accounting system to resolve financial

problems....................................................................................................................................10

M4 Analysing financial problem that can lead organisations to sustainable success...............11

D3: Evaluation of financial planning tools for responding financial issues.............................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is the activity of preparing management reports and accounts

that provide faithful financial information. It is assistive for management to report the accounting

methods, schemes and proficiency with particular cognition and quality, to exploit profit and

understate losses (Management Accounting, 2018). Planning tools for budgetary control are

helpful in estimating the future consequences and risk, and cater guidance to deal with the same.

There are many financial problems that a company is dealing, management has to implement

impressive techniques to deal with those financial problems to strengthen company's financial

perspective (Bennett, and James, 2017).

R.L. Maynard Ltd. was incorporated on 22 March 1973. It is a construction and

development company. The main motive of the company is to supply best service to the

customers and encourage the customers by providing best services and by environmental friendly

behaviour. This report is based on different financial management systems, and this report

includes various techniques of accounting, planning tools for budgetary control and solutions to

the financial problems.

TASK 1

P1 Management accounting system and essential requirements of its types

Management accounting system is the technique, which is used to achieve organisational

goals. It stipulates information to the managers to proceed financial decisions related to business.

It is used in the business activities like planning, controlling, staffing, directing and reporting. It

belongs to the insider system that R.L. Maynard Ltd. exercise to measure and assess its processes

for management of the organisation. Its elements are monetary funds, internal management

execution report, reports of the return on investment and sales investigation.

Cost accounting system – It is also known as product costing method or system, it is

enforced by the firms to measure cost of the product and outcome of the cost on the productivity.

A firm must have the idea of the product that product is profitable for firm or not. This system is

facilitative in calculating closing values of inventories, raw material, work in progress and

finished goods. There are two main types of cost accounting system :-

1

Management accounting is the activity of preparing management reports and accounts

that provide faithful financial information. It is assistive for management to report the accounting

methods, schemes and proficiency with particular cognition and quality, to exploit profit and

understate losses (Management Accounting, 2018). Planning tools for budgetary control are

helpful in estimating the future consequences and risk, and cater guidance to deal with the same.

There are many financial problems that a company is dealing, management has to implement

impressive techniques to deal with those financial problems to strengthen company's financial

perspective (Bennett, and James, 2017).

R.L. Maynard Ltd. was incorporated on 22 March 1973. It is a construction and

development company. The main motive of the company is to supply best service to the

customers and encourage the customers by providing best services and by environmental friendly

behaviour. This report is based on different financial management systems, and this report

includes various techniques of accounting, planning tools for budgetary control and solutions to

the financial problems.

TASK 1

P1 Management accounting system and essential requirements of its types

Management accounting system is the technique, which is used to achieve organisational

goals. It stipulates information to the managers to proceed financial decisions related to business.

It is used in the business activities like planning, controlling, staffing, directing and reporting. It

belongs to the insider system that R.L. Maynard Ltd. exercise to measure and assess its processes

for management of the organisation. Its elements are monetary funds, internal management

execution report, reports of the return on investment and sales investigation.

Cost accounting system – It is also known as product costing method or system, it is

enforced by the firms to measure cost of the product and outcome of the cost on the productivity.

A firm must have the idea of the product that product is profitable for firm or not. This system is

facilitative in calculating closing values of inventories, raw material, work in progress and

finished goods. There are two main types of cost accounting system :-

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job order costing – It is an action of distributing cost to a particular unit or product. This

method is only used when the products, produced are adequately different from each

other. This is exclusively applied in the small bulk of products that are clearly different

form the other bulk's products.

Process costing – It is used in R.L. Maynard Ltd. to elaborate a method for assembling

and distributing production costs to the units produced. It assigns cost to the collective

abstraction of a product.

Inventory management system – It is an activity of moving parts and products into and

extinct of the firm's location. It is used for tracking, predicting and reordering inventories in R.L.

Maynard Ltd, and it covers every part of production. It is used to keep an eye on every activity

that is happing in and out of the business unit, and it helps to make better decisions and

investments. Various inventory handler focus on various parts of the activity series in this

system. It is principally used to keep elaborated evidence of each and every action of the

firm(Bovens, Goodin, and Schillemans, 2014).

Price optimisation system – This system is used in R.L. Maynard Ltd. to find out that

how customers will react to the various values for products and services through different

transmission. It is also used to regulate that when the firm will achieve its goals such as

maximising profits and minimising losses.

Job costing system – It is competent to evidence the cost of materials that are divided

during instruction of the job in R.L. Maynard Ltd. It concerns the procedure of collecting content

about the cost related to a specific production or job, and this content is needed in state to refer

cost substance to a customer under an agreement where costs are compensated.

P2 Management accounting reporting and its methods

Management accounting reports are such form of reports that have flooded information of

the business performance. These reports are prepared to yield a holistic position of the business

economics. These reports provide information to lean cost, reinforce employees for the foremost

presentation, spend in such securities that return to the highest degree, cut weaken product lines

etc. These reports should be prepared accurately because many important decisions reckon on

these reports. There are four types of management account reporting, these are as follows :-

Budget report – These reports are generated as a whole for organisation and are very

important in analysing its performance. R.L. Maynard Ltd. creates an entire budget to interpret

2

method is only used when the products, produced are adequately different from each

other. This is exclusively applied in the small bulk of products that are clearly different

form the other bulk's products.

Process costing – It is used in R.L. Maynard Ltd. to elaborate a method for assembling

and distributing production costs to the units produced. It assigns cost to the collective

abstraction of a product.

Inventory management system – It is an activity of moving parts and products into and

extinct of the firm's location. It is used for tracking, predicting and reordering inventories in R.L.

Maynard Ltd, and it covers every part of production. It is used to keep an eye on every activity

that is happing in and out of the business unit, and it helps to make better decisions and

investments. Various inventory handler focus on various parts of the activity series in this

system. It is principally used to keep elaborated evidence of each and every action of the

firm(Bovens, Goodin, and Schillemans, 2014).

Price optimisation system – This system is used in R.L. Maynard Ltd. to find out that

how customers will react to the various values for products and services through different

transmission. It is also used to regulate that when the firm will achieve its goals such as

maximising profits and minimising losses.

Job costing system – It is competent to evidence the cost of materials that are divided

during instruction of the job in R.L. Maynard Ltd. It concerns the procedure of collecting content

about the cost related to a specific production or job, and this content is needed in state to refer

cost substance to a customer under an agreement where costs are compensated.

P2 Management accounting reporting and its methods

Management accounting reports are such form of reports that have flooded information of

the business performance. These reports are prepared to yield a holistic position of the business

economics. These reports provide information to lean cost, reinforce employees for the foremost

presentation, spend in such securities that return to the highest degree, cut weaken product lines

etc. These reports should be prepared accurately because many important decisions reckon on

these reports. There are four types of management account reporting, these are as follows :-

Budget report – These reports are generated as a whole for organisation and are very

important in analysing its performance. R.L. Maynard Ltd. creates an entire budget to interpret

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

heroic strategy of its business. These reports are supported by former experiences. It assists the

mangers to interpret and control costs crosswise the firm. Executives of the firm also use budget

reports to provide incentives to employees, and budget funds may be granted out as bonuses to

employees for achieving peculiar financial goals. Financial data recorded in budget reports, that's

why these reports are also called financial reports. A budget report usually elaborated document

but the report can be concise or simple it depends on the proprietor of the business.

Account receivable report – These reports are made by R.L. Maynard Ltd. to take an

summary of credit balances according to date. It helps to set credit policies to match them with

customer's refund capacity. It is helpful for the managers to discover difficulty with the firm's

accumulation operation. If there are huge number of customers who are incapable to pay their

credit, then the firm require to stiffen its credit policies. It always helps the aggregation division

from dominating old debts. This report also provide substance regarding the average aggregation

period of time which shows the number of days for collection of owed. Receivables are reasoned

as the possession of the business and because it have the worth. This report is the primary tool

implemented by the collection department to determine that which account is delinquent of

payment(Bryer, 2013.).

Job cost report – This report show detriment for a particular project supported by R.L.

Maynard Ltd. These are commonly compatible with an approximation of revenue so firm can

appraise the job's earnings. These reports render an accurate position of the total cost

accumulated in a single project compared to the anticipated revenue issued by that project. These

reports are assistive for the managers to measure the lucrativeness of particular type of jobs and

modify their operations by concentrating on activities that are atypically the most profitable as a

whole. This is helpful in identifying the maximum earning arena in the business so that firm can

centre extra attempts there rather than wasting time and monitory resources on jobs with

degraded profitability.

Inventory and manufacturing report – These reports are valuable to R.L. Maynard

Ltd. to manufacture product with a low fault. It helps to modify aggregation on product costs,

labour and different forms of expenditures involved in the operation, supplying unprocessed data

to optimize equipments. It is also implemented to compare assorted assembly lines inside the

enterprise to highlight field for modification. It is also helpful in evaluating best performance

departments to offer incentives and bonuses. Managers exercise these reports to sort central

3

mangers to interpret and control costs crosswise the firm. Executives of the firm also use budget

reports to provide incentives to employees, and budget funds may be granted out as bonuses to

employees for achieving peculiar financial goals. Financial data recorded in budget reports, that's

why these reports are also called financial reports. A budget report usually elaborated document

but the report can be concise or simple it depends on the proprietor of the business.

Account receivable report – These reports are made by R.L. Maynard Ltd. to take an

summary of credit balances according to date. It helps to set credit policies to match them with

customer's refund capacity. It is helpful for the managers to discover difficulty with the firm's

accumulation operation. If there are huge number of customers who are incapable to pay their

credit, then the firm require to stiffen its credit policies. It always helps the aggregation division

from dominating old debts. This report also provide substance regarding the average aggregation

period of time which shows the number of days for collection of owed. Receivables are reasoned

as the possession of the business and because it have the worth. This report is the primary tool

implemented by the collection department to determine that which account is delinquent of

payment(Bryer, 2013.).

Job cost report – This report show detriment for a particular project supported by R.L.

Maynard Ltd. These are commonly compatible with an approximation of revenue so firm can

appraise the job's earnings. These reports render an accurate position of the total cost

accumulated in a single project compared to the anticipated revenue issued by that project. These

reports are assistive for the managers to measure the lucrativeness of particular type of jobs and

modify their operations by concentrating on activities that are atypically the most profitable as a

whole. This is helpful in identifying the maximum earning arena in the business so that firm can

centre extra attempts there rather than wasting time and monitory resources on jobs with

degraded profitability.

Inventory and manufacturing report – These reports are valuable to R.L. Maynard

Ltd. to manufacture product with a low fault. It helps to modify aggregation on product costs,

labour and different forms of expenditures involved in the operation, supplying unprocessed data

to optimize equipments. It is also implemented to compare assorted assembly lines inside the

enterprise to highlight field for modification. It is also helpful in evaluating best performance

departments to offer incentives and bonuses. Managers exercise these reports to sort central

3

strategic determination about the future of the firm. This report is mainly related to the inventory

status and secondly related to the firm's profitability and productivity(Bui, and De Villiers,

2017).

M1 Benefits of management accounting system and application within the organisation

There are many benefits of management accounting system, it is helpful in increasing the

efficiency of R.L. Maynard Ltd. in performing tasks, by contributing in striving for improved

presentation. It increases the bar of profitability for the firm by budgetary control and capital

budgeting, and alter the decision devising of financial statements. It provides cost transparency,

adaptability, freedom and provide assistance in goal completion of the firm. It is an advanced

technique which is used by R.L. Maynard Ltd. to make future articulation from foregone

consequence and also implementable in marginal costing.

D1 Integration of management accounting system and management accounting reporting

Management accounting system and its reporting both are used in R.L. Maynard Ltd. to

deal with financial consequences, to predict future conditions and these are also helpful in

evaluating employees performance at work. These are the techniques which are used to

determine the cost involved in the production and also implemented to get the accurate insider

information of the business to provide strength to the business's financial condition. Management

accounting reporting is used by R.L. Maynard Ltd. to prepare various type of reports like budget

report, account receivable report, job cost report and manufacturing reports to get the

information of the firm (Zoni, Dossi, and Morelli, 2012).

4

status and secondly related to the firm's profitability and productivity(Bui, and De Villiers,

2017).

M1 Benefits of management accounting system and application within the organisation

There are many benefits of management accounting system, it is helpful in increasing the

efficiency of R.L. Maynard Ltd. in performing tasks, by contributing in striving for improved

presentation. It increases the bar of profitability for the firm by budgetary control and capital

budgeting, and alter the decision devising of financial statements. It provides cost transparency,

adaptability, freedom and provide assistance in goal completion of the firm. It is an advanced

technique which is used by R.L. Maynard Ltd. to make future articulation from foregone

consequence and also implementable in marginal costing.

D1 Integration of management accounting system and management accounting reporting

Management accounting system and its reporting both are used in R.L. Maynard Ltd. to

deal with financial consequences, to predict future conditions and these are also helpful in

evaluating employees performance at work. These are the techniques which are used to

determine the cost involved in the production and also implemented to get the accurate insider

information of the business to provide strength to the business's financial condition. Management

accounting reporting is used by R.L. Maynard Ltd. to prepare various type of reports like budget

report, account receivable report, job cost report and manufacturing reports to get the

information of the firm (Zoni, Dossi, and Morelli, 2012).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

P3: Calculation of cost using an appropriate techniques

Cost: It refers to the amount of money that an organisation invest or spend to create or

produce something such as products and services. It doesn't include only monetary amount but

also includes valuation of efforts, resources utilised, time and utilities, risk etc. which are

required to invest so as to execute business activities in an effective and efficient manner. To

determine the net profitability of company, the management have two costing methods such as

absorption and marginal costing method (Burkert,and Lueg, 2013).

RL Maynard is a construction company due to which it is important for them to manage

and allocate cost to different project activities so that while calculating net profitability the

overall incurred cost are easily determined. Purchasing raw materials, hiring labours,

transportations etc. required huge cost amount thus it is essential for RL Maynard to proper

allocate the cost so that the chances of increasing wastage will be very low. There are mainly two

costing method which are more helpful in calculating net profitability of company such as

marginal and absorption costing methods. It is briefly described under the below:

Marginal costing:

It is a method which consider only variable cost while determining the net profitability of

company. It is also known as variable cost due to inclusion of labour and material costs in

addition with estimated portion of fixed cost. Most of the organisations mainly adopted such

costing method due to increment in net profitability as compared with using absorption costing

method.

Absorption costing:

In this method, both variable and fixed cost are includes due to which the net profitability

of company are affected. It is needed to Generally Accepted Accounting Principles (GAAP)

external reporting. Such costing method includes wages cost, raw materials used and overhead

costs. It lowers the profit due to which less preferred to adopt by an organisation.

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

5

P3: Calculation of cost using an appropriate techniques

Cost: It refers to the amount of money that an organisation invest or spend to create or

produce something such as products and services. It doesn't include only monetary amount but

also includes valuation of efforts, resources utilised, time and utilities, risk etc. which are

required to invest so as to execute business activities in an effective and efficient manner. To

determine the net profitability of company, the management have two costing methods such as

absorption and marginal costing method (Burkert,and Lueg, 2013).

RL Maynard is a construction company due to which it is important for them to manage

and allocate cost to different project activities so that while calculating net profitability the

overall incurred cost are easily determined. Purchasing raw materials, hiring labours,

transportations etc. required huge cost amount thus it is essential for RL Maynard to proper

allocate the cost so that the chances of increasing wastage will be very low. There are mainly two

costing method which are more helpful in calculating net profitability of company such as

marginal and absorption costing methods. It is briefly described under the below:

Marginal costing:

It is a method which consider only variable cost while determining the net profitability of

company. It is also known as variable cost due to inclusion of labour and material costs in

addition with estimated portion of fixed cost. Most of the organisations mainly adopted such

costing method due to increment in net profitability as compared with using absorption costing

method.

Absorption costing:

In this method, both variable and fixed cost are includes due to which the net profitability

of company are affected. It is needed to Generally Accepted Accounting Principles (GAAP)

external reporting. Such costing method includes wages cost, raw materials used and overhead

costs. It lowers the profit due to which less preferred to adopt by an organisation.

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200 + 1200 + 1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break even analysis: Such analysis is done in order to determine the need of RL

Maynard that how much they desire to sell their products and services on monthly or annually

basis so as to cover their cost invested in doing business. It refers to the point at which revenue

received equals the cost incurred in receiving revenue (Edwards, and Boyns, 2012).

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

c. Calculation for getting desire profit of 10,000

6

16) 3200

Contribution 23400

Fixed cost ( 3200 + 1200 + 1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break even analysis: Such analysis is done in order to determine the need of RL

Maynard that how much they desire to sell their products and services on monthly or annually

basis so as to cover their cost invested in doing business. It refers to the point at which revenue

received equals the cost incurred in receiving revenue (Edwards, and Boyns, 2012).

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

c. Calculation for getting desire profit of 10,000

6

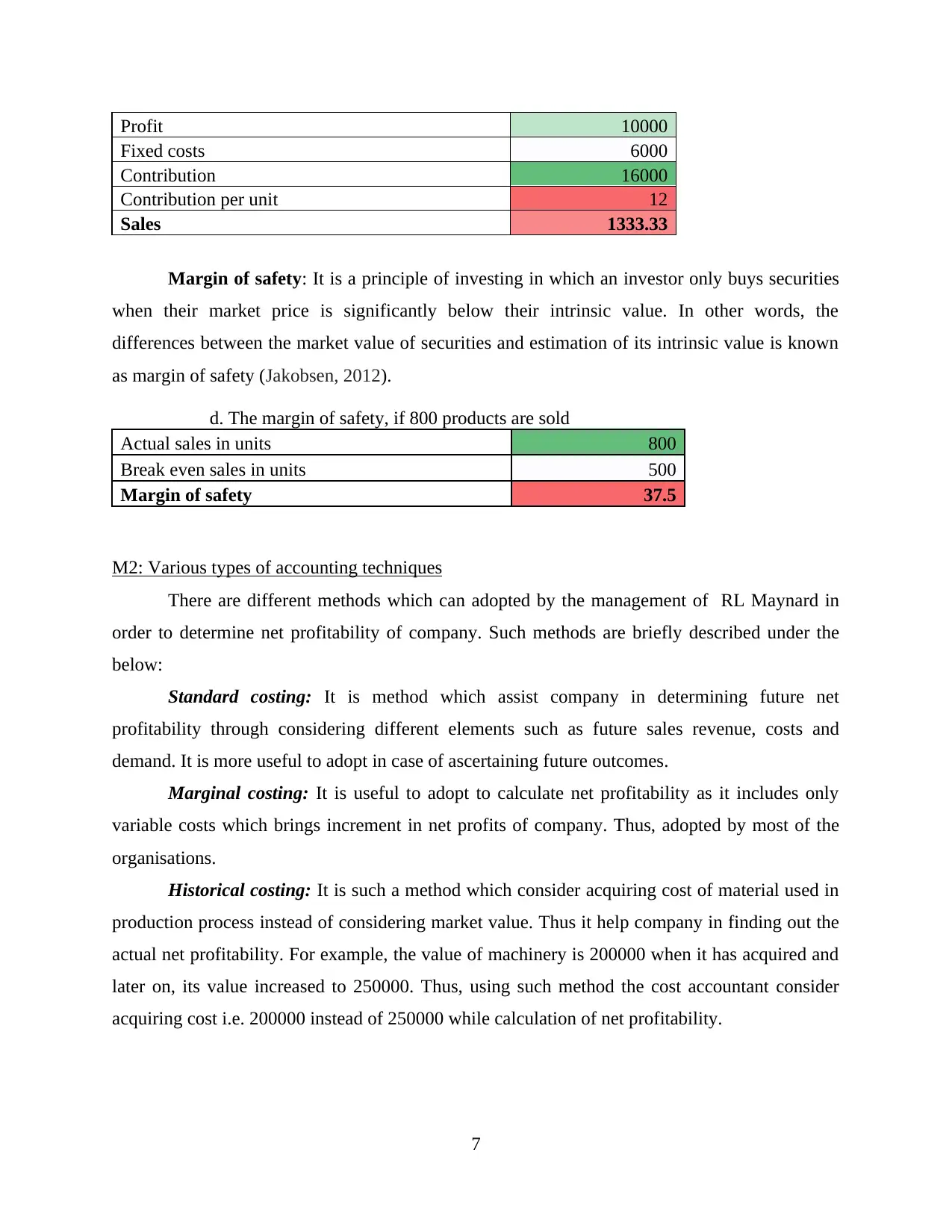

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: It is a principle of investing in which an investor only buys securities

when their market price is significantly below their intrinsic value. In other words, the

differences between the market value of securities and estimation of its intrinsic value is known

as margin of safety (Jakobsen, 2012).

d. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2: Various types of accounting techniques

There are different methods which can adopted by the management of RL Maynard in

order to determine net profitability of company. Such methods are briefly described under the

below:

Standard costing: It is method which assist company in determining future net

profitability through considering different elements such as future sales revenue, costs and

demand. It is more useful to adopt in case of ascertaining future outcomes.

Marginal costing: It is useful to adopt to calculate net profitability as it includes only

variable costs which brings increment in net profits of company. Thus, adopted by most of the

organisations.

Historical costing: It is such a method which consider acquiring cost of material used in

production process instead of considering market value. Thus it help company in finding out the

actual net profitability. For example, the value of machinery is 200000 when it has acquired and

later on, its value increased to 250000. Thus, using such method the cost accountant consider

acquiring cost i.e. 200000 instead of 250000 while calculation of net profitability.

7

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: It is a principle of investing in which an investor only buys securities

when their market price is significantly below their intrinsic value. In other words, the

differences between the market value of securities and estimation of its intrinsic value is known

as margin of safety (Jakobsen, 2012).

d. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2: Various types of accounting techniques

There are different methods which can adopted by the management of RL Maynard in

order to determine net profitability of company. Such methods are briefly described under the

below:

Standard costing: It is method which assist company in determining future net

profitability through considering different elements such as future sales revenue, costs and

demand. It is more useful to adopt in case of ascertaining future outcomes.

Marginal costing: It is useful to adopt to calculate net profitability as it includes only

variable costs which brings increment in net profits of company. Thus, adopted by most of the

organisations.

Historical costing: It is such a method which consider acquiring cost of material used in

production process instead of considering market value. Thus it help company in finding out the

actual net profitability. For example, the value of machinery is 200000 when it has acquired and

later on, its value increased to 250000. Thus, using such method the cost accountant consider

acquiring cost i.e. 200000 instead of 250000 while calculation of net profitability.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

D2: Data interpretation

As per the above calculation, it has been seen that marginal costing method will be more

profitable to RL Maynard as compared with absorption costing method. This is because of

increment in profit while using marginal costing method. While calculating net profitability, the

marginal costing method calculates £17500 as profit whereas absorption costing method

calculates £15675 as profit. Thus, the differences of £9600 in profit comes due to changing in

variable cost. In Break even, the total number of units sold are 500 and total amount of sales

revenue to achieve break even is 20000. Thus, to earn minimum profit of £1000, RL Maynard

need to achieve sales revenue of £1333.33. MOS is 37.5 when 800 products are sold.

TASK 3

P4 Advantages and disadvantages of Budgetary- control planning tools

Budgetary control is a systematic approach where actual inflows and outflows are

compared with planned inflows and outflows, so that management can identify whether their

plans are properly implemented or not and if they need any alterations to arise profits. R. L.

Maynard limited needs a efficient budgetary control process to set operational and financial

objectives (Lee, 2012). The process of budgetary control includes creation of budgets by

preparing organisation chart, budget centre and budget manual, period, committee and key

factors which used in comparing, analyse and interpretation of budgets to achieving goals on

time. Contingency, forecasting and scenario planning are the budgetary control planning tools

and are explained below:

Contingency Planning: It is a planning techniques used as risk management based on

an unexpected outcomes other than expected plan. This tool designed to help an organisation for

effective working for future uncertain events. R. L. Maynard limited uses this planning tool as a

safe side against the occurrence of emergency or unexpected events that may arise between

company operations.

Advantages: Contingency tool helps company in minimization the loss of production by

running continue production in spite of unexpected circumstances. Managers need not to

wait for instructions in emergency cases and move frequently towards activate actions

without any crisis. It is a best type of budgetary control tool which emphases on the

importance of a better decision making. It is a task and people oriented technique.

8

As per the above calculation, it has been seen that marginal costing method will be more

profitable to RL Maynard as compared with absorption costing method. This is because of

increment in profit while using marginal costing method. While calculating net profitability, the

marginal costing method calculates £17500 as profit whereas absorption costing method

calculates £15675 as profit. Thus, the differences of £9600 in profit comes due to changing in

variable cost. In Break even, the total number of units sold are 500 and total amount of sales

revenue to achieve break even is 20000. Thus, to earn minimum profit of £1000, RL Maynard

need to achieve sales revenue of £1333.33. MOS is 37.5 when 800 products are sold.

TASK 3

P4 Advantages and disadvantages of Budgetary- control planning tools

Budgetary control is a systematic approach where actual inflows and outflows are

compared with planned inflows and outflows, so that management can identify whether their

plans are properly implemented or not and if they need any alterations to arise profits. R. L.

Maynard limited needs a efficient budgetary control process to set operational and financial

objectives (Lee, 2012). The process of budgetary control includes creation of budgets by

preparing organisation chart, budget centre and budget manual, period, committee and key

factors which used in comparing, analyse and interpretation of budgets to achieving goals on

time. Contingency, forecasting and scenario planning are the budgetary control planning tools

and are explained below:

Contingency Planning: It is a planning techniques used as risk management based on

an unexpected outcomes other than expected plan. This tool designed to help an organisation for

effective working for future uncertain events. R. L. Maynard limited uses this planning tool as a

safe side against the occurrence of emergency or unexpected events that may arise between

company operations.

Advantages: Contingency tool helps company in minimization the loss of production by

running continue production in spite of unexpected circumstances. Managers need not to

wait for instructions in emergency cases and move frequently towards activate actions

without any crisis. It is a best type of budgetary control tool which emphases on the

importance of a better decision making. It is a task and people oriented technique.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Disadvantages: This approach is simple as manager need to work according to the

situation but when he apply this tool into practical situation he finds contingency as a

complex tool because while dealing with situation one may ignore other variable factors .

Forecasting Planning: In this tool company uses a forecasting model to examine fiscal

conditions which is helpful in making prediction for future based on past and present analysis of

information and trends. There are various forecasting methods like qualitative and quantitative

approach, average, time series, judgemental, artificial intelligence, drift method and seasonal

approach and many more. These methods are very useful in taking decisions regarding planning

of production, distribution and estimation of future growth. R. L. Maynard limited uses

forecasting technique to determine their revenue and compare with budgeted (Youssef, 2013).

Advantages: Forecasting method used by R. L. Maynard limited helps in its operations

and evaluate potential outcomes that organisation is using in decision making by

providing valuable information and uses quantitative and qualitative data for forecasting

that helps in determination of actions which bring favourable outcomes and avoid

unsuccessful scenarios based on forecasting.

Disadvantages: No one is sure about future events and the important disadvantage of

forecasting is similar as other methods of future prediction. Any unexpected components

can make a forecasting method unprofitable.

Scenario Planning: This planning tool is opted by various companies to make a long

term flexible plan. Scenario panning set a guidelines for company on the basis of historical data,

statistical analysis to become popular and unique in fast growing world. R. L. Maynard limited

develops strategy in a well organised way so that they can change it according to the situation for

assembling options and creating possible future. This approach combines various facts regarding

future like political, demographics, industrial information and resources reserves, with important

forces identified by different trends (Ossadnik, and Kaspar, 2013.).

Advantages: Scenario approach do not explain just one future but upcoming years future

also as accurate as possible. It is an appropriate method used by R. L. Maynard limited to

recognise weak points or disruptive events and considered them into long term planning.

Scenario are very flexible and can be applied to specific situation.

9

situation but when he apply this tool into practical situation he finds contingency as a

complex tool because while dealing with situation one may ignore other variable factors .

Forecasting Planning: In this tool company uses a forecasting model to examine fiscal

conditions which is helpful in making prediction for future based on past and present analysis of

information and trends. There are various forecasting methods like qualitative and quantitative

approach, average, time series, judgemental, artificial intelligence, drift method and seasonal

approach and many more. These methods are very useful in taking decisions regarding planning

of production, distribution and estimation of future growth. R. L. Maynard limited uses

forecasting technique to determine their revenue and compare with budgeted (Youssef, 2013).

Advantages: Forecasting method used by R. L. Maynard limited helps in its operations

and evaluate potential outcomes that organisation is using in decision making by

providing valuable information and uses quantitative and qualitative data for forecasting

that helps in determination of actions which bring favourable outcomes and avoid

unsuccessful scenarios based on forecasting.

Disadvantages: No one is sure about future events and the important disadvantage of

forecasting is similar as other methods of future prediction. Any unexpected components

can make a forecasting method unprofitable.

Scenario Planning: This planning tool is opted by various companies to make a long

term flexible plan. Scenario panning set a guidelines for company on the basis of historical data,

statistical analysis to become popular and unique in fast growing world. R. L. Maynard limited

develops strategy in a well organised way so that they can change it according to the situation for

assembling options and creating possible future. This approach combines various facts regarding

future like political, demographics, industrial information and resources reserves, with important

forces identified by different trends (Ossadnik, and Kaspar, 2013.).

Advantages: Scenario approach do not explain just one future but upcoming years future

also as accurate as possible. It is an appropriate method used by R. L. Maynard limited to

recognise weak points or disruptive events and considered them into long term planning.

Scenario are very flexible and can be applied to specific situation.

9

Disadvantages: The use of this approach can change the culture of organisation by

opening their minds to uncertainty, impossible possibilities and compelling its

management to rethink over their strategies.

M3 Analysis of different planning tools and their application for preparing and forecasting

budgets

All budgetary control planning tools helps R. L. Maynard limited in overall performance

by organising, directing, controlling and operating proper planning in the financial period. These

tools are implemented for achieving estimated target for proper decision making which is

fruitful for management growth.

TASK 4

P5 comparison between organisations management accounting system to resolve financial

problems

Financial problems is a state where shortage of money causes stress and worries in the

functioning of organisation. Many organisation are facing financial problems like payments after

due date, insufficient financial resources, cash flows, financial market instability, debt recovery,

funding etc. which impact on the working of organisation so it is better to overcome from the

problem now before it gets worse. R. L. Maynard limited is facing many problems related to

finance such that delay in construction projects and high employee turnover. Benchmarking, key

performance indicators, financial planning, statistical or graphical presentation, analysis of

financial statements through ratio analysis, Financial governance etc. are various management

accounting tools to respond company's financial problems without any delays (Schaltegger, and

Burritt, 2017). Some of them are mention below:

Key Performance Indicators: This approach is used to determine effective and efficient

working of organisation to achieve strategic organisation objectives. Company is using multiple

levels of KPI to measure their progress targets. KPI at high level focuses on overall performance

of the company but KPI at low level focus on departmental and operational processes. It's point

of measures are elements of a state which includes input indicators, output of activities, control

over production and mechanism which helps in periodically measurement of organisations and

their departments performance. There are two types of KPI 'leading indicators' and 'lagging

indicators'.

10

opening their minds to uncertainty, impossible possibilities and compelling its

management to rethink over their strategies.

M3 Analysis of different planning tools and their application for preparing and forecasting

budgets

All budgetary control planning tools helps R. L. Maynard limited in overall performance

by organising, directing, controlling and operating proper planning in the financial period. These

tools are implemented for achieving estimated target for proper decision making which is

fruitful for management growth.

TASK 4

P5 comparison between organisations management accounting system to resolve financial

problems

Financial problems is a state where shortage of money causes stress and worries in the

functioning of organisation. Many organisation are facing financial problems like payments after

due date, insufficient financial resources, cash flows, financial market instability, debt recovery,

funding etc. which impact on the working of organisation so it is better to overcome from the

problem now before it gets worse. R. L. Maynard limited is facing many problems related to

finance such that delay in construction projects and high employee turnover. Benchmarking, key

performance indicators, financial planning, statistical or graphical presentation, analysis of

financial statements through ratio analysis, Financial governance etc. are various management

accounting tools to respond company's financial problems without any delays (Schaltegger, and

Burritt, 2017). Some of them are mention below:

Key Performance Indicators: This approach is used to determine effective and efficient

working of organisation to achieve strategic organisation objectives. Company is using multiple

levels of KPI to measure their progress targets. KPI at high level focuses on overall performance

of the company but KPI at low level focus on departmental and operational processes. It's point

of measures are elements of a state which includes input indicators, output of activities, control

over production and mechanism which helps in periodically measurement of organisations and

their departments performance. There are two types of KPI 'leading indicators' and 'lagging

indicators'.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.