Management Accounting Report: Principles, Systems, and Applications

VerifiedAdded on 2021/02/19

|21

|4381

|864

Report

AI Summary

This report offers a comprehensive overview of management accounting, encompassing key definitions, systems, and principles. It explores the differences between financial and management accounting, detailing the benefits and characteristics of effective management accounting systems. The report delves into cost analysis, including various cost types, cost volume profit analysis, flexible budgeting, and cost variance. It also covers inventory management, pricing strategies, and different types of budgets, along with alternative budgeting approaches and the behavioral implications of budgeting. Furthermore, the report discusses key performance indicators, financial governance, and the roles and characteristics of effective management accountants. It concludes by examining the development of strategies and systems for effective reporting and full disclosure within an organization. The report is a valuable resource for understanding the multifaceted nature of management accounting and its applications in strategic decision-making.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

1.1.1 Management accounting definition...............................................................................1

1.1.2 Definition of management accounting system..............................................................1

1.1.3 Management accounting system adds value to the organization...................................2

1.1.4 Discuss the role, origin and principle of management system......................................2

1.1.5 Difference between the financial and management accounting....................................2

Management accounting.........................................................................................................2

1.2.1 Explain the types of management accounting system...................................................3

1.2.2 Benefits of the management accounting system...........................................................3

1.3.1 Explain the characteristic of good management system................................................4

1.3.2 Why there is importance of the information to be understandable...............................4

1.3.3 Types of managerial accounting report.........................................................................4

LO2..................................................................................................................................................5

2.1.1 Definition of cost along with its different types and analyses.......................................5

2.1.2 Cost volume profit, flexible budgeting and cost variance.............................................5

2.1.3 Application of absorption and marginal costing...........................................................6

2.2.1 Fixed and variable cost along with cost allocation........................................................8

2.2.2 Normal and standard costing, activity based costing and role in setting price..............8

2.3.1 Inventory cost and type.................................................................................................9

2.3.2 Benefits of reducing inventory cost.............................................................................10

2.3.3 Valuation method........................................................................................................10

2.3.4 Cost variance...............................................................................................................11

2.3.5 Overhead cost..............................................................................................................11

LO3................................................................................................................................................11

3.1.1 Preparing budget..........................................................................................................11

3.1.2 Different types of budget.............................................................................................11

3.1.3 Alternative budgeting..................................................................................................12

3.1.4 Behavioural implication of budget..............................................................................12

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

1.1.1 Management accounting definition...............................................................................1

1.1.2 Definition of management accounting system..............................................................1

1.1.3 Management accounting system adds value to the organization...................................2

1.1.4 Discuss the role, origin and principle of management system......................................2

1.1.5 Difference between the financial and management accounting....................................2

Management accounting.........................................................................................................2

1.2.1 Explain the types of management accounting system...................................................3

1.2.2 Benefits of the management accounting system...........................................................3

1.3.1 Explain the characteristic of good management system................................................4

1.3.2 Why there is importance of the information to be understandable...............................4

1.3.3 Types of managerial accounting report.........................................................................4

LO2..................................................................................................................................................5

2.1.1 Definition of cost along with its different types and analyses.......................................5

2.1.2 Cost volume profit, flexible budgeting and cost variance.............................................5

2.1.3 Application of absorption and marginal costing...........................................................6

2.2.1 Fixed and variable cost along with cost allocation........................................................8

2.2.2 Normal and standard costing, activity based costing and role in setting price..............8

2.3.1 Inventory cost and type.................................................................................................9

2.3.2 Benefits of reducing inventory cost.............................................................................10

2.3.3 Valuation method........................................................................................................10

2.3.4 Cost variance...............................................................................................................11

2.3.5 Overhead cost..............................................................................................................11

LO3................................................................................................................................................11

3.1.1 Preparing budget..........................................................................................................11

3.1.2 Different types of budget.............................................................................................11

3.1.3 Alternative budgeting..................................................................................................12

3.1.4 Behavioural implication of budget..............................................................................12

3.2.1 Pricing strategies.........................................................................................................12

3.2.2 Determination of price.................................................................................................12

3.2.3 Supply and demand consideration...............................................................................12

3.4.1 Porters five forces analysis..........................................................................................12

LO4................................................................................................................................................13

4.1.1Key performance indicators.........................................................................................13

4.2.1Financial governance and how it helps in solving financial problem..........................13

4.3.1 Characteristics of an effective management accountant.............................................13

4.3.2 Role of the skills in order to deal with the problems...................................................14

4.4.1 Development of strategies and systems for effective and timely reporting, full disclosure

..............................................................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

3.2.2 Determination of price.................................................................................................12

3.2.3 Supply and demand consideration...............................................................................12

3.4.1 Porters five forces analysis..........................................................................................12

LO4................................................................................................................................................13

4.1.1Key performance indicators.........................................................................................13

4.2.1Financial governance and how it helps in solving financial problem..........................13

4.3.1 Characteristics of an effective management accountant.............................................13

4.3.2 Role of the skills in order to deal with the problems...................................................14

4.4.1 Development of strategies and systems for effective and timely reporting, full disclosure

..............................................................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting refers to the accounting done by the managers to well manage

the resources with requirement of the company to take the managerial decision for the

development of the organization. The managerial accounting helps in the proving financial

information of resources by the help of internal team and management of the company. Financial

accounting is total different from the financial accounting as well as cost accounting.

Management accounting is the major concept in which financial accounting and cost accounting

comes. This help in the financial, Cost and business analysis as the requirement of tool and

techniques for the development with the help of this better decision-making can do. The report

will discuss the budget plans, strategic planning, pricing, accounting system and there following

description of reports.

LO1

1.1.1 Management accounting definition

The management accounting is also defined as managerial accounting which means

accounting done by managers of financial information and resources as to make the decision

regarding the development of company. Internal management of company use the managerial

accounting to meet the objective and target of the company with effectiveness and efficiency.

This accounting is different from financial and cost accounting as the management accounting is

border concept. This help in analysis of business, economics, trend in market and finance of

company.

1.1.2 Definition of management accounting system.

Management accounting system refers to the process of identifying, organizing, planning

and the analysis the accounting data for to the management as to take strategic decision to

increase the effectiveness and efficiency of organization by devising the planning and

performance of system of management. There are variety of management accounting system

such as cost accounting system, job costing system, inventory management, price optimizing

system and the job cost system. The management accounting system (MAS) provide the

information towards the strategic sense making as it somewhere neglect the relationship between

the dimensions and the use of MAS.

Management accounting refers to the accounting done by the managers to well manage

the resources with requirement of the company to take the managerial decision for the

development of the organization. The managerial accounting helps in the proving financial

information of resources by the help of internal team and management of the company. Financial

accounting is total different from the financial accounting as well as cost accounting.

Management accounting is the major concept in which financial accounting and cost accounting

comes. This help in the financial, Cost and business analysis as the requirement of tool and

techniques for the development with the help of this better decision-making can do. The report

will discuss the budget plans, strategic planning, pricing, accounting system and there following

description of reports.

LO1

1.1.1 Management accounting definition

The management accounting is also defined as managerial accounting which means

accounting done by managers of financial information and resources as to make the decision

regarding the development of company. Internal management of company use the managerial

accounting to meet the objective and target of the company with effectiveness and efficiency.

This accounting is different from financial and cost accounting as the management accounting is

border concept. This help in analysis of business, economics, trend in market and finance of

company.

1.1.2 Definition of management accounting system.

Management accounting system refers to the process of identifying, organizing, planning

and the analysis the accounting data for to the management as to take strategic decision to

increase the effectiveness and efficiency of organization by devising the planning and

performance of system of management. There are variety of management accounting system

such as cost accounting system, job costing system, inventory management, price optimizing

system and the job cost system. The management accounting system (MAS) provide the

information towards the strategic sense making as it somewhere neglect the relationship between

the dimensions and the use of MAS.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.1.3 Management accounting system adds value to the organization.

The management accounting system adds the value to the working of organization as

there is various management system that competitive in providing the information in the carious

department. The management accounting adds the value to the organization is various ways such

as continues improvement. Through the proper decision-making there is continuous

improvement in the services along with total waste management. The quality management is

done by managerial accounting as to bring the efficiency and effectiveness in organization. The

value addition is cost management by controlling the cost of the goods produced and profit

margin.

1.1.4 Discuss the role, origin and principle of management system.

The origin of management accounting has evolves from the cost accounting techniques

that were having the development in England in the duration of industrial revolution according to

the traditional management accounting.

The major principle of management accounting-

Influence- the management accounting gave the start and end through conversation to take the

management decision. So the communication should be very influential in the company so that

the management can improve the quality of work.

Relevance- the information passed to management to have decision should be relevant along

with the needs to be kept in mind with decision style used for decision. There should be balanced

between internal and external, financial and non-financial.

Value- take the decision is not as important but the impact of decision has also to be analysed.

The company should take the decision keeping all factors, risk and opportunities.

Roles-

It helps in decision-making of the organization

It targets the vision and mission of company

Focus on future trends

Increase the efficiency and effectiveness of company.

1.1.5 Difference between the financial and management accounting

Basis Financial accounting Management accounting

The management accounting system adds the value to the working of organization as

there is various management system that competitive in providing the information in the carious

department. The management accounting adds the value to the organization is various ways such

as continues improvement. Through the proper decision-making there is continuous

improvement in the services along with total waste management. The quality management is

done by managerial accounting as to bring the efficiency and effectiveness in organization. The

value addition is cost management by controlling the cost of the goods produced and profit

margin.

1.1.4 Discuss the role, origin and principle of management system.

The origin of management accounting has evolves from the cost accounting techniques

that were having the development in England in the duration of industrial revolution according to

the traditional management accounting.

The major principle of management accounting-

Influence- the management accounting gave the start and end through conversation to take the

management decision. So the communication should be very influential in the company so that

the management can improve the quality of work.

Relevance- the information passed to management to have decision should be relevant along

with the needs to be kept in mind with decision style used for decision. There should be balanced

between internal and external, financial and non-financial.

Value- take the decision is not as important but the impact of decision has also to be analysed.

The company should take the decision keeping all factors, risk and opportunities.

Roles-

It helps in decision-making of the organization

It targets the vision and mission of company

Focus on future trends

Increase the efficiency and effectiveness of company.

1.1.5 Difference between the financial and management accounting

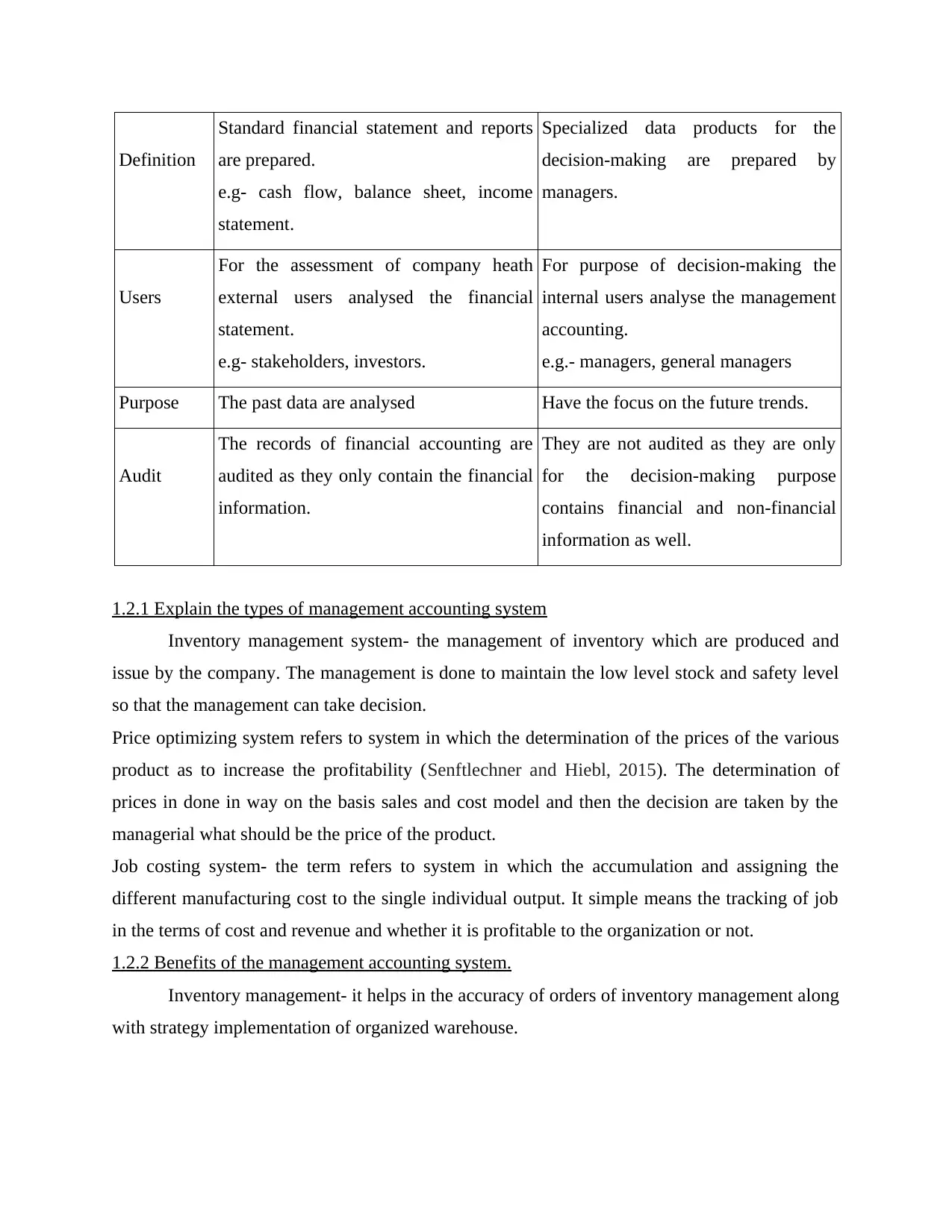

Basis Financial accounting Management accounting

Definition

Standard financial statement and reports

are prepared.

e.g- cash flow, balance sheet, income

statement.

Specialized data products for the

decision-making are prepared by

managers.

Users

For the assessment of company heath

external users analysed the financial

statement.

e.g- stakeholders, investors.

For purpose of decision-making the

internal users analyse the management

accounting.

e.g.- managers, general managers

Purpose The past data are analysed Have the focus on the future trends.

Audit

The records of financial accounting are

audited as they only contain the financial

information.

They are not audited as they are only

for the decision-making purpose

contains financial and non-financial

information as well.

1.2.1 Explain the types of management accounting system

Inventory management system- the management of inventory which are produced and

issue by the company. The management is done to maintain the low level stock and safety level

so that the management can take decision.

Price optimizing system refers to system in which the determination of the prices of the various

product as to increase the profitability (Senftlechner and Hiebl, 2015). The determination of

prices in done in way on the basis sales and cost model and then the decision are taken by the

managerial what should be the price of the product.

Job costing system- the term refers to system in which the accumulation and assigning the

different manufacturing cost to the single individual output. It simple means the tracking of job

in the terms of cost and revenue and whether it is profitable to the organization or not.

1.2.2 Benefits of the management accounting system.

Inventory management- it helps in the accuracy of orders of inventory management along

with strategy implementation of organized warehouse.

Standard financial statement and reports

are prepared.

e.g- cash flow, balance sheet, income

statement.

Specialized data products for the

decision-making are prepared by

managers.

Users

For the assessment of company heath

external users analysed the financial

statement.

e.g- stakeholders, investors.

For purpose of decision-making the

internal users analyse the management

accounting.

e.g.- managers, general managers

Purpose The past data are analysed Have the focus on the future trends.

Audit

The records of financial accounting are

audited as they only contain the financial

information.

They are not audited as they are only

for the decision-making purpose

contains financial and non-financial

information as well.

1.2.1 Explain the types of management accounting system

Inventory management system- the management of inventory which are produced and

issue by the company. The management is done to maintain the low level stock and safety level

so that the management can take decision.

Price optimizing system refers to system in which the determination of the prices of the various

product as to increase the profitability (Senftlechner and Hiebl, 2015). The determination of

prices in done in way on the basis sales and cost model and then the decision are taken by the

managerial what should be the price of the product.

Job costing system- the term refers to system in which the accumulation and assigning the

different manufacturing cost to the single individual output. It simple means the tracking of job

in the terms of cost and revenue and whether it is profitable to the organization or not.

1.2.2 Benefits of the management accounting system.

Inventory management- it helps in the accuracy of orders of inventory management along

with strategy implementation of organized warehouse.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost management- help in improvement of efficiency and recognition of profitable and

unprofitable activities. It provides the suitable information for planning and risk management in

company.

Price optimization- it benefits in balancing the cost minimization and risk while increasing the

business value. It helps in reduction of cost by removing the barriers.

Job costing- benefit of job costing is the ability to track all the input along with material and

labour used so that the profitability of job can be measures. It helps in cost control, efficiency

and productivity of company.

1.3.1 Explain the characteristic of good management system

For the proper and efficient decision-making the information should be perfectly. There

should not be biasness in the information. The information should reliable and related to the

decision-making purpose. Then the information transfers for the decision should be updated and

to thr point so that there should be detailed planning for the decision. The information should

always be accurate. The information also be concise and to the point so that effectiveness could

be maintained.

1.3.2 Why there is importance of the information to be understandable.

The information should be understandable so that the accuracy can be maintained in the

decision. The management decision taken as to increase the profit maximization and the

efficiency of organization. I'd there is the business in the decision the complete decision of the

organization will be got reluctant. The company will try have the proper decision-making so that

the effective information can be passed on. His information should be understandable so that

accuracy can be maintained.

1.3.3 Types of managerial accounting report

Budgets report

These types of the reports help in analyse the performance of the small business and the

performance of the various department (Sands and et.al, 2015). This helps in analysing the

performance of the organization that what is planned and what to be achieved by the company. It

helps in predict the future budgets.

Accounts receivable ageing

It refers to budget in whichever the cash flow of the organization has to be maintained. The

credit to the customer will be calculated so that risk of the company can be reduced and write

unprofitable activities. It provides the suitable information for planning and risk management in

company.

Price optimization- it benefits in balancing the cost minimization and risk while increasing the

business value. It helps in reduction of cost by removing the barriers.

Job costing- benefit of job costing is the ability to track all the input along with material and

labour used so that the profitability of job can be measures. It helps in cost control, efficiency

and productivity of company.

1.3.1 Explain the characteristic of good management system

For the proper and efficient decision-making the information should be perfectly. There

should not be biasness in the information. The information should reliable and related to the

decision-making purpose. Then the information transfers for the decision should be updated and

to thr point so that there should be detailed planning for the decision. The information should

always be accurate. The information also be concise and to the point so that effectiveness could

be maintained.

1.3.2 Why there is importance of the information to be understandable.

The information should be understandable so that the accuracy can be maintained in the

decision. The management decision taken as to increase the profit maximization and the

efficiency of organization. I'd there is the business in the decision the complete decision of the

organization will be got reluctant. The company will try have the proper decision-making so that

the effective information can be passed on. His information should be understandable so that

accuracy can be maintained.

1.3.3 Types of managerial accounting report

Budgets report

These types of the reports help in analyse the performance of the small business and the

performance of the various department (Sands and et.al, 2015). This helps in analysing the

performance of the organization that what is planned and what to be achieved by the company. It

helps in predict the future budgets.

Accounts receivable ageing

It refers to budget in whichever the cash flow of the organization has to be maintained. The

credit to the customer will be calculated so that risk of the company can be reduced and write

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

down the invoice for 30 days, 60 days and 90 days. If the customer are not paying the credit then

meek your credit policy stricter.

Job cost report- in this report there are the clear explanations of expenses of each cost. He

must there is the expense of company of that particular job and what are its revenue and

profitability. It also analyses the performance of project and intent is of waste.

LO2

2.1.1 Definition of cost along with its different types and analyses.

Cost refers to sacrifice done as to achieve something. The cost is not always the expense.

The cost management refers financial identification of any goods and services at to identify the

effectiveness of the particular time. There is the variety of cost in the accounting-

Explicit cost- the cost of the production of any product does include expenditure is

explicit cost.

Implicit cost -the cost which includes the non-expenditure in the production of any good

is implicit cost.

Differential cost.-This is cost which changed when there is the explanation in the

company. Either it is remitted to adding product line, new machine or replacement.

Short run cost- the one variable is fixed (fixed capital), then the cost incurred by the

output is called as short run cost. It helps in the decision-making of hoe much to

produce.

Long run cost- the cost which in incurred by all the output factors in the long term

including plant and machinery in the organization. The long run cost help in the

expansion decision of company.

Cost analysis refers with determining the value of the product input value or the overall

cost of production of the product (Myrelid and Olhager, 2015). It can be done through the cost

analysis by using-

Cost concept- to analysis the financial position of the company

Analytical cost concept-done to analyse the profitability of company as it is used by economist.

2.1.2 Cost volume profit, flexible budgeting and cost variance

Cost volume profit- this analysis shows that the changes in the cost and volume of

product change the net income of company along with several assumptions of selling price per

unit is constant and other market factored.

meek your credit policy stricter.

Job cost report- in this report there are the clear explanations of expenses of each cost. He

must there is the expense of company of that particular job and what are its revenue and

profitability. It also analyses the performance of project and intent is of waste.

LO2

2.1.1 Definition of cost along with its different types and analyses.

Cost refers to sacrifice done as to achieve something. The cost is not always the expense.

The cost management refers financial identification of any goods and services at to identify the

effectiveness of the particular time. There is the variety of cost in the accounting-

Explicit cost- the cost of the production of any product does include expenditure is

explicit cost.

Implicit cost -the cost which includes the non-expenditure in the production of any good

is implicit cost.

Differential cost.-This is cost which changed when there is the explanation in the

company. Either it is remitted to adding product line, new machine or replacement.

Short run cost- the one variable is fixed (fixed capital), then the cost incurred by the

output is called as short run cost. It helps in the decision-making of hoe much to

produce.

Long run cost- the cost which in incurred by all the output factors in the long term

including plant and machinery in the organization. The long run cost help in the

expansion decision of company.

Cost analysis refers with determining the value of the product input value or the overall

cost of production of the product (Myrelid and Olhager, 2015). It can be done through the cost

analysis by using-

Cost concept- to analysis the financial position of the company

Analytical cost concept-done to analyse the profitability of company as it is used by economist.

2.1.2 Cost volume profit, flexible budgeting and cost variance

Cost volume profit- this analysis shows that the changes in the cost and volume of

product change the net income of company along with several assumptions of selling price per

unit is constant and other market factored.

Flexible Budgeting- the budget which includes the variable rate along with volume at the

per unit of activity instead of fixed cost is termed as the flexible budget. It is also termed as

flexible budget.

Cost variance- The difference between the actual and planned cost id refers as the cost variance.

Or in other term it can be said that the difference between the actual cost and planned

expenditure.

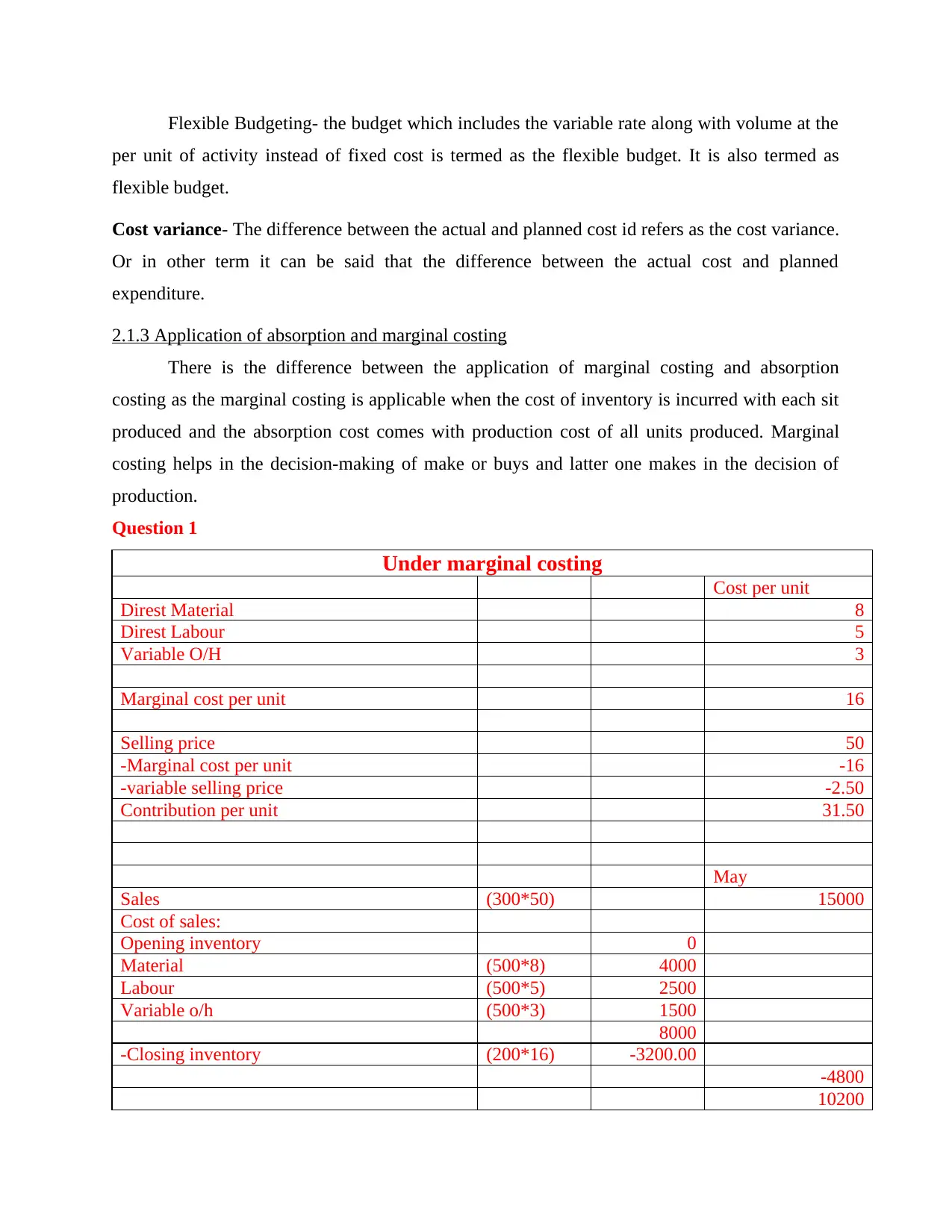

2.1.3 Application of absorption and marginal costing

There is the difference between the application of marginal costing and absorption

costing as the marginal costing is applicable when the cost of inventory is incurred with each sit

produced and the absorption cost comes with production cost of all units produced. Marginal

costing helps in the decision-making of make or buys and latter one makes in the decision of

production.

Question 1

Under marginal costing

Cost per unit

Direst Material 8

Direst Labour 5

Variable O/H 3

Marginal cost per unit 16

Selling price 50

-Marginal cost per unit -16

-variable selling price -2.50

Contribution per unit 31.50

May

Sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Variable o/h (500*3) 1500

8000

-Closing inventory (200*16) -3200.00

-4800

10200

per unit of activity instead of fixed cost is termed as the flexible budget. It is also termed as

flexible budget.

Cost variance- The difference between the actual and planned cost id refers as the cost variance.

Or in other term it can be said that the difference between the actual cost and planned

expenditure.

2.1.3 Application of absorption and marginal costing

There is the difference between the application of marginal costing and absorption

costing as the marginal costing is applicable when the cost of inventory is incurred with each sit

produced and the absorption cost comes with production cost of all units produced. Marginal

costing helps in the decision-making of make or buys and latter one makes in the decision of

production.

Question 1

Under marginal costing

Cost per unit

Direst Material 8

Direst Labour 5

Variable O/H 3

Marginal cost per unit 16

Selling price 50

-Marginal cost per unit -16

-variable selling price -2.50

Contribution per unit 31.50

May

Sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Variable o/h (500*3) 1500

8000

-Closing inventory (200*16) -3200.00

-4800

10200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

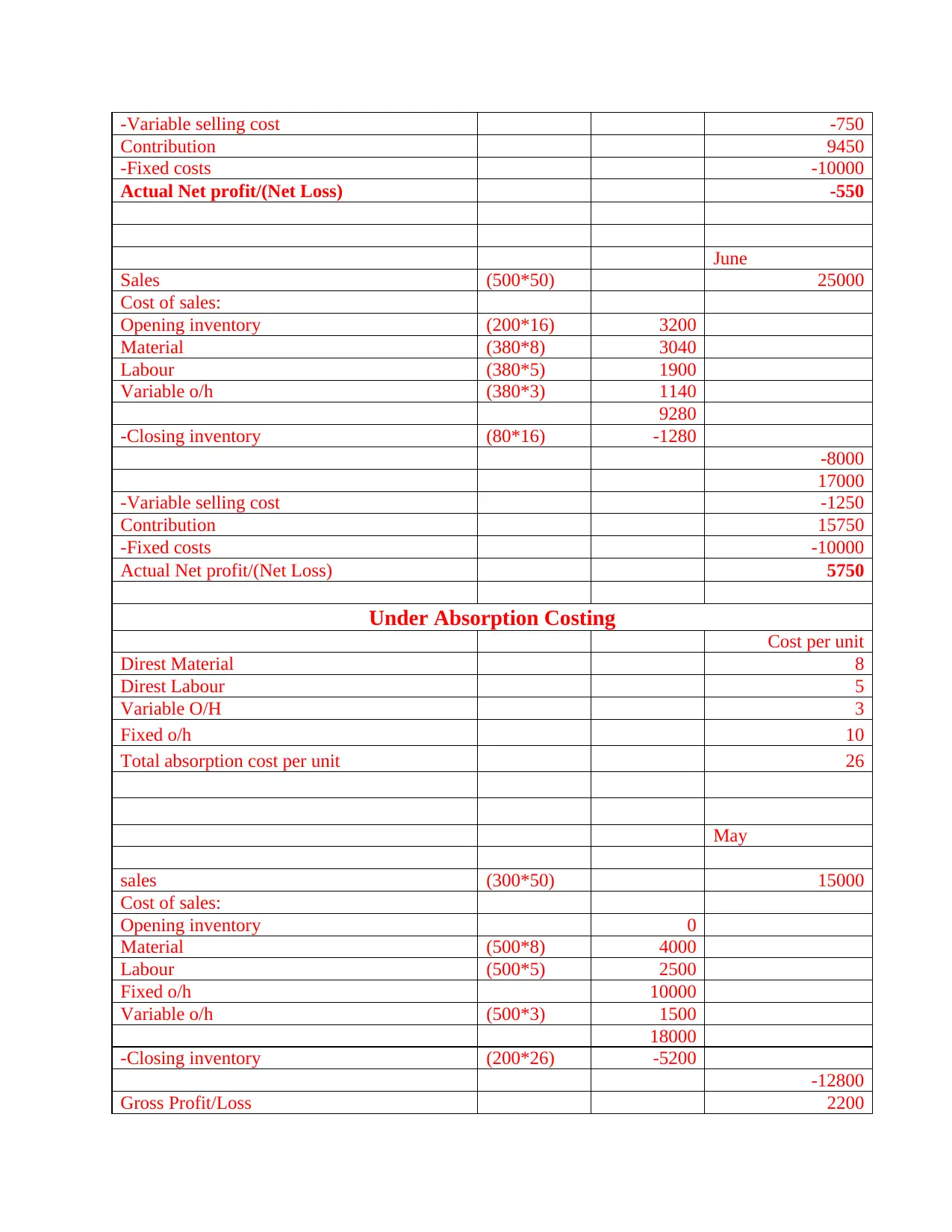

-Variable selling cost -750

Contribution 9450

-Fixed costs -10000

Actual Net profit/(Net Loss) -550

June

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*16) 3200

Material (380*8) 3040

Labour (380*5) 1900

Variable o/h (380*3) 1140

9280

-Closing inventory (80*16) -1280

-8000

17000

-Variable selling cost -1250

Contribution 15750

-Fixed costs -10000

Actual Net profit/(Net Loss) 5750

Under Absorption Costing

Cost per unit

Direst Material 8

Direst Labour 5

Variable O/H 3

Fixed o/h 10

Total absorption cost per unit 26

May

sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Fixed o/h 10000

Variable o/h (500*3) 1500

18000

-Closing inventory (200*26) -5200

-12800

Gross Profit/Loss 2200

Contribution 9450

-Fixed costs -10000

Actual Net profit/(Net Loss) -550

June

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*16) 3200

Material (380*8) 3040

Labour (380*5) 1900

Variable o/h (380*3) 1140

9280

-Closing inventory (80*16) -1280

-8000

17000

-Variable selling cost -1250

Contribution 15750

-Fixed costs -10000

Actual Net profit/(Net Loss) 5750

Under Absorption Costing

Cost per unit

Direst Material 8

Direst Labour 5

Variable O/H 3

Fixed o/h 10

Total absorption cost per unit 26

May

sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Fixed o/h 10000

Variable o/h (500*3) 1500

18000

-Closing inventory (200*26) -5200

-12800

Gross Profit/Loss 2200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

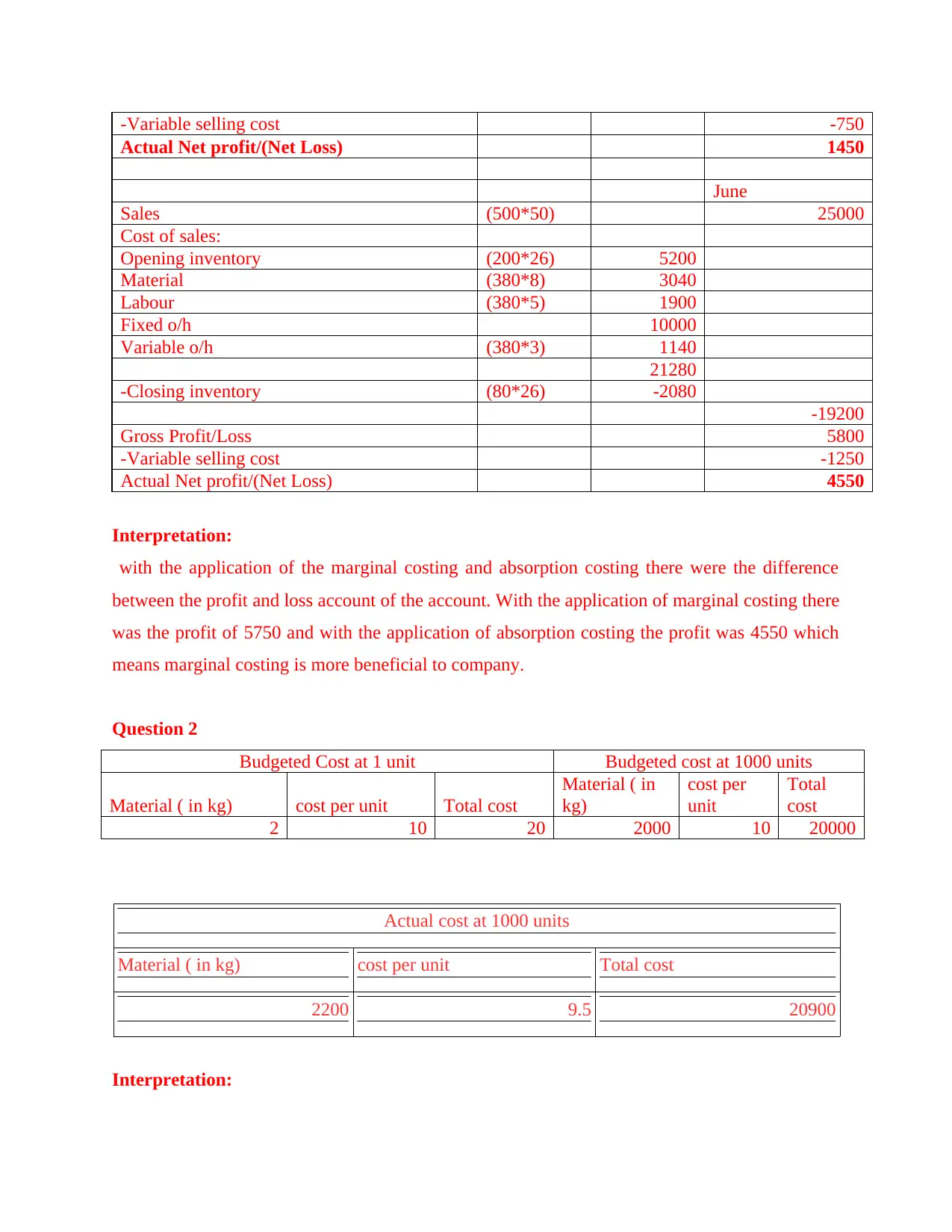

-Variable selling cost -750

Actual Net profit/(Net Loss) 1450

June

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*26) 5200

Material (380*8) 3040

Labour (380*5) 1900

Fixed o/h 10000

Variable o/h (380*3) 1140

21280

-Closing inventory (80*26) -2080

-19200

Gross Profit/Loss 5800

-Variable selling cost -1250

Actual Net profit/(Net Loss) 4550

Interpretation:

with the application of the marginal costing and absorption costing there were the difference

between the profit and loss account of the account. With the application of marginal costing there

was the profit of 5750 and with the application of absorption costing the profit was 4550 which

means marginal costing is more beneficial to company.

Question 2

Budgeted Cost at 1 unit Budgeted cost at 1000 units

Material ( in kg) cost per unit Total cost

Material ( in

kg)

cost per

unit

Total

cost

2 10 20 2000 10 20000

Actual cost at 1000 units

Material ( in kg) cost per unit Total cost

2200 9.5 20900

Interpretation:

Actual Net profit/(Net Loss) 1450

June

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*26) 5200

Material (380*8) 3040

Labour (380*5) 1900

Fixed o/h 10000

Variable o/h (380*3) 1140

21280

-Closing inventory (80*26) -2080

-19200

Gross Profit/Loss 5800

-Variable selling cost -1250

Actual Net profit/(Net Loss) 4550

Interpretation:

with the application of the marginal costing and absorption costing there were the difference

between the profit and loss account of the account. With the application of marginal costing there

was the profit of 5750 and with the application of absorption costing the profit was 4550 which

means marginal costing is more beneficial to company.

Question 2

Budgeted Cost at 1 unit Budgeted cost at 1000 units

Material ( in kg) cost per unit Total cost

Material ( in

kg)

cost per

unit

Total

cost

2 10 20 2000 10 20000

Actual cost at 1000 units

Material ( in kg) cost per unit Total cost

2200 9.5 20900

Interpretation:

As per the budget the cost for the material was estimated was 20000 but the actual cost of the per

1000 units is 20900 which means the cost was increased by 900 per 10000 unit. It means the cost

of the unit are varying the budgeted cost.

2.2.1 Fixed and variable cost along with cost allocation.

Fixed cost refers to cost which is fixed at the zero level of units production whereas the

cost which is variable with production of each unit is called as variable cost (Kihn and Ihantola,

2015. ). As the cost allocation is done by identifying the different cost for the production of

different unit.

2.2.2 Normal and standard costing, activity based costing and role in setting price

Normal costing refers to the cost derived from cost derivation. In exception

manufacturing overhead of not included in taking the cost of actual input whereas in the standard

costing the cost are already will decide in budget and then the comparison between the planned

and actual budget is there.

2.3.1 Inventory cost and type

The cost incurred to collect the inventory in the step of three steps as the raw material,

work in progress and finished goods. There are various type of inventory cost such as holding

cost and purchase cost.

Holding cost refer to the cost insured by the company to hold the inventory for longer period

such as warehouse cost.

Purchase cost- it refers to the cost which is incurred in the purchasing of product is called as

purchase cost.

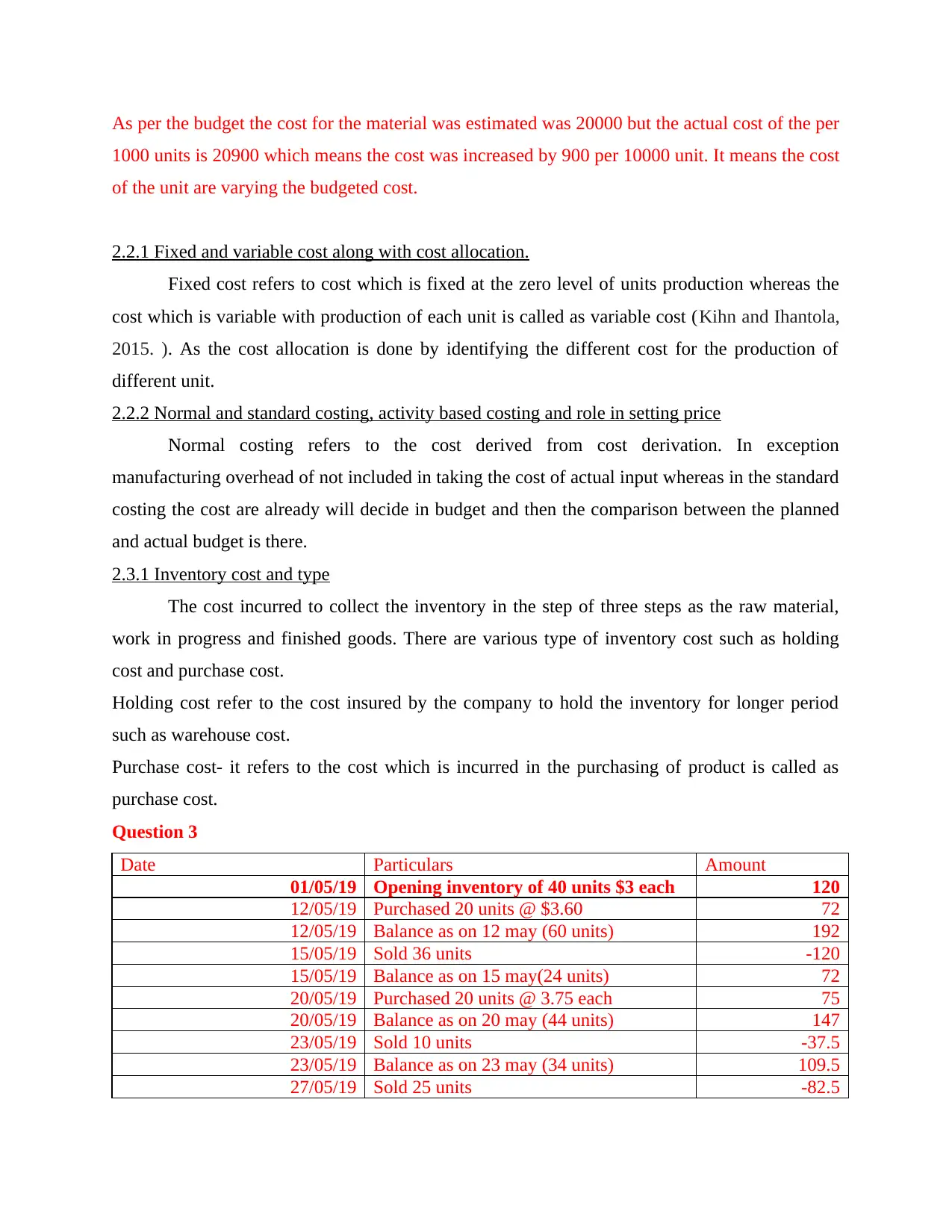

Question 3

Date Particulars Amount

01/05/19 Opening inventory of 40 units $3 each 120

12/05/19 Purchased 20 units @ $3.60 72

12/05/19 Balance as on 12 may (60 units) 192

15/05/19 Sold 36 units -120

15/05/19 Balance as on 15 may(24 units) 72

20/05/19 Purchased 20 units @ 3.75 each 75

20/05/19 Balance as on 20 may (44 units) 147

23/05/19 Sold 10 units -37.5

23/05/19 Balance as on 23 may (34 units) 109.5

27/05/19 Sold 25 units -82.5

1000 units is 20900 which means the cost was increased by 900 per 10000 unit. It means the cost

of the unit are varying the budgeted cost.

2.2.1 Fixed and variable cost along with cost allocation.

Fixed cost refers to cost which is fixed at the zero level of units production whereas the

cost which is variable with production of each unit is called as variable cost (Kihn and Ihantola,

2015. ). As the cost allocation is done by identifying the different cost for the production of

different unit.

2.2.2 Normal and standard costing, activity based costing and role in setting price

Normal costing refers to the cost derived from cost derivation. In exception

manufacturing overhead of not included in taking the cost of actual input whereas in the standard

costing the cost are already will decide in budget and then the comparison between the planned

and actual budget is there.

2.3.1 Inventory cost and type

The cost incurred to collect the inventory in the step of three steps as the raw material,

work in progress and finished goods. There are various type of inventory cost such as holding

cost and purchase cost.

Holding cost refer to the cost insured by the company to hold the inventory for longer period

such as warehouse cost.

Purchase cost- it refers to the cost which is incurred in the purchasing of product is called as

purchase cost.

Question 3

Date Particulars Amount

01/05/19 Opening inventory of 40 units $3 each 120

12/05/19 Purchased 20 units @ $3.60 72

12/05/19 Balance as on 12 may (60 units) 192

15/05/19 Sold 36 units -120

15/05/19 Balance as on 15 may(24 units) 72

20/05/19 Purchased 20 units @ 3.75 each 75

20/05/19 Balance as on 20 may (44 units) 147

23/05/19 Sold 10 units -37.5

23/05/19 Balance as on 23 may (34 units) 109.5

27/05/19 Sold 25 units -82.5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.