Management Accounting: Systems, Methods, and Financial Reports

VerifiedAdded on 2021/01/01

|17

|4999

|134

Report

AI Summary

This report provides a comprehensive overview of management accounting, encompassing various systems such as cost accounting, job costing, price optimization, and inventory management systems. It delves into different reporting methods, including budget reports, cost managerial accounting reports, performance reports, and accounts receivable reports. The report also includes a critical evaluation of management accounting statement and reporting integration within organizations. Furthermore, it presents calculations using both absorption and marginal costing methods for a case study involving TSR Pvt Ltd, and analyzes the application of planning tools for budgetary control, comparing the adaptation of management accounting systems to respond to financial problems and lead to sustainable success. The report concludes with an evaluation of the use of planning tools to address financial issues effectively.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

P1 Explaining the management accounting and presenting essential requirements of different

types of management accounting system....................................................................................1

M1 Evaluation of the benefits of management account systems and their application in

business.......................................................................................................................................2

P2 Explaining different methods used for management accounting reporting...........................3

D1 Critical evaluation of management accounting Statement and reporting integration in

organisation.................................................................................................................................4

P3 Calculation of the cost by use of absorption and marginal costing method for TSR Pvt Ltd.

.....................................................................................................................................................4

M2 Application of range of management accounting techniques and producing appropriate

financial reporting documents.....................................................................................................6

D2 Producing financial reports that accurately apply and interpret data for a range of business

activities......................................................................................................................................7

P4 Explaining advantages and disadvantages of different types of planning tools for budgetary

control.........................................................................................................................................7

M3 Analysing the use of different planning tools and their application.....................................9

P5 Comparing the adaption of management accounting system to respond to financial

problems......................................................................................................................................9

M4 Analysing the fact that with responding to financial problem organisation can lead to

sustainable success....................................................................................................................10

D3 Evaluation of use of planning tools to respond appropriately to solving financial problems

to lead organisations to sustainable success..............................................................................11

CONCLUSION..............................................................................................................................11

REFERENCE.................................................................................................................................12

INTRODUCTION...........................................................................................................................1

P1 Explaining the management accounting and presenting essential requirements of different

types of management accounting system....................................................................................1

M1 Evaluation of the benefits of management account systems and their application in

business.......................................................................................................................................2

P2 Explaining different methods used for management accounting reporting...........................3

D1 Critical evaluation of management accounting Statement and reporting integration in

organisation.................................................................................................................................4

P3 Calculation of the cost by use of absorption and marginal costing method for TSR Pvt Ltd.

.....................................................................................................................................................4

M2 Application of range of management accounting techniques and producing appropriate

financial reporting documents.....................................................................................................6

D2 Producing financial reports that accurately apply and interpret data for a range of business

activities......................................................................................................................................7

P4 Explaining advantages and disadvantages of different types of planning tools for budgetary

control.........................................................................................................................................7

M3 Analysing the use of different planning tools and their application.....................................9

P5 Comparing the adaption of management accounting system to respond to financial

problems......................................................................................................................................9

M4 Analysing the fact that with responding to financial problem organisation can lead to

sustainable success....................................................................................................................10

D3 Evaluation of use of planning tools to respond appropriately to solving financial problems

to lead organisations to sustainable success..............................................................................11

CONCLUSION..............................................................................................................................11

REFERENCE.................................................................................................................................12

INTRODUCTION

Management accounting is the branch of accounting which deals with both statistical as

well as financial restrict pertaining to a business organization. It presents and analysis the

business activities to the internal management and aid them in decision making process. In the

present report a detailed discussion related with management accounting, is different systems

and reporting is done. Along with unit cost of the products is determined with marginal as well

as absorption costing method. Moreover, the application of planning tool is done and it is defined

that how the management accounting system helps in identification and solving of financial

problems and lead business to sustainable success.

P1 Explaining the management accounting and presenting essential requirements of different

types of management accounting system

Management accounting: is a process of analyzing the costs and operations of the

business for preparation of internal financial report, records and accounts to assist the

management in decision making process to achieve the business goals and objectives (Maas,

Schaltegger and Crutzen, 2016). It is an act of making the sense out of the financial and costing

data by translating it into the useful information for the managers and officers of the

organization.

As per the institute of Cost and Management Accountant London it is defined as

application of professional knowledge and skill for preparing the accounting information in such

which can assist the management in formulating the policies and in planing and control of the

operations of the business.

Management Accounting System: is that system that deals with both financial as well

as statistical information which can be used to reach different decisions of the organization

which are related with costing, controlling the price, managing the inventory (Management

Accounting – Meaning, Advantages & Functions, 2018). It system consist of internal

information that is used by the organization to measure and evaluate the process for the

management. There are different types of accounting systems:

Cost accounting system: the cost accounting system is a framework that is used by the

organization to estimate the cost of their various products which assist in analysis of profitability,

valuation of the inventory and controlling the cost. The essential requirement of this system is to

estimate the accurate cost of the products which is critical for operating under profits. All the

1

Management accounting is the branch of accounting which deals with both statistical as

well as financial restrict pertaining to a business organization. It presents and analysis the

business activities to the internal management and aid them in decision making process. In the

present report a detailed discussion related with management accounting, is different systems

and reporting is done. Along with unit cost of the products is determined with marginal as well

as absorption costing method. Moreover, the application of planning tool is done and it is defined

that how the management accounting system helps in identification and solving of financial

problems and lead business to sustainable success.

P1 Explaining the management accounting and presenting essential requirements of different

types of management accounting system

Management accounting: is a process of analyzing the costs and operations of the

business for preparation of internal financial report, records and accounts to assist the

management in decision making process to achieve the business goals and objectives (Maas,

Schaltegger and Crutzen, 2016). It is an act of making the sense out of the financial and costing

data by translating it into the useful information for the managers and officers of the

organization.

As per the institute of Cost and Management Accountant London it is defined as

application of professional knowledge and skill for preparing the accounting information in such

which can assist the management in formulating the policies and in planing and control of the

operations of the business.

Management Accounting System: is that system that deals with both financial as well

as statistical information which can be used to reach different decisions of the organization

which are related with costing, controlling the price, managing the inventory (Management

Accounting – Meaning, Advantages & Functions, 2018). It system consist of internal

information that is used by the organization to measure and evaluate the process for the

management. There are different types of accounting systems:

Cost accounting system: the cost accounting system is a framework that is used by the

organization to estimate the cost of their various products which assist in analysis of profitability,

valuation of the inventory and controlling the cost. The essential requirement of this system is to

estimate the accurate cost of the products which is critical for operating under profits. All the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accurate information must be there to evaluate the cost and to determine that which product is

profitable and which one is not. This includes two other system which are job order costing and

process costing.

Job costing System: includes the process of accumulation of all the information related

with the cost which is associated to the specific production or service job. Under this system the

cost related with direct material, direct labour and overhead is accumulated. This meet the need

of the consumers. The cost related with particular job is determined with identification of all the

elements of cost separately (Quattrone, 2016). The essential requirement for this system is

detailed information regarding each cost elements.

Price optimization system: is related with the mathematical programs which calculate

the demand variations at different level of the prices for the same product. This combines all the

data with information related with cost ans inventory level and recommend the prices at which

the profits can be improvised. The essential need of this system is that it typically requires

information related with three critical pricing elements which are pricing strategy, value of

products for both buyer and seller and the tactics to manage all the elements having impact on

profitability.

Inventory management system: woks by tracking two main functions of the inventory

and the warehouses these are to keep information regarding receiving the inventory incoming of

the supplies and the shipping that is out going. The main objective of this system is to know

what is the current level of inventory and to manage the situation of under and over stock.

The essential requirement of this system is desktop software, barcod scanner, bare code

printers and the mobile devices to streamline the management of the inventory of the

organisation. The inventory includes goods, consumables, supplies and stock.

M1 Evaluation of the benefits of management account systems and their application in business

Cost accounting system:

This system assist in clustering the revenue and expenses with the cost objective such as

product line and distribution channel.

Costs can be tracked on a trend line to discover expense surges that may be indicative of

long-term trends.

An effective cost accountant not only locates problems within a company, but also drills

down through the data to determine the exact cause of the issue

2

profitable and which one is not. This includes two other system which are job order costing and

process costing.

Job costing System: includes the process of accumulation of all the information related

with the cost which is associated to the specific production or service job. Under this system the

cost related with direct material, direct labour and overhead is accumulated. This meet the need

of the consumers. The cost related with particular job is determined with identification of all the

elements of cost separately (Quattrone, 2016). The essential requirement for this system is

detailed information regarding each cost elements.

Price optimization system: is related with the mathematical programs which calculate

the demand variations at different level of the prices for the same product. This combines all the

data with information related with cost ans inventory level and recommend the prices at which

the profits can be improvised. The essential need of this system is that it typically requires

information related with three critical pricing elements which are pricing strategy, value of

products for both buyer and seller and the tactics to manage all the elements having impact on

profitability.

Inventory management system: woks by tracking two main functions of the inventory

and the warehouses these are to keep information regarding receiving the inventory incoming of

the supplies and the shipping that is out going. The main objective of this system is to know

what is the current level of inventory and to manage the situation of under and over stock.

The essential requirement of this system is desktop software, barcod scanner, bare code

printers and the mobile devices to streamline the management of the inventory of the

organisation. The inventory includes goods, consumables, supplies and stock.

M1 Evaluation of the benefits of management account systems and their application in business

Cost accounting system:

This system assist in clustering the revenue and expenses with the cost objective such as

product line and distribution channel.

Costs can be tracked on a trend line to discover expense surges that may be indicative of

long-term trends.

An effective cost accountant not only locates problems within a company, but also drills

down through the data to determine the exact cause of the issue

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job costing System:

It allows the mangers to calculate the profits earned on the individual jobs which assist

them in ascertain that which jobs are desired to be pursued in the future.

The mangers can track the individual job ans team performances to control the cost,

efficiency and productivity.

Price optimization system:

This system helps the business in determining the initial prices of the products which are

launched for the first time (Bromwich and Scapens, 2016).

It identifies the promotional prices at which the costumers is attracted to by the products.

This also defines the markdown or discounting prices of the product to attract consumers

and without affecting the profitability of the business.

Inventory management system:

It helps in activating the efficiency and productivity in the operations.

With this system the cost on inventory is minimized and maximise sales and profits.

This integrates the whole business with automation of the manual task and maintain the

happiness of the consumers.

P2 Explaining different methods used for management accounting reporting

Under the management accounting the emphasis is given on the inside information

received through the financial as and the managerial accounting reports which used for planning,

regulating and decision making with measuring the performance. The reports are generated on

regular intervals throughout the income year. These reports are of key importance as some

crucial decision depends no it. The reports under the management accounting are:

Budget Report: are responsible to measure the performance of the company. In the

organisation an overall budget is prepared to create an understanding of the overall objective and

gaol of the business. The provides information about the sources of incomes and expenditure.

The tries to achieve its goals and mission while staying in the budgeted amount (Modugno and

Di Carlo, 2019). Moreover, this reports guide the managers to offer better employees incentives,

cost cutting and negotiating the terms with the suppliers.

Cost managerial Accounting report: is responsible for computation of the cost of

products and commodities that are manufactured by the organisation (TYPES OF MANAGERIAL

ACCOUNTING REPORTS, 2018). The data related with material, labour and others cost is

3

It allows the mangers to calculate the profits earned on the individual jobs which assist

them in ascertain that which jobs are desired to be pursued in the future.

The mangers can track the individual job ans team performances to control the cost,

efficiency and productivity.

Price optimization system:

This system helps the business in determining the initial prices of the products which are

launched for the first time (Bromwich and Scapens, 2016).

It identifies the promotional prices at which the costumers is attracted to by the products.

This also defines the markdown or discounting prices of the product to attract consumers

and without affecting the profitability of the business.

Inventory management system:

It helps in activating the efficiency and productivity in the operations.

With this system the cost on inventory is minimized and maximise sales and profits.

This integrates the whole business with automation of the manual task and maintain the

happiness of the consumers.

P2 Explaining different methods used for management accounting reporting

Under the management accounting the emphasis is given on the inside information

received through the financial as and the managerial accounting reports which used for planning,

regulating and decision making with measuring the performance. The reports are generated on

regular intervals throughout the income year. These reports are of key importance as some

crucial decision depends no it. The reports under the management accounting are:

Budget Report: are responsible to measure the performance of the company. In the

organisation an overall budget is prepared to create an understanding of the overall objective and

gaol of the business. The provides information about the sources of incomes and expenditure.

The tries to achieve its goals and mission while staying in the budgeted amount (Modugno and

Di Carlo, 2019). Moreover, this reports guide the managers to offer better employees incentives,

cost cutting and negotiating the terms with the suppliers.

Cost managerial Accounting report: is responsible for computation of the cost of

products and commodities that are manufactured by the organisation (TYPES OF MANAGERIAL

ACCOUNTING REPORTS, 2018). The data related with material, labour and others cost is

3

considered in this report. The total cost is divided by the units of goods produced. This reports

give the synopsis of all the cost related information. The mangers are assisted in comparisons

the cost and the sales price of the goods so that a good profit margin can be ascertained.

Performance report: are created with a view to critically review the performance of the

company as a whole as well each employee within the firm. Managers use these performance

reports to make key strategic decisions about the future of the organization. Individuals are often

awarded for their commitment to the organization and under performers are laid off or dealt with

as required. Performance-related managerial accounting reports also offer deep insight into the

working of a company.

Account receivable report: gives the information regarding the money extended on

credit and this report plays a vital role for business involved much in this activity. The managers

break down the information about the balances due from the clients and the time allowed to them

to make the repayment (Budgetary Controlling Techniques, 2018). The reports outline those who

can be defaulter and with this company can make the return policy more strict and tighter by

revising the credit policy.

D1 Critical evaluation of management accounting Statement and reporting integration in

organisation

The management accounting system is crucial for the organisation and different systems

are integrated in the organisation as determine the unit cost of the product to know the expenses

incurred to produce a single unit of the finished goods with identifying all the elements of cost.

Moreover, the systems are used by the management to determine which product is profitable or

nor and to determine the prices as which consumer is willing to buy the product with managing

the inventory in and out flow (Jermias, Gani and Juliana, 2018). The management accounting

reports plays a vital role in evaluating the performance of the business with setting the path to

reach the golds of the business. The overall and individual performance is evaluated to mitigate

any gap in the desired performance. The budgets set the target for the company to achieve the

mission of company within stipules funds only for which decision are taken on how it can be

done in effective manner.

P3 Calculation of the cost by use of absorption and marginal costing method for TSR Pvt Ltd.

Margin costing: is that method of the costing where the variable cost is charged to the

unit cost of product where the fixed cost is charges as the period cost. This means the fixed cost

4

give the synopsis of all the cost related information. The mangers are assisted in comparisons

the cost and the sales price of the goods so that a good profit margin can be ascertained.

Performance report: are created with a view to critically review the performance of the

company as a whole as well each employee within the firm. Managers use these performance

reports to make key strategic decisions about the future of the organization. Individuals are often

awarded for their commitment to the organization and under performers are laid off or dealt with

as required. Performance-related managerial accounting reports also offer deep insight into the

working of a company.

Account receivable report: gives the information regarding the money extended on

credit and this report plays a vital role for business involved much in this activity. The managers

break down the information about the balances due from the clients and the time allowed to them

to make the repayment (Budgetary Controlling Techniques, 2018). The reports outline those who

can be defaulter and with this company can make the return policy more strict and tighter by

revising the credit policy.

D1 Critical evaluation of management accounting Statement and reporting integration in

organisation

The management accounting system is crucial for the organisation and different systems

are integrated in the organisation as determine the unit cost of the product to know the expenses

incurred to produce a single unit of the finished goods with identifying all the elements of cost.

Moreover, the systems are used by the management to determine which product is profitable or

nor and to determine the prices as which consumer is willing to buy the product with managing

the inventory in and out flow (Jermias, Gani and Juliana, 2018). The management accounting

reports plays a vital role in evaluating the performance of the business with setting the path to

reach the golds of the business. The overall and individual performance is evaluated to mitigate

any gap in the desired performance. The budgets set the target for the company to achieve the

mission of company within stipules funds only for which decision are taken on how it can be

done in effective manner.

P3 Calculation of the cost by use of absorption and marginal costing method for TSR Pvt Ltd.

Margin costing: is that method of the costing where the variable cost is charged to the

unit cost of product where the fixed cost is charges as the period cost. This means the fixed cost

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is completely written off against the contribution. It includes direct material, labour and direct

expenses and variable overheads. The marginal cost implies the fact that the addition la cost

incurred to produce an extra unit of output.

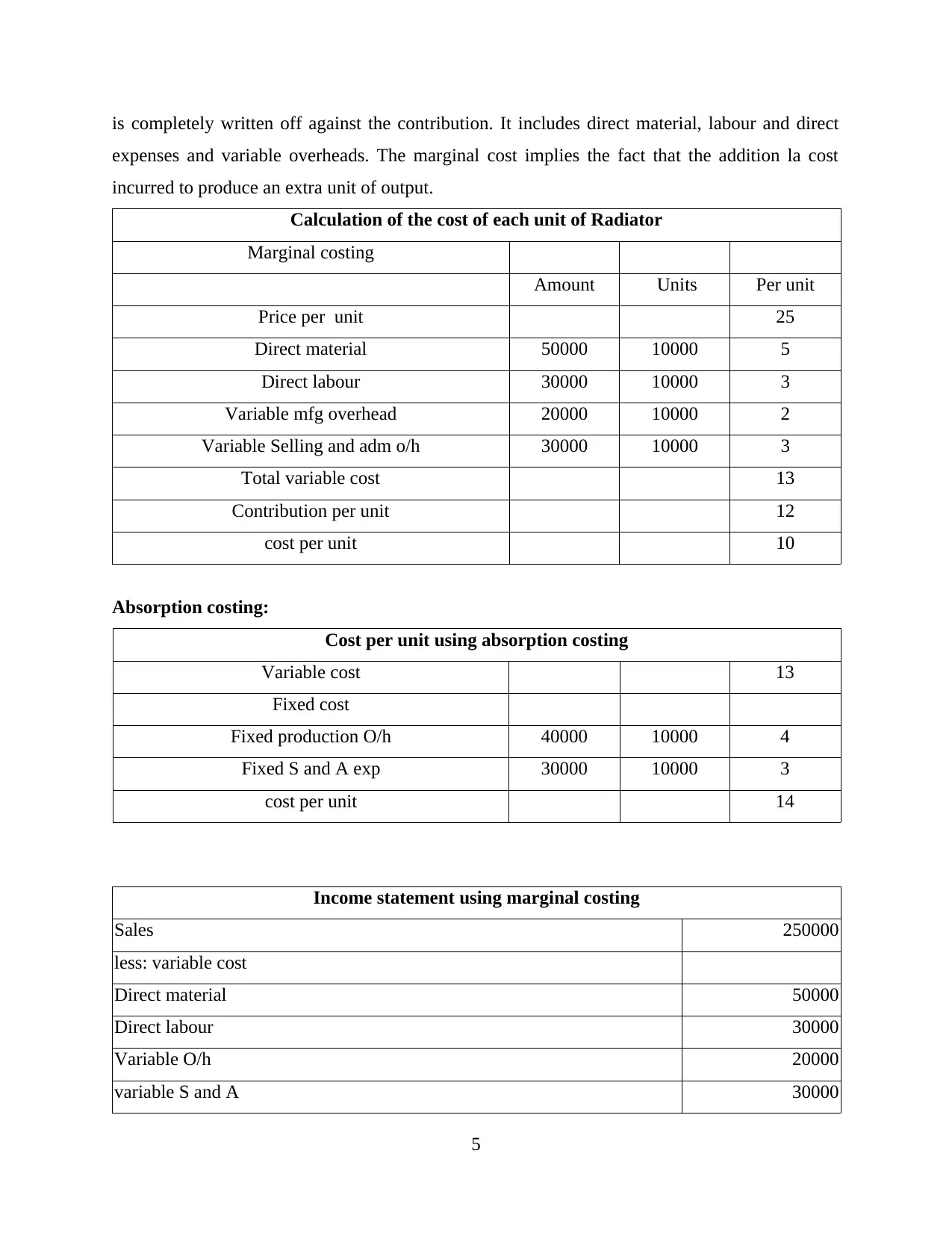

Calculation of the cost of each unit of Radiator

Marginal costing

Amount Units Per unit

Price per unit 25

Direct material 50000 10000 5

Direct labour 30000 10000 3

Variable mfg overhead 20000 10000 2

Variable Selling and adm o/h 30000 10000 3

Total variable cost 13

Contribution per unit 12

cost per unit 10

Absorption costing:

Cost per unit using absorption costing

Variable cost 13

Fixed cost

Fixed production O/h 40000 10000 4

Fixed S and A exp 30000 10000 3

cost per unit 14

Income statement using marginal costing

Sales 250000

less: variable cost

Direct material 50000

Direct labour 30000

Variable O/h 20000

variable S and A 30000

5

expenses and variable overheads. The marginal cost implies the fact that the addition la cost

incurred to produce an extra unit of output.

Calculation of the cost of each unit of Radiator

Marginal costing

Amount Units Per unit

Price per unit 25

Direct material 50000 10000 5

Direct labour 30000 10000 3

Variable mfg overhead 20000 10000 2

Variable Selling and adm o/h 30000 10000 3

Total variable cost 13

Contribution per unit 12

cost per unit 10

Absorption costing:

Cost per unit using absorption costing

Variable cost 13

Fixed cost

Fixed production O/h 40000 10000 4

Fixed S and A exp 30000 10000 3

cost per unit 14

Income statement using marginal costing

Sales 250000

less: variable cost

Direct material 50000

Direct labour 30000

Variable O/h 20000

variable S and A 30000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

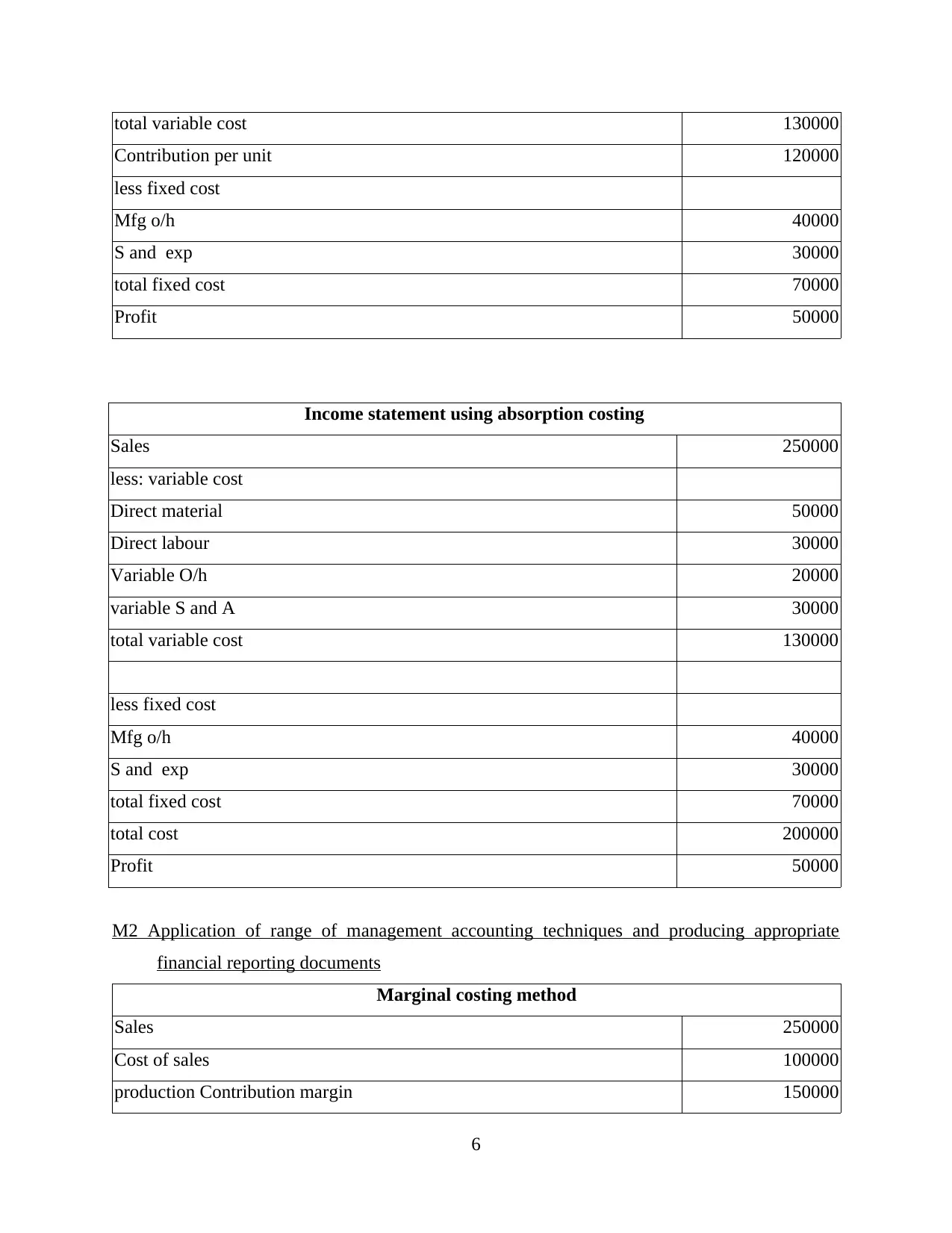

total variable cost 130000

Contribution per unit 120000

less fixed cost

Mfg o/h 40000

S and exp 30000

total fixed cost 70000

Profit 50000

Income statement using absorption costing

Sales 250000

less: variable cost

Direct material 50000

Direct labour 30000

Variable O/h 20000

variable S and A 30000

total variable cost 130000

less fixed cost

Mfg o/h 40000

S and exp 30000

total fixed cost 70000

total cost 200000

Profit 50000

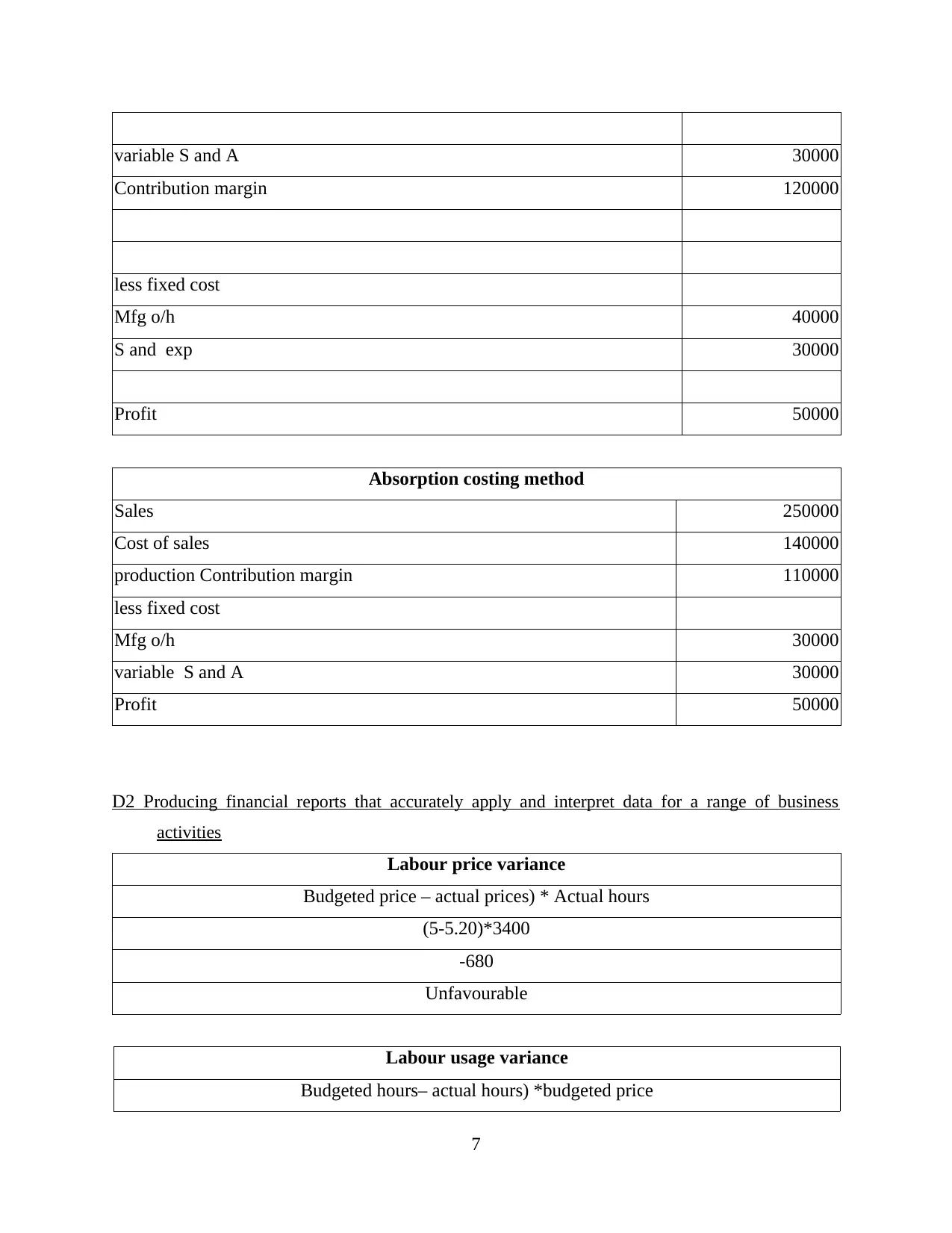

M2 Application of range of management accounting techniques and producing appropriate

financial reporting documents

Marginal costing method

Sales 250000

Cost of sales 100000

production Contribution margin 150000

6

Contribution per unit 120000

less fixed cost

Mfg o/h 40000

S and exp 30000

total fixed cost 70000

Profit 50000

Income statement using absorption costing

Sales 250000

less: variable cost

Direct material 50000

Direct labour 30000

Variable O/h 20000

variable S and A 30000

total variable cost 130000

less fixed cost

Mfg o/h 40000

S and exp 30000

total fixed cost 70000

total cost 200000

Profit 50000

M2 Application of range of management accounting techniques and producing appropriate

financial reporting documents

Marginal costing method

Sales 250000

Cost of sales 100000

production Contribution margin 150000

6

variable S and A 30000

Contribution margin 120000

less fixed cost

Mfg o/h 40000

S and exp 30000

Profit 50000

Absorption costing method

Sales 250000

Cost of sales 140000

production Contribution margin 110000

less fixed cost

Mfg o/h 30000

variable S and A 30000

Profit 50000

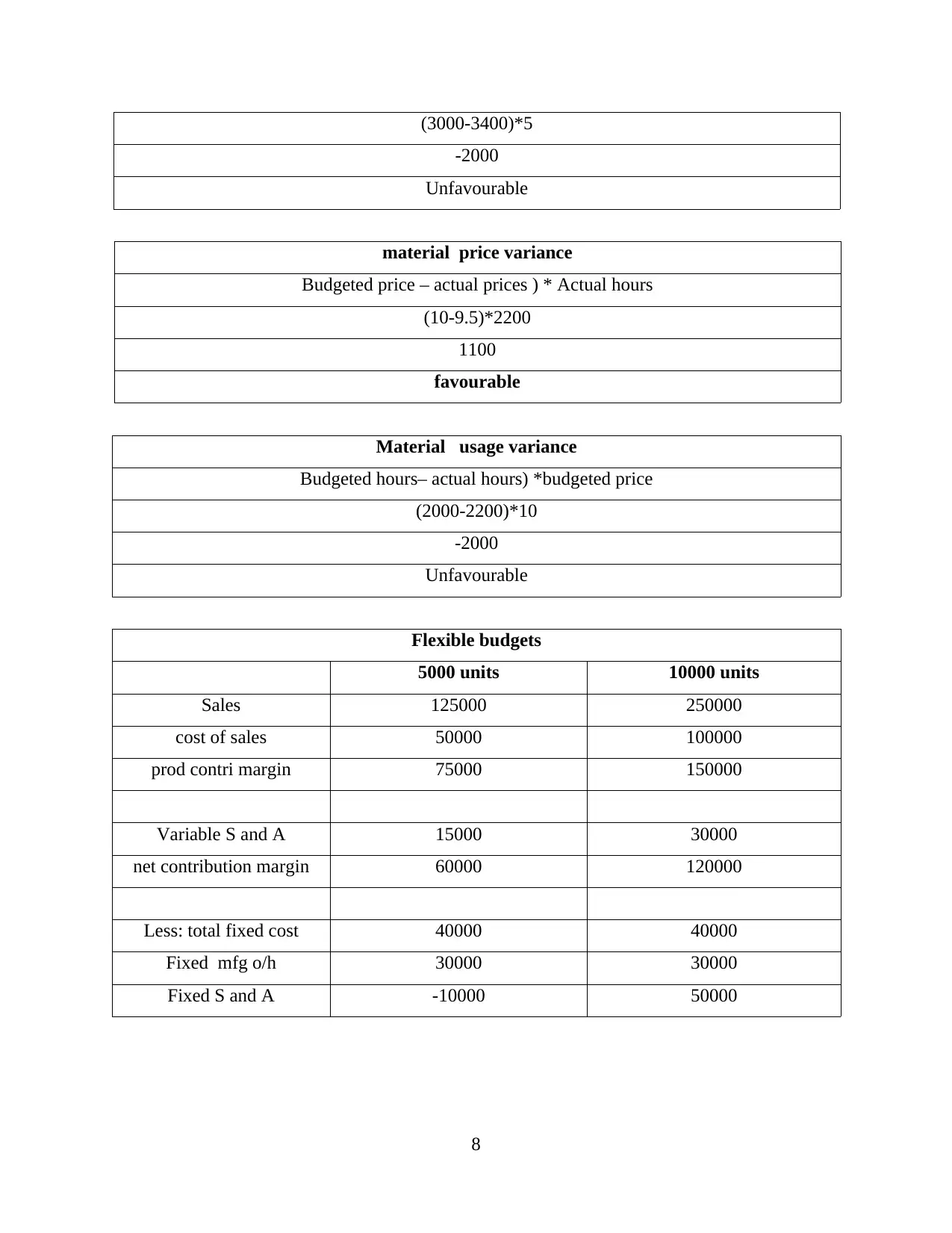

D2 Producing financial reports that accurately apply and interpret data for a range of business

activities

Labour price variance

Budgeted price – actual prices) * Actual hours

(5-5.20)*3400

-680

Unfavourable

Labour usage variance

Budgeted hours– actual hours) *budgeted price

7

Contribution margin 120000

less fixed cost

Mfg o/h 40000

S and exp 30000

Profit 50000

Absorption costing method

Sales 250000

Cost of sales 140000

production Contribution margin 110000

less fixed cost

Mfg o/h 30000

variable S and A 30000

Profit 50000

D2 Producing financial reports that accurately apply and interpret data for a range of business

activities

Labour price variance

Budgeted price – actual prices) * Actual hours

(5-5.20)*3400

-680

Unfavourable

Labour usage variance

Budgeted hours– actual hours) *budgeted price

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(3000-3400)*5

-2000

Unfavourable

material price variance

Budgeted price – actual prices ) * Actual hours

(10-9.5)*2200

1100

favourable

Material usage variance

Budgeted hours– actual hours) *budgeted price

(2000-2200)*10

-2000

Unfavourable

Flexible budgets

5000 units 10000 units

Sales 125000 250000

cost of sales 50000 100000

prod contri margin 75000 150000

Variable S and A 15000 30000

net contribution margin 60000 120000

Less: total fixed cost 40000 40000

Fixed mfg o/h 30000 30000

Fixed S and A -10000 50000

8

-2000

Unfavourable

material price variance

Budgeted price – actual prices ) * Actual hours

(10-9.5)*2200

1100

favourable

Material usage variance

Budgeted hours– actual hours) *budgeted price

(2000-2200)*10

-2000

Unfavourable

Flexible budgets

5000 units 10000 units

Sales 125000 250000

cost of sales 50000 100000

prod contri margin 75000 150000

Variable S and A 15000 30000

net contribution margin 60000 120000

Less: total fixed cost 40000 40000

Fixed mfg o/h 30000 30000

Fixed S and A -10000 50000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P4 Explaining advantages and disadvantages of different types of planning tools for budgetary

control

Zero based budget:

The advantage of this budget can be described as it insures that mangers are creditable for

spending every penny of the organisation and also force them to justify al the operating expense.

This budgeting assist in prevention of misallocation of the resources when done correctly

(Boiral, 2016). The disadvantage of this planning tool are that it rewards the short term thinking

by allowing the shift of the resources to that area of the company which can generate good

profits in coming financial year which results in non tiding to the long term revenues. Moreover,

this is resource intensive which means it takes more effort and time to review and justify the

elements of budgets.

Cash budgets:

The benefits of cash budget can be outlined as this aids in determination of the fact that

whether the cash balance with the organisation is sufficient or not to regulate its operations with

limited liquidity position. This budgets identify the amount of cash required to meet the

immediate obligation of the business (The Advantages and Disadvantages of Using Cash

Budgeting, 2018). The drawback of this budget can explained as it causes distortions and the

cash inflows do not match with the profits. Cash inflows resulting from security deposits, fines,

the sale of capital assets, or any other one-off, non-sustainable activity do not necessarily

represent reliable ongoing sources of revenue.

Sales budgets:

The pros of the sales budgets can be defined as this is planning oriented and the process

of cretin the budgets takes the management away from its short term and day to day management

and force it to think for the log term objectives and goals of the business. The con of this budget

is that it controls the expenditure on all the resources including money, materiel, facilities and

people and makes it difficult to reach the forecasted sales target.

Fixed cost budgets:

The advantages of fixed budget is that it is easy to implement and to follow and this do not

require regular updates in accounting period (Maas, Schaltegger and Crutzen, 2016). This allows

the organisation to see the area do over and under estimation of the expenses and revenues so

alternation can be made timely. The disadvantages of this budget can be stated as it does not

9

control

Zero based budget:

The advantage of this budget can be described as it insures that mangers are creditable for

spending every penny of the organisation and also force them to justify al the operating expense.

This budgeting assist in prevention of misallocation of the resources when done correctly

(Boiral, 2016). The disadvantage of this planning tool are that it rewards the short term thinking

by allowing the shift of the resources to that area of the company which can generate good

profits in coming financial year which results in non tiding to the long term revenues. Moreover,

this is resource intensive which means it takes more effort and time to review and justify the

elements of budgets.

Cash budgets:

The benefits of cash budget can be outlined as this aids in determination of the fact that

whether the cash balance with the organisation is sufficient or not to regulate its operations with

limited liquidity position. This budgets identify the amount of cash required to meet the

immediate obligation of the business (The Advantages and Disadvantages of Using Cash

Budgeting, 2018). The drawback of this budget can explained as it causes distortions and the

cash inflows do not match with the profits. Cash inflows resulting from security deposits, fines,

the sale of capital assets, or any other one-off, non-sustainable activity do not necessarily

represent reliable ongoing sources of revenue.

Sales budgets:

The pros of the sales budgets can be defined as this is planning oriented and the process

of cretin the budgets takes the management away from its short term and day to day management

and force it to think for the log term objectives and goals of the business. The con of this budget

is that it controls the expenditure on all the resources including money, materiel, facilities and

people and makes it difficult to reach the forecasted sales target.

Fixed cost budgets:

The advantages of fixed budget is that it is easy to implement and to follow and this do not

require regular updates in accounting period (Maas, Schaltegger and Crutzen, 2016). This allows

the organisation to see the area do over and under estimation of the expenses and revenues so

alternation can be made timely. The disadvantages of this budget can be stated as it does not

9

consider the flexibly approach and do not considerer the change in the level of sales and

increased volume. This is based on earlier data so it is difficult to establish and implement it.

M3 Analysing the use of different planning tools and their application

The budging is the formulation of the plans for the given future period in the numeric

terms. The organisations establish different budgets for the units, departments, job, division or

for the whole organisation. The budgets are used as planning tools they serve various purposes

for them manager in the controlling and measuring the performance of the organisation. The

various king of planning tools used in budgetary control are:

Zero based budget: is a method of budgeting where all the expanses are justified for

each new period. In this all the expenses are determined form zero level and no reference or

increment form the part budgets is taken (Zero Based Budgeting, 2018). This is useful for the

organisation to determined the actual cost and expenses incurred in the business pertaining to a

single accounting year. Budgets are then built around what is needed for the upcoming period,

regardless of whether each budget is higher or lower than the previous one.

Cash budgets: are responsibly for forecasting the cash receipts and the disbursement of

cash against the actual cash expenditure. It gives essential control to the organisation by breaking

down the inflow and out flow of the cash on monthly, weekly and yearly basis. This budget

make sure that the organisation is able to meet its current obligation by remaining in the

stipulated by budgeted funds.

Sales budgets: have direct focus on the income of the business which is expects to

receive from the normal and regular operation of the organisational activity. It is essential for the

firm as it assist the manager in understanding of the facts that at what financial position business

will be.

Fixed cost budgets: are those which ascertain the expenses which the business is

required it incurs whether the business activities are operating or not. The budgets include the

expenses related with salary and wages, rent, maintenance cost of plant and machinery,

electricity bill.

P5 Comparing the adaption of management accounting system to respond to financial problems

Identification of the

financial problem

Method 1 Method 2 Conclusion

The business is faced KPI: A Key Another option For this issue the

10

increased volume. This is based on earlier data so it is difficult to establish and implement it.

M3 Analysing the use of different planning tools and their application

The budging is the formulation of the plans for the given future period in the numeric

terms. The organisations establish different budgets for the units, departments, job, division or

for the whole organisation. The budgets are used as planning tools they serve various purposes

for them manager in the controlling and measuring the performance of the organisation. The

various king of planning tools used in budgetary control are:

Zero based budget: is a method of budgeting where all the expanses are justified for

each new period. In this all the expenses are determined form zero level and no reference or

increment form the part budgets is taken (Zero Based Budgeting, 2018). This is useful for the

organisation to determined the actual cost and expenses incurred in the business pertaining to a

single accounting year. Budgets are then built around what is needed for the upcoming period,

regardless of whether each budget is higher or lower than the previous one.

Cash budgets: are responsibly for forecasting the cash receipts and the disbursement of

cash against the actual cash expenditure. It gives essential control to the organisation by breaking

down the inflow and out flow of the cash on monthly, weekly and yearly basis. This budget

make sure that the organisation is able to meet its current obligation by remaining in the

stipulated by budgeted funds.

Sales budgets: have direct focus on the income of the business which is expects to

receive from the normal and regular operation of the organisational activity. It is essential for the

firm as it assist the manager in understanding of the facts that at what financial position business

will be.

Fixed cost budgets: are those which ascertain the expenses which the business is

required it incurs whether the business activities are operating or not. The budgets include the

expenses related with salary and wages, rent, maintenance cost of plant and machinery,

electricity bill.

P5 Comparing the adaption of management accounting system to respond to financial problems

Identification of the

financial problem

Method 1 Method 2 Conclusion

The business is faced KPI: A Key Another option For this issue the

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.