Management Accounting: Systems, Techniques and Reporting

VerifiedAdded on 2020/12/29

|21

|5511

|494

Report

AI Summary

This report provides a comprehensive overview of management accounting, exploring its core principles and applications within business organizations. It delves into the significance of management accounting in aiding decision-making by providing accurate and timely data. The report examines various management accounting systems, including cost accounting and inventory management, and their roles in optimizing profitability and market share. It also discusses different reporting methods, such as budgets and performance reports, and the importance of these reports for internal stakeholders. Furthermore, the report analyzes several management accounting techniques, including marginal costing and absorption costing, highlighting their advantages and disadvantages in different scenarios. The annexures provide raw data and financial statements to support the analysis. Overall, the report demonstrates how management accounting systems and techniques help businesses manage costs, improve operational efficiency, and make informed strategic decisions.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

Management Accounting & its requirements..............................................................................1

Methods of management accounting reporting............................................................................3

Different types of Management Accounting Techniques............................................................4

ANNEX A....................................................................................................................................5

ANNEX B..................................................................................................................................10

ACTIVITY 2..................................................................................................................................11

Advantage & Disadvantage of planning tools...........................................................................11

ANNEX C..................................................................................................................................14

Adaption of management accounting system for resolving financial problems........................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

Management Accounting & its requirements..............................................................................1

Methods of management accounting reporting............................................................................3

Different types of Management Accounting Techniques............................................................4

ANNEX A....................................................................................................................................5

ANNEX B..................................................................................................................................10

ACTIVITY 2..................................................................................................................................11

Advantage & Disadvantage of planning tools...........................................................................11

ANNEX C..................................................................................................................................14

Adaption of management accounting system for resolving financial problems........................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting is basically the process which involves preparing of the

management reports which helps to ascertain the accurate and timely data to the users so that

financial and statistical information generated from the reports can be used by them in their

decision-making.

The present study is based on the management accounting system which focuses on

preparation of the effective and efficient reports which help users to aid decision making.

Different costing techniques, planning tools of budgetary control will also be explained in the

report for their understanding and requirements in the organisation. In addition to this different

type some of the methods used for the management accounting reporting will be discussed in the

report. Some tools which are generally used by the management which helps in solving the

financial problems will also be explained in the given report for effective learnings of the entire

management accounting systems.

ACTIVITY 1

Management Accounting & its requirements

Management Accounting is an accounting process according to which benefits managers

of a business organisation in making important decision so that organisation can run smoothly

and can achieve more profits. With this accounting method managers of company analyse

financial information of firm and plan & project its future financials.

Through manager accounting managers are able to eliminate unnecessary cost incurred

during production and distribution process so that performance and efficiency of companies

operations can be improved(Ax and Greve, 2017).

Management Accounting Systems

Systems of management accounting is used in an business organisation to improve its

profitably and market share by managing cost and by preparing & formulating various reports &

plans. Various management accounting systems are used by companies for different purpose,

these systems are discussed below-

Cost Accounting System

According to (Boučková, 2015), Cost Accounting System is an essential requirement of

management accounting as it enable manager in making decisions regarding allocation of cost to

the different production departments and different products.

1

Management accounting is basically the process which involves preparing of the

management reports which helps to ascertain the accurate and timely data to the users so that

financial and statistical information generated from the reports can be used by them in their

decision-making.

The present study is based on the management accounting system which focuses on

preparation of the effective and efficient reports which help users to aid decision making.

Different costing techniques, planning tools of budgetary control will also be explained in the

report for their understanding and requirements in the organisation. In addition to this different

type some of the methods used for the management accounting reporting will be discussed in the

report. Some tools which are generally used by the management which helps in solving the

financial problems will also be explained in the given report for effective learnings of the entire

management accounting systems.

ACTIVITY 1

Management Accounting & its requirements

Management Accounting is an accounting process according to which benefits managers

of a business organisation in making important decision so that organisation can run smoothly

and can achieve more profits. With this accounting method managers of company analyse

financial information of firm and plan & project its future financials.

Through manager accounting managers are able to eliminate unnecessary cost incurred

during production and distribution process so that performance and efficiency of companies

operations can be improved(Ax and Greve, 2017).

Management Accounting Systems

Systems of management accounting is used in an business organisation to improve its

profitably and market share by managing cost and by preparing & formulating various reports &

plans. Various management accounting systems are used by companies for different purpose,

these systems are discussed below-

Cost Accounting System

According to (Boučková, 2015), Cost Accounting System is an essential requirement of

management accounting as it enable manager in making decisions regarding allocation of cost to

the different production departments and different products.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This is the most important management accounting systems which is required to use in

managing different types of cost of manufacturing such as labour cost, cost of material and

overhead cost. With this accounting system a company is able to sale its product and services at a

lower price by minimising cost and setting up higher profit margin which in turn enhances

profitability and performance. This systems also required for companies in tracking its inventory

level and requirement of raw materials because cost of a product is determined after evaluating

these elements(Bromwich and Scapens, 2016).

Further, this provide various Cost Accounting Techniques with which a business

organisation is able to analyse cost of its product and service and make budget of future expenses

of production. These accounting techniques are Job Costing, Process Costing, Contract Costing,

Marginal Costing and Services Costing. This is beneficial for a business venture which is

including wide range of products and services in its product portfolio. Because, this type of

companies can use suitable techniques of each department to determine and manage cost.

This system is also required in management accounting as it compare actual cost of

product with the standard cost, differentiate direct & indirect cost and operating and non

operating expenses. Inventory Management System

This system is also an essential requirement of management accounting according to (),

as it helps manager of production department by determining requirement and availability of

inventory. Further, manager are able to manage inventory according to demand of customers and

requirement of production department. It is necessary for a company to manage its stock as

without inventory a company can not manufacture its goods and services.

Further, this system uses various software's so that inventory managers can track level of

inventory, sales volume and cost of inventory available. Further, this system is require to

generate bill of all the material included in production process and supports in placing orders.

Most important benefit of this system is it helps managers in managing supply chain of a

company as without checking inventory level a company is unable to place further order for raw

materials(Carlsson-Wall, Kraus and Lind, 2015). Job Costing Systems

This system is required as with this manager can determine cost involved in a particular

job and it gives all the related information of manufacturing cost of each job separately which in

2

managing different types of cost of manufacturing such as labour cost, cost of material and

overhead cost. With this accounting system a company is able to sale its product and services at a

lower price by minimising cost and setting up higher profit margin which in turn enhances

profitability and performance. This systems also required for companies in tracking its inventory

level and requirement of raw materials because cost of a product is determined after evaluating

these elements(Bromwich and Scapens, 2016).

Further, this provide various Cost Accounting Techniques with which a business

organisation is able to analyse cost of its product and service and make budget of future expenses

of production. These accounting techniques are Job Costing, Process Costing, Contract Costing,

Marginal Costing and Services Costing. This is beneficial for a business venture which is

including wide range of products and services in its product portfolio. Because, this type of

companies can use suitable techniques of each department to determine and manage cost.

This system is also required in management accounting as it compare actual cost of

product with the standard cost, differentiate direct & indirect cost and operating and non

operating expenses. Inventory Management System

This system is also an essential requirement of management accounting according to (),

as it helps manager of production department by determining requirement and availability of

inventory. Further, manager are able to manage inventory according to demand of customers and

requirement of production department. It is necessary for a company to manage its stock as

without inventory a company can not manufacture its goods and services.

Further, this system uses various software's so that inventory managers can track level of

inventory, sales volume and cost of inventory available. Further, this system is require to

generate bill of all the material included in production process and supports in placing orders.

Most important benefit of this system is it helps managers in managing supply chain of a

company as without checking inventory level a company is unable to place further order for raw

materials(Carlsson-Wall, Kraus and Lind, 2015). Job Costing Systems

This system is required as with this manager can determine cost involved in a particular

job and it gives all the related information of manufacturing cost of each job separately which in

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

turn benefits manager in resolving problems of each product and job. According to (Chenhall

and Moers, 2015), Event Management Companies and Furniture Manufacturers uses this system

because this businesses manufacture different type of products. Price Optimising System

Price Optimising System benefits a business organisation in setting its prices which gives

satisfaction to customers. Further, with this systems manager can track change in customers

demand of products & services according to changes made in prices and with this they made

pricing decisions. Thus, this system is also an important requirement of management accounting.

Benefits of Management Accounting Systems

Management Accounting is important as with this managers can make various decisions

such cost minimisation, price determination and inventory management which in turn

enhance profits, market share and customer base of the business organisations. Further,

theses accounting systems are also important for companies as it provides optimum utilisation

of resources which in turn enhances production output and sales volume by managing waste.

Further, systems of management accounting is beneficial for companies by determining

framework of operating activities related to business.

Systems of management accounting is applied in various departments of an organisation

such as marketing, manufacturing, selling and financial(Hald and Thrane, 2016).

Methods of management accounting reporting

Management Accounting Reports are prepared and presented by business organizations

with the purpose of making important decision and resolving problems occurred in different

department. This reports are also used by managers for evaluating efficiency of companies

financials and operations. Further, future plans of companies are formulated on the basis of

previous years reports. These reports are presented to internal users of companies only and

prepared according to the understanding of managers. It is not required by manager's to follow

all the accounting principles during the preparation of management accounting reports.

Types of Management Accounting Reports Budget

Budget shows details of future expense and incomes of a business firm and it is prepared

on the basis of historical data. Thus, Budget Report is used by managers to monitor and control

cost so that operations of company can be operated according to the allocated cost in future

3

and Moers, 2015), Event Management Companies and Furniture Manufacturers uses this system

because this businesses manufacture different type of products. Price Optimising System

Price Optimising System benefits a business organisation in setting its prices which gives

satisfaction to customers. Further, with this systems manager can track change in customers

demand of products & services according to changes made in prices and with this they made

pricing decisions. Thus, this system is also an important requirement of management accounting.

Benefits of Management Accounting Systems

Management Accounting is important as with this managers can make various decisions

such cost minimisation, price determination and inventory management which in turn

enhance profits, market share and customer base of the business organisations. Further,

theses accounting systems are also important for companies as it provides optimum utilisation

of resources which in turn enhances production output and sales volume by managing waste.

Further, systems of management accounting is beneficial for companies by determining

framework of operating activities related to business.

Systems of management accounting is applied in various departments of an organisation

such as marketing, manufacturing, selling and financial(Hald and Thrane, 2016).

Methods of management accounting reporting

Management Accounting Reports are prepared and presented by business organizations

with the purpose of making important decision and resolving problems occurred in different

department. This reports are also used by managers for evaluating efficiency of companies

financials and operations. Further, future plans of companies are formulated on the basis of

previous years reports. These reports are presented to internal users of companies only and

prepared according to the understanding of managers. It is not required by manager's to follow

all the accounting principles during the preparation of management accounting reports.

Types of Management Accounting Reports Budget

Budget shows details of future expense and incomes of a business firm and it is prepared

on the basis of historical data. Thus, Budget Report is used by managers to monitor and control

cost so that operations of company can be operated according to the allocated cost in future

3

Financial plan. Further, companies develop budget for different departments which helps

managers in evaluating performance of each department.

This report is essential for management accounting as with this managers are able to set

incentives for their employees and can negotiate with suppliers for prices of raw

material(Honggowati and et.al., 2017). Cost Accounting Reports

These reports are prepared for computation, controlling and monitoring cost involved in

manufacturing of products. All types of cost such as raw material, indirect & direct labour and

Overheads are included in this reports with this managers are able to make decisions related to

cost reduction, management of waste, determining cost of overheads and labour. This report

gives an exact information of expenses incurred by company. Performance Reports

Performance Reports are prepared with the purpose of analysing financial, managerial

and operational performance of a business organisations. Managers of a business firm set future

objectives and goals in accordance with these reports. Further, this reports also helps managers in

developing future strategies so that organisation can achieve higher profits and market share.

Different types of Management Accounting Techniques

Management Accounting Techniques

Management Accounting techniques are used by business organisation with the purpose

of managing risk, developing strategies and taking decision related to business expansion. This

techniques are used by businesses for analysing both financial and non financial information.

Various management accounting use by companies are discussed below-

Marginal Costing

Marginal Cost consider additional cost incurred in production of goods and services due

to increase in sales units. Thus, these technique of management accounting helps business firms

in calculating and determining extra cost included in production process (Marginal Cost). This

techniques gives accurate amount of profit to the business firms as manufacturing cost of product

is controlled and monitored on a daily basis and manager make decisions to improve the cost

with the changes(Jansen, 2018).

Advantage

4

managers in evaluating performance of each department.

This report is essential for management accounting as with this managers are able to set

incentives for their employees and can negotiate with suppliers for prices of raw

material(Honggowati and et.al., 2017). Cost Accounting Reports

These reports are prepared for computation, controlling and monitoring cost involved in

manufacturing of products. All types of cost such as raw material, indirect & direct labour and

Overheads are included in this reports with this managers are able to make decisions related to

cost reduction, management of waste, determining cost of overheads and labour. This report

gives an exact information of expenses incurred by company. Performance Reports

Performance Reports are prepared with the purpose of analysing financial, managerial

and operational performance of a business organisations. Managers of a business firm set future

objectives and goals in accordance with these reports. Further, this reports also helps managers in

developing future strategies so that organisation can achieve higher profits and market share.

Different types of Management Accounting Techniques

Management Accounting Techniques

Management Accounting techniques are used by business organisation with the purpose

of managing risk, developing strategies and taking decision related to business expansion. This

techniques are used by businesses for analysing both financial and non financial information.

Various management accounting use by companies are discussed below-

Marginal Costing

Marginal Cost consider additional cost incurred in production of goods and services due

to increase in sales units. Thus, these technique of management accounting helps business firms

in calculating and determining extra cost included in production process (Marginal Cost). This

techniques gives accurate amount of profit to the business firms as manufacturing cost of product

is controlled and monitored on a daily basis and manager make decisions to improve the cost

with the changes(Jansen, 2018).

Advantage

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It benefits manager in managing and controlling marginal cost as this techniques

considers only variable cost.

This techniques gives appropriate overhead recovery rate.

Marginal costing benefits business organisation in maximising their profits as this

method gives highest profit as compared to all the other methods.

Disadvantage

This method does not consider fixed overhead. So, it is difficult for managers to

differentiate different types of cost.

Marginal Costing is not helpful for long term decision making. This method is not able to classify semi variable cost which in tuen gives inappropriate

profits.

Absorption Costing

Absorption Costing techniques measure amount of cost by considering both direct cost

and indirect cost. As this techniques consider all coat related to manufacturing its helps business

firms in calculating amount of net profit. Further, managers are able to prepare Statement of

profit & loss by using this technique of management accounting(Kaplan and Atkinson, 2015).

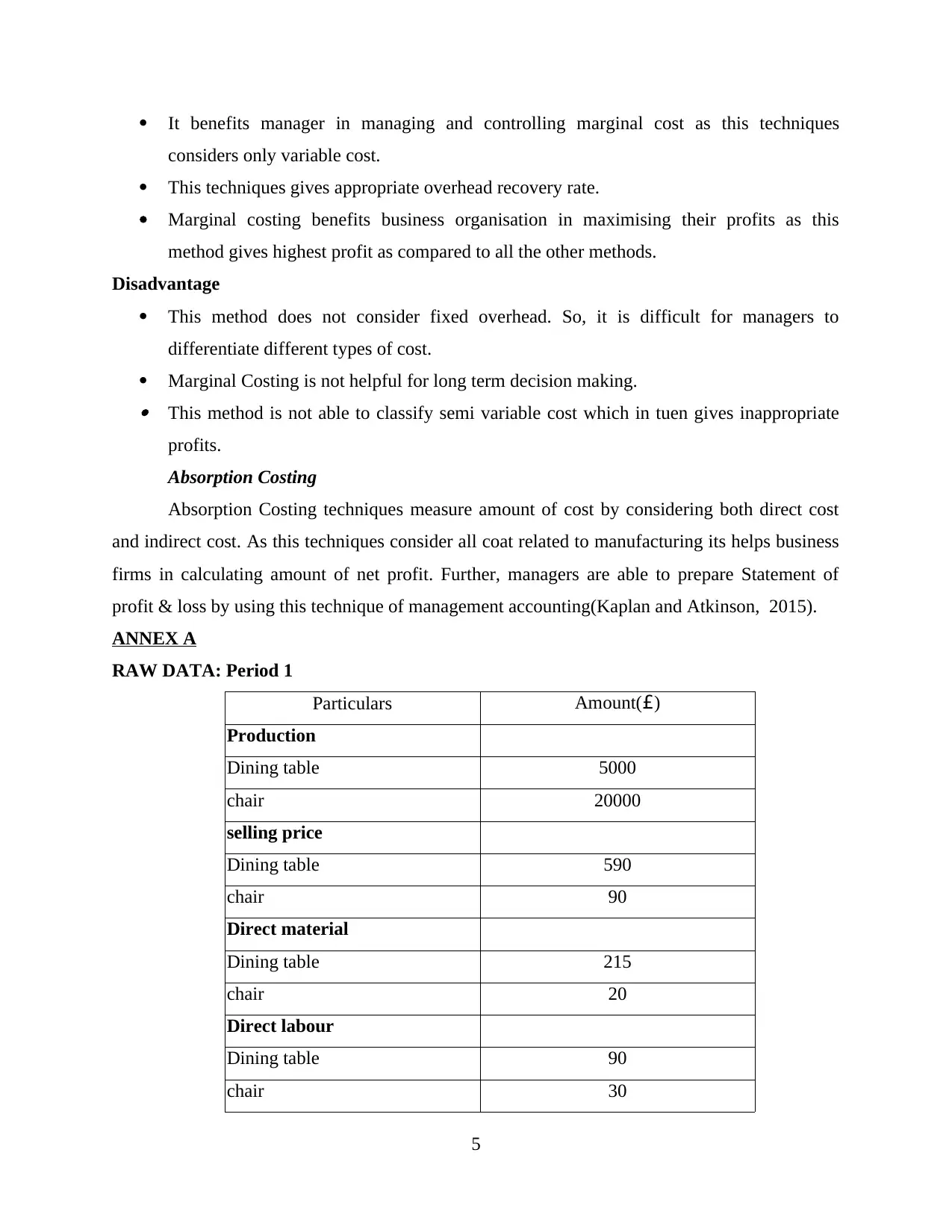

ANNEX A

RAW DATA: Period 1

Particulars Amount(£)

Production

Dining table 5000

chair 20000

selling price

Dining table 590

chair 90

Direct material

Dining table 215

chair 20

Direct labour

Dining table 90

chair 30

5

considers only variable cost.

This techniques gives appropriate overhead recovery rate.

Marginal costing benefits business organisation in maximising their profits as this

method gives highest profit as compared to all the other methods.

Disadvantage

This method does not consider fixed overhead. So, it is difficult for managers to

differentiate different types of cost.

Marginal Costing is not helpful for long term decision making. This method is not able to classify semi variable cost which in tuen gives inappropriate

profits.

Absorption Costing

Absorption Costing techniques measure amount of cost by considering both direct cost

and indirect cost. As this techniques consider all coat related to manufacturing its helps business

firms in calculating amount of net profit. Further, managers are able to prepare Statement of

profit & loss by using this technique of management accounting(Kaplan and Atkinson, 2015).

ANNEX A

RAW DATA: Period 1

Particulars Amount(£)

Production

Dining table 5000

chair 20000

selling price

Dining table 590

chair 90

Direct material

Dining table 215

chair 20

Direct labour

Dining table 90

chair 30

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

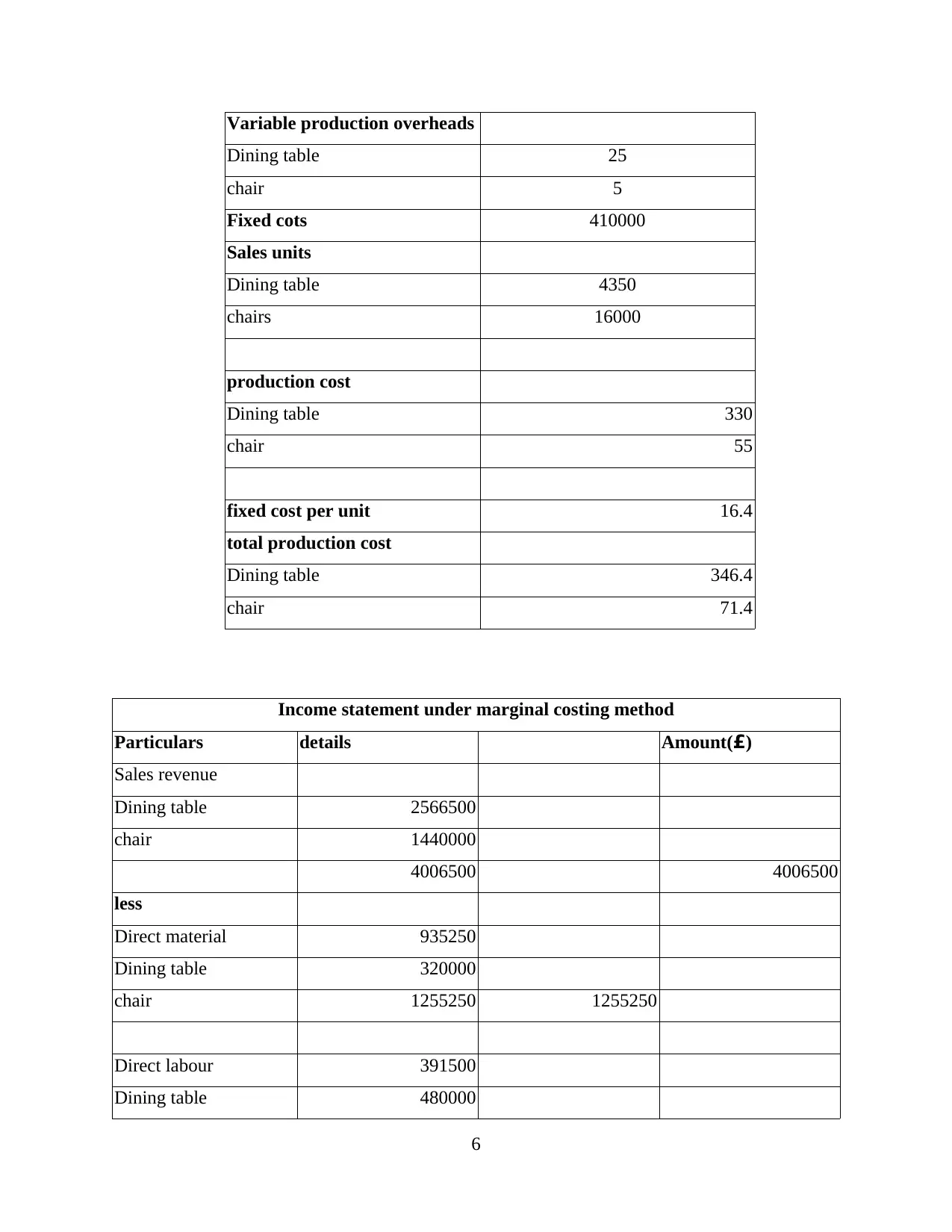

Variable production overheads

Dining table 25

chair 5

Fixed cots 410000

Sales units

Dining table 4350

chairs 16000

production cost

Dining table 330

chair 55

fixed cost per unit 16.4

total production cost

Dining table 346.4

chair 71.4

Income statement under marginal costing method

Particulars details Amount(£)

Sales revenue

Dining table 2566500

chair 1440000

4006500 4006500

less

Direct material 935250

Dining table 320000

chair 1255250 1255250

Direct labour 391500

Dining table 480000

6

Dining table 25

chair 5

Fixed cots 410000

Sales units

Dining table 4350

chairs 16000

production cost

Dining table 330

chair 55

fixed cost per unit 16.4

total production cost

Dining table 346.4

chair 71.4

Income statement under marginal costing method

Particulars details Amount(£)

Sales revenue

Dining table 2566500

chair 1440000

4006500 4006500

less

Direct material 935250

Dining table 320000

chair 1255250 1255250

Direct labour 391500

Dining table 480000

6

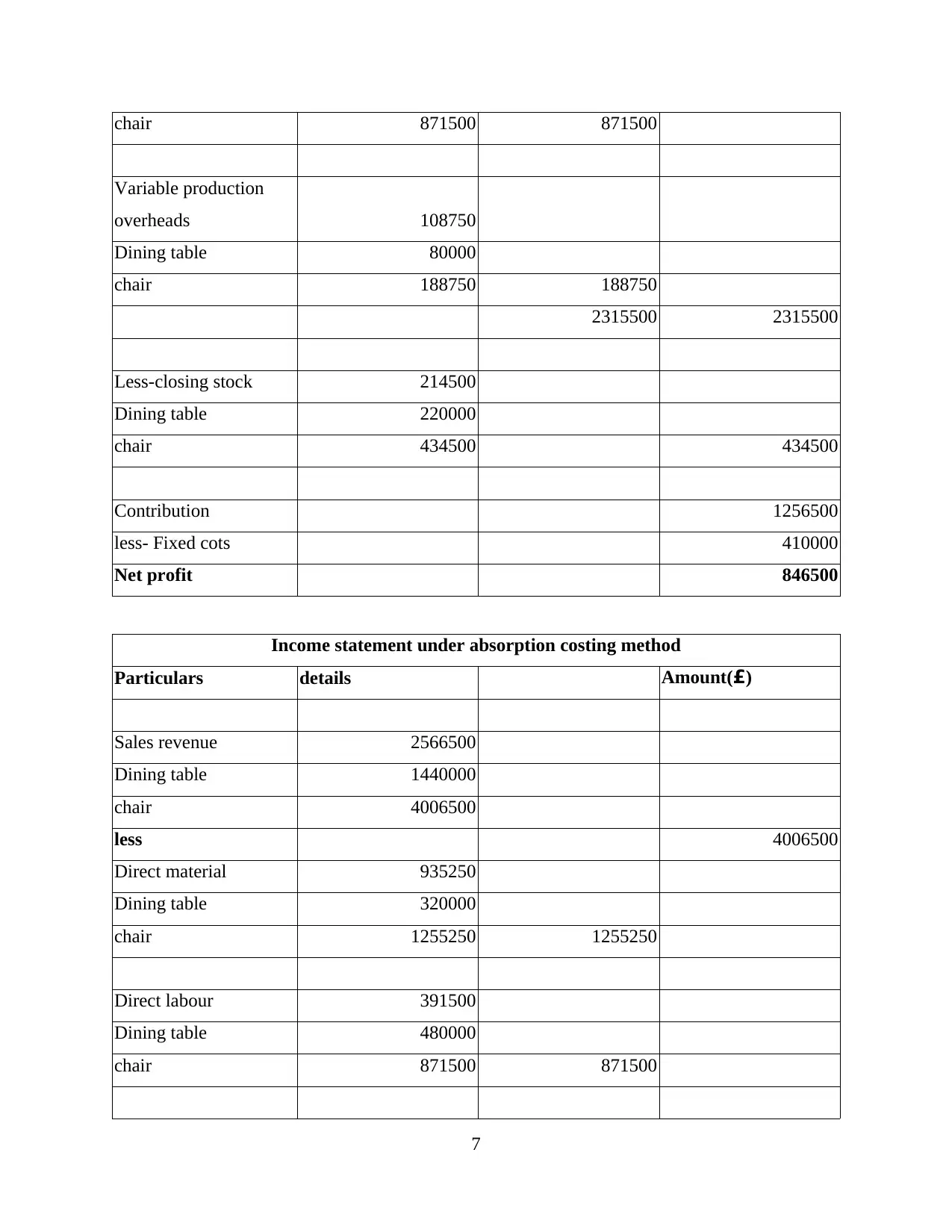

chair 871500 871500

Variable production

overheads 108750

Dining table 80000

chair 188750 188750

2315500 2315500

Less-closing stock 214500

Dining table 220000

chair 434500 434500

Contribution 1256500

less- Fixed cots 410000

Net profit 846500

Income statement under absorption costing method

Particulars details Amount(£)

Sales revenue 2566500

Dining table 1440000

chair 4006500

less 4006500

Direct material 935250

Dining table 320000

chair 1255250 1255250

Direct labour 391500

Dining table 480000

chair 871500 871500

7

Variable production

overheads 108750

Dining table 80000

chair 188750 188750

2315500 2315500

Less-closing stock 214500

Dining table 220000

chair 434500 434500

Contribution 1256500

less- Fixed cots 410000

Net profit 846500

Income statement under absorption costing method

Particulars details Amount(£)

Sales revenue 2566500

Dining table 1440000

chair 4006500

less 4006500

Direct material 935250

Dining table 320000

chair 1255250 1255250

Direct labour 391500

Dining table 480000

chair 871500 871500

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable production

overheads

Dining table 108750

chair 80000

188750 188750 2315500

less- Fixed cots 410000

Less-closing stock 410000

Dining table 225160

chair 285600 510760

510760

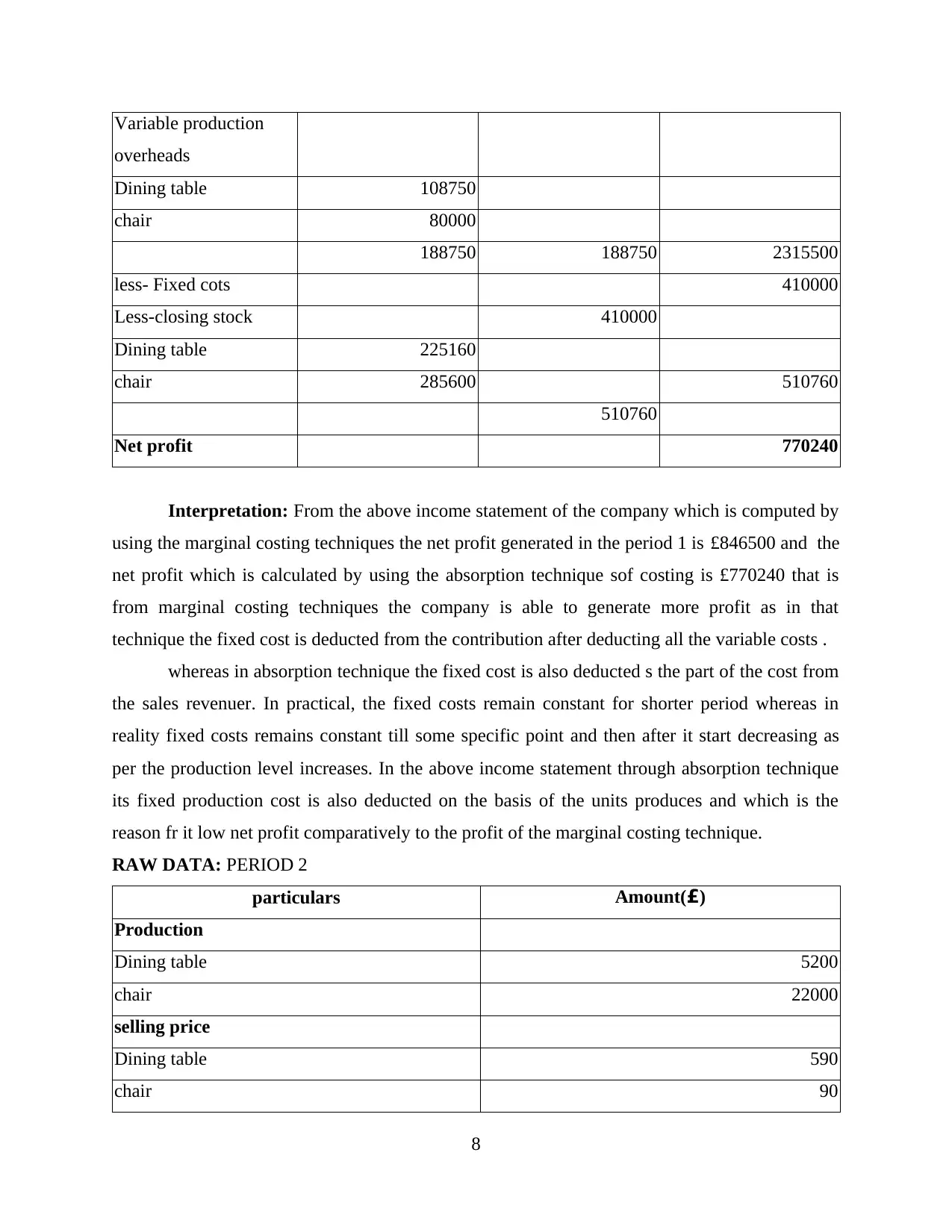

Net profit 770240

Interpretation: From the above income statement of the company which is computed by

using the marginal costing techniques the net profit generated in the period 1 is £846500 and the

net profit which is calculated by using the absorption technique sof costing is £770240 that is

from marginal costing techniques the company is able to generate more profit as in that

technique the fixed cost is deducted from the contribution after deducting all the variable costs .

whereas in absorption technique the fixed cost is also deducted s the part of the cost from

the sales revenuer. In practical, the fixed costs remain constant for shorter period whereas in

reality fixed costs remains constant till some specific point and then after it start decreasing as

per the production level increases. In the above income statement through absorption technique

its fixed production cost is also deducted on the basis of the units produces and which is the

reason fr it low net profit comparatively to the profit of the marginal costing technique.

RAW DATA: PERIOD 2

particulars Amount(£)

Production

Dining table 5200

chair 22000

selling price

Dining table 590

chair 90

8

overheads

Dining table 108750

chair 80000

188750 188750 2315500

less- Fixed cots 410000

Less-closing stock 410000

Dining table 225160

chair 285600 510760

510760

Net profit 770240

Interpretation: From the above income statement of the company which is computed by

using the marginal costing techniques the net profit generated in the period 1 is £846500 and the

net profit which is calculated by using the absorption technique sof costing is £770240 that is

from marginal costing techniques the company is able to generate more profit as in that

technique the fixed cost is deducted from the contribution after deducting all the variable costs .

whereas in absorption technique the fixed cost is also deducted s the part of the cost from

the sales revenuer. In practical, the fixed costs remain constant for shorter period whereas in

reality fixed costs remains constant till some specific point and then after it start decreasing as

per the production level increases. In the above income statement through absorption technique

its fixed production cost is also deducted on the basis of the units produces and which is the

reason fr it low net profit comparatively to the profit of the marginal costing technique.

RAW DATA: PERIOD 2

particulars Amount(£)

Production

Dining table 5200

chair 22000

selling price

Dining table 590

chair 90

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

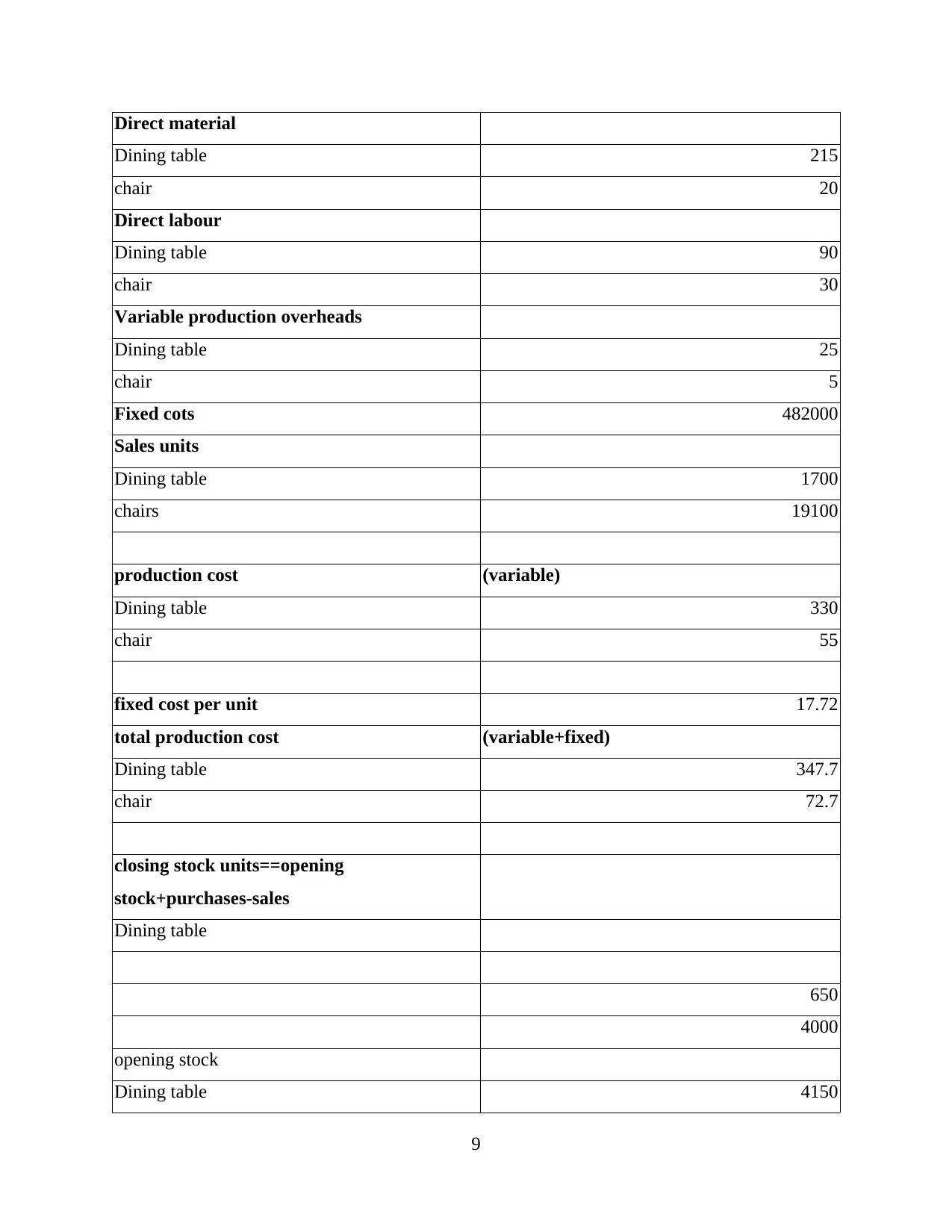

Direct material

Dining table 215

chair 20

Direct labour

Dining table 90

chair 30

Variable production overheads

Dining table 25

chair 5

Fixed cots 482000

Sales units

Dining table 1700

chairs 19100

production cost (variable)

Dining table 330

chair 55

fixed cost per unit 17.72

total production cost (variable+fixed)

Dining table 347.7

chair 72.7

closing stock units==opening

stock+purchases-sales

Dining table

650

4000

opening stock

Dining table 4150

9

Dining table 215

chair 20

Direct labour

Dining table 90

chair 30

Variable production overheads

Dining table 25

chair 5

Fixed cots 482000

Sales units

Dining table 1700

chairs 19100

production cost (variable)

Dining table 330

chair 55

fixed cost per unit 17.72

total production cost (variable+fixed)

Dining table 347.7

chair 72.7

closing stock units==opening

stock+purchases-sales

Dining table

650

4000

opening stock

Dining table 4150

9

chair 6900

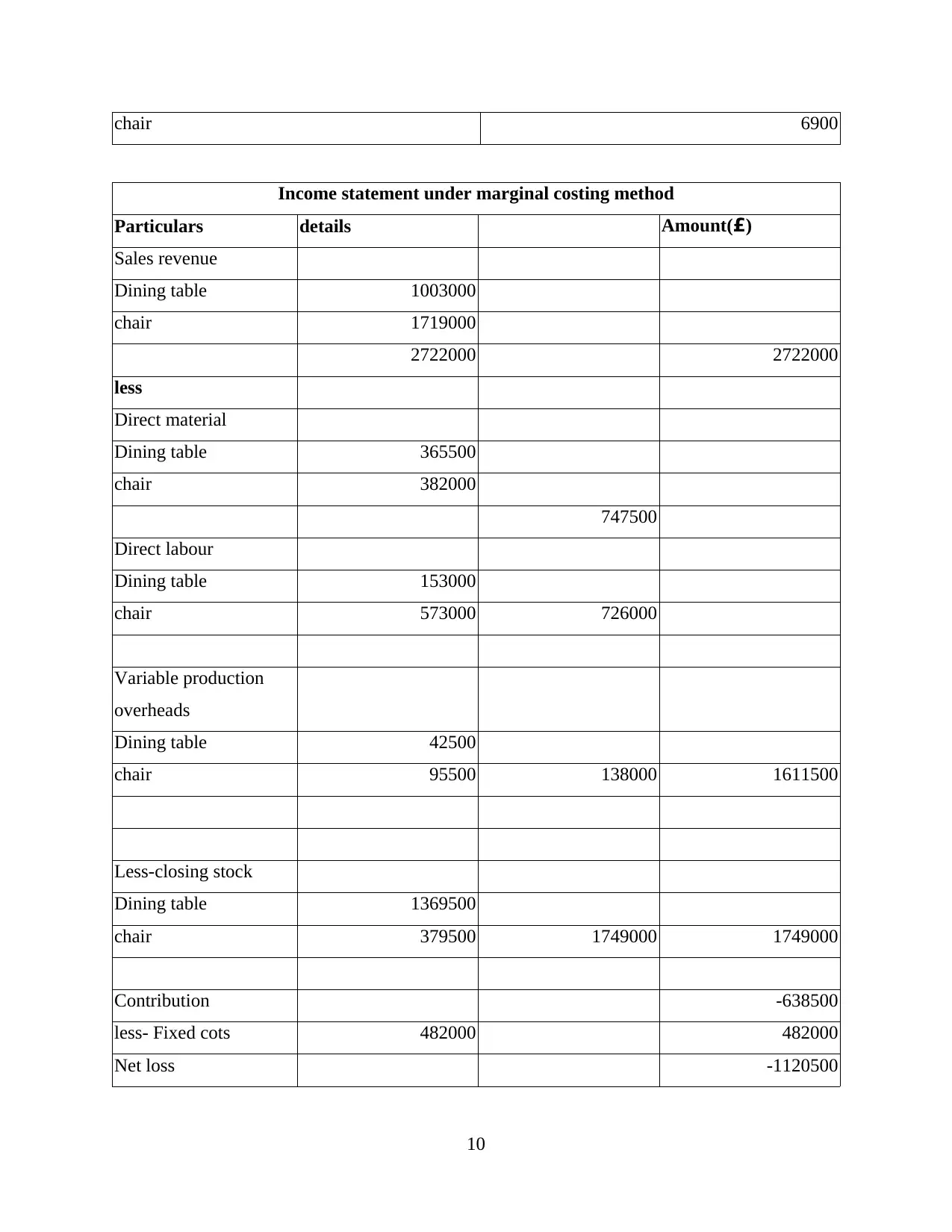

Income statement under marginal costing method

Particulars details Amount(£)

Sales revenue

Dining table 1003000

chair 1719000

2722000 2722000

less

Direct material

Dining table 365500

chair 382000

747500

Direct labour

Dining table 153000

chair 573000 726000

Variable production

overheads

Dining table 42500

chair 95500 138000 1611500

Less-closing stock

Dining table 1369500

chair 379500 1749000 1749000

Contribution -638500

less- Fixed cots 482000 482000

Net loss -1120500

10

Income statement under marginal costing method

Particulars details Amount(£)

Sales revenue

Dining table 1003000

chair 1719000

2722000 2722000

less

Direct material

Dining table 365500

chair 382000

747500

Direct labour

Dining table 153000

chair 573000 726000

Variable production

overheads

Dining table 42500

chair 95500 138000 1611500

Less-closing stock

Dining table 1369500

chair 379500 1749000 1749000

Contribution -638500

less- Fixed cots 482000 482000

Net loss -1120500

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.