Management Accounting Systems and Applications for Agmet Company

VerifiedAdded on 2020/06/06

|13

|3826

|45

Report

AI Summary

This report delves into the realm of management accounting, specifically examining its importance and applications within Agmet Company. It explores various types of management accounting, including cost accounting, inventory management, price optimization, and job costing, highlighting their significance in internal decision-making. The report details different management accounting reports such as segmental, performance, inventory management, accounts receivables ageing, and job cost reports, emphasizing their role in performance evaluation and financial control. Furthermore, it includes calculations for marginal and absorption costing, comparing their impact on the income statement, and provides a reconciled statement. The report also discusses the advantages and disadvantages of planning tools like zero-based budgeting, and how management accounting systems aid in addressing financial problems, thereby providing a comprehensive analysis of management accounting practices and their practical implications.

Management accounting

systems and its applications

1

systems and its applications

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

SECTION 1.....................................................................................................................................3

(P1) Discuss management accounting and enumerate various types of it...................................3

(P2) Types of management accounting reports...........................................................................5

(P3) Calculate marginal and absorption costing for the firm......................................................7

SECTION 2.....................................................................................................................................8

(P4) Advantages and disadvantages of planning tools................................................................8

P5) How management accounting system help to respond to financial problems......................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

2

INTRODUCTION...........................................................................................................................3

SECTION 1.....................................................................................................................................3

(P1) Discuss management accounting and enumerate various types of it...................................3

(P2) Types of management accounting reports...........................................................................5

(P3) Calculate marginal and absorption costing for the firm......................................................7

SECTION 2.....................................................................................................................................8

(P4) Advantages and disadvantages of planning tools................................................................8

P5) How management accounting system help to respond to financial problems......................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

2

INTRODUCTION

Management accounting is useful tool for managers to take effective decisions in the best

possible manner. The present report deals with Agmet Company engaged in manufacturing

chemical products and selling goods to customers for maximising their level of satisfaction quite

effectively. The report discusses about importance of management accounting information and

company should implement this accounting so that it can achieve desired objectives and

maximise productivity in the best possible way. Moreover, various management accounting

techniques are discussed and managerial reports are explained which assists manager in taking

effective decisions quite easily. Various planning tools such as NPV, IRR and other tools are

discussed which assist management whether to invest in the project or not. Marginal and

absorption costing are explained and various accounting systems are discussed which help to

respond to financial problems quite effectively.

SECTION 1

(P1) Discuss management accounting and enumerate various types of it

Management accounting is helpful for organisation so that it may take internal decisions

with much ease. Top management is benefited by such information to take better and effective

decisions in the best possible way. This information is not provided to external users, as it is

purely available to management only (Nitzl, 2018). Financial accounting provide financial data,

which are then provided to management for taking decisions for the betterment of the company.

Management accounting is concerned with reducing costs in effective way so that management

may be able to take better decisions for the betterment of the company. Agmet Company is also

utilises management accounting as it provides them with useful insight to take into account

internal strength of the company whether internal operations are up to the mark or not. If there

are any weaknesses then, corrective actions are taken quite easily.

On the other hand, management accounting not only provides useful information to the

managers but also investors and creditors be benefited by it (Pratheepkanth, 2018). However, this

information is not available for other stakeholders but management takes effective decision

which eventually help investors and creditors to take decision whether to invest funds in the

company or not. Thus, it has several features and beneficial to company in all aspects to achieve

desired goals. In addressing this, various types of management accounting are listed below-

The different types of management accounting are as follows-

3

Management accounting is useful tool for managers to take effective decisions in the best

possible manner. The present report deals with Agmet Company engaged in manufacturing

chemical products and selling goods to customers for maximising their level of satisfaction quite

effectively. The report discusses about importance of management accounting information and

company should implement this accounting so that it can achieve desired objectives and

maximise productivity in the best possible way. Moreover, various management accounting

techniques are discussed and managerial reports are explained which assists manager in taking

effective decisions quite easily. Various planning tools such as NPV, IRR and other tools are

discussed which assist management whether to invest in the project or not. Marginal and

absorption costing are explained and various accounting systems are discussed which help to

respond to financial problems quite effectively.

SECTION 1

(P1) Discuss management accounting and enumerate various types of it

Management accounting is helpful for organisation so that it may take internal decisions

with much ease. Top management is benefited by such information to take better and effective

decisions in the best possible way. This information is not provided to external users, as it is

purely available to management only (Nitzl, 2018). Financial accounting provide financial data,

which are then provided to management for taking decisions for the betterment of the company.

Management accounting is concerned with reducing costs in effective way so that management

may be able to take better decisions for the betterment of the company. Agmet Company is also

utilises management accounting as it provides them with useful insight to take into account

internal strength of the company whether internal operations are up to the mark or not. If there

are any weaknesses then, corrective actions are taken quite easily.

On the other hand, management accounting not only provides useful information to the

managers but also investors and creditors be benefited by it (Pratheepkanth, 2018). However, this

information is not available for other stakeholders but management takes effective decision

which eventually help investors and creditors to take decision whether to invest funds in the

company or not. Thus, it has several features and beneficial to company in all aspects to achieve

desired goals. In addressing this, various types of management accounting are listed below-

The different types of management accounting are as follows-

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1. Cost accounting-

This branch of accounting deals with controlling various costs and expenses which are

incurred in the production process or any other purpose. The recording and summarizing of costs

is carried out so that overall performance of company can be enhanced by reducing costs in

effectual way. The various types of costs, which are incurred in the production process, are

direct, indirect, fixed and variable costs which are allocated in that way so that these do not

exceed profit. Thus, management is benefited by such information and as such, it can take better

decisions so that costs can be controlled in a better manner. Cost efficiency is achieved by

management with the help of such much needed information. Thus, company becomes effective

and efficient to yield better results (Englund and Gerdin, 2018).

2. Inventory management system-

Inventory is important part of firm, as without it production process cannot be

accomplished by department. Stock requires to be maintain in appropriate quantity so that it may

fulfil requirement of production department in effective way. Overstocking may led to wastage

of scarce resources and management does not want to reduce profits by spoiling inventory. In

regards to this, inventory management system is established by organisation so that inventory is

not wasted and at the same time, need of production department is fulfilled eventually. Firm

places new orders on daily basis and as such, it is required that inventory may be managed in the

best possible way and customer demand may be fulfil.

3. Price optimisation-

Price optimisation is quite helpful for the company to take effective way. Agmet

Company also uses this technique to implement price in the best possible way. Price optimisation

is a mathematical analysis technique which help firm to set price in quite effective manner by

assessing consumer behaviour (Mueller and Trost, 2018). This implies that firm analysis demand

of customers which are ready to pay for the price, firm is willing to sell. If customers do not

prefer to buy commodity, then organisation quote price in accordance to their preferences. This

way company set prices by assessing demand of potential customers and quote similar price so

that they may not be driven away by the rivals.

4. Job costing-

Job costing is the major essence of the manufacturing sector. In relation to this, Agmet

Company also uses job costing so that it may be able to control upon various job expenditures in

4

This branch of accounting deals with controlling various costs and expenses which are

incurred in the production process or any other purpose. The recording and summarizing of costs

is carried out so that overall performance of company can be enhanced by reducing costs in

effectual way. The various types of costs, which are incurred in the production process, are

direct, indirect, fixed and variable costs which are allocated in that way so that these do not

exceed profit. Thus, management is benefited by such information and as such, it can take better

decisions so that costs can be controlled in a better manner. Cost efficiency is achieved by

management with the help of such much needed information. Thus, company becomes effective

and efficient to yield better results (Englund and Gerdin, 2018).

2. Inventory management system-

Inventory is important part of firm, as without it production process cannot be

accomplished by department. Stock requires to be maintain in appropriate quantity so that it may

fulfil requirement of production department in effective way. Overstocking may led to wastage

of scarce resources and management does not want to reduce profits by spoiling inventory. In

regards to this, inventory management system is established by organisation so that inventory is

not wasted and at the same time, need of production department is fulfilled eventually. Firm

places new orders on daily basis and as such, it is required that inventory may be managed in the

best possible way and customer demand may be fulfil.

3. Price optimisation-

Price optimisation is quite helpful for the company to take effective way. Agmet

Company also uses this technique to implement price in the best possible way. Price optimisation

is a mathematical analysis technique which help firm to set price in quite effective manner by

assessing consumer behaviour (Mueller and Trost, 2018). This implies that firm analysis demand

of customers which are ready to pay for the price, firm is willing to sell. If customers do not

prefer to buy commodity, then organisation quote price in accordance to their preferences. This

way company set prices by assessing demand of potential customers and quote similar price so

that they may not be driven away by the rivals.

4. Job costing-

Job costing is the major essence of the manufacturing sector. In relation to this, Agmet

Company also uses job costing so that it may be able to control upon various job expenditures in

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the best possible way. This implies that all manufacturing jobs are controlled in effective way so

that higher production may be achieved with much ease. This is required so that inefficient jobs

may be reduced in the best possible way. Manufacturing jobs are required to be controlled in

effective way so that firm may be able to garner good revenue by initiating higher production

and that too at lower operating costs (Dekker, Kawai and Sakaguchi, 2018).

(P2) Types of management accounting reports

There are various types of management accounting reports help company to prepare and

analyse effectiveness of them and to take enhanced decisions by the management. Various

reports are as follows-

1. Segmental report-

This type of report is prepared by the company which is based on operating segments and

the same information is disclosed in the financial statements. This is done so that investors,

creditors and other stakeholders may take decision on the basis of their interest in the financial

performance of the company. However, this report is not required to be prepared by the private

organisation as it is held for public firms only. The segmental report consists of type of good sold

by the segment, expenses and related to depreciation as well. Moreover, information is also listed

in the segmental reporting such as income tax expenditure and other non-cash items are included

in this report. This helps management and other stakeholders to take enhanced decisions with

much ease.

2. Performance report-

Performance report is another useful management accounting report for Agmet Company

to assess the performance of something related to the business. Generally, this report is prepared

for analysing the effectiveness and efficiency of the employees. In simple words, firm assess

performance of workers in that way which help company to take corrective measures to improve

employees’ productivity in the best possible way (Quinn and et.al, 2018). Thus, performance of

employees is assessed by the management with the help of this report. It is helpful for the

company to measure actual performance with the budgeted one and as a result, steps are taken to

improve performance in the best possible way.

3. Inventory management report-

Goods in the manufacturing industry cannot be produced without having adequate

amount of inventory on the warehouse of the company. This is much related to Agmet Company

5

that higher production may be achieved with much ease. This is required so that inefficient jobs

may be reduced in the best possible way. Manufacturing jobs are required to be controlled in

effective way so that firm may be able to garner good revenue by initiating higher production

and that too at lower operating costs (Dekker, Kawai and Sakaguchi, 2018).

(P2) Types of management accounting reports

There are various types of management accounting reports help company to prepare and

analyse effectiveness of them and to take enhanced decisions by the management. Various

reports are as follows-

1. Segmental report-

This type of report is prepared by the company which is based on operating segments and

the same information is disclosed in the financial statements. This is done so that investors,

creditors and other stakeholders may take decision on the basis of their interest in the financial

performance of the company. However, this report is not required to be prepared by the private

organisation as it is held for public firms only. The segmental report consists of type of good sold

by the segment, expenses and related to depreciation as well. Moreover, information is also listed

in the segmental reporting such as income tax expenditure and other non-cash items are included

in this report. This helps management and other stakeholders to take enhanced decisions with

much ease.

2. Performance report-

Performance report is another useful management accounting report for Agmet Company

to assess the performance of something related to the business. Generally, this report is prepared

for analysing the effectiveness and efficiency of the employees. In simple words, firm assess

performance of workers in that way which help company to take corrective measures to improve

employees’ productivity in the best possible way (Quinn and et.al, 2018). Thus, performance of

employees is assessed by the management with the help of this report. It is helpful for the

company to measure actual performance with the budgeted one and as a result, steps are taken to

improve performance in the best possible way.

3. Inventory management report-

Goods in the manufacturing industry cannot be produced without having adequate

amount of inventory on the warehouse of the company. This is much related to Agmet Company

5

which operates in the chemical manufacturing of various products and as such, it requires

inventory in desired quantity to achieve demand of customers. Numerous orders are laced by the

customers on daily basis and as such, stocks are required. Id inventory is purchased in more

quantity, then it adds to handling costs to the company and as such, expenses increases. Thus, in

order to minimise the wastage pf inventory, management is provided with inventory report in

which desired stock quantity is listed in accordance to the need of production department. Thus,

production is achieved as management scrutinises report and order only required quantity to

meet production (Qian, Hörisch and Schaltegger, 2018).

4. Accounts receivables ageing report-

Sales are made by the company on the basis of cash and credit which is the normal course

of business. When goods are sold on credit, payment is made afterwards and not when customer

purchase goods. Thus in order to assess outstanding credit from customers, accounts receivables

ageing report is prepared. This report lists down all the unpaid credit invoices of customers from

payment is required to be availed by the company. This is required in due time so that firm may

be able to carry out operational tasks in the best possible manner. Thus report highlights names

of customers and money outstanding on the goods purchased by them on credit basis. Thus,

company calls for payment so that it may be achieved in due time. If credit outstanding is more

than Agmet Company should implement strict credit policies so that payment may be recovered

within stipulated time.

5. Job cost report-

Job cost report is another method of management accounting report which outlines each

cost of manufacturing jobs in the best possible way (Giovannoni, 2018). This report deals with

various costs, which are incurred while carrying out production in Agmet Company. This help

firm to have proper analysis of various expenses incurred on jobs so that inefficient jobs can be

reduced up to high extent. This report is prepared and provided to management, which assess the

same and take measures to control costs in the production process so that more production can be

achieved with much ease.

The benefits of management accounting are numerous to the organisation. Among this,

main benefit is that it helps in making better and effective decisions by analysing various reports

and as such, adequate decisions are taken to remove weaknesses. Moreover, stakeholders are

6

inventory in desired quantity to achieve demand of customers. Numerous orders are laced by the

customers on daily basis and as such, stocks are required. Id inventory is purchased in more

quantity, then it adds to handling costs to the company and as such, expenses increases. Thus, in

order to minimise the wastage pf inventory, management is provided with inventory report in

which desired stock quantity is listed in accordance to the need of production department. Thus,

production is achieved as management scrutinises report and order only required quantity to

meet production (Qian, Hörisch and Schaltegger, 2018).

4. Accounts receivables ageing report-

Sales are made by the company on the basis of cash and credit which is the normal course

of business. When goods are sold on credit, payment is made afterwards and not when customer

purchase goods. Thus in order to assess outstanding credit from customers, accounts receivables

ageing report is prepared. This report lists down all the unpaid credit invoices of customers from

payment is required to be availed by the company. This is required in due time so that firm may

be able to carry out operational tasks in the best possible manner. Thus report highlights names

of customers and money outstanding on the goods purchased by them on credit basis. Thus,

company calls for payment so that it may be achieved in due time. If credit outstanding is more

than Agmet Company should implement strict credit policies so that payment may be recovered

within stipulated time.

5. Job cost report-

Job cost report is another method of management accounting report which outlines each

cost of manufacturing jobs in the best possible way (Giovannoni, 2018). This report deals with

various costs, which are incurred while carrying out production in Agmet Company. This help

firm to have proper analysis of various expenses incurred on jobs so that inefficient jobs can be

reduced up to high extent. This report is prepared and provided to management, which assess the

same and take measures to control costs in the production process so that more production can be

achieved with much ease.

The benefits of management accounting are numerous to the organisation. Among this,

main benefit is that it helps in making better and effective decisions by analysing various reports

and as such, adequate decisions are taken to remove weaknesses. Moreover, stakeholders are

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

benefited by enhancement of firm’s earnings as it becomes internal strong and they make

decision to provide funds to the company.

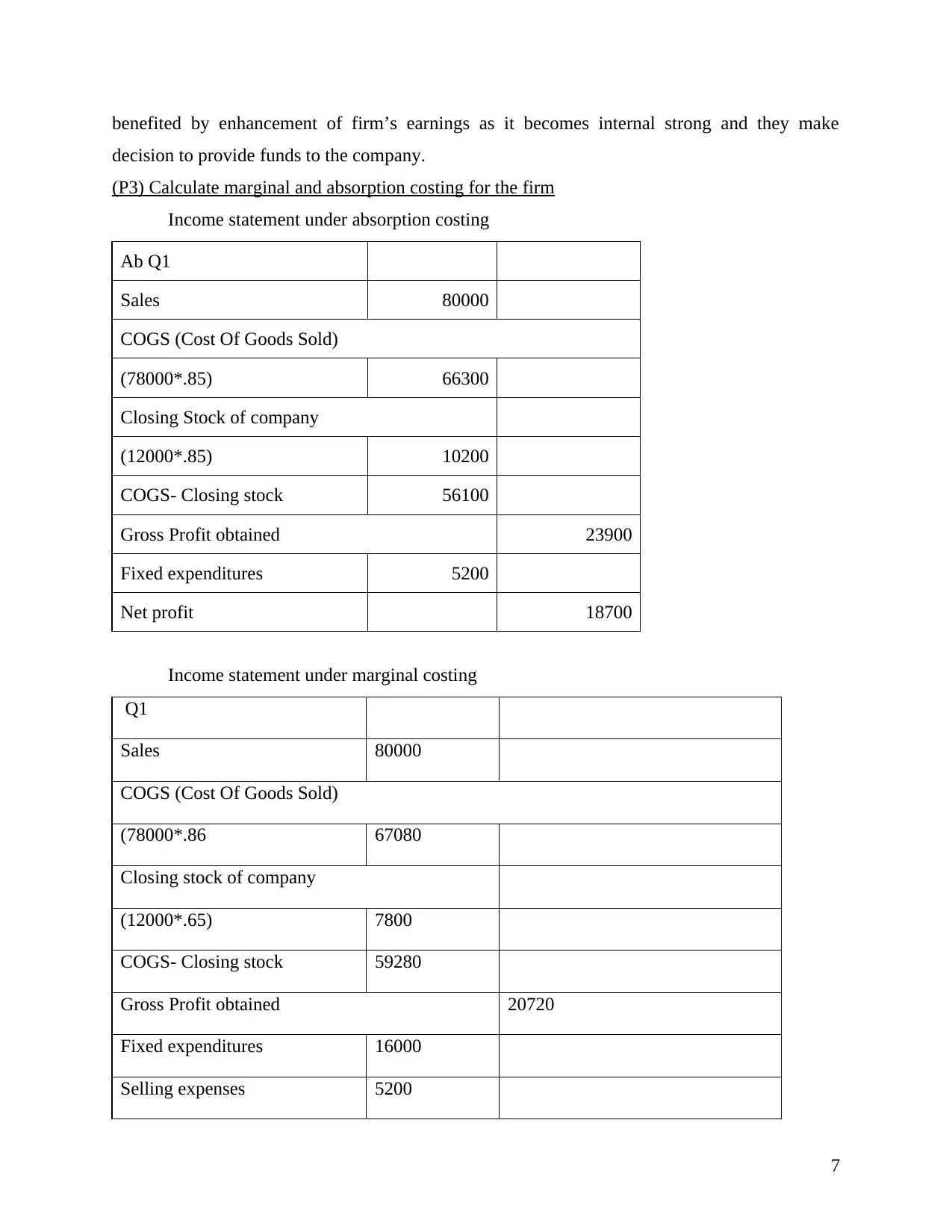

(P3) Calculate marginal and absorption costing for the firm

Income statement under absorption costing

Ab Q1

Sales 80000

COGS (Cost Of Goods Sold)

(78000*.85) 66300

Closing Stock of company

(12000*.85) 10200

COGS- Closing stock 56100

Gross Profit obtained 23900

Fixed expenditures 5200

Net profit 18700

Income statement under marginal costing

Q1

Sales 80000

COGS (Cost Of Goods Sold)

(78000*.86 67080

Closing stock of company

(12000*.65) 7800

COGS- Closing stock 59280

Gross Profit obtained 20720

Fixed expenditures 16000

Selling expenses 5200

7

decision to provide funds to the company.

(P3) Calculate marginal and absorption costing for the firm

Income statement under absorption costing

Ab Q1

Sales 80000

COGS (Cost Of Goods Sold)

(78000*.85) 66300

Closing Stock of company

(12000*.85) 10200

COGS- Closing stock 56100

Gross Profit obtained 23900

Fixed expenditures 5200

Net profit 18700

Income statement under marginal costing

Q1

Sales 80000

COGS (Cost Of Goods Sold)

(78000*.86 67080

Closing stock of company

(12000*.65) 7800

COGS- Closing stock 59280

Gross Profit obtained 20720

Fixed expenditures 16000

Selling expenses 5200

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

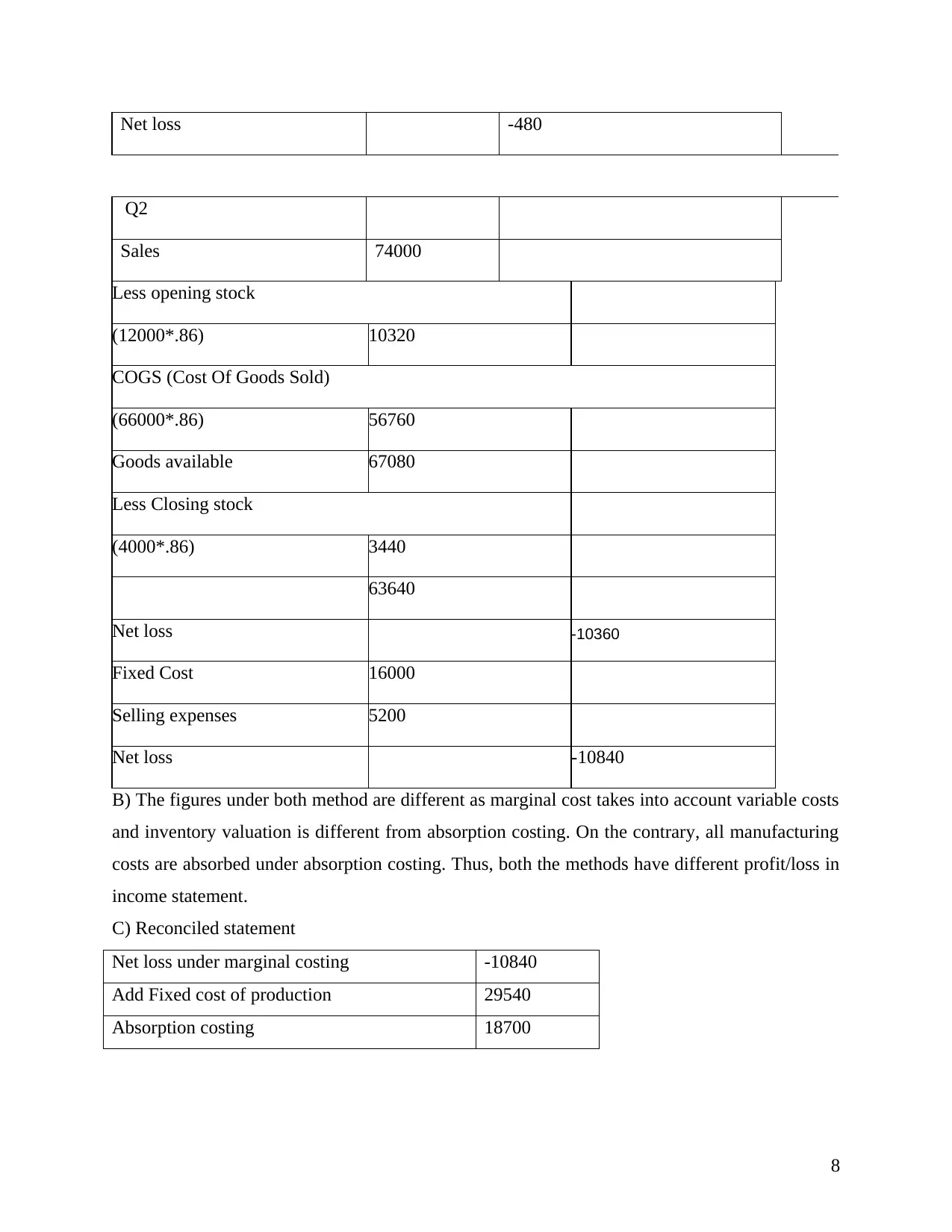

Net loss -480

Q2

Sales 74000

Less opening stock

(12000*.86) 10320

COGS (Cost Of Goods Sold)

(66000*.86) 56760

Goods available 67080

Less Closing stock

(4000*.86) 3440

63640

Net loss -10360

Fixed Cost 16000

Selling expenses 5200

Net loss -10840

B) The figures under both method are different as marginal cost takes into account variable costs

and inventory valuation is different from absorption costing. On the contrary, all manufacturing

costs are absorbed under absorption costing. Thus, both the methods have different profit/loss in

income statement.

C) Reconciled statement

Net loss under marginal costing -10840

Add Fixed cost of production 29540

Absorption costing 18700

8

Q2

Sales 74000

Less opening stock

(12000*.86) 10320

COGS (Cost Of Goods Sold)

(66000*.86) 56760

Goods available 67080

Less Closing stock

(4000*.86) 3440

63640

Net loss -10360

Fixed Cost 16000

Selling expenses 5200

Net loss -10840

B) The figures under both method are different as marginal cost takes into account variable costs

and inventory valuation is different from absorption costing. On the contrary, all manufacturing

costs are absorbed under absorption costing. Thus, both the methods have different profit/loss in

income statement.

C) Reconciled statement

Net loss under marginal costing -10840

Add Fixed cost of production 29540

Absorption costing 18700

8

SECTION 2

(P4) Advantages and disadvantages of planning tools

There are various planning tools which help Agmet Company to evaluate new project in

the best possible way. The planning tools are discussed below along with advantages and

disadvantages-

1. Zero based budgeting-

Zero-based budgeting is prepared without reference to historical or past year figures. It

means that completely new figures are formulated and budget is easily prepared by analysing

requirements of departments (Lee and Herold, 2018).

Advantages

1. It is easiest way of preparing of budget as no historical numbers are indulged and

budget is prepared in accordance to the current requirements

2. It is cost-effective method as forecasting can be done with much ease and

complications are observed.

Disadvantages

1. It is not useful, as it requires lot of time while preparing budget from zero base.

2. It requires lot of manpower as entirely new budget is to be prepared which is the

tedious task for employees and as such, it is time-consuming process.

2. NPV

NPV (Net Present Value) is another useful planning tool as it evaluates new project on

the basis of profitability aspect. It is required in Agmet Company to assess effectiveness of

project.

Advantages

1. It is quite easy to calculate and easier to interpret outcomes as it evaluates project on

profitability.

2. NPV has the main advantage as it utilises concept of time value of money while

assessing attractiveness of project (Advantages and Disadvantages of Net Present Value (NPV)

2018).

Disadvantages

1. It is not useful for the company as it ignores when project will yield returns in terms of

period as it considers only profitability aspect of the project.

9

(P4) Advantages and disadvantages of planning tools

There are various planning tools which help Agmet Company to evaluate new project in

the best possible way. The planning tools are discussed below along with advantages and

disadvantages-

1. Zero based budgeting-

Zero-based budgeting is prepared without reference to historical or past year figures. It

means that completely new figures are formulated and budget is easily prepared by analysing

requirements of departments (Lee and Herold, 2018).

Advantages

1. It is easiest way of preparing of budget as no historical numbers are indulged and

budget is prepared in accordance to the current requirements

2. It is cost-effective method as forecasting can be done with much ease and

complications are observed.

Disadvantages

1. It is not useful, as it requires lot of time while preparing budget from zero base.

2. It requires lot of manpower as entirely new budget is to be prepared which is the

tedious task for employees and as such, it is time-consuming process.

2. NPV

NPV (Net Present Value) is another useful planning tool as it evaluates new project on

the basis of profitability aspect. It is required in Agmet Company to assess effectiveness of

project.

Advantages

1. It is quite easy to calculate and easier to interpret outcomes as it evaluates project on

profitability.

2. NPV has the main advantage as it utilises concept of time value of money while

assessing attractiveness of project (Advantages and Disadvantages of Net Present Value (NPV)

2018).

Disadvantages

1. It is not useful for the company as it ignores when project will yield returns in terms of

period as it considers only profitability aspect of the project.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. It is not suitable when two projects are mutually exclusive in terms of time and size.

3. IRR

IRR (Internal Rate of Return) is another useful technique as it assess effectiveness of new

project by taking into account net present value of cash flows and investment becomes equal to

zero. It is a discount rate, which provides attractiveness of project.

Advantages

1. It is useful technique as it takes into account time value of money and assess

effectiveness of new project in the best possible way.

2. It takes discounting rate while assessing project, which provides correct profitability of

project with much ease (Advantages and Disadvantages of Internal Rate of Return (IRR), 2018).

Disadvantages

1. It is not suitable when two projects are mutually exclusive. It gives inaccurate results

when two projects differ in terms of size and time.

2. It is hard to calculate discounting rate and moreover, results obtained through IRR are

not always accurate to rely on.

P5) How management accounting system help to respond to financial problems

Benchmarking

Benchmarking is quite useful in the company so that it may be able to improve upon its

operational activities in the best possible way. It is simple technique in which one company

compares itself with industry’s best organisation so that it may apply tactics of the same in

achieving goals in effective manner. Agmet Company can easily compares itself from the best

manufacturing firm and can make necessary improvements. This in turn help to respond to

financial problems as improvement is made which affects overall financial health of the

company. Thus, benchmarking is useful management accounting system, which eradicates

financial problems of organisation by implementing well-structured tactics to achieve efficiency

in the best possible manner.

Balanced Scorecard

Balanced scorecard is another technique, which help to respond to financial problems of

Agmet Company quite easily (Salvatore and Gesso, 2018). Balanced scorecard is the

performance measurement technique, which was developed by Kaplan and Norton. The balanced

10

3. IRR

IRR (Internal Rate of Return) is another useful technique as it assess effectiveness of new

project by taking into account net present value of cash flows and investment becomes equal to

zero. It is a discount rate, which provides attractiveness of project.

Advantages

1. It is useful technique as it takes into account time value of money and assess

effectiveness of new project in the best possible way.

2. It takes discounting rate while assessing project, which provides correct profitability of

project with much ease (Advantages and Disadvantages of Internal Rate of Return (IRR), 2018).

Disadvantages

1. It is not suitable when two projects are mutually exclusive. It gives inaccurate results

when two projects differ in terms of size and time.

2. It is hard to calculate discounting rate and moreover, results obtained through IRR are

not always accurate to rely on.

P5) How management accounting system help to respond to financial problems

Benchmarking

Benchmarking is quite useful in the company so that it may be able to improve upon its

operational activities in the best possible way. It is simple technique in which one company

compares itself with industry’s best organisation so that it may apply tactics of the same in

achieving goals in effective manner. Agmet Company can easily compares itself from the best

manufacturing firm and can make necessary improvements. This in turn help to respond to

financial problems as improvement is made which affects overall financial health of the

company. Thus, benchmarking is useful management accounting system, which eradicates

financial problems of organisation by implementing well-structured tactics to achieve efficiency

in the best possible manner.

Balanced Scorecard

Balanced scorecard is another technique, which help to respond to financial problems of

Agmet Company quite easily (Salvatore and Gesso, 2018). Balanced scorecard is the

performance measurement technique, which was developed by Kaplan and Norton. The balanced

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

scorecard technique has four perspectives such as financial, customer, internal process and

learning and growth perspectives, which is used to strengthen internal operations. This help

management to respond to financial problems and as such, performance of employees can be

strengthen in the best possible manner. Financial health can be easily improved and resulting

outcomes can be attained with much ease.

Budgetary Target

Budget is a financial goal which Agmet Company prepares for the coming period in

effective way. Budgetary target is the management accounting system which is used to plan and

make budget for various departments so that these all units may perform well and carry out daily

operational activities in the best possible way. Budgetary target is required so that business may

achieve desired goals in accordance with the stated targets and as such, objectives can be

accomplished in desired way. Moreover, it help to control upon expenses in effectual way and as

a result, budget help to respond to financial problems in effective manner. It help to forecast

activities and as such, if there exists any variances, then corrective action is taken to improve the

situation. Thus, budgeted results can be easily matched with actual outcome to take effective

steps to remove deviations (Ahmetshina, Vagizova and Kaspina, 2018).

KPI (Key Performance Indicators)

KPI is another useful management accounting system used to measure performance of

employees, departments so that improvement can be done in the event of any deviations.

Strategic goals should be achieved and as such, performance of employees is measured with

much ease. KPI’s are useful as it provides clarity to company whether it is performing as per set

standards or not. Thus, it is helpful for evaluating effectiveness of performance and in the event

of any deviations observed; corrective actions are taken so that efficiency can be maintained in

the best possible manner. Thus, KPI is useful performance measurement technique to assess

productivity of various departments in the best possible manner (Hiebl and Richter, 2018).

CONCLUSION

Hereby it can be concluded that management accounting is effective branch of

accounting which help management to take enhanced decisions in the best possible manner.

There are various managerial reports which provides clarity to management to assess financial

health of organisation in effectual way. Moreover, planning tools also help managers to assess

effectiveness of the project whether to invest in the same or not. In addition to this, marginal and

11

learning and growth perspectives, which is used to strengthen internal operations. This help

management to respond to financial problems and as such, performance of employees can be

strengthen in the best possible manner. Financial health can be easily improved and resulting

outcomes can be attained with much ease.

Budgetary Target

Budget is a financial goal which Agmet Company prepares for the coming period in

effective way. Budgetary target is the management accounting system which is used to plan and

make budget for various departments so that these all units may perform well and carry out daily

operational activities in the best possible way. Budgetary target is required so that business may

achieve desired goals in accordance with the stated targets and as such, objectives can be

accomplished in desired way. Moreover, it help to control upon expenses in effectual way and as

a result, budget help to respond to financial problems in effective manner. It help to forecast

activities and as such, if there exists any variances, then corrective action is taken to improve the

situation. Thus, budgeted results can be easily matched with actual outcome to take effective

steps to remove deviations (Ahmetshina, Vagizova and Kaspina, 2018).

KPI (Key Performance Indicators)

KPI is another useful management accounting system used to measure performance of

employees, departments so that improvement can be done in the event of any deviations.

Strategic goals should be achieved and as such, performance of employees is measured with

much ease. KPI’s are useful as it provides clarity to company whether it is performing as per set

standards or not. Thus, it is helpful for evaluating effectiveness of performance and in the event

of any deviations observed; corrective actions are taken so that efficiency can be maintained in

the best possible manner. Thus, KPI is useful performance measurement technique to assess

productivity of various departments in the best possible manner (Hiebl and Richter, 2018).

CONCLUSION

Hereby it can be concluded that management accounting is effective branch of

accounting which help management to take enhanced decisions in the best possible manner.

There are various managerial reports which provides clarity to management to assess financial

health of organisation in effectual way. Moreover, planning tools also help managers to assess

effectiveness of the project whether to invest in the same or not. In addition to this, marginal and

11

absorption costing are useful method of assessing cost and prepare income statements in the best

possible way. Moreover, management accounting system are useful tool in responding to

financial problems.

REFERENCES

Books and Journals

Abernethy, M.A. and Wallis, M.S., 2018. Critique on the'Manager Effects' Research and

Implications for Management Accounting Research. Journal of Management Accounting

Research.

Ahmetshina, A., Vagizova, V. and Kaspina, R., 2018. The Use of Management Accounting

Information in Non-financial Reporting and Interaction with Stakeholders of Public Companies.

In The Impact of Globalization on International Finance and Accounting (pp. 433-439).

Springer, Cham.

Dekker, H. C., Kawai, T. and Sakaguchi, J., 2018. The Interfirm Contracting Value of

Management Accounting Information. Journal of Management Accounting Research.

Englund, H. and Gerdin, J., 2018. Management accounting and the paradox of embedded

agency: A framework for analyzing sources of structural change.

Giovannoni, E., 2018. ENROAC-European Network for Research on Organizational and

Accounting Change (Doctoral dissertation, University of Groningen, The Netherlands).

Hiebl, M. R. and Richter, J. F., 2018. Response Rates in Management Accounting Survey

Research. Journal of Management Accounting Research.

Lee, K.H. and Herold, D.M., 2018. Cultural Relevance in Environmental and Sustainability

Management Accounting (EMA) in the Asia-Pacific Region: A Link Between Cultural Values

and Accounting Values Towards EMA Values. In Accounting for Sustainability: Asia Pacific

Perspectives (pp. 11-37). Springer, Cham.

12

possible way. Moreover, management accounting system are useful tool in responding to

financial problems.

REFERENCES

Books and Journals

Abernethy, M.A. and Wallis, M.S., 2018. Critique on the'Manager Effects' Research and

Implications for Management Accounting Research. Journal of Management Accounting

Research.

Ahmetshina, A., Vagizova, V. and Kaspina, R., 2018. The Use of Management Accounting

Information in Non-financial Reporting and Interaction with Stakeholders of Public Companies.

In The Impact of Globalization on International Finance and Accounting (pp. 433-439).

Springer, Cham.

Dekker, H. C., Kawai, T. and Sakaguchi, J., 2018. The Interfirm Contracting Value of

Management Accounting Information. Journal of Management Accounting Research.

Englund, H. and Gerdin, J., 2018. Management accounting and the paradox of embedded

agency: A framework for analyzing sources of structural change.

Giovannoni, E., 2018. ENROAC-European Network for Research on Organizational and

Accounting Change (Doctoral dissertation, University of Groningen, The Netherlands).

Hiebl, M. R. and Richter, J. F., 2018. Response Rates in Management Accounting Survey

Research. Journal of Management Accounting Research.

Lee, K.H. and Herold, D.M., 2018. Cultural Relevance in Environmental and Sustainability

Management Accounting (EMA) in the Asia-Pacific Region: A Link Between Cultural Values

and Accounting Values Towards EMA Values. In Accounting for Sustainability: Asia Pacific

Perspectives (pp. 11-37). Springer, Cham.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.