Management Accounting Systems & Techniques: A Unit 5 Report

VerifiedAdded on 2023/01/04

|17

|4167

|32

Report

AI Summary

This report provides a comprehensive overview of management accounting systems and techniques. It begins with an explanation of management accounting, its essential requirements, and different types of management accounting systems, including cost accounting, inventory manageme...

UNIT 5

Management Accounting Systems &

Techniques

Management Accounting Systems &

Techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

P1. Explain management accounting and give the essential requirements of different types of

management accounting systems.....................................................................................................4

P2 Explain different methods used for management accounting reporting.....................................8

P3. Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs..............................................................................................10

P4. Explain the advantages and disadvantages of different types of planning tools used for

budgetary control...........................................................................................................................13

P5. Compare how organizations are adapting management accounting systems to respond to

financial problems.........................................................................................................................14

Conclusion.....................................................................................................................................16

References......................................................................................................................................17

Introduction......................................................................................................................................3

P1. Explain management accounting and give the essential requirements of different types of

management accounting systems.....................................................................................................4

P2 Explain different methods used for management accounting reporting.....................................8

P3. Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs..............................................................................................10

P4. Explain the advantages and disadvantages of different types of planning tools used for

budgetary control...........................................................................................................................13

P5. Compare how organizations are adapting management accounting systems to respond to

financial problems.........................................................................................................................14

Conclusion.....................................................................................................................................16

References......................................................................................................................................17

Introduction

This project report consists about management accounting, its essential requirement for

company. It also discusses about management accounting reporting and its types. Difference

between marginal costing and absorption costing also been discussed with numerical examples.

In scenario 1; the role of management accountant has been discussed by considering self

as Trainee management accountant in medium sized financial consultancy organization having

client base of 50 small and medium-sized businesses. In scenario 2; report on behalf of Trainee

management accountant has been prepared by taking scenario 1 as a base.

This project report consists about management accounting, its essential requirement for

company. It also discusses about management accounting reporting and its types. Difference

between marginal costing and absorption costing also been discussed with numerical examples.

In scenario 1; the role of management accountant has been discussed by considering self

as Trainee management accountant in medium sized financial consultancy organization having

client base of 50 small and medium-sized businesses. In scenario 2; report on behalf of Trainee

management accountant has been prepared by taking scenario 1 as a base.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P1. Explain management accounting and give the essential requirements

of different types of management accounting systems.

Management Accounting:

Management accounting is the way to prepare business activity reports that help leaders decide

on usual and long-term options. It allows companies to pursue their goals by identifying,

estimating, analyzing, validating and providing data to management.

Management accounting focuses on all accounting marking clear management of active

asset measurement. Use the data to identify the costs of items or administrations purchased by

your organization. Financial plans are regularly used to measure the choices made in operating

procedures. Act accountants use execution reports to identify variances between actual financial

plan results.

Difference

The main difference between management accounting and financial accounting is the accounting

related to cash, as well as the accounting information to do the function of the books to be

managed within a business exchange.

Principals of management accounting

1. Designing and Compiling

Accounting data, records, reports, explanations and other evidence of past, present or future

results should be designed and organized to address the specific business issues and also obvious

issue.

This means that the administrative accounting framework is designed to include relevant

information. As long as this is true, there is a need to understand a particular problem. In

addition, accounting data can be modified and adopted to meet the needs of executive officers.

2. Management by Exception

The status of dedicated executive officers is followed when data is submitted to the board. This

means that the budgetary control framework and standard costing strategies are maintained

within an administrative accounting framework.

In this sense, the show itself is compared and tested to find trends. The board is given a

of different types of management accounting systems.

Management Accounting:

Management accounting is the way to prepare business activity reports that help leaders decide

on usual and long-term options. It allows companies to pursue their goals by identifying,

estimating, analyzing, validating and providing data to management.

Management accounting focuses on all accounting marking clear management of active

asset measurement. Use the data to identify the costs of items or administrations purchased by

your organization. Financial plans are regularly used to measure the choices made in operating

procedures. Act accountants use execution reports to identify variances between actual financial

plan results.

Difference

The main difference between management accounting and financial accounting is the accounting

related to cash, as well as the accounting information to do the function of the books to be

managed within a business exchange.

Principals of management accounting

1. Designing and Compiling

Accounting data, records, reports, explanations and other evidence of past, present or future

results should be designed and organized to address the specific business issues and also obvious

issue.

This means that the administrative accounting framework is designed to include relevant

information. As long as this is true, there is a need to understand a particular problem. In

addition, accounting data can be modified and adopted to meet the needs of executive officers.

2. Management by Exception

The status of dedicated executive officers is followed when data is submitted to the board. This

means that the budgetary control framework and standard costing strategies are maintained

within an administrative accounting framework.

In this sense, the show itself is compared and tested to find trends. The board is given a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

vague account of what goes wrong. As far as this is concerned, the administration has invested

less energy to analyze and consider the data and more opportunities for migration.

3. Control at Source Accounting

Cost control is better at the focus areas where they are caused: look at source accounting.

Disclosure of individual employees, relevance of matters relating to materials and use and

administration of administrations, eg machinery, strength, repair and maintenance, vehicles and

so on, are established as quantitative and thematic data. Therefore, it is possible to control the

producers, products and tools they bring to the administration.

4. Accounting for Inflation

Benefits can only be purchased if the capital is kept unchanged. It means that financial

compliance is not sustainable. From this point on, it is important to evaluate the capital estimates

that entrepreneurs have worried about in terms of real money estimates by keeping revaluation

records. Therefore, the speed of expansion is believed to judge the real performance of the

sector.

5. Use of Return on Investment

The calculated profit is generally referred to as Return on Capital Employed. Production speed

shows the effectiveness of the industry concern. For this reason, the used capital is proven as far

as real money is concerned.

6. Utility

Accounting frameworks and associated structures should be used especially when filling with

ancillary purposes.

7. Integration

It means that all the essential data of the administration are included so that they can be used

quickly at the highest level and at the same time, the accounting administration is coordinated

minimum cost.

less energy to analyze and consider the data and more opportunities for migration.

3. Control at Source Accounting

Cost control is better at the focus areas where they are caused: look at source accounting.

Disclosure of individual employees, relevance of matters relating to materials and use and

administration of administrations, eg machinery, strength, repair and maintenance, vehicles and

so on, are established as quantitative and thematic data. Therefore, it is possible to control the

producers, products and tools they bring to the administration.

4. Accounting for Inflation

Benefits can only be purchased if the capital is kept unchanged. It means that financial

compliance is not sustainable. From this point on, it is important to evaluate the capital estimates

that entrepreneurs have worried about in terms of real money estimates by keeping revaluation

records. Therefore, the speed of expansion is believed to judge the real performance of the

sector.

5. Use of Return on Investment

The calculated profit is generally referred to as Return on Capital Employed. Production speed

shows the effectiveness of the industry concern. For this reason, the used capital is proven as far

as real money is concerned.

6. Utility

Accounting frameworks and associated structures should be used especially when filling with

ancillary purposes.

7. Integration

It means that all the essential data of the administration are included so that they can be used

quickly at the highest level and at the same time, the accounting administration is coordinated

minimum cost.

Importance and need of Management accounting in Capital Joinery Ltd.

Management accounting is a remarkable type of bookkeeping that emerges from accounting or

accounting. In any case, it is firmly related, yet it is more about furnishing budgetary information

to help with regulatory choices. This implies that authoritative bookkeeping goes past every day

tallying of records and zeros just as long haul business assessment and alternatives. Another

fundamental capacity of board bookkeeping is to help chiefs in choosing the expense of things,

giving all information on costs, market components and advantages. Also, activity bookkeepers

can help decide the existence pattern of existing things just as the discernment of new things.

Essentially, activity bookkeepers give key data that can enable an association's administration to

aggregate settle on a significant number of their decisions. They similarly keep up intra-

association portability by giving an abundance of budgetary and quantifiable information, upheld

by steady bookkeeping accounts.

Essential requirements of Management Accounting Systems in Capital Joinery Ltd.

Management accounting is a technique utilized by the association's top heads to determine

essential business data, for instance, with the goal that everyday working decisions can be made

according to the affiliation's spending setting. Otherwise called managerial bookkeeping, this

cycle consistently requires office supervisors to plan different reports and present that

information to the senior administration gathering. Not at all like other cash related reports, these

data’s will not unveiled to speculators, banks and other external associations.

The fundamental objective of the board bookkeeping data is to attract inward information

the executive’s information from different sources and to assist administrators with making the

information available to them. This information assists overseers with settling on fundamental

decisions about assessment, methodology, association, cost decrease, and so forth Nonetheless,

while executing regulatory bookkeeping procedures; chiefs ought to be aware of these essential

prerequisites.

1) Management style: the manner in which the organization follows the style of the officials

impacts the administration bookkeeping system. It is basic to follow a particular sort of card style

as it determines who and how the information will be dealt with to give a standard outcome.

Management accounting is a remarkable type of bookkeeping that emerges from accounting or

accounting. In any case, it is firmly related, yet it is more about furnishing budgetary information

to help with regulatory choices. This implies that authoritative bookkeeping goes past every day

tallying of records and zeros just as long haul business assessment and alternatives. Another

fundamental capacity of board bookkeeping is to help chiefs in choosing the expense of things,

giving all information on costs, market components and advantages. Also, activity bookkeepers

can help decide the existence pattern of existing things just as the discernment of new things.

Essentially, activity bookkeepers give key data that can enable an association's administration to

aggregate settle on a significant number of their decisions. They similarly keep up intra-

association portability by giving an abundance of budgetary and quantifiable information, upheld

by steady bookkeeping accounts.

Essential requirements of Management Accounting Systems in Capital Joinery Ltd.

Management accounting is a technique utilized by the association's top heads to determine

essential business data, for instance, with the goal that everyday working decisions can be made

according to the affiliation's spending setting. Otherwise called managerial bookkeeping, this

cycle consistently requires office supervisors to plan different reports and present that

information to the senior administration gathering. Not at all like other cash related reports, these

data’s will not unveiled to speculators, banks and other external associations.

The fundamental objective of the board bookkeeping data is to attract inward information

the executive’s information from different sources and to assist administrators with making the

information available to them. This information assists overseers with settling on fundamental

decisions about assessment, methodology, association, cost decrease, and so forth Nonetheless,

while executing regulatory bookkeeping procedures; chiefs ought to be aware of these essential

prerequisites.

1) Management style: the manner in which the organization follows the style of the officials

impacts the administration bookkeeping system. It is basic to follow a particular sort of card style

as it determines who and how the information will be dealt with to give a standard outcome.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2) Organizational structure: the structure of the affiliation demonstrates the extent of the

information mentioned by the head and the degree to which it gives the mentioned information.

3) Information: the main requirement for utilizing on-board bookkeeping is data. Soul is the

quantity of apparently essential decisions. Nonetheless, this information may need to have a few

credits to be substantial for its utilization.

Different Management accounting systems:

1. Cost Accounting Systems

A cost accounting system (also called product costing system or costing system) is a framework

utilized by organizations to gauge the expense of their things for advantage examination, stock

valuation, and cost control. Assessing the genuine expense of an organization is urgent. A

business should know which items are beneficial and which are not, and this must be resolved

subsequent to assessing the right expense of the thing. Likewise, the thing cost system causes

you assess the last gauge of stock of products, work in progress, and completed merchandise

stock with a definitive objective of spending synopsis settlement. A cost bookkeeping system

(otherwise called a thing costing or costing structure) is a system that organizations use to gauge

the expense of their things for efficiency examination, stock valuation, and cost control.

Assessing the genuine expense of a business is fundamental. A business should know which

items are beneficial and which are not, and this must be found in the wake of assessing the right

expense of the thing. Moreover, the cost structure of the things assists with assessing the last

gauge of stock, work in progress and arrangement stock finished with the last objective of the

spending synopsis settlement.

2. Inventory management systems

A Inventory management framework (or stock system) is the cycle through which products are

followed all through the whole adaptable chain, from buy and creation to definite arrangement. A

stock administration structure is a device that permits Capital Joinery Ltd. track results over the

business chain in an adaptable manner. Advance the full reach from mentioning a position with

the gathering purchaser to organizing transportation for your client, arranging a total visit

through something.

information mentioned by the head and the degree to which it gives the mentioned information.

3) Information: the main requirement for utilizing on-board bookkeeping is data. Soul is the

quantity of apparently essential decisions. Nonetheless, this information may need to have a few

credits to be substantial for its utilization.

Different Management accounting systems:

1. Cost Accounting Systems

A cost accounting system (also called product costing system or costing system) is a framework

utilized by organizations to gauge the expense of their things for advantage examination, stock

valuation, and cost control. Assessing the genuine expense of an organization is urgent. A

business should know which items are beneficial and which are not, and this must be resolved

subsequent to assessing the right expense of the thing. Likewise, the thing cost system causes

you assess the last gauge of stock of products, work in progress, and completed merchandise

stock with a definitive objective of spending synopsis settlement. A cost bookkeeping system

(otherwise called a thing costing or costing structure) is a system that organizations use to gauge

the expense of their things for efficiency examination, stock valuation, and cost control.

Assessing the genuine expense of a business is fundamental. A business should know which

items are beneficial and which are not, and this must be found in the wake of assessing the right

expense of the thing. Moreover, the cost structure of the things assists with assessing the last

gauge of stock, work in progress and arrangement stock finished with the last objective of the

spending synopsis settlement.

2. Inventory management systems

A Inventory management framework (or stock system) is the cycle through which products are

followed all through the whole adaptable chain, from buy and creation to definite arrangement. A

stock administration structure is a device that permits Capital Joinery Ltd. track results over the

business chain in an adaptable manner. Advance the full reach from mentioning a position with

the gathering purchaser to organizing transportation for your client, arranging a total visit

through something.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Job Costing Systems

An Job costing framework includes the way toward gathering information on the expenses

related with a specific creation or organization. This information might be needed to introduce

cost information to a client under an understanding where expenses are repaid. The Capital

Joinery Ltd. contrasts the expense of every activity and the pay expected to guarantee the

positions are beneficial. Some of the time the association may secure that a few positions are too

costly considering the costs they can cause.

4. Price Optimizing Systems

Value Optimization Models are mathematical activities that decide how request changes at

various degrees of significant worth, so, all things considered they join cost data and speculation

level information to diminish costs propose which benefits. Worth streamlining models need to

focus on three fundamental assessment segments: the valuation strategy, the thing gauge for both

the purchaser and the merchant, and methodologies that address all the segments that influence

profitability.

P2 Explain different methods used for management accounting

reporting

The following task covers the various methods use for management accounting reporting by

companies to produce accurate analyses of given information.

Management Accounting Reporting:

Accounting reports are a fundamental piece of ensuring you have a total image of how

your business is getting along. A bookkeeping report should be conveyed quarterly to give you a

diagram of your business accounts. This is particularly basic for business visionaries, who get

key experiences from these fundamental reports.

Management accounting reports show the current and current monetary status of an

organization. These reports extricate spending information from bookkeeping books and can

incorporate data, for example, exchange, working costs, thing advantages, and nearby

agreements. These reports are created to empower supervisors to decide business alternatives

learned. When associations are depending on assisting with keeping up the executives books,

they can gather information all the more effectively that will assist pioneers with directing the

An Job costing framework includes the way toward gathering information on the expenses

related with a specific creation or organization. This information might be needed to introduce

cost information to a client under an understanding where expenses are repaid. The Capital

Joinery Ltd. contrasts the expense of every activity and the pay expected to guarantee the

positions are beneficial. Some of the time the association may secure that a few positions are too

costly considering the costs they can cause.

4. Price Optimizing Systems

Value Optimization Models are mathematical activities that decide how request changes at

various degrees of significant worth, so, all things considered they join cost data and speculation

level information to diminish costs propose which benefits. Worth streamlining models need to

focus on three fundamental assessment segments: the valuation strategy, the thing gauge for both

the purchaser and the merchant, and methodologies that address all the segments that influence

profitability.

P2 Explain different methods used for management accounting

reporting

The following task covers the various methods use for management accounting reporting by

companies to produce accurate analyses of given information.

Management Accounting Reporting:

Accounting reports are a fundamental piece of ensuring you have a total image of how

your business is getting along. A bookkeeping report should be conveyed quarterly to give you a

diagram of your business accounts. This is particularly basic for business visionaries, who get

key experiences from these fundamental reports.

Management accounting reports show the current and current monetary status of an

organization. These reports extricate spending information from bookkeeping books and can

incorporate data, for example, exchange, working costs, thing advantages, and nearby

agreements. These reports are created to empower supervisors to decide business alternatives

learned. When associations are depending on assisting with keeping up the executives books,

they can gather information all the more effectively that will assist pioneers with directing the

organization towards accomplishing its objectives.

Types of Management Accounting Reports:

1. Job costing reports

In its most straightforward structure, it is a report that screens the continuous expenses of an

advancement organization. Some JC reports just incorporate finish of-business costs and this can

be useful in separating issues to get around future vocations. Nonetheless, it is unmistakably

better if the report screens work costs in a manner that is reliable with the objective that issues

can be distinguished and settled before they go frantic.

Exact Job Costing can just assist with separating issues during work and after it is done;

issues, for example, a blunder in computing the equipment will be relied upon to finish a specific

tallness or step lost during development.

2. Inventory management reports

An inventory report is a rundown of the measure of stock accessible to an organization at some

random time. The speculation report is a physical or electronic chronicle with numbers

discussing what you are presently prepared to sell, the stock you need, or the stock you

requirement for in-house business use.

Good inventory reports contain exceptional information with a decent arrangement of detail

and use pictures to feature the amount of a specific item you have. Record reports help you to

stop by request or unavailable when clients look for your items on the web.

3. Operating budget reports

An operating budget reflects the expansion in the association’s income and related expenses for a

long time to come, as a rule the next year, and is frequently remembered for the finance

arranging. Much of the time, the load up gets comfortable with the way for gathering the

budgetary arrangement before the beginning of every year, after which an update is made

consistently. A working monetary arrangement can incorporate an upset arrangement, kept in

detail to help everything about the spending plan.

4. Accounts receivable aging reports

Types of Management Accounting Reports:

1. Job costing reports

In its most straightforward structure, it is a report that screens the continuous expenses of an

advancement organization. Some JC reports just incorporate finish of-business costs and this can

be useful in separating issues to get around future vocations. Nonetheless, it is unmistakably

better if the report screens work costs in a manner that is reliable with the objective that issues

can be distinguished and settled before they go frantic.

Exact Job Costing can just assist with separating issues during work and after it is done;

issues, for example, a blunder in computing the equipment will be relied upon to finish a specific

tallness or step lost during development.

2. Inventory management reports

An inventory report is a rundown of the measure of stock accessible to an organization at some

random time. The speculation report is a physical or electronic chronicle with numbers

discussing what you are presently prepared to sell, the stock you need, or the stock you

requirement for in-house business use.

Good inventory reports contain exceptional information with a decent arrangement of detail

and use pictures to feature the amount of a specific item you have. Record reports help you to

stop by request or unavailable when clients look for your items on the web.

3. Operating budget reports

An operating budget reflects the expansion in the association’s income and related expenses for a

long time to come, as a rule the next year, and is frequently remembered for the finance

arranging. Much of the time, the load up gets comfortable with the way for gathering the

budgetary arrangement before the beginning of every year, after which an update is made

consistently. A working monetary arrangement can incorporate an upset arrangement, kept in

detail to help everything about the spending plan.

4. Accounts receivable aging reports

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounts receivable aging (classified by means of an aged receivables report) is a between time

report that requests bunch records to be accessible dependent on the astounding removal time. It

is utilized as a measure to decide the money related prosperity of an association's clients. On the

off chance that the accessible records show that gathering receipts are being gathered much more

slow than expected, this demonstrates that an organization could recuperate or that the

association is in decrease perceives that there is a more explicit proposition danger in their

economic deals.

5. Performance reports

Performance reports are incorporated to confirm the distribution of an association overall

similarly as any agent is close to the furthest limit of a term. Departmental execution reports are

additionally produced in enormous affiliations. Pioneers utilize these introduction reports to

discover key alternatives for the fate of society. Individuals are frequently allocated to their

obligations to the general public and illustrators are terminated or controlled varying. Execution

the board bookkeeping reports additionally give a point by point comprehension of how an

association works. In case you don't think you need to work inside a specific cutoff yet somehow

that won't occur, these connections can lead you to defects in the setup. The portion of the

execution report is essential for any association to keep up an immediate extent of their way to

deal with the primary objective.

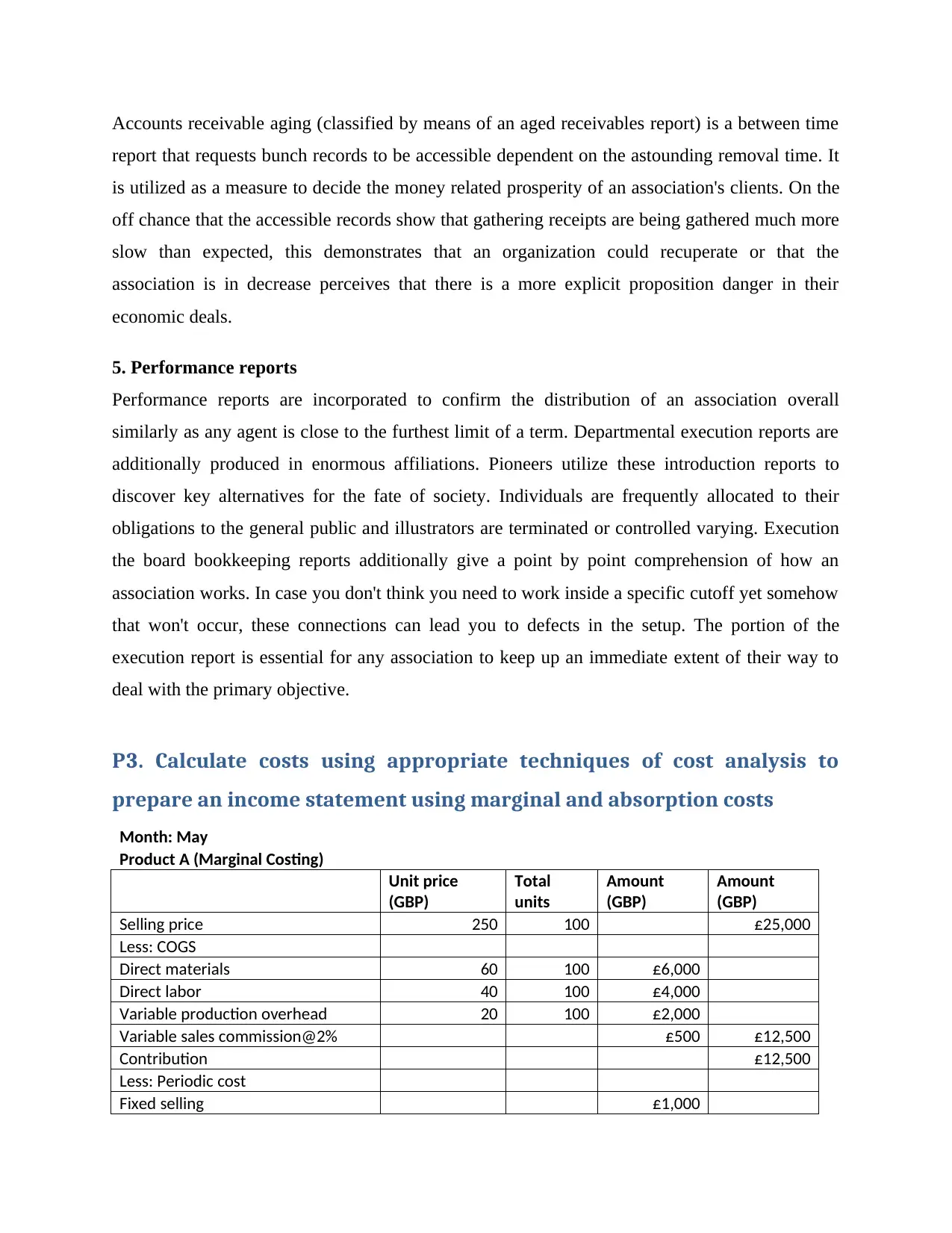

P3. Calculate costs using appropriate techniques of cost analysis to

prepare an income statement using marginal and absorption costs

Month: May

Product A (Marginal Costing)

Unit price

(GBP)

Total

units

Amount

(GBP)

Amount

(GBP)

Selling price 250 100 £25,000

Less: COGS

Direct materials 60 100 £6,000

Direct labor 40 100 £4,000

Variable production overhead 20 100 £2,000

Variable sales commission@2% £500 £12,500

Contribution £12,500

Less: Periodic cost

Fixed selling £1,000

report that requests bunch records to be accessible dependent on the astounding removal time. It

is utilized as a measure to decide the money related prosperity of an association's clients. On the

off chance that the accessible records show that gathering receipts are being gathered much more

slow than expected, this demonstrates that an organization could recuperate or that the

association is in decrease perceives that there is a more explicit proposition danger in their

economic deals.

5. Performance reports

Performance reports are incorporated to confirm the distribution of an association overall

similarly as any agent is close to the furthest limit of a term. Departmental execution reports are

additionally produced in enormous affiliations. Pioneers utilize these introduction reports to

discover key alternatives for the fate of society. Individuals are frequently allocated to their

obligations to the general public and illustrators are terminated or controlled varying. Execution

the board bookkeeping reports additionally give a point by point comprehension of how an

association works. In case you don't think you need to work inside a specific cutoff yet somehow

that won't occur, these connections can lead you to defects in the setup. The portion of the

execution report is essential for any association to keep up an immediate extent of their way to

deal with the primary objective.

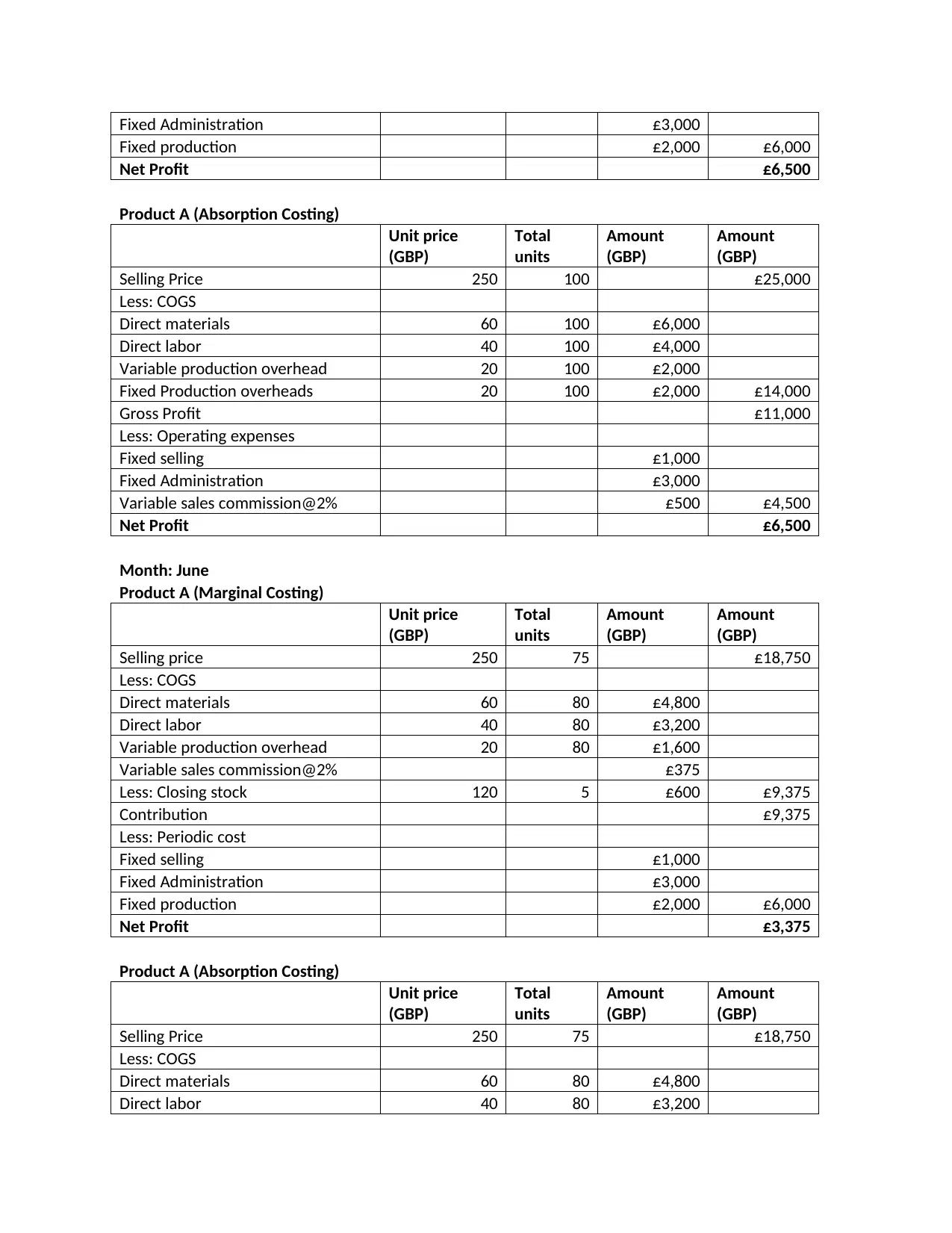

P3. Calculate costs using appropriate techniques of cost analysis to

prepare an income statement using marginal and absorption costs

Month: May

Product A (Marginal Costing)

Unit price

(GBP)

Total

units

Amount

(GBP)

Amount

(GBP)

Selling price 250 100 £25,000

Less: COGS

Direct materials 60 100 £6,000

Direct labor 40 100 £4,000

Variable production overhead 20 100 £2,000

Variable sales commission@2% £500 £12,500

Contribution £12,500

Less: Periodic cost

Fixed selling £1,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed Administration £3,000

Fixed production £2,000 £6,000

Net Profit £6,500

Product A (Absorption Costing)

Unit price

(GBP)

Total

units

Amount

(GBP)

Amount

(GBP)

Selling Price 250 100 £25,000

Less: COGS

Direct materials 60 100 £6,000

Direct labor 40 100 £4,000

Variable production overhead 20 100 £2,000

Fixed Production overheads 20 100 £2,000 £14,000

Gross Profit £11,000

Less: Operating expenses

Fixed selling £1,000

Fixed Administration £3,000

Variable sales commission@2% £500 £4,500

Net Profit £6,500

Month: June

Product A (Marginal Costing)

Unit price

(GBP)

Total

units

Amount

(GBP)

Amount

(GBP)

Selling price 250 75 £18,750

Less: COGS

Direct materials 60 80 £4,800

Direct labor 40 80 £3,200

Variable production overhead 20 80 £1,600

Variable sales commission@2% £375

Less: Closing stock 120 5 £600 £9,375

Contribution £9,375

Less: Periodic cost

Fixed selling £1,000

Fixed Administration £3,000

Fixed production £2,000 £6,000

Net Profit £3,375

Product A (Absorption Costing)

Unit price

(GBP)

Total

units

Amount

(GBP)

Amount

(GBP)

Selling Price 250 75 £18,750

Less: COGS

Direct materials 60 80 £4,800

Direct labor 40 80 £3,200

Fixed production £2,000 £6,000

Net Profit £6,500

Product A (Absorption Costing)

Unit price

(GBP)

Total

units

Amount

(GBP)

Amount

(GBP)

Selling Price 250 100 £25,000

Less: COGS

Direct materials 60 100 £6,000

Direct labor 40 100 £4,000

Variable production overhead 20 100 £2,000

Fixed Production overheads 20 100 £2,000 £14,000

Gross Profit £11,000

Less: Operating expenses

Fixed selling £1,000

Fixed Administration £3,000

Variable sales commission@2% £500 £4,500

Net Profit £6,500

Month: June

Product A (Marginal Costing)

Unit price

(GBP)

Total

units

Amount

(GBP)

Amount

(GBP)

Selling price 250 75 £18,750

Less: COGS

Direct materials 60 80 £4,800

Direct labor 40 80 £3,200

Variable production overhead 20 80 £1,600

Variable sales commission@2% £375

Less: Closing stock 120 5 £600 £9,375

Contribution £9,375

Less: Periodic cost

Fixed selling £1,000

Fixed Administration £3,000

Fixed production £2,000 £6,000

Net Profit £3,375

Product A (Absorption Costing)

Unit price

(GBP)

Total

units

Amount

(GBP)

Amount

(GBP)

Selling Price 250 75 £18,750

Less: COGS

Direct materials 60 80 £4,800

Direct labor 40 80 £3,200

Variable production overhead 20 80 £1,600

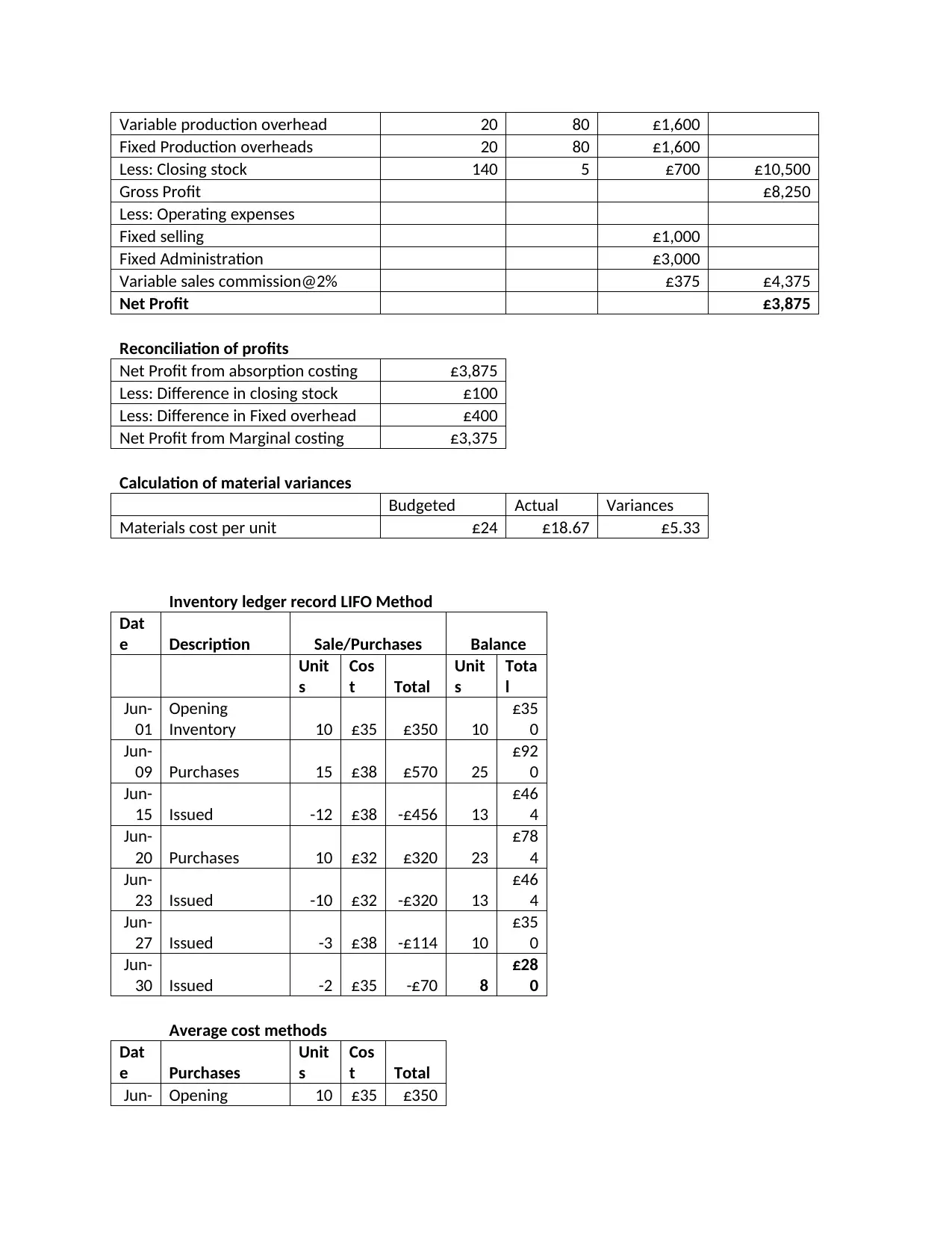

Fixed Production overheads 20 80 £1,600

Less: Closing stock 140 5 £700 £10,500

Gross Profit £8,250

Less: Operating expenses

Fixed selling £1,000

Fixed Administration £3,000

Variable sales commission@2% £375 £4,375

Net Profit £3,875

Reconciliation of profits

Net Profit from absorption costing £3,875

Less: Difference in closing stock £100

Less: Difference in Fixed overhead £400

Net Profit from Marginal costing £3,375

Calculation of material variances

Budgeted Actual Variances

Materials cost per unit £24 £18.67 £5.33

Inventory ledger record LIFO Method

Dat

e Description Sale/Purchases Balance

Unit

s

Cos

t Total

Unit

s

Tota

l

Jun-

01

Opening

Inventory 10 £35 £350 10

£35

0

Jun-

09 Purchases 15 £38 £570 25

£92

0

Jun-

15 Issued -12 £38 -£456 13

£46

4

Jun-

20 Purchases 10 £32 £320 23

£78

4

Jun-

23 Issued -10 £32 -£320 13

£46

4

Jun-

27 Issued -3 £38 -£114 10

£35

0

Jun-

30 Issued -2 £35 -£70 8

£28

0

Average cost methods

Dat

e Purchases

Unit

s

Cos

t Total

Jun- Opening 10 £35 £350

Fixed Production overheads 20 80 £1,600

Less: Closing stock 140 5 £700 £10,500

Gross Profit £8,250

Less: Operating expenses

Fixed selling £1,000

Fixed Administration £3,000

Variable sales commission@2% £375 £4,375

Net Profit £3,875

Reconciliation of profits

Net Profit from absorption costing £3,875

Less: Difference in closing stock £100

Less: Difference in Fixed overhead £400

Net Profit from Marginal costing £3,375

Calculation of material variances

Budgeted Actual Variances

Materials cost per unit £24 £18.67 £5.33

Inventory ledger record LIFO Method

Dat

e Description Sale/Purchases Balance

Unit

s

Cos

t Total

Unit

s

Tota

l

Jun-

01

Opening

Inventory 10 £35 £350 10

£35

0

Jun-

09 Purchases 15 £38 £570 25

£92

0

Jun-

15 Issued -12 £38 -£456 13

£46

4

Jun-

20 Purchases 10 £32 £320 23

£78

4

Jun-

23 Issued -10 £32 -£320 13

£46

4

Jun-

27 Issued -3 £38 -£114 10

£35

0

Jun-

30 Issued -2 £35 -£70 8

£28

0

Average cost methods

Dat

e Purchases

Unit

s

Cos

t Total

Jun- Opening 10 £35 £350

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

01 Inventory

Jun-

09 Purchases 15 £38 £570

Jun-

20 Purchases 10 £32 £320

Total 35

£1,24

0

Average cost of Inventory =

Total/Units

= 1240/35

= 35.42857143

P4. Explain the advantages and disadvantages of different types of

planning tools used for budgetary control

Budgets

Budget is a plan to show how much money an individual or society makes and how much they

ask for or can afford to spend. A spending plan is a cash agreement for a fixed period, often a

year. In the same way, it could include the size and income of agreed agreements, the amounts of

funds, the amount of expenses, resources, liabilities and income. It is used by organizations,

governments, families and various associations to communicate master plans or times of exercise

in measurable quantities.

A budget is the amount of money set aside for a specific purpose and the expected

spending pattern along with suggestions on how to meet them. It could involve overcharging,

providing money for future use, or a shortage where costs exceed pay.

Budgetary Control

Advantages Disadvantages

Interdepartmental initiative activities. A genuine issue will emerge when budgetary

plans are executed with exactness and

consistency.

Clarify the ground breaking strategies. They

decide the assets, pay and budgetary years

expected to make the vital game plans.

It can propel makers for absence of interest.

With the likelihood that top-down spending

plans won't be forced, agents won't

comprehend or zero in on the reasoning behind

arranged spending.

Jun-

09 Purchases 15 £38 £570

Jun-

20 Purchases 10 £32 £320

Total 35

£1,24

0

Average cost of Inventory =

Total/Units

= 1240/35

= 35.42857143

P4. Explain the advantages and disadvantages of different types of

planning tools used for budgetary control

Budgets

Budget is a plan to show how much money an individual or society makes and how much they

ask for or can afford to spend. A spending plan is a cash agreement for a fixed period, often a

year. In the same way, it could include the size and income of agreed agreements, the amounts of

funds, the amount of expenses, resources, liabilities and income. It is used by organizations,

governments, families and various associations to communicate master plans or times of exercise

in measurable quantities.

A budget is the amount of money set aside for a specific purpose and the expected

spending pattern along with suggestions on how to meet them. It could involve overcharging,

providing money for future use, or a shortage where costs exceed pay.

Budgetary Control

Advantages Disadvantages

Interdepartmental initiative activities. A genuine issue will emerge when budgetary

plans are executed with exactness and

consistency.

Clarify the ground breaking strategies. They

decide the assets, pay and budgetary years

expected to make the vital game plans.

It can propel makers for absence of interest.

With the likelihood that top-down spending

plans won't be forced, agents won't

comprehend or zero in on the reasoning behind

arranged spending.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Give an exquisite rundown of progressive

activities.

It can de motivate employees.

Cost volume profit analysis

Cost volume profit analysis is a strategy for authoritative bookkeeping that quantifies the impact

of the size of an agreement and the expense of a thing on the business advantage of an

organization. Consider how changes in fixed costs, variable costs, cost of deals per unit, and a

business blend of at any rate two explicit components influence business productivity. The

investigation of most books accepts all costs that might be fixed or variable, the expense of uses

per unit and the expense per unit are both variable and fixed and all offer of all units made.

Cost volume profit analysis

Advantages Disadvantages

Simplicity is approximate, using a handful of

standard recipes; the numbers can be adjusted

to quickly determine changes in factors.

Accuracy - assume all costs are fixed but costs

are subject to change with creation.

Adjusting the break-even helps leaders assess

future spending and how creation affects

industry goals.

Accept offers that are durable, but interest in

an item may change over time.

Evaluation: Assist clan leaders by deciding the

cost of what they can and will offer more.

Consider just the set time after this period the

results can be unreliable.

P5. Compare how organizations are adapting management accounting

systems to respond to financial problems

Today affiliations are confronting numerous issues identified with cash, which can be recognized

in various ways, which are examined beneath:

Benchmarking: Benchmarking is a cycle of estimating the exhibition of an organization's items,

administrations, or cycles contrasted with those of another industry thought about the best in the

business, otherwise called high positioning. The motivation behind a model is to separate inside

open entryways for improvement. By thinking about high-performing associations, isolating

activities.

It can de motivate employees.

Cost volume profit analysis

Cost volume profit analysis is a strategy for authoritative bookkeeping that quantifies the impact

of the size of an agreement and the expense of a thing on the business advantage of an

organization. Consider how changes in fixed costs, variable costs, cost of deals per unit, and a

business blend of at any rate two explicit components influence business productivity. The

investigation of most books accepts all costs that might be fixed or variable, the expense of uses

per unit and the expense per unit are both variable and fixed and all offer of all units made.

Cost volume profit analysis

Advantages Disadvantages

Simplicity is approximate, using a handful of

standard recipes; the numbers can be adjusted

to quickly determine changes in factors.

Accuracy - assume all costs are fixed but costs

are subject to change with creation.

Adjusting the break-even helps leaders assess

future spending and how creation affects

industry goals.

Accept offers that are durable, but interest in

an item may change over time.

Evaluation: Assist clan leaders by deciding the

cost of what they can and will offer more.

Consider just the set time after this period the

results can be unreliable.

P5. Compare how organizations are adapting management accounting

systems to respond to financial problems

Today affiliations are confronting numerous issues identified with cash, which can be recognized

in various ways, which are examined beneath:

Benchmarking: Benchmarking is a cycle of estimating the exhibition of an organization's items,

administrations, or cycles contrasted with those of another industry thought about the best in the

business, otherwise called high positioning. The motivation behind a model is to separate inside

open entryways for improvement. By thinking about high-performing associations, isolating

what makes such execution conceivable, and afterward contrasting these circles and how your

business functions, you can actualize changes that will achieve the essential updates; like for

example Creams ltd. has set benchmarking of achieving 25% of past arrangements pay. On the

other hand, Starbucks has set benchmark on the base of cost and variable expenses. It centers to

reduce wastage and lessening variable cost by 10% consistently.

KPI: Also known as key execution marker; Ratio checks are huge KPIs of any connection. It

logically ponders the adjudicator reliant on in any occasion two years of budgetary reports and

the market's standard extents and passes an explanation with respect to whether the affiliation

performs well. For example; Creams ltd. keeps up current extent of 2:1 as an ideal extent;

underneath this shows budgetary issue inside association. Moreover association has set worth

25% income driven edge. Underneath this standard exhibits budgetary issue. Of course;

Starbucks follows return on esteem, which is 9% picked by association; underneath this value

exhibits cash related issue.

Money Administration: This is the affiliation's fundamental structure to assess how a thing

chooses to amass maintain for the business. There are two exceptional ways to deal with fund-

raise; Liability and Value. Both require some cost to be paid by the business; A blend of two

costs known as the weighted conventional utilization of capital.

business functions, you can actualize changes that will achieve the essential updates; like for

example Creams ltd. has set benchmarking of achieving 25% of past arrangements pay. On the

other hand, Starbucks has set benchmark on the base of cost and variable expenses. It centers to

reduce wastage and lessening variable cost by 10% consistently.

KPI: Also known as key execution marker; Ratio checks are huge KPIs of any connection. It

logically ponders the adjudicator reliant on in any occasion two years of budgetary reports and

the market's standard extents and passes an explanation with respect to whether the affiliation

performs well. For example; Creams ltd. keeps up current extent of 2:1 as an ideal extent;

underneath this shows budgetary issue inside association. Moreover association has set worth

25% income driven edge. Underneath this standard exhibits budgetary issue. Of course;

Starbucks follows return on esteem, which is 9% picked by association; underneath this value

exhibits cash related issue.

Money Administration: This is the affiliation's fundamental structure to assess how a thing

chooses to amass maintain for the business. There are two exceptional ways to deal with fund-

raise; Liability and Value. Both require some cost to be paid by the business; A blend of two

costs known as the weighted conventional utilization of capital.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conclusion

After analyzing whole report, it very well may be reasoned that; the norm of the

executives accounts are not made and never were. Most associations have defective structures to

encounter the genuine presentation of cash - in case they didn't, so, all in all they would have a

beginning stage, as opposed to simply dubious it is frequently disconnected. For instance, a

realtor with occupations in three urban areas - when asked what the profitable position was

among the work environments, the two proprietors had no information. They meant to zero in on

the circumstance. At the perfect time real authoritative records were totally dismissed, however

were viewed as severe heads.

Budgeting control is utilized as a change device to design and deal with the relationship

of assortment or offer of items or organizations, to advance coordination and correspondence

between offices, to propel pioneers and to accomplish assess. The Budget control is a sheltered

game plan of all parts of the affiliation's business to guarantee that the affiliation accomplishes

its objectives at a particular time later on; the different divisions must give an association and

pioneers on the objectives gave.

After analyzing whole report, it very well may be reasoned that; the norm of the

executives accounts are not made and never were. Most associations have defective structures to

encounter the genuine presentation of cash - in case they didn't, so, all in all they would have a

beginning stage, as opposed to simply dubious it is frequently disconnected. For instance, a

realtor with occupations in three urban areas - when asked what the profitable position was

among the work environments, the two proprietors had no information. They meant to zero in on

the circumstance. At the perfect time real authoritative records were totally dismissed, however

were viewed as severe heads.

Budgeting control is utilized as a change device to design and deal with the relationship

of assortment or offer of items or organizations, to advance coordination and correspondence

between offices, to propel pioneers and to accomplish assess. The Budget control is a sheltered

game plan of all parts of the affiliation's business to guarantee that the affiliation accomplishes

its objectives at a particular time later on; the different divisions must give an association and

pioneers on the objectives gave.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

DRURY, C. (2015) Management and Cost Accounting. 9th Ed. Cengage Learning.

EDMONDS, T. and OLDS, P. (2013) Fundamental Managerial Accounting Concepts. 7th

Ed. Maidenhead: McGraw-Hill. HORNGREN, C., SUNDEN, G., STRATTON, W.,

BURGSTALHER, D. and SCHATZBERG, J. (2013) Introduction to Management

Accounting. Global Ed. Harlow: Pearson. (This text is available electronically and is

supported by access to an online course)

SEAL, W. et al (2014) Management Accounting. 5th Ed. Maidenhead: McGraw-Hill

DRURY, C. (2015) Management and Cost Accounting. 9th Ed. Cengage Learning.

EDMONDS, T. and OLDS, P. (2013) Fundamental Managerial Accounting Concepts. 7th

Ed. Maidenhead: McGraw-Hill. HORNGREN, C., SUNDEN, G., STRATTON, W.,

BURGSTALHER, D. and SCHATZBERG, J. (2013) Introduction to Management

Accounting. Global Ed. Harlow: Pearson. (This text is available electronically and is

supported by access to an online course)

SEAL, W. et al (2014) Management Accounting. 5th Ed. Maidenhead: McGraw-Hill

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.