Comprehensive Report on Management Accounting Systems and Methods

VerifiedAdded on 2022/12/27

|11

|2592

|90

Report

AI Summary

This report delves into the realm of management accounting, offering a comprehensive overview of its systems, reporting methods, and cost accounting techniques. It begins with an introduction to management accounting, emphasizing its role in evaluating financial data for decision-making. The report then explores various management accounting systems, including Inventory Management Systems (IMS), Cost Accounting Systems (CAS), Job Costing Systems (JCS), and Price Optimization Systems. It also examines different management accounting reporting techniques, such as Cost Accounting Reports, Inventory Reports, Debtors Ageing Reports, Performance Reports, and Budgeting Reports. Furthermore, the report discusses cost accounting techniques like marginal costing and absorption costing, providing income statements for both. The integration of management accounting within an organization and the benefits of its functions are also highlighted. This report serves as a valuable resource for understanding the principles and applications of management accounting, providing insights into financial analysis and decision-making processes.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

CONCLUSION................................................................................................................................1

REFERENCES................................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

CONCLUSION................................................................................................................................1

REFERENCES................................................................................................................................2

INTRODUCTION

Management accounting is the process that evaluates financial data to get information

that will help the top management to take short term as well as long term decision-making and

goal setting of organization. The MA systems allows to monitor and control the different

business processes. Present report will provide about different systems of management

accounting, reporting methods and cost accounting techniques used for computing cost.

REPORT

Management Accounting

Management accounting provides useful and only relevant information to the

management, so they can make fast and more efficient decision. It also considers the time value

of money so the future of any project can be estimated. It will help to make optimum utilization

of resources analysing cost per unit and reducing the wastage by proper forecasting.

Management can make better control in the organization because all the activities are pre

defined.

Management Accounting Principles

Accounting for inflation and forward-looking approach - In management accounting, when a

new project is prepared it always considers time value of money with inflation rate. It means the

projects are made with due consideration to inflation rate so chance for failure became less.

Management accounting uses the financial to find out information that helps the future goals and

preparation.

Absorption overhead cost- Overhead cost are absorbed on any predetermined basis. So the rate

for the absorption is fixed and the overhead cost can be allocated accordingly. Overhead cost are

indirect raw material, indirect labour, indirect expenses (Kudryashova and et.al., 2020). This rate

is calculated to find out the over and under absorbed condition of the production.

Utilization of resources- Some resources are limited and some are expensive in nature,

management accounting helps in the better allocation of resources with the help of cost

accounting techniques so the better use can be assured.

Controllable and uncontrollable cost- There are two types of cost one is controllable and

uncontrollable, the classification are to be made by this the controllable cost can be find out and

reduce them because these are the controllable cost that should be controlled.

1

Management accounting is the process that evaluates financial data to get information

that will help the top management to take short term as well as long term decision-making and

goal setting of organization. The MA systems allows to monitor and control the different

business processes. Present report will provide about different systems of management

accounting, reporting methods and cost accounting techniques used for computing cost.

REPORT

Management Accounting

Management accounting provides useful and only relevant information to the

management, so they can make fast and more efficient decision. It also considers the time value

of money so the future of any project can be estimated. It will help to make optimum utilization

of resources analysing cost per unit and reducing the wastage by proper forecasting.

Management can make better control in the organization because all the activities are pre

defined.

Management Accounting Principles

Accounting for inflation and forward-looking approach - In management accounting, when a

new project is prepared it always considers time value of money with inflation rate. It means the

projects are made with due consideration to inflation rate so chance for failure became less.

Management accounting uses the financial to find out information that helps the future goals and

preparation.

Absorption overhead cost- Overhead cost are absorbed on any predetermined basis. So the rate

for the absorption is fixed and the overhead cost can be allocated accordingly. Overhead cost are

indirect raw material, indirect labour, indirect expenses (Kudryashova and et.al., 2020). This rate

is calculated to find out the over and under absorbed condition of the production.

Utilization of resources- Some resources are limited and some are expensive in nature,

management accounting helps in the better allocation of resources with the help of cost

accounting techniques so the better use can be assured.

Controllable and uncontrollable cost- There are two types of cost one is controllable and

uncontrollable, the classification are to be made by this the controllable cost can be find out and

reduce them because these are the controllable cost that should be controlled.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Role of management accounting and management accounting systems

Inventory Management System

IMS is important MA system that enables the company to keep record for every

movement of inventory within and outside the organisation that has not been sold. It allows the

management to keep complete control over stocks from raw material, company assets and

finished products. IMS stores information for future period to make forecasts for the production

activities to place the purchase order.

Requirements

IMS is required for tracking all the stock movement to and from production house to

warehouse and sales.

The reports generated by IMS allows management to make budgets for stock purchase

orders.

It reduces the excessive storage costs for inventory and also keeps safety stock.

Cost Accounting System

It refers to the tool that helps to determine actual cost associated with manufacturing of

products or providing services. The actual costs are computed after covering all the variable and

fixed expenses within supply chain (Abdusalomova, 2020). The CAS is used for internal

management of the company to calculate the prices of products or services. It enables the

company to measure the profit margins that company will enable the company to grow.

Requirements

It is required by the company to calculate actual cost of the products and services.

It enables the company to compute both variable and fixed expenses for allocation of

resources.

Cost accounting helps the company to determine adequate profit margin on products.

Job Costing System

JCS is referred as process that accumulates information about costs and expenses that are

associated wit particular products or services. The information is required by company to derive

information of all costs involved in producing a particular job under contracts in which costs or

products are reimbursed back. JCS has been used by organisation where production of a item

involves more than one step.

Required

2

Inventory Management System

IMS is important MA system that enables the company to keep record for every

movement of inventory within and outside the organisation that has not been sold. It allows the

management to keep complete control over stocks from raw material, company assets and

finished products. IMS stores information for future period to make forecasts for the production

activities to place the purchase order.

Requirements

IMS is required for tracking all the stock movement to and from production house to

warehouse and sales.

The reports generated by IMS allows management to make budgets for stock purchase

orders.

It reduces the excessive storage costs for inventory and also keeps safety stock.

Cost Accounting System

It refers to the tool that helps to determine actual cost associated with manufacturing of

products or providing services. The actual costs are computed after covering all the variable and

fixed expenses within supply chain (Abdusalomova, 2020). The CAS is used for internal

management of the company to calculate the prices of products or services. It enables the

company to measure the profit margins that company will enable the company to grow.

Requirements

It is required by the company to calculate actual cost of the products and services.

It enables the company to compute both variable and fixed expenses for allocation of

resources.

Cost accounting helps the company to determine adequate profit margin on products.

Job Costing System

JCS is referred as process that accumulates information about costs and expenses that are

associated wit particular products or services. The information is required by company to derive

information of all costs involved in producing a particular job under contracts in which costs or

products are reimbursed back. JCS has been used by organisation where production of a item

involves more than one step.

Required

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is required to compute all the costs such as raw materials, labour and production related

with particular job.

It is used when company has to make products under special order or contract.

The company calculates the profit margin to be kept after analysing the cost.

Price Optimisation System

The process is used to find sweet spot pricing or the maximum prices against customers

that they are willing to pay. The companies up & down, supply chain, B2C and B2B rightly

dedicate massive time towards the price optimisation for ensuring that products would be sold

quickly at right (Price Optimisation System, 2020). If items are priced high it may difficult for

the company to clear the stocks and it may not make decent profit.

Requirement

It is required by company to determine demand of products at different level of prices.

It enables to identify the optimum prices of the product at which they will generate

desired sales.

It allows company to make proper balance between the profit and value of product.

Management accounting reporting techniques

Company generates different management accounting reports to make important

decisions for the business. These reports contain the information regarding previous and current

figures to identify whether they are moving over right direction or not. It is essential for the firm

to earn adequate profits over all the products and services. The different types of reports that are

used by the management are

Cost Accounting Reports

It contains the information related to all the costs incurred by firm over the period. Report

provides detailed lists of variable and fixed expenses that are incurred related to products. The

report contains both estimated figures and actual figures to identify the variances between them.

The variances are calculated to identify reason behind them and root cause (Novas, Alves and

Sousa, 2017). It allows company to take actions to reduce the variances and to control costs.

Inventory Report

Report comprises of all the details and information regarding the stock. It helps the

management to identify the purchases, consumption and the closing stock. On the basis of this

report management identifies whether company is generating required output or not. Report

3

with particular job.

It is used when company has to make products under special order or contract.

The company calculates the profit margin to be kept after analysing the cost.

Price Optimisation System

The process is used to find sweet spot pricing or the maximum prices against customers

that they are willing to pay. The companies up & down, supply chain, B2C and B2B rightly

dedicate massive time towards the price optimisation for ensuring that products would be sold

quickly at right (Price Optimisation System, 2020). If items are priced high it may difficult for

the company to clear the stocks and it may not make decent profit.

Requirement

It is required by company to determine demand of products at different level of prices.

It enables to identify the optimum prices of the product at which they will generate

desired sales.

It allows company to make proper balance between the profit and value of product.

Management accounting reporting techniques

Company generates different management accounting reports to make important

decisions for the business. These reports contain the information regarding previous and current

figures to identify whether they are moving over right direction or not. It is essential for the firm

to earn adequate profits over all the products and services. The different types of reports that are

used by the management are

Cost Accounting Reports

It contains the information related to all the costs incurred by firm over the period. Report

provides detailed lists of variable and fixed expenses that are incurred related to products. The

report contains both estimated figures and actual figures to identify the variances between them.

The variances are calculated to identify reason behind them and root cause (Novas, Alves and

Sousa, 2017). It allows company to take actions to reduce the variances and to control costs.

Inventory Report

Report comprises of all the details and information regarding the stock. It helps the

management to identify the purchases, consumption and the closing stock. On the basis of this

report management identifies whether company is generating required output or not. Report

3

enable the company to make forecasts for future requirement of inventory to carry out the

operation.

Debtors Ageing Report

The report states about the debtors of company over the period. The report states the

debtors based on their time period. Company analyses debtors that are due from long period and

no recovery action has been made since they are due. It is essential for the business to identify

the debtors that are due from long so that strict actions could be taken for their recovery and

those which are irrecoverable should be written off from the lists.

Performance Report

The report states about the performance of employees in organisation. The report is

prepared based on the benchmarks and targets that are kept by company to be achieved within

given time frame. On the basis of this report management could identify whether employees are

working with full efficiency or not (Laguecir, Kern and Kharoubi, 2020). Firm motivates and

encourages employees by providing rewards and incentives for achieving the given target.

Budgeting Report

The budget report is an important report for management as it allows to make allocation

of resources among different departments and processes. Budget report is prepared based on

previous reports along with analysing current trends, inflation, demand, market and such other

factors. The budget report also involves comparison of actual and budgeted outcomes. This

allows the management to take steps for improving the existing processes or to change the

policies.

Different cost accounting techniques

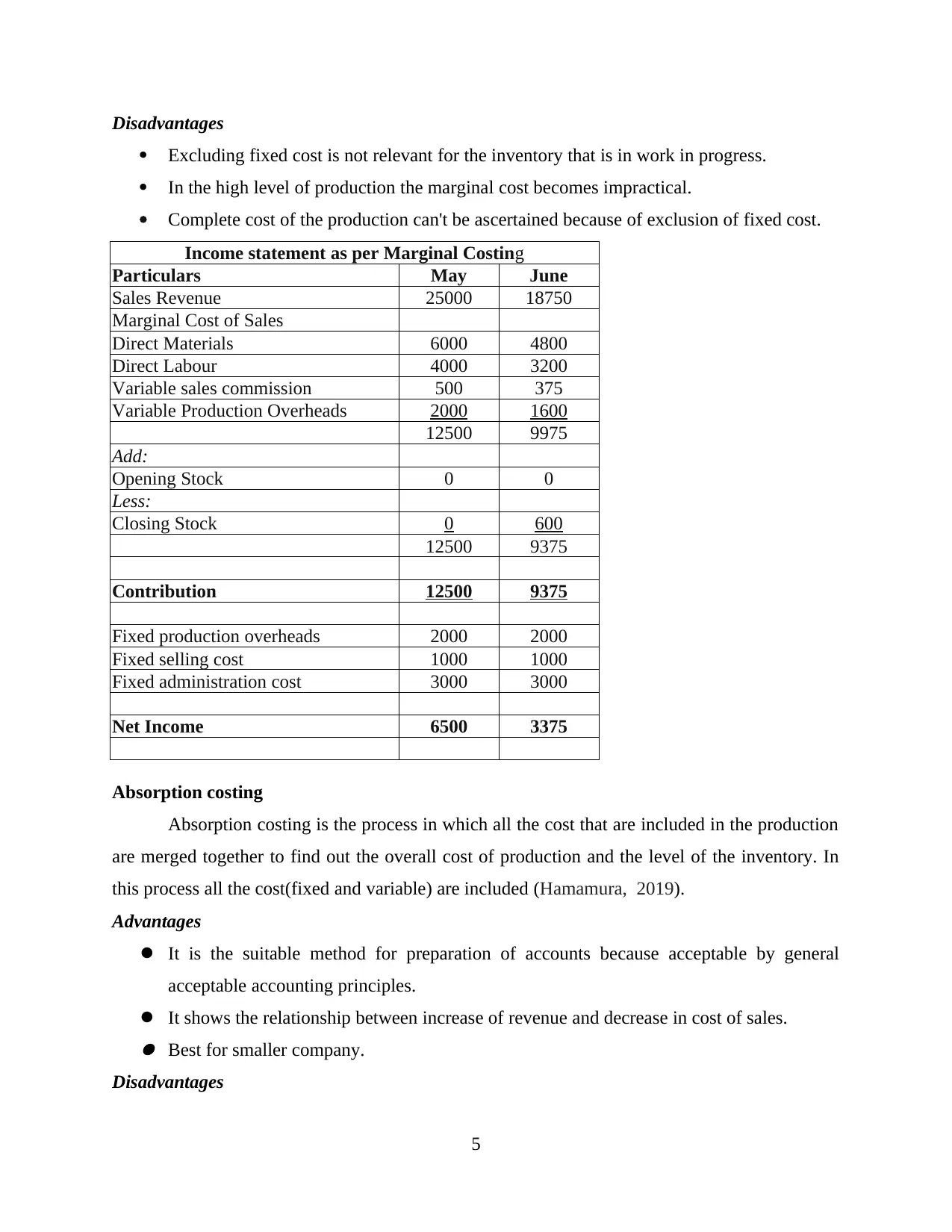

Marginal Costing

Marginal costing is a part of costing techniques where the marginal cost(variable cost) is

charged to the coat per unit and the fixed cost of the period is written off against the contribution.

Advantages

Marginal costing helps in the preparation of the budgetary policy of the company.

It will help in the determination of the price of the product and determination of profit

margin. Can be use for cost control, marginal costing serves the information about per unit cost

and level of the material and labour, so it can be use for cost control.

4

operation.

Debtors Ageing Report

The report states about the debtors of company over the period. The report states the

debtors based on their time period. Company analyses debtors that are due from long period and

no recovery action has been made since they are due. It is essential for the business to identify

the debtors that are due from long so that strict actions could be taken for their recovery and

those which are irrecoverable should be written off from the lists.

Performance Report

The report states about the performance of employees in organisation. The report is

prepared based on the benchmarks and targets that are kept by company to be achieved within

given time frame. On the basis of this report management could identify whether employees are

working with full efficiency or not (Laguecir, Kern and Kharoubi, 2020). Firm motivates and

encourages employees by providing rewards and incentives for achieving the given target.

Budgeting Report

The budget report is an important report for management as it allows to make allocation

of resources among different departments and processes. Budget report is prepared based on

previous reports along with analysing current trends, inflation, demand, market and such other

factors. The budget report also involves comparison of actual and budgeted outcomes. This

allows the management to take steps for improving the existing processes or to change the

policies.

Different cost accounting techniques

Marginal Costing

Marginal costing is a part of costing techniques where the marginal cost(variable cost) is

charged to the coat per unit and the fixed cost of the period is written off against the contribution.

Advantages

Marginal costing helps in the preparation of the budgetary policy of the company.

It will help in the determination of the price of the product and determination of profit

margin. Can be use for cost control, marginal costing serves the information about per unit cost

and level of the material and labour, so it can be use for cost control.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Disadvantages

Excluding fixed cost is not relevant for the inventory that is in work in progress.

In the high level of production the marginal cost becomes impractical.

Complete cost of the production can't be ascertained because of exclusion of fixed cost.

Income statement as per Marginal Costing

Particulars May June

Sales Revenue 25000 18750

Marginal Cost of Sales

Direct Materials 6000 4800

Direct Labour 4000 3200

Variable sales commission 500 375

Variable Production Overheads 2000 1600

12500 9975

Add:

Opening Stock 0 0

Less:

Closing Stock 0 600

12500 9375

Contribution 12500 9375

Fixed production overheads 2000 2000

Fixed selling cost 1000 1000

Fixed administration cost 3000 3000

Net Income 6500 3375

Absorption costing

Absorption costing is the process in which all the cost that are included in the production

are merged together to find out the overall cost of production and the level of the inventory. In

this process all the cost(fixed and variable) are included (Hamamura, 2019).

Advantages

It is the suitable method for preparation of accounts because acceptable by general

acceptable accounting principles.

It shows the relationship between increase of revenue and decrease in cost of sales. Best for smaller company.

Disadvantages

5

Excluding fixed cost is not relevant for the inventory that is in work in progress.

In the high level of production the marginal cost becomes impractical.

Complete cost of the production can't be ascertained because of exclusion of fixed cost.

Income statement as per Marginal Costing

Particulars May June

Sales Revenue 25000 18750

Marginal Cost of Sales

Direct Materials 6000 4800

Direct Labour 4000 3200

Variable sales commission 500 375

Variable Production Overheads 2000 1600

12500 9975

Add:

Opening Stock 0 0

Less:

Closing Stock 0 600

12500 9375

Contribution 12500 9375

Fixed production overheads 2000 2000

Fixed selling cost 1000 1000

Fixed administration cost 3000 3000

Net Income 6500 3375

Absorption costing

Absorption costing is the process in which all the cost that are included in the production

are merged together to find out the overall cost of production and the level of the inventory. In

this process all the cost(fixed and variable) are included (Hamamura, 2019).

Advantages

It is the suitable method for preparation of accounts because acceptable by general

acceptable accounting principles.

It shows the relationship between increase of revenue and decrease in cost of sales. Best for smaller company.

Disadvantages

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

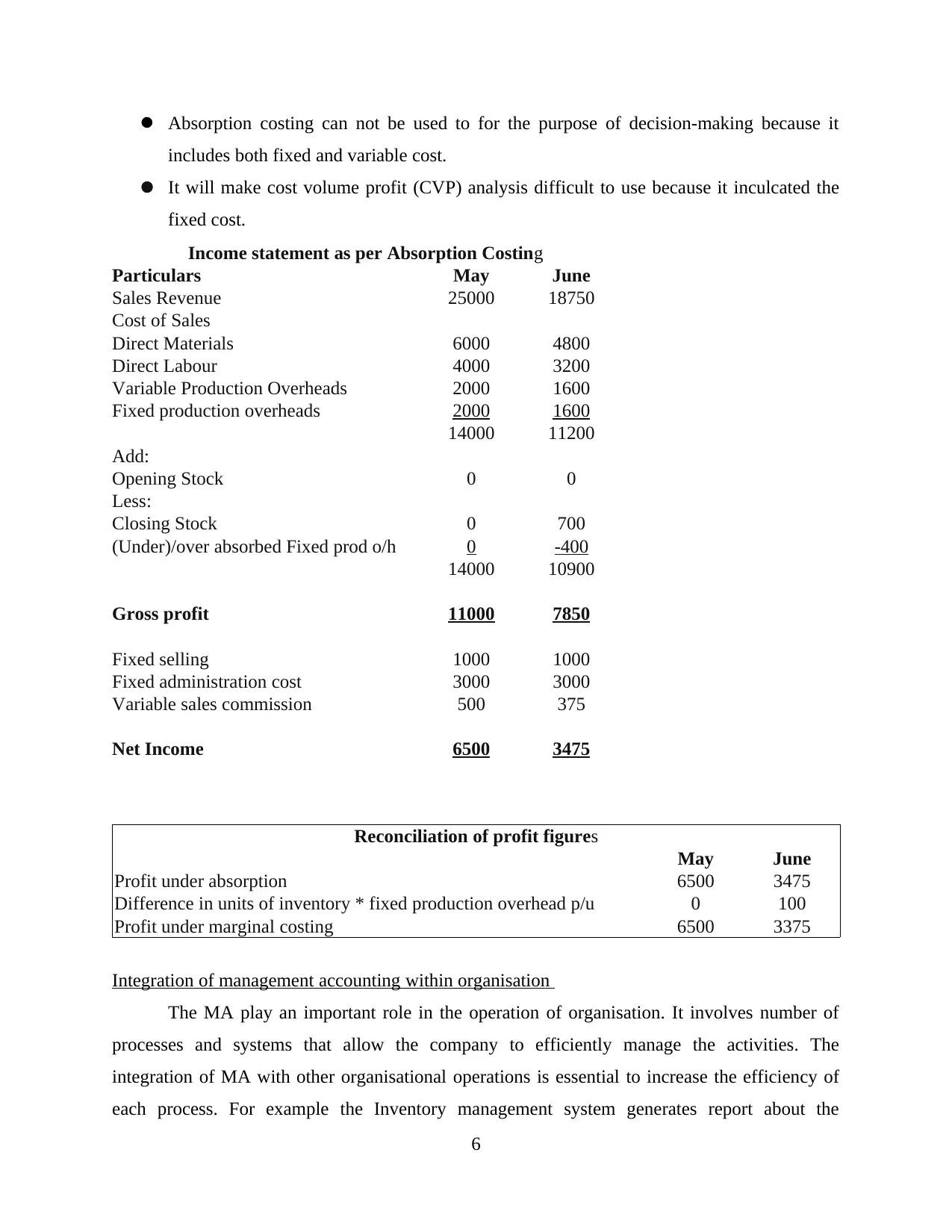

Absorption costing can not be used to for the purpose of decision-making because it

includes both fixed and variable cost.

It will make cost volume profit (CVP) analysis difficult to use because it inculcated the

fixed cost.

Income statement as per Absorption Costing

Particulars May June

Sales Revenue 25000 18750

Cost of Sales

Direct Materials 6000 4800

Direct Labour 4000 3200

Variable Production Overheads 2000 1600

Fixed production overheads 2000 1600

14000 11200

Add:

Opening Stock 0 0

Less:

Closing Stock 0 700

(Under)/over absorbed Fixed prod o/h 0 -400

14000 10900

Gross profit 11000 7850

Fixed selling 1000 1000

Fixed administration cost 3000 3000

Variable sales commission 500 375

Net Income 6500 3475

Reconciliation of profit figures

May June

Profit under absorption 6500 3475

Difference in units of inventory * fixed production overhead p/u 0 100

Profit under marginal costing 6500 3375

Integration of management accounting within organisation

The MA play an important role in the operation of organisation. It involves number of

processes and systems that allow the company to efficiently manage the activities. The

integration of MA with other organisational operations is essential to increase the efficiency of

each process. For example the Inventory management system generates report about the

6

includes both fixed and variable cost.

It will make cost volume profit (CVP) analysis difficult to use because it inculcated the

fixed cost.

Income statement as per Absorption Costing

Particulars May June

Sales Revenue 25000 18750

Cost of Sales

Direct Materials 6000 4800

Direct Labour 4000 3200

Variable Production Overheads 2000 1600

Fixed production overheads 2000 1600

14000 11200

Add:

Opening Stock 0 0

Less:

Closing Stock 0 700

(Under)/over absorbed Fixed prod o/h 0 -400

14000 10900

Gross profit 11000 7850

Fixed selling 1000 1000

Fixed administration cost 3000 3000

Variable sales commission 500 375

Net Income 6500 3475

Reconciliation of profit figures

May June

Profit under absorption 6500 3475

Difference in units of inventory * fixed production overhead p/u 0 100

Profit under marginal costing 6500 3375

Integration of management accounting within organisation

The MA play an important role in the operation of organisation. It involves number of

processes and systems that allow the company to efficiently manage the activities. The

integration of MA with other organisational operations is essential to increase the efficiency of

each process. For example the Inventory management system generates report about the

6

inventory periodically as per requirement that is used by the management to make business

decisions. On the basis of this report different purchase orders are made (Amara and Benelifa,

2017). Likewise cost accounting system allows the cost accountant to prepare cost report that is

used to analyse the different costs associated with manufacturing of products. It allows

management to take decisions for cost control.

Benefits of functions to organisation

Inventory management System

The system provides a simplified version of the inventory management through software.

Use of IMS enables the company to reduce the risk of overselling.

The increase in cost due to shortfall and excess of stocks is controlled through this

system.

It enables the company to identify the product or item from previous record in case of

issue.

Cost Accounting System

The system enables company to identify the profitable as well as unprofitable company.

Management uses the cost reports to prepare budgets for future and reference.

Control over costs and increasing expenses could be made using cost accounting (Abba,

Yahaya and Suleiman, 2018).

It enables company to make comparison between actual and budgeted costs.

Job Costing System

It provides the company with accurate profitability report on product and job.

Management forms performance benchmark using cost reports for particular jobs and

products.

It allows the company to make indirect cost measurement to determine the profits.

Price Optimisation System

It helps the company to determine adequate prices for products and services.

Company could identify the demand of products in market at different price levels.

The method helps the company to determine adequate profit level through pricing.

CONCLUSION

It could be concluded from the above report MA has vital importance in the success of

organisation. It allows the firm to manage all its operation and process in defined and structured

7

decisions. On the basis of this report different purchase orders are made (Amara and Benelifa,

2017). Likewise cost accounting system allows the cost accountant to prepare cost report that is

used to analyse the different costs associated with manufacturing of products. It allows

management to take decisions for cost control.

Benefits of functions to organisation

Inventory management System

The system provides a simplified version of the inventory management through software.

Use of IMS enables the company to reduce the risk of overselling.

The increase in cost due to shortfall and excess of stocks is controlled through this

system.

It enables the company to identify the product or item from previous record in case of

issue.

Cost Accounting System

The system enables company to identify the profitable as well as unprofitable company.

Management uses the cost reports to prepare budgets for future and reference.

Control over costs and increasing expenses could be made using cost accounting (Abba,

Yahaya and Suleiman, 2018).

It enables company to make comparison between actual and budgeted costs.

Job Costing System

It provides the company with accurate profitability report on product and job.

Management forms performance benchmark using cost reports for particular jobs and

products.

It allows the company to make indirect cost measurement to determine the profits.

Price Optimisation System

It helps the company to determine adequate prices for products and services.

Company could identify the demand of products in market at different price levels.

The method helps the company to determine adequate profit level through pricing.

CONCLUSION

It could be concluded from the above report MA has vital importance in the success of

organisation. It allows the firm to manage all its operation and process in defined and structured

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

manner. The reports generated by MA allows the management in making informed decisions

essential for the growth and success or organisation. The different costing techniques allow to

record and compute the profits for business. Based on profits company identifies whether profits

are adequate or not so that further actions could be taken.

8

essential for the growth and success or organisation. The different costing techniques allow to

record and compute the profits for business. Based on profits company identifies whether profits

are adequate or not so that further actions could be taken.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Abdusalomova, N., 2020. Principles of ties of internal control and management accounting

systems at the enterprises of black metallurgy. Архив научных исследований. (2).

Novas, J.C., Alves, M.D.C.G. and Sousa, A., 2017. The role of management accounting systems

in the development of intellectual capital. Journal of Intellectual Capital.

Laguecir, A., Kern, A. and Kharoubi, C., 2020. Management accounting systems in institutional

complexity: Hysteresis and boundaries of practices in social housing. Management

Accounting Research. 49. p.100715.

Amara, T. and Benelifa, S., 2017. The impact of external and internal factors on the management

accounting practices. International Journal of Finance and Accounting. 6(2). pp.46-58.

Abba, M., Yahaya, L. and Suleiman, N., 2018. Explored and critique of contingency theory for

management accounting research. Journal of Accounting and Financial Management

ISSN. 4(5). p.2018.

Kudryashova, Y. N., and et.al., 2020. The organization of management accounting as a

mechanism to improve the efficiency of agricultural enterprises. In BIO Web of

Conferences (Vol. 17). EDP Sciences.

Hamamura, J., 2019. Unobservable transfer price exceeds marginal cost when the manager is

evaluated using a balanced scorecard. Advances in accounting. 44. pp.22-28.

Online

Price Optimisation System. 2020. [Online] Available trough: <https://blog.blackcurve.com/what-

is-price-optimisation>

9

Books and Journals

Abdusalomova, N., 2020. Principles of ties of internal control and management accounting

systems at the enterprises of black metallurgy. Архив научных исследований. (2).

Novas, J.C., Alves, M.D.C.G. and Sousa, A., 2017. The role of management accounting systems

in the development of intellectual capital. Journal of Intellectual Capital.

Laguecir, A., Kern, A. and Kharoubi, C., 2020. Management accounting systems in institutional

complexity: Hysteresis and boundaries of practices in social housing. Management

Accounting Research. 49. p.100715.

Amara, T. and Benelifa, S., 2017. The impact of external and internal factors on the management

accounting practices. International Journal of Finance and Accounting. 6(2). pp.46-58.

Abba, M., Yahaya, L. and Suleiman, N., 2018. Explored and critique of contingency theory for

management accounting research. Journal of Accounting and Financial Management

ISSN. 4(5). p.2018.

Kudryashova, Y. N., and et.al., 2020. The organization of management accounting as a

mechanism to improve the efficiency of agricultural enterprises. In BIO Web of

Conferences (Vol. 17). EDP Sciences.

Hamamura, J., 2019. Unobservable transfer price exceeds marginal cost when the manager is

evaluated using a balanced scorecard. Advances in accounting. 44. pp.22-28.

Online

Price Optimisation System. 2020. [Online] Available trough: <https://blog.blackcurve.com/what-

is-price-optimisation>

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.