Capital Joinery Ltd: Management Accounting Systems & Techniques Report

VerifiedAdded on 2023/01/04

|17

|4735

|96

Report

AI Summary

This report delves into the realm of management accounting, focusing on systems and techniques applicable to businesses like Capital Joinery Ltd. It examines various management accounting systems, including cost accounting, inventory management, job costing, and price optimization, outlining their benefits and applications. The report further explores different methods of management accounting reporting, such as job costing reports, performance reports, and inventory reports, highlighting their roles in organizational processes. Additionally, it analyzes planning tools for budgetary control, comparing activity-based budgeting and zero-based budgeting, and discusses their advantages and limitations. The report also covers the integration of management accounting systems and reporting in organizational processes, emphasizing their impact on decision-making and performance improvement. Finally, the report includes a comparative analysis of management accounting systems used by different organizations, providing insights into adapting to financial challenges.

Unit 5 Management Accounting

Systems & Techniques

Systems & Techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................3

SCENARIO 1.............................................................................................................................3

Management accounting system and its essential requirements............................................3

Different methods of MA reporting.......................................................................................5

Benefits and the limitation of different planning tools for budgetary control.......................7

SCENARIO 2.............................................................................................................................9

Application of different types of management accounting techniques..................................9

Comparing ways companies are adapting management accounting systems for responding

to financial problems............................................................................................................12

CONCLUSION........................................................................................................................14

REFERENCES.........................................................................................................................15

APPENDIX..............................................................................................................................16

INTRODUCTION......................................................................................................................3

SCENARIO 1.............................................................................................................................3

Management accounting system and its essential requirements............................................3

Different methods of MA reporting.......................................................................................5

Benefits and the limitation of different planning tools for budgetary control.......................7

SCENARIO 2.............................................................................................................................9

Application of different types of management accounting techniques..................................9

Comparing ways companies are adapting management accounting systems for responding

to financial problems............................................................................................................12

CONCLUSION........................................................................................................................14

REFERENCES.........................................................................................................................15

APPENDIX..............................................................................................................................16

INTRODUCTION

Management accounting (MA) refers to the accounting system which assists the

business entity in gathering important business-related information which is being utilized by

the internal management team and is different from the financial accounting. The major

reason behind using MA is to undertake managerial decisions pertaining to cost and other

operational activities. In this report, Capital Joinery Ltd is taken as an organization, which is

into broad range of joiners, windows and the mad to measure doors and so forth. This report

states about the different types of MA systems along with its benefits and application. Along

with this, it throws light on the various types of MA reporting with the techniques which is

being utilized by the business entities. It covers the pros and cons of the planning tools for

building up the budgetary control and along with carrying out a comparative analysis of eth

MA systems being used by the two large organizations.

SCENARIO 1

Management accounting system and its essential requirements

As per the IMA, London, management accounting refers to application of the

professional skills and knowledge in the preparing of the crucial reports which result into

providing support to the management in regard to the formulation of the policies and the

other strategic plans and implementing control.

There are various types of management accounting systems which can be used by the

business organization for meeting with its operational requirements. A detailed analysis of

the various MA system is stated below.

Cost accounting system

This MA system is being utilized by the entities in order to determine or estimating

the cost of the its products. This system is also used for the purpose of valuation of inventory,

exercising cost control and in carrying out the profit analysis. It mainly designed for keeping

track of the flow of the stocks from the different stages of the production. For instance, if the

material A transferred from one process to another (Hasyim and Jabid, 2019). It will be

updated automatically in the system. This approach is mainly used by the manufacturing

organization in order to determine how much inventory is put under the different stages. The

essential requirement of this system, is in regard to recording the cost of every transaction

that takes place which assist in establishing the control as well.

Benefits:

This system assists in identifying the activities which are profitable in nature.

Management accounting (MA) refers to the accounting system which assists the

business entity in gathering important business-related information which is being utilized by

the internal management team and is different from the financial accounting. The major

reason behind using MA is to undertake managerial decisions pertaining to cost and other

operational activities. In this report, Capital Joinery Ltd is taken as an organization, which is

into broad range of joiners, windows and the mad to measure doors and so forth. This report

states about the different types of MA systems along with its benefits and application. Along

with this, it throws light on the various types of MA reporting with the techniques which is

being utilized by the business entities. It covers the pros and cons of the planning tools for

building up the budgetary control and along with carrying out a comparative analysis of eth

MA systems being used by the two large organizations.

SCENARIO 1

Management accounting system and its essential requirements

As per the IMA, London, management accounting refers to application of the

professional skills and knowledge in the preparing of the crucial reports which result into

providing support to the management in regard to the formulation of the policies and the

other strategic plans and implementing control.

There are various types of management accounting systems which can be used by the

business organization for meeting with its operational requirements. A detailed analysis of

the various MA system is stated below.

Cost accounting system

This MA system is being utilized by the entities in order to determine or estimating

the cost of the its products. This system is also used for the purpose of valuation of inventory,

exercising cost control and in carrying out the profit analysis. It mainly designed for keeping

track of the flow of the stocks from the different stages of the production. For instance, if the

material A transferred from one process to another (Hasyim and Jabid, 2019). It will be

updated automatically in the system. This approach is mainly used by the manufacturing

organization in order to determine how much inventory is put under the different stages. The

essential requirement of this system, is in regard to recording the cost of every transaction

that takes place which assist in establishing the control as well.

Benefits:

This system assists in identifying the activities which are profitable in nature.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The information gathered through it provides support to organization n undertaking

decision making.

This can be used in calculating the profit/loss pertaining to the product on a periodic

basis.

It can be utilized in establishing cost control in regard to inputs and supplies.

Application

The cost accounting system is used by the manufacturing concerns for appropriately

recording the cost in association with the production of the good.

Inventory management system

This system is mainly implemented for effectively measuring and monitoring the

inventory of the goods in whichever form they are like work in progress, just raw material or

the processed finished product. For the large organizations having complex supply chain, this

system is very much useful (May, Atkinson and Ferrer, 2017). This is very crucial for all

businesses which assist in systematically managing the inventory related problems. This

system is essential in determining the proper time for the placing a new order and the size of

it along with the cost associated with holding it.

Benefits:

This MA system is effective in overcoming the situation of under or over stock of

goods.

It provides assistance in identifying the right time to place order.

It can be further utilized for forecasting eth future requirement and trends.

Application

It can be used by Capital Joinery Ltd for the purpose of managing its stocks of

materials and the business supplies.

Job costing

This type of system is being used when the products are created as per the

specification provide by the client. This system actually incorporates the cost which will be

incurred for completing the given job (Alami and ElMaraghy, 2020). This helps the entity in

putting price of the good which is reasonable in terms of profit. It takes into consideration all

types of cost whether direct or indirect cost. This approach is essential for the firms which are

producing multiple products which are different from one another.

Benefits:

Through this system, cost is being analyzed from different side which results into

increasing the operational efficiency of the firm.

decision making.

This can be used in calculating the profit/loss pertaining to the product on a periodic

basis.

It can be utilized in establishing cost control in regard to inputs and supplies.

Application

The cost accounting system is used by the manufacturing concerns for appropriately

recording the cost in association with the production of the good.

Inventory management system

This system is mainly implemented for effectively measuring and monitoring the

inventory of the goods in whichever form they are like work in progress, just raw material or

the processed finished product. For the large organizations having complex supply chain, this

system is very much useful (May, Atkinson and Ferrer, 2017). This is very crucial for all

businesses which assist in systematically managing the inventory related problems. This

system is essential in determining the proper time for the placing a new order and the size of

it along with the cost associated with holding it.

Benefits:

This MA system is effective in overcoming the situation of under or over stock of

goods.

It provides assistance in identifying the right time to place order.

It can be further utilized for forecasting eth future requirement and trends.

Application

It can be used by Capital Joinery Ltd for the purpose of managing its stocks of

materials and the business supplies.

Job costing

This type of system is being used when the products are created as per the

specification provide by the client. This system actually incorporates the cost which will be

incurred for completing the given job (Alami and ElMaraghy, 2020). This helps the entity in

putting price of the good which is reasonable in terms of profit. It takes into consideration all

types of cost whether direct or indirect cost. This approach is essential for the firms which are

producing multiple products which are different from one another.

Benefits:

Through this system, cost is being analyzed from different side which results into

increasing the operational efficiency of the firm.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In this the cost recorded are very accurate which can be used in comparing budgets

with the actual outcomes so that cost can be controlled.

The cost sheet created one’s can be further for costing the other similar job which

might come up in future.

It can be utilized for figuring any type of defects or spoilage associated with the

production system.

Application

This method is applicable to Capital Joinery Ltd as it can use this system for

identifying the profits in respect to various products being produced by it.

Price optimization system

This MA system is basically the mathematical program which is being utilized for

deciding the price of the item. It is mainly based upon the demand and supply of the good sin

the market (Simchi-Levi, 2017). It takes into account the willingness of the clients pertaining

to buying that product. This helps in achieving the maximum profitability. It is essential for

the purpose of determining the right price for the product according to demand and customer

willingness.

Benefits:

The price is decided as per the demand of it which various according to the

willingness of the customers.

Helps in enhancing the profits of the organization.

It assists the entity in gaining an insight into the market pattern.

It involves optimizing of the entire process which results into reducing the manual

task and risk.

Application

This MA system will support Capital Joinery Ltd which will help in undertaking

business decisions through analysing the price.

Different methods of MA reporting

Job costing

It is mainly utilized by the management for the purpose of evaluating the cost

pertaining to the project in accordance with the standards set. This report provides an analysis

of the total cost that will be incurred in a particular job as against the expected return.

Through this, the profitability in relation to the different jobs can be determined and decision

can be taken to put more focus on the jobs which are more profitable instead of wasting time

and efforts in in the less profitable jobs (Blanchfield, Acharya and Mort, 2018). This report

with the actual outcomes so that cost can be controlled.

The cost sheet created one’s can be further for costing the other similar job which

might come up in future.

It can be utilized for figuring any type of defects or spoilage associated with the

production system.

Application

This method is applicable to Capital Joinery Ltd as it can use this system for

identifying the profits in respect to various products being produced by it.

Price optimization system

This MA system is basically the mathematical program which is being utilized for

deciding the price of the item. It is mainly based upon the demand and supply of the good sin

the market (Simchi-Levi, 2017). It takes into account the willingness of the clients pertaining

to buying that product. This helps in achieving the maximum profitability. It is essential for

the purpose of determining the right price for the product according to demand and customer

willingness.

Benefits:

The price is decided as per the demand of it which various according to the

willingness of the customers.

Helps in enhancing the profits of the organization.

It assists the entity in gaining an insight into the market pattern.

It involves optimizing of the entire process which results into reducing the manual

task and risk.

Application

This MA system will support Capital Joinery Ltd which will help in undertaking

business decisions through analysing the price.

Different methods of MA reporting

Job costing

It is mainly utilized by the management for the purpose of evaluating the cost

pertaining to the project in accordance with the standards set. This report provides an analysis

of the total cost that will be incurred in a particular job as against the expected return.

Through this, the profitability in relation to the different jobs can be determined and decision

can be taken to put more focus on the jobs which are more profitable instead of wasting time

and efforts in in the less profitable jobs (Blanchfield, Acharya and Mort, 2018). This report

provides an insight in analyzing the expenditure in time so that corrective actions can be

taken on time.

Performance report

This report is prepared for analyzing and reviewing the performance of the individuals

and the departments. In the large business concerns, the division wise report is being

prepared. These reports are valuable for the association to take vital business choices

regarding the future of the association. In view of this report, the workers are rewarded for

their responsibility towards work and the association while the under performers are either

laid off or managed in alternate manner (Kim, Watkins and Lu, 2017). This report gives

profound knowledge about the working state of the organization dependent on its exhibition

as for the specific rules. It demonstrates any imperfection in the framework which is limiting

it for accomplishing ideal performance level. Hence, the function of this report is

fundamental for any association in getting precise information of the strategy for

accomplishing the objectives.

Account receivable aging report

It is an important report which is being utilized by the management in case if the

goods are sold on credit to the customers. This report gives the total breakdown of the clients

remaining balance. This report is significant as it enables the administration in distinguishing

the any issue in the organization's collection system (Ndebugri and Tweneboah Senzu, 2017).

Aside from this, it likewise permits management in recognizing the defaulters. In view of this

report, arrangement is made for defaulters and if any adjustment in the credit strategy is

required, the equivalent is additionally done.

Inventory report

This report gives the synopsis of existing stock of the business. It gives total insights

concerning the how much stock is there, which item is selling quicker, different criteria based

performance of the item. It includes total record keeping of every single exchange separately

and monitors each exchange of stock. In light of the data given in the report, helps the

business associations in creation projections about the future necessities. It likewise helps in

recognizing the any wastage of the stock and depicts the areas of progress. Therefore, it

prompts ideal usage of resources.

Integration of management accounting system and reporting in the organizational

process

The integration of MA system and reporting will assist the management in

accomplishing the required goals and targets. It will support the entity in effectively handling

taken on time.

Performance report

This report is prepared for analyzing and reviewing the performance of the individuals

and the departments. In the large business concerns, the division wise report is being

prepared. These reports are valuable for the association to take vital business choices

regarding the future of the association. In view of this report, the workers are rewarded for

their responsibility towards work and the association while the under performers are either

laid off or managed in alternate manner (Kim, Watkins and Lu, 2017). This report gives

profound knowledge about the working state of the organization dependent on its exhibition

as for the specific rules. It demonstrates any imperfection in the framework which is limiting

it for accomplishing ideal performance level. Hence, the function of this report is

fundamental for any association in getting precise information of the strategy for

accomplishing the objectives.

Account receivable aging report

It is an important report which is being utilized by the management in case if the

goods are sold on credit to the customers. This report gives the total breakdown of the clients

remaining balance. This report is significant as it enables the administration in distinguishing

the any issue in the organization's collection system (Ndebugri and Tweneboah Senzu, 2017).

Aside from this, it likewise permits management in recognizing the defaulters. In view of this

report, arrangement is made for defaulters and if any adjustment in the credit strategy is

required, the equivalent is additionally done.

Inventory report

This report gives the synopsis of existing stock of the business. It gives total insights

concerning the how much stock is there, which item is selling quicker, different criteria based

performance of the item. It includes total record keeping of every single exchange separately

and monitors each exchange of stock. In light of the data given in the report, helps the

business associations in creation projections about the future necessities. It likewise helps in

recognizing the any wastage of the stock and depicts the areas of progress. Therefore, it

prompts ideal usage of resources.

Integration of management accounting system and reporting in the organizational

process

The integration of MA system and reporting will assist the management in

accomplishing the required goals and targets. It will support the entity in effectively handling

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the operational activities and tasks in an appropriate way with the available amount of

information. This will assist the organization in determining the areas where further

improvement and focus is required which will help in enhancing the performance and

profitability of the company. The integration will support the organization in undertaking the

right decision for undertaking the effective and right planning.

Benefits and the limitation of different planning tools for budgetary control

The budget prepared assists the business in gaining knowledge pertaining to the

expected future income along with the usage of the same in a business organization. This

helps in distribution of the resources across the various business-related tasks. The various

tools that can be used by the Capital Joinery Ltd are described below.

Activity Based Budgeting

It is the planning strategy where the association gets ready spending plans based on

the activities as opposed to the organizational divisions. The spending plans are set up based

on forecasted figure of assets to be utilized and profitability produced under each activity.

The planning method don't utilize the financial plans arranged for earlier year for the

readiness of current spending plan (Klimenko, 2019). It helps the entity in recognizing the

cost and the expenses related with every action being acted in the production cycle of the

undertaking. The activity based financial plan will help the Capital Joinery Ltd in recognizing

the loopholes of expenses and wastages and agreeing to which the organizations take

remedial measures. Following are the advantages and disadvantages of it to Capital Joinery

Ltd:

Advantages

This method is very easy to actualize as it is not a time-consuming process.

It provides support to the business in identifying the errors in the production

procedures.

This tool does not take into account the previous year’s budget.

Disadvantages

This tool requires highly experienced professional with the relevant skills and ability.

This might be costly for implementing it in the business.

Zero based Budgeting

It refers to the planning procedure that don't think about the financial plans of earlier

year in the readiness of financial plan for current year. The whole financial plan is set up after

legitimate examination and investigation identified with the spending plan. In this financial

plan, the chances of blunders and any mistake of the past financial plans are not conveyed

information. This will assist the organization in determining the areas where further

improvement and focus is required which will help in enhancing the performance and

profitability of the company. The integration will support the organization in undertaking the

right decision for undertaking the effective and right planning.

Benefits and the limitation of different planning tools for budgetary control

The budget prepared assists the business in gaining knowledge pertaining to the

expected future income along with the usage of the same in a business organization. This

helps in distribution of the resources across the various business-related tasks. The various

tools that can be used by the Capital Joinery Ltd are described below.

Activity Based Budgeting

It is the planning strategy where the association gets ready spending plans based on

the activities as opposed to the organizational divisions. The spending plans are set up based

on forecasted figure of assets to be utilized and profitability produced under each activity.

The planning method don't utilize the financial plans arranged for earlier year for the

readiness of current spending plan (Klimenko, 2019). It helps the entity in recognizing the

cost and the expenses related with every action being acted in the production cycle of the

undertaking. The activity based financial plan will help the Capital Joinery Ltd in recognizing

the loopholes of expenses and wastages and agreeing to which the organizations take

remedial measures. Following are the advantages and disadvantages of it to Capital Joinery

Ltd:

Advantages

This method is very easy to actualize as it is not a time-consuming process.

It provides support to the business in identifying the errors in the production

procedures.

This tool does not take into account the previous year’s budget.

Disadvantages

This tool requires highly experienced professional with the relevant skills and ability.

This might be costly for implementing it in the business.

Zero based Budgeting

It refers to the planning procedure that don't think about the financial plans of earlier

year in the readiness of financial plan for current year. The whole financial plan is set up after

legitimate examination and investigation identified with the spending plan. In this financial

plan, the chances of blunders and any mistake of the past financial plans are not conveyed

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

forward in the financial plans for current (Lobodina and et.al., 2020). This helps the Capital

Joinery Ltd in outlining more exact spending plans with least fluctuations as everything is

begun from the new. The justification isn't needed to be given for each thing like the

conventional planning technique as each thing is embedded after research and its impact. Its

advantages and disadvantages to Capital Joinery Ltd are stated below:

Advantages

It does not consider past year’s budget plan.

Proper investigation is being carried out before putting an item into budget.

It is relevant for the businesses which faces frequent changes.

Disadvantages

This tool requires lot of time and efforts.

It is expensive enough to be implemented in the small businesses.

Operational budget

Operational financial plan accounts to the spending plans arranged for the operational

tasks of the association. It includes determining the future pay and costs of the venture

dependent on the past patterns (Sulindawati, Yudantara and Musmini, 2019). The operational

financial plans studies about the spending plans of a year ago for getting ready spending

plans for current year. It helps the Capital Joinery Ltd in legitimate assignment of assets

between the various divisions and different business tasks. Its pros and cons are given below

to the Capital Joinery Ltd.

Advantages

This tool is easy to understand by the individuals having interest in it.

It provides assistance to the management in timely and appropriate distribution of the

resources.

The planning tool can be utilized for the purpose of establishing control over the

operational expenses.

Disadvantages

It is dependent on the last year’s financial plan which might increase the chance of

making the mistakes.

Through this tool, the estimation made might not be accurate which results into

undertaking wrong decision.

Joinery Ltd in outlining more exact spending plans with least fluctuations as everything is

begun from the new. The justification isn't needed to be given for each thing like the

conventional planning technique as each thing is embedded after research and its impact. Its

advantages and disadvantages to Capital Joinery Ltd are stated below:

Advantages

It does not consider past year’s budget plan.

Proper investigation is being carried out before putting an item into budget.

It is relevant for the businesses which faces frequent changes.

Disadvantages

This tool requires lot of time and efforts.

It is expensive enough to be implemented in the small businesses.

Operational budget

Operational financial plan accounts to the spending plans arranged for the operational

tasks of the association. It includes determining the future pay and costs of the venture

dependent on the past patterns (Sulindawati, Yudantara and Musmini, 2019). The operational

financial plans studies about the spending plans of a year ago for getting ready spending

plans for current year. It helps the Capital Joinery Ltd in legitimate assignment of assets

between the various divisions and different business tasks. Its pros and cons are given below

to the Capital Joinery Ltd.

Advantages

This tool is easy to understand by the individuals having interest in it.

It provides assistance to the management in timely and appropriate distribution of the

resources.

The planning tool can be utilized for the purpose of establishing control over the

operational expenses.

Disadvantages

It is dependent on the last year’s financial plan which might increase the chance of

making the mistakes.

Through this tool, the estimation made might not be accurate which results into

undertaking wrong decision.

SCENARIO 2

Application of different types of management accounting techniques

There are various types of MA techniques which can be utilized by the organization

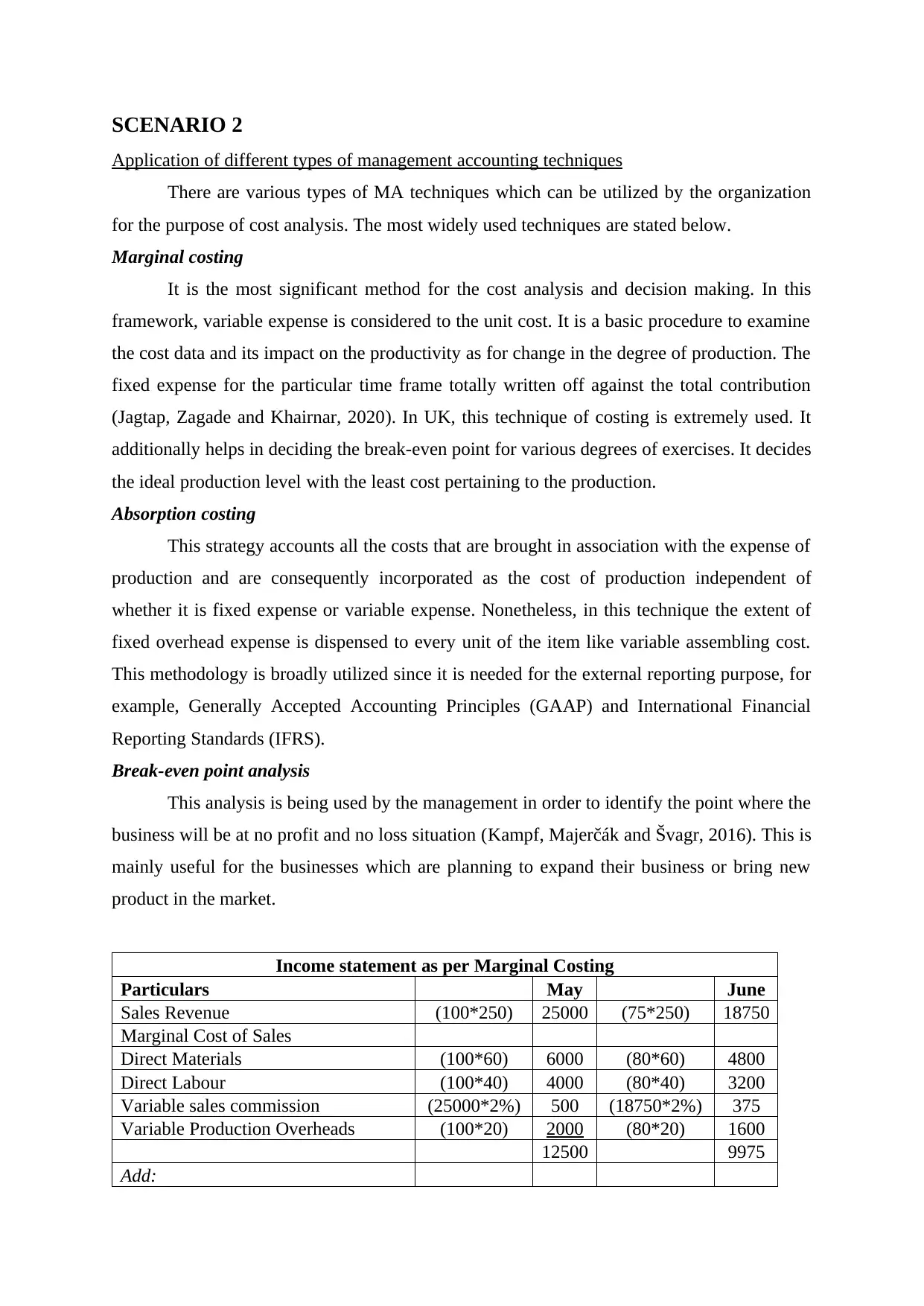

for the purpose of cost analysis. The most widely used techniques are stated below.

Marginal costing

It is the most significant method for the cost analysis and decision making. In this

framework, variable expense is considered to the unit cost. It is a basic procedure to examine

the cost data and its impact on the productivity as for change in the degree of production. The

fixed expense for the particular time frame totally written off against the total contribution

(Jagtap, Zagade and Khairnar, 2020). In UK, this technique of costing is extremely used. It

additionally helps in deciding the break-even point for various degrees of exercises. It decides

the ideal production level with the least cost pertaining to the production.

Absorption costing

This strategy accounts all the costs that are brought in association with the expense of

production and are consequently incorporated as the cost of production independent of

whether it is fixed expense or variable expense. Nonetheless, in this technique the extent of

fixed overhead expense is dispensed to every unit of the item like variable assembling cost.

This methodology is broadly utilized since it is needed for the external reporting purpose, for

example, Generally Accepted Accounting Principles (GAAP) and International Financial

Reporting Standards (IFRS).

Break-even point analysis

This analysis is being used by the management in order to identify the point where the

business will be at no profit and no loss situation (Kampf, Majerčák and Švagr, 2016). This is

mainly useful for the businesses which are planning to expand their business or bring new

product in the market.

Income statement as per Marginal Costing

Particulars May June

Sales Revenue (100*250) 25000 (75*250) 18750

Marginal Cost of Sales

Direct Materials (100*60) 6000 (80*60) 4800

Direct Labour (100*40) 4000 (80*40) 3200

Variable sales commission (25000*2%) 500 (18750*2%) 375

Variable Production Overheads (100*20) 2000 (80*20) 1600

12500 9975

Add:

Application of different types of management accounting techniques

There are various types of MA techniques which can be utilized by the organization

for the purpose of cost analysis. The most widely used techniques are stated below.

Marginal costing

It is the most significant method for the cost analysis and decision making. In this

framework, variable expense is considered to the unit cost. It is a basic procedure to examine

the cost data and its impact on the productivity as for change in the degree of production. The

fixed expense for the particular time frame totally written off against the total contribution

(Jagtap, Zagade and Khairnar, 2020). In UK, this technique of costing is extremely used. It

additionally helps in deciding the break-even point for various degrees of exercises. It decides

the ideal production level with the least cost pertaining to the production.

Absorption costing

This strategy accounts all the costs that are brought in association with the expense of

production and are consequently incorporated as the cost of production independent of

whether it is fixed expense or variable expense. Nonetheless, in this technique the extent of

fixed overhead expense is dispensed to every unit of the item like variable assembling cost.

This methodology is broadly utilized since it is needed for the external reporting purpose, for

example, Generally Accepted Accounting Principles (GAAP) and International Financial

Reporting Standards (IFRS).

Break-even point analysis

This analysis is being used by the management in order to identify the point where the

business will be at no profit and no loss situation (Kampf, Majerčák and Švagr, 2016). This is

mainly useful for the businesses which are planning to expand their business or bring new

product in the market.

Income statement as per Marginal Costing

Particulars May June

Sales Revenue (100*250) 25000 (75*250) 18750

Marginal Cost of Sales

Direct Materials (100*60) 6000 (80*60) 4800

Direct Labour (100*40) 4000 (80*40) 3200

Variable sales commission (25000*2%) 500 (18750*2%) 375

Variable Production Overheads (100*20) 2000 (80*20) 1600

12500 9975

Add:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Opening Stock 0 0

Less:

Closing Stock 0 (5*120) 600

12500 9375

Contribution 12500 9375

Fixed production overheads 2000 2000

Fixed selling cost 1000 1000

Fixed administration cost 3000 3000

Net Income 6500 3375

Income statement as per Absorption Costing

Particulars May June

Sales Revenue (100*250) 25000 (75*250) 18750

Cost of Sales

Direct Materials (100*60) 6000 (80*60) 4800

Direct Labour (100*40) 4000 (80*40) 3200

Variable Production Overheads (100*20) 2000 (80*20) 1600

Fixed production overheads (100*20) 2000 (80*20) 1600

14000 11200

Add:

Opening Stock 0 0

Less:

Closing Stock 0 (5*140) 700

14000 10500

Gross profit 11000 8250

Fixed selling 1000 1000

Fixed administration cost 3000 3000

Variable sales commission (25000*2%) 500 (18750*2%) 375

Net Income 6500 3875

Reconciliation of profit figures

May June

Profit under absorption 6500 3875

Difference in units of inventory * fixed production

overhead p/u 0 (20*20) 400

Profit under marginal costing 6500 3475

Less:

Closing Stock 0 (5*120) 600

12500 9375

Contribution 12500 9375

Fixed production overheads 2000 2000

Fixed selling cost 1000 1000

Fixed administration cost 3000 3000

Net Income 6500 3375

Income statement as per Absorption Costing

Particulars May June

Sales Revenue (100*250) 25000 (75*250) 18750

Cost of Sales

Direct Materials (100*60) 6000 (80*60) 4800

Direct Labour (100*40) 4000 (80*40) 3200

Variable Production Overheads (100*20) 2000 (80*20) 1600

Fixed production overheads (100*20) 2000 (80*20) 1600

14000 11200

Add:

Opening Stock 0 0

Less:

Closing Stock 0 (5*140) 700

14000 10500

Gross profit 11000 8250

Fixed selling 1000 1000

Fixed administration cost 3000 3000

Variable sales commission (25000*2%) 500 (18750*2%) 375

Net Income 6500 3875

Reconciliation of profit figures

May June

Profit under absorption 6500 3875

Difference in units of inventory * fixed production

overhead p/u 0 (20*20) 400

Profit under marginal costing 6500 3475

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation: It can be said that the profit under the absorption cost is higher than that of

marginal costing which is because it incorporates the fixed expenses while determining the

cost of production. Along with that, absorption costing is recommended for the external

reporting purpose as well.

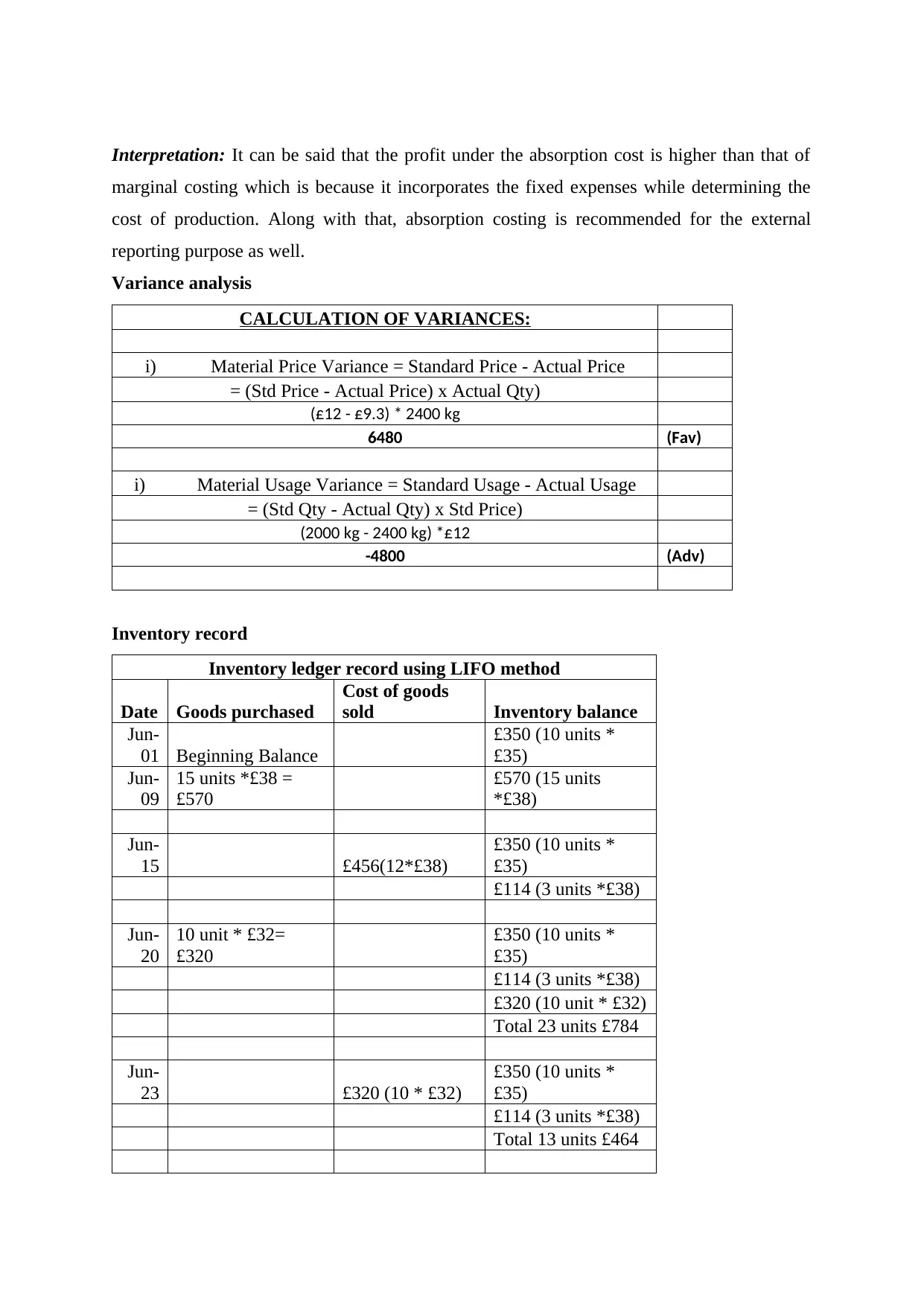

Variance analysis

CALCULATION OF VARIANCES:

i) Material Price Variance = Standard Price - Actual Price

= (Std Price - Actual Price) x Actual Qty)

(£12 - £9.3) * 2400 kg

6480 (Fav)

i) Material Usage Variance = Standard Usage - Actual Usage

= (Std Qty - Actual Qty) x Std Price)

(2000 kg - 2400 kg) *£12

-4800 (Adv)

Inventory record

Inventory ledger record using LIFO method

Date Goods purchased

Cost of goods

sold Inventory balance

Jun-

01 Beginning Balance

£350 (10 units *

£35)

Jun-

09

15 units *£38 =

£570

£570 (15 units

*£38)

Jun-

15 £456(12*£38)

£350 (10 units *

£35)

£114 (3 units *£38)

Jun-

20

10 unit * £32=

£320

£350 (10 units *

£35)

£114 (3 units *£38)

£320 (10 unit * £32)

Total 23 units £784

Jun-

23 £320 (10 * £32)

£350 (10 units *

£35)

£114 (3 units *£38)

Total 13 units £464

marginal costing which is because it incorporates the fixed expenses while determining the

cost of production. Along with that, absorption costing is recommended for the external

reporting purpose as well.

Variance analysis

CALCULATION OF VARIANCES:

i) Material Price Variance = Standard Price - Actual Price

= (Std Price - Actual Price) x Actual Qty)

(£12 - £9.3) * 2400 kg

6480 (Fav)

i) Material Usage Variance = Standard Usage - Actual Usage

= (Std Qty - Actual Qty) x Std Price)

(2000 kg - 2400 kg) *£12

-4800 (Adv)

Inventory record

Inventory ledger record using LIFO method

Date Goods purchased

Cost of goods

sold Inventory balance

Jun-

01 Beginning Balance

£350 (10 units *

£35)

Jun-

09

15 units *£38 =

£570

£570 (15 units

*£38)

Jun-

15 £456(12*£38)

£350 (10 units *

£35)

£114 (3 units *£38)

Jun-

20

10 unit * £32=

£320

£350 (10 units *

£35)

£114 (3 units *£38)

£320 (10 unit * £32)

Total 23 units £784

Jun-

23 £320 (10 * £32)

£350 (10 units *

£35)

£114 (3 units *£38)

Total 13 units £464

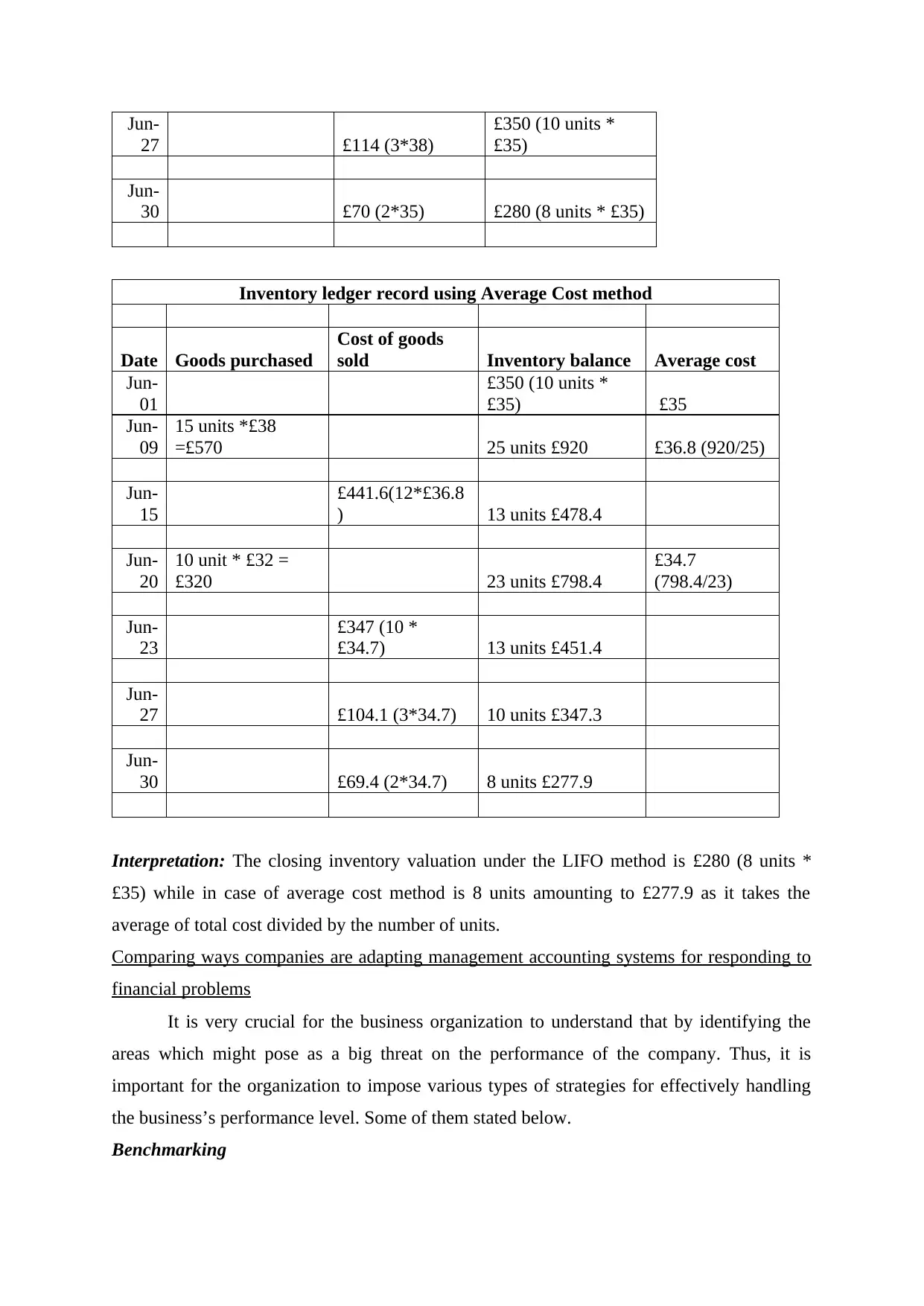

Jun-

27 £114 (3*38)

£350 (10 units *

£35)

Jun-

30 £70 (2*35) £280 (8 units * £35)

Inventory ledger record using Average Cost method

Date Goods purchased

Cost of goods

sold Inventory balance Average cost

Jun-

01

£350 (10 units *

£35) £35

Jun-

09

15 units *£38

=£570 25 units £920 £36.8 (920/25)

Jun-

15

£441.6(12*£36.8

) 13 units £478.4

Jun-

20

10 unit * £32 =

£320 23 units £798.4

£34.7

(798.4/23)

Jun-

23

£347 (10 *

£34.7) 13 units £451.4

Jun-

27 £104.1 (3*34.7) 10 units £347.3

Jun-

30 £69.4 (2*34.7) 8 units £277.9

Interpretation: The closing inventory valuation under the LIFO method is £280 (8 units *

£35) while in case of average cost method is 8 units amounting to £277.9 as it takes the

average of total cost divided by the number of units.

Comparing ways companies are adapting management accounting systems for responding to

financial problems

It is very crucial for the business organization to understand that by identifying the

areas which might pose as a big threat on the performance of the company. Thus, it is

important for the organization to impose various types of strategies for effectively handling

the business’s performance level. Some of them stated below.

Benchmarking

27 £114 (3*38)

£350 (10 units *

£35)

Jun-

30 £70 (2*35) £280 (8 units * £35)

Inventory ledger record using Average Cost method

Date Goods purchased

Cost of goods

sold Inventory balance Average cost

Jun-

01

£350 (10 units *

£35) £35

Jun-

09

15 units *£38

=£570 25 units £920 £36.8 (920/25)

Jun-

15

£441.6(12*£36.8

) 13 units £478.4

Jun-

20

10 unit * £32 =

£320 23 units £798.4

£34.7

(798.4/23)

Jun-

23

£347 (10 *

£34.7) 13 units £451.4

Jun-

27 £104.1 (3*34.7) 10 units £347.3

Jun-

30 £69.4 (2*34.7) 8 units £277.9

Interpretation: The closing inventory valuation under the LIFO method is £280 (8 units *

£35) while in case of average cost method is 8 units amounting to £277.9 as it takes the

average of total cost divided by the number of units.

Comparing ways companies are adapting management accounting systems for responding to

financial problems

It is very crucial for the business organization to understand that by identifying the

areas which might pose as a big threat on the performance of the company. Thus, it is

important for the organization to impose various types of strategies for effectively handling

the business’s performance level. Some of them stated below.

Benchmarking

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.