Management Accounting Systems and Techniques Report - Finance Module

VerifiedAdded on 2021/01/02

|18

|5683

|22

Report

AI Summary

This report delves into the core concepts of management accounting, exploring its role in financial decision-making and organizational goal achievement. It begins by defining management accounting and outlining the essential requirements of various systems, including cost accounting, inventory management, job costing, and price-optimizing systems. The report then examines different methods used for management accounting reporting, such as inventory reports, performance reports, accounts receivable reports, cost accounting reports, and cash flow reports. A significant portion of the report is dedicated to cost analysis, where it calculates costs using appropriate techniques to prepare income statements under both marginal and absorption costing methods. Furthermore, the report discusses the advantages and disadvantages of different types of planning tools used for budgetary control. Finally, it compares how organizations adapt management accounting systems to respond to financial problems, providing a comprehensive overview of the subject matter.

Management

Accounting Systems

&

Techniques

Accounting Systems

&

Techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Explain management accounting and essential requirements of various types of

management accounting systems................................................................................................3

P2. Explain different methods used for management accounting reporting...............................6

TASK 2............................................................................................................................................7

P3. Calculate costs using appropriate techniques of cost analysis to prepare and income

statement using marginal and absorption costs...........................................................................7

TASK 3..........................................................................................................................................11

P4 Advantages and disadvantages of different types of planning tools used for budgetary

control ......................................................................................................................................11

TASK 4..........................................................................................................................................14

P5. Compare how organisations are adapting management accounting systems to respond to

financial problems.....................................................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

.......................................................................................................................................................17

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Explain management accounting and essential requirements of various types of

management accounting systems................................................................................................3

P2. Explain different methods used for management accounting reporting...............................6

TASK 2............................................................................................................................................7

P3. Calculate costs using appropriate techniques of cost analysis to prepare and income

statement using marginal and absorption costs...........................................................................7

TASK 3..........................................................................................................................................11

P4 Advantages and disadvantages of different types of planning tools used for budgetary

control ......................................................................................................................................11

TASK 4..........................................................................................................................................14

P5. Compare how organisations are adapting management accounting systems to respond to

financial problems.....................................................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

.......................................................................................................................................................17

INTRODUCTION

Management accounting is concerned with the process of assessing costs incurred in

business operations to prepare internal financial report, accounts and records for making

informed decision to accomplish organizational goals (DRURY, 2013). It is also known as

managerial or cost accounting. UK Financial Consultants Ltd. Has been chosen for this report.

Further, it covers meaning of management accounting along with its essential requirements and

different methods used for management accounting reporting. Furthermore, calculation of costs

through appropriate techniques of cost analysis and advantages and disadvantages of different

types of planing tools for budgetary control. Lastly, comparison of organizations opting

management accounting system to address financial problems.

TASK 1

P1. Explain management accounting and essential requirements of various types of management

accounting systems

The Institute of Cost and Management Accountants, London, has defined

Management Accounting as “The application of professional knowledge and skill in the

preparation of accounting information in such a way as to assist management in the formulation

of policies and in the planning and control of the operation of the undertakings.” In simple

words, it involves business activities of planning, organising, staffing, directing and controlling

the day-to-day activities for achieving goals and objectives of an entity. Policies are a major part

of this accounting by following which decisions are made (Hilton, and Platt, 2013).

Management Accounting System comprise of actions and framework which are applied

to each departments functioning in an organization. It forms a co-ordination between internal

parties. The scope of this system is vast as it takes into both financial as well as non-financial

data. Johnson and Kaplan defined that management accounting system should effective enough

to provide accurate, reliable and timely information so that costs can be controlled, measured in

order to improve productivity by implementing better production processes.

Managerial accounting can provide numerous benefits to an entity which can have

significant impact on its operations. Further, it is importance to make a part in as internal parties

use qualitative and quantitative information to make decisions. This encourages continuous

Management accounting is concerned with the process of assessing costs incurred in

business operations to prepare internal financial report, accounts and records for making

informed decision to accomplish organizational goals (DRURY, 2013). It is also known as

managerial or cost accounting. UK Financial Consultants Ltd. Has been chosen for this report.

Further, it covers meaning of management accounting along with its essential requirements and

different methods used for management accounting reporting. Furthermore, calculation of costs

through appropriate techniques of cost analysis and advantages and disadvantages of different

types of planing tools for budgetary control. Lastly, comparison of organizations opting

management accounting system to address financial problems.

TASK 1

P1. Explain management accounting and essential requirements of various types of management

accounting systems

The Institute of Cost and Management Accountants, London, has defined

Management Accounting as “The application of professional knowledge and skill in the

preparation of accounting information in such a way as to assist management in the formulation

of policies and in the planning and control of the operation of the undertakings.” In simple

words, it involves business activities of planning, organising, staffing, directing and controlling

the day-to-day activities for achieving goals and objectives of an entity. Policies are a major part

of this accounting by following which decisions are made (Hilton, and Platt, 2013).

Management Accounting System comprise of actions and framework which are applied

to each departments functioning in an organization. It forms a co-ordination between internal

parties. The scope of this system is vast as it takes into both financial as well as non-financial

data. Johnson and Kaplan defined that management accounting system should effective enough

to provide accurate, reliable and timely information so that costs can be controlled, measured in

order to improve productivity by implementing better production processes.

Managerial accounting can provide numerous benefits to an entity which can have

significant impact on its operations. Further, it is importance to make a part in as internal parties

use qualitative and quantitative information to make decisions. This encourages continuous

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

improvement, effective management of cost, management of quality etc. Further, it helps in

measuring costs in order to reduce unnecessary costs. It has four basic principles viz. Influence,

relevance, value and trust. Management Accounting undertakes number of tasks and activities

for managing business through strategic planning. It has its roots from stewardship role in

European merchant trading venture. It evolved during industrial revolution and emerged after

financial accounting.

Basis Management Accounting Financial Accounting

Meaning It provides qualitative and

quantitative information to managers

for making decisions, strategies,

plans and policies for smooth

functioning of business.

It refers to preparation of financial

statements on the basis of historical

and current financial information in

order to provide report to outside

parties whose decisions can be

influenced by such information.

Inherent It help in making fruitful decisions by

applying which organizational goals

can be achieved.

It classifies, analyses, records and

summarizes financial data into a

report form.

Application It improves the capabilities of

management to make strategies, plans

and policies to be applicable within

the organization (Hiebl, 2014).

The financial data is used to disclose

true picture of viability of financial

affairs.

Scope It has wider scope as it consists both

financial and non-financial

information.

It is not as wider as management

accounting.

Dependence It depends on financial accounting to

make right and accurate decisions.

It is independent of management

accounting.

Basis of

decision-

making

It takes into account past as well as

forecasted information to make

decisions.

Only previous financial data form the

basis for decisions that will be

implemented in future.

Statutory There is no legal requirements or It is legally compulsory for companies

measuring costs in order to reduce unnecessary costs. It has four basic principles viz. Influence,

relevance, value and trust. Management Accounting undertakes number of tasks and activities

for managing business through strategic planning. It has its roots from stewardship role in

European merchant trading venture. It evolved during industrial revolution and emerged after

financial accounting.

Basis Management Accounting Financial Accounting

Meaning It provides qualitative and

quantitative information to managers

for making decisions, strategies,

plans and policies for smooth

functioning of business.

It refers to preparation of financial

statements on the basis of historical

and current financial information in

order to provide report to outside

parties whose decisions can be

influenced by such information.

Inherent It help in making fruitful decisions by

applying which organizational goals

can be achieved.

It classifies, analyses, records and

summarizes financial data into a

report form.

Application It improves the capabilities of

management to make strategies, plans

and policies to be applicable within

the organization (Hiebl, 2014).

The financial data is used to disclose

true picture of viability of financial

affairs.

Scope It has wider scope as it consists both

financial and non-financial

information.

It is not as wider as management

accounting.

Dependence It depends on financial accounting to

make right and accurate decisions.

It is independent of management

accounting.

Basis of

decision-

making

It takes into account past as well as

forecasted information to make

decisions.

Only previous financial data form the

basis for decisions that will be

implemented in future.

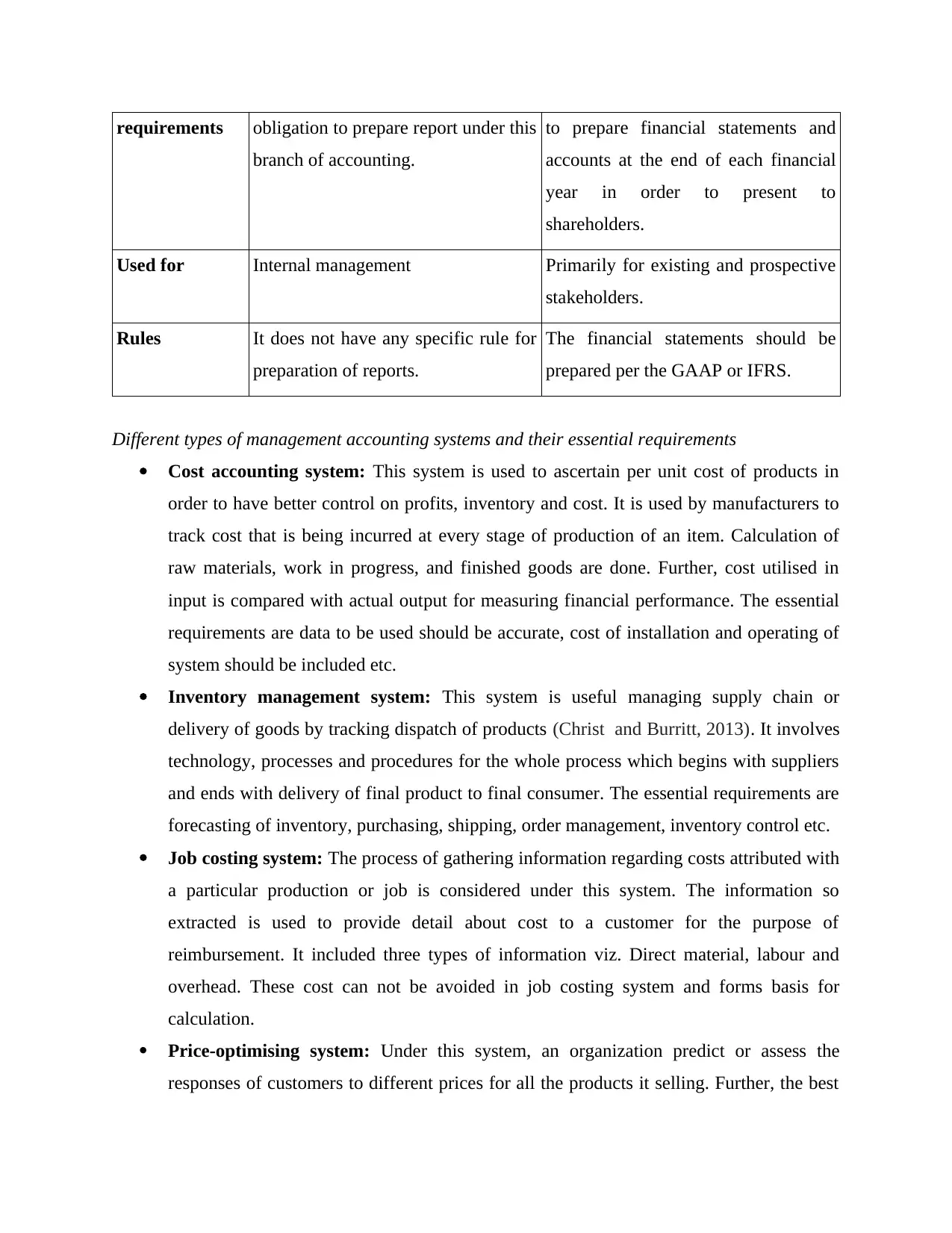

Statutory There is no legal requirements or It is legally compulsory for companies

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

requirements obligation to prepare report under this

branch of accounting.

to prepare financial statements and

accounts at the end of each financial

year in order to present to

shareholders.

Used for Internal management Primarily for existing and prospective

stakeholders.

Rules It does not have any specific rule for

preparation of reports.

The financial statements should be

prepared per the GAAP or IFRS.

Different types of management accounting systems and their essential requirements

Cost accounting system: This system is used to ascertain per unit cost of products in

order to have better control on profits, inventory and cost. It is used by manufacturers to

track cost that is being incurred at every stage of production of an item. Calculation of

raw materials, work in progress, and finished goods are done. Further, cost utilised in

input is compared with actual output for measuring financial performance. The essential

requirements are data to be used should be accurate, cost of installation and operating of

system should be included etc.

Inventory management system: This system is useful managing supply chain or

delivery of goods by tracking dispatch of products (Christ and Burritt, 2013). It involves

technology, processes and procedures for the whole process which begins with suppliers

and ends with delivery of final product to final consumer. The essential requirements are

forecasting of inventory, purchasing, shipping, order management, inventory control etc.

Job costing system: The process of gathering information regarding costs attributed with

a particular production or job is considered under this system. The information so

extracted is used to provide detail about cost to a customer for the purpose of

reimbursement. It included three types of information viz. Direct material, labour and

overhead. These cost can not be avoided in job costing system and forms basis for

calculation.

Price-optimising system: Under this system, an organization predict or assess the

responses of customers to different prices for all the products it selling. Further, the best

branch of accounting.

to prepare financial statements and

accounts at the end of each financial

year in order to present to

shareholders.

Used for Internal management Primarily for existing and prospective

stakeholders.

Rules It does not have any specific rule for

preparation of reports.

The financial statements should be

prepared per the GAAP or IFRS.

Different types of management accounting systems and their essential requirements

Cost accounting system: This system is used to ascertain per unit cost of products in

order to have better control on profits, inventory and cost. It is used by manufacturers to

track cost that is being incurred at every stage of production of an item. Calculation of

raw materials, work in progress, and finished goods are done. Further, cost utilised in

input is compared with actual output for measuring financial performance. The essential

requirements are data to be used should be accurate, cost of installation and operating of

system should be included etc.

Inventory management system: This system is useful managing supply chain or

delivery of goods by tracking dispatch of products (Christ and Burritt, 2013). It involves

technology, processes and procedures for the whole process which begins with suppliers

and ends with delivery of final product to final consumer. The essential requirements are

forecasting of inventory, purchasing, shipping, order management, inventory control etc.

Job costing system: The process of gathering information regarding costs attributed with

a particular production or job is considered under this system. The information so

extracted is used to provide detail about cost to a customer for the purpose of

reimbursement. It included three types of information viz. Direct material, labour and

overhead. These cost can not be avoided in job costing system and forms basis for

calculation.

Price-optimising system: Under this system, an organization predict or assess the

responses of customers to different prices for all the products it selling. Further, the best

price is chosen which fits all the criteria such as objectives of the entity. Such information

can be obtained by conducting survey data, operating costs, inventories etc. The essential

requirements for this system are adopting a suitable optimization model, collection of

past data, monitoring results etc.

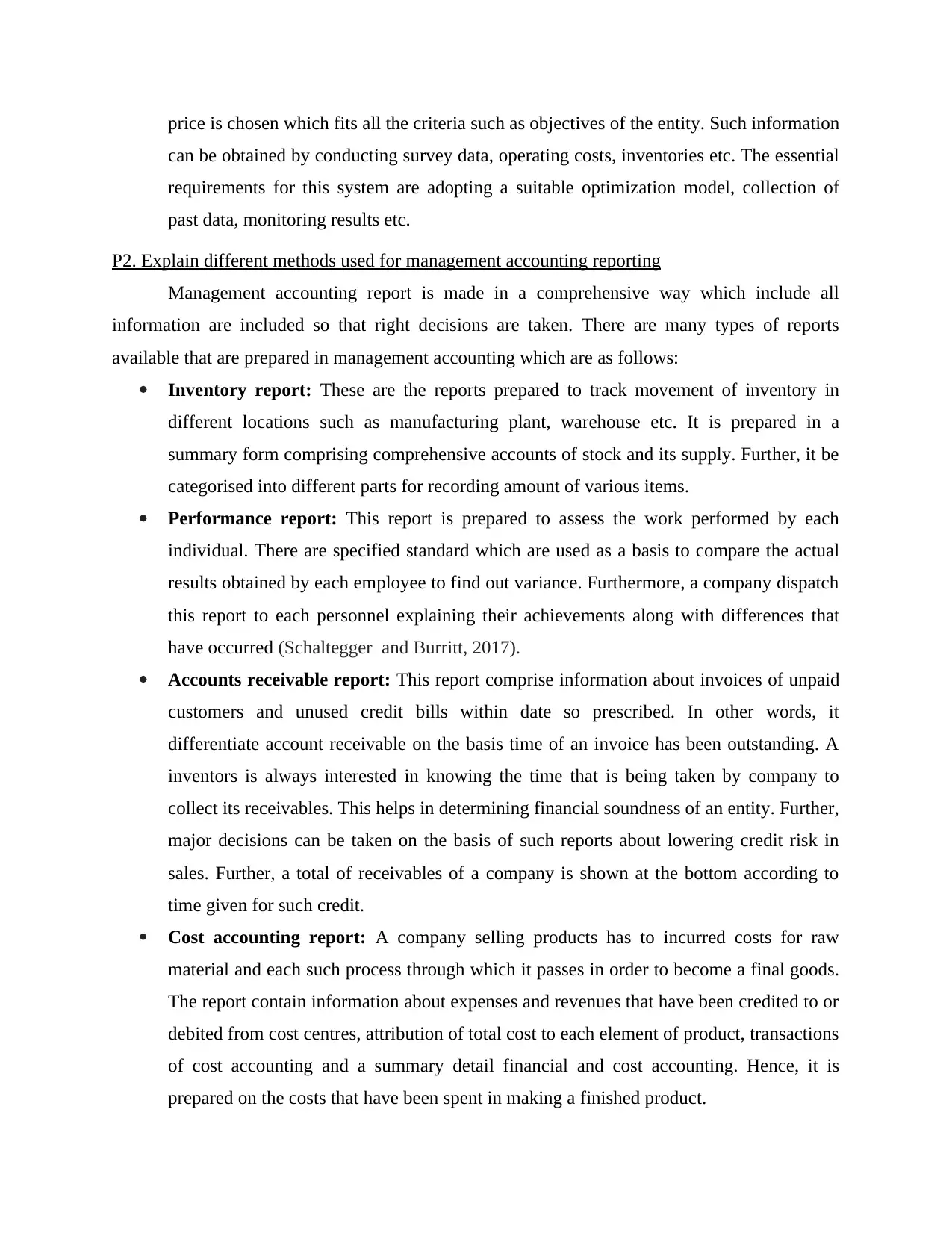

P2. Explain different methods used for management accounting reporting

Management accounting report is made in a comprehensive way which include all

information are included so that right decisions are taken. There are many types of reports

available that are prepared in management accounting which are as follows:

Inventory report: These are the reports prepared to track movement of inventory in

different locations such as manufacturing plant, warehouse etc. It is prepared in a

summary form comprising comprehensive accounts of stock and its supply. Further, it be

categorised into different parts for recording amount of various items.

Performance report: This report is prepared to assess the work performed by each

individual. There are specified standard which are used as a basis to compare the actual

results obtained by each employee to find out variance. Furthermore, a company dispatch

this report to each personnel explaining their achievements along with differences that

have occurred (Schaltegger and Burritt, 2017).

Accounts receivable report: This report comprise information about invoices of unpaid

customers and unused credit bills within date so prescribed. In other words, it

differentiate account receivable on the basis time of an invoice has been outstanding. A

inventors is always interested in knowing the time that is being taken by company to

collect its receivables. This helps in determining financial soundness of an entity. Further,

major decisions can be taken on the basis of such reports about lowering credit risk in

sales. Further, a total of receivables of a company is shown at the bottom according to

time given for such credit.

Cost accounting report: A company selling products has to incurred costs for raw

material and each such process through which it passes in order to become a final goods.

The report contain information about expenses and revenues that have been credited to or

debited from cost centres, attribution of total cost to each element of product, transactions

of cost accounting and a summary detail financial and cost accounting. Hence, it is

prepared on the costs that have been spent in making a finished product.

can be obtained by conducting survey data, operating costs, inventories etc. The essential

requirements for this system are adopting a suitable optimization model, collection of

past data, monitoring results etc.

P2. Explain different methods used for management accounting reporting

Management accounting report is made in a comprehensive way which include all

information are included so that right decisions are taken. There are many types of reports

available that are prepared in management accounting which are as follows:

Inventory report: These are the reports prepared to track movement of inventory in

different locations such as manufacturing plant, warehouse etc. It is prepared in a

summary form comprising comprehensive accounts of stock and its supply. Further, it be

categorised into different parts for recording amount of various items.

Performance report: This report is prepared to assess the work performed by each

individual. There are specified standard which are used as a basis to compare the actual

results obtained by each employee to find out variance. Furthermore, a company dispatch

this report to each personnel explaining their achievements along with differences that

have occurred (Schaltegger and Burritt, 2017).

Accounts receivable report: This report comprise information about invoices of unpaid

customers and unused credit bills within date so prescribed. In other words, it

differentiate account receivable on the basis time of an invoice has been outstanding. A

inventors is always interested in knowing the time that is being taken by company to

collect its receivables. This helps in determining financial soundness of an entity. Further,

major decisions can be taken on the basis of such reports about lowering credit risk in

sales. Further, a total of receivables of a company is shown at the bottom according to

time given for such credit.

Cost accounting report: A company selling products has to incurred costs for raw

material and each such process through which it passes in order to become a final goods.

The report contain information about expenses and revenues that have been credited to or

debited from cost centres, attribution of total cost to each element of product, transactions

of cost accounting and a summary detail financial and cost accounting. Hence, it is

prepared on the costs that have been spent in making a finished product.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash flow report: It is an important part of financial statement which is prepared to

show inflow and outflow of cash in business operations. It presents an overview of

financial activity in the company for a specified time period. These may be prepared on a

quarterly basis to have better control on management of costs. Further, it may include

balance sheets, income statement, statement of changes in equity, prime transactions of

company which may have significant impact etc.

TASK 2

P3. Calculate costs using appropriate techniques of cost analysis to prepare and income statement

using marginal and absorption costs

Cost is an amount refers to an amount expressed in monetary value that is spent by

company in order to manufacture a product. This is spent for creation of a goods or service.

Moreover, profits are not included while calculating costs.

Absorption costing: It is associated with involving the cost attributed to production of a

particular product. These include direct costs such as wages, raw material etc. which form the

basis for whole calculation. It is also called full costing whereby fixed overhead charges are

included as product cost (Anandarajan , Anandarajan and Srinivasan,Eds., 2012).

Marginal costing: Under this costing system, only variable costs are considered and

fixed costs are not at all taken into account for the calculation. Further, it involves additional

costs incurred for producing an extra unit of output which can be computed by total variable cost

assigned to one unit.

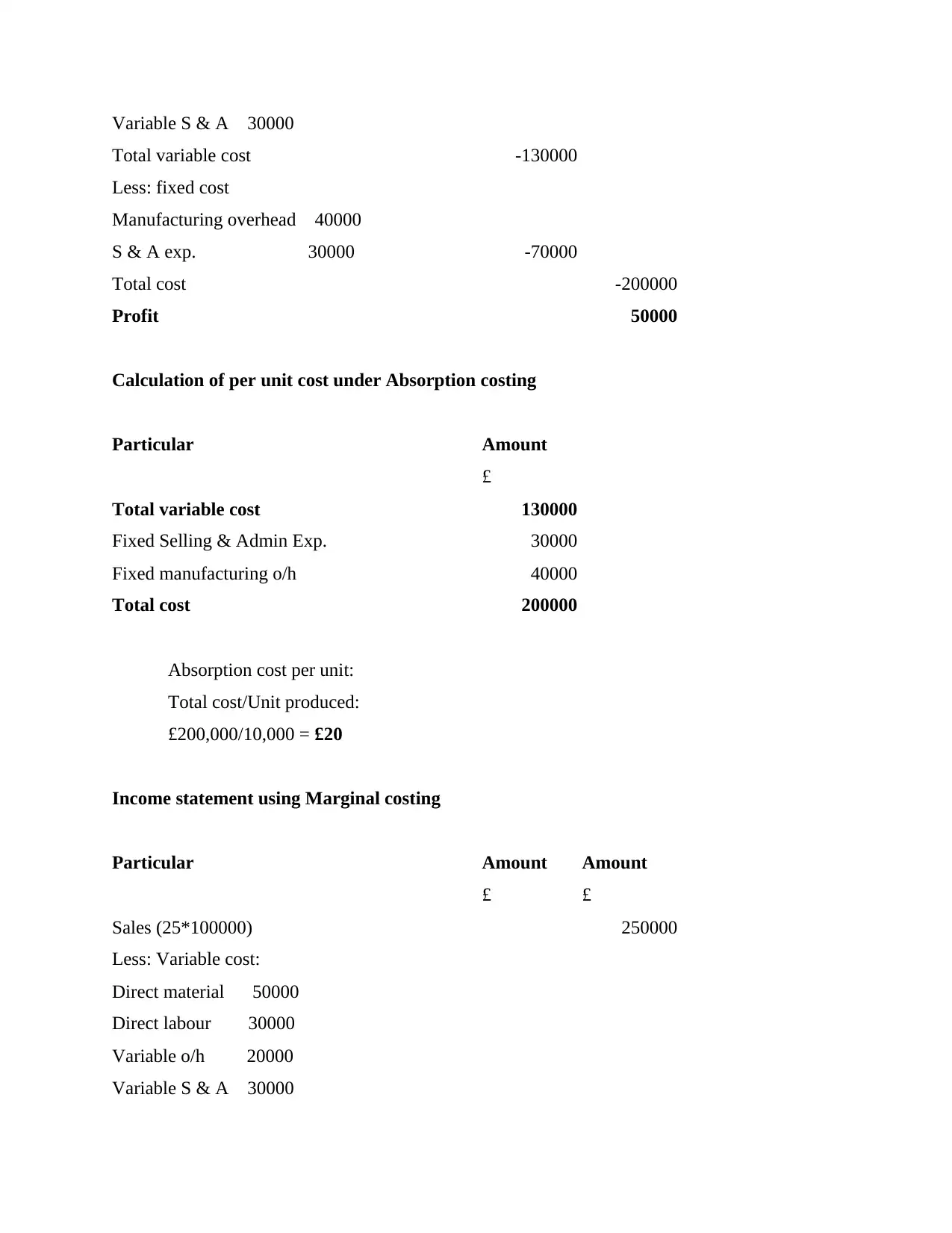

Income statement using Absorption costing

Particular Amount Amount

£ £

Sales (25*100000) 250000

Less: Variable cost:

Direct material 50000

Direct labour 30000

Variable o/h 20000

show inflow and outflow of cash in business operations. It presents an overview of

financial activity in the company for a specified time period. These may be prepared on a

quarterly basis to have better control on management of costs. Further, it may include

balance sheets, income statement, statement of changes in equity, prime transactions of

company which may have significant impact etc.

TASK 2

P3. Calculate costs using appropriate techniques of cost analysis to prepare and income statement

using marginal and absorption costs

Cost is an amount refers to an amount expressed in monetary value that is spent by

company in order to manufacture a product. This is spent for creation of a goods or service.

Moreover, profits are not included while calculating costs.

Absorption costing: It is associated with involving the cost attributed to production of a

particular product. These include direct costs such as wages, raw material etc. which form the

basis for whole calculation. It is also called full costing whereby fixed overhead charges are

included as product cost (Anandarajan , Anandarajan and Srinivasan,Eds., 2012).

Marginal costing: Under this costing system, only variable costs are considered and

fixed costs are not at all taken into account for the calculation. Further, it involves additional

costs incurred for producing an extra unit of output which can be computed by total variable cost

assigned to one unit.

Income statement using Absorption costing

Particular Amount Amount

£ £

Sales (25*100000) 250000

Less: Variable cost:

Direct material 50000

Direct labour 30000

Variable o/h 20000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Variable S & A 30000

Total variable cost -130000

Less: fixed cost

Manufacturing overhead 40000

S & A exp. 30000 -70000

Total cost -200000

Profit 50000

Calculation of per unit cost under Absorption costing

Particular Amount

£

Total variable cost 130000

Fixed Selling & Admin Exp. 30000

Fixed manufacturing o/h 40000

Total cost 200000

Absorption cost per unit:

Total cost/Unit produced:

£200,000/10,000 = £20

Income statement using Marginal costing

Particular Amount Amount

£ £

Sales (25*100000) 250000

Less: Variable cost:

Direct material 50000

Direct labour 30000

Variable o/h 20000

Variable S & A 30000

Total variable cost -130000

Less: fixed cost

Manufacturing overhead 40000

S & A exp. 30000 -70000

Total cost -200000

Profit 50000

Calculation of per unit cost under Absorption costing

Particular Amount

£

Total variable cost 130000

Fixed Selling & Admin Exp. 30000

Fixed manufacturing o/h 40000

Total cost 200000

Absorption cost per unit:

Total cost/Unit produced:

£200,000/10,000 = £20

Income statement using Marginal costing

Particular Amount Amount

£ £

Sales (25*100000) 250000

Less: Variable cost:

Direct material 50000

Direct labour 30000

Variable o/h 20000

Variable S & A 30000

Total variable cost -130000

Contribution 120000

Less: Fixed cost:

Manuf. O/h 40000

S & Admin Exp. 30000 -70000

Profit 50000

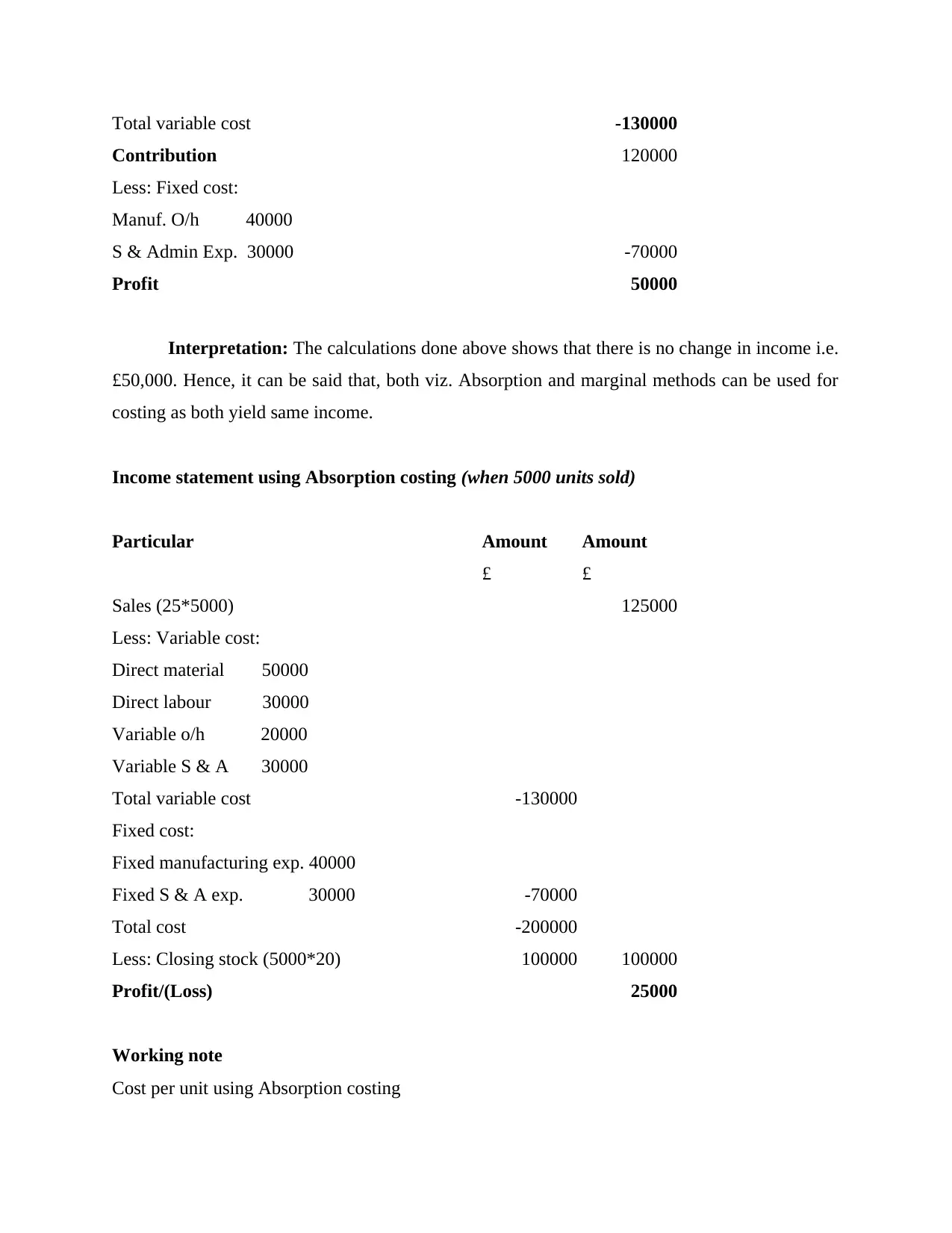

Interpretation: The calculations done above shows that there is no change in income i.e.

£50,000. Hence, it can be said that, both viz. Absorption and marginal methods can be used for

costing as both yield same income.

Income statement using Absorption costing (when 5000 units sold)

Particular Amount Amount

£ £

Sales (25*5000) 125000

Less: Variable cost:

Direct material 50000

Direct labour 30000

Variable o/h 20000

Variable S & A 30000

Total variable cost -130000

Fixed cost:

Fixed manufacturing exp. 40000

Fixed S & A exp. 30000 -70000

Total cost -200000

Less: Closing stock (5000*20) 100000 100000

Profit/(Loss) 25000

Working note

Cost per unit using Absorption costing

Contribution 120000

Less: Fixed cost:

Manuf. O/h 40000

S & Admin Exp. 30000 -70000

Profit 50000

Interpretation: The calculations done above shows that there is no change in income i.e.

£50,000. Hence, it can be said that, both viz. Absorption and marginal methods can be used for

costing as both yield same income.

Income statement using Absorption costing (when 5000 units sold)

Particular Amount Amount

£ £

Sales (25*5000) 125000

Less: Variable cost:

Direct material 50000

Direct labour 30000

Variable o/h 20000

Variable S & A 30000

Total variable cost -130000

Fixed cost:

Fixed manufacturing exp. 40000

Fixed S & A exp. 30000 -70000

Total cost -200000

Less: Closing stock (5000*20) 100000 100000

Profit/(Loss) 25000

Working note

Cost per unit using Absorption costing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

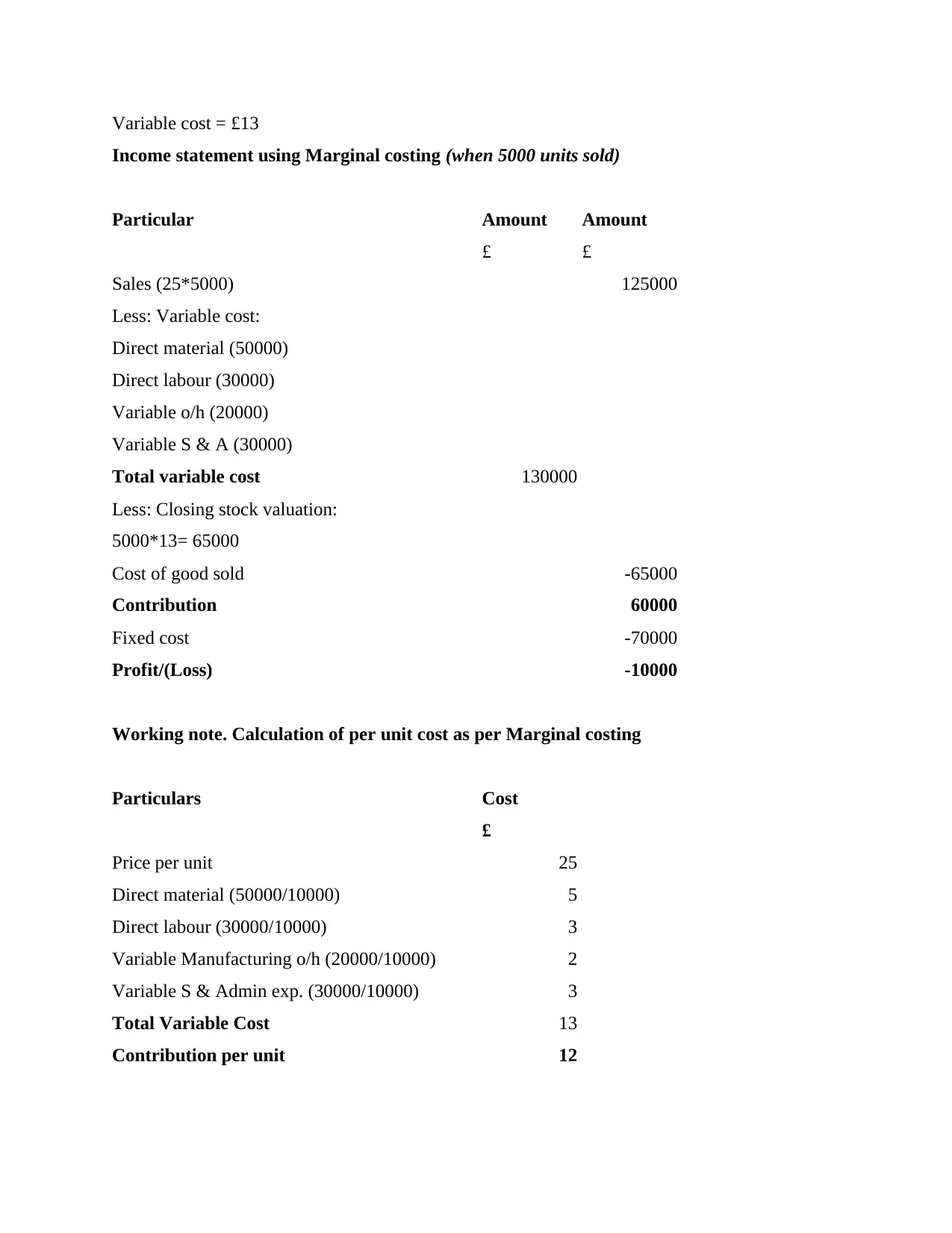

Variable cost = £13

Income statement using Marginal costing (when 5000 units sold)

Particular Amount Amount

£ £

Sales (25*5000) 125000

Less: Variable cost:

Direct material (50000)

Direct labour (30000)

Variable o/h (20000)

Variable S & A (30000)

Total variable cost 130000

Less: Closing stock valuation:

5000*13= 65000

Cost of good sold -65000

Contribution 60000

Fixed cost -70000

Profit/(Loss) -10000

Working note. Calculation of per unit cost as per Marginal costing

Particulars Cost

£

Price per unit 25

Direct material (50000/10000) 5

Direct labour (30000/10000) 3

Variable Manufacturing o/h (20000/10000) 2

Variable S & Admin exp. (30000/10000) 3

Total Variable Cost 13

Contribution per unit 12

Income statement using Marginal costing (when 5000 units sold)

Particular Amount Amount

£ £

Sales (25*5000) 125000

Less: Variable cost:

Direct material (50000)

Direct labour (30000)

Variable o/h (20000)

Variable S & A (30000)

Total variable cost 130000

Less: Closing stock valuation:

5000*13= 65000

Cost of good sold -65000

Contribution 60000

Fixed cost -70000

Profit/(Loss) -10000

Working note. Calculation of per unit cost as per Marginal costing

Particulars Cost

£

Price per unit 25

Direct material (50000/10000) 5

Direct labour (30000/10000) 3

Variable Manufacturing o/h (20000/10000) 2

Variable S & Admin exp. (30000/10000) 3

Total Variable Cost 13

Contribution per unit 12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation: These two methods give different net amount when used for calculating

cost when 5000 units are sold. The absorption costing give a profit of £25000, whereas under

marginal costing a loss of £10,000 has been incurred. Hence, the company should use former

method to get profits.

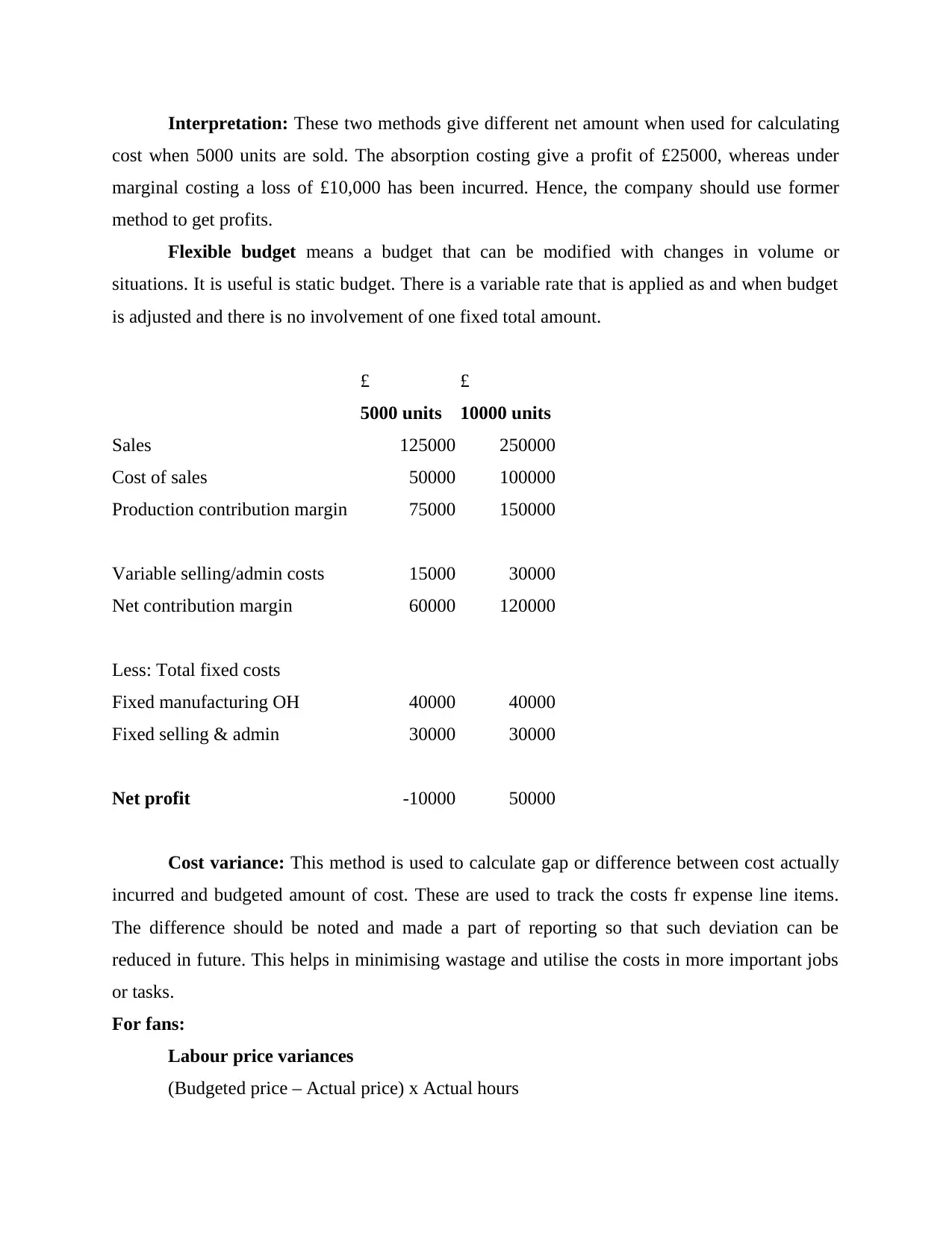

Flexible budget means a budget that can be modified with changes in volume or

situations. It is useful is static budget. There is a variable rate that is applied as and when budget

is adjusted and there is no involvement of one fixed total amount.

£ £

5000 units 10000 units

Sales 125000 250000

Cost of sales 50000 100000

Production contribution margin 75000 150000

Variable selling/admin costs 15000 30000

Net contribution margin 60000 120000

Less: Total fixed costs

Fixed manufacturing OH 40000 40000

Fixed selling & admin 30000 30000

Net profit -10000 50000

Cost variance: This method is used to calculate gap or difference between cost actually

incurred and budgeted amount of cost. These are used to track the costs fr expense line items.

The difference should be noted and made a part of reporting so that such deviation can be

reduced in future. This helps in minimising wastage and utilise the costs in more important jobs

or tasks.

For fans:

Labour price variances

(Budgeted price – Actual price) x Actual hours

cost when 5000 units are sold. The absorption costing give a profit of £25000, whereas under

marginal costing a loss of £10,000 has been incurred. Hence, the company should use former

method to get profits.

Flexible budget means a budget that can be modified with changes in volume or

situations. It is useful is static budget. There is a variable rate that is applied as and when budget

is adjusted and there is no involvement of one fixed total amount.

£ £

5000 units 10000 units

Sales 125000 250000

Cost of sales 50000 100000

Production contribution margin 75000 150000

Variable selling/admin costs 15000 30000

Net contribution margin 60000 120000

Less: Total fixed costs

Fixed manufacturing OH 40000 40000

Fixed selling & admin 30000 30000

Net profit -10000 50000

Cost variance: This method is used to calculate gap or difference between cost actually

incurred and budgeted amount of cost. These are used to track the costs fr expense line items.

The difference should be noted and made a part of reporting so that such deviation can be

reduced in future. This helps in minimising wastage and utilise the costs in more important jobs

or tasks.

For fans:

Labour price variances

(Budgeted price – Actual price) x Actual hours

(5 – 5.20) x 3400

= -680 Unfavourable

Labour usage variance

(Budgeted Hours – Actual Hours) x Budgeted Price

(3000-3400) x 5

= -2000 Unfavourable

For packaging boxes:

Material Price Variances

(Budgeted price – Actual price) x Actual usage

(10 – 9.5) x 2200

= 1100 Favourable

Material usage variance

(Budgeted Use – Actual Use) x Budgeted Price

(2000 – 2200) x 10

= -2000 Unfavourable

Actual costing system: It is a process of recording product cost which is based on

various factors such as actual cost of materials, actual cost of labour, and actual overhead costs.

Along with this, the main concept of actual costing system is they used only actual cost and

allocate base experienced.

Normal costing system: In this system includes all those cost which helps in making a

product such as material cost, actual direct cost and manufacturing overhead. The key point of

normal costing system is to find the overall cost of particular product which use in making up the

product.

Standard costing system: It is a tool which use in preparing budget, managing and

controlling cost, and also to evaluate it for measuring performance. Along with this, standard

costing system main motive is to evaluate the different cost such as standard and actual for

maintaining the productivity of their organisation.

Job costing: This costing helps in determining the manufacturing costs by categorised it

in three parts such as overhead, direct material and direct labor cost for estimating its actual

value. Also it is a process of keeping an account in the form of direct cost and indirect cost.

= -680 Unfavourable

Labour usage variance

(Budgeted Hours – Actual Hours) x Budgeted Price

(3000-3400) x 5

= -2000 Unfavourable

For packaging boxes:

Material Price Variances

(Budgeted price – Actual price) x Actual usage

(10 – 9.5) x 2200

= 1100 Favourable

Material usage variance

(Budgeted Use – Actual Use) x Budgeted Price

(2000 – 2200) x 10

= -2000 Unfavourable

Actual costing system: It is a process of recording product cost which is based on

various factors such as actual cost of materials, actual cost of labour, and actual overhead costs.

Along with this, the main concept of actual costing system is they used only actual cost and

allocate base experienced.

Normal costing system: In this system includes all those cost which helps in making a

product such as material cost, actual direct cost and manufacturing overhead. The key point of

normal costing system is to find the overall cost of particular product which use in making up the

product.

Standard costing system: It is a tool which use in preparing budget, managing and

controlling cost, and also to evaluate it for measuring performance. Along with this, standard

costing system main motive is to evaluate the different cost such as standard and actual for

maintaining the productivity of their organisation.

Job costing: This costing helps in determining the manufacturing costs by categorised it

in three parts such as overhead, direct material and direct labor cost for estimating its actual

value. Also it is a process of keeping an account in the form of direct cost and indirect cost.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.