Comprehensive Report: Management Accounting Systems and Techniques

VerifiedAdded on 2023/01/13

|13

|3947

|54

Report

AI Summary

This report provides a detailed overview of management accounting systems and techniques. It begins by defining management accounting and its role within a company, particularly focusing on the functions of a management accountant at KEF Ltd, a loudspeaker manufacturing company. The report explores different types of cost reports, including job costing, batch costing, inventory costing, and activity-based costing, explaining their applications and importance. It also contrasts financial and management accounting, highlighting their differences and areas of overlap, such as budgeting and costing. Furthermore, the report discusses the benefits of implementing a robust management accounting system and its integration with reporting processes. Finally, the report includes relevant calculations and analyses to identify the income statement of the organization.

MANAGEMENT

ACCOUNTING SYSTEMS

AND TECHNIQUES

ACCOUNTING SYSTEMS

AND TECHNIQUES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS.................................................................................................................2

INTRODUCTION...........................................................................................................................3

P 1 Management accounting and system of management accounting...................................3

P 2 Different types of cost reports..........................................................................................6

M 1 Benefits of management accounting system...................................................................8

D 1 Integration of management accounting and reporting.....................................................8

P 3 calculations.......................................................................................................................9

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

TABLE OF CONTENTS.................................................................................................................2

INTRODUCTION...........................................................................................................................3

P 1 Management accounting and system of management accounting...................................3

P 2 Different types of cost reports..........................................................................................6

M 1 Benefits of management accounting system...................................................................8

D 1 Integration of management accounting and reporting.....................................................8

P 3 calculations.......................................................................................................................9

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is that branch of accounting which is helpful in discussing and

deciding and taking decision relating to the management of company. This decision is taken by

keeping all financial facts and information as base. The present report is based on company KEF

Ltd which is loud speaker manufacturing company with international distributor.

This report will carry the matter relating to examining the meaning of the management

accounting and also its different types of managing the accounting systems. It also includes

various methods which is used for managing the accounting reporting. Further it includes the

calculation by using the appropriate techniques of costing to identify the income statement of the

organization.

P 1 Management accounting and system of management accounting

The management accounting is a system that involves analysis of financial information

and statistics in order to take decision relating to the management of company (Alsharari and

Youssef, 2017). The person taking all decision relating to the management of the company by

analysing the financial information is termed as management accountant. The management

accountant plays a crucial role in success of the company which is discussed in the following

points- Long term and short- term planning- This is the most crucial role of the management

accountant of KEF Ltd because the major role is to forecast and set the plan for working.

At this role the management accountant establishes different goals and objectives for

working. Maintaining optimum cost structure- This is another role of management accountant of

KEF Ltd wherein they have to raise the funds and manage its application to different

areas. The accountant has to balance and maintain a mix of both debt and equity so that

the cost structure is maintained in optimum manner. Decision making- This is another important role of management accountant of KEF Ltd

wherein they have to take decision for the betterment of KEF Ltd (Ismail, Isa and Mia,

2018). They have to take decision like where to take money from, capital budgeting

decision, investing and many other decisions. Control- This is yet another crucial role which the accountant of the KEF Ltd has to

perform. This is the most important role because without any control nothing can be

Management accounting is that branch of accounting which is helpful in discussing and

deciding and taking decision relating to the management of company. This decision is taken by

keeping all financial facts and information as base. The present report is based on company KEF

Ltd which is loud speaker manufacturing company with international distributor.

This report will carry the matter relating to examining the meaning of the management

accounting and also its different types of managing the accounting systems. It also includes

various methods which is used for managing the accounting reporting. Further it includes the

calculation by using the appropriate techniques of costing to identify the income statement of the

organization.

P 1 Management accounting and system of management accounting

The management accounting is a system that involves analysis of financial information

and statistics in order to take decision relating to the management of company (Alsharari and

Youssef, 2017). The person taking all decision relating to the management of the company by

analysing the financial information is termed as management accountant. The management

accountant plays a crucial role in success of the company which is discussed in the following

points- Long term and short- term planning- This is the most crucial role of the management

accountant of KEF Ltd because the major role is to forecast and set the plan for working.

At this role the management accountant establishes different goals and objectives for

working. Maintaining optimum cost structure- This is another role of management accountant of

KEF Ltd wherein they have to raise the funds and manage its application to different

areas. The accountant has to balance and maintain a mix of both debt and equity so that

the cost structure is maintained in optimum manner. Decision making- This is another important role of management accountant of KEF Ltd

wherein they have to take decision for the betterment of KEF Ltd (Ismail, Isa and Mia,

2018). They have to take decision like where to take money from, capital budgeting

decision, investing and many other decisions. Control- This is yet another crucial role which the accountant of the KEF Ltd has to

perform. This is the most important role because without any control nothing can be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

managed in effective manner hence, they need to properly control all activities. Here the

accountant has to properly control the cost and other variables in order to manage the

overall organization in smooth and effective manner. Participation in management process- This is one of the major roles which the

accountant plays within KEF Ltd. Under this accountant performs the staff function that

is controlling the employees and along with this also has authority over the employees

and their management. Here the role of the accountant is to help the executives in

controlling the information and then helping them in using the information and preparing

the reports in clear manner. Advising- This is another role of management accountant which it plays in the control of

KEF Ltd (Järvinen, 2016). Here the accountant after the analysis of all the information

and facts and figures advices the management and board for improvement. These advices

can be used as these have been made after thorough analysis of the information and is

helpful in improving their profitability.

Role of management accounting within each function of business

The scope of the role of management accounting is very wide and cover all the aspect

which are necessary for the taking of decision by keeping in mind the financial information. This

scope includes the fulfilment of the objective of the company as all the decision under

management accounting are taken for the attainment of the objective.

The major functions of the KEF Ltd include planning, organizing, leading and

controlling. Without these functions the business cannot run in proper and effective manner.

Thus, it is very important for the company to apply all the business functions in proper manner.

In the same way, management accounting is also applied in the business for its effective working

and this also performs all the business functions for attaining success. The role of management

accounting within every business function of KEF Ltd is discussed in the following points- Planning- This is the first business function which is performed by KEF Ltd where the

company plans what to do. In this stage the management accounting of KEF Ltd is

responsible for the planning of different short- term and long- term plans for the effective

working of the company. Here the management accounting’s function is to plan all the

financial activities in form of budget so that very employee knows what and how they

have to use the resources and money.

accountant has to properly control the cost and other variables in order to manage the

overall organization in smooth and effective manner. Participation in management process- This is one of the major roles which the

accountant plays within KEF Ltd. Under this accountant performs the staff function that

is controlling the employees and along with this also has authority over the employees

and their management. Here the role of the accountant is to help the executives in

controlling the information and then helping them in using the information and preparing

the reports in clear manner. Advising- This is another role of management accountant which it plays in the control of

KEF Ltd (Järvinen, 2016). Here the accountant after the analysis of all the information

and facts and figures advices the management and board for improvement. These advices

can be used as these have been made after thorough analysis of the information and is

helpful in improving their profitability.

Role of management accounting within each function of business

The scope of the role of management accounting is very wide and cover all the aspect

which are necessary for the taking of decision by keeping in mind the financial information. This

scope includes the fulfilment of the objective of the company as all the decision under

management accounting are taken for the attainment of the objective.

The major functions of the KEF Ltd include planning, organizing, leading and

controlling. Without these functions the business cannot run in proper and effective manner.

Thus, it is very important for the company to apply all the business functions in proper manner.

In the same way, management accounting is also applied in the business for its effective working

and this also performs all the business functions for attaining success. The role of management

accounting within every business function of KEF Ltd is discussed in the following points- Planning- This is the first business function which is performed by KEF Ltd where the

company plans what to do. In this stage the management accounting of KEF Ltd is

responsible for the planning of different short- term and long- term plans for the effective

working of the company. Here the management accounting’s function is to plan all the

financial activities in form of budget so that very employee knows what and how they

have to use the resources and money.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Organizing- This is the function of KEF Ltd where the company arranges for the

resources which are required to work for accomplishing the planned activities. Thus, the

management accounting also plays an important role within this business function of

KEF Ltd. The management accounting here helps the managers of KEF Ltd in providing

necessary information from different system such as cost accounting, inventory

management and others which are essential for the procurement of which types of

resources so that the work can be successfully accomplished (Jermias, 2017). Here these

systems will help the company in organizing for the resources as their will be list of the

things needed to perform any activity. Thus, management accountant of KEF Ltd will

assist in analysing the resources which are required to carry on the production. Controlling- This is the function of KEF Ltd wherein the monitoring of the activities take

place and if their activity is not matched with the standard performance then some

corrective measures are taken place. Thus, these help the management of KEF Ltd in

controlling all the activities in the direction of the success. There are many different types

of report prepared under management accounting which help company in controlling like,

inventory reports, cost report, budgets and may others. Like for instance, the cost report

will outline the cost of the product and also the past record of the cost will be there in the

report. Thus, this will help the company in controlling the cost as compared to the last

year. Leading- This is a business function where KEF Ltd tries to lead the company in way of

profit earning and the attainment of the business objectives. Here the management

accounting also plays a crucial role in leading the business activities as here it plays the

role of forming aims and objective through which the management leads the company in

that direction. The management accounting plays a role in forming aims and objectives

because they analyse all the information and they know in which direction they have to

develop the aims and objectives so that business grows.

Difference in financial and management accountant

The financial and management accountant are both part of accounting system but are

different from one another.

Management accountant Financial accountant

The work done by the management accountant The work done by the financial accountant is

resources which are required to work for accomplishing the planned activities. Thus, the

management accounting also plays an important role within this business function of

KEF Ltd. The management accounting here helps the managers of KEF Ltd in providing

necessary information from different system such as cost accounting, inventory

management and others which are essential for the procurement of which types of

resources so that the work can be successfully accomplished (Jermias, 2017). Here these

systems will help the company in organizing for the resources as their will be list of the

things needed to perform any activity. Thus, management accountant of KEF Ltd will

assist in analysing the resources which are required to carry on the production. Controlling- This is the function of KEF Ltd wherein the monitoring of the activities take

place and if their activity is not matched with the standard performance then some

corrective measures are taken place. Thus, these help the management of KEF Ltd in

controlling all the activities in the direction of the success. There are many different types

of report prepared under management accounting which help company in controlling like,

inventory reports, cost report, budgets and may others. Like for instance, the cost report

will outline the cost of the product and also the past record of the cost will be there in the

report. Thus, this will help the company in controlling the cost as compared to the last

year. Leading- This is a business function where KEF Ltd tries to lead the company in way of

profit earning and the attainment of the business objectives. Here the management

accounting also plays a crucial role in leading the business activities as here it plays the

role of forming aims and objective through which the management leads the company in

that direction. The management accounting plays a role in forming aims and objectives

because they analyse all the information and they know in which direction they have to

develop the aims and objectives so that business grows.

Difference in financial and management accountant

The financial and management accountant are both part of accounting system but are

different from one another.

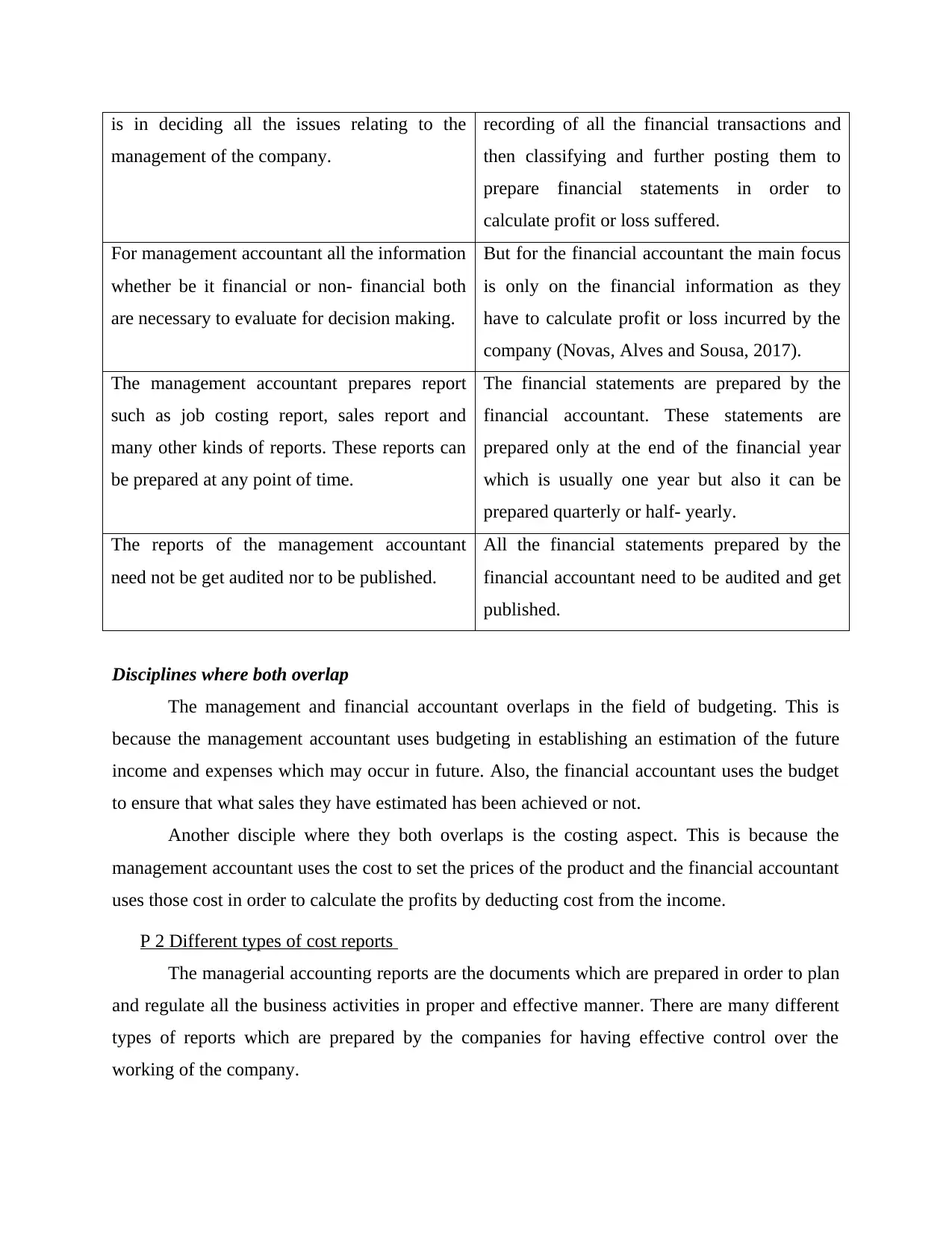

Management accountant Financial accountant

The work done by the management accountant The work done by the financial accountant is

is in deciding all the issues relating to the

management of the company.

recording of all the financial transactions and

then classifying and further posting them to

prepare financial statements in order to

calculate profit or loss suffered.

For management accountant all the information

whether be it financial or non- financial both

are necessary to evaluate for decision making.

But for the financial accountant the main focus

is only on the financial information as they

have to calculate profit or loss incurred by the

company (Novas, Alves and Sousa, 2017).

The management accountant prepares report

such as job costing report, sales report and

many other kinds of reports. These reports can

be prepared at any point of time.

The financial statements are prepared by the

financial accountant. These statements are

prepared only at the end of the financial year

which is usually one year but also it can be

prepared quarterly or half- yearly.

The reports of the management accountant

need not be get audited nor to be published.

All the financial statements prepared by the

financial accountant need to be audited and get

published.

Disciplines where both overlap

The management and financial accountant overlaps in the field of budgeting. This is

because the management accountant uses budgeting in establishing an estimation of the future

income and expenses which may occur in future. Also, the financial accountant uses the budget

to ensure that what sales they have estimated has been achieved or not.

Another disciple where they both overlaps is the costing aspect. This is because the

management accountant uses the cost to set the prices of the product and the financial accountant

uses those cost in order to calculate the profits by deducting cost from the income.

P 2 Different types of cost reports

The managerial accounting reports are the documents which are prepared in order to plan

and regulate all the business activities in proper and effective manner. There are many different

types of reports which are prepared by the companies for having effective control over the

working of the company.

management of the company.

recording of all the financial transactions and

then classifying and further posting them to

prepare financial statements in order to

calculate profit or loss suffered.

For management accountant all the information

whether be it financial or non- financial both

are necessary to evaluate for decision making.

But for the financial accountant the main focus

is only on the financial information as they

have to calculate profit or loss incurred by the

company (Novas, Alves and Sousa, 2017).

The management accountant prepares report

such as job costing report, sales report and

many other kinds of reports. These reports can

be prepared at any point of time.

The financial statements are prepared by the

financial accountant. These statements are

prepared only at the end of the financial year

which is usually one year but also it can be

prepared quarterly or half- yearly.

The reports of the management accountant

need not be get audited nor to be published.

All the financial statements prepared by the

financial accountant need to be audited and get

published.

Disciplines where both overlap

The management and financial accountant overlaps in the field of budgeting. This is

because the management accountant uses budgeting in establishing an estimation of the future

income and expenses which may occur in future. Also, the financial accountant uses the budget

to ensure that what sales they have estimated has been achieved or not.

Another disciple where they both overlaps is the costing aspect. This is because the

management accountant uses the cost to set the prices of the product and the financial accountant

uses those cost in order to calculate the profits by deducting cost from the income.

P 2 Different types of cost reports

The managerial accounting reports are the documents which are prepared in order to plan

and regulate all the business activities in proper and effective manner. There are many different

types of reports which are prepared by the companies for having effective control over the

working of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

All these costing methods are different form one another because they all deals in

different aspect like discussed below-

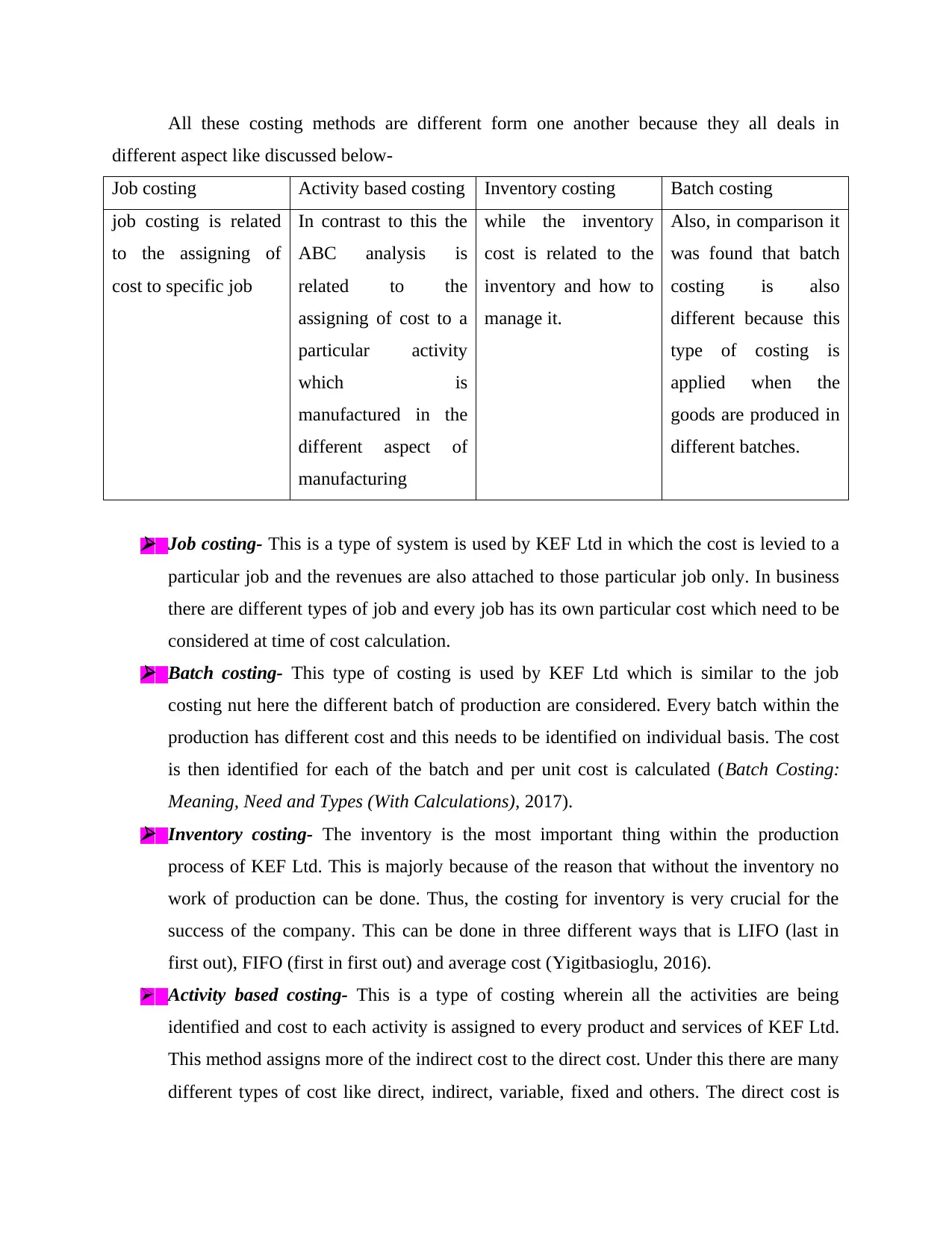

Job costing Activity based costing Inventory costing Batch costing

job costing is related

to the assigning of

cost to specific job

In contrast to this the

ABC analysis is

related to the

assigning of cost to a

particular activity

which is

manufactured in the

different aspect of

manufacturing

while the inventory

cost is related to the

inventory and how to

manage it.

Also, in comparison it

was found that batch

costing is also

different because this

type of costing is

applied when the

goods are produced in

different batches.

Job costing- This is a type of system is used by KEF Ltd in which the cost is levied to a

particular job and the revenues are also attached to those particular job only. In business

there are different types of job and every job has its own particular cost which need to be

considered at time of cost calculation. Batch costing- This type of costing is used by KEF Ltd which is similar to the job

costing nut here the different batch of production are considered. Every batch within the

production has different cost and this needs to be identified on individual basis. The cost

is then identified for each of the batch and per unit cost is calculated (Batch Costing:

Meaning, Need and Types (With Calculations), 2017). Inventory costing- The inventory is the most important thing within the production

process of KEF Ltd. This is majorly because of the reason that without the inventory no

work of production can be done. Thus, the costing for inventory is very crucial for the

success of the company. This can be done in three different ways that is LIFO (last in

first out), FIFO (first in first out) and average cost (Yigitbasioglu, 2016).

Activity based costing- This is a type of costing wherein all the activities are being

identified and cost to each activity is assigned to every product and services of KEF Ltd.

This method assigns more of the indirect cost to the direct cost. Under this there are many

different types of cost like direct, indirect, variable, fixed and others. The direct cost is

different aspect like discussed below-

Job costing Activity based costing Inventory costing Batch costing

job costing is related

to the assigning of

cost to specific job

In contrast to this the

ABC analysis is

related to the

assigning of cost to a

particular activity

which is

manufactured in the

different aspect of

manufacturing

while the inventory

cost is related to the

inventory and how to

manage it.

Also, in comparison it

was found that batch

costing is also

different because this

type of costing is

applied when the

goods are produced in

different batches.

Job costing- This is a type of system is used by KEF Ltd in which the cost is levied to a

particular job and the revenues are also attached to those particular job only. In business

there are different types of job and every job has its own particular cost which need to be

considered at time of cost calculation. Batch costing- This type of costing is used by KEF Ltd which is similar to the job

costing nut here the different batch of production are considered. Every batch within the

production has different cost and this needs to be identified on individual basis. The cost

is then identified for each of the batch and per unit cost is calculated (Batch Costing:

Meaning, Need and Types (With Calculations), 2017). Inventory costing- The inventory is the most important thing within the production

process of KEF Ltd. This is majorly because of the reason that without the inventory no

work of production can be done. Thus, the costing for inventory is very crucial for the

success of the company. This can be done in three different ways that is LIFO (last in

first out), FIFO (first in first out) and average cost (Yigitbasioglu, 2016).

Activity based costing- This is a type of costing wherein all the activities are being

identified and cost to each activity is assigned to every product and services of KEF Ltd.

This method assigns more of the indirect cost to the direct cost. Under this there are many

different types of cost like direct, indirect, variable, fixed and others. The direct cost is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the one which is directly attached to the production like direct labour, material and many

other. Indirect cost is the one which is not directly applied to the production process like

administration cost, rent and others (Otley, 2016). On the other hand, fixed cost is the one

which is fixed at every level of production and the variable cost is the one which varies

with the quantity of production.

M 1 Benefits of management accounting system

Job costing- The major benefit of this costing for KEF Ltd is that this help the company in

having better control over the cost. This is majorly because of the reason that this provides an

idea of the cost as every job is having a particular cost so it is easier for the manager to assign

the cost. The job costing adds the value to the company because this help in properly

allocating the cost to individual job. This help the company in achievement of organizational

objective as all the jobs are being able to optimise the cost and this increases the profitability

of the company.

Batch costing- The major benefit of using this costing method for KEF Ltd is that here the

supervision is easier as the manager has to supervise all the identical cost and if there is some

flaw in one batch then it will be identical with another. The batch costing adds value to the

KEF ltd because of the reason that this help the company in differentiating the different

batches and assigning specific cost to them. This help in attaining the organizational

objective because this cut the cost of the batch which is not operating.

Inventory costing- The major benefit for KEF Ltd in using this costing system is that this

system helps in getting more information relating to the managerial planning and decision

making. This is because this help in deciding which inventory to use at what time. The cost

of stock can be reduced by avoiding the minimum order quantity and by reordering at that

point of time when the inventory has reached to zero. This method add value to the company

as the inventory is ordered only when there is requirement. Thus, this help in attaining the

organizational objective as cost of holding the stock will be reduced.

Activity based costing- The major benefit of using this method for KEF Ltd is that this help

in analysing accurate product cost as this method brings in accuracy at time of accessing the

cost in better terms. This adds values to KEF Ltd because it helps in identifying the type of

cost to be levied. Thus, this will help in achievement of organizational objective of

profitability as here the cost will be levied in proper manner and this will increase the profits.

other. Indirect cost is the one which is not directly applied to the production process like

administration cost, rent and others (Otley, 2016). On the other hand, fixed cost is the one

which is fixed at every level of production and the variable cost is the one which varies

with the quantity of production.

M 1 Benefits of management accounting system

Job costing- The major benefit of this costing for KEF Ltd is that this help the company in

having better control over the cost. This is majorly because of the reason that this provides an

idea of the cost as every job is having a particular cost so it is easier for the manager to assign

the cost. The job costing adds the value to the company because this help in properly

allocating the cost to individual job. This help the company in achievement of organizational

objective as all the jobs are being able to optimise the cost and this increases the profitability

of the company.

Batch costing- The major benefit of using this costing method for KEF Ltd is that here the

supervision is easier as the manager has to supervise all the identical cost and if there is some

flaw in one batch then it will be identical with another. The batch costing adds value to the

KEF ltd because of the reason that this help the company in differentiating the different

batches and assigning specific cost to them. This help in attaining the organizational

objective because this cut the cost of the batch which is not operating.

Inventory costing- The major benefit for KEF Ltd in using this costing system is that this

system helps in getting more information relating to the managerial planning and decision

making. This is because this help in deciding which inventory to use at what time. The cost

of stock can be reduced by avoiding the minimum order quantity and by reordering at that

point of time when the inventory has reached to zero. This method add value to the company

as the inventory is ordered only when there is requirement. Thus, this help in attaining the

organizational objective as cost of holding the stock will be reduced.

Activity based costing- The major benefit of using this method for KEF Ltd is that this help

in analysing accurate product cost as this method brings in accuracy at time of accessing the

cost in better terms. This adds values to KEF Ltd because it helps in identifying the type of

cost to be levied. Thus, this will help in achievement of organizational objective of

profitability as here the cost will be levied in proper manner and this will increase the profits.

D 1 Integration of management accounting and reporting

The management accounting and management accounting reporting are integrated with

one another because with this integration the reports will assist the management in taking good

decision. Thus, this integration will help the company in assisting management of the company

in taking decision.

P 3 calculations

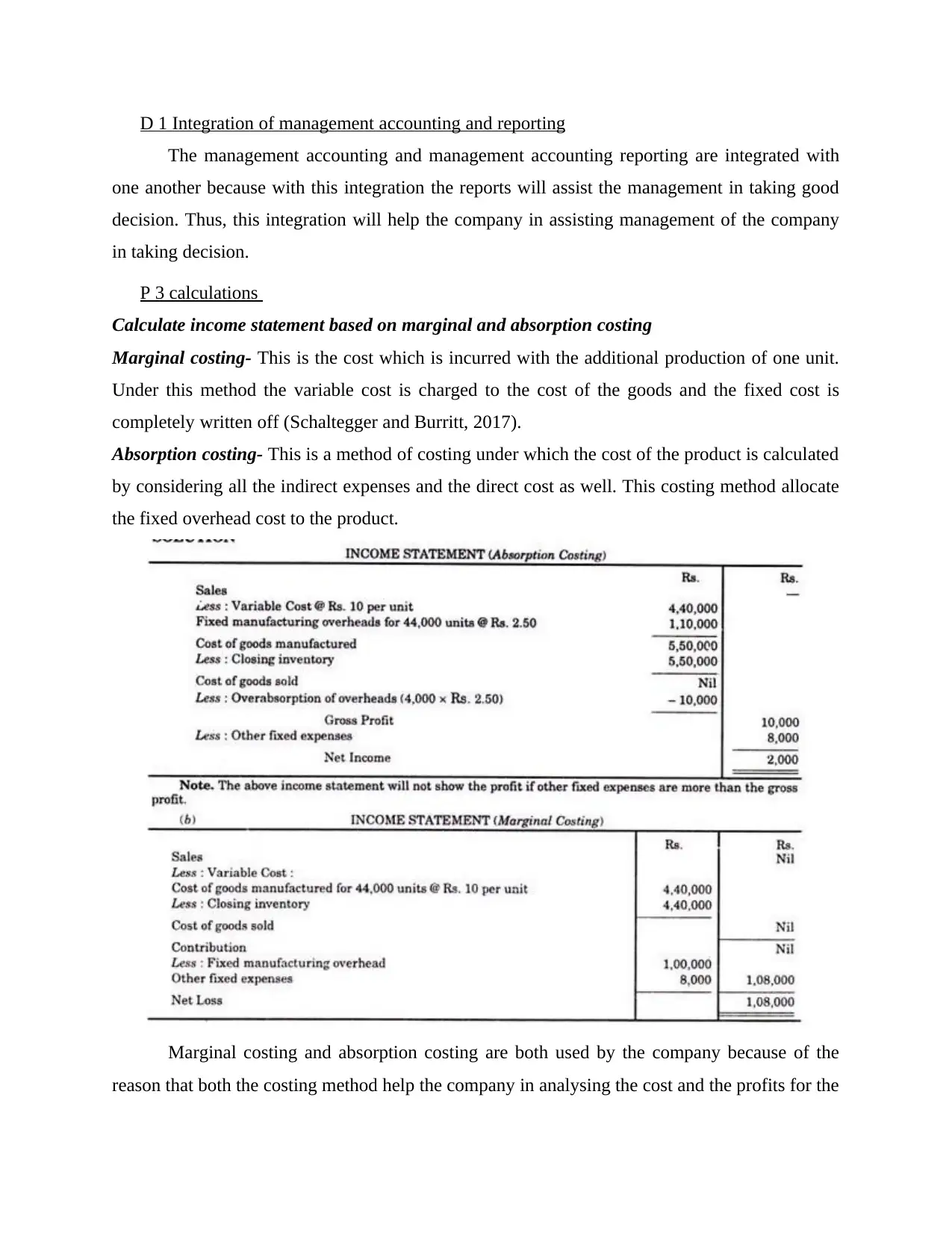

Calculate income statement based on marginal and absorption costing

Marginal costing- This is the cost which is incurred with the additional production of one unit.

Under this method the variable cost is charged to the cost of the goods and the fixed cost is

completely written off (Schaltegger and Burritt, 2017).

Absorption costing- This is a method of costing under which the cost of the product is calculated

by considering all the indirect expenses and the direct cost as well. This costing method allocate

the fixed overhead cost to the product.

Marginal costing and absorption costing are both used by the company because of the

reason that both the costing method help the company in analysing the cost and the profits for the

The management accounting and management accounting reporting are integrated with

one another because with this integration the reports will assist the management in taking good

decision. Thus, this integration will help the company in assisting management of the company

in taking decision.

P 3 calculations

Calculate income statement based on marginal and absorption costing

Marginal costing- This is the cost which is incurred with the additional production of one unit.

Under this method the variable cost is charged to the cost of the goods and the fixed cost is

completely written off (Schaltegger and Burritt, 2017).

Absorption costing- This is a method of costing under which the cost of the product is calculated

by considering all the indirect expenses and the direct cost as well. This costing method allocate

the fixed overhead cost to the product.

Marginal costing and absorption costing are both used by the company because of the

reason that both the costing method help the company in analysing the cost and the profits for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company. But the absorption costing is preferred over the marginal costing because of the fact

that this costing applies to all the production cost. Whereas the marginal costing is the method

wherein the fixed cost is not considered and is completely written off.

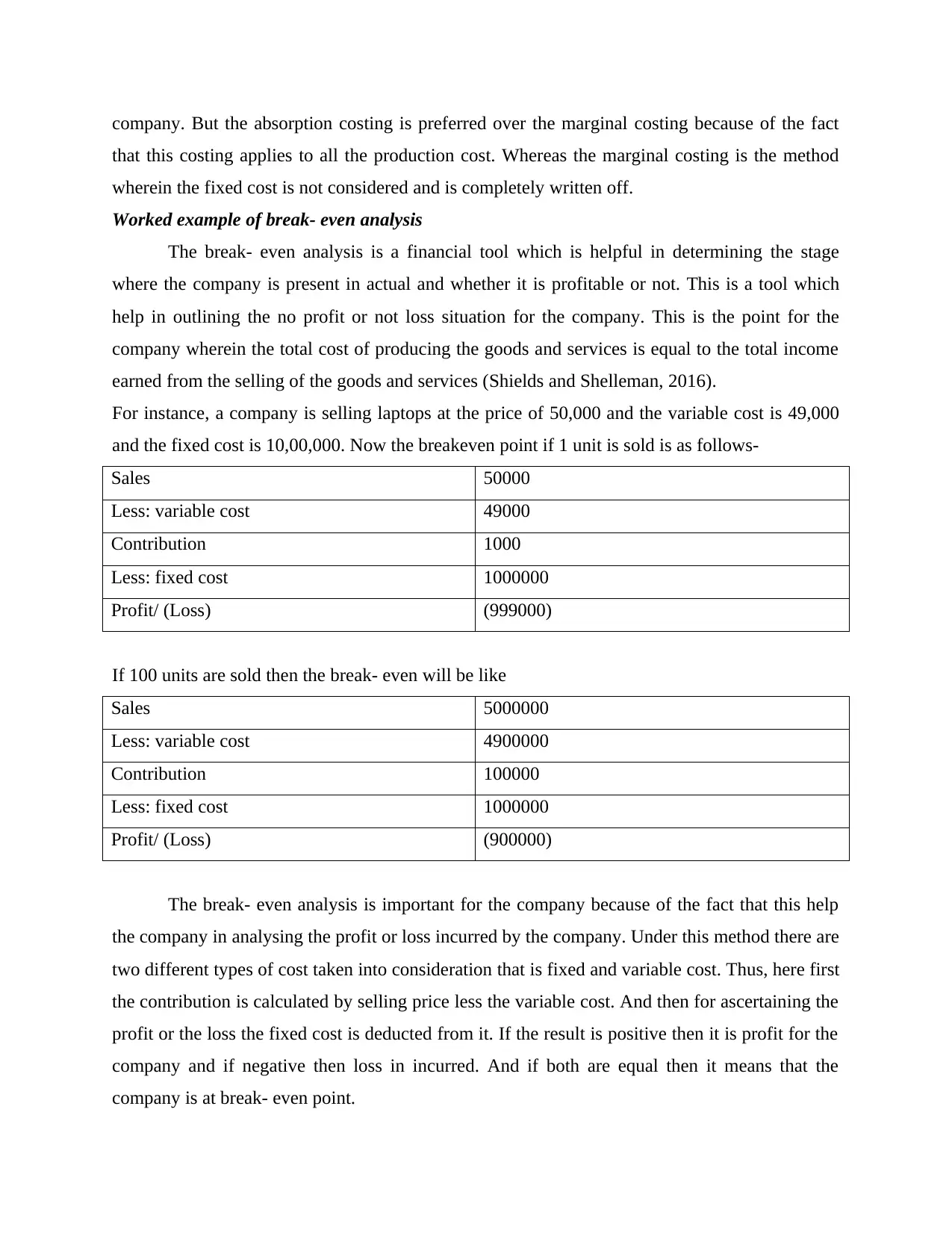

Worked example of break- even analysis

The break- even analysis is a financial tool which is helpful in determining the stage

where the company is present in actual and whether it is profitable or not. This is a tool which

help in outlining the no profit or not loss situation for the company. This is the point for the

company wherein the total cost of producing the goods and services is equal to the total income

earned from the selling of the goods and services (Shields and Shelleman, 2016).

For instance, a company is selling laptops at the price of 50,000 and the variable cost is 49,000

and the fixed cost is 10,00,000. Now the breakeven point if 1 unit is sold is as follows-

Sales 50000

Less: variable cost 49000

Contribution 1000

Less: fixed cost 1000000

Profit/ (Loss) (999000)

If 100 units are sold then the break- even will be like

Sales 5000000

Less: variable cost 4900000

Contribution 100000

Less: fixed cost 1000000

Profit/ (Loss) (900000)

The break- even analysis is important for the company because of the fact that this help

the company in analysing the profit or loss incurred by the company. Under this method there are

two different types of cost taken into consideration that is fixed and variable cost. Thus, here first

the contribution is calculated by selling price less the variable cost. And then for ascertaining the

profit or the loss the fixed cost is deducted from it. If the result is positive then it is profit for the

company and if negative then loss in incurred. And if both are equal then it means that the

company is at break- even point.

that this costing applies to all the production cost. Whereas the marginal costing is the method

wherein the fixed cost is not considered and is completely written off.

Worked example of break- even analysis

The break- even analysis is a financial tool which is helpful in determining the stage

where the company is present in actual and whether it is profitable or not. This is a tool which

help in outlining the no profit or not loss situation for the company. This is the point for the

company wherein the total cost of producing the goods and services is equal to the total income

earned from the selling of the goods and services (Shields and Shelleman, 2016).

For instance, a company is selling laptops at the price of 50,000 and the variable cost is 49,000

and the fixed cost is 10,00,000. Now the breakeven point if 1 unit is sold is as follows-

Sales 50000

Less: variable cost 49000

Contribution 1000

Less: fixed cost 1000000

Profit/ (Loss) (999000)

If 100 units are sold then the break- even will be like

Sales 5000000

Less: variable cost 4900000

Contribution 100000

Less: fixed cost 1000000

Profit/ (Loss) (900000)

The break- even analysis is important for the company because of the fact that this help

the company in analysing the profit or loss incurred by the company. Under this method there are

two different types of cost taken into consideration that is fixed and variable cost. Thus, here first

the contribution is calculated by selling price less the variable cost. And then for ascertaining the

profit or the loss the fixed cost is deducted from it. If the result is positive then it is profit for the

company and if negative then loss in incurred. And if both are equal then it means that the

company is at break- even point.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

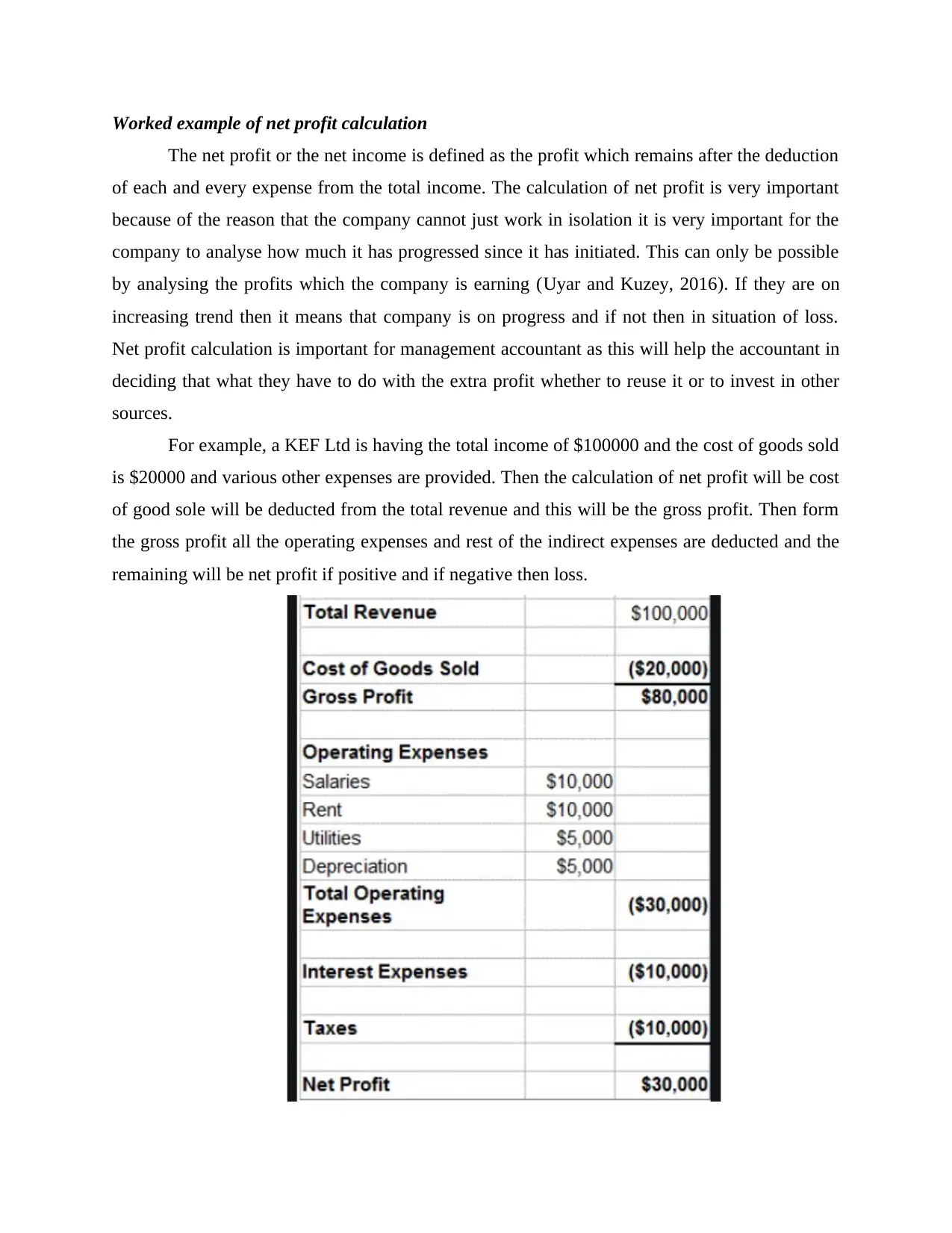

Worked example of net profit calculation

The net profit or the net income is defined as the profit which remains after the deduction

of each and every expense from the total income. The calculation of net profit is very important

because of the reason that the company cannot just work in isolation it is very important for the

company to analyse how much it has progressed since it has initiated. This can only be possible

by analysing the profits which the company is earning (Uyar and Kuzey, 2016). If they are on

increasing trend then it means that company is on progress and if not then in situation of loss.

Net profit calculation is important for management accountant as this will help the accountant in

deciding that what they have to do with the extra profit whether to reuse it or to invest in other

sources.

For example, a KEF Ltd is having the total income of $100000 and the cost of goods sold

is $20000 and various other expenses are provided. Then the calculation of net profit will be cost

of good sole will be deducted from the total revenue and this will be the gross profit. Then form

the gross profit all the operating expenses and rest of the indirect expenses are deducted and the

remaining will be net profit if positive and if negative then loss.

The net profit or the net income is defined as the profit which remains after the deduction

of each and every expense from the total income. The calculation of net profit is very important

because of the reason that the company cannot just work in isolation it is very important for the

company to analyse how much it has progressed since it has initiated. This can only be possible

by analysing the profits which the company is earning (Uyar and Kuzey, 2016). If they are on

increasing trend then it means that company is on progress and if not then in situation of loss.

Net profit calculation is important for management accountant as this will help the accountant in

deciding that what they have to do with the extra profit whether to reuse it or to invest in other

sources.

For example, a KEF Ltd is having the total income of $100000 and the cost of goods sold

is $20000 and various other expenses are provided. Then the calculation of net profit will be cost

of good sole will be deducted from the total revenue and this will be the gross profit. Then form

the gross profit all the operating expenses and rest of the indirect expenses are deducted and the

remaining will be net profit if positive and if negative then loss.

Figure: calculation of net profit

Hence in the end it can be concluded that calculation of net profit is necessary as it

depicts the financial health of the company as it outlines the net income which the company is

earning. Thus, this is very important for the company to calculate the net profit for survival of

company. the calculation of the net profit will help KEF Ltd in knowing the level of profit

which it has earned and this will help them to identify their market position by comparing this

profit with that of the other competitors. Thus, this net profit comparison will help the company

in deciding how to increase the profit so that it can beat the competitors.

CONCLUSION

From the above summary it is concluded that management accounting is very important

for the success of the company. This is pertaining to the fact that this help the company in

effectively take the decision for company. The present report discussed about different

management accounting system like cost accounting, inventory, activity-based costing and many

others. further it discussed about different calculations for the betterment of the company like

marginal costing, absorption costing, break- even analysis and many other for analysing the

profitability of the company.

Hence in the end it can be concluded that calculation of net profit is necessary as it

depicts the financial health of the company as it outlines the net income which the company is

earning. Thus, this is very important for the company to calculate the net profit for survival of

company. the calculation of the net profit will help KEF Ltd in knowing the level of profit

which it has earned and this will help them to identify their market position by comparing this

profit with that of the other competitors. Thus, this net profit comparison will help the company

in deciding how to increase the profit so that it can beat the competitors.

CONCLUSION

From the above summary it is concluded that management accounting is very important

for the success of the company. This is pertaining to the fact that this help the company in

effectively take the decision for company. The present report discussed about different

management accounting system like cost accounting, inventory, activity-based costing and many

others. further it discussed about different calculations for the betterment of the company like

marginal costing, absorption costing, break- even analysis and many other for analysing the

profitability of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.