Marks & Spencer: Management Accounting Systems and Financial Analysis

VerifiedAdded on 2023/01/10

|21

|6465

|2

Report

AI Summary

This report delves into the realm of management accounting, exploring its significance in organizational decision-making, particularly within the context of Marks & Spencer. It examines various management accounting systems, including cost accounting, inventory management, job costing, and price optimization, highlighting their benefits and applications. The report further analyzes different reporting methods like job cost reports, profit and loss statements, inventory reports, and budget reports, critically evaluating their application. It also explores the advantages and disadvantages of planning tools used for budgetary control and compares how organizations adapt management accounting systems to address financial problems. The report provides a comprehensive overview of how management accounting aids in financial planning, performance management, and effective decision-making, ultimately contributing to organizational success.

Unit 5: Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION................................................................................................................................3

Article...................................................................................................................................................3

P1 Background of management accounting.....................................................................................3

P2 Management accounting reporting..............................................................................................7

Critically evaluating MA systems and reporting along with their application.................................8

Income Statement.................................................................................................................................8

P3 Application of different types of cost analysis techniques..........................................................8

Financial Report.................................................................................................................................13

P4 Explain advantages and disadvantage of different types of planning tools used for the

budgetary control............................................................................................................................13

P5 Compare how the organisations are adapting the management accounting systems for

responding to the financial problems.............................................................................................17

CONCLUSION..................................................................................................................................19

REFERENCES...................................................................................................................................20

INTRODUCTION................................................................................................................................3

Article...................................................................................................................................................3

P1 Background of management accounting.....................................................................................3

P2 Management accounting reporting..............................................................................................7

Critically evaluating MA systems and reporting along with their application.................................8

Income Statement.................................................................................................................................8

P3 Application of different types of cost analysis techniques..........................................................8

Financial Report.................................................................................................................................13

P4 Explain advantages and disadvantage of different types of planning tools used for the

budgetary control............................................................................................................................13

P5 Compare how the organisations are adapting the management accounting systems for

responding to the financial problems.............................................................................................17

CONCLUSION..................................................................................................................................19

REFERENCES...................................................................................................................................20

INTRODUCTION

Management accounting refers to accounting process which includes combination of

financial as well as non financial statement for enabling the organisation to make effective

decisions. Managers use MA information for managing the different operations and activities by

having effective control over the costs. It plays important role planning, performance management,

integrated financial records and sound decision making.

Marks & Spencer is multinational retailer having headquarters at London, England which

specialise in selling clothes, food products and home products. It is listed over London Stock

exchange. Company has net revenues of 10181.9 million and net income of 27.4 million. It is

present over 1463 locations. Report includes MA accounting systems and requirement and the

reporting systems used by company. Report will address the different types of costing techniques

for making income statements. It will provide about the different planning tool in budgetary

systems for managing the resources of company. Lastly it will provide about the financial issues

faced by the organisation and how MA systems help in resolving the financial issues.

Article

P1 Background of management accounting

MA means to the representation of business operations & the financial information for

internal management of company (Shields and Shelleman, 2016). It refers to applying professional

and the knowledgeable skills in formulating accounting & the financial data in such a manner that

would help an internal management in framing the policies, planning & controlling the activities of

an enterprise. It aid the management in taking most suitable & the best decisions relating to daily

activities of business concern.

Basis of comparison Management accounting Financial accounting

Aim The MA information is used

by the internal management

for taking business

decisions.

The aim is to provide

information to the external

users which includes

creditors, investors, financial

institutions etc.

Compliance Management accounting is

the internal report, there is

no set standards to be

followed (Hlaciuc and et.al,

Financial report is required

to compile with different

standards before showing

Management accounting refers to accounting process which includes combination of

financial as well as non financial statement for enabling the organisation to make effective

decisions. Managers use MA information for managing the different operations and activities by

having effective control over the costs. It plays important role planning, performance management,

integrated financial records and sound decision making.

Marks & Spencer is multinational retailer having headquarters at London, England which

specialise in selling clothes, food products and home products. It is listed over London Stock

exchange. Company has net revenues of 10181.9 million and net income of 27.4 million. It is

present over 1463 locations. Report includes MA accounting systems and requirement and the

reporting systems used by company. Report will address the different types of costing techniques

for making income statements. It will provide about the different planning tool in budgetary

systems for managing the resources of company. Lastly it will provide about the financial issues

faced by the organisation and how MA systems help in resolving the financial issues.

Article

P1 Background of management accounting

MA means to the representation of business operations & the financial information for

internal management of company (Shields and Shelleman, 2016). It refers to applying professional

and the knowledgeable skills in formulating accounting & the financial data in such a manner that

would help an internal management in framing the policies, planning & controlling the activities of

an enterprise. It aid the management in taking most suitable & the best decisions relating to daily

activities of business concern.

Basis of comparison Management accounting Financial accounting

Aim The MA information is used

by the internal management

for taking business

decisions.

The aim is to provide

information to the external

users which includes

creditors, investors, financial

institutions etc.

Compliance Management accounting is

the internal report, there is

no set standards to be

followed (Hlaciuc and et.al,

Financial report is required

to compile with different

standards before showing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2017). the result.

Independent audit There is no prerequisite yet

the management can take

initiative so as to lead an

independent review.

The independent audit is

mandatory.

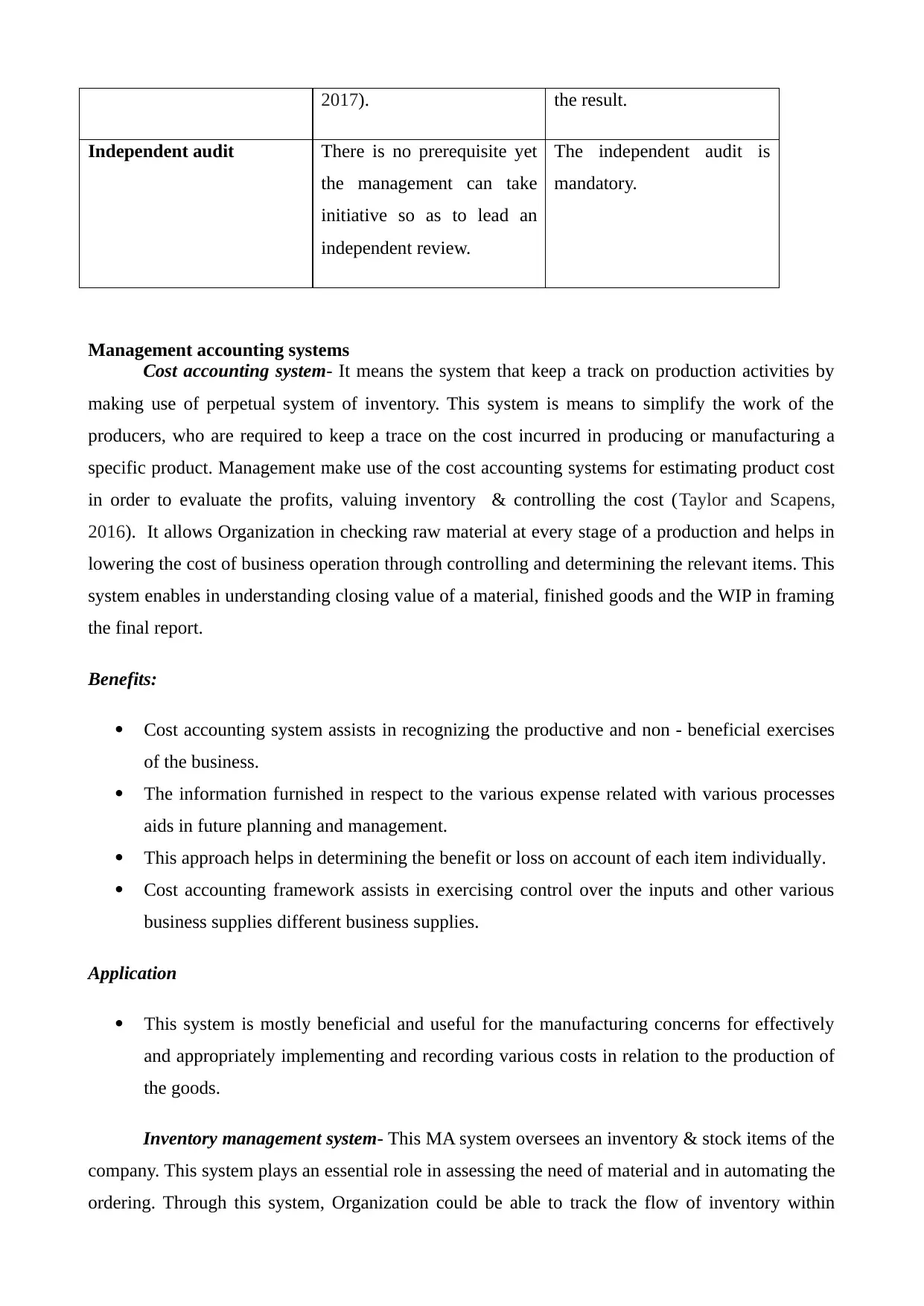

Management accounting systems

Cost accounting system- It means the system that keep a track on production activities by

making use of perpetual system of inventory. This system is means to simplify the work of the

producers, who are required to keep a trace on the cost incurred in producing or manufacturing a

specific product. Management make use of the cost accounting systems for estimating product cost

in order to evaluate the profits, valuing inventory & controlling the cost (Taylor and Scapens,

2016). It allows Organization in checking raw material at every stage of a production and helps in

lowering the cost of business operation through controlling and determining the relevant items. This

system enables in understanding closing value of a material, finished goods and the WIP in framing

the final report.

Benefits:

Cost accounting system assists in recognizing the productive and non - beneficial exercises

of the business.

The information furnished in respect to the various expense related with various processes

aids in future planning and management.

This approach helps in determining the benefit or loss on account of each item individually.

Cost accounting framework assists in exercising control over the inputs and other various

business supplies different business supplies.

Application

This system is mostly beneficial and useful for the manufacturing concerns for effectively

and appropriately implementing and recording various costs in relation to the production of

the goods.

Inventory management system- This MA system oversees an inventory & stock items of the

company. This system plays an essential role in assessing the need of material and in automating the

ordering. Through this system, Organization could be able to track the flow of inventory within

Independent audit There is no prerequisite yet

the management can take

initiative so as to lead an

independent review.

The independent audit is

mandatory.

Management accounting systems

Cost accounting system- It means the system that keep a track on production activities by

making use of perpetual system of inventory. This system is means to simplify the work of the

producers, who are required to keep a trace on the cost incurred in producing or manufacturing a

specific product. Management make use of the cost accounting systems for estimating product cost

in order to evaluate the profits, valuing inventory & controlling the cost (Taylor and Scapens,

2016). It allows Organization in checking raw material at every stage of a production and helps in

lowering the cost of business operation through controlling and determining the relevant items. This

system enables in understanding closing value of a material, finished goods and the WIP in framing

the final report.

Benefits:

Cost accounting system assists in recognizing the productive and non - beneficial exercises

of the business.

The information furnished in respect to the various expense related with various processes

aids in future planning and management.

This approach helps in determining the benefit or loss on account of each item individually.

Cost accounting framework assists in exercising control over the inputs and other various

business supplies different business supplies.

Application

This system is mostly beneficial and useful for the manufacturing concerns for effectively

and appropriately implementing and recording various costs in relation to the production of

the goods.

Inventory management system- This MA system oversees an inventory & stock items of the

company. This system plays an essential role in assessing the need of material and in automating the

ordering. Through this system, Organization could be able to track the flow of inventory within

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

overall supply chain management starting from transit to reaching it with ultimate customers. It

helps in understanding the assets & in maximizing their potential by improving the business

activities and increasing amount of profits.

Benefits:

The major advantage of this system is that it provides assistance to the organization in

effectively managing its inventory very easily which results into cost saving, time, efforts

and money as well. The instability prevailing in the market leads to variation in the

inventory level continuously, therefore, this system assists the organization in avoiding the

chances of risk of human errors as it is fully automated.

It helps in appropriate management of stock and the delivery of the same within the specific

time frame which results into making customers happier and more satisfied.

This system provides assistance in eliminating the unnecessary cost that is occurred because

of the human error and it also assists in additional cost saving, for instance, shortening the

lead time by effectively maintaining a good relation with its suppliers and vendors.

Application

The inventory management system can be utilized by organization for measuring,

monitoring and managing its stock level in a cost-effective manner which results into cost

savings.

Job costing system- It includes the practice of accumulating an information in relation to

cost attached with particular job or production. This information might be required for submitting

information relating to cost to the customer under the contract where the costs have been

reimbursed. It acts as the most useful system for Organization as it helps in identifying accuracy

level of its estimating system that need to quote the prices which allows for the reasonable profit.

This kind of information could also use for assigning an inventory costs in manufacturing the

goods.

Benefits:

The job costing system provides support in assigning cost individually to each and every job

undertaken for producing the product and also helps in determining the profits.

This framework also helps in analysing the performance level of its staff which as a result

helps in understanding the assets & in maximizing their potential by improving the business

activities and increasing amount of profits.

Benefits:

The major advantage of this system is that it provides assistance to the organization in

effectively managing its inventory very easily which results into cost saving, time, efforts

and money as well. The instability prevailing in the market leads to variation in the

inventory level continuously, therefore, this system assists the organization in avoiding the

chances of risk of human errors as it is fully automated.

It helps in appropriate management of stock and the delivery of the same within the specific

time frame which results into making customers happier and more satisfied.

This system provides assistance in eliminating the unnecessary cost that is occurred because

of the human error and it also assists in additional cost saving, for instance, shortening the

lead time by effectively maintaining a good relation with its suppliers and vendors.

Application

The inventory management system can be utilized by organization for measuring,

monitoring and managing its stock level in a cost-effective manner which results into cost

savings.

Job costing system- It includes the practice of accumulating an information in relation to

cost attached with particular job or production. This information might be required for submitting

information relating to cost to the customer under the contract where the costs have been

reimbursed. It acts as the most useful system for Organization as it helps in identifying accuracy

level of its estimating system that need to quote the prices which allows for the reasonable profit.

This kind of information could also use for assigning an inventory costs in manufacturing the

goods.

Benefits:

The job costing system provides support in assigning cost individually to each and every job

undertaken for producing the product and also helps in determining the profits.

This framework also helps in analysing the performance level of its staff which as a result

helps in gathering important information on the basis of which the performance of the

employees can be evaluated on account of efficiency, productivity etc.

It assigns the specific cost to the right account which leads to proper and appropriate

recording of the cost with respect to each job through which a product goes through.

Application

The job costing method will help organization in evaluating its profits on account of

different jobs undertaken by it.

Price optimization system- It refers to the mathematical program that computes the way in

which the demand varies at the different level of price and helps in analysing the optimal pricing at

which the customers might count as affordable. It allows the firm in using the pricing as the

powerful lever that often seen as underdeveloped (ПАНЧЕНКО, 2018). This assist the company in

tailoring the prices for customer sector through stimulating the manner in which the target audience

would respond to the price changes with the data-driven scenarios.

Benefits:

This framework assists the management in focussing on the important goals which are more

relevant for growth and success, for instance, margin of sales, conversion rate etc. This helps

in analysing the benefits which is being attached to it in an effective manner.

It also helps organization in taking fast and informed business decisions by analysing and

evaluating the different consumer buying patterns and the changing trends.

This approach leads to the reduction in the manual work which consequently results into

reduction in the human errors, leading to generating data which results into attaining more

accurate forecasting.

Application

The price optimization process will help the organization in taking informed business

decisions where it can set the price of its products in such a way that it will help in maximising its

profits.

P2 Management accounting reporting

Job cost report

employees can be evaluated on account of efficiency, productivity etc.

It assigns the specific cost to the right account which leads to proper and appropriate

recording of the cost with respect to each job through which a product goes through.

Application

The job costing method will help organization in evaluating its profits on account of

different jobs undertaken by it.

Price optimization system- It refers to the mathematical program that computes the way in

which the demand varies at the different level of price and helps in analysing the optimal pricing at

which the customers might count as affordable. It allows the firm in using the pricing as the

powerful lever that often seen as underdeveloped (ПАНЧЕНКО, 2018). This assist the company in

tailoring the prices for customer sector through stimulating the manner in which the target audience

would respond to the price changes with the data-driven scenarios.

Benefits:

This framework assists the management in focussing on the important goals which are more

relevant for growth and success, for instance, margin of sales, conversion rate etc. This helps

in analysing the benefits which is being attached to it in an effective manner.

It also helps organization in taking fast and informed business decisions by analysing and

evaluating the different consumer buying patterns and the changing trends.

This approach leads to the reduction in the manual work which consequently results into

reduction in the human errors, leading to generating data which results into attaining more

accurate forecasting.

Application

The price optimization process will help the organization in taking informed business

decisions where it can set the price of its products in such a way that it will help in maximising its

profits.

P2 Management accounting reporting

Job cost report

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is used in evaluating the projects against the set standards. This works on evaluating the

total cost incurred in a particular project in respect to the revenue estimated. It is utilized in

evaluating the profitability associated with each job undertaken. This helps the business in

focussing in only these jobs which are profitable. This report assists the management in determining

expenses at the right time so that action scan be taken to control it.

Profit & Loss statement report

It is prepared at the end of the specific period or mainly the accounting year. Which shows

the revenue, cost, expenditures incurred in that period. It is mainly prepared as it is required for the

public company to publish it quarterly (GUŢĂ, 2017). Also, it can be further used in identifying the

trends, comparing the performance with the past years and quarters and in identifying any potential

threats in terms of cash flow of the business.

Inventory and manufacturing report

This MA report provides complete summary of the existing inventory level of the business

entity. This provides knowledge and idea to the management in in respect to the how much

inventory is currently available with the business; which product is being sold at the faster ate along

with the performance in various categories. Business organizations tales into consideration the

information provided in the report for the purpose of making future projections on account of

inventory required. This report also helps in determining any wastage or defect in the stock and

identifies the area requirement progress. This leads to effective utilization of resources.

Account receivable aging report

It is utilized by the management of the organization for the purpose of managing the revenue

of the business where goods are being sold to the customers on credit. It provides complete details

of the customers along with the amount due, due date etc. This helps the organization in identifying

the future losses that may arise because of non-payment of due amount from its customers.

Therefore, timely provision for doubtful debts can be created for the same (Yao and Deng, 2018).

Apart from this, this will provide support to the management in making changes to its credit policy

which will result into effective management of the its debtors and avoid the default in payment.

Budget report

It is a standard document which is states about the forecasted income and expenditure for

specific period. Under this, the actual performance and the standards set by the business

total cost incurred in a particular project in respect to the revenue estimated. It is utilized in

evaluating the profitability associated with each job undertaken. This helps the business in

focussing in only these jobs which are profitable. This report assists the management in determining

expenses at the right time so that action scan be taken to control it.

Profit & Loss statement report

It is prepared at the end of the specific period or mainly the accounting year. Which shows

the revenue, cost, expenditures incurred in that period. It is mainly prepared as it is required for the

public company to publish it quarterly (GUŢĂ, 2017). Also, it can be further used in identifying the

trends, comparing the performance with the past years and quarters and in identifying any potential

threats in terms of cash flow of the business.

Inventory and manufacturing report

This MA report provides complete summary of the existing inventory level of the business

entity. This provides knowledge and idea to the management in in respect to the how much

inventory is currently available with the business; which product is being sold at the faster ate along

with the performance in various categories. Business organizations tales into consideration the

information provided in the report for the purpose of making future projections on account of

inventory required. This report also helps in determining any wastage or defect in the stock and

identifies the area requirement progress. This leads to effective utilization of resources.

Account receivable aging report

It is utilized by the management of the organization for the purpose of managing the revenue

of the business where goods are being sold to the customers on credit. It provides complete details

of the customers along with the amount due, due date etc. This helps the organization in identifying

the future losses that may arise because of non-payment of due amount from its customers.

Therefore, timely provision for doubtful debts can be created for the same (Yao and Deng, 2018).

Apart from this, this will provide support to the management in making changes to its credit policy

which will result into effective management of the its debtors and avoid the default in payment.

Budget report

It is a standard document which is states about the forecasted income and expenditure for

specific period. Under this, the actual performance and the standards set by the business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organization are compared and evaluated in order to determine if there is any deviation. In case,

there is difference, remedial steps are undertaken to mitigate the difference (Rogulenko and et.al,

2016). This report is also useful in determining the whether the expenditure is very high or low so

that initiatives can be taken for exercising control over it. The budget reports vary every year and

also from one organization to another which is because of difference in the goals of the

organization.

Operating budget report

This budget report involves all the revenue and expenditure of the business over a specific

time frame which can eb a quarter or a year. This used by the businesses for formulating financial

plans for carrying out its business operations smoothly. It is prepared in advance of the reporting

period which is considered as a goal to eb achieved by the business. It is prepared separately to

create plans for various functions or areas of business such as sales, production, overhead and

administration expenses.

Critically evaluating MA systems and reporting along with their application

The MA system assists the business entity in running the business operation effectively. The

various types of MA system provide support to the organization for attaining greater profits along

with minimising the cost elements. The integration of MA system and reporting will result into an

integrated system which will assist the organization in effectively evaluating the performance and

productivity resulting into taking improved and better decisions considering the goals and

objectives of the business and the MA reports provides direction to the management for

implementing right strategy. All this together will result into increasing the efficiency level of the

business.

Income Statement

P3 Application of different types of cost analysis techniques

Cost and cost analysis: The cost refers to the amount being spend by the business for producing the

product and cost analysis refers to the process for analysing the cost to output relationship (Datar

and Rajan, 2018). There are different types of cost which are stated below.

Fixed cost: This is the cost which the company is required to pay irrespective of production

is going on or not.

Variable cost: This cost depends upon the level of production.

there is difference, remedial steps are undertaken to mitigate the difference (Rogulenko and et.al,

2016). This report is also useful in determining the whether the expenditure is very high or low so

that initiatives can be taken for exercising control over it. The budget reports vary every year and

also from one organization to another which is because of difference in the goals of the

organization.

Operating budget report

This budget report involves all the revenue and expenditure of the business over a specific

time frame which can eb a quarter or a year. This used by the businesses for formulating financial

plans for carrying out its business operations smoothly. It is prepared in advance of the reporting

period which is considered as a goal to eb achieved by the business. It is prepared separately to

create plans for various functions or areas of business such as sales, production, overhead and

administration expenses.

Critically evaluating MA systems and reporting along with their application

The MA system assists the business entity in running the business operation effectively. The

various types of MA system provide support to the organization for attaining greater profits along

with minimising the cost elements. The integration of MA system and reporting will result into an

integrated system which will assist the organization in effectively evaluating the performance and

productivity resulting into taking improved and better decisions considering the goals and

objectives of the business and the MA reports provides direction to the management for

implementing right strategy. All this together will result into increasing the efficiency level of the

business.

Income Statement

P3 Application of different types of cost analysis techniques

Cost and cost analysis: The cost refers to the amount being spend by the business for producing the

product and cost analysis refers to the process for analysing the cost to output relationship (Datar

and Rajan, 2018). There are different types of cost which are stated below.

Fixed cost: This is the cost which the company is required to pay irrespective of production

is going on or not.

Variable cost: This cost depends upon the level of production.

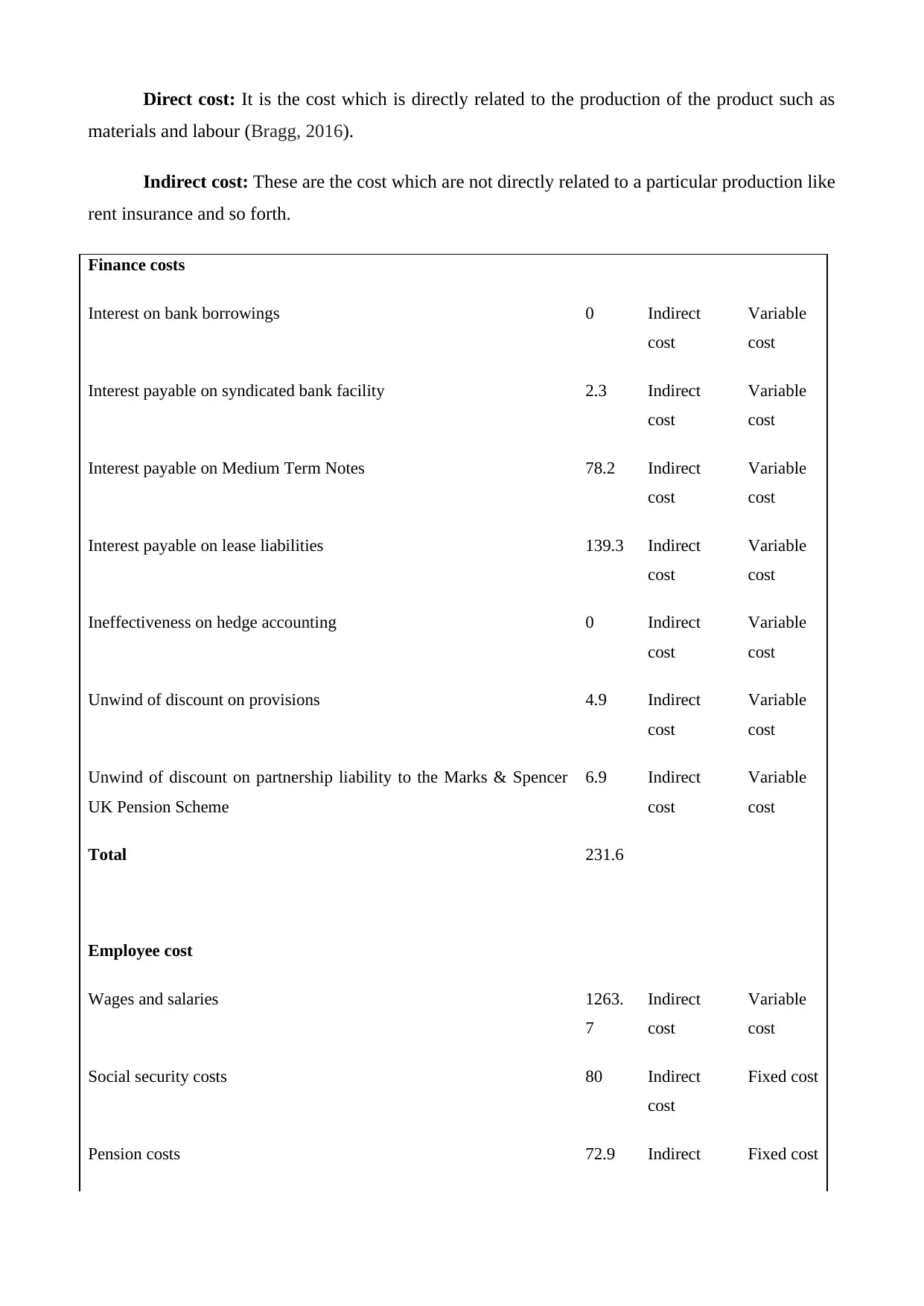

Direct cost: It is the cost which is directly related to the production of the product such as

materials and labour (Bragg, 2016).

Indirect cost: These are the cost which are not directly related to a particular production like

rent insurance and so forth.

Finance costs

Interest on bank borrowings 0 Indirect

cost

Variable

cost

Interest payable on syndicated bank facility 2.3 Indirect

cost

Variable

cost

Interest payable on Medium Term Notes 78.2 Indirect

cost

Variable

cost

Interest payable on lease liabilities 139.3 Indirect

cost

Variable

cost

Ineffectiveness on hedge accounting 0 Indirect

cost

Variable

cost

Unwind of discount on provisions 4.9 Indirect

cost

Variable

cost

Unwind of discount on partnership liability to the Marks & Spencer

UK Pension Scheme

6.9 Indirect

cost

Variable

cost

Total 231.6

Employee cost

Wages and salaries 1263.

7

Indirect

cost

Variable

cost

Social security costs 80 Indirect

cost

Fixed cost

Pension costs 72.9 Indirect Fixed cost

materials and labour (Bragg, 2016).

Indirect cost: These are the cost which are not directly related to a particular production like

rent insurance and so forth.

Finance costs

Interest on bank borrowings 0 Indirect

cost

Variable

cost

Interest payable on syndicated bank facility 2.3 Indirect

cost

Variable

cost

Interest payable on Medium Term Notes 78.2 Indirect

cost

Variable

cost

Interest payable on lease liabilities 139.3 Indirect

cost

Variable

cost

Ineffectiveness on hedge accounting 0 Indirect

cost

Variable

cost

Unwind of discount on provisions 4.9 Indirect

cost

Variable

cost

Unwind of discount on partnership liability to the Marks & Spencer

UK Pension Scheme

6.9 Indirect

cost

Variable

cost

Total 231.6

Employee cost

Wages and salaries 1263.

7

Indirect

cost

Variable

cost

Social security costs 80 Indirect

cost

Fixed cost

Pension costs 72.9 Indirect Fixed cost

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

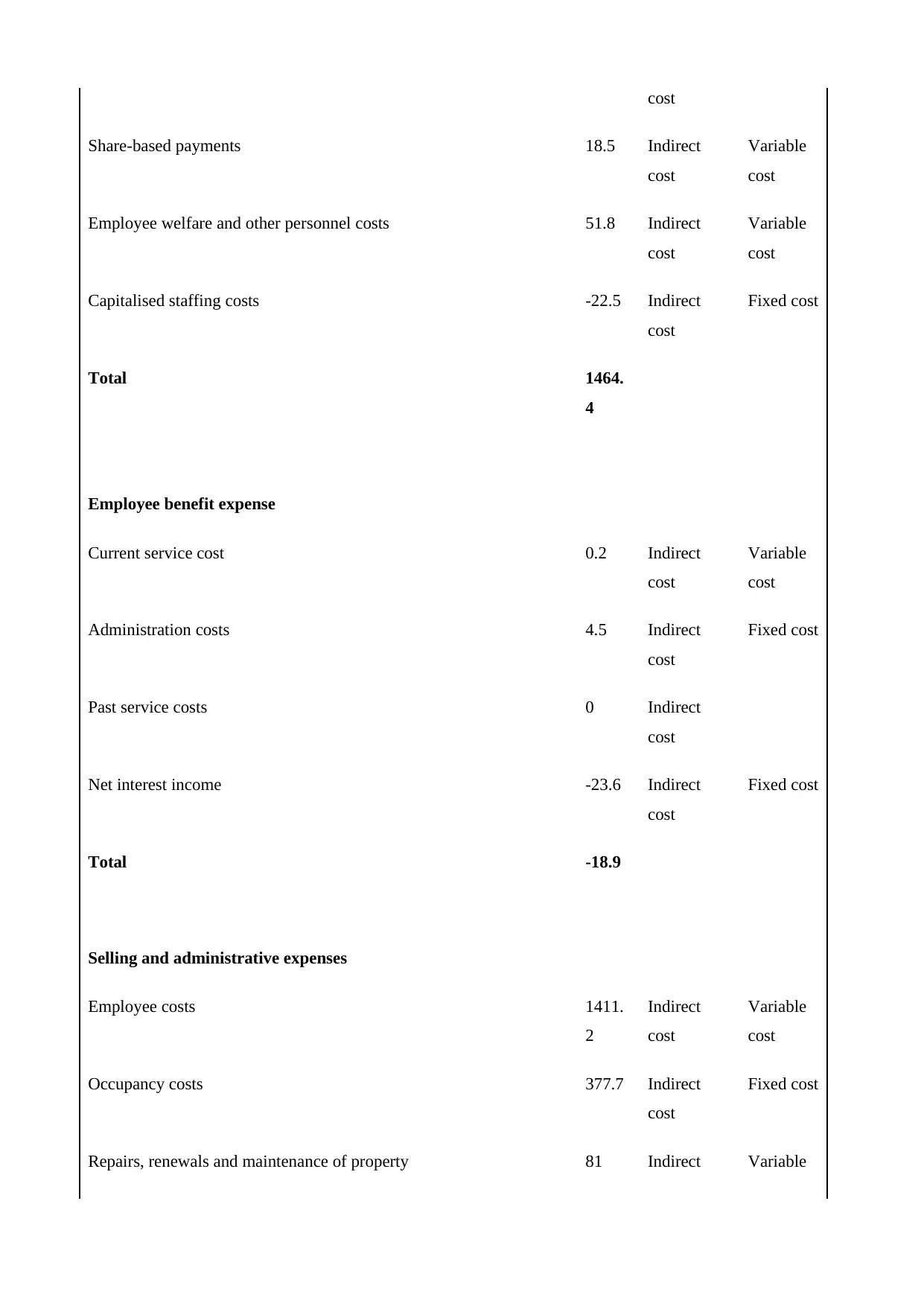

cost

Share-based payments 18.5 Indirect

cost

Variable

cost

Employee welfare and other personnel costs 51.8 Indirect

cost

Variable

cost

Capitalised staffing costs -22.5 Indirect

cost

Fixed cost

Total 1464.

4

Employee benefit expense

Current service cost 0.2 Indirect

cost

Variable

cost

Administration costs 4.5 Indirect

cost

Fixed cost

Past service costs 0 Indirect

cost

Net interest income -23.6 Indirect

cost

Fixed cost

Total -18.9

Selling and administrative expenses

Employee costs 1411.

2

Indirect

cost

Variable

cost

Occupancy costs 377.7 Indirect

cost

Fixed cost

Repairs, renewals and maintenance of property 81 Indirect Variable

Share-based payments 18.5 Indirect

cost

Variable

cost

Employee welfare and other personnel costs 51.8 Indirect

cost

Variable

cost

Capitalised staffing costs -22.5 Indirect

cost

Fixed cost

Total 1464.

4

Employee benefit expense

Current service cost 0.2 Indirect

cost

Variable

cost

Administration costs 4.5 Indirect

cost

Fixed cost

Past service costs 0 Indirect

cost

Net interest income -23.6 Indirect

cost

Fixed cost

Total -18.9

Selling and administrative expenses

Employee costs 1411.

2

Indirect

cost

Variable

cost

Occupancy costs 377.7 Indirect

cost

Fixed cost

Repairs, renewals and maintenance of property 81 Indirect Variable

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

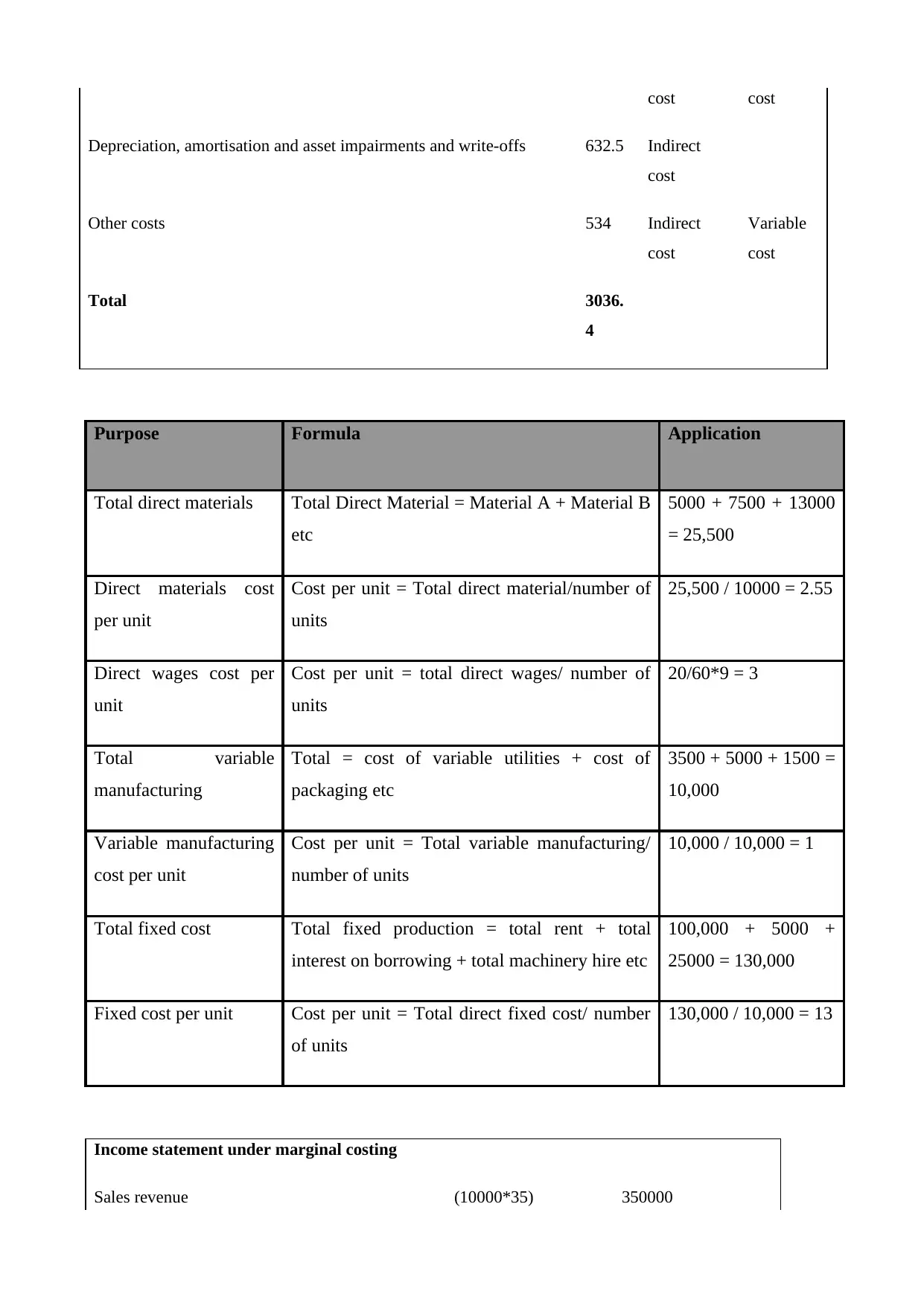

cost cost

Depreciation, amortisation and asset impairments and write-offs 632.5 Indirect

cost

Other costs 534 Indirect

cost

Variable

cost

Total 3036.

4

Purpose Formula Application

Total direct materials Total Direct Material = Material A + Material B

etc

5000 + 7500 + 13000

= 25,500

Direct materials cost

per unit

Cost per unit = Total direct material/number of

units

25,500 / 10000 = 2.55

Direct wages cost per

unit

Cost per unit = total direct wages/ number of

units

20/60*9 = 3

Total variable

manufacturing

Total = cost of variable utilities + cost of

packaging etc

3500 + 5000 + 1500 =

10,000

Variable manufacturing

cost per unit

Cost per unit = Total variable manufacturing/

number of units

10,000 / 10,000 = 1

Total fixed cost Total fixed production = total rent + total

interest on borrowing + total machinery hire etc

100,000 + 5000 +

25000 = 130,000

Fixed cost per unit Cost per unit = Total direct fixed cost/ number

of units

130,000 / 10,000 = 13

Income statement under marginal costing

Sales revenue (10000*35) 350000

Depreciation, amortisation and asset impairments and write-offs 632.5 Indirect

cost

Other costs 534 Indirect

cost

Variable

cost

Total 3036.

4

Purpose Formula Application

Total direct materials Total Direct Material = Material A + Material B

etc

5000 + 7500 + 13000

= 25,500

Direct materials cost

per unit

Cost per unit = Total direct material/number of

units

25,500 / 10000 = 2.55

Direct wages cost per

unit

Cost per unit = total direct wages/ number of

units

20/60*9 = 3

Total variable

manufacturing

Total = cost of variable utilities + cost of

packaging etc

3500 + 5000 + 1500 =

10,000

Variable manufacturing

cost per unit

Cost per unit = Total variable manufacturing/

number of units

10,000 / 10,000 = 1

Total fixed cost Total fixed production = total rent + total

interest on borrowing + total machinery hire etc

100,000 + 5000 +

25000 = 130,000

Fixed cost per unit Cost per unit = Total direct fixed cost/ number

of units

130,000 / 10,000 = 13

Income statement under marginal costing

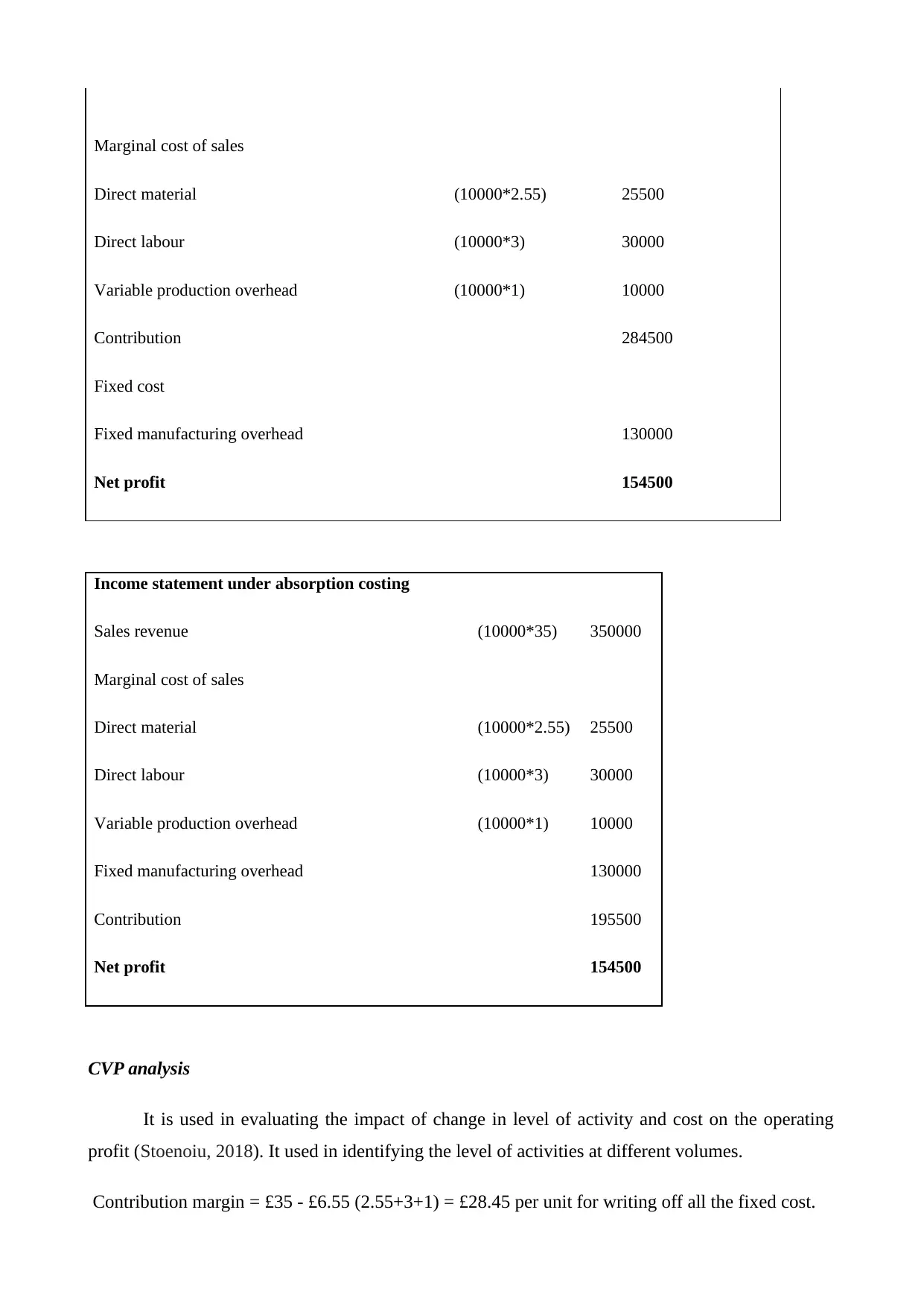

Sales revenue (10000*35) 350000

Marginal cost of sales

Direct material (10000*2.55) 25500

Direct labour (10000*3) 30000

Variable production overhead (10000*1) 10000

Contribution 284500

Fixed cost

Fixed manufacturing overhead 130000

Net profit 154500

Income statement under absorption costing

Sales revenue (10000*35) 350000

Marginal cost of sales

Direct material (10000*2.55) 25500

Direct labour (10000*3) 30000

Variable production overhead (10000*1) 10000

Fixed manufacturing overhead 130000

Contribution 195500

Net profit 154500

CVP analysis

It is used in evaluating the impact of change in level of activity and cost on the operating

profit (Stoenoiu, 2018). It used in identifying the level of activities at different volumes.

Contribution margin = £35 - £6.55 (2.55+3+1) = £28.45 per unit for writing off all the fixed cost.

Direct material (10000*2.55) 25500

Direct labour (10000*3) 30000

Variable production overhead (10000*1) 10000

Contribution 284500

Fixed cost

Fixed manufacturing overhead 130000

Net profit 154500

Income statement under absorption costing

Sales revenue (10000*35) 350000

Marginal cost of sales

Direct material (10000*2.55) 25500

Direct labour (10000*3) 30000

Variable production overhead (10000*1) 10000

Fixed manufacturing overhead 130000

Contribution 195500

Net profit 154500

CVP analysis

It is used in evaluating the impact of change in level of activity and cost on the operating

profit (Stoenoiu, 2018). It used in identifying the level of activities at different volumes.

Contribution margin = £35 - £6.55 (2.55+3+1) = £28.45 per unit for writing off all the fixed cost.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.